Taxation Law: Analysis of Labor's Dividend Imputation Proposal

VerifiedAdded on 2021/06/15

|10

|3715

|110

Report

AI Summary

This report analyzes the Labor Party's proposal concerning dividend imputation in the Australian taxation system. It begins by explaining the original dividend imputation system introduced in 1987, which aimed to eliminate double taxation by allowing companies to 'frank' dividends, effectively passing on corporate tax already paid to shareholders. The report then details the changes introduced by the Labor government in 2001, which allowed for cash refunds of excess imputation credits. The core of the report examines the proposed reversal of these changes by the current Labor Party, which would reinstate the original system and eliminate cash refunds, except for pensioners under a proposed 'Pensioner Guarantee'. The analysis explores the advantages and disadvantages of the proposal, focusing on its impact on self-managed superannuation funds, foreign investment, and the potential loss of franking credits. The report also considers the political feasibility of the proposal, highlighting the need for the Labor Party to win the next election and secure a majority in both houses of parliament to implement the changes. The report concludes by summarizing the current Australian imputation tax credit system.

TAXATION LAW

TASK – A

Labor’s Proposal for Dividend Imputation

The Original System of Imputation

The system of dividend imputation was introduced in 1987 by the Australian

government. When an Australian Resident Company earns a profit, it is required to pay

a part or whole of this profit to its shareholders (Bakker & Kloosterhof (ed.), 2010).

This sharing of profit is termed as ‘Dividend Distribution’. Just like the individual

resident taxpayer, resident companies too have the obligation of paying tax on the

profits earned (Barkoczy, 2018). The only difference between the two is that individuals

are taxed on a linear scale while companies pay corporate tax whose rate is of a single

slab, currently at 30% (Bakker & Kloosterhof (ed.), 2010).

Prior to 1987, when there was no system of dividend imputation, ATO taxed both the

payer (company) and the receiver (investor/shareholder). This resulted in double

taxation, as the single income source was being taxed in two hands (Tooma (ed.), 2008).

This anomaly was done away by the introduction of this system of dividend imputation.

Since the implementation of this system, the investor/shareholder, who is receiving the

dividend, is being taxed only for the difference between the corporate tax rate of 30%

and the marginal tax rate of the individual taxpayer (Coughlan, 2003). Now, if the

individual taxpayer is being taxed at 30%, then it has nothing to pay as tax as it has

already been paid by the company at the same rate. Hence, for the individual, the

dividend is tax free (Barkoczy, 2018). This has been illustrated more clearly in the

example section below (McCouat, 2012).

Changes in the Dividend Imputation System

Till 2001, when the Labor government introduced the New System of Imputation for

Dividends, the system was being managed under the following noted sections of the

Income Tax Assessment Act, 1997 –

s200-5 defines the Imputation System

s200-10 explains about franking a distribution

s200-15 explains how to maintain the franking account

TASK – A

Labor’s Proposal for Dividend Imputation

The Original System of Imputation

The system of dividend imputation was introduced in 1987 by the Australian

government. When an Australian Resident Company earns a profit, it is required to pay

a part or whole of this profit to its shareholders (Bakker & Kloosterhof (ed.), 2010).

This sharing of profit is termed as ‘Dividend Distribution’. Just like the individual

resident taxpayer, resident companies too have the obligation of paying tax on the

profits earned (Barkoczy, 2018). The only difference between the two is that individuals

are taxed on a linear scale while companies pay corporate tax whose rate is of a single

slab, currently at 30% (Bakker & Kloosterhof (ed.), 2010).

Prior to 1987, when there was no system of dividend imputation, ATO taxed both the

payer (company) and the receiver (investor/shareholder). This resulted in double

taxation, as the single income source was being taxed in two hands (Tooma (ed.), 2008).

This anomaly was done away by the introduction of this system of dividend imputation.

Since the implementation of this system, the investor/shareholder, who is receiving the

dividend, is being taxed only for the difference between the corporate tax rate of 30%

and the marginal tax rate of the individual taxpayer (Coughlan, 2003). Now, if the

individual taxpayer is being taxed at 30%, then it has nothing to pay as tax as it has

already been paid by the company at the same rate. Hence, for the individual, the

dividend is tax free (Barkoczy, 2018). This has been illustrated more clearly in the

example section below (McCouat, 2012).

Changes in the Dividend Imputation System

Till 2001, when the Labor government introduced the New System of Imputation for

Dividends, the system was being managed under the following noted sections of the

Income Tax Assessment Act, 1997 –

s200-5 defines the Imputation System

s200-10 explains about franking a distribution

s200-15 explains how to maintain the franking account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

s200-20 demonstrates how a distribution is franked

s207-20 illustrates how to calculate the Tax Liability of a franked distribution

Labor government planned to bring about a major reform in the dividend imputation

system in 2001 as per (Nethercott, Devos & Richardson, 2010), with an amendment

which would allow a cash refund to the taxpayer of any excess imputation credits. This

refund will be given after making adjustment of any tax liability of the taxpayer

(Barkoczy, 2018). This action would benefit those taxpayers who were being taxed with

a tax rate lower than that of corporate tax rate, at present being 30%, as they will

become eligible for a cash refund in case they have no other tax liability (Nethercott,

Devos & Richardson, 2010).

