LAW2453 Taxation 1: Comprehensive Analysis of Stella and Mia's Taxes

VerifiedAdded on 2023/06/08

|9

|2943

|443

Report

AI Summary

This assignment provides a detailed analysis of the tax implications for two taxpayers, Stella and Mia, focusing on various income sources and potential tax liabilities. Stella, a tax accountant and keen runner, faces issues regarding the taxability of her running-related income, including prize money, sponsorships, and appearance fees. The analysis considers whether these proceeds constitute ordinary income under s. 6-5 ITAA 1997, referencing the Stone v FCT case. Mia, a teacher and gardener, encounters tax issues related to her prize money, the classification of her gardening activities as a business or hobby, and potential capital gains tax (CGT) on the sale of her previous house. The assignment also examines the timing of CGT, treatment of gifts, and the applicability of the main residence exemption, referencing relevant legislation, case law, and tax rulings to provide a comprehensive understanding of their tax obligations. Desklib offers more solved assignments for students.

TAXATION

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The given situation tends to deal with two taxpayers namely Stella and Mia. Both have their

full time employment as accountant and teacher respectively. However, the taxpayers have

other pursuits also which lead to earnings being derived. For instance, Stella derives a

significant income from running events. Also, Mia is focusing on gardening on a 5 acre plot

is a big way. Considering these, the key objective of the given scenario is to highlight the tax

implications for the concerned taxpayers with regards to the underlying circumstances and

the applicable legislation, case law and tax rulings.

Facts

Stella is a tax accountant who has a full time job. However, she is also a keen runner and has

participated in various national and international events. On the basis of the running events,

she has derived $ 85,300 income which includes prize money, sponsorship and fees for game

attending. For attending these games, Stella uses the annual leaves that are available to her.

Stella has a friend Mia who is also a runner but has not participated in as many events as

Stella and thereby has won only $ 5,000 as prize from regional event participation.

Mia is employed as a teacher in local primary school but also has a 7 acre piece of land. Out

of these 7 acres, 2 acres have been used for construction of house which got completed in

August 2017 and was immediately used by Mia as her residence. The remaining space is

being used to plant walnut, fig and avocado trees. The previous house that Mia lived in was

sold with the contract signed in June 2017 and proceeds being obtained in October 2017. This

previous house was purchased by her in 2007 though she started living in the same only in

2010 and continued to do so till the sale of house. Also, Stella helped Mia in cleaning up the

old house before sale and an antique mirror was gifted to Stella. Once Mia had moved into

the new house, a house warming gift was given to her by Stella.

Issue

The main issues based on the above facts are highlighted below.

1) The proceeds derived by Stella from running to the tune of $ 85,300 would be ordinary

income or not with consideration to the various underlying proceeds.

2) The proceeds derived by Mia from running would be assessable income or not.

The given situation tends to deal with two taxpayers namely Stella and Mia. Both have their

full time employment as accountant and teacher respectively. However, the taxpayers have

other pursuits also which lead to earnings being derived. For instance, Stella derives a

significant income from running events. Also, Mia is focusing on gardening on a 5 acre plot

is a big way. Considering these, the key objective of the given scenario is to highlight the tax

implications for the concerned taxpayers with regards to the underlying circumstances and

the applicable legislation, case law and tax rulings.

Facts

Stella is a tax accountant who has a full time job. However, she is also a keen runner and has

participated in various national and international events. On the basis of the running events,

she has derived $ 85,300 income which includes prize money, sponsorship and fees for game

attending. For attending these games, Stella uses the annual leaves that are available to her.

Stella has a friend Mia who is also a runner but has not participated in as many events as

Stella and thereby has won only $ 5,000 as prize from regional event participation.

Mia is employed as a teacher in local primary school but also has a 7 acre piece of land. Out

of these 7 acres, 2 acres have been used for construction of house which got completed in

August 2017 and was immediately used by Mia as her residence. The remaining space is

being used to plant walnut, fig and avocado trees. The previous house that Mia lived in was

sold with the contract signed in June 2017 and proceeds being obtained in October 2017. This

previous house was purchased by her in 2007 though she started living in the same only in

2010 and continued to do so till the sale of house. Also, Stella helped Mia in cleaning up the

old house before sale and an antique mirror was gifted to Stella. Once Mia had moved into

the new house, a house warming gift was given to her by Stella.

