AF304 Auditing Report: Las Vegas Group Corporation Analysis

VerifiedAdded on 2022/10/17

|23

|5235

|14

Report

AI Summary

This comprehensive auditing report analyzes the financial statements of Las Vegas Group Corporation (USA) Limited, conducted by DisneyLand Audit Company Limited. The report covers various aspects of the audit process, including adherence to ethical standards (APES 110), quality control (ASA 220), audit documentation (ASA 230), and the auditor's responsibility to report misconduct (ASA 240). The report addresses key audit areas such as audit planning, risk assessment (detection, control, and inherent risk), materiality, and audit approaches for receivables, inventory, land and buildings, and overseas operations. It includes detailed analyses of materiality levels, audit procedures for verifying brand names, inventory valuation, internal control systems, debtors' balances, and payroll systems. The report also discusses the impact of economic downturns and technological advancements on the company, providing a thorough examination of the financial and operational aspects of Las Vegas Group Corporation.

Running head: AUDITING

Auditing

Name of Student:

Name of the University:

Authors’ note

Auditing

Name of Student:

Name of the University:

Authors’ note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Audit Report:..............................................................................................................................2

Answer to Question 1:................................................................................................................3

Answer to Question 2:................................................................................................................5

Answer to Question 3:..............................................................................................................10

Answer to Question 4:..............................................................................................................13

Answer to Question 5:..............................................................................................................15

References & Bibliography:.....................................................................................................18

Table of Contents

Audit Report:..............................................................................................................................2

Answer to Question 1:................................................................................................................3

Answer to Question 2:................................................................................................................5

Answer to Question 3:..............................................................................................................10

Answer to Question 4:..............................................................................................................13

Answer to Question 5:..............................................................................................................15

References & Bibliography:.....................................................................................................18

2AUDITING

Audit Report:

To the Member of Las Vegas Group Corporation

Las Vegas Group Corporation (USA)

Nevada.

According to the Apes 110 code of ethics, an auditor needs to maintain the proper ethical

manner in case of performing his audit standards. According to the provision of section 307

of corporations act, it is generally consider as the auditors duty, to present an audit report

along with the relevant accounting provisions. Such report is needed to provide all

information, explanations and true and fair views of financial statements. According to ASA

220 an auditor needs to maintain the quality control for an audit financial report. According

to the ASA 230 an auditor need to present the proper audit documentation while submitting

his audit report. As per ASA240 it is generally the auditor’s responsibility to present any

misconduct in the audit report at the end of audit procedures.

Here the company Las Vegas Group Corporation has five subsidiary companies that facing

some misstatement issues relating to the accounting transactions. While the companies

performing their accounting records they are unable to maintain some relevant accounting

policies, which is turning to the misstatements of accounting materiality.

However those accounting issues are rectified in this present report and it was also suggesting

to this company, to consider the relevant accounting standards and policies while maintain

such documents.

Thank you.

Audit Report:

To the Member of Las Vegas Group Corporation

Las Vegas Group Corporation (USA)

Nevada.

According to the Apes 110 code of ethics, an auditor needs to maintain the proper ethical

manner in case of performing his audit standards. According to the provision of section 307

of corporations act, it is generally consider as the auditors duty, to present an audit report

along with the relevant accounting provisions. Such report is needed to provide all

information, explanations and true and fair views of financial statements. According to ASA

220 an auditor needs to maintain the quality control for an audit financial report. According

to the ASA 230 an auditor need to present the proper audit documentation while submitting

his audit report. As per ASA240 it is generally the auditor’s responsibility to present any

misconduct in the audit report at the end of audit procedures.

Here the company Las Vegas Group Corporation has five subsidiary companies that facing

some misstatement issues relating to the accounting transactions. While the companies

performing their accounting records they are unable to maintain some relevant accounting

policies, which is turning to the misstatements of accounting materiality.

However those accounting issues are rectified in this present report and it was also suggesting

to this company, to consider the relevant accounting standards and policies while maintain

such documents.

