Evaluating L Brand Inc.'s WACC and Dividend Policy Strategies

VerifiedAdded on 2023/06/03

|18

|3251

|221

Report

AI Summary

This report provides a financial analysis of L Brand Inc., focusing on its weighted average cost of capital (WACC) and dividend policy. It calculates the cost of equity using both historical and implied equity premiums, determines the cost of debt, and then computes the WACC. The analysis also evaluates the company's dividend policy over the last five years, examining cash returned to shareholders through dividends and buybacks, comparing these figures to Free Cash Flow to Equity (FCFE). The report assesses the firm's performance using ROE and cost of equity benchmarks, discusses recent financial changes including share repurchases, and provides a recommendation to reduce the dividend payout ratio to improve retained earnings and overall financial performance. The FCFE analysis suggests the stock is undervalued. The report concludes that a reduced dividend payout could enhance the company's capital market position.

1

Weighted Average cost of capital of L Brand

Weighted Average cost of capital of L Brand

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

2.1: Cost of Equity...................................................................................................................................3

2.1.1: Risk free rate of return..................................................................................................................3

2.1.2: Market equity premium................................................................................................................3

2.1.3: Stock Beta......................................................................................................................................5

2.2: Cost of Debt......................................................................................................................................5

2.3 Weighted Average Cost of Capital (WACC)........................................................................................6

Section 3......................................................................................................................................................8

Introduction.................................................................................................................................................9

Current dividend policy...............................................................................................................................9

Recent financial changes.............................................................................................................................9

FCFE analysis.............................................................................................................................................10

Performance of the firm............................................................................................................................10

Recommendation and conclusion.............................................................................................................11

Appendix...................................................................................................................................................13

Contents

2.1: Cost of Equity...................................................................................................................................3

2.1.1: Risk free rate of return..................................................................................................................3

2.1.2: Market equity premium................................................................................................................3

2.1.3: Stock Beta......................................................................................................................................5

2.2: Cost of Debt......................................................................................................................................5

2.3 Weighted Average Cost of Capital (WACC)........................................................................................6

Section 3......................................................................................................................................................8

Introduction.................................................................................................................................................9

Current dividend policy...............................................................................................................................9

Recent financial changes.............................................................................................................................9

FCFE analysis.............................................................................................................................................10

Performance of the firm............................................................................................................................10

Recommendation and conclusion.............................................................................................................11

Appendix...................................................................................................................................................13

3

2.1: Cost of Equity

2.1.1: Risk free rate of return

In order to select the risk free rate of return, it has been decided to choose 10 years US

Treasury bond rate as the risk free rate return. The 10 years US T-Bond rate has been chosen

from website of US treasury department (Link: https://www.treasury.gov/resource-center/data-

chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=2018 ) and it has taken

on January, 2 , 2018. The 10 years US T-Bond rate was 2.46 % (U.S. Department of the

Treasury) and it is taken as the proxy for risk free rate of return.

2.1.2: Market equity premium

In this part there is need to calculate two measures of market equity premium:

(A) Historical Premium: It is calculated as average of market premium for last ten years

The market index chosen for the purpose this assignment is S&P 500 and to calculate the

average historical market premium, historical price of last 10 years has been taken from January,

01, 2008 to December, 31, 2017. Data can be found in excel sheet and calculation of historical

market premium has been shown here. Historical data of S&P 500 has been taken from Yahoo

Finance (Source: Yahoo Finance: S&P 500, 2018).

Market index price has been given in appendix:

In order to calculate the historical market premium there is need to make three important

decisions and they have taken as below:

Estimation period: 10 years estimation are preferred (January, 01, 2008 to December,

31, 2017)

Choice of risk free rate of return: In order to choose risk free rate of return, 10 years

US T-Bond rate has been chosen and it has been taken from the link

(https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/

TextView.aspx?data=yieldYear&year=2017). As there is need to calculate risk free rate

of return for last 10 years, it has been decided to use T-Bond rate of December, 31 of

every year and it can be found in excel sheet and also in calculation shown below (U.S.

Department of the Treasury).

Arithmetic or Geometric Averages: As the period use for estimating the T-Bond rate

was larger than 1 year it is decided to use geometric mean to estimate the historical

market premium.

(Note: Source of Market Return is yahoo finance and that of risk free rate of return is US

Treasury Department)

2.1: Cost of Equity

2.1.1: Risk free rate of return

In order to select the risk free rate of return, it has been decided to choose 10 years US

Treasury bond rate as the risk free rate return. The 10 years US T-Bond rate has been chosen

from website of US treasury department (Link: https://www.treasury.gov/resource-center/data-

chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=2018 ) and it has taken

on January, 2 , 2018. The 10 years US T-Bond rate was 2.46 % (U.S. Department of the

Treasury) and it is taken as the proxy for risk free rate of return.

2.1.2: Market equity premium

In this part there is need to calculate two measures of market equity premium:

(A) Historical Premium: It is calculated as average of market premium for last ten years

The market index chosen for the purpose this assignment is S&P 500 and to calculate the

average historical market premium, historical price of last 10 years has been taken from January,

01, 2008 to December, 31, 2017. Data can be found in excel sheet and calculation of historical

market premium has been shown here. Historical data of S&P 500 has been taken from Yahoo

Finance (Source: Yahoo Finance: S&P 500, 2018).

Market index price has been given in appendix:

In order to calculate the historical market premium there is need to make three important

decisions and they have taken as below:

Estimation period: 10 years estimation are preferred (January, 01, 2008 to December,

31, 2017)

Choice of risk free rate of return: In order to choose risk free rate of return, 10 years

US T-Bond rate has been chosen and it has been taken from the link

(https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/

TextView.aspx?data=yieldYear&year=2017). As there is need to calculate risk free rate

of return for last 10 years, it has been decided to use T-Bond rate of December, 31 of

every year and it can be found in excel sheet and also in calculation shown below (U.S.

Department of the Treasury).

Arithmetic or Geometric Averages: As the period use for estimating the T-Bond rate

was larger than 1 year it is decided to use geometric mean to estimate the historical

market premium.