Issue

The main issues based on the above facts are highlighted below.

1) The proceeds derived by Stella from running to the tune of $ 85,300 would be ordinary

income or not with consideration to the various underlying proceeds.

2) The proceeds derived by Mia from running would be assessable income or not.

3) The engagement of Mia in the activity of tree growing is a business or hobby with

consideration to relevant cases and tax rulings.

4) The potential capital gains on the old house sold by Mia. The year in which CGT (Capital

Gains Tax) would be levied on any potential capital gains is also an issue considering that

contract was signed in tax year 2016/2017 while the proceeds have been received in

2017/2018.

5) CGT implications of antique mirror and artwork for the respective owners i.e. Mia and

Stella.

6) Suitable taxation treatment of receipt on the gifts on the part of Stella and Mia.

Rule

The objective is to highlight the relevant rules in order to resolve the issues that have been

highlighted above.

Ordinary Income

One of the key components of assessable income is ordinary income that has been outlined in

s. 6-5 ITAA 1997. This income is defined as the proceeds which are generated from ordinary

concepts and typically include employment income, proceeds from business, investment

income (such as interest, dividends, coupon) along with rent income (Barkoczy, 2017).

Prize Money

With regards to prize money, the basic principle highlighted in TR 1999/17 is that the

proceeds would be considered as assessable income if the income is ordinary in nature or

produced during the ordinary course of profession/business. A key role with regards to prize

money is played by the underlying circumstances which play a crucial role in correct tax

treatment of proceeds from prize money. The key factors to consider the assessability of prize

money are highlighted below (Reuters, 2017).

Prize money derived on account of luck or skill as the latter is more likely to be

categorised as assessable income.

Activity undertaken as hobby or profession which would consider additional factors

such as amount of participation, time and other resource involvement in practice and

other related aspects.

consideration to relevant cases and tax rulings.

4) The potential capital gains on the old house sold by Mia. The year in which CGT (Capital

Gains Tax) would be levied on any potential capital gains is also an issue considering that

contract was signed in tax year 2016/2017 while the proceeds have been received in

2017/2018.

5) CGT implications of antique mirror and artwork for the respective owners i.e. Mia and

Stella.

6) Suitable taxation treatment of receipt on the gifts on the part of Stella and Mia.

Rule

The objective is to highlight the relevant rules in order to resolve the issues that have been

highlighted above.

Ordinary Income

One of the key components of assessable income is ordinary income that has been outlined in

s. 6-5 ITAA 1997. This income is defined as the proceeds which are generated from ordinary

concepts and typically include employment income, proceeds from business, investment

income (such as interest, dividends, coupon) along with rent income (Barkoczy, 2017).

Prize Money

With regards to prize money, the basic principle highlighted in TR 1999/17 is that the

proceeds would be considered as assessable income if the income is ordinary in nature or

produced during the ordinary course of profession/business. A key role with regards to prize

money is played by the underlying circumstances which play a crucial role in correct tax

treatment of proceeds from prize money. The key factors to consider the assessability of prize

money are highlighted below (Reuters, 2017).

Prize money derived on account of luck or skill as the latter is more likely to be

categorised as assessable income.

Activity undertaken as hobby or profession which would consider additional factors

such as amount of participation, time and other resource involvement in practice and

