Financial Performance Analysis of a Landscaping Business Report

VerifiedAdded on 2020/04/01

|6

|1470

|47

Report

AI Summary

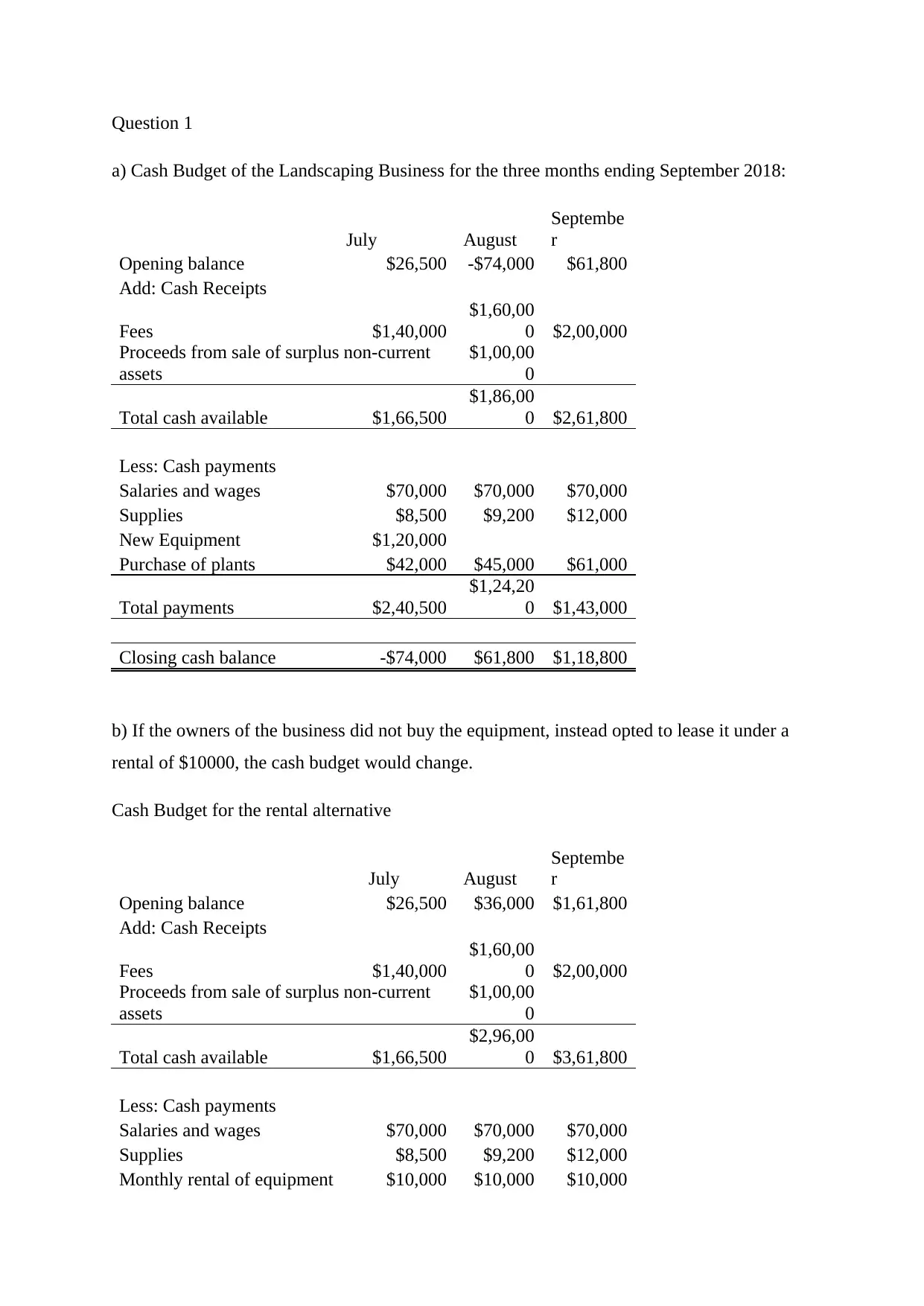

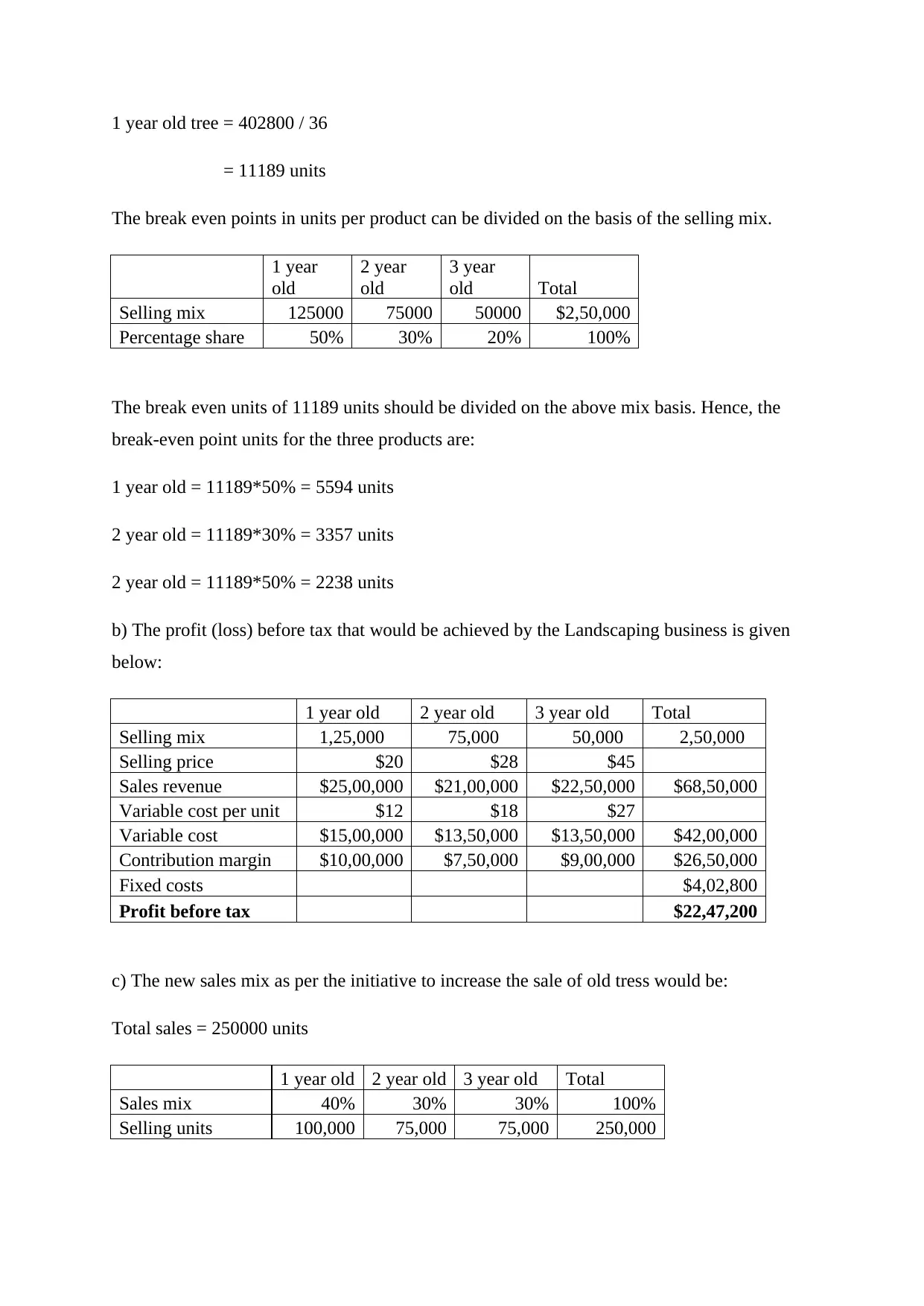

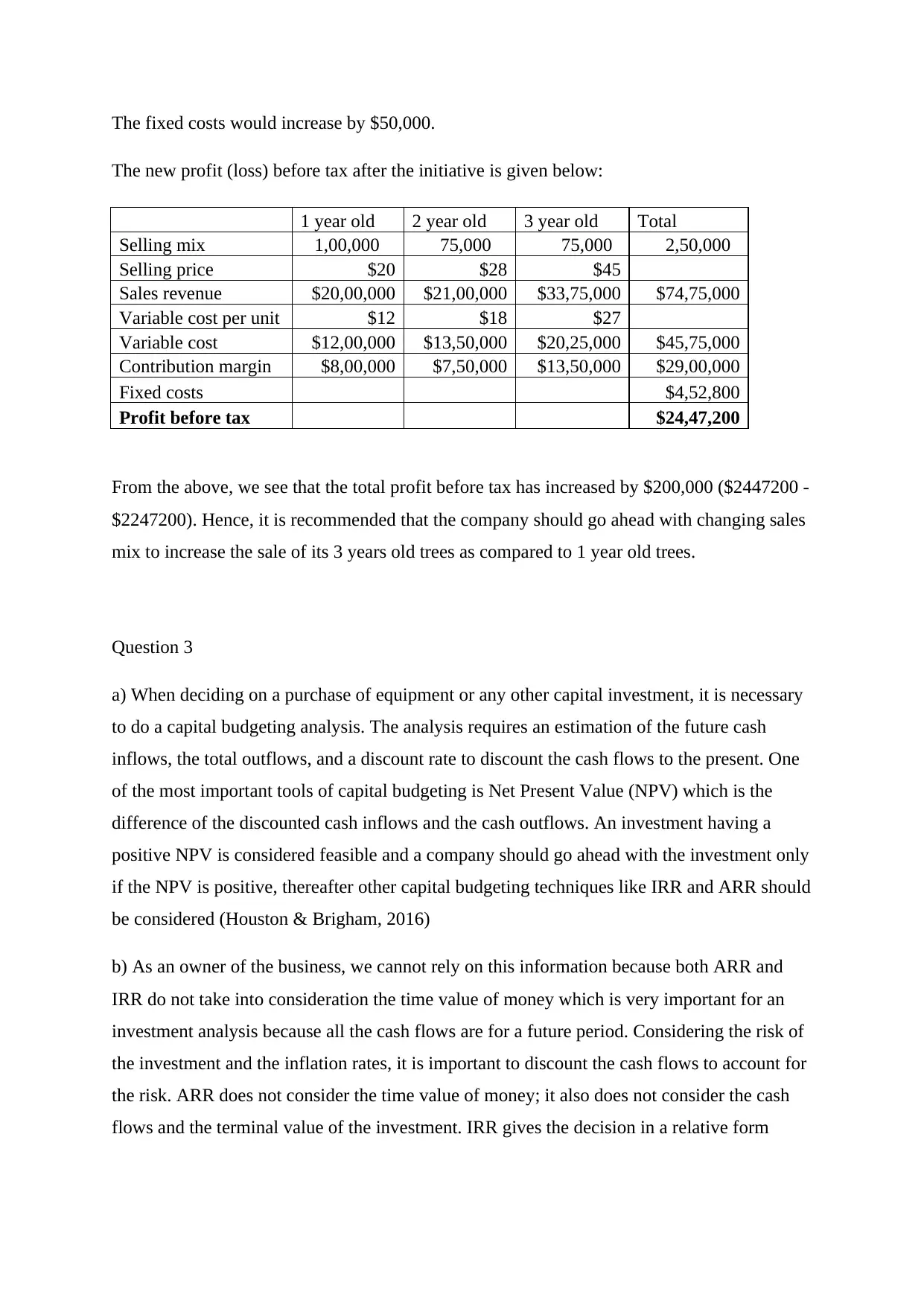

This report presents a comprehensive financial analysis of a landscaping business. It begins with a cash budget analysis for three months, comparing scenarios of equipment purchase versus leasing, highlighting the impact on cash flow. The report then calculates break-even points for different product lines, considering various sales mixes and their effect on overall profitability. Furthermore, it delves into capital budgeting, emphasizing the importance of Net Present Value (NPV) and contrasting the limitations of Average Rate of Return (ARR) and Internal Rate of Return (IRR) in investment decisions. The analysis concludes with recommendations on optimizing sales mix to enhance profit, supported by detailed financial calculations and references to relevant financial management literature.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.