LAWS20060 Taxation Law of Australia Assignment, Term 1, 2019

VerifiedAdded on 2023/02/01

|18

|4324

|44

Homework Assignment

AI Summary

This document presents a detailed solution to a Taxation Law assignment, addressing key concepts and principles of Australian tax law. The assignment covers various aspects, including the effective life of depreciating assets, claiming tax offsets, the highest tax rates for Australian residents, capital gains tax (CGT) on collectibles, CGT events, calculation of income tax, legal expenses deductions, marginal and average tax rates, and consumption tax. It further analyzes deductible expenses under section 8-1 of the ITAA 1997, including business and private use expenses, personal or domestic nature losses, diminished financial resources, and preliminary expenses. The document also delves into CGT events such as granting long-term leases, passing the use and enjoyment of title, main residence exemptions, and the CGT discount. Additionally, it explores the tax treatment of prizes, reimbursements, and assesses the tax implications of various scenarios, including ordinary income and capital gains, offering a comprehensive overview of taxation principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer A:..............................................................................................................................8

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer A:..............................................................................................................................8

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................9

2TAXATION LAW

Answer D:..............................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................11

Answer D:............................................................................................................................11

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................12

Application:..........................................................................................................................13

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

Answer D:..............................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................11

Answer D:............................................................................................................................11

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................12

Application:..........................................................................................................................13

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

The topic that is explained in “Taxation Ruling of TR 2018/4” covers about the

effective life of the asset which are depreciating in nature under “section 40-100, ITAA

1997”.

Answer B:

A taxpayer under the “Division 13, ITAA 1997” of the ITAA 1997 provides the

explanation about claiming tax offsets.

Answer C:

The highest rate of tax which is applied on the resident of Australia for taxation

purpose stands 54,097 + 45c for each $1 above 180,000.

Answer D:

Under the “section 118-10 (1), ITAA 1997”, capital gains tax that are made from the

collectible costing $500 or less must be disregarded1.

Answer E:

Under the “section 104-15” it states the use of title prior to it passes to others. Where

an individual creates an arrangement or agreement with some other individual and the right of

using the title is passed on to other person the entity then it results in CGT event B12. Where

1 Graetz, Michael, et al. Federal Income Taxation, Principles and Policies (University

Casebook Series). Foundation Press/West Academic, 2015.

2 Klein, William A., Joseph Bankman, and Daniel N. Shaviro. Federal income taxation.

Aspen Publishers, 2013.

Answer to question 1:

Answer A:

The topic that is explained in “Taxation Ruling of TR 2018/4” covers about the

effective life of the asset which are depreciating in nature under “section 40-100, ITAA

1997”.

Answer B:

A taxpayer under the “Division 13, ITAA 1997” of the ITAA 1997 provides the

explanation about claiming tax offsets.

Answer C:

The highest rate of tax which is applied on the resident of Australia for taxation

purpose stands 54,097 + 45c for each $1 above 180,000.

Answer D:

Under the “section 118-10 (1), ITAA 1997”, capital gains tax that are made from the

collectible costing $500 or less must be disregarded1.

Answer E:

Under the “section 104-15” it states the use of title prior to it passes to others. Where

an individual creates an arrangement or agreement with some other individual and the right of

using the title is passed on to other person the entity then it results in CGT event B12. Where

1 Graetz, Michael, et al. Federal Income Taxation, Principles and Policies (University

Casebook Series). Foundation Press/West Academic, 2015.

2 Klein, William A., Joseph Bankman, and Daniel N. Shaviro. Federal income taxation.

Aspen Publishers, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

the title of the asset is passed to another entity prior the end of a contract or agreement then a

CGT event B1 takes place.

Answer F:

As it has been defined under the “section 4-10 of the ITAA 1997” the taxpayer

should pay the tax each and every year. furthermore, “section 4-10 (3), ITAA 1997” lay

down the formula for calculating the income tax3. The formula is given below

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

The decision that was made in “FC of T v Day 2008 ATC 20-064” explains that legal

expenses incurred to derive the taxable earnings on meeting the criteria given under

“paragraph 8-1 (1) (a), ITAA 1997” was allowed as deduction4. The law court held that legal

expense was allowed for deduction because it did not relate to taxpayer personal income and

the expenses originated from the service of public servant. The federal court passed its

verdict by explaining that the legal expenditure was allowable for tax deduction under

“section 8-1, ITAA 1997”.