(Note: Source of Market Return is yahoo finance and that of risk free rate of return is US

Treasury Department)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

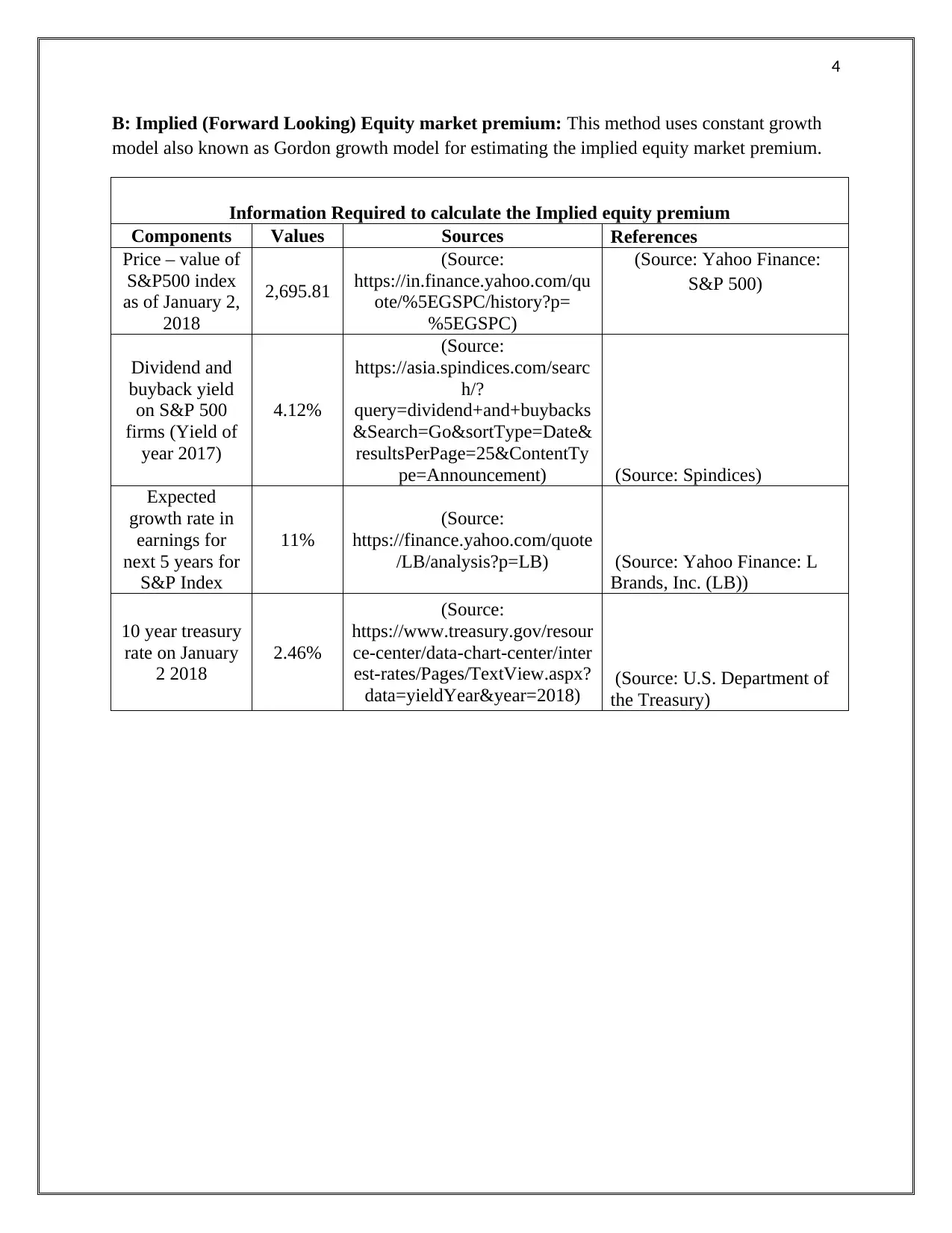

B: Implied (Forward Looking) Equity market premium: This method uses constant growth

model also known as Gordon growth model for estimating the implied equity market premium.

Information Required to calculate the Implied equity premium

Components Values Sources References

Price – value of

S&P500 index

as of January 2,

2018

2,695.81

(Source:

https://in.finance.yahoo.com/qu

ote/%5EGSPC/history?p=

%5EGSPC)

(Source: Yahoo Finance:

S&P 500)

Dividend and

buyback yield

on S&P 500

firms (Yield of

year 2017)

4.12%

(Source:

https://asia.spindices.com/searc

h/?

query=dividend+and+buybacks

&Search=Go&sortType=Date&

resultsPerPage=25&ContentTy

pe=Announcement) (Source: Spindices)

Expected

growth rate in

earnings for

next 5 years for

S&P Index

11%

(Source:

https://finance.yahoo.com/quote

/LB/analysis?p=LB) (Source: Yahoo Finance: L

Brands, Inc. (LB))

10 year treasury

rate on January

2 2018

2.46%

(Source:

https://www.treasury.gov/resour

ce-center/data-chart-center/inter

est-rates/Pages/TextView.aspx?

data=yieldYear&year=2018) (Source: U.S. Department of

the Treasury)

B: Implied (Forward Looking) Equity market premium: This method uses constant growth

model also known as Gordon growth model for estimating the implied equity market premium.

