Taxation Law Case Study: Applying ITAA and Providing Client Advice

VerifiedAdded on 2022/12/23

|12

|2811

|73

Case Study

AI Summary

This case study delves into various aspects of Australian taxation law, addressing questions related to constitutional powers, the roles of the government and the ATO, and the tax implications of business profits and capital gains. It analyzes scenarios involving property sales, post-cessation expenditure, and the application of Capital Gains Tax (CGT) rules. The assignment also examines two articles from the Australian Financial Review concerning ATO measures on home office expenses and the removal of refundable franking credits, linking these concepts to good tax policy. Furthermore, the case study explores the legal principles and precedents relevant to each scenario, offering detailed explanations and providing recommendations to the client based on the interpretation of relevant legislation and case law. The document provides a comprehensive analysis of the tax implications for various business and personal financial situations, including capital gains and losses.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO measures on crackdown on home office expenses claims:...............................7

Article 2: ATO measures of removing “inequitable” inquiry:...................................................8

Answer to question 7:.................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO measures on crackdown on home office expenses claims:...............................7

Article 2: ATO measures of removing “inequitable” inquiry:...................................................8

Answer to question 7:.................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer to A:

Denoting the explanation that is given under the “Section 51 (ii)” the constitution

possess the power to make laws in Australia. Referring to the “Section 51 (ii)” the powers of

the commonwealth include the making of laws related to the tax but does not accounts

making any kind of discrimination between the state as well as country (Bankman et al.,

2018). Furthermore, the commonwealth with respect to the “Section 51 (ii)” has the authority

of imposing tax that is conferred under this legislation and has the power of framing

constitutional laws.

Answer to B:

The government of Australia is responsible for delivering an overall improvement in

the taxation policy and minister of treasury is responsible for practically implementing the

laws. The responsibility of the ATO remains in creation of tax policies and judicial procedure

which explains that the relation between the laws and administrative aspects of taxation

system (Schmalbeck et al., 2015). The ATO is responsible for managing the laws that relates

to the superannuation and tax which the parliament passes. In order to implement the laws,

the government levies taxes that are created by ATO and also includes the valued advice to

taxpayers relating to the duties and accountabilities.

Answer to question 2:

The business profits of the enterprise relating to the contracting country will only be

liable for taxation in that country except when the company is performing the business in the

another contracting country with the help of permanent establishment located therein. If the

company is carrying on the business as mentioned above, then the profits of the company

may be considered taxable in the other country but only to the extent that majority of the

Answer to question 1:

Answer to A:

Denoting the explanation that is given under the “Section 51 (ii)” the constitution

possess the power to make laws in Australia. Referring to the “Section 51 (ii)” the powers of

the commonwealth include the making of laws related to the tax but does not accounts

making any kind of discrimination between the state as well as country (Bankman et al.,

2018). Furthermore, the commonwealth with respect to the “Section 51 (ii)” has the authority

of imposing tax that is conferred under this legislation and has the power of framing

constitutional laws.

Answer to B:

The government of Australia is responsible for delivering an overall improvement in

the taxation policy and minister of treasury is responsible for practically implementing the

laws. The responsibility of the ATO remains in creation of tax policies and judicial procedure

which explains that the relation between the laws and administrative aspects of taxation

system (Schmalbeck et al., 2015). The ATO is responsible for managing the laws that relates

to the superannuation and tax which the parliament passes. In order to implement the laws,

the government levies taxes that are created by ATO and also includes the valued advice to

taxpayers relating to the duties and accountabilities.

Answer to question 2:

The business profits of the enterprise relating to the contracting country will only be

liable for taxation in that country except when the company is performing the business in the

another contracting country with the help of permanent establishment located therein. If the

company is carrying on the business as mentioned above, then the profits of the company

may be considered taxable in the other country but only to the extent that majority of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

profits is attributable to that permanent establishment (Brownlee, 2016). A company is only

considered as the Australian resident company if the company is incorporated in Australia,

irrespective of whether the company performs the business in overseas, administered in

overseas or a control is imposed by the foreign shareholders. The decision handed by the

court in “Malayan Shipping Company Ltd v FCT (1946)” held that the company is

performing the business in Australia because the central management and control was in

Australia.