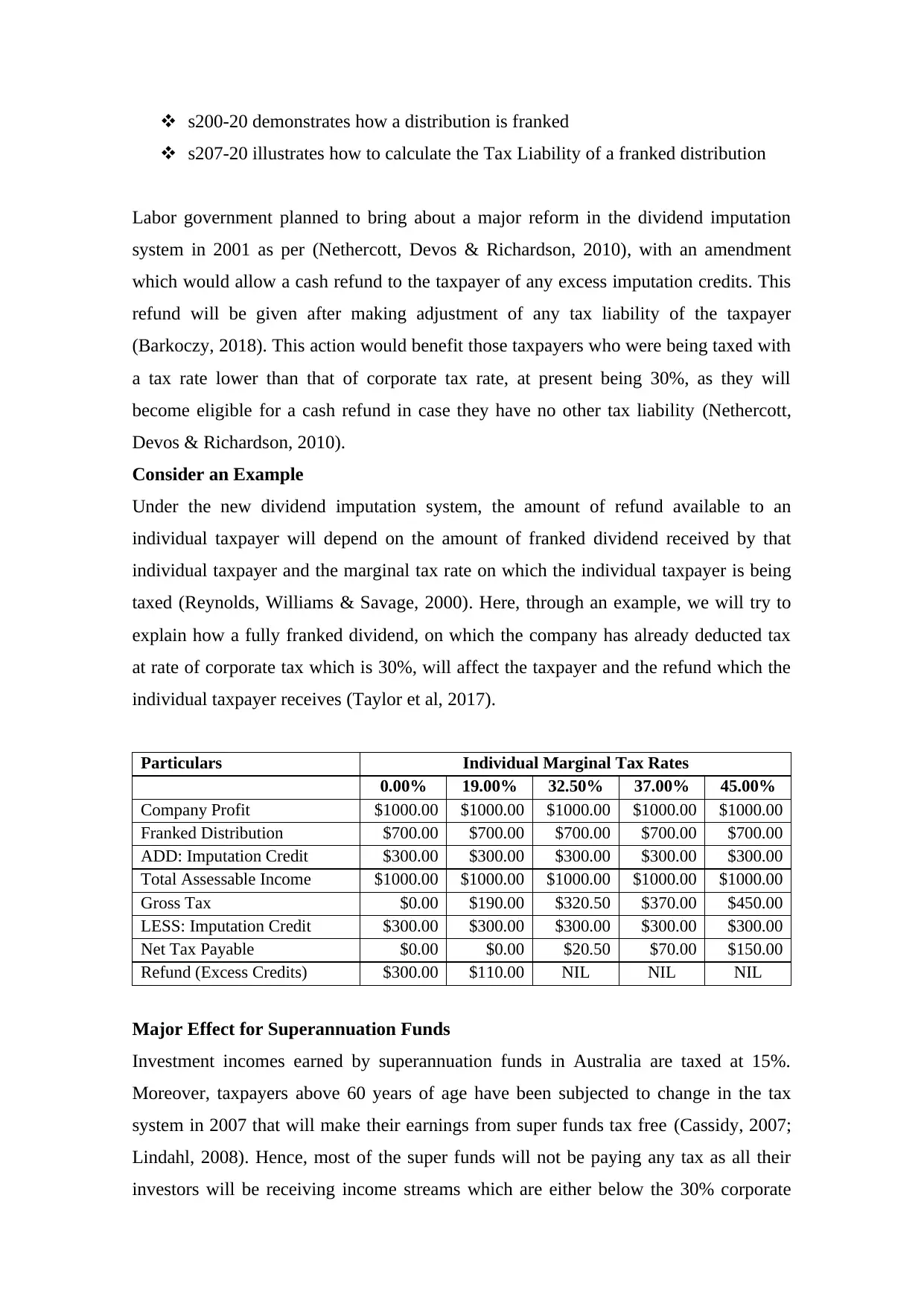

Consider an Example

Under the new dividend imputation system, the amount of refund available to an

individual taxpayer will depend on the amount of franked dividend received by that

individual taxpayer and the marginal tax rate on which the individual taxpayer is being

taxed (Reynolds, Williams & Savage, 2000). Here, through an example, we will try to

explain how a fully franked dividend, on which the company has already deducted tax

at rate of corporate tax which is 30%, will affect the taxpayer and the refund which the

individual taxpayer receives (Taylor et al, 2017).