Information Required to calculate the Implied equity premium

Components Values Sources References

Price – value of

S&P500 index

as of January 2,

2018

2,695.81

(Source:

https://in.finance.yahoo.com/qu

ote/%5EGSPC/history?p=

%5EGSPC)

(Source: Yahoo Finance:

S&P 500)

Dividend and

buyback yield

on S&P 500

firms (Yield of

year 2017)

4.12%

(Source:

https://asia.spindices.com/searc

h/?

query=dividend+and+buybacks

&Search=Go&sortType=Date&

resultsPerPage=25&ContentTy

pe=Announcement) (Source: Spindices)

Expected

growth rate in

earnings for

next 5 years for

S&P Index

11%

(Source:

https://finance.yahoo.com/quote

/LB/analysis?p=LB) (Source: Yahoo Finance: L

Brands, Inc. (LB))

10 year treasury

rate on January

2 2018

2.46%

(Source:

https://www.treasury.gov/resour

ce-center/data-chart-center/inter

est-rates/Pages/TextView.aspx?

data=yieldYear&year=2018) (Source: U.S. Department of

the Treasury)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

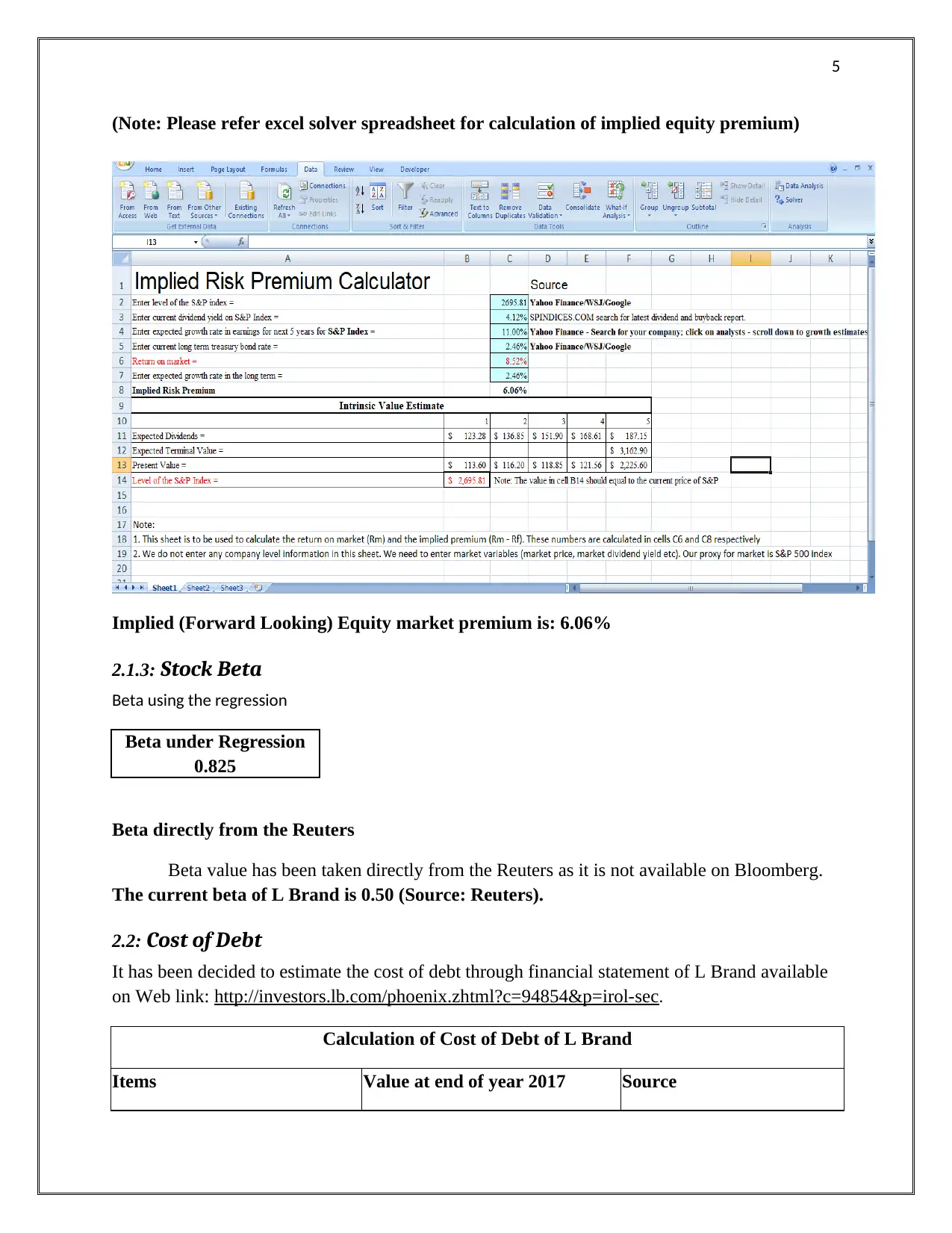

(Note: Please refer excel solver spreadsheet for calculation of implied equity premium)

Implied (Forward Looking) Equity market premium is: 6.06%

2.1.3: Stock Beta

Beta using the regression

Beta under Regression

0.825

Beta directly from the Reuters

Beta value has been taken directly from the Reuters as it is not available on Bloomberg.

The current beta of L Brand is 0.50 (Source: Reuters).

