LAWS20060 Taxation Law of Australia Assignment - Term 2 2019

VerifiedAdded on 2022/10/07

|19

|3343

|26

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing several key areas of Australian tax law. The assignment covers topics such as the definition of business income, allowable tax deductions, the application of the Capital Gains Tax (CGT), and the distinction between ordinary and statutory income. It also explores the concepts of 'usual place of abode' and 'permanent place of abode' in relation to residency, as well as deductible and non-deductible expenses. The solution includes detailed explanations, references to relevant legislation and case law, and calculations where necessary, providing a thorough analysis of the tax implications in various scenarios. The assignment also examines the application of CGT event F1 and the implications of using part of a main residence for business purposes. The solution adheres to the Australian Guide to Legal Citation (AGLC) referencing method.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to Question 3:................................................................................................................8

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................13

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to Question 3:................................................................................................................8

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................13

2TAXATION LAW

Answer to C:........................................................................................................................14

Answer to D:........................................................................................................................14

Answer to E:.........................................................................................................................15

References:...............................................................................................................................16

Answer to C:........................................................................................................................14

Answer to D:........................................................................................................................14

Answer to E:.........................................................................................................................15

References:...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

As per the commissioner view it lay down that the ruling of taxation TR 2019/1 states

when a business carried by an organisation in the sense of small entity business under the

section 23, “Income Tax Rates Act 1986” as the case of income in the F.Y of 2015-16 and

2016-17 or under “section 328-110, ITAA 1997”1.

Answer B:

As per the “Division 30, ITAA 1997” explains the rule and regulation related to allow

of deduction from tax in case of gifts and contribution2.

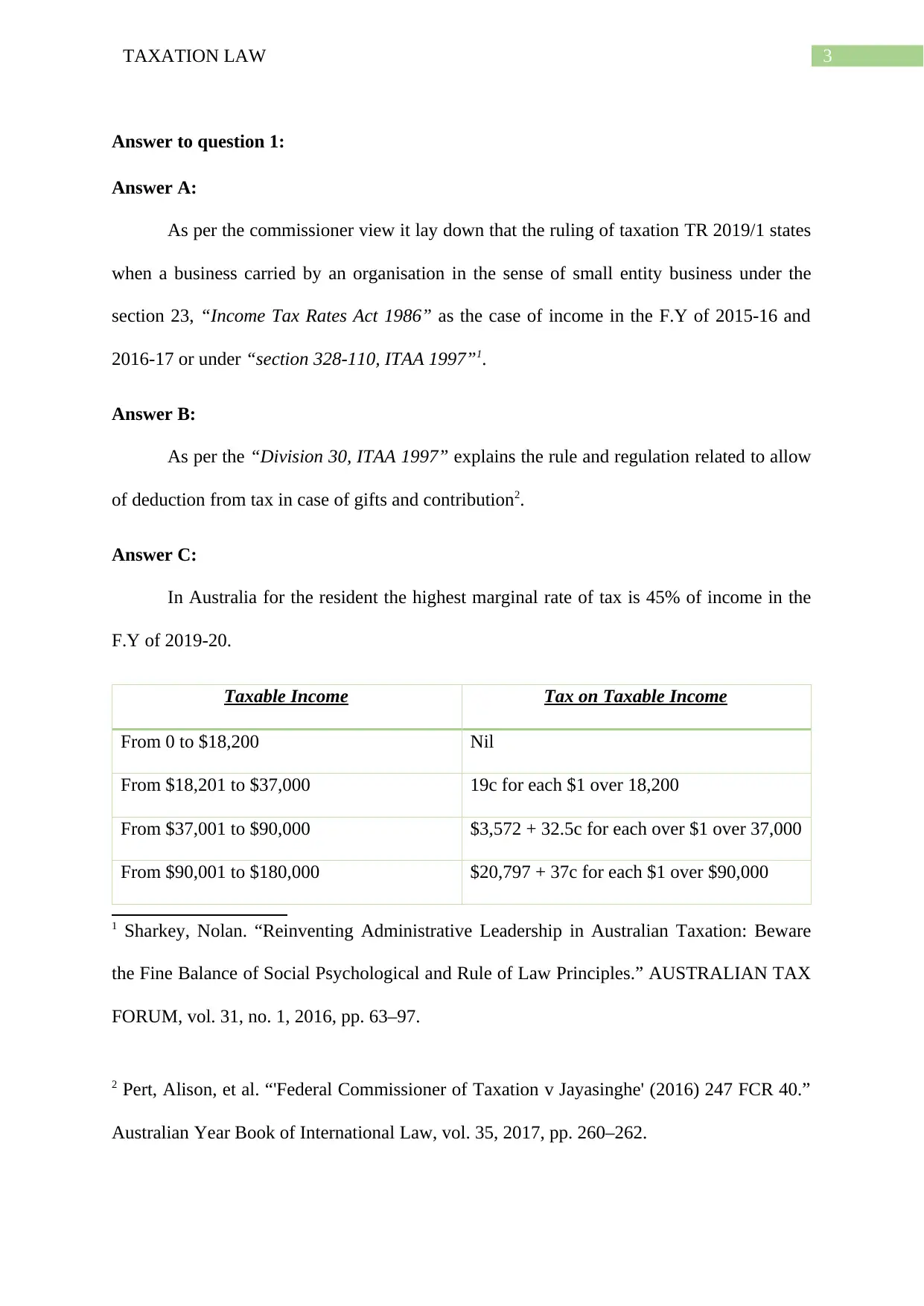

Answer C:

In Australia for the resident the highest marginal rate of tax is 45% of income in the

F.Y of 2019-20.