Answer H:

Distinction between the marginal and average tax is given below;

a. The average tax weighs the tax burden. On the other hand, marginal tax rates weigh

the effect of tax on incentives, income and expenditure.

3 Blakey, Roy Gillispie, and Gladys C. Blakey. The federal income tax. The Lawbook

Exchange, Ltd., 2006.

4 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

the title of the asset is passed to another entity prior the end of a contract or agreement then a

CGT event B1 takes place.

Answer F:

As it has been defined under the “section 4-10 of the ITAA 1997” the taxpayer

should pay the tax each and every year. furthermore, “section 4-10 (3), ITAA 1997” lay

down the formula for calculating the income tax3. The formula is given below

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

The decision that was made in “FC of T v Day 2008 ATC 20-064” explains that legal

expenses incurred to derive the taxable earnings on meeting the criteria given under

“paragraph 8-1 (1) (a), ITAA 1997” was allowed as deduction4. The law court held that legal

expense was allowed for deduction because it did not relate to taxpayer personal income and

the expenses originated from the service of public servant. The federal court passed its

verdict by explaining that the legal expenditure was allowable for tax deduction under

“section 8-1, ITAA 1997”.

Answer H:

Distinction between the marginal and average tax is given below;

a. The average tax weighs the tax burden. On the other hand, marginal tax rates weigh

the effect of tax on incentives, income and expenditure.

3 Blakey, Roy Gillispie, and Gladys C. Blakey. The federal income tax. The Lawbook

Exchange, Ltd., 2006.

4 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

5TAXATION LAW

b. Average tax measures the tax burden on households and the impact on the consumer’s

ability to consume presently5. Marginal tax rate assesses the extent to which tax

impact the household economic incentives such as to work and save more by

accepting high investment risks.

Answer I:

Consumption tax can be defined as the expenditure incurred on goods and services.

The tax base comprises of the sum of money which is spend on consumption. Consumption

tax is usually indirect tax and involves sales and value added tax.

Answer to question 2:

Answer to A:

“Section 8-1, ITAA 1997” lists down two positive limbs. Under the limbs a taxpayer

is permitted to deduct from their taxable income any kind of loss or outgoings till the extent

that it is occurred in producing the taxable income and the expenses that are occurred in

performing business activities for gaining assessable income. As held in “Ronpibon Tin NL

v FCT (1949)” expenses are only allowed to be tax deductible when it is occurred in gaining

or generating the taxable income6.

Brett took a loan to pay the employee wages and incurred interest on loan. The

interest on loan is tax deductible because it is it is occurred in gaining or generating the

taxable income in the ordinary business course.

5 Oishi, Shigehiro, Kostadin Kushlev, and Ulrich Schimmack. "Progressive taxation, income

inequality, and happiness." American Psychologist 73.2 (2018): 157.

6 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

b. Average tax measures the tax burden on households and the impact on the consumer’s

ability to consume presently5. Marginal tax rate assesses the extent to which tax

impact the household economic incentives such as to work and save more by

accepting high investment risks.

Answer I:

Consumption tax can be defined as the expenditure incurred on goods and services.

The tax base comprises of the sum of money which is spend on consumption. Consumption

tax is usually indirect tax and involves sales and value added tax.

Answer to question 2:

Answer to A:

“Section 8-1, ITAA 1997” lists down two positive limbs. Under the limbs a taxpayer

is permitted to deduct from their taxable income any kind of loss or outgoings till the extent

that it is occurred in producing the taxable income and the expenses that are occurred in

performing business activities for gaining assessable income. As held in “Ronpibon Tin NL

v FCT (1949)” expenses are only allowed to be tax deductible when it is occurred in gaining

or generating the taxable income6.

Brett took a loan to pay the employee wages and incurred interest on loan. The

interest on loan is tax deductible because it is it is occurred in gaining or generating the

taxable income in the ordinary business course.

5 Oishi, Shigehiro, Kostadin Kushlev, and Ulrich Schimmack. "Progressive taxation, income

inequality, and happiness." American Psychologist 73.2 (2018): 157.

6 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to B:

As explained by ATO if a person occurs expenditure that are for both the business and

private use, a taxpayer is only permitted to claim deduction for the business portion. Julie

reports $500 as mobile phone charges during the year. The work purpose expenses amounts

to 60% while 40% amounts to private expenses. Julie can only claim deduction for 60% of

mobile phone expenses because it is related to business portion.