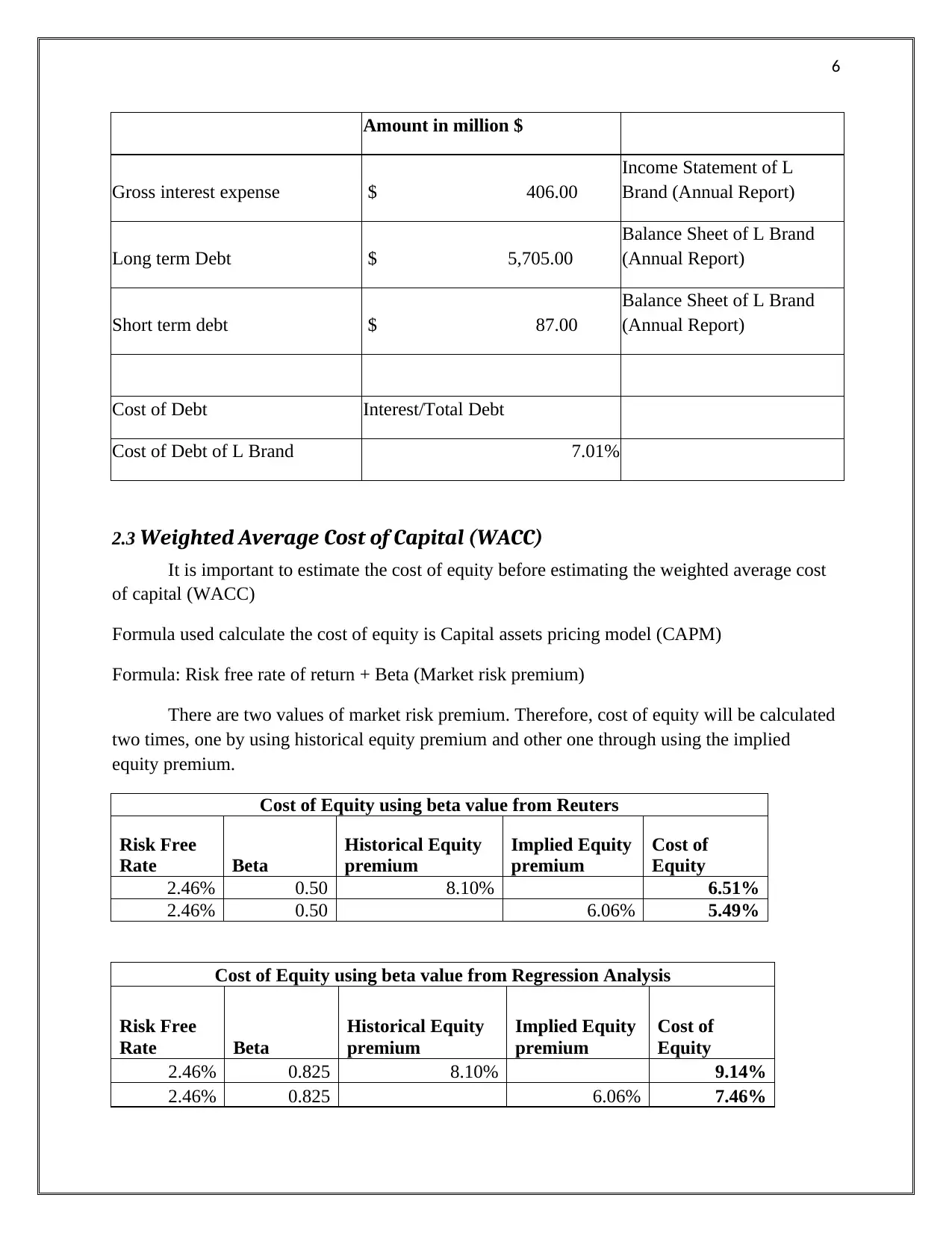

2.2: Cost of Debt

It has been decided to estimate the cost of debt through financial statement of L Brand available

on Web link: http://investors.lb.com/phoenix.zhtml?c=94854&p=irol-sec.

Calculation of Cost of Debt of L Brand

Items Value at end of year 2017 Source

(Note: Please refer excel solver spreadsheet for calculation of implied equity premium)

Implied (Forward Looking) Equity market premium is: 6.06%

2.1.3: Stock Beta

Beta using the regression

Beta under Regression

0.825

Beta directly from the Reuters

Beta value has been taken directly from the Reuters as it is not available on Bloomberg.

The current beta of L Brand is 0.50 (Source: Reuters).

2.2: Cost of Debt

It has been decided to estimate the cost of debt through financial statement of L Brand available

on Web link: http://investors.lb.com/phoenix.zhtml?c=94854&p=irol-sec.

Calculation of Cost of Debt of L Brand

Items Value at end of year 2017 Source

6

Amount in million $

Gross interest expense $ 406.00

Income Statement of L

Brand (Annual Report)

Long term Debt $ 5,705.00

Balance Sheet of L Brand

(Annual Report)

Short term debt $ 87.00

Balance Sheet of L Brand

(Annual Report)

Cost of Debt Interest/Total Debt

Cost of Debt of L Brand 7.01%

2.3 Weighted Average Cost of Capital (WACC)

It is important to estimate the cost of equity before estimating the weighted average cost

of capital (WACC)

Formula used calculate the cost of equity is Capital assets pricing model (CAPM)

Formula: Risk free rate of return + Beta (Market risk premium)

There are two values of market risk premium. Therefore, cost of equity will be calculated

two times, one by using historical equity premium and other one through using the implied

equity premium.

Cost of Equity using beta value from Reuters

Risk Free

Rate Beta

Historical Equity

premium

Implied Equity

premium

Cost of

Equity

2.46% 0.50 8.10% 6.51%

2.46% 0.50 6.06% 5.49%

Cost of Equity using beta value from Regression Analysis

Risk Free

Rate Beta

Historical Equity

premium

Implied Equity

premium

Cost of

Equity

2.46% 0.825 8.10% 9.14%

2.46% 0.825 6.06% 7.46%

Amount in million $

Gross interest expense $ 406.00

Income Statement of L

Brand (Annual Report)

Long term Debt $ 5,705.00

Balance Sheet of L Brand

(Annual Report)

Short term debt $ 87.00

Balance Sheet of L Brand

(Annual Report)

Cost of Debt Interest/Total Debt

Cost of Debt of L Brand 7.01%

2.3 Weighted Average Cost of Capital (WACC)

It is important to estimate the cost of equity before estimating the weighted average cost

of capital (WACC)

Formula used calculate the cost of equity is Capital assets pricing model (CAPM)

Formula: Risk free rate of return + Beta (Market risk premium)

There are two values of market risk premium. Therefore, cost of equity will be calculated

two times, one by using historical equity premium and other one through using the implied

equity premium.

Cost of Equity using beta value from Reuters

Risk Free

Rate Beta

Historical Equity

premium

Implied Equity

premium

Cost of

Equity

2.46% 0.50 8.10% 6.51%

2.46% 0.50 6.06% 5.49%

Cost of Equity using beta value from Regression Analysis

Risk Free

Rate Beta

Historical Equity

premium

Implied Equity

premium

Cost of

Equity

2.46% 0.825 8.10% 9.14%

2.46% 0.825 6.06% 7.46%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

As all the values for calculating the cost of equity and cost of debt has been on January 2,

2018, therefore, it has been decided to take value of debt and value of equity as on starting of

January, 2018. Financial data in latest annual report of L Brand has been considered as it shows

data as on February 3, 2018. For estimating the value of debt it has been decided to use book

value of long term debt and short term debt. To estimate the value of equity market price of as on

January 2, 2018 has been multiplied by number of shares issued by L Brand.

