Accounting and Financial Analysis for a Landscaping Business Project

VerifiedAdded on 2020/03/23

|8

|2058

|77

Homework Assignment

AI Summary

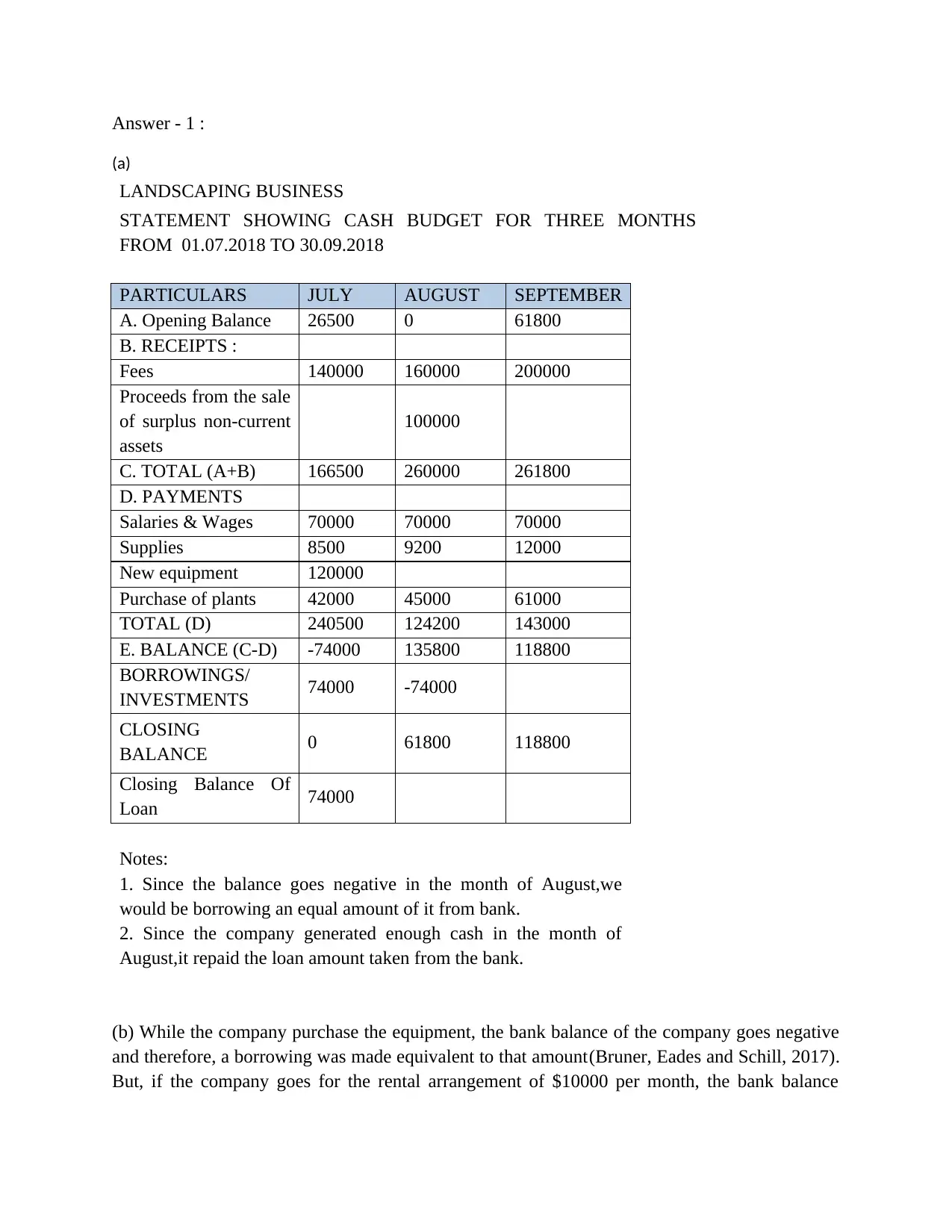

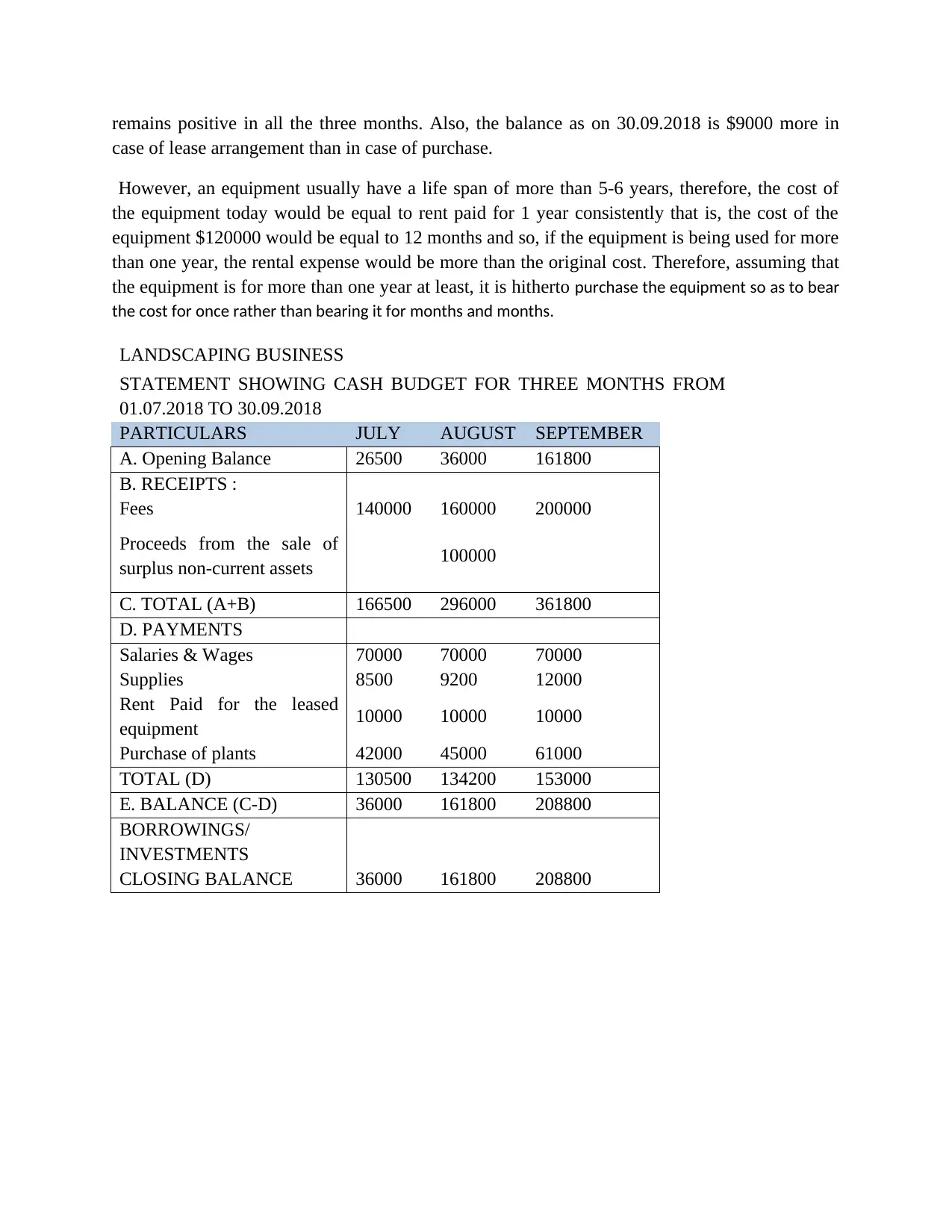

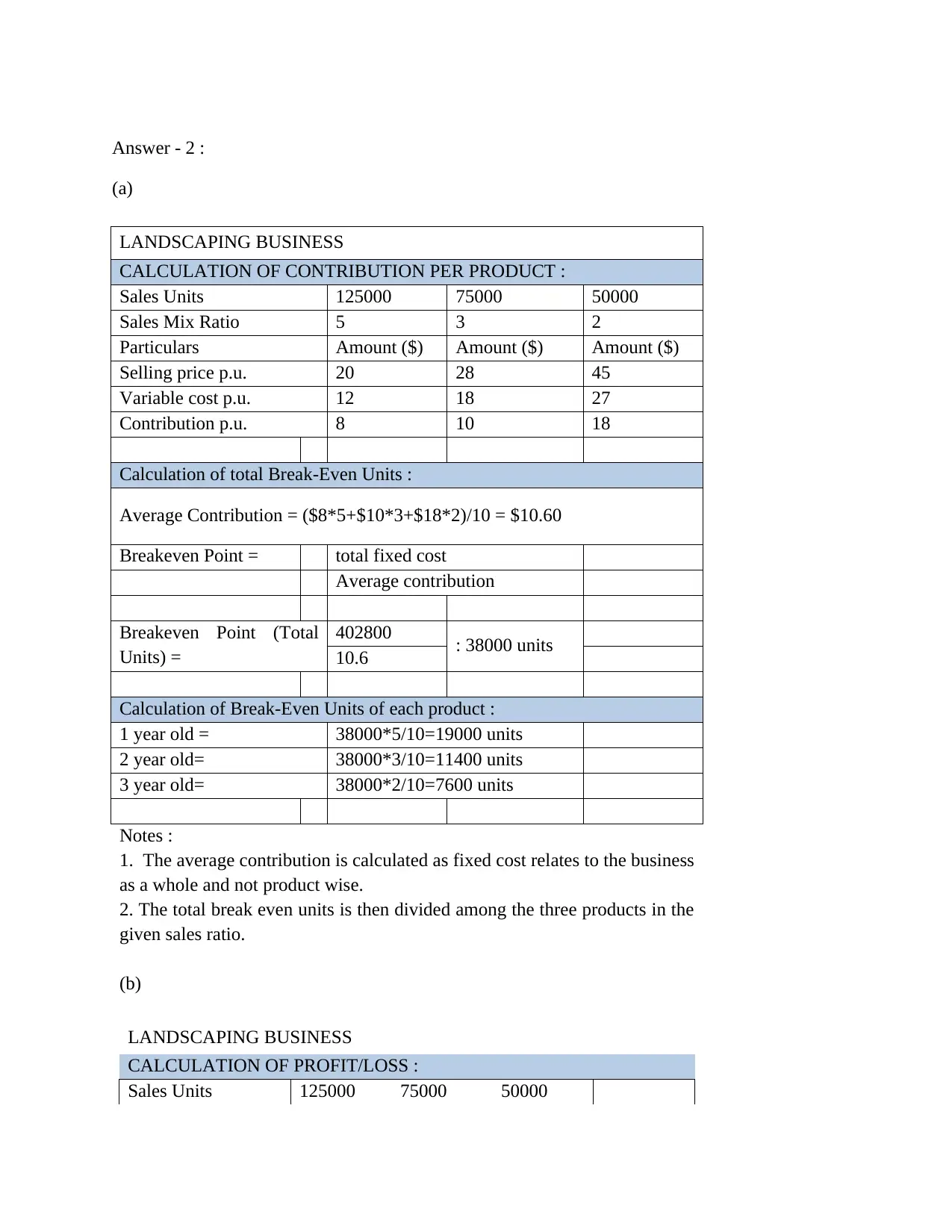

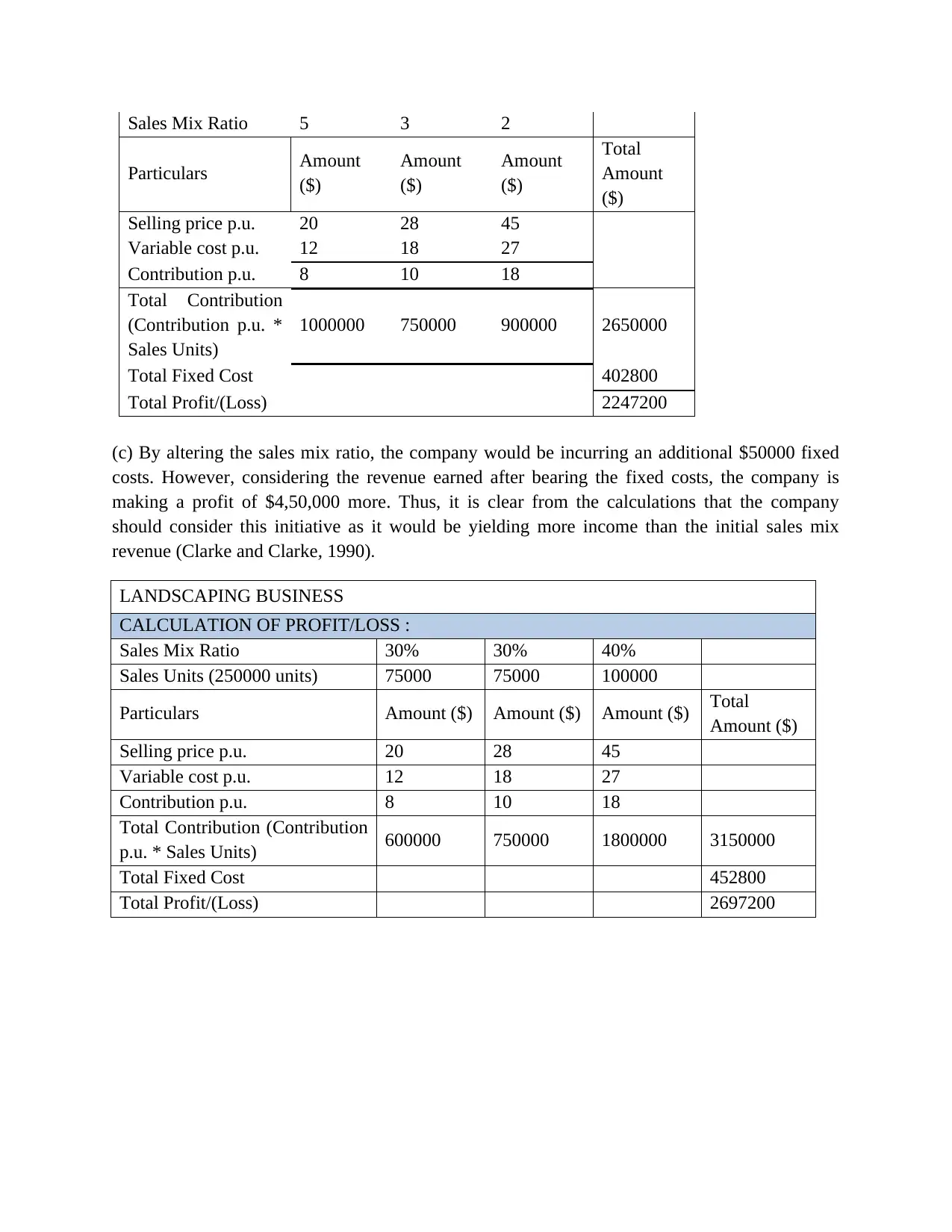

This assignment analyzes the financial performance of a landscaping business through cash budgeting, break-even analysis, and investment decision-making. It presents a cash budget for three months, detailing receipts, payments, and the resulting cash balance, including scenarios with and without equipment purchase. The assignment calculates the contribution per product and determines the break-even point, as well as the profit/loss under different sales mix ratios. Finally, it evaluates the decision-making process for equipment purchase, comparing accounting rate of return (ARR) and internal rate of return (IRR) and discussing the limitations of using these metrics in isolation. The assignment emphasizes the importance of considering time value of money and cash flow for effective financial decisions. It also provides references for further reading.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.