In light of the above stated decision it can be stated that the profits derived by the US

based manufacturing company from the sales made to the Australian customers will be held

taxable in Australia. This is because the business profits are generated here in Australia since

the transaction has the source in Australia.

Answer to question 3:

Part 1:

Answer to A:

As defined in “Section 102-5, ITAA 1997” the taxpayers are required to include in

their taxable income the net value of capital gains made (Schenk, 2017). Taxpayers should

disregard the capital loss and they are only permitted to claim offset against the capital gains

which is not allowed for deduction and the net loss should be carried to subsequent years. If

Indiana subdivides the land and sells the same then the profits that is made from the sale will

be included for taxable purpose. Nevertheless, if the property is purchased by Indiana earlier

to the introduction of CGT regime than the capital gains from sale is exempted from tax

because it amounts to pre-CGT.

profits is attributable to that permanent establishment (Brownlee, 2016). A company is only

considered as the Australian resident company if the company is incorporated in Australia,

irrespective of whether the company performs the business in overseas, administered in

overseas or a control is imposed by the foreign shareholders. The decision handed by the

court in “Malayan Shipping Company Ltd v FCT (1946)” held that the company is

performing the business in Australia because the central management and control was in

Australia.

In light of the above stated decision it can be stated that the profits derived by the US

based manufacturing company from the sales made to the Australian customers will be held

taxable in Australia. This is because the business profits are generated here in Australia since

the transaction has the source in Australia.

Answer to question 3:

Part 1:

Answer to A:

As defined in “Section 102-5, ITAA 1997” the taxpayers are required to include in

their taxable income the net value of capital gains made (Schenk, 2017). Taxpayers should

disregard the capital loss and they are only permitted to claim offset against the capital gains

which is not allowed for deduction and the net loss should be carried to subsequent years. If

Indiana subdivides the land and sells the same then the profits that is made from the sale will

be included for taxable purpose. Nevertheless, if the property is purchased by Indiana earlier

to the introduction of CGT regime than the capital gains from sale is exempted from tax

because it amounts to pre-CGT.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to B:

First Option: If Indiana buys the property in 1986 and then sells the land to developer

of property, the revenue provision must be considered in this option. The land will not be

treated as trading stock and any gains made will be attract tax liability under the ordinary

concept of “section 6-5, ITAA 1997”.

Second Option: If she decides to sell the land to the highest bidder then the

subdivided 80 blocks of land will be treated as trading stock. Under the “section 6-5, ITAA

1997” the capital gains will be taxable as ordinary income from profit making scheme (Liu &

Williams, 2019).

Third Option: Under the third option, if Indiana decides against the subdivision of

land and selling to the real estate developer then any amount of capital gains which will be

earned following the sale of land will be regarded as the taxable capital gains. The gains are

taxable under the ordinary sense of income and the profits obtained will also be subjected to

GST.

Answer to part 2:

Option A:

Where the subdivision of land gives rise to simple realisation of the capital asset by

Indiana then the capital gains which is made by Indiana would amount to gain beneficially

obtained from the land development. The sale of subdivided land will be considered as

revenue asset and under the “section 6-5, ITAA 1997” the capital gains will be taxable as

ordinary income (Kaeding, 2016).

Option B:

Answer to B:

First Option: If Indiana buys the property in 1986 and then sells the land to developer

of property, the revenue provision must be considered in this option. The land will not be

treated as trading stock and any gains made will be attract tax liability under the ordinary

concept of “section 6-5, ITAA 1997”.