Thank you.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Answer to Question 1:

A) The AU section 329 normally stated the analytical procedures regarding the audit

planning. Under the sub-section 6 of section 329, it is stated that the main purpose of

applying analytical procedure is to provide assistance in audit planning relating to the nature,

timing and extent to audit procedures, which will be used generally to obtain evidential

matters for particular account balances and transactions details. For such purpose the audit

planning is need to be focused on, enhancing the auditors’ knowledge regarding the clients’

business including the accounting transactions and events that occurred up to the date of audit

process. Along with such an auditor need to identify the key areas that may represent

particular risks relevant with the audit performances. An auditor need to follow the below

mentioned procedures as an analytical review of audit procedures;

Need to compare the present year’s financial information along with previous years’

data.

Need to compare the present financial information along with the budgeted or

forecasted reports.

Provide relevant judgements relating to the accounting growths of an organization

with the using of ratio analysis.

Comparing between financial and non-financial information.

B) Generally the audit risk is implies the risk that an auditor may not able to detect at the

time of examine the financial statements of his clients. In case of the present scenario the type

of risk relating to companies receivables accounts and inventories, that an auditor is probably

faced during his audit examination is the detection risk. The detection risk is one type of audit

risk that an auditor is unable to detect due to material misstatements.

Answer to Question 1:

A) The AU section 329 normally stated the analytical procedures regarding the audit

planning. Under the sub-section 6 of section 329, it is stated that the main purpose of

applying analytical procedure is to provide assistance in audit planning relating to the nature,

timing and extent to audit procedures, which will be used generally to obtain evidential

matters for particular account balances and transactions details. For such purpose the audit

planning is need to be focused on, enhancing the auditors’ knowledge regarding the clients’

business including the accounting transactions and events that occurred up to the date of audit

process. Along with such an auditor need to identify the key areas that may represent

particular risks relevant with the audit performances. An auditor need to follow the below

mentioned procedures as an analytical review of audit procedures;

Need to compare the present year’s financial information along with previous years’

data.

Need to compare the present financial information along with the budgeted or

forecasted reports.

Provide relevant judgements relating to the accounting growths of an organization

with the using of ratio analysis.

Comparing between financial and non-financial information.

B) Generally the audit risk is implies the risk that an auditor may not able to detect at the

time of examine the financial statements of his clients. In case of the present scenario the type

of risk relating to companies receivables accounts and inventories, that an auditor is probably

faced during his audit examination is the detection risk. The detection risk is one type of audit

risk that an auditor is unable to detect due to material misstatements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

C) In an audit procedures, generally three different types of risks are exists. Excluding

the detection risk, two others audit risks are control risk- relating to material misstatements,

which are not be prevented using the client’s controlling system. And the other one is

Inherent risk- such risks are normally susceptible due to the reason of material misstatements

that occurred during the transactions’ recording.

D) According to ISA 320, the concept of materiality is used in both the planning and

performing the audit function. As per the Para 10, the planning materiality is generally set

before the commencement of detailed testing of accounts. In case of any misstatements

relating to accounting information is revealed at the time of onset the audit procedure,

therefore an auditor is needed to implement lower level of materiality. As per the Para 9, the

auditor need to implement performance materiality in case to examine the complete financial

statements and for such propose an auditor need to maintain the higher level of materiality.

Followed the provision of auditing generally in case of set up the levels of materiality,

generally 5%-10% is consider as material level and below 5% is consider as immaterial and

required proper judgements.

E) MEMORANDUM

To: The Partners.

From:

Cc:

Subject: Audit approaches on behalf of Receivables, Inventory and Land and

Buildings.

Date: 25th September 2019.

This memorandum is particularly based on the concept of audit approach for different

accounting components. Those components are the receivables, Inventories and the land and

C) In an audit procedures, generally three different types of risks are exists. Excluding

the detection risk, two others audit risks are control risk- relating to material misstatements,

which are not be prevented using the client’s controlling system. And the other one is

Inherent risk- such risks are normally susceptible due to the reason of material misstatements

that occurred during the transactions’ recording.