As all the values for calculating the cost of equity and cost of debt has been on January 2,

2018, therefore, it has been decided to take value of debt and value of equity as on starting of

January, 2018. Financial data in latest annual report of L Brand has been considered as it shows

data as on February 3, 2018. For estimating the value of debt it has been decided to use book

value of long term debt and short term debt. To estimate the value of equity market price of as on

January 2, 2018 has been multiplied by number of shares issued by L Brand.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

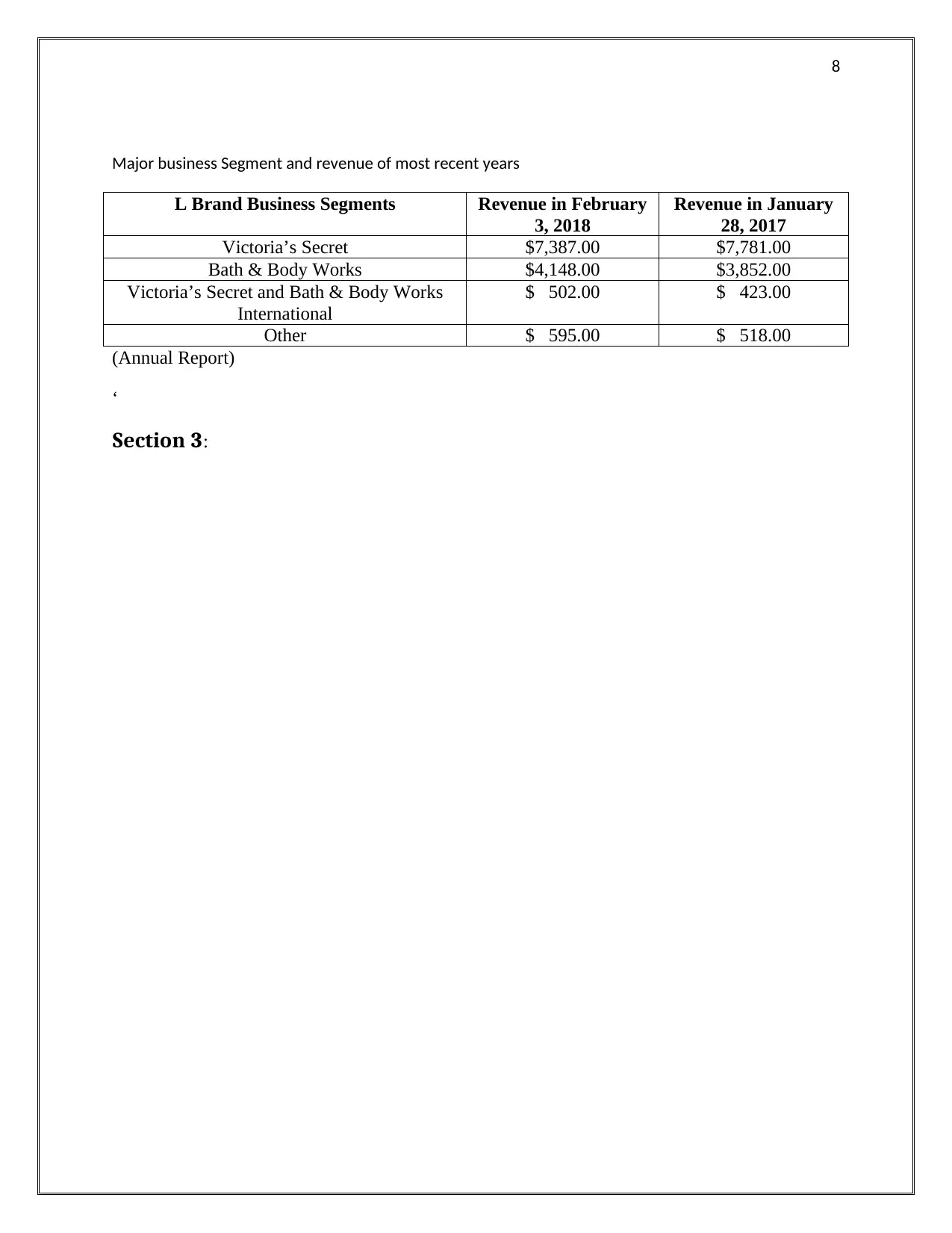

Major business Segment and revenue of most recent years

L Brand Business Segments Revenue in February

3, 2018

Revenue in January

28, 2017

Victoria’s Secret $7,387.00 $7,781.00

Bath & Body Works $4,148.00 $3,852.00

Victoria’s Secret and Bath & Body Works

International

$ 502.00 $ 423.00

Other $ 595.00 $ 518.00

(Annual Report)

‘

Section 3:

Major business Segment and revenue of most recent years

L Brand Business Segments Revenue in February

3, 2018

Revenue in January

28, 2017

Victoria’s Secret $7,387.00 $7,781.00

Bath & Body Works $4,148.00 $3,852.00

Victoria’s Secret and Bath & Body Works

International

$ 502.00 $ 423.00

Other $ 595.00 $ 518.00

(Annual Report)

‘

Section 3:

9

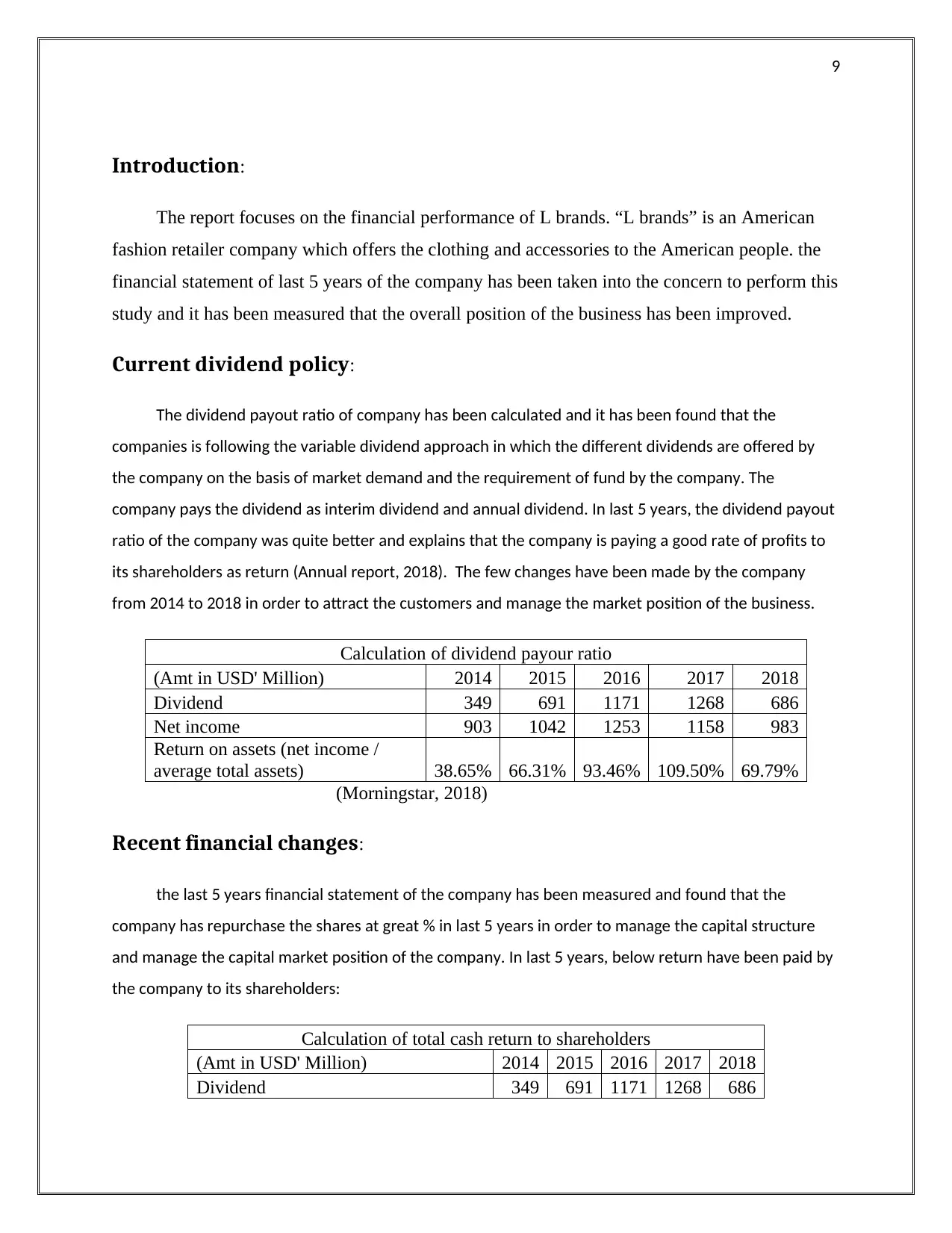

Introduction:

The report focuses on the financial performance of L brands. “L brands” is an American

fashion retailer company which offers the clothing and accessories to the American people. the

financial statement of last 5 years of the company has been taken into the concern to perform this

study and it has been measured that the overall position of the business has been improved.

Current dividend policy:

The dividend payout ratio of company has been calculated and it has been found that the

companies is following the variable dividend approach in which the different dividends are offered by

the company on the basis of market demand and the requirement of fund by the company. The

company pays the dividend as interim dividend and annual dividend. In last 5 years, the dividend payout

ratio of the company was quite better and explains that the company is paying a good rate of profits to

its shareholders as return (Annual report, 2018). The few changes have been made by the company

from 2014 to 2018 in order to attract the customers and manage the market position of the business.

Calculation of dividend payour ratio

(Amt in USD' Million) 2014 2015 2016 2017 2018

Dividend 349 691 1171 1268 686

Net income 903 1042 1253 1158 983

Return on assets (net income /

average total assets) 38.65% 66.31% 93.46% 109.50% 69.79%

(Morningstar, 2018)

Recent financial changes:

the last 5 years financial statement of the company has been measured and found that the

company has repurchase the shares at great % in last 5 years in order to manage the capital structure

and manage the capital market position of the company. In last 5 years, below return have been paid by

the company to its shareholders:

Calculation of total cash return to shareholders

(Amt in USD' Million) 2014 2015 2016 2017 2018

Dividend 349 691 1171 1268 686

Introduction:

The report focuses on the financial performance of L brands. “L brands” is an American

fashion retailer company which offers the clothing and accessories to the American people. the

financial statement of last 5 years of the company has been taken into the concern to perform this

study and it has been measured that the overall position of the business has been improved.

Current dividend policy:

The dividend payout ratio of company has been calculated and it has been found that the

companies is following the variable dividend approach in which the different dividends are offered by

the company on the basis of market demand and the requirement of fund by the company. The

company pays the dividend as interim dividend and annual dividend. In last 5 years, the dividend payout

ratio of the company was quite better and explains that the company is paying a good rate of profits to

its shareholders as return (Annual report, 2018). The few changes have been made by the company

from 2014 to 2018 in order to attract the customers and manage the market position of the business.

Calculation of dividend payour ratio

(Amt in USD' Million) 2014 2015 2016 2017 2018

Dividend 349 691 1171 1268 686

Net income 903 1042 1253 1158 983

Return on assets (net income /

average total assets) 38.65% 66.31% 93.46% 109.50% 69.79%

(Morningstar, 2018)

Recent financial changes:

the last 5 years financial statement of the company has been measured and found that the

company has repurchase the shares at great % in last 5 years in order to manage the capital structure

and manage the capital market position of the company. In last 5 years, below return have been paid by

the company to its shareholders:

Calculation of total cash return to shareholders

(Amt in USD' Million) 2014 2015 2016 2017 2018

Dividend 349 691 1171 1268 686

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Buy back 60 87 483 435 446

Total cash return to shareholders 409 778 1654 1703 1132

(Annual report, 2018)

It explains that recent financial changes are in the favour of the company and explains that

the financial position of the company is quite attractive for the investor’s point of view. These

have even helped the business to improve the stock price of the business.