other related aspects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

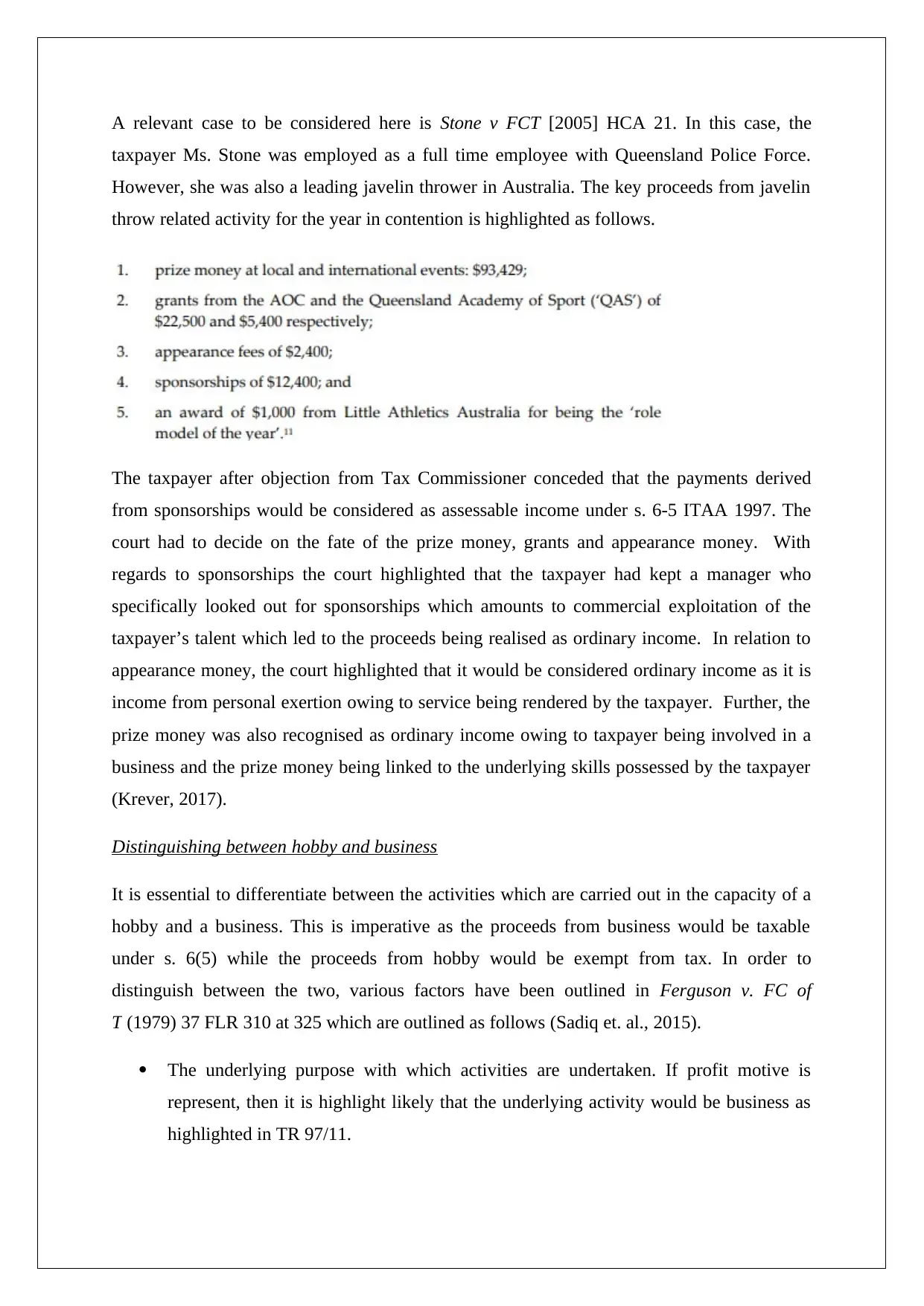

A relevant case to be considered here is Stone v FCT [2005] HCA 21. In this case, the

taxpayer Ms. Stone was employed as a full time employee with Queensland Police Force.

However, she was also a leading javelin thrower in Australia. The key proceeds from javelin

throw related activity for the year in contention is highlighted as follows.

The taxpayer after objection from Tax Commissioner conceded that the payments derived

from sponsorships would be considered as assessable income under s. 6-5 ITAA 1997. The

court had to decide on the fate of the prize money, grants and appearance money. With

regards to sponsorships the court highlighted that the taxpayer had kept a manager who

specifically looked out for sponsorships which amounts to commercial exploitation of the

taxpayer’s talent which led to the proceeds being realised as ordinary income. In relation to

appearance money, the court highlighted that it would be considered ordinary income as it is

income from personal exertion owing to service being rendered by the taxpayer. Further, the

prize money was also recognised as ordinary income owing to taxpayer being involved in a

business and the prize money being linked to the underlying skills possessed by the taxpayer

(Krever, 2017).

Distinguishing between hobby and business

It is essential to differentiate between the activities which are carried out in the capacity of a

hobby and a business. This is imperative as the proceeds from business would be taxable

under s. 6(5) while the proceeds from hobby would be exempt from tax. In order to

distinguish between the two, various factors have been outlined in Ferguson v. FC of

T (1979) 37 FLR 310 at 325 which are outlined as follows (Sadiq et. al., 2015).