Second Option: If she decides to sell the land to the highest bidder then the

subdivided 80 blocks of land will be treated as trading stock. Under the “section 6-5, ITAA

1997” the capital gains will be taxable as ordinary income from profit making scheme (Liu &

Williams, 2019).

Third Option: Under the third option, if Indiana decides against the subdivision of

land and selling to the real estate developer then any amount of capital gains which will be

earned following the sale of land will be regarded as the taxable capital gains. The gains are

taxable under the ordinary sense of income and the profits obtained will also be subjected to

GST.

Answer to part 2:

Option A:

Where the subdivision of land gives rise to simple realisation of the capital asset by

Indiana then the capital gains which is made by Indiana would amount to gain beneficially

obtained from the land development. The sale of subdivided land will be considered as

revenue asset and under the “section 6-5, ITAA 1997” the capital gains will be taxable as

ordinary income (Kaeding, 2016).

Option B:

5TAXATION LAW

If Indiana decides to conduct auction on 80 block of subdivided land and those blocks

of land will be counted as trading stock beginning from when the process of subdivision

commenced. It is presumed that the land that is subdivided by Indiana is sold at the current

market value. Indiana in such situation will be treated for assessment purpose because she

undertook the commercial method of disposing the land for obtaining the profit. Therefore,

the capital gains which is made upon the sale of land is an income in accordance with the

ordinary meaning of “section 6-5, ITAA 1997”.

Option C:

Indiana in the final option simply takes the decision of dividing the land and selling

the several plots of land to the real estate property development then the capital gains would

represent that Indiana is carrying the business of land development and the profits will be

considered for tax purpose under “section 25 (1), ITAA 1936”.

Answer to question 4:

Post-cessation expenditure is permitted as allowable deduction provided that the event

of loss or the outgoing is recognized in the operation of business which the taxpayers have

previously carried on with the ultimate objective of deriving taxable income (Maley &

Maley, 2018). Post-cessation expenditure are permitted for deduction given the event of

business function is found to be directed towards gaining or producing the assessable income.

The court of law in “Placer Pacific Management Pty Ltd v FCT (1995)” found that the

event of expenditure was in the business operation which was in the direction of producing

assessable income and does not matter the outgoing was a year later when the business was

ceased (Burman et al., 2016). The taxation commissioner permitted the taxpayer with

deduction for outgoings for the business arrangement that was entered among the customer

and taxpayer for the supply of conveyor belt.

If Indiana decides to conduct auction on 80 block of subdivided land and those blocks

of land will be counted as trading stock beginning from when the process of subdivision

commenced. It is presumed that the land that is subdivided by Indiana is sold at the current

market value. Indiana in such situation will be treated for assessment purpose because she

undertook the commercial method of disposing the land for obtaining the profit. Therefore,

the capital gains which is made upon the sale of land is an income in accordance with the

ordinary meaning of “section 6-5, ITAA 1997”.

Option C:

Indiana in the final option simply takes the decision of dividing the land and selling

the several plots of land to the real estate property development then the capital gains would

represent that Indiana is carrying the business of land development and the profits will be

considered for tax purpose under “section 25 (1), ITAA 1936”.

Answer to question 4:

Post-cessation expenditure is permitted as allowable deduction provided that the event

of loss or the outgoing is recognized in the operation of business which the taxpayers have

previously carried on with the ultimate objective of deriving taxable income (Maley &

Maley, 2018). Post-cessation expenditure are permitted for deduction given the event of

business function is found to be directed towards gaining or producing the assessable income.

The court of law in “Placer Pacific Management Pty Ltd v FCT (1995)” found that the

event of expenditure was in the business operation which was in the direction of producing

assessable income and does not matter the outgoing was a year later when the business was

ceased (Burman et al., 2016). The taxation commissioner permitted the taxpayer with

deduction for outgoings for the business arrangement that was entered among the customer

and taxpayer for the supply of conveyor belt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

In the current case Amity here incurred interest on loan for developing the

accommodation business over the three year period. Citing the case of “Placer Pacific

Management Pty Ltd v FCT (1995)” the expenses can be found to have occurred during the

business operation that was directed towards the derivation of income (Wanless, 2018). As a

result, Amity can claim the deduction for the interest on loan since the occasion of outgoing

was for the business arrangement that was entered between Amity and her partner Archie.