Answer to C:

Loss and outgoings of a personal or domestic nature is not allowed for deduction

because it does not meet either the positive limbs and not permitted for deduction under

second negative limb of “section 8-1 (2)(b)”. In “Lodge v FCT (1972)” no deduction from

assessable was permitted to taxpayer for child care expenses because not relevant in

producing income7.

A total of $1200 was paid by Sally for babysitting purpose because so that she can go

to work. These babysitting expenses is not permissible deduction because it does not meet

either the positive limbs and not permitted for deduction under second negative limb of

“section 8-1 (2)(b)”. The babysitting expenses is irrelevant in producing taxable income8.

7 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

8 Mertens, Karel, and José Luis Montiel Olea. "Marginal tax rates and income: New time

series evidence." The Quarterly Journal of Economics 133.4 (2018): 1803-1884.

Answer to B:

As explained by ATO if a person occurs expenditure that are for both the business and

private use, a taxpayer is only permitted to claim deduction for the business portion. Julie

reports $500 as mobile phone charges during the year. The work purpose expenses amounts

to 60% while 40% amounts to private expenses. Julie can only claim deduction for 60% of

mobile phone expenses because it is related to business portion.

Answer to C:

Loss and outgoings of a personal or domestic nature is not allowed for deduction

because it does not meet either the positive limbs and not permitted for deduction under

second negative limb of “section 8-1 (2)(b)”. In “Lodge v FCT (1972)” no deduction from

assessable was permitted to taxpayer for child care expenses because not relevant in

producing income7.

A total of $1200 was paid by Sally for babysitting purpose because so that she can go

to work. These babysitting expenses is not permissible deduction because it does not meet

either the positive limbs and not permitted for deduction under second negative limb of

“section 8-1 (2)(b)”. The babysitting expenses is irrelevant in producing taxable income8.

7 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

8 Mertens, Karel, and José Luis Montiel Olea. "Marginal tax rates and income: New time

series evidence." The Quarterly Journal of Economics 133.4 (2018): 1803-1884.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to D:

Deduction for outgoings or loss is permitted only under circumstances when the

financial resources of a taxpayer has been diminished. In “Charles Moore & Co Pty Ltd v

FCT (1956)” deduction was permitted to taxpayer for money that was stolen9.

The loss of $20,000 in the form of theft of business goods by Jerry’s long term

employee is permitted for deduction under “section 8-1, ITAA 1997” because the financial

resources for taxpayer has been diminished.

Answer to E:

Loss or outgoings that are preliminary to commencement of income producing

activities is not deductible under “section 8-1” because the expenses are not in the ordinary

business course. Under 1st positive limb, outgoings occurred in getting new employment is

not in the course of producing taxable income. In “FCT v Maddelena (1971)” a football

player was not allowed deduction for expenses incurred in travelling to another club for

negotiating contract because the outgoings occurred at a point too soon.

Outgoings of $5,000 occurred in hosting the local government election is non-

deductible under “section 8-1” because it is not in the business course and occurred at a point

too soon.

9 Abrams, Howard E., and Don Leatherman. Federal income taxation of corporations and

partnerships. Wolters Kluwer Law & Business, 2019.

Answer to D:

Deduction for outgoings or loss is permitted only under circumstances when the

financial resources of a taxpayer has been diminished. In “Charles Moore & Co Pty Ltd v

FCT (1956)” deduction was permitted to taxpayer for money that was stolen9.

The loss of $20,000 in the form of theft of business goods by Jerry’s long term

employee is permitted for deduction under “section 8-1, ITAA 1997” because the financial

resources for taxpayer has been diminished.

Answer to E:

Loss or outgoings that are preliminary to commencement of income producing

activities is not deductible under “section 8-1” because the expenses are not in the ordinary

business course. Under 1st positive limb, outgoings occurred in getting new employment is

not in the course of producing taxable income. In “FCT v Maddelena (1971)” a football

player was not allowed deduction for expenses incurred in travelling to another club for

negotiating contract because the outgoings occurred at a point too soon.

Outgoings of $5,000 occurred in hosting the local government election is non-

deductible under “section 8-1” because it is not in the business course and occurred at a point

too soon.

9 Abrams, Howard E., and Don Leatherman. Federal income taxation of corporations and

partnerships. Wolters Kluwer Law & Business, 2019.

8TAXATION LAW

Answer to question 3:

Answer A:

According to the explanation of ATO taxpayers are permitted to apply CGT event F2

upon granting the long term lease or renewing the same by taxpayers10. The CGT event F2 is

applicable when the taxpayer as the land owner grants any sub-lease of land. The taxpayers

should denote that CGT discount is not applicable when a CGT event F2 happens.