The underlying purpose with which activities are undertaken. If profit motive is

represent, then it is highlight likely that the underlying activity would be business as

highlighted in TR 97/11.

taxpayer Ms. Stone was employed as a full time employee with Queensland Police Force.

However, she was also a leading javelin thrower in Australia. The key proceeds from javelin

throw related activity for the year in contention is highlighted as follows.

The taxpayer after objection from Tax Commissioner conceded that the payments derived

from sponsorships would be considered as assessable income under s. 6-5 ITAA 1997. The

court had to decide on the fate of the prize money, grants and appearance money. With

regards to sponsorships the court highlighted that the taxpayer had kept a manager who

specifically looked out for sponsorships which amounts to commercial exploitation of the

taxpayer’s talent which led to the proceeds being realised as ordinary income. In relation to

appearance money, the court highlighted that it would be considered ordinary income as it is

income from personal exertion owing to service being rendered by the taxpayer. Further, the

prize money was also recognised as ordinary income owing to taxpayer being involved in a

business and the prize money being linked to the underlying skills possessed by the taxpayer

(Krever, 2017).

Distinguishing between hobby and business

It is essential to differentiate between the activities which are carried out in the capacity of a

hobby and a business. This is imperative as the proceeds from business would be taxable

under s. 6(5) while the proceeds from hobby would be exempt from tax. In order to

distinguish between the two, various factors have been outlined in Ferguson v. FC of

T (1979) 37 FLR 310 at 325 which are outlined as follows (Sadiq et. al., 2015).

The underlying purpose with which activities are undertaken. If profit motive is

represent, then it is highlight likely that the underlying activity would be business as

highlighted in TR 97/11.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another factor to be considered is the repetition and regularity with which the

underlying activities are performed. Business activities tend to be more regular and

repetitive unlike hobby which is contingent on the availability of spare time and hence

irregular.

The organisation of activities is also a vital factor. This is because with regards to

business, the activities are arranged in a manner akin to business which would involve

proper book keeping and maintenance of requisite records pertaining to the activities.

In contrast, the activities under hobby do not tend to be organised and record keeping

is often missing.

The extent of resources deployed and the size of activities is also a crucial factor. In

case of business activities, a large amount of capital and human resources are

involved and often the size of operations is large so as to maximise the profits. In

contrast, for activities pursued as hobby, the resource deployment in terms of capital,

time, labour is low and also the scale is small.

Further, it has been indicated in Evans v. FC of T 89 ATC 4540 that no one factor is decisive

from the above list and also that the underlying factors would typically overlap. Also, the

case law Martin v. FC of T (1953) 90 CLR 470 at 474 highlighted that the decision whether

the given activity is business or hobby is based on a general impression derived on the

collective essence of the various factors that have been outlined above (Barkoczy, 2015).

General Deduction

As per s. 8-1 ITAA 1997, general deduction for losses or outgoings may be claimed provided

there is sufficient nexus between the expenses and the assessable income production. Further,

three negative limbs have been highlighted in ss. 8-1(2) where the deduction would not apply.

These are highlighted as follows (Krever, 2017).

The expenses are domestic or private in nature.

The expenses are capital in nature and not revenue.

The expenses are undertaken for production of non-assessable income.

Deductions would not be available if any of the above negative limbs is satisfied.

Main Residence Exemption

underlying activities are performed. Business activities tend to be more regular and

repetitive unlike hobby which is contingent on the availability of spare time and hence

irregular.

The organisation of activities is also a vital factor. This is because with regards to

business, the activities are arranged in a manner akin to business which would involve

proper book keeping and maintenance of requisite records pertaining to the activities.

In contrast, the activities under hobby do not tend to be organised and record keeping

is often missing.

The extent of resources deployed and the size of activities is also a crucial factor. In

case of business activities, a large amount of capital and human resources are

involved and often the size of operations is large so as to maximise the profits. In

contrast, for activities pursued as hobby, the resource deployment in terms of capital,

time, labour is low and also the scale is small.

