Law Assignment: Contract, Insurance, Consumer, and Business Law

VerifiedAdded on 2020/04/15

|8

|1258

|82

Homework Assignment

AI Summary

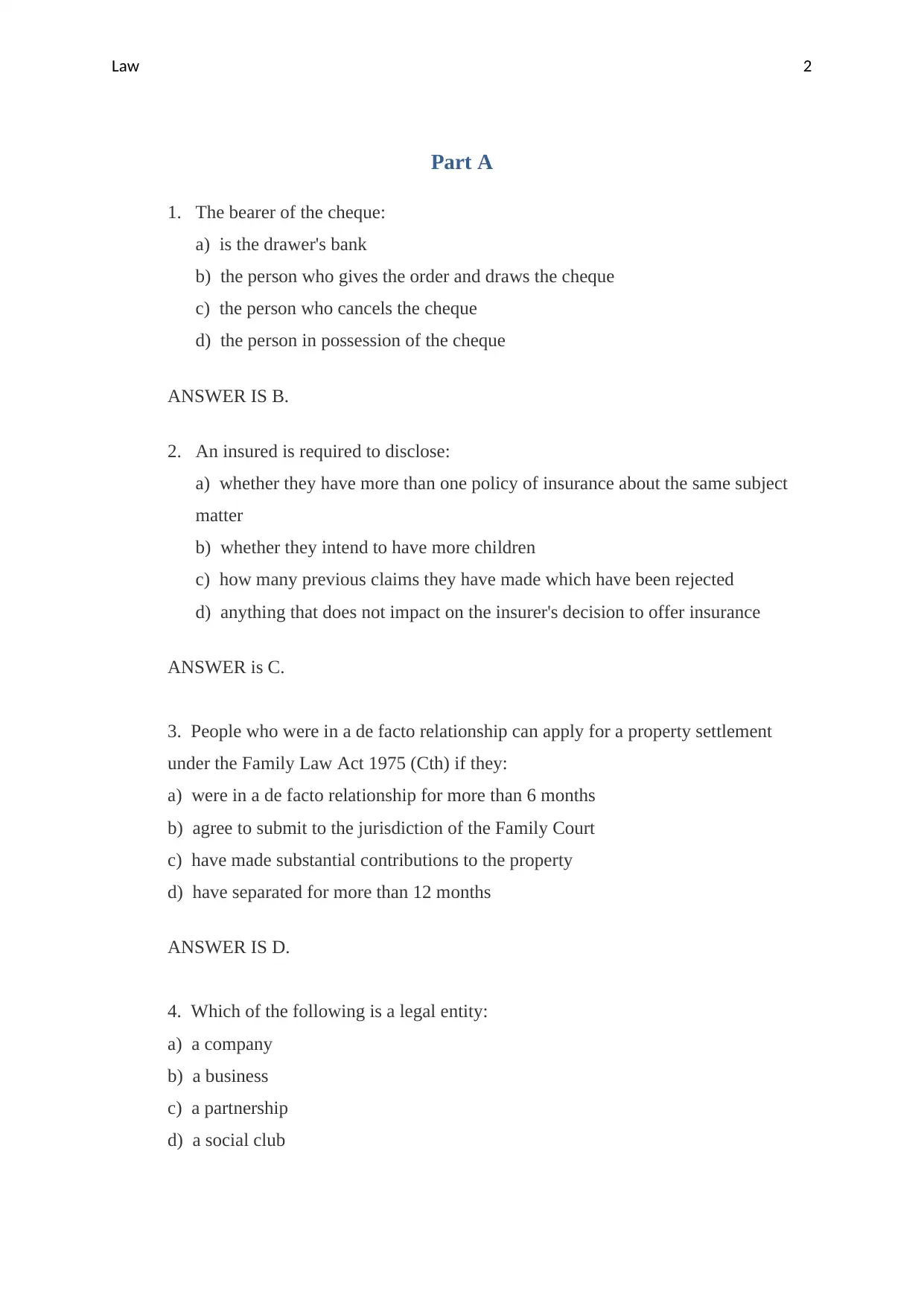

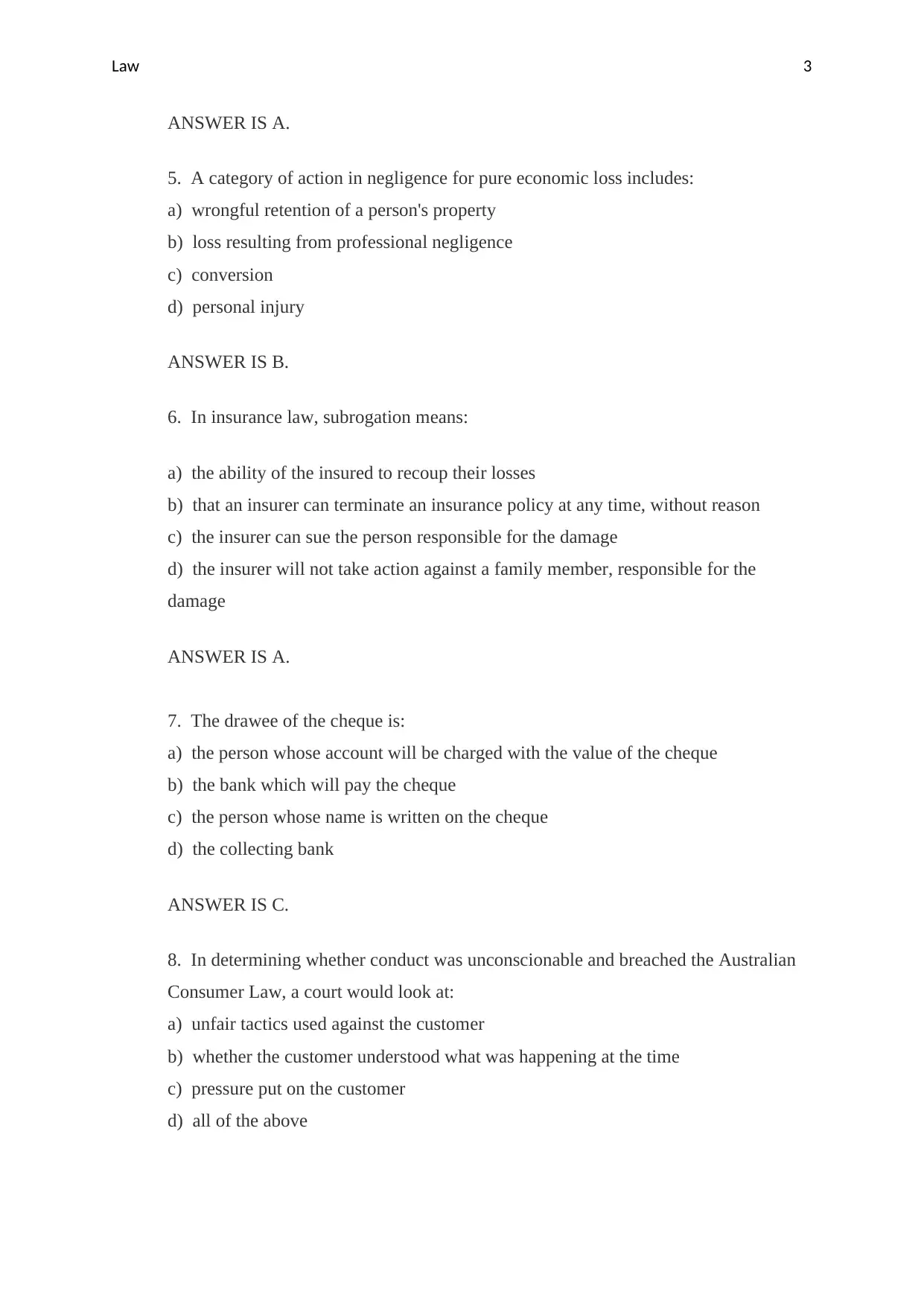

This law assignment solution addresses various aspects of law, encompassing contract, insurance, and consumer law. Part A consists of multiple-choice questions testing knowledge of legal entities, insurance, and negotiable instruments. Part B provides detailed answers to case studies, focusing on unfair contract terms, misleading conduct, and breaches of the Australian Consumer Law. The answers analyze scenarios involving retail contracts, real estate agents, and insurance policies, explaining legal principles and relevant case references. The assignment covers topics such as the L'Estrange Rule, misleading or deceptive conduct, unconscionable conduct, and the rights and obligations of insured parties under the Insurance Act.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.