Taxable Income Tax on Taxable Income

From 0 to $18,200 Nil

From $18,201 to $37,000 19c for each $1 over 18,200

From $37,001 to $90,000 $3,572 + 32.5c for each over $1 over 37,000

From $90,001 to $180,000 $20,797 + 37c for each $1 over $90,000

1 Sharkey, Nolan. “Reinventing Administrative Leadership in Australian Taxation: Beware

the Fine Balance of Social Psychological and Rule of Law Principles.” AUSTRALIAN TAX

FORUM, vol. 31, no. 1, 2016, pp. 63–97.

2 Pert, Alison, et al. “'Federal Commissioner of Taxation v Jayasinghe' (2016) 247 FCR 40.”

Australian Year Book of International Law, vol. 35, 2017, pp. 260–262.

Answer to question 1:

Answer A:

As per the commissioner view it lay down that the ruling of taxation TR 2019/1 states

when a business carried by an organisation in the sense of small entity business under the

section 23, “Income Tax Rates Act 1986” as the case of income in the F.Y of 2015-16 and

2016-17 or under “section 328-110, ITAA 1997”1.

Answer B:

As per the “Division 30, ITAA 1997” explains the rule and regulation related to allow

of deduction from tax in case of gifts and contribution2.

Answer C:

In Australia for the resident the highest marginal rate of tax is 45% of income in the

F.Y of 2019-20.

Taxable Income Tax on Taxable Income

From 0 to $18,200 Nil

From $18,201 to $37,000 19c for each $1 over 18,200

From $37,001 to $90,000 $3,572 + 32.5c for each over $1 over 37,000

From $90,001 to $180,000 $20,797 + 37c for each $1 over $90,000

1 Sharkey, Nolan. “Reinventing Administrative Leadership in Australian Taxation: Beware

the Fine Balance of Social Psychological and Rule of Law Principles.” AUSTRALIAN TAX

FORUM, vol. 31, no. 1, 2016, pp. 63–97.

2 Pert, Alison, et al. “'Federal Commissioner of Taxation v Jayasinghe' (2016) 247 FCR 40.”

Australian Year Book of International Law, vol. 35, 2017, pp. 260–262.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