Particulars Individual Marginal Tax Rates

0.00% 19.00% 32.50% 37.00% 45.00%

Company Profit $1000.00 $1000.00 $1000.00 $1000.00 $1000.00

Franked Distribution $700.00 $700.00 $700.00 $700.00 $700.00

ADD: Imputation Credit $300.00 $300.00 $300.00 $300.00 $300.00

Total Assessable Income $1000.00 $1000.00 $1000.00 $1000.00 $1000.00

Gross Tax $0.00 $190.00 $320.50 $370.00 $450.00

LESS: Imputation Credit $300.00 $300.00 $300.00 $300.00 $300.00

Net Tax Payable $0.00 $0.00 $20.50 $70.00 $150.00

Refund (Excess Credits) $300.00 $110.00 NIL NIL NIL

Major Effect for Superannuation Funds

Investment incomes earned by superannuation funds in Australia are taxed at 15%.

Moreover, taxpayers above 60 years of age have been subjected to change in the tax

system in 2007 that will make their earnings from super funds tax free (Cassidy, 2007;

Lindahl, 2008). Hence, most of the super funds will not be paying any tax as all their

investors will be receiving income streams which are either below the 30% corporate

s207-20 illustrates how to calculate the Tax Liability of a franked distribution

Labor government planned to bring about a major reform in the dividend imputation

system in 2001 as per (Nethercott, Devos & Richardson, 2010), with an amendment

which would allow a cash refund to the taxpayer of any excess imputation credits. This

refund will be given after making adjustment of any tax liability of the taxpayer

(Barkoczy, 2018). This action would benefit those taxpayers who were being taxed with

a tax rate lower than that of corporate tax rate, at present being 30%, as they will

become eligible for a cash refund in case they have no other tax liability (Nethercott,

Devos & Richardson, 2010).

Consider an Example

Under the new dividend imputation system, the amount of refund available to an

individual taxpayer will depend on the amount of franked dividend received by that

individual taxpayer and the marginal tax rate on which the individual taxpayer is being

taxed (Reynolds, Williams & Savage, 2000). Here, through an example, we will try to

explain how a fully franked dividend, on which the company has already deducted tax

at rate of corporate tax which is 30%, will affect the taxpayer and the refund which the

individual taxpayer receives (Taylor et al, 2017).

Particulars Individual Marginal Tax Rates

0.00% 19.00% 32.50% 37.00% 45.00%

Company Profit $1000.00 $1000.00 $1000.00 $1000.00 $1000.00

Franked Distribution $700.00 $700.00 $700.00 $700.00 $700.00

ADD: Imputation Credit $300.00 $300.00 $300.00 $300.00 $300.00

Total Assessable Income $1000.00 $1000.00 $1000.00 $1000.00 $1000.00

Gross Tax $0.00 $190.00 $320.50 $370.00 $450.00

LESS: Imputation Credit $300.00 $300.00 $300.00 $300.00 $300.00

Net Tax Payable $0.00 $0.00 $20.50 $70.00 $150.00

Refund (Excess Credits) $300.00 $110.00 NIL NIL NIL

Major Effect for Superannuation Funds

Investment incomes earned by superannuation funds in Australia are taxed at 15%.

Moreover, taxpayers above 60 years of age have been subjected to change in the tax

system in 2007 that will make their earnings from super funds tax free (Cassidy, 2007;

Lindahl, 2008). Hence, most of the super funds will not be paying any tax as all their

investors will be receiving income streams which are either below the 30% corporate

tax rate stream or are exempt from tax (Taylor et al, 2017; Nethercott, Devos &

Richardson, 2010).

As per this discussion, all investments made by superannuation funds in Resident

Australian Company Shares, will result in cash refund under the new system of dividend

imputation credits (Bakker & Kloosterhof (ed.), 2010; Barkoczy, 2018). As many old

age Australian taxpayers are using self-managed superannuation funds, which invest

directly in Australian Resident Company Shares, will receive a cash refund which will

be equivalent to the imputation credit amount and this will increase the effective yield

for them from their investments (Taylor et al, 2017; Tooma (ed.), 2008).

Proposed Changes

Since the Labor Party is in the opposition, it has proposed that the changes it had

introduced in 2001 should be reversed by altering section 46F of the ITAA 1936. This

means that Labor Party now wants that the original imputation system, which was in

force prior to 2001, should be restored effective 1 July 2019 (Reynolds, Williams &

Savage, 2000; Tooma (ed.), 2008). This will imply that any excess imputation credit,

being paid as a rebate to taxpayer under section 46 and 46A of the ITAA 1936, will no

longer be payable to taxpayers as cash refund (Taylor et al, 2017). However, the Labor

Party is also considering the proposal that this revised measure does not make any

impact on taxpayers receiving government pension or allowance. For the safety of the

pensioners, Labor has proposed a Pensioner Guarantee, which will allow the pensioners

to receive Cash Refund of any excess dividend imputation credit (Bakker & Kloosterhof

(ed.), 2010; Barkoczy, 2018).

Who is going to be affected the most?