D) According to ISA 320, the concept of materiality is used in both the planning and

performing the audit function. As per the Para 10, the planning materiality is generally set

before the commencement of detailed testing of accounts. In case of any misstatements

relating to accounting information is revealed at the time of onset the audit procedure,

therefore an auditor is needed to implement lower level of materiality. As per the Para 9, the

auditor need to implement performance materiality in case to examine the complete financial

statements and for such propose an auditor need to maintain the higher level of materiality.

Followed the provision of auditing generally in case of set up the levels of materiality,

generally 5%-10% is consider as material level and below 5% is consider as immaterial and

required proper judgements.

E) MEMORANDUM

To: The Partners.

From:

Cc:

Subject: Audit approaches on behalf of Receivables, Inventory and Land and

Buildings.

Date: 25th September 2019.

This memorandum is particularly based on the concept of audit approach for different

accounting components. Those components are the receivables, Inventories and the land and

5AUDITING

building of the company. An audit approach is normally known as the strategy, which is used

by an auditor to conduct an audit programme.

The Company’s 80% of customers are international customer and most of the

transactions are exchanged in foreign currency. Generally, the company is allowing 60days

credit period for individual customers. In case to evaluate the collected amount an auditor

needs to implement some approaches like check general ledger, calculate the receivable total

amount, check the collection details etc.

The company usually followed the standard costing system in case to compute the

value of inventory and the raw materials are normally valued at invoice price. For such

purpose the auditor need to check the invoice details properly.

According to the provision of AASB 116, the company is required to follow the fair

value system in case of compute the value of land and building or any other tangible assets.

For such purpose an auditor needs to check the current fair value of the assets and also need

to check the amount of depreciation and any amortisations losses, if occurred.

It can be concluded from the above discussion that an auditor with the use of

following audit approaches can evaluate the individual prices of receivables, inventories and

Land & Buildings.

building of the company. An audit approach is normally known as the strategy, which is used

by an auditor to conduct an audit programme.

The Company’s 80% of customers are international customer and most of the

transactions are exchanged in foreign currency. Generally, the company is allowing 60days

credit period for individual customers. In case to evaluate the collected amount an auditor

needs to implement some approaches like check general ledger, calculate the receivable total

amount, check the collection details etc.

The company usually followed the standard costing system in case to compute the

value of inventory and the raw materials are normally valued at invoice price. For such

purpose the auditor need to check the invoice details properly.

According to the provision of AASB 116, the company is required to follow the fair

value system in case of compute the value of land and building or any other tangible assets.

For such purpose an auditor needs to check the current fair value of the assets and also need

to check the amount of depreciation and any amortisations losses, if occurred.

It can be concluded from the above discussion that an auditor with the use of

following audit approaches can evaluate the individual prices of receivables, inventories and