FCFE analysis:

FCFE analysis represents that how much cash is available in the company for the

shareholders and it represents about the intrinsic share price of the company. On the basis of the

FCFE analysis, it has been found that the intrinsic price of the company is USD 41.52 whereas

the market price is USD 33.85 which explains that the stock price of the company is undervalued

and company is not required to pay this much of dividend (Reuters, 2018). Even the lower

dividend could help the business to maintain the capital market position.

The lower dividend is quite enough because if the shareholders want they could generate

the revenue through selling the stock of the company in the market and it would help them to

generate great revenue. The FCFE analysis represent about better investment opportunities in the

company.

Performance of the firm:

The financial performance of the company in last 5 years has been changed a lot and it has

impacted on the investment opportunities a capital market position of the company. Such as, in case of

comparison among the ROE and cost of equity, it has been found that the return on equity of the

company is negative because of the higher share repurchase and negative retained earnings of the

business whereas the cost of equity of the business represents that shareholders are expecting

minimum 4.89% of return from the company (Bloomberg and market risk premia, 2018). Though, the

number of shareholders and equity worth of the company is quite lower. It explains that in order to

manage the better financial position in the market, it becomes important for the business to maintain

better equity funds in the market.

Calculation of return on equity

Buy back 60 87 483 435 446

Total cash return to shareholders 409 778 1654 1703 1132

(Annual report, 2018)

It explains that recent financial changes are in the favour of the company and explains that

the financial position of the company is quite attractive for the investor’s point of view. These

have even helped the business to improve the stock price of the business.

FCFE analysis:

FCFE analysis represents that how much cash is available in the company for the

shareholders and it represents about the intrinsic share price of the company. On the basis of the

FCFE analysis, it has been found that the intrinsic price of the company is USD 41.52 whereas

the market price is USD 33.85 which explains that the stock price of the company is undervalued

and company is not required to pay this much of dividend (Reuters, 2018). Even the lower

dividend could help the business to maintain the capital market position.

The lower dividend is quite enough because if the shareholders want they could generate

the revenue through selling the stock of the company in the market and it would help them to

generate great revenue. The FCFE analysis represent about better investment opportunities in the

company.

Performance of the firm:

The financial performance of the company in last 5 years has been changed a lot and it has

impacted on the investment opportunities a capital market position of the company. Such as, in case of

comparison among the ROE and cost of equity, it has been found that the return on equity of the

company is negative because of the higher share repurchase and negative retained earnings of the

business whereas the cost of equity of the business represents that shareholders are expecting

minimum 4.89% of return from the company (Bloomberg and market risk premia, 2018). Though, the

number of shareholders and equity worth of the company is quite lower. It explains that in order to

manage the better financial position in the market, it becomes important for the business to maintain

better equity funds in the market.

Calculation of return on equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