As has been discussed above in this paper, this proposal of the Labor Party will greatly

impact the self-managed super fund investors, as these funds are the biggest

contributors to the Australian share market and are mostly made up of pensioners

(Nethercott, Devos & Richardson, 2010; Reynolds, Williams & Savage, 2000;

Barkoczy, 2018).

Some Important Points

The most important point is that this policy does not have the support of the present

ruling party running the government (Bakker & Kloosterhof (ed.), 2010). Hence, to

implement this proposal, the Labor Party has to first win the next general election,

Richardson, 2010).

As per this discussion, all investments made by superannuation funds in Resident

Australian Company Shares, will result in cash refund under the new system of dividend

imputation credits (Bakker & Kloosterhof (ed.), 2010; Barkoczy, 2018). As many old

age Australian taxpayers are using self-managed superannuation funds, which invest

directly in Australian Resident Company Shares, will receive a cash refund which will

be equivalent to the imputation credit amount and this will increase the effective yield

for them from their investments (Taylor et al, 2017; Tooma (ed.), 2008).

Proposed Changes

Since the Labor Party is in the opposition, it has proposed that the changes it had

introduced in 2001 should be reversed by altering section 46F of the ITAA 1936. This

means that Labor Party now wants that the original imputation system, which was in

force prior to 2001, should be restored effective 1 July 2019 (Reynolds, Williams &

Savage, 2000; Tooma (ed.), 2008). This will imply that any excess imputation credit,

being paid as a rebate to taxpayer under section 46 and 46A of the ITAA 1936, will no

longer be payable to taxpayers as cash refund (Taylor et al, 2017). However, the Labor

Party is also considering the proposal that this revised measure does not make any

impact on taxpayers receiving government pension or allowance. For the safety of the

pensioners, Labor has proposed a Pensioner Guarantee, which will allow the pensioners

to receive Cash Refund of any excess dividend imputation credit (Bakker & Kloosterhof

(ed.), 2010; Barkoczy, 2018).

Who is going to be affected the most?

As has been discussed above in this paper, this proposal of the Labor Party will greatly

impact the self-managed super fund investors, as these funds are the biggest

contributors to the Australian share market and are mostly made up of pensioners

(Nethercott, Devos & Richardson, 2010; Reynolds, Williams & Savage, 2000;

Barkoczy, 2018).

Some Important Points

The most important point is that this policy does not have the support of the present

ruling party running the government (Bakker & Kloosterhof (ed.), 2010). Hence, to

implement this proposal, the Labor Party has to first win the next general election,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which is proposed to be held before 18 May 2019 (Reynolds, Williams & Savage, 2000;

Barkoczy, 2018).

The second important point is that a successful Labor government will need absolute

majority in both the lower and the upper house for passing of this proposal so that it can

become a legislation (Reynolds, Williams & Savage, 2000; Taylor et al, 2017).

Finally, for favoring the pensioners through the Pensioner Guarantee, the new

government would be expected to bring further amendments in the proposal (Lindahl,

2008).

TASK – B

Advantages and Disadvantages of Labor’s Proposal

ADVANTAGES

Australian system of imputation of tax credits is operated for providing tax benefits to

domestic shareholders of Australian Resident Companies. These shareholders are

entitled to a tax credit (considered as a rebate available under section 46 and 46A of the

ITAA, 1936) as the holding company has already paid tax at the corporate tax level of

30% and the tax threshold of the individual resident taxpayer is below 30% threshold

(Bakker & Kloosterhof (ed.), 2010). Thus, this tax credit helps the individual taxpayer

by reducing their personal income tax liability which the shareholder is required to fulfil

on the dividend income earned. It can be said that the tax being paid by the shareholder

under the existing dividend imputation system is a top‐up tax after reducing the amount

of tax already paid by the dividend paying company on the income which originated

from its corporate profits (Taylor et al, 2017; Cch, 2010).

This can be better explained by the following example. Here we are assuming that the

Australian Resident Company has declared a profit of $100 before‐tax. The existing

rules governing income tax require that the company pay tax of $30 at the statutory

corporate tax rate of 30% (Barkoczy, 2018; Nethercott, Devos & Richardson, 2010).

The company can generate an Imputation Credit of $30 in its franking account, after

Barkoczy, 2018).

The second important point is that a successful Labor government will need absolute

majority in both the lower and the upper house for passing of this proposal so that it can

become a legislation (Reynolds, Williams & Savage, 2000; Taylor et al, 2017).

Finally, for favoring the pensioners through the Pensioner Guarantee, the new

government would be expected to bring further amendments in the proposal (Lindahl,

2008).