Land & Buildings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

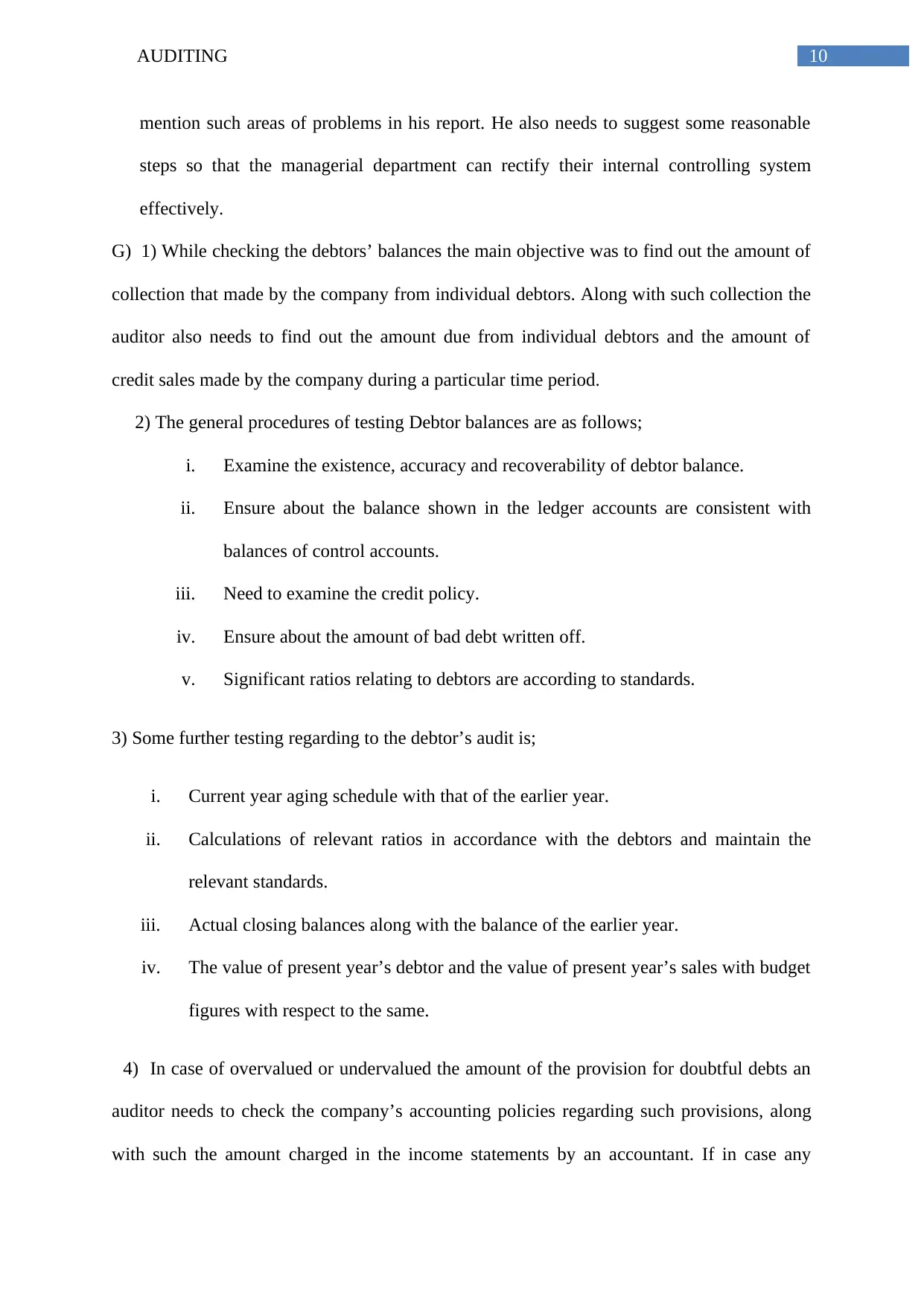

Answer to Question 2:

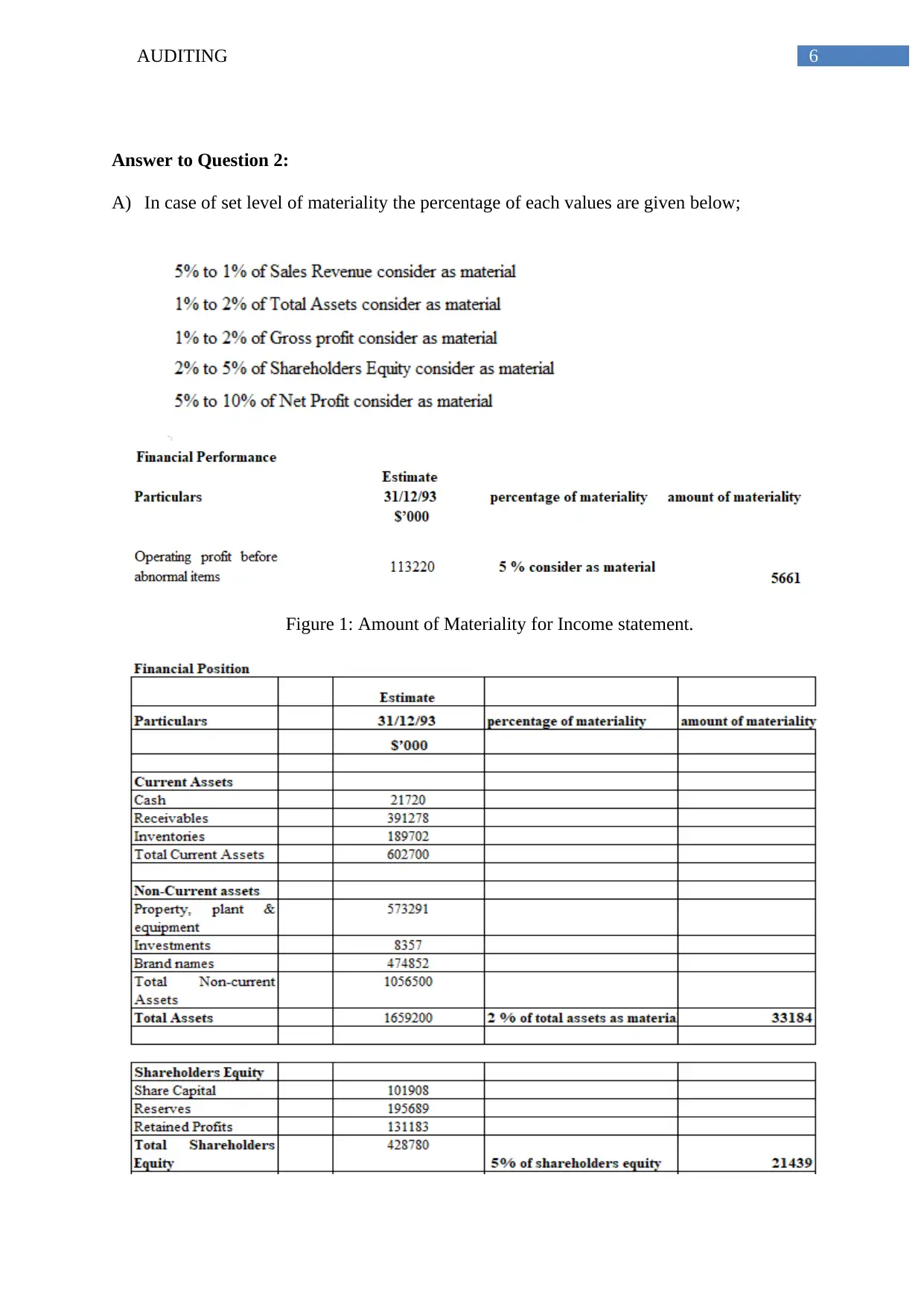

A) In case of set level of materiality the percentage of each values are given below;

Figure 1: Amount of Materiality for Income statement.

Answer to Question 2:

A) In case of set level of materiality the percentage of each values are given below;

Figure 1: Amount of Materiality for Income statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