Answer to question 5:

Capital gains tax is only applied on the assets that are purchased after 20th September

1985. While the capital loss can only be offset against the capital gains or can be deducted or

carry forward to subsequent years (Liesegang & Runkel, 2018). The ATO states that the

taxpayers are usually not required to pay the CGT for their main residence that used for

dwelling purpose. However, the taxpayers are not permitted full exemption when the house

was used for producing income. Maurice bought the house on 20th February 1989 for

$140,000 and was solely used for dwelling purpose. The capital gains made by Maurice from

the sale of home is exempted from CGT because the home was never used for running

business or producing income (Mitu & Stanciu, 2018). Maurice sold the FUL shares on 15th

March 2018 for $19,000. The shares were initially bought on 10th April 1984. As the shares

were purchased before the introduction of CGT regime, the capital gains made thereof is

disregarded in case of Maurice.

Rendering to “section 108-20 (2), ITAA 1997” personal use assets means those assets

that are bought by taxpayer for their personal use and enjoyment (Feher & Jousten, 2018).

Under section 118-10 (3), ITAA 1997 the taxpayers should disregard the capital gains where

the asset cost is less than $10,000. The furniture that was bought by Maurice is below the

prescribed cost limit of $10,000. The capital losses derived from the sale is disregarded under

the section 108-20 (1), ITAA 1997.

In the current case Amity here incurred interest on loan for developing the

accommodation business over the three year period. Citing the case of “Placer Pacific

Management Pty Ltd v FCT (1995)” the expenses can be found to have occurred during the

business operation that was directed towards the derivation of income (Wanless, 2018). As a

result, Amity can claim the deduction for the interest on loan since the occasion of outgoing

was for the business arrangement that was entered between Amity and her partner Archie.

Answer to question 5:

Capital gains tax is only applied on the assets that are purchased after 20th September

1985. While the capital loss can only be offset against the capital gains or can be deducted or

carry forward to subsequent years (Liesegang & Runkel, 2018). The ATO states that the

taxpayers are usually not required to pay the CGT for their main residence that used for

dwelling purpose. However, the taxpayers are not permitted full exemption when the house

was used for producing income. Maurice bought the house on 20th February 1989 for

$140,000 and was solely used for dwelling purpose. The capital gains made by Maurice from

the sale of home is exempted from CGT because the home was never used for running

business or producing income (Mitu & Stanciu, 2018). Maurice sold the FUL shares on 15th

March 2018 for $19,000. The shares were initially bought on 10th April 1984. As the shares

were purchased before the introduction of CGT regime, the capital gains made thereof is

disregarded in case of Maurice.

Rendering to “section 108-20 (2), ITAA 1997” personal use assets means those assets

that are bought by taxpayer for their personal use and enjoyment (Feher & Jousten, 2018).

Under section 118-10 (3), ITAA 1997 the taxpayers should disregard the capital gains where

the asset cost is less than $10,000. The furniture that was bought by Maurice is below the

prescribed cost limit of $10,000. The capital losses derived from the sale is disregarded under

the section 108-20 (1), ITAA 1997.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