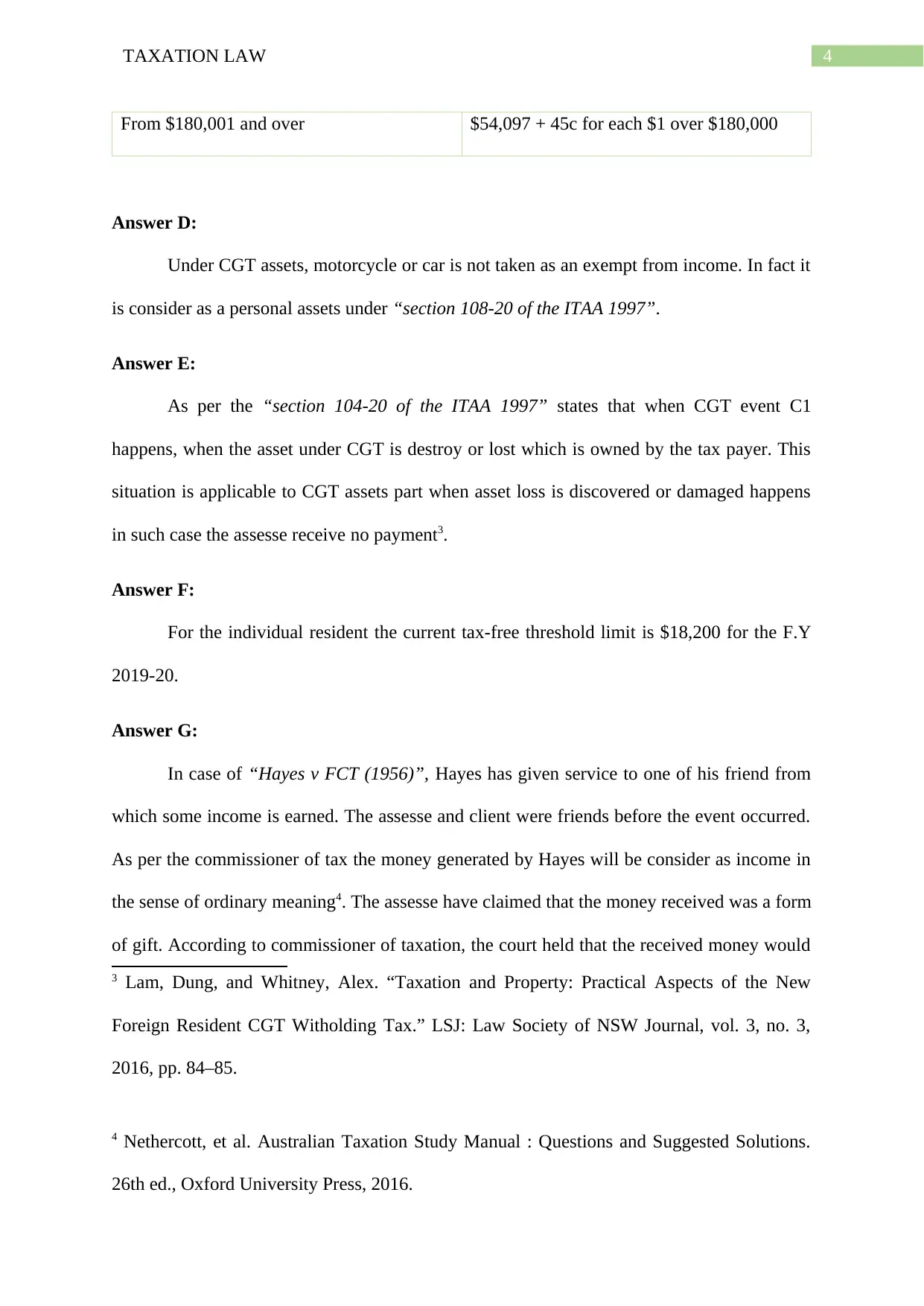

From $180,001 and over $54,097 + 45c for each $1 over $180,000

Answer D:

Under CGT assets, motorcycle or car is not taken as an exempt from income. In fact it

is consider as a personal assets under “section 108-20 of the ITAA 1997”.

Answer E:

As per the “section 104-20 of the ITAA 1997” states that when CGT event C1

happens, when the asset under CGT is destroy or lost which is owned by the tax payer. This

situation is applicable to CGT assets part when asset loss is discovered or damaged happens

in such case the assesse receive no payment3.

Answer F:

For the individual resident the current tax-free threshold limit is $18,200 for the F.Y

2019-20.

Answer G:

In case of “Hayes v FCT (1956)”, Hayes has given service to one of his friend from

which some income is earned. The assesse and client were friends before the event occurred.

As per the commissioner of tax the money generated by Hayes will be consider as income in

the sense of ordinary meaning4. The assesse have claimed that the money received was a form

of gift. According to commissioner of taxation, the court held that the received money would

3 Lam, Dung, and Whitney, Alex. “Taxation and Property: Practical Aspects of the New

Foreign Resident CGT Witholding Tax.” LSJ: Law Society of NSW Journal, vol. 3, no. 3,

2016, pp. 84–85.

4 Nethercott, et al. Australian Taxation Study Manual : Questions and Suggested Solutions.

26th ed., Oxford University Press, 2016.

From $180,001 and over $54,097 + 45c for each $1 over $180,000

Answer D:

Under CGT assets, motorcycle or car is not taken as an exempt from income. In fact it

is consider as a personal assets under “section 108-20 of the ITAA 1997”.

Answer E:

As per the “section 104-20 of the ITAA 1997” states that when CGT event C1

happens, when the asset under CGT is destroy or lost which is owned by the tax payer. This

situation is applicable to CGT assets part when asset loss is discovered or damaged happens

in such case the assesse receive no payment3.

Answer F:

For the individual resident the current tax-free threshold limit is $18,200 for the F.Y

2019-20.

Answer G:

In case of “Hayes v FCT (1956)”, Hayes has given service to one of his friend from

which some income is earned. The assesse and client were friends before the event occurred.

As per the commissioner of tax the money generated by Hayes will be consider as income in

the sense of ordinary meaning4. The assesse have claimed that the money received was a form

of gift. According to commissioner of taxation, the court held that the received money would

3 Lam, Dung, and Whitney, Alex. “Taxation and Property: Practical Aspects of the New

Foreign Resident CGT Witholding Tax.” LSJ: Law Society of NSW Journal, vol. 3, no. 3,

2016, pp. 84–85.

4 Nethercott, et al. Australian Taxation Study Manual : Questions and Suggested Solutions.

26th ed., Oxford University Press, 2016.

5TAXATION LAW

be consider as voluntary gift payment and so it will not be taken as income which will be

taxable.