Further, it has been indicated in Evans v. FC of T 89 ATC 4540 that no one factor is decisive

from the above list and also that the underlying factors would typically overlap. Also, the

case law Martin v. FC of T (1953) 90 CLR 470 at 474 highlighted that the decision whether

the given activity is business or hobby is based on a general impression derived on the

collective essence of the various factors that have been outlined above (Barkoczy, 2015).

General Deduction

As per s. 8-1 ITAA 1997, general deduction for losses or outgoings may be claimed provided

there is sufficient nexus between the expenses and the assessable income production. Further,

three negative limbs have been highlighted in ss. 8-1(2) where the deduction would not apply.

These are highlighted as follows (Krever, 2017).

The expenses are domestic or private in nature.

The expenses are capital in nature and not revenue.

The expenses are undertaken for production of non-assessable income.

Deductions would not be available if any of the above negative limbs is satisfied.

Main Residence Exemption

With regards to a property which is used by a taxpayer for personal residence, main residence

exemption may be possible which would result in exemption of capital gains tax from any

potential capital gains realised from sale of house. In order to ensure that the main residence

exemption is available under subdivision 118-B ITAA 1997, it is imperative that the

underlying property should be used as the main residence of the taxpayer for the ownership

period. Also, it is imperative that no commercial income by way of rent or otherwise should

be derived from the house. Additionally, it is possible that even when the taxpayer is not

residing in the house, it may consider it as main residence for six years (Reuters, 2017).

Timing of CGT

In liquidation of CGT assets, it may so happen that the contract for asset sale is enacted in a

given tax year while the associated receipts are received in the next tax year. In such a

situation, the taxpayer may be confused in regards to when the CGT consequences related to

the asset must be booked. In accordance with TR 94/29, in such a scenario, the CGT

consequences would arise when the contract for sale of the asset has been enacted without

consideration to the timing of the cash receipts of asset sale (Sadiq et. al., 2015).

Treatment of Gift

Gifts tend to be non-assessable and tax exempt income. In accordance with TR2005/13

Federal Commissioner of Taxation v. McPhail (1968) 117 CLR 111 case law, there are four

conditions which ought to be satisfied for a payment to be categorised as gift. These are listed

as follows (Barkoczy, 2017).

The transfer must be voluntary in nature.

There should be an ownership change in the favour of transferee from transferor.

The transferee should not have mutual reciprocal expectations in lieu of the payment.

It must be driven by personal affection, gratitude.

Application

In relation to the above discussion of the relevant law, the following conclusion can be made

in regards to the various receipts that are derived by Stella and Mia.

Tax implications for Stella

exemption may be possible which would result in exemption of capital gains tax from any

potential capital gains realised from sale of house. In order to ensure that the main residence

exemption is available under subdivision 118-B ITAA 1997, it is imperative that the

underlying property should be used as the main residence of the taxpayer for the ownership

period. Also, it is imperative that no commercial income by way of rent or otherwise should

be derived from the house. Additionally, it is possible that even when the taxpayer is not

residing in the house, it may consider it as main residence for six years (Reuters, 2017).

Timing of CGT

In liquidation of CGT assets, it may so happen that the contract for asset sale is enacted in a

given tax year while the associated receipts are received in the next tax year. In such a

situation, the taxpayer may be confused in regards to when the CGT consequences related to

the asset must be booked. In accordance with TR 94/29, in such a scenario, the CGT

consequences would arise when the contract for sale of the asset has been enacted without

consideration to the timing of the cash receipts of asset sale (Sadiq et. al., 2015).

Treatment of Gift

Gifts tend to be non-assessable and tax exempt income. In accordance with TR2005/13

Federal Commissioner of Taxation v. McPhail (1968) 117 CLR 111 case law, there are four

conditions which ought to be satisfied for a payment to be categorised as gift. These are listed

as follows (Barkoczy, 2017).

The transfer must be voluntary in nature.

There should be an ownership change in the favour of transferee from transferor.

The transferee should not have mutual reciprocal expectations in lieu of the payment.

It must be driven by personal affection, gratitude.

Application

In relation to the above discussion of the relevant law, the following conclusion can be made

in regards to the various receipts that are derived by Stella and Mia.

Tax implications for Stella

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1) Salary income from Hound Accounting Pty Ltd – The employment income would be

considered as ordinary income and thereby considered taxable in accordance with s. 6-5

ITAA 1997.