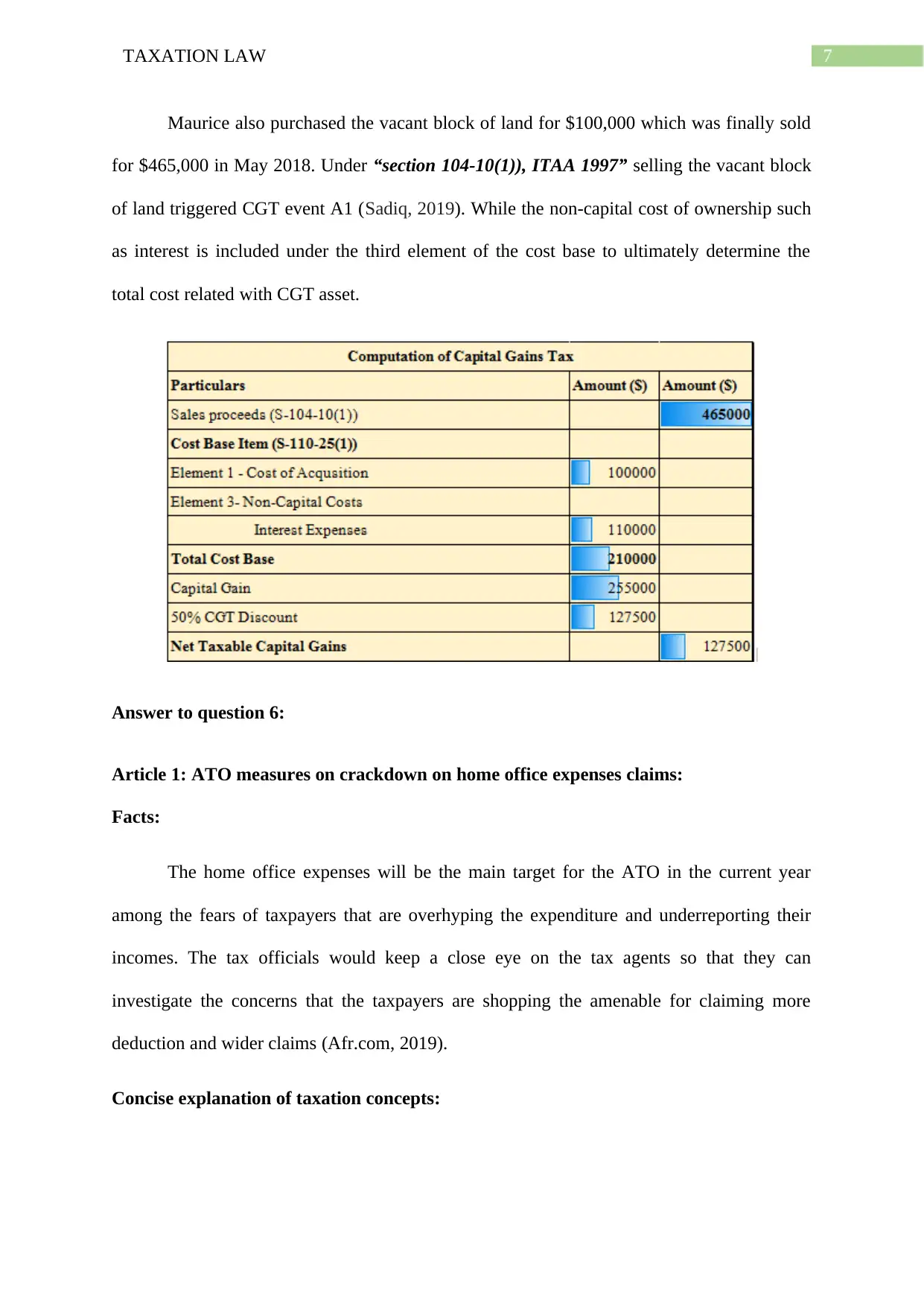

Maurice also purchased the vacant block of land for $100,000 which was finally sold

for $465,000 in May 2018. Under “section 104-10(1)), ITAA 1997” selling the vacant block

of land triggered CGT event A1 (Sadiq, 2019). While the non-capital cost of ownership such

as interest is included under the third element of the cost base to ultimately determine the

total cost related with CGT asset.