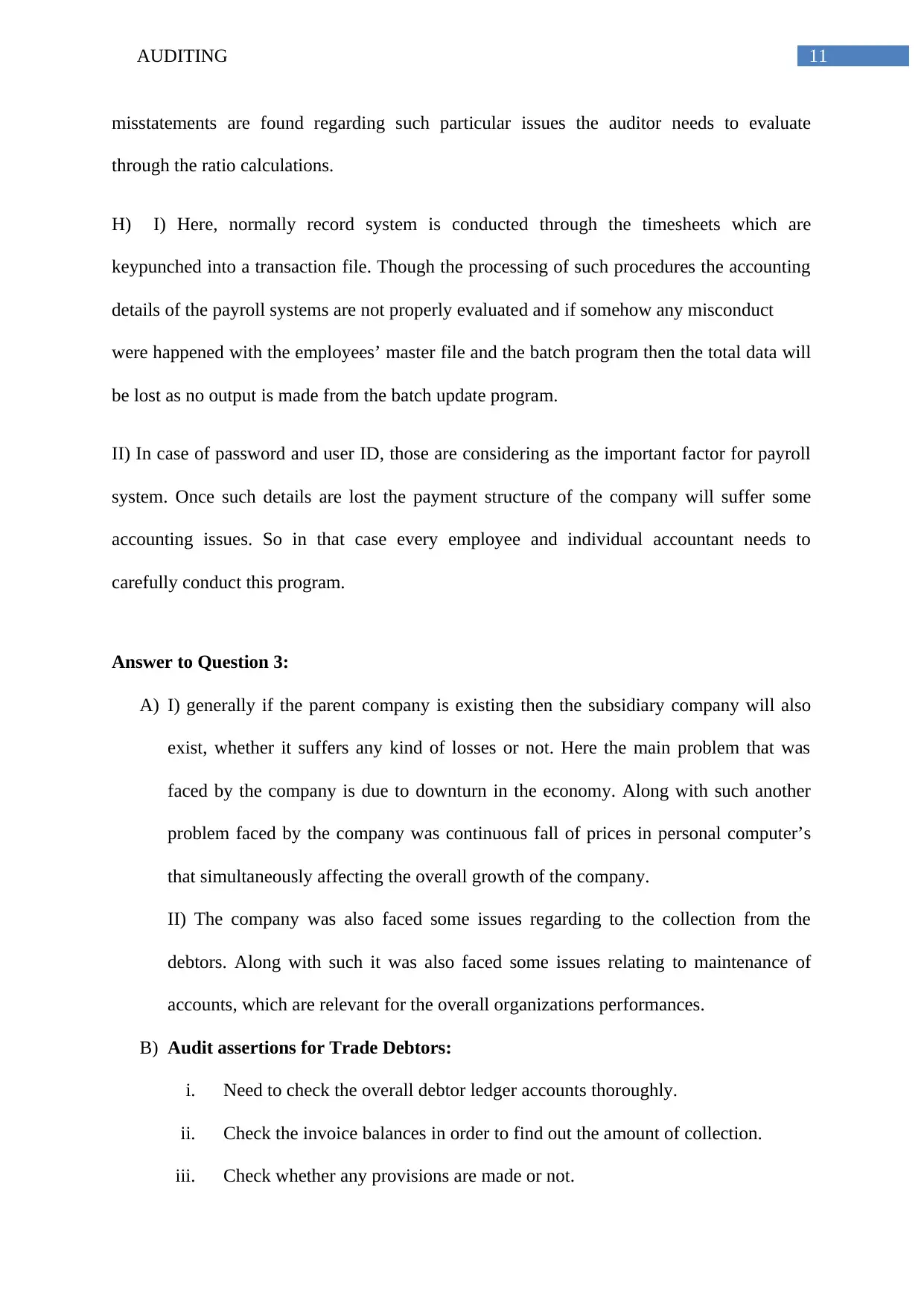

Figure 2: Amount of Materiality for Balance sheet.

Figure 2: Amount of Materiality for Balance sheet.

8AUDITING

B) MEMORANDUM

To: The Audit Partners.

From:

Cc:

Subject: Detailing the procedures required regarding the overseas operations.

Date: 25th September 2019.

This memorandum is particularly based on the concept of audit procedures required regarding

the overseas operations. The company is engaged in overseas operation since 1992. In 1992

the company accounted 15% of group turnover and 10% of gross profit through the overseas

operations.

For the purpose of such overseas operation, the auditors need to check all the relevant

accounting details of purchasing and sales account thoroughly. An auditor needs to follow

such procedure for audit the overseas operations. Those procedures are; review the internal

controls over this area including authorisation level for making the sale, if the assets are sold

through an agent, examine corresponding details, check the amount received with reference

to copy of receipts issued, examine the reasonable price through an auditor and ensure that

the sale proceeds have been fully accounted for.

It can be concluded from the above discussion that an auditor can implement such audit

procedure in case to examine the overseas operations.

C) The audit procedure for verifying the Brand name:

In case of brand name the auditor needs to examine the certificate of registration.

If the brand names are purchased then the agreement with the seller need to verify.

Need to examine the copy of receipts with respect to renewal payment made.

B) MEMORANDUM

To: The Audit Partners.

From:

Cc:

Subject: Detailing the procedures required regarding the overseas operations.

Date: 25th September 2019.

This memorandum is particularly based on the concept of audit procedures required regarding

the overseas operations. The company is engaged in overseas operation since 1992. In 1992

the company accounted 15% of group turnover and 10% of gross profit through the overseas

operations.