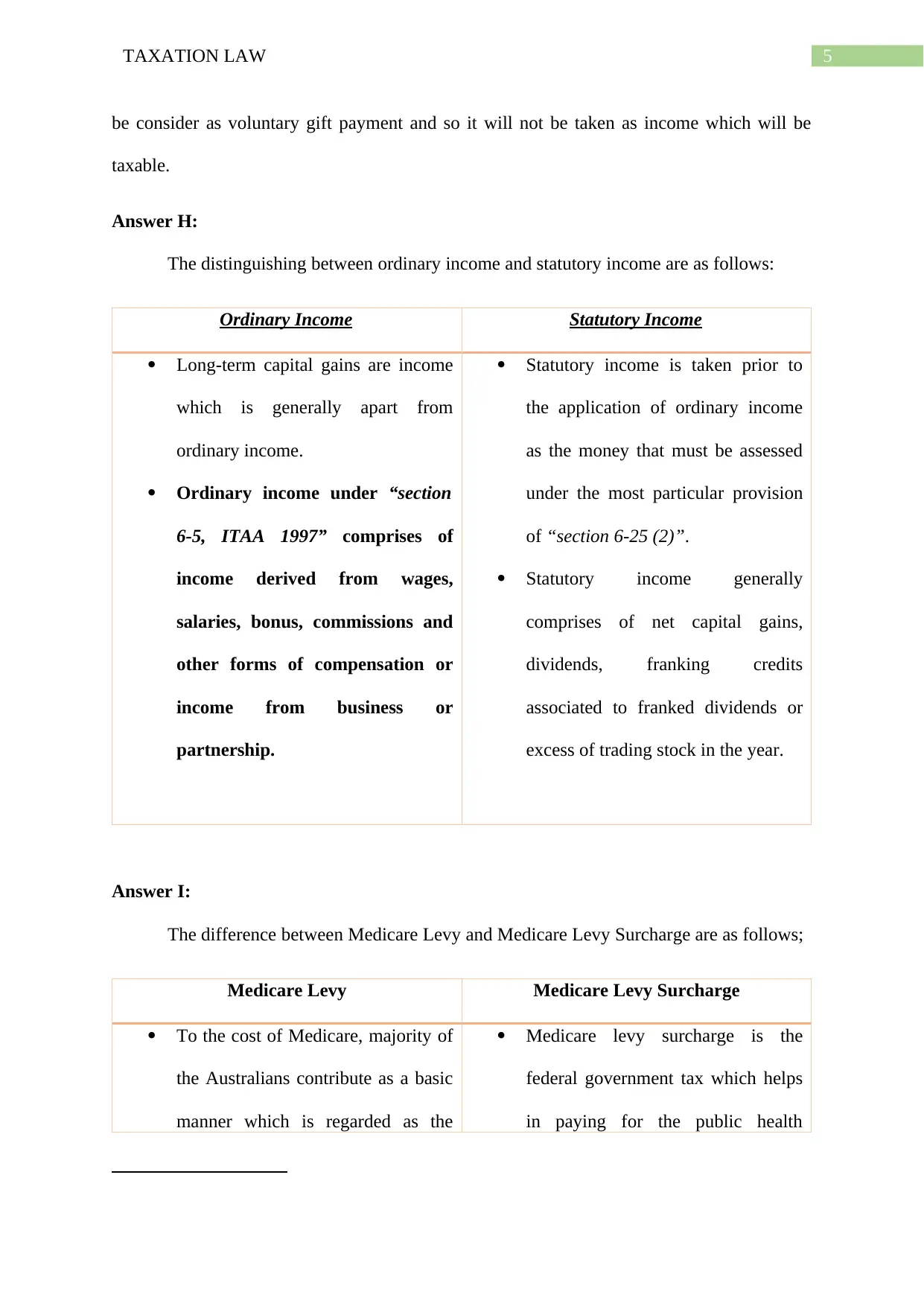

Answer H:

The distinguishing between ordinary income and statutory income are as follows:

Ordinary Income Statutory Income

Long-term capital gains are income

which is generally apart from

ordinary income.

Ordinary income under “section

6-5, ITAA 1997” comprises of

income derived from wages,

salaries, bonus, commissions and

other forms of compensation or

income from business or

partnership.

Statutory income is taken prior to

the application of ordinary income

as the money that must be assessed

under the most particular provision

of “section 6-25 (2)”.

Statutory income generally

comprises of net capital gains,

dividends, franking credits

associated to franked dividends or

excess of trading stock in the year.

Answer I:

The difference between Medicare Levy and Medicare Levy Surcharge are as follows;

Medicare Levy Medicare Levy Surcharge

To the cost of Medicare, majority of

the Australians contribute as a basic

manner which is regarded as the

Medicare levy surcharge is the

federal government tax which helps

in paying for the public health

be consider as voluntary gift payment and so it will not be taken as income which will be

taxable.

Answer H:

The distinguishing between ordinary income and statutory income are as follows:

Ordinary Income Statutory Income

Long-term capital gains are income

which is generally apart from

ordinary income.

Ordinary income under “section

6-5, ITAA 1997” comprises of

income derived from wages,

salaries, bonus, commissions and

other forms of compensation or

income from business or

partnership.

Statutory income is taken prior to

the application of ordinary income

as the money that must be assessed

under the most particular provision

of “section 6-25 (2)”.