Answer to question 6:

Article 1: ATO measures on crackdown on home office expenses claims:

Facts:

The home office expenses will be the main target for the ATO in the current year

among the fears of taxpayers that are overhyping the expenditure and underreporting their

incomes. The tax officials would keep a close eye on the tax agents so that they can

investigate the concerns that the taxpayers are shopping the amenable for claiming more

deduction and wider claims (Afr.com, 2019).

Concise explanation of taxation concepts:

Maurice also purchased the vacant block of land for $100,000 which was finally sold

for $465,000 in May 2018. Under “section 104-10(1)), ITAA 1997” selling the vacant block

of land triggered CGT event A1 (Sadiq, 2019). While the non-capital cost of ownership such

as interest is included under the third element of the cost base to ultimately determine the

total cost related with CGT asset.

Answer to question 6:

Article 1: ATO measures on crackdown on home office expenses claims:

Facts:

The home office expenses will be the main target for the ATO in the current year

among the fears of taxpayers that are overhyping the expenditure and underreporting their

incomes. The tax officials would keep a close eye on the tax agents so that they can

investigate the concerns that the taxpayers are shopping the amenable for claiming more

deduction and wider claims (Afr.com, 2019).

Concise explanation of taxation concepts:

8TAXATION LAW

If a taxpayer home forms the place of business and they have set up the area that are

exclusively directed towards work activities, then they will be allowed to obtain deduction for

both the running and occupancy expenditure (Afr.com, 2019). The taxpayers are required to

keep the record in a timely manner regarding their home office spending.

Explanation of connection between concepts and indicators of good tax policy:

In a bid to attain good tax policy, the ATO would continue its focus on the incorrect

claims of deductions along with the understating of income. The ATO states that around $8

billion has been claimed as home office deduction by around 6.7 million by the taxpayer in

their 2016-17 returns.

Article 2: ATO measures of removing “inequitable” inquiry:

Facts:

According to the parliamentary inquiry the policy of labour for removing the

refundable franking credit for both the individual taxpayers and SMSF is considered as

highly faulty (Afr.com, 2019). The committee following the consideration of the case

regarding the removal of franking credits for individuals and SMSF is considered as totally

inequitable and deeply flawed policy.

Concise explanation of taxation concepts:

In the enquiry that was set up by the Coalition government has submitted its reports

that has recommended against the removal of the refundable franking credits.

Description of link between concepts and indicators of good tax policy:

Abolishing the refundable franking credits would create an unfair situation which will

hit the middle income group people that have long retired and are not in the position of

coming back to work for the purpose of getting back the income which they will lose

If a taxpayer home forms the place of business and they have set up the area that are

exclusively directed towards work activities, then they will be allowed to obtain deduction for

both the running and occupancy expenditure (Afr.com, 2019). The taxpayers are required to

keep the record in a timely manner regarding their home office spending.

Explanation of connection between concepts and indicators of good tax policy:

In a bid to attain good tax policy, the ATO would continue its focus on the incorrect

claims of deductions along with the understating of income. The ATO states that around $8

billion has been claimed as home office deduction by around 6.7 million by the taxpayer in

their 2016-17 returns.

Article 2: ATO measures of removing “inequitable” inquiry:

Facts:

According to the parliamentary inquiry the policy of labour for removing the

refundable franking credit for both the individual taxpayers and SMSF is considered as

highly faulty (Afr.com, 2019). The committee following the consideration of the case

regarding the removal of franking credits for individuals and SMSF is considered as totally

inequitable and deeply flawed policy.

Concise explanation of taxation concepts:

In the enquiry that was set up by the Coalition government has submitted its reports

that has recommended against the removal of the refundable franking credits.

Description of link between concepts and indicators of good tax policy:

Abolishing the refundable franking credits would create an unfair situation which will

hit the middle income group people that have long retired and are not in the position of

coming back to work for the purpose of getting back the income which they will lose

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

(Afr.com, 2019). The report has however recommended that such kind of policy can be

considered as the portion of equal package for the complete tax reformation.