TASK – B

Advantages and Disadvantages of Labor’s Proposal

ADVANTAGES

Australian system of imputation of tax credits is operated for providing tax benefits to

domestic shareholders of Australian Resident Companies. These shareholders are

entitled to a tax credit (considered as a rebate available under section 46 and 46A of the

ITAA, 1936) as the holding company has already paid tax at the corporate tax level of

30% and the tax threshold of the individual resident taxpayer is below 30% threshold

(Bakker & Kloosterhof (ed.), 2010). Thus, this tax credit helps the individual taxpayer

by reducing their personal income tax liability which the shareholder is required to fulfil

on the dividend income earned. It can be said that the tax being paid by the shareholder

under the existing dividend imputation system is a top‐up tax after reducing the amount

of tax already paid by the dividend paying company on the income which originated

from its corporate profits (Taylor et al, 2017; Cch, 2010).

This can be better explained by the following example. Here we are assuming that the

Australian Resident Company has declared a profit of $100 before‐tax. The existing

rules governing income tax require that the company pay tax of $30 at the statutory

corporate tax rate of 30% (Barkoczy, 2018; Nethercott, Devos & Richardson, 2010).

The company can generate an Imputation Credit of $30 in its franking account, after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

paying the corporate tax of $30. The after tax retained profit of the company is $70.

Subsequently, when the company pays dividend of $70 to the shareholder, it will attach

the franking credit of $30 to the dividend amount. Now, the company’s franking

account will show ‘NIL’ balance (Nethercott, Devos & Richardson, 2010; Tooma (ed.),

2008; Lindahl, 2008).

Now consider the accounting of the individual shareholder. After receiving the franked

dividend of $70 and the ‘grossed-up’ franking credit of $30, the individual taxpayer has

earned a before‐tax income of $100 (Reynolds, Williams & Savage, 2000). Supposing

that the individual taxpayer is being taxed at the top bracket of 45%, it will create a tax

liability of $45, calculated on the grossed‐up franked dividend amount of $100. Under

the prevailing dividend imputation system, the Australian resident taxpayer is entitled to

the franking credit of $30 (Barkoczy, 2018). When this is offset against the individual’s

tax liability of $49, the net tax liability of the individual taxpayer stands at $49–$30 =

$19. This is the justified advantage which every resident taxpayer in Australia is getting

from the imputation credit system (Reynolds, Williams & Savage, 2000).

The only big advantage from abolishing of the present imputation tax credit system can

be the promotion of foreign direct investment in Australia, as the use of jurisdiction for

a company’s residence status will not be considered (Taylor et al, 2017; Bakker &

Kloosterhof (ed.), 2010).

DISADVANTAGES

The biggest disadvantage to which the individual taxpayer will be subjected is the loss

of the franking credit. Consider, in the above example, the situation when the

imputation system is abolished (Bakker & Kloosterhof (ed.), 2010; McCouat, 2012).

Against the residual tax liability of $19 at the individual taxpayer’s, under the revised

imputation tax system, when no tax credit is available to the individual taxpayer on

account of the previously paid tax by the company, the total income tax paid to the ATO

on the original profit of $100 earned by the company, would be $79 ($30 paid by the

company and $49 paid by the shareholder) (Taylor et al, 2017; Cassidy, 2007; Cch,

2010).

Subsequently, when the company pays dividend of $70 to the shareholder, it will attach

the franking credit of $30 to the dividend amount. Now, the company’s franking

account will show ‘NIL’ balance (Nethercott, Devos & Richardson, 2010; Tooma (ed.),

2008; Lindahl, 2008).

Now consider the accounting of the individual shareholder. After receiving the franked

dividend of $70 and the ‘grossed-up’ franking credit of $30, the individual taxpayer has

earned a before‐tax income of $100 (Reynolds, Williams & Savage, 2000). Supposing

that the individual taxpayer is being taxed at the top bracket of 45%, it will create a tax

liability of $45, calculated on the grossed‐up franked dividend amount of $100. Under

the prevailing dividend imputation system, the Australian resident taxpayer is entitled to

the franking credit of $30 (Barkoczy, 2018). When this is offset against the individual’s

tax liability of $49, the net tax liability of the individual taxpayer stands at $49–$30 =

$19. This is the justified advantage which every resident taxpayer in Australia is getting

from the imputation credit system (Reynolds, Williams & Savage, 2000).

The only big advantage from abolishing of the present imputation tax credit system can

be the promotion of foreign direct investment in Australia, as the use of jurisdiction for

a company’s residence status will not be considered (Taylor et al, 2017; Bakker &

Kloosterhof (ed.), 2010).

DISADVANTAGES

The biggest disadvantage to which the individual taxpayer will be subjected is the loss

of the franking credit. Consider, in the above example, the situation when the

imputation system is abolished (Bakker & Kloosterhof (ed.), 2010; McCouat, 2012).

Against the residual tax liability of $19 at the individual taxpayer’s, under the revised

imputation tax system, when no tax credit is available to the individual taxpayer on

account of the previously paid tax by the company, the total income tax paid to the ATO

on the original profit of $100 earned by the company, would be $79 ($30 paid by the

company and $49 paid by the shareholder) (Taylor et al, 2017; Cassidy, 2007; Cch,

2010).