According to facts obtained it is understood that Andy as the land owner is granted

with the five-year lease of land based on the premium of $5,000. The lease that is granted by

Andy for the period of five years has resulted in CGT event F2. Therefore, no CGT discount

is applied in this case.

Answer B:

When any use as well as enjoyment of the title is passed to others then a CGT event

B1 happens. On using the CGT asset whose title is already passed then the capital gains after

subtracting the cost of acquisition of land may lead to CGT event B111. The usage and

enjoyment of asset from the practical viewpoint takes place only when the ownership of the

asset is passed to new owner where the owner is allowed rent the land and derive profits from

it. As understood in case of Farm Ltd, an option was granted for purchasing the farm for a

sum of $800,000. The granting of option for purchasing the land is viewed as CGT event B1.

Consequently, John can apply the CGT discount before the title of land is passed.

10 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50.3 (2015): 277-300.

11 Alpanda, Sami, and Sarah Zubairy. "Housing and tax policy." Journal of Money, Credit

and Banking 48.2-3 (2016): 485-512.

Answer to question 3:

Answer A:

According to the explanation of ATO taxpayers are permitted to apply CGT event F2

upon granting the long term lease or renewing the same by taxpayers10. The CGT event F2 is

applicable when the taxpayer as the land owner grants any sub-lease of land. The taxpayers

should denote that CGT discount is not applicable when a CGT event F2 happens.

According to facts obtained it is understood that Andy as the land owner is granted

with the five-year lease of land based on the premium of $5,000. The lease that is granted by

Andy for the period of five years has resulted in CGT event F2. Therefore, no CGT discount

is applied in this case.

Answer B:

When any use as well as enjoyment of the title is passed to others then a CGT event

B1 happens. On using the CGT asset whose title is already passed then the capital gains after

subtracting the cost of acquisition of land may lead to CGT event B111. The usage and

enjoyment of asset from the practical viewpoint takes place only when the ownership of the

asset is passed to new owner where the owner is allowed rent the land and derive profits from

it. As understood in case of Farm Ltd, an option was granted for purchasing the farm for a

sum of $800,000. The granting of option for purchasing the land is viewed as CGT event B1.

Consequently, John can apply the CGT discount before the title of land is passed.

10 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50.3 (2015): 277-300.

11 Alpanda, Sami, and Sarah Zubairy. "Housing and tax policy." Journal of Money, Credit

and Banking 48.2-3 (2016): 485-512.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer C:

For capital gains tax purpose the main residence of tax payer is generally exempted.

However, full main residence is only applied when no part of the house is used for running

business. Where any portion of the house is used for deriving profits or running business then

a partial main residence exemption is provided for capital gains tax12.

Jamie and Olivia bought a property which they rented it out for two years. From 2008

onwards the property was used for dwelling purpose and eventually sold in 2018. Jamie and

Olivia can only be permitted to claim partial main residence exemption from capital gains

tax. Furthermore, they are eligible for 50% CGT discount upon the sale of house.

Answer D:

CGT discount is only allowed on capital gains where the asset is held for a 12 months or

more.