For the purpose of such overseas operation, the auditors need to check all the relevant

accounting details of purchasing and sales account thoroughly. An auditor needs to follow

such procedure for audit the overseas operations. Those procedures are; review the internal

controls over this area including authorisation level for making the sale, if the assets are sold

through an agent, examine corresponding details, check the amount received with reference

to copy of receipts issued, examine the reasonable price through an auditor and ensure that

the sale proceeds have been fully accounted for.

It can be concluded from the above discussion that an auditor can implement such audit

procedure in case to examine the overseas operations.

C) The audit procedure for verifying the Brand name:

In case of brand name the auditor needs to examine the certificate of registration.

If the brand names are purchased then the agreement with the seller need to verify.

Need to examine the copy of receipts with respect to renewal payment made.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

Need to show the value of such brand name in the balance sheet at their cost less

amortization charges.

D) For the purpose of issued a qualified audit report, the amortization process is need to

follow for the value of intangible assets. Normally the cost of an intangible assets is

amortized over a particular number of years, regardless the actual useful life of such

assets. In case to present the fair value of an intangible asset the amortization charges are

need to deduct from the cost of such assets.

E) Audit strategy for Inventory valuation: The Company is generally charged the average

costing method for the purpose of valuation of inventories. In case to audit the value of

such inventories an auditor need to check;

Invoice list of each inventories.

Present market value of such inventory.

Examine the store ledger account properly.

Examine the amount paid for purchasing such inventories.

Enquiry about the charges on Inventory.

F) 1) While checking the internal control system it was found that some accounting

transactions are not recorded properly. Those transactions are mandatory to records in

case to evaluate the overall performance of the company. However the overall internal

control system is good for the company; regarding the records of abnormal items, stock

valuations etc. So, in that case if any small changes in internal controlling system can be

rectify the overall systems.

2) However, if the managerial department was already issued a letter regarding the

problem of internal controlling system and the organizations does not rectify the problem

yet, therefore as an auditor while reporting on behalf of his performance must needs to

Need to show the value of such brand name in the balance sheet at their cost less

amortization charges.

D) For the purpose of issued a qualified audit report, the amortization process is need to

follow for the value of intangible assets. Normally the cost of an intangible assets is

amortized over a particular number of years, regardless the actual useful life of such

assets. In case to present the fair value of an intangible asset the amortization charges are

need to deduct from the cost of such assets.

E) Audit strategy for Inventory valuation: The Company is generally charged the average

costing method for the purpose of valuation of inventories. In case to audit the value of

such inventories an auditor need to check;

Invoice list of each inventories.

Present market value of such inventory.

Examine the store ledger account properly.

Examine the amount paid for purchasing such inventories.

Enquiry about the charges on Inventory.

F) 1) While checking the internal control system it was found that some accounting

transactions are not recorded properly. Those transactions are mandatory to records in

case to evaluate the overall performance of the company. However the overall internal

control system is good for the company; regarding the records of abnormal items, stock

valuations etc. So, in that case if any small changes in internal controlling system can be

rectify the overall systems.

2) However, if the managerial department was already issued a letter regarding the

problem of internal controlling system and the organizations does not rectify the problem

yet, therefore as an auditor while reporting on behalf of his performance must needs to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

mention such areas of problems in his report. He also needs to suggest some reasonable

steps so that the managerial department can rectify their internal controlling system

effectively.

G) 1) While checking the debtors’ balances the main objective was to find out the amount of

collection that made by the company from individual debtors. Along with such collection the

auditor also needs to find out the amount due from individual debtors and the amount of

credit sales made by the company during a particular time period.

2) The general procedures of testing Debtor balances are as follows;

i. Examine the existence, accuracy and recoverability of debtor balance.

ii. Ensure about the balance shown in the ledger accounts are consistent with

balances of control accounts.

iii. Need to examine the credit policy.

iv. Ensure about the amount of bad debt written off.

v. Significant ratios relating to debtors are according to standards.

3) Some further testing regarding to the debtor’s audit is;

i. Current year aging schedule with that of the earlier year.

ii. Calculations of relevant ratios in accordance with the debtors and maintain the

relevant standards.

iii. Actual closing balances along with the balance of the earlier year.

iv. The value of present year’s debtor and the value of present year’s sales with budget

figures with respect to the same.