Another disadvantage occurs in cases where the Australian resident company is paying

tax at a rate which is lower as compared to the statutory tax rate, the company will be

having insufficient franking credits in its franking account and will not be able to issue

fully franked dividends (Cch, 2010: Coughlan, 2003; McCouat, 2012). The third

disadvantage created by the new system would occur in situations where the company is

not required to pay any income tax on the profits earned because it is availing tax offsets

on account of research and development activities (Taylor et al, 2017). Such companies

will be distributing the dividends as unfranked dividends. Disadvantage is also created

when the dividend paying company is Non-resident or the recipient shareholder is Non-

resident (Tooma (ed.), 2008; Nethercott, Devos & Richardson, 2010; Reynolds,

Williams & Savage, 2000).

The biggest disadvantage of this new system would be the effect on pensioners and the

tax-exempt bodies. These will not be able to take advantage of building their resources

from the tax refunds they receive (Reynolds, Williams & Savage, 2000; Bakker &

Kloosterhof (ed.), 2010).

CREATING A GOOD POLICY

Considering the pros and cons discussed above, it can be safely stated that present

Australian imputation tax credit system is a system where prepayment of tax is made by

the companies on the corporate profits and the resident shareholder pays income tax on

these distributed company profits at the applicable marginal tax rate (Lindahl, 2008;

Taylor et al, 2017; Tooma (ed.), 2008). However, the current imputation tax credit

system can also distort the dividend payments in a situation where a company is unable

to pay maximum dividend to its shareholders because it has insufficient franking credit

(Cch, 2010; Barkoczy, 2018; Tooma (ed.), 2008).

The first step towards creating a Good Policy is to minimize this restriction by treating

the franking credit paid by the company to the ATO as an advance tax payment by the

company on account of its income tax liability on the profits earned. The second step

towards a Good Policy is to abolish any tier-ranking system of dividends (franked and

unfranked) and maintain only tax-exempt dividends category. This can be affected by

altering section 46F of the ITAA, 1936.

tax at a rate which is lower as compared to the statutory tax rate, the company will be

having insufficient franking credits in its franking account and will not be able to issue

fully franked dividends (Cch, 2010: Coughlan, 2003; McCouat, 2012). The third

disadvantage created by the new system would occur in situations where the company is

not required to pay any income tax on the profits earned because it is availing tax offsets

on account of research and development activities (Taylor et al, 2017). Such companies

will be distributing the dividends as unfranked dividends. Disadvantage is also created

when the dividend paying company is Non-resident or the recipient shareholder is Non-

resident (Tooma (ed.), 2008; Nethercott, Devos & Richardson, 2010; Reynolds,

Williams & Savage, 2000).

The biggest disadvantage of this new system would be the effect on pensioners and the

tax-exempt bodies. These will not be able to take advantage of building their resources

from the tax refunds they receive (Reynolds, Williams & Savage, 2000; Bakker &

Kloosterhof (ed.), 2010).

CREATING A GOOD POLICY

Considering the pros and cons discussed above, it can be safely stated that present

Australian imputation tax credit system is a system where prepayment of tax is made by

the companies on the corporate profits and the resident shareholder pays income tax on

these distributed company profits at the applicable marginal tax rate (Lindahl, 2008;

Taylor et al, 2017; Tooma (ed.), 2008). However, the current imputation tax credit

system can also distort the dividend payments in a situation where a company is unable

to pay maximum dividend to its shareholders because it has insufficient franking credit

(Cch, 2010; Barkoczy, 2018; Tooma (ed.), 2008).

The first step towards creating a Good Policy is to minimize this restriction by treating

the franking credit paid by the company to the ATO as an advance tax payment by the

company on account of its income tax liability on the profits earned. The second step

towards a Good Policy is to abolish any tier-ranking system of dividends (franked and

unfranked) and maintain only tax-exempt dividends category. This can be affected by

altering section 46F of the ITAA, 1936.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The third step towards creating a Good Policy is through a corporate tax system, to be

known as the Classical System where the companies are taxed at a lower rate on the

profits earned and there is no franking credit system when dividends are distributed

(Lindahl, 2008). Simply tax the recipient shareholder on the dividends received by

them. This will also do away with the double taxation scenario. Such a Classical System

will discourage the businesses (especially the family-controlled companies) to use

corporations as vehicles for hindering dividend payments (Nethercott, Devos &

Richardson, 2010; Barkoczy, 2018; Reynolds, Williams & Savage, 2000).

Finally, a way to compensate the pensioners can be to encourage them in investing in

high-yield convertible debt instruments, instead of in shares and these new investment

vehicles be allowed tax exemptions (Tooma (ed.), 2008; Lindahl, 2008).

TASK – C

ANSWER – 1

During the FY 2015-16 the threshold for a Small Business Entity (SBE) was $2 million.