Statutory income generally

comprises of net capital gains,

dividends, franking credits

associated to franked dividends or

excess of trading stock in the year.

Answer I:

The difference between Medicare Levy and Medicare Levy Surcharge are as follows;

Medicare Levy Medicare Levy Surcharge

To the cost of Medicare, majority of

the Australians contribute as a basic

manner which is regarded as the

Medicare levy surcharge is the

federal government tax which helps

in paying for the public health

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Medicare Levy.

Medicare Levy is applicable at a rate

2% on taxable income when an

individual earn higher than $27,069

in the current financial year5.

system.

The Medicare Levy Surcharge is

paid by the single individuals that

earn more than $90,000 in a year or

by couples or families that have the

combined earnings of $180,000 a

year.

Answer to question 2:

The term “usual place of abode” should not be taken as having same sense as term

“permanent place of abode”. The word usual and abode must be interpreted based on their

regular and normal senses. The query of “usual place of abode” is based on question of fact.

Usually the word is considered as the customary abode or it is usually used when a person is

actually existent in the state. An individual’s place of abode should be fixed but should

display the qualities of the place of dwelling or the residence to live in contrast with an

overnight, weekly or monthly lodging of a traveller6. An individual “usual place of abode”

should be permanent but it should define the quality of dwelling in contrary to weekly basis,

overnight or monthly housing of a traveller.

If a assesse have “usual place of adobe” at Australia and has no fixed dwelling outside

the country but visit country to country or migrating constantly in the domestic zone or the

5 Nethercott, Les., and G. L. Shaw. Australian Taxation Study Manual : Questions and

Suggested Solutions. 10th ed., CCH Australia, 2016.

6 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

Medicare Levy.

Medicare Levy is applicable at a rate

2% on taxable income when an

individual earn higher than $27,069

in the current financial year5.

system.

The Medicare Levy Surcharge is

paid by the single individuals that

earn more than $90,000 in a year or

by couples or families that have the

combined earnings of $180,000 a

year.

Answer to question 2:

The term “usual place of abode” should not be taken as having same sense as term

“permanent place of abode”. The word usual and abode must be interpreted based on their

regular and normal senses. The query of “usual place of abode” is based on question of fact.

Usually the word is considered as the customary abode or it is usually used when a person is

actually existent in the state. An individual’s place of abode should be fixed but should

display the qualities of the place of dwelling or the residence to live in contrast with an

overnight, weekly or monthly lodging of a traveller6. An individual “usual place of abode”

should be permanent but it should define the quality of dwelling in contrary to weekly basis,

overnight or monthly housing of a traveller.

If a assesse have “usual place of adobe” at Australia and has no fixed dwelling outside

the country but visit country to country or migrating constantly in the domestic zone or the

5 Nethercott, Les., and G. L. Shaw. Australian Taxation Study Manual : Questions and

Suggested Solutions. 10th ed., CCH Australia, 2016.

6 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

relation to the specific place in overseas, they the dwelling will not be permanent. In such

situation it should be considered that the assesse would not consider to have adopted the

dwelling of their self-choice or “permanent place of abode” outside the Australia7.

On the other hand, the word “permanent place of abode” specifies that an individual

has their residence in Australia. As per the “subparagraph (a)(i)” the definition of “resident”

needs the tax officer to be content that the person’s permanent place of abode is not out of

Australia8. The word “place of abode” signifies that assesse has the residence where an

individual resides with their family and sleeps at night. The court in “Levene v IRC (1928)”

stated that an individual’s “place of abode” represents a person’s place of dwelling or the

physical environments in which a person lives.

According to court in the leading case of “FCT v Applegate (1979)” held that the

taxpayer whose residence was in Australia, was directed by his company to set up an office

branch in Vila, New Hebrides. The law court of Australia stated that the taxpayer had the

permanent place of abode outside Australia and hence he was treated as non-resident in the

income year. While in another case of “FCT v Jenkins (1982)” it involved the bank officer

that was relocated to New Hebrides for 3 years and returned following 18 months due to ill-

health9. The Supreme Court of Queensland held that taxpayer had the “permanent place of

7 Kenny, Paul, et al. Australian Tax 2016. 2016.

8 Clark, William, and Regan Maas. “Spatial Mobility and Opportunity in Australia:

Residential Selection and Neighbourhood Connections.” Urban Studies, vol. 53, no. 6, 2016,

pp. 1317–1331.

9 Kenny, Paul. LexisNexis Concise Tax Legislation 2016.

relation to the specific place in overseas, they the dwelling will not be permanent. In such

situation it should be considered that the assesse would not consider to have adopted the

dwelling of their self-choice or “permanent place of abode” outside the Australia7.

On the other hand, the word “permanent place of abode” specifies that an individual

has their residence in Australia. As per the “subparagraph (a)(i)” the definition of “resident”

needs the tax officer to be content that the person’s permanent place of abode is not out of

Australia8. The word “place of abode” signifies that assesse has the residence where an

individual resides with their family and sleeps at night. The court in “Levene v IRC (1928)”

stated that an individual’s “place of abode” represents a person’s place of dwelling or the

physical environments in which a person lives.