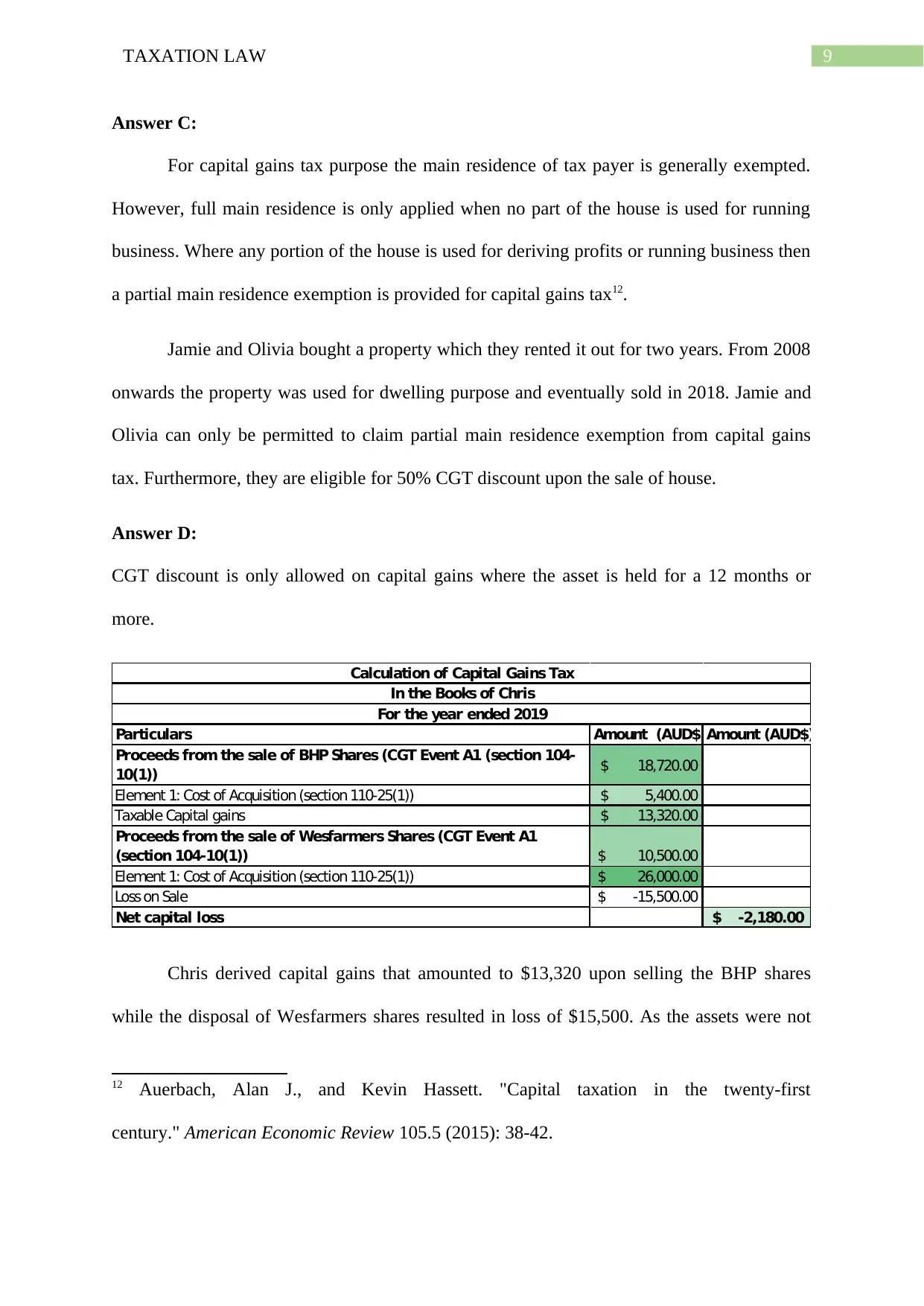

Particulars Amount (AUD$)Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-

10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1

(section 104-10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris derived capital gains that amounted to $13,320 upon selling the BHP shares

while the disposal of Wesfarmers shares resulted in loss of $15,500. As the assets were not

12 Auerbach, Alan J., and Kevin Hassett. "Capital taxation in the twenty-first

century." American Economic Review 105.5 (2015): 38-42.

Answer C:

For capital gains tax purpose the main residence of tax payer is generally exempted.

However, full main residence is only applied when no part of the house is used for running

business. Where any portion of the house is used for deriving profits or running business then

a partial main residence exemption is provided for capital gains tax12.

Jamie and Olivia bought a property which they rented it out for two years. From 2008

onwards the property was used for dwelling purpose and eventually sold in 2018. Jamie and

Olivia can only be permitted to claim partial main residence exemption from capital gains

tax. Furthermore, they are eligible for 50% CGT discount upon the sale of house.

Answer D:

CGT discount is only allowed on capital gains where the asset is held for a 12 months or

more.

Particulars Amount (AUD$)Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-

10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1

(section 104-10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris derived capital gains that amounted to $13,320 upon selling the BHP shares

while the disposal of Wesfarmers shares resulted in loss of $15,500. As the assets were not

12 Auerbach, Alan J., and Kevin Hassett. "Capital taxation in the twenty-first

century." American Economic Review 105.5 (2015): 38-42.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

held for 12 months from the date of purchase, Chris would not be allowed to apply 50% CGT

discount and he can include into his assessable income the capital gains of $13,320 in the

taxable income. the capital loss should carry forward by Chris to subsequent year.

Answer to question 4:

Answer A:

Prizes are not normally considered for tax. However, prizes would be taxable if it

associated to an individual’s revenue earning activity. As held in “FCT v Stone (2005)” the

taxpayer made income from salary and prize money13. The taxpayer was found to be carrying

the business of professional athlete and the prize money was taxable.