Since Sigma Pty Ltd had an annual turnover of $12 million, it did not qualify for the

SBE category (within the meaning of s. 328-115 of ITAA, 1997), hence it would be

taxed at Corporate Tax Rate of 30% (Barkoczy, 2018). However, in the FY 2016-17,

Sigma had a turnover of $9 million and since it was below the threshold limit of $10

million (within the meaning of s. 328-115 of ITAA, 1997), Sigma would be taxed at

Corporate Tax Rate of 27.5%.

ANSWER – 2

The maximum franking credit which a company can be allocated for distribution of

dividend for the 2015-16 and 2016-17 income years has been based on the corporate tax

entity's applicable corporate tax rate for the purpose of imputation (Barkoczy, 2018).

ANSWER – 3

known as the Classical System where the companies are taxed at a lower rate on the

profits earned and there is no franking credit system when dividends are distributed

(Lindahl, 2008). Simply tax the recipient shareholder on the dividends received by

them. This will also do away with the double taxation scenario. Such a Classical System

will discourage the businesses (especially the family-controlled companies) to use

corporations as vehicles for hindering dividend payments (Nethercott, Devos &

Richardson, 2010; Barkoczy, 2018; Reynolds, Williams & Savage, 2000).

Finally, a way to compensate the pensioners can be to encourage them in investing in

high-yield convertible debt instruments, instead of in shares and these new investment

vehicles be allowed tax exemptions (Tooma (ed.), 2008; Lindahl, 2008).

TASK – C

ANSWER – 1

During the FY 2015-16 the threshold for a Small Business Entity (SBE) was $2 million.

Since Sigma Pty Ltd had an annual turnover of $12 million, it did not qualify for the

SBE category (within the meaning of s. 328-115 of ITAA, 1997), hence it would be

taxed at Corporate Tax Rate of 30% (Barkoczy, 2018). However, in the FY 2016-17,

Sigma had a turnover of $9 million and since it was below the threshold limit of $10

million (within the meaning of s. 328-115 of ITAA, 1997), Sigma would be taxed at

Corporate Tax Rate of 27.5%.

ANSWER – 2

The maximum franking credit which a company can be allocated for distribution of

dividend for the 2015-16 and 2016-17 income years has been based on the corporate tax

entity's applicable corporate tax rate for the purpose of imputation (Barkoczy, 2018).

ANSWER – 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the FY 2015-16, Sigma had a turnover of $12 million and since this was above the

threshold limit of $2 million, Sigma was liable to be taxed at the Corporate Tax Rate of

30.0% (McCouat, 2012). Sigma declared taxable income of $1,000,000 for the income

year 2015-16. Hence, the company’s tax liability stands at $300,000 ($1,000,000*30%)

(Nethercott, Devos & Richardson, 2010).

Since the dividend was declared and paid to the shareholders in August 2016, Yolande

shall receive dividend of $100,000, which Sigma’s board announced to be paid to each

shareholder (Nethercott, Devos & Richardson, 2010). Since it has been stated that

Yolande was paying income tax under the highest slab of 45%, she has a tax liability of

$ 45,000 - $30,000 of franking credit. Hence, Yolande has a Net Tax Liability, on

account of franked dividend from Sigma, at $15,000 (Taylor et al, 2017).

Net distribution received by Yolande = $55,000.00

Total tax paid by Sigma and Yolande = $45,000.00

ANSWER – 4

In the above discussed scenario, the dividend of $100,000, declared by Sigma Pty Ltd in

August 2016, was in relation to company’s income year 2015-16, when Sigma had

declared a taxable income of $1 million. Based on the fact that Yolande was already

owning 10% shares of Sigma, the tax liability arose on account of Sigma and Yolande

(Reynolds, Williams & Savage, 2000).

But in this revised situation, when it is stated that Yolande will become a shareholder

from 30 May 2017, there is no liability of tax either on Sigma or on Yolande as Yolande

is not entitled for any portion of the dividend declared by Sigma in August 2016 (Taylor

et al, 2017).

ANSWER – 5

In case Sigma reports an annual turnover of $20 million in place of $9 million reported

now, it will lose its advantage of getting rebate under the Small Business Enterprise

(SBE) category, as it will be above the threshold limit of $10 million (within the

meaning of s. 328-115 of ITAA, 1997) (Bakker & Kloosterhof (ed.), 2010). Under this

threshold limit of $2 million, Sigma was liable to be taxed at the Corporate Tax Rate of

30.0% (McCouat, 2012). Sigma declared taxable income of $1,000,000 for the income

year 2015-16. Hence, the company’s tax liability stands at $300,000 ($1,000,000*30%)

(Nethercott, Devos & Richardson, 2010).

Since the dividend was declared and paid to the shareholders in August 2016, Yolande

shall receive dividend of $100,000, which Sigma’s board announced to be paid to each

shareholder (Nethercott, Devos & Richardson, 2010). Since it has been stated that

Yolande was paying income tax under the highest slab of 45%, she has a tax liability of

$ 45,000 - $30,000 of franking credit. Hence, Yolande has a Net Tax Liability, on

account of franked dividend from Sigma, at $15,000 (Taylor et al, 2017).