According to court in the leading case of “FCT v Applegate (1979)” held that the

taxpayer whose residence was in Australia, was directed by his company to set up an office

branch in Vila, New Hebrides. The law court of Australia stated that the taxpayer had the

permanent place of abode outside Australia and hence he was treated as non-resident in the

income year. While in another case of “FCT v Jenkins (1982)” it involved the bank officer

that was relocated to New Hebrides for 3 years and returned following 18 months due to ill-

health9. The Supreme Court of Queensland held that taxpayer had the “permanent place of

7 Kenny, Paul, et al. Australian Tax 2016. 2016.

8 Clark, William, and Regan Maas. “Spatial Mobility and Opportunity in Australia:

Residential Selection and Neighbourhood Connections.” Urban Studies, vol. 53, no. 6, 2016,

pp. 1317–1331.

9 Kenny, Paul. LexisNexis Concise Tax Legislation 2016.

8TAXATION LAW

abode” out of Australia throughout the period he was foreign even though he did not have

any kind of physical time to live in New Hebrides. As evident from the Applegate and

Jenkins that an individual’s “permanent place of abode” cannot be determined by applying

any kind of speedy rules. As per the discussion a person must be content that if Australia is

not their usual place of adobe, while the first statutory test (domicile) need a person to be

contented that their permanent place of abode is out of Australia10.

Answer to Question 3:

HECS-HELP: $850:

As described by the ATO, acceptable income Tax deduction is allowed to taxpayer for

certain types of expenditure that is related to self-education provided that the expenses are

occurred in relevant calculated earnings of the taxpayers. As per the ATO, the individual

taxpayer who sustains expenditure on self-education and satisfies the eligibility criteria then

some particular expenditure like Fee-Help, Vet or the loan of a student that is paid inside the

HECS-HELP is not applicable for deduction. In the same way the expense of $850 occurred

for HECS-HELP is a non-deductible expenditure.

Travel – work to university $110

The self-education expenditure that occurs are normally deductible but the

expenditure for maintaining and increasing the skills of taxpayers working in their present

field for increasing their future income.

As per “FCT v Finn 1961” those who are employed as architect by the WA

Government are allowed to deduct permissible income tax for the travelling expenses for a

10 Anderson, Colin, et al. “The Australian Taxation Office - What Role Does It Play in Anti-

Phoenix Activity?” Insolvency Law Journal, vol. 24, no. 2, 2016, pp. 127–140.

abode” out of Australia throughout the period he was foreign even though he did not have

any kind of physical time to live in New Hebrides. As evident from the Applegate and

Jenkins that an individual’s “permanent place of abode” cannot be determined by applying

any kind of speedy rules. As per the discussion a person must be content that if Australia is

not their usual place of adobe, while the first statutory test (domicile) need a person to be

contented that their permanent place of abode is out of Australia10.

Answer to Question 3:

HECS-HELP: $850:

As described by the ATO, acceptable income Tax deduction is allowed to taxpayer for

certain types of expenditure that is related to self-education provided that the expenses are

occurred in relevant calculated earnings of the taxpayers. As per the ATO, the individual

taxpayer who sustains expenditure on self-education and satisfies the eligibility criteria then

some particular expenditure like Fee-Help, Vet or the loan of a student that is paid inside the

HECS-HELP is not applicable for deduction. In the same way the expense of $850 occurred

for HECS-HELP is a non-deductible expenditure.

Travel – work to university $110

The self-education expenditure that occurs are normally deductible but the

expenditure for maintaining and increasing the skills of taxpayers working in their present

field for increasing their future income.

As per “FCT v Finn 1961” those who are employed as architect by the WA

Government are allowed to deduct permissible income tax for the travelling expenses for a

10 Anderson, Colin, et al. “The Australian Taxation Office - What Role Does It Play in Anti-

Phoenix Activity?” Insolvency Law Journal, vol. 24, no. 2, 2016, pp. 127–140.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

year to study architecture by travelling overseas11. Court also held that tour is a natural and

relevant for the employment of taxpayer.

Travelling from work to university are currently is an allowable deduction under

“section 8-1, ITAA 1997” as the travelling expenditure are natural and relevant.

Books $200:

Expenditure related to self-education are mainly study materials, textbooks,

stationery, calculators and related items for improving the future strength and earning

capacities of the taxpayers are allowed for deduction under “section 8-1,ITAA 1997”. A

general practicing dentist is also permissible for deduction of expenditure done for self-

education.

Under “section 8-, ITAA 1997” an accountant who incurred expenses for books will

also be allowed for deduction as this expenses are for improving the future promotion and

earning capacity of the taxpayer.

Childcare during her evening classes $80:

According to the “section 8-1 (2)(b), ITAA 1997” the expenses that are incurred in

domestic area are not allowed for deduction as it does not meet the standard stated. In “FCT v

Lodge 1972” case court did not allowed deduction to taxpayers as the expenses occurred for

child care and the expenses are not for income generation activity of taxpayer.