2) Earnings of $ 85,300 from running events – These would be recognised as ordinary

income in line with the verdict of the High Court in Stone v FCT case. Clearly, Stella is

regularly participating in national and international events which would give it a business like

character. Further, the prize money derived is not linked to luck but rather the underlying

skill of Stella, the taxpayer. Also, appearance fee would be income from personal exertion

since she renders services and uses her annual leaves for the same. Besides, sponsorships are

also part of the underlying business like profession that Stella is engaged in and hence the

underlying proceeds would be taxable.

3) Antique worth $ 1,500 from Mia – Clearly, this is not a gift since this has been given to

Stella on behalf of the help that she has extended to Mia with regards to cleaning her previous

house. Further, there was significant personal exertion involved on part of Stella which is

apparent from the trips that were made. Further, Mia would not have provided the antique

mirror to Stella if she would not have assisted her in the cleaning process. Therefore, this

would be statutory income and contribute $ 1,500 to assessable income.

Tax Implications for Mia

1) Earnings of $ 5,000 – The commercial aspect associated with running seems to be missing

for Mia who seems to pursue it more as a hobby which is apparent from the lack of

participation in major events. As a result, the proceeds would not be taxable.

2) Activity of Gardening – The activity of gardening is essentially a business activity and not

a hobby. This is apparent from the presence of profit motive on part of Mia from the

beginning. This is highlighted from the fact that she is already exploring avenues for selling

the produce. Also, she has created a Facebook page with a brand name so as to attract buyers

from far regions and thereby maximise the profits. Also, the scale is quite large considering

that five acre of plantation has been done. Further, she is also devoting time with regards to

conducting research on organic farming and has a dedicated room set aside for such

equipment. As a result, any expenses that would be undertaken by Mia would be deductible

under s. 8-1 from the current year only even though assessable income may be produced in

the future years.

considered as ordinary income and thereby considered taxable in accordance with s. 6-5

ITAA 1997.

2) Earnings of $ 85,300 from running events – These would be recognised as ordinary

income in line with the verdict of the High Court in Stone v FCT case. Clearly, Stella is

regularly participating in national and international events which would give it a business like

character. Further, the prize money derived is not linked to luck but rather the underlying

skill of Stella, the taxpayer. Also, appearance fee would be income from personal exertion

since she renders services and uses her annual leaves for the same. Besides, sponsorships are

also part of the underlying business like profession that Stella is engaged in and hence the

underlying proceeds would be taxable.

3) Antique worth $ 1,500 from Mia – Clearly, this is not a gift since this has been given to

Stella on behalf of the help that she has extended to Mia with regards to cleaning her previous

house. Further, there was significant personal exertion involved on part of Stella which is

apparent from the trips that were made. Further, Mia would not have provided the antique

mirror to Stella if she would not have assisted her in the cleaning process. Therefore, this

would be statutory income and contribute $ 1,500 to assessable income.

Tax Implications for Mia

1) Earnings of $ 5,000 – The commercial aspect associated with running seems to be missing

for Mia who seems to pursue it more as a hobby which is apparent from the lack of

participation in major events. As a result, the proceeds would not be taxable.

2) Activity of Gardening – The activity of gardening is essentially a business activity and not

a hobby. This is apparent from the presence of profit motive on part of Mia from the

beginning. This is highlighted from the fact that she is already exploring avenues for selling

the produce. Also, she has created a Facebook page with a brand name so as to attract buyers

from far regions and thereby maximise the profits. Also, the scale is quite large considering

that five acre of plantation has been done. Further, she is also devoting time with regards to

conducting research on organic farming and has a dedicated room set aside for such

equipment. As a result, any expenses that would be undertaken by Mia would be deductible

under s. 8-1 from the current year only even though assessable income may be produced in

the future years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3) Sale of Old House – The proceeds of house would be capital in nature and thereby non-

taxable. Further, the house after initial renovation was used as main residence by Mia till the

time of sale. Hence, exemption under Subdivision 118-B would be available from any capital

gains arising from house sale since the house was not used for any rental income.

4) House warming gift from Stella- This would be gift for Mia considering the fact that all

the conditions are fulfilled as have been outlined in Federal Commissioner of Taxation v.