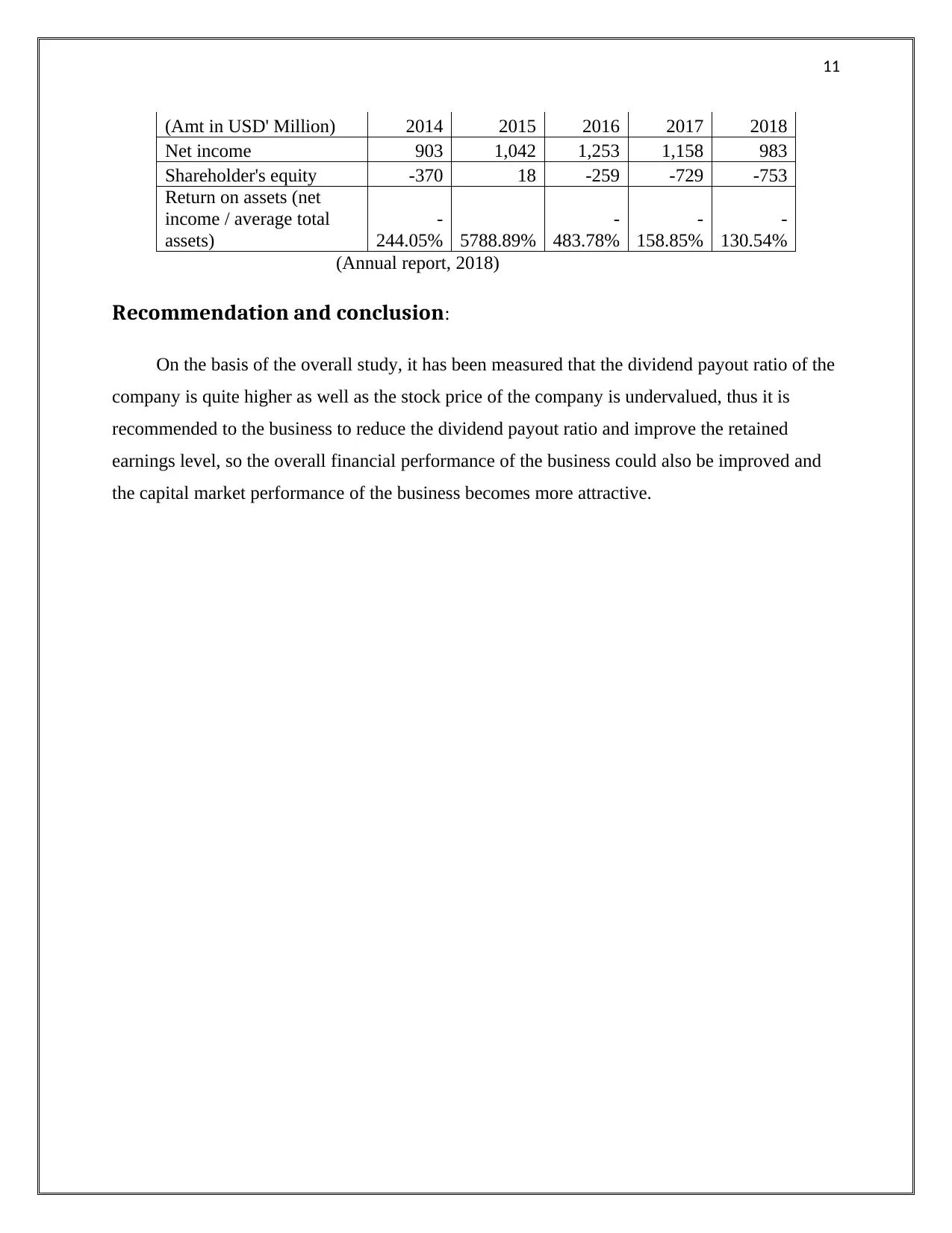

(Amt in USD' Million) 2014 2015 2016 2017 2018

Net income 903 1,042 1,253 1,158 983

Shareholder's equity -370 18 -259 -729 -753

Return on assets (net

income / average total

assets)

-

244.05% 5788.89%

-

483.78%

-

158.85%

-

130.54%

(Annual report, 2018)

Recommendation and conclusion:

On the basis of the overall study, it has been measured that the dividend payout ratio of the

company is quite higher as well as the stock price of the company is undervalued, thus it is

recommended to the business to reduce the dividend payout ratio and improve the retained

earnings level, so the overall financial performance of the business could also be improved and

the capital market performance of the business becomes more attractive.

(Amt in USD' Million) 2014 2015 2016 2017 2018

Net income 903 1,042 1,253 1,158 983

Shareholder's equity -370 18 -259 -729 -753

Return on assets (net

income / average total

assets)

-

244.05% 5788.89%

-

483.78%

-

158.85%

-

130.54%

(Annual report, 2018)

Recommendation and conclusion:

On the basis of the overall study, it has been measured that the dividend payout ratio of the

company is quite higher as well as the stock price of the company is undervalued, thus it is

recommended to the business to reduce the dividend payout ratio and improve the retained

earnings level, so the overall financial performance of the business could also be improved and

the capital market performance of the business becomes more attractive.

12

References

Annual Report. L Brand. Web. 2018. 27 October 2018. < http://investors.lb.com/phoenix.zhtml?

c=94854&p=irol-sec >

Reuters. L Brands Inc (LB.N). 2018. Web. 27 October 2018. <

https://www.reuters.com/finance/stocks/overview/LB.N >.

Spindices. S&P Dow Jones Indices. Web. 27 October 2018. <https://asia.spindices.com/search/?

query=dividend+and+buybacks&Search=Go&sortType=Date&resultsPerPage=25&ContentType

=Announcement >.

U.S. Department of the Treasury. Resource Center: Daily Treasury Yield Curve Rates, 2018.

Web. 27 October 2018. <https://www.treasury.gov/resource-center/data-chart-center/interest-

rates/Pages/TextView.aspx?data=yieldYear&year=2017>.

Yahoo Finance. L Brands, Inc. (LB). Analysis, 2018. Web. 27 October 2018. < h

https://finance.yahoo.com/quote/LB/analysis?p=LB >.

Yahoo Finance. S&P 500 (GSPC) Historical Data, 2018. Web. 27 October 2018. <

https://in.finance.yahoo.com/quote/%5EGSPC/history Annual report. “L Brands”.

Bloomberg. “Market rates”. Bloomberg, 2018. Web. 3rd Nov 2018.

<https://www.bloomberg.com/markets/rates>

Morningstar. “L Brands”. Morningstar, 2018. Web. 3rd Nov 2018.

<http://financials.morningstar.com/balance-sheet/bs.html?t=LB®ion=usa&culture=en-US>

Market risk premia. “USA market premium rates”. Market risk premia, 2018. Web. 3rd Nov 2018.

<http://www.market-risk-premia.com/us.html>

Reuters. “L Brands”. Reuters, 2018. Web. 3rd Nov 2018.

<https://www.reuters.com/finance/stocks/overview/LB.N>

?period1=1199125800&period2=1517337000&interval=1d&filter=history&frequency=1d >.

References

Annual Report. L Brand. Web. 2018. 27 October 2018. < http://investors.lb.com/phoenix.zhtml?

c=94854&p=irol-sec >

Reuters. L Brands Inc (LB.N). 2018. Web. 27 October 2018. <

https://www.reuters.com/finance/stocks/overview/LB.N >.

Spindices. S&P Dow Jones Indices. Web. 27 October 2018. <https://asia.spindices.com/search/?

query=dividend+and+buybacks&Search=Go&sortType=Date&resultsPerPage=25&ContentType

=Announcement >.

U.S. Department of the Treasury. Resource Center: Daily Treasury Yield Curve Rates, 2018.

Web. 27 October 2018. <https://www.treasury.gov/resource-center/data-chart-center/interest-

rates/Pages/TextView.aspx?data=yieldYear&year=2017>.

Yahoo Finance. L Brands, Inc. (LB). Analysis, 2018. Web. 27 October 2018. < h

https://finance.yahoo.com/quote/LB/analysis?p=LB >.

Yahoo Finance. S&P 500 (GSPC) Historical Data, 2018. Web. 27 October 2018. <

https://in.finance.yahoo.com/quote/%5EGSPC/history Annual report. “L Brands”.

Bloomberg. “Market rates”. Bloomberg, 2018. Web. 3rd Nov 2018.

<https://www.bloomberg.com/markets/rates>

Morningstar. “L Brands”. Morningstar, 2018. Web. 3rd Nov 2018.

<http://financials.morningstar.com/balance-sheet/bs.html?t=LB®ion=usa&culture=en-US>

Market risk premia. “USA market premium rates”. Market risk premia, 2018. Web. 3rd Nov 2018.

<http://www.market-risk-premia.com/us.html>

Reuters. “L Brands”. Reuters, 2018. Web. 3rd Nov 2018.

<https://www.reuters.com/finance/stocks/overview/LB.N>

?period1=1199125800&period2=1517337000&interval=1d&filter=history&frequency=1d >.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.