Answer to question 7:

The roles of the tax agent advisors is explained below;

a. The tax agent are accountable for making sure the clients take the informed decision

and asks the advisors to engage in the tax arrangement that does not impacts the

reputational damage.

b. The tax advisors are accountable for assisting the clients so that they can comply with

the obligations under the taxation laws and enable them to make a complete use of the

rights relating to taxation matters (Igt.gov.au, 2019).

c. The taxpayers play the vital role in enabling the client to completely respect the law.

This involves the case law, and unwritten law that recognizes the legal principles.

(Afr.com, 2019). The report has however recommended that such kind of policy can be

considered as the portion of equal package for the complete tax reformation.

Answer to question 7:

The roles of the tax agent advisors is explained below;

a. The tax agent are accountable for making sure the clients take the informed decision

and asks the advisors to engage in the tax arrangement that does not impacts the

reputational damage.

b. The tax advisors are accountable for assisting the clients so that they can comply with

the obligations under the taxation laws and enable them to make a complete use of the

rights relating to taxation matters (Igt.gov.au, 2019).

c. The taxpayers play the vital role in enabling the client to completely respect the law.

This involves the case law, and unwritten law that recognizes the legal principles.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Beware the ATO's crackdown on home office claims. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/beware-the-ato-s-crackdown-on-home-

office-claims-20190325-p517g7

Brownlee, W. E. (2016). Federal Taxation in America. Cambridge University Press.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J., & Rosenthal, S. (2016). Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), 171.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/

Feher, C., & Jousten, A. (2018). Taxation and pensions: An overview of interplay.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Kaeding, N. (2016). State individual income tax rates and brackets for 2016. The Tax

Foundation.

Liesegang, C., & Runkel, M. (2018). Tax competition and fiscal equalization under corporate

income taxation. International Tax and Public Finance, 25(2), 311-324.

Liu, C., & Williams, N. (2019). State-Level Implications of Federal Tax Policies. Journal of

Monetary Economics.

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Beware the ATO's crackdown on home office claims. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/beware-the-ato-s-crackdown-on-home-

office-claims-20190325-p517g7

Brownlee, W. E. (2016). Federal Taxation in America. Cambridge University Press.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J., & Rosenthal, S. (2016). Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), 171.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/

Feher, C., & Jousten, A. (2018). Taxation and pensions: An overview of interplay.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Kaeding, N. (2016). State individual income tax rates and brackets for 2016. The Tax

Foundation.

Liesegang, C., & Runkel, M. (2018). Tax competition and fiscal equalization under corporate

income taxation. International Tax and Public Finance, 25(2), 311-324.

Liu, C., & Williams, N. (2019). State-Level Implications of Federal Tax Policies. Journal of

Monetary Economics.

11TAXATION LAW

Maley, M. N., & Maley, D. M. (2018). Australian Taxation Office Guidance on the Diverted

Profits Tax.

Mitu, N. E., & Stanciu, C. (2018). Tax Principles between Theory, Practice and Social

Responsibility. In Current Issues in Corporate Social Responsibility (pp. 11-24).

Springer, Cham.

Sadiq, K. (2019). Australian Taxation Law Cases 2019. Thomson Reuters.

Schenk, D. H. (2017). Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Wanless, P. T. (2018). Taxation in centrally planned economies. Routledge.

Maley, M. N., & Maley, D. M. (2018). Australian Taxation Office Guidance on the Diverted

Profits Tax.

Mitu, N. E., & Stanciu, C. (2018). Tax Principles between Theory, Practice and Social

Responsibility. In Current Issues in Corporate Social Responsibility (pp. 11-24).

Springer, Cham.

Sadiq, K. (2019). Australian Taxation Law Cases 2019. Thomson Reuters.

Schenk, D. H. (2017). Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Wanless, P. T. (2018). Taxation in centrally planned economies. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.