McPhail (1968) 117 CLR. The house warming gift from Stella was voluntary and involved

ownership transfer. Further, Stella did not have any expectations for any favours to be

returns. Besides, the gesture arose because of personal affection between the two.

5) Income from being a teacher - The employment income would be considered as ordinary

income and thereby considered taxable in accordance with s. 6-5 ITAA 1997.

Conclusion

Based on the above discussion, it can be concluded that in case of Stella ordinary income

would be derived from employment as an accountant and earnings from running (including

prizes, appearance fees and sponsorships) since the running activity is being performed as a

business. Further, the antique mirror given to Stella from Mia would also contribute to

assessable income as it is not a gift but compensation received in kind for the services

offered.

In regards to Mia, ordinary income is derived based on her employment as teacher. However,

the running related receipts would not be taxable since it seems a hobby rather than a

business. The gardening activity that Mia is undertaking has the character of business

considering the various efforts taken by her to maximise profits. Besides, no CGT

consequences would arise in wake of old house sale since it was main residence and hence

exempted. Also, the house warming gift that Mia received from Stella would also not be

taxable.

taxable. Further, the house after initial renovation was used as main residence by Mia till the

time of sale. Hence, exemption under Subdivision 118-B would be available from any capital

gains arising from house sale since the house was not used for any rental income.

4) House warming gift from Stella- This would be gift for Mia considering the fact that all

the conditions are fulfilled as have been outlined in Federal Commissioner of Taxation v.

McPhail (1968) 117 CLR. The house warming gift from Stella was voluntary and involved

ownership transfer. Further, Stella did not have any expectations for any favours to be

returns. Besides, the gesture arose because of personal affection between the two.

5) Income from being a teacher - The employment income would be considered as ordinary

income and thereby considered taxable in accordance with s. 6-5 ITAA 1997.

Conclusion

Based on the above discussion, it can be concluded that in case of Stella ordinary income

would be derived from employment as an accountant and earnings from running (including

prizes, appearance fees and sponsorships) since the running activity is being performed as a

business. Further, the antique mirror given to Stella from Mia would also contribute to

assessable income as it is not a gift but compensation received in kind for the services

offered.

In regards to Mia, ordinary income is derived based on her employment as teacher. However,

the running related receipts would not be taxable since it seems a hobby rather than a

business. The gardening activity that Mia is undertaking has the character of business

considering the various efforts taken by her to maximise profits. Besides, no CGT

consequences would arise in wake of old house sale since it was main residence and hence

exempted. Also, the house warming gift that Mia received from Stella would also not be

taxable.

References

Textbooks

Barkoczy, S. (2017) Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH

Publications.

Krever, R. (2017) Australian Taxation Law Cases 2017 (2nd ed.). Brisbane: THOMSON

LAWBOOK Company.

Reuters, T. (2017) Australian Tax Legislation 2017 (4th ed.). Sydney. THOMSON

REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A.

(2015) Principles of Taxation Law 2015 (7th ed.). Pymont: Thomson Reuters.

Case Law, Tax Rulings & Legislation

Evans v. FC of T 89 ATC 4540

Federal Commissioner of Taxation v. McPhail (1968) 117 CLR

Ferguson v. FC of T (1979) 37 FLR 310 at 325

Martin v. FC of T (1953) 90 CLR 470 at 474

Stone v FCT [2005] HCA 21

TR 94/29

TR 97/11

TR 1999/17

TR 2005/13

Income Tax Assessment Act, 1997

Textbooks

Barkoczy, S. (2017) Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH

Publications.

Krever, R. (2017) Australian Taxation Law Cases 2017 (2nd ed.). Brisbane: THOMSON

LAWBOOK Company.

Reuters, T. (2017) Australian Tax Legislation 2017 (4th ed.). Sydney. THOMSON

REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A.

(2015) Principles of Taxation Law 2015 (7th ed.). Pymont: Thomson Reuters.

Case Law, Tax Rulings & Legislation

Evans v. FC of T 89 ATC 4540

Federal Commissioner of Taxation v. McPhail (1968) 117 CLR

Ferguson v. FC of T (1979) 37 FLR 310 at 325

Martin v. FC of T (1953) 90 CLR 470 at 474

Stone v FCT [2005] HCA 21

TR 94/29

TR 97/11

TR 1999/17

TR 2005/13

Income Tax Assessment Act, 1997

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.