The prize money of $2,000 received is taxable based on the assumption that the

amount received is in relation to the taxpayer’s income earning activity. The money is taxable

as ordinary income under “section 6-5, ITAA 1997”.

Answer B:

Reimbursement of expenditure incurred by the employer to the employee is not

treated as income. In the present situation it is noticed that an employee occurred expenses of

$500 in travelling to Sydney for work purpose. However, the employee here incurred only

$120 for the entire trip14. Therefore, the remaining amount of $380 constitutes a real gain for

the employee and hence it is an income under the ordinary concept of “section 6-5, ITAA

1997”.

13 Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in

Australia: an alternative way forward." Austl. Tax F. 30 (2015): 735.

14 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

held for 12 months from the date of purchase, Chris would not be allowed to apply 50% CGT

discount and he can include into his assessable income the capital gains of $13,320 in the

taxable income. the capital loss should carry forward by Chris to subsequent year.

Answer to question 4:

Answer A:

Prizes are not normally considered for tax. However, prizes would be taxable if it

associated to an individual’s revenue earning activity. As held in “FCT v Stone (2005)” the

taxpayer made income from salary and prize money13. The taxpayer was found to be carrying

the business of professional athlete and the prize money was taxable.

The prize money of $2,000 received is taxable based on the assumption that the

amount received is in relation to the taxpayer’s income earning activity. The money is taxable

as ordinary income under “section 6-5, ITAA 1997”.

Answer B:

Reimbursement of expenditure incurred by the employer to the employee is not

treated as income. In the present situation it is noticed that an employee occurred expenses of

$500 in travelling to Sydney for work purpose. However, the employee here incurred only

$120 for the entire trip14. Therefore, the remaining amount of $380 constitutes a real gain for

the employee and hence it is an income under the ordinary concept of “section 6-5, ITAA

1997”.

13 Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in

Australia: an alternative way forward." Austl. Tax F. 30 (2015): 735.

14 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

11TAXATION LAW

Answer C:

A gain that are treated as simple gifts normally does not possess any income

characteristics. As stated in “Scott v FCT (1966)” the solicitor was given a gift that amounted

to $10,000 from the clients wife out of the long estate of husband was not treated as income15.

In agreement with the above stated case it can be stated that the iphone of $1,000 received

from the client is not treated as having an income character.

Answer D:

In certain situations an individual may get lump sum payment that can be considered

taxable income. As it is explained in “paragraph 118-37 (1), (b), ITAA 1997” the taxpayers

should not include the receipts that are received as compensation payment for any kind of

personal injury suffered due to wrong or illness.

A taxpayer here is awarded with the amount of $10,000 as a result of personal injuries

suffered from the car accident. The amount under the “paragraph 118-37 (1), (b), ITAA

1997” should be excluded from assessment purpose because it is not an income.

Answer E:

There may be circumstances where the taxpayer may expect earning income in the

future period of time on the basis of currently being entitled to income in the upcoming year

is considered too remote to offer any form of connection with the present income year16. A

taxpayer purchases a share for $5 during the year and on 30th June, the taxpayer yet owns the

shares which is presently trending for $7.50. No income is earned in this situation because the

15 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

16 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Answer C:

A gain that are treated as simple gifts normally does not possess any income

characteristics. As stated in “Scott v FCT (1966)” the solicitor was given a gift that amounted

to $10,000 from the clients wife out of the long estate of husband was not treated as income15.

In agreement with the above stated case it can be stated that the iphone of $1,000 received

from the client is not treated as having an income character.

Answer D:

In certain situations an individual may get lump sum payment that can be considered

taxable income. As it is explained in “paragraph 118-37 (1), (b), ITAA 1997” the taxpayers

should not include the receipts that are received as compensation payment for any kind of

personal injury suffered due to wrong or illness.

A taxpayer here is awarded with the amount of $10,000 as a result of personal injuries

suffered from the car accident. The amount under the “paragraph 118-37 (1), (b), ITAA

1997” should be excluded from assessment purpose because it is not an income.

Answer E:

There may be circumstances where the taxpayer may expect earning income in the

future period of time on the basis of currently being entitled to income in the upcoming year

is considered too remote to offer any form of connection with the present income year16. A

taxpayer purchases a share for $5 during the year and on 30th June, the taxpayer yet owns the

shares which is presently trending for $7.50. No income is earned in this situation because the

15 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

16 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.