Repair to her fridge at home $250:

11 Trakman, Leon. "Domicile of choice in English law: an Achilles heel?." Journal of Private

International Law 11.2 (2015): 317-343.

year to study architecture by travelling overseas11. Court also held that tour is a natural and

relevant for the employment of taxpayer.

Travelling from work to university are currently is an allowable deduction under

“section 8-1, ITAA 1997” as the travelling expenditure are natural and relevant.

Books $200:

Expenditure related to self-education are mainly study materials, textbooks,

stationery, calculators and related items for improving the future strength and earning

capacities of the taxpayers are allowed for deduction under “section 8-1,ITAA 1997”. A

general practicing dentist is also permissible for deduction of expenditure done for self-

education.

Under “section 8-, ITAA 1997” an accountant who incurred expenses for books will

also be allowed for deduction as this expenses are for improving the future promotion and

earning capacity of the taxpayer.

Childcare during her evening classes $80:

According to the “section 8-1 (2)(b), ITAA 1997” the expenses that are incurred in

domestic area are not allowed for deduction as it does not meet the standard stated. In “FCT v

Lodge 1972” case court did not allowed deduction to taxpayers as the expenses occurred for

child care and the expenses are not for income generation activity of taxpayer.

Repair to her fridge at home $250:

11 Trakman, Leon. "Domicile of choice in English law: an Achilles heel?." Journal of Private

International Law 11.2 (2015): 317-343.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Under “section 8-1 (2)(b), ITAA 1997” an individual taxpayer is not allowed to claim

deduction for outgoing which is of domestic or private in nature. In case “Lunney v FCT

1958” court held that it is important to determine the outgoings to know the deduction for

perquisites. Under “section 8-1 (2)(b), ITAA 1997” repairs of fridge at home for $250 will

not be allowed as deduction as the expenses are private and domestic in nature and it is not a

perquisites in source of taxable income12.

Black trouser and shirt required to be worn at office $145:

According to the “section 8-1, ITAA 1997” cost of purchasing an ordinary item like

cloths, suits are not permitted as deduction. In case “Mansfield v FCT 1996” court held that

the general expenses on ordinary articles are not to be treated as deductible although the

expenses are required to maintain a particular appearance in job or profession13.

Expenses incurred for buying a black trouser and a shirt is not allowed for deduction

irrespective of the fact that it is necessary to maintain a suitable office appearance.

Legal expenses occurred in writing up a new employment with a new employer $300:

Expenses incurred in the course of getting a new employment is also not considered in

the course of taxable income. In case “Maddalena v FCT 1971 it was held that expenses

incurred for obtaining new employment is not allowed as deduction as it occurred point is

too soon.

12 Sharkey, Nolan. "Departing Australia: a complex tax situation with possible benefits and

hidden traps." Tax Specialist 19.5 (2016): 180.

13 Main, Jim. “Taxation: Accountants and Lawyers: Friends or Adversaries?” LSJ: Law

Society of NSW Journal, no. 41, 2018, p. 78.

Under “section 8-1 (2)(b), ITAA 1997” an individual taxpayer is not allowed to claim

deduction for outgoing which is of domestic or private in nature. In case “Lunney v FCT

1958” court held that it is important to determine the outgoings to know the deduction for

perquisites. Under “section 8-1 (2)(b), ITAA 1997” repairs of fridge at home for $250 will

not be allowed as deduction as the expenses are private and domestic in nature and it is not a

perquisites in source of taxable income12.

Black trouser and shirt required to be worn at office $145:

According to the “section 8-1, ITAA 1997” cost of purchasing an ordinary item like

cloths, suits are not permitted as deduction. In case “Mansfield v FCT 1996” court held that

the general expenses on ordinary articles are not to be treated as deductible although the

expenses are required to maintain a particular appearance in job or profession13.

Expenses incurred for buying a black trouser and a shirt is not allowed for deduction

irrespective of the fact that it is necessary to maintain a suitable office appearance.

Legal expenses occurred in writing up a new employment with a new employer $300:

Expenses incurred in the course of getting a new employment is also not considered in

the course of taxable income. In case “Maddalena v FCT 1971 it was held that expenses

incurred for obtaining new employment is not allowed as deduction as it occurred point is

too soon.

12 Sharkey, Nolan. "Departing Australia: a complex tax situation with possible benefits and

hidden traps." Tax Specialist 19.5 (2016): 180.

13 Main, Jim. “Taxation: Accountants and Lawyers: Friends or Adversaries?” LSJ: Law

Society of NSW Journal, no. 41, 2018, p. 78.

11TAXATION LAW

Answer to question 4:

Answer to A:

F1 event of CGT take place when a party gets grant by taxpayer to extend or renew

the lease period which was previously owned by the taxpayer. Under CGT event F1 50 %

CGT discount is not allowed14. When john leased his own land at a premium of $7000 for

seven years then a CGT event F1 occurred but john cannot get 50% CGT discount from the

CGT event.