Net distribution received by Yolande = $55,000.00

Total tax paid by Sigma and Yolande = $45,000.00

ANSWER – 4

In the above discussed scenario, the dividend of $100,000, declared by Sigma Pty Ltd in

August 2016, was in relation to company’s income year 2015-16, when Sigma had

declared a taxable income of $1 million. Based on the fact that Yolande was already

owning 10% shares of Sigma, the tax liability arose on account of Sigma and Yolande

(Reynolds, Williams & Savage, 2000).

But in this revised situation, when it is stated that Yolande will become a shareholder

from 30 May 2017, there is no liability of tax either on Sigma or on Yolande as Yolande

is not entitled for any portion of the dividend declared by Sigma in August 2016 (Taylor

et al, 2017).

ANSWER – 5

In case Sigma reports an annual turnover of $20 million in place of $9 million reported

now, it will lose its advantage of getting rebate under the Small Business Enterprise

(SBE) category, as it will be above the threshold limit of $10 million (within the

meaning of s. 328-115 of ITAA, 1997) (Bakker & Kloosterhof (ed.), 2010). Under this

changed scenario, the corporate tax rate of Sigma will also change from the present

27.5% to 30%.

This changed scenario will change the proportion of tax being paid by Sigma, which

will go up because of increased tax rate (from 27.5% to 30%). On the other hand, the

tax liability of Yolande will be reduced as Sigma will deduct franking credit at 30% and

since Yolande is taxed at 45%, it will pay tax at 15% (45% - 30%).

LIST OF REFERENCES

Bakker, A. and Kloosterhof, S. (ed.). 2010 Tax risk management. Amsterdam: IBFD.

Barkoczy, S. 2018 Core Tax Legislation and Study Guide (21st ed). Oxford: Oxford

University Press.

Cassidy, J. 2007 Concise Income Tax, 4th ed. Annandale, NSW: Federation Press.

Cch. 2010 Australian Master Financial Planning Guide. Sydney, NSW: CCH Australia

Limited.

Coughlan, L. 2003 The Law and You. Glebe, NSW: Pascal Press.

Lindahl, D. 2008 How Small Investors Can Get Started and Make It Big. Hoboken, NJ:

John Wiley & Sons.

McCouat, P. 2012 Australian Master GST Guide, 13th ed. Sydney, NSW: CCH Australia

Limited.

Nethercott, L., Devos, K. and Richardson, G. 2010 Master Tax Examples 2010/11, 9th

ed. Sydney, NSW: CCH Australia Limited.

Reynolds, W., Williams, A. J. and Savage, W. 2000 Your Own Business: A Practical

Guide to Success, 3rd ed. Sydney, NSW: Cengage Learning Australia.

Taylor, C.J., Taylor, J.E.A., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2017

Understanding Taxation Law 2017. New York: LexisNexis Butterworths.

Tooma, R. A. (ed.). 2008 Legislating against Tax Avoidance. Amsterdam: IBFD.

27.5% to 30%.

This changed scenario will change the proportion of tax being paid by Sigma, which

will go up because of increased tax rate (from 27.5% to 30%). On the other hand, the

tax liability of Yolande will be reduced as Sigma will deduct franking credit at 30% and

since Yolande is taxed at 45%, it will pay tax at 15% (45% - 30%).

LIST OF REFERENCES

Bakker, A. and Kloosterhof, S. (ed.). 2010 Tax risk management. Amsterdam: IBFD.

Barkoczy, S. 2018 Core Tax Legislation and Study Guide (21st ed). Oxford: Oxford

University Press.

Cassidy, J. 2007 Concise Income Tax, 4th ed. Annandale, NSW: Federation Press.

Cch. 2010 Australian Master Financial Planning Guide. Sydney, NSW: CCH Australia

Limited.

Coughlan, L. 2003 The Law and You. Glebe, NSW: Pascal Press.

Lindahl, D. 2008 How Small Investors Can Get Started and Make It Big. Hoboken, NJ:

John Wiley & Sons.

McCouat, P. 2012 Australian Master GST Guide, 13th ed. Sydney, NSW: CCH Australia

Limited.

Nethercott, L., Devos, K. and Richardson, G. 2010 Master Tax Examples 2010/11, 9th

ed. Sydney, NSW: CCH Australia Limited.

Reynolds, W., Williams, A. J. and Savage, W. 2000 Your Own Business: A Practical

Guide to Success, 3rd ed. Sydney, NSW: Cengage Learning Australia.

Taylor, C.J., Taylor, J.E.A., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2017

Understanding Taxation Law 2017. New York: LexisNexis Butterworths.

Tooma, R. A. (ed.). 2008 Legislating against Tax Avoidance. Amsterdam: IBFD.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.