4) In case of overvalued or undervalued the amount of the provision for doubtful debts an

auditor needs to check the company’s accounting policies regarding such provisions, along

with such the amount charged in the income statements by an accountant. If in case any

mention such areas of problems in his report. He also needs to suggest some reasonable

steps so that the managerial department can rectify their internal controlling system

effectively.

G) 1) While checking the debtors’ balances the main objective was to find out the amount of

collection that made by the company from individual debtors. Along with such collection the

auditor also needs to find out the amount due from individual debtors and the amount of

credit sales made by the company during a particular time period.

2) The general procedures of testing Debtor balances are as follows;

i. Examine the existence, accuracy and recoverability of debtor balance.

ii. Ensure about the balance shown in the ledger accounts are consistent with

balances of control accounts.

iii. Need to examine the credit policy.

iv. Ensure about the amount of bad debt written off.

v. Significant ratios relating to debtors are according to standards.

3) Some further testing regarding to the debtor’s audit is;

i. Current year aging schedule with that of the earlier year.

ii. Calculations of relevant ratios in accordance with the debtors and maintain the

relevant standards.

iii. Actual closing balances along with the balance of the earlier year.

iv. The value of present year’s debtor and the value of present year’s sales with budget

figures with respect to the same.

4) In case of overvalued or undervalued the amount of the provision for doubtful debts an

auditor needs to check the company’s accounting policies regarding such provisions, along

with such the amount charged in the income statements by an accountant. If in case any

11AUDITING

misstatements are found regarding such particular issues the auditor needs to evaluate

through the ratio calculations.

H) I) Here, normally record system is conducted through the timesheets which are

keypunched into a transaction file. Though the processing of such procedures the accounting

details of the payroll systems are not properly evaluated and if somehow any misconduct

were happened with the employees’ master file and the batch program then the total data will

be lost as no output is made from the batch update program.

II) In case of password and user ID, those are considering as the important factor for payroll

system. Once such details are lost the payment structure of the company will suffer some

accounting issues. So in that case every employee and individual accountant needs to

carefully conduct this program.

Answer to Question 3:

A) I) generally if the parent company is existing then the subsidiary company will also

exist, whether it suffers any kind of losses or not. Here the main problem that was

faced by the company is due to downturn in the economy. Along with such another

problem faced by the company was continuous fall of prices in personal computer’s

that simultaneously affecting the overall growth of the company.

II) The company was also faced some issues regarding to the collection from the

debtors. Along with such it was also faced some issues relating to maintenance of

accounts, which are relevant for the overall organizations performances.

B) Audit assertions for Trade Debtors:

i. Need to check the overall debtor ledger accounts thoroughly.

ii. Check the invoice balances in order to find out the amount of collection.

iii. Check whether any provisions are made or not.

misstatements are found regarding such particular issues the auditor needs to evaluate

through the ratio calculations.

H) I) Here, normally record system is conducted through the timesheets which are

keypunched into a transaction file. Though the processing of such procedures the accounting

details of the payroll systems are not properly evaluated and if somehow any misconduct

were happened with the employees’ master file and the batch program then the total data will

be lost as no output is made from the batch update program.

II) In case of password and user ID, those are considering as the important factor for payroll

system. Once such details are lost the payment structure of the company will suffer some

accounting issues. So in that case every employee and individual accountant needs to

carefully conduct this program.

Answer to Question 3:

A) I) generally if the parent company is existing then the subsidiary company will also

exist, whether it suffers any kind of losses or not. Here the main problem that was

faced by the company is due to downturn in the economy. Along with such another

problem faced by the company was continuous fall of prices in personal computer’s

that simultaneously affecting the overall growth of the company.

II) The company was also faced some issues regarding to the collection from the

debtors. Along with such it was also faced some issues relating to maintenance of

accounts, which are relevant for the overall organizations performances.

B) Audit assertions for Trade Debtors:

i. Need to check the overall debtor ledger accounts thoroughly.

ii. Check the invoice balances in order to find out the amount of collection.

iii. Check whether any provisions are made or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.