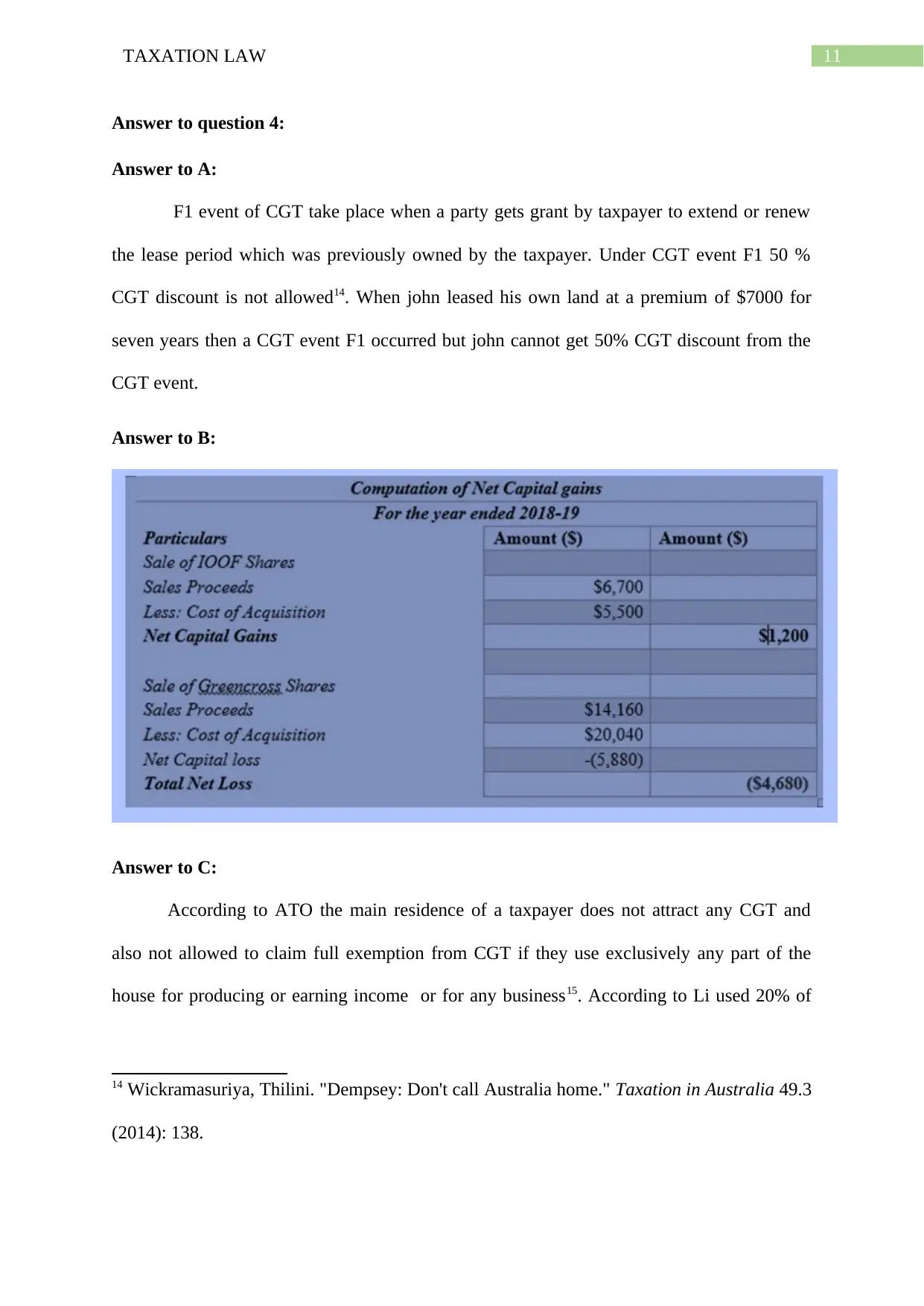

Answer to B:

Answer to C:

According to ATO the main residence of a taxpayer does not attract any CGT and

also not allowed to claim full exemption from CGT if they use exclusively any part of the

house for producing or earning income or for any business15. According to Li used 20% of

14 Wickramasuriya, Thilini. "Dempsey: Don't call Australia home." Taxation in Australia 49.3

(2014): 138.

Answer to question 4:

Answer to A:

F1 event of CGT take place when a party gets grant by taxpayer to extend or renew

the lease period which was previously owned by the taxpayer. Under CGT event F1 50 %

CGT discount is not allowed14. When john leased his own land at a premium of $7000 for

seven years then a CGT event F1 occurred but john cannot get 50% CGT discount from the

CGT event.

Answer to B:

Answer to C:

According to ATO the main residence of a taxpayer does not attract any CGT and

also not allowed to claim full exemption from CGT if they use exclusively any part of the

house for producing or earning income or for any business15. According to Li used 20% of

14 Wickramasuriya, Thilini. "Dempsey: Don't call Australia home." Taxation in Australia 49.3

(2014): 138.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.