LAWS20060: Taxation Law of Australia Individual Assignment 2019

VerifiedAdded on 2023/01/16

|16

|3653

|22

Homework Assignment

AI Summary

This document provides a comprehensive solution to a Taxation Law assignment, specifically for the LAWS20060 course. The assignment covers various aspects of Australian taxation law, including capital gains tax (CGT), tax deductions, and income tax calculations. The solution addresses multiple questions, offering detailed explanations, case analysis, and references to relevant legislation and rulings. It explores topics such as asset effective life, tax offsets, taxation of Australian residents, personal use assets, CGT events, and the calculation of taxable income. Furthermore, it delves into deductions for business expenses, child care, and stolen goods, while also examining CGT implications for leases, land transactions, and main residences. The document concludes with a discussion on the taxability of prize winnings and the application of relevant laws and provisions.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note

Taxation Law

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to question 1:................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:..............................................................................................................................3

Answer C:..............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:..............................................................................................................................4

Answer F:..............................................................................................................................4

Answer G:..............................................................................................................................4

Answer to H:..........................................................................................................................5

Answer to I:...........................................................................................................................5

Answer to question 2:................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:..............................................................................................................................6

Answer C:..............................................................................................................................7

Answer D:..............................................................................................................................7

Answer E:..............................................................................................................................8

Answer to Question 3................................................................................................................8

Answer A...............................................................................................................................8

Answer B...............................................................................................................................9

TAXATION LAW

Table of Contents

Answer to question 1:................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:..............................................................................................................................3

Answer C:..............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:..............................................................................................................................4

Answer F:..............................................................................................................................4

Answer G:..............................................................................................................................4

Answer to H:..........................................................................................................................5

Answer to I:...........................................................................................................................5

Answer to question 2:................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:..............................................................................................................................6

Answer C:..............................................................................................................................7

Answer D:..............................................................................................................................7

Answer E:..............................................................................................................................8

Answer to Question 3................................................................................................................8

Answer A...............................................................................................................................8

Answer B...............................................................................................................................9

2

TAXATION LAW

Answer C...............................................................................................................................9

Answer D.............................................................................................................................10

Answer to Question 4..............................................................................................................10

Answer A.............................................................................................................................10

Answer B.............................................................................................................................11

Answer C.............................................................................................................................11

Answer D.............................................................................................................................12

Answer E.............................................................................................................................12

Answer to Question 5..............................................................................................................13

Issues...................................................................................................................................13

Laws....................................................................................................................................13

Application..........................................................................................................................14

Conclusion...........................................................................................................................14

Reference.................................................................................................................................15

TAXATION LAW

Answer C...............................................................................................................................9

Answer D.............................................................................................................................10

Answer to Question 4..............................................................................................................10

Answer A.............................................................................................................................10

Answer B.............................................................................................................................11

Answer C.............................................................................................................................11

Answer D.............................................................................................................................12

Answer E.............................................................................................................................12

Answer to Question 5..............................................................................................................13

Issues...................................................................................................................................13

Laws....................................................................................................................................13

Application..........................................................................................................................14

Conclusion...........................................................................................................................14

Reference.................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

Answer to question 1:

Answer A:

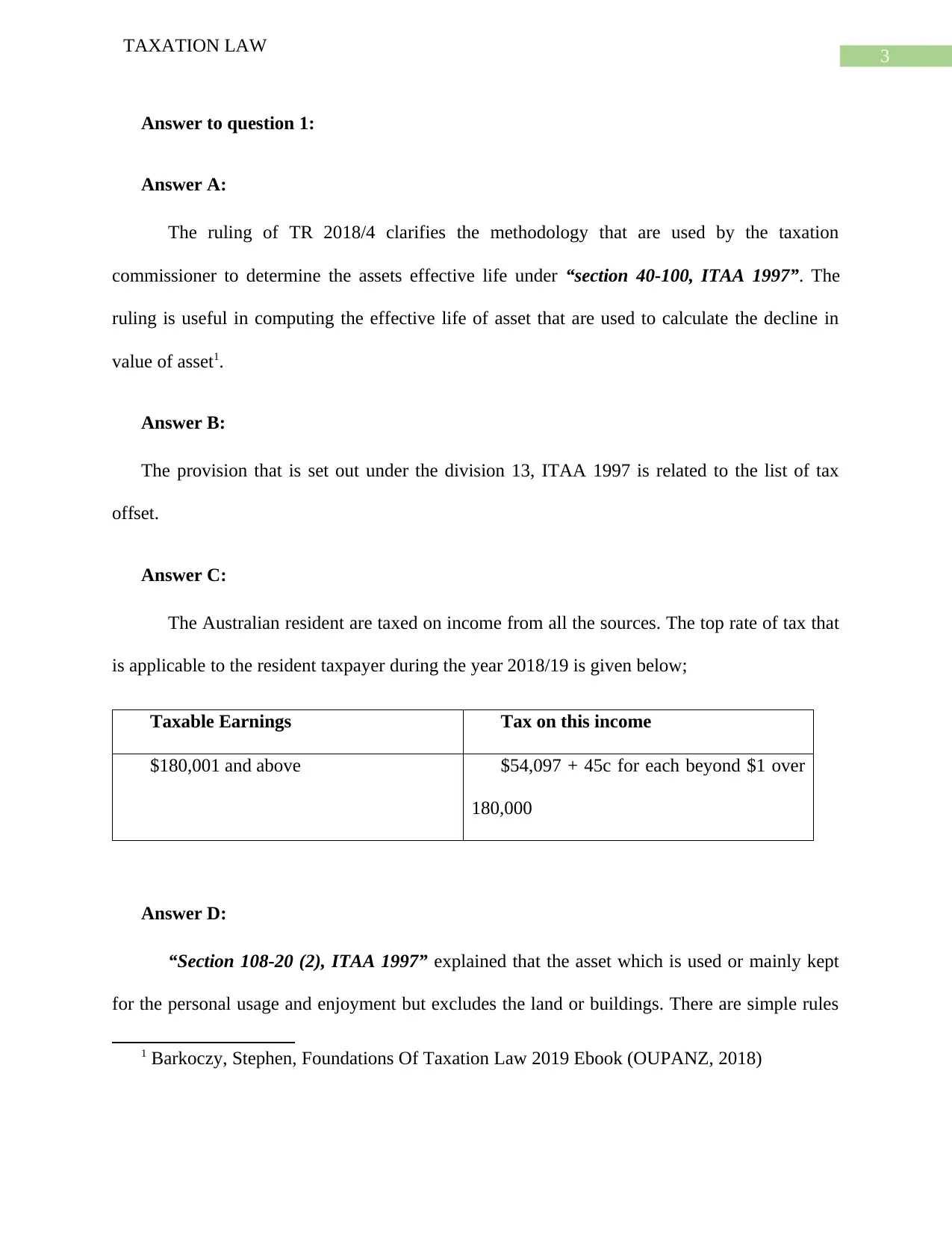

The ruling of TR 2018/4 clarifies the methodology that are used by the taxation

commissioner to determine the assets effective life under “section 40-100, ITAA 1997”. The

ruling is useful in computing the effective life of asset that are used to calculate the decline in

value of asset1.

Answer B:

The provision that is set out under the division 13, ITAA 1997 is related to the list of tax

offset.

Answer C:

The Australian resident are taxed on income from all the sources. The top rate of tax that

is applicable to the resident taxpayer during the year 2018/19 is given below;

Taxable Earnings Tax on this income

$180,001 and above $54,097 + 45c for each beyond $1 over

180,000

Answer D:

“Section 108-20 (2), ITAA 1997” explained that the asset which is used or mainly kept

for the personal usage and enjoyment but excludes the land or buildings. There are simple rules

1 Barkoczy, Stephen, Foundations Of Taxation Law 2019 Ebook (OUPANZ, 2018)

TAXATION LAW

Answer to question 1:

Answer A:

The ruling of TR 2018/4 clarifies the methodology that are used by the taxation

commissioner to determine the assets effective life under “section 40-100, ITAA 1997”. The

ruling is useful in computing the effective life of asset that are used to calculate the decline in

value of asset1.

Answer B:

The provision that is set out under the division 13, ITAA 1997 is related to the list of tax

offset.

Answer C:

The Australian resident are taxed on income from all the sources. The top rate of tax that

is applicable to the resident taxpayer during the year 2018/19 is given below;

Taxable Earnings Tax on this income

$180,001 and above $54,097 + 45c for each beyond $1 over

180,000

Answer D:

“Section 108-20 (2), ITAA 1997” explained that the asset which is used or mainly kept

for the personal usage and enjoyment but excludes the land or buildings. There are simple rules

1 Barkoczy, Stephen, Foundations Of Taxation Law 2019 Ebook (OUPANZ, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

that are applicable to the personal use assets2. This includes that capital gains should be ignored

for personal use assets when it is purchased for less than $10,000 under section 118-10 (3),

ITAA 1997.

Answer E:

Under the section 104-15, ITAA 1997 CGT event B1 is mainly associated with the

enjoyment and use prior to the title passes. Accordingly, CGT event B1 is triggered when an

individual enters into the settlement with the one more entity, based on which;

a. The right of using and enjoying the title of CGT asset that under the ownership of a

person is passed to other entity;

b. The title of the asset might be passed to other entity before or prior to the agreement.

Answer F:

As per the section 4-10, ITAA 1997 it explains the method of working out the tax a

person should pay. The section requires a person to work out the income for the financial year by

using the below stated formula;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer G:

The judgement given in “FC of T v Day 2008 ATC 20-064” held that the legal

expenditure was not allowed for deductible purpose under the “section 8-1, ITAA 1997” because

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of

Business Taxation

TAXATION LAW

that are applicable to the personal use assets2. This includes that capital gains should be ignored

for personal use assets when it is purchased for less than $10,000 under section 118-10 (3),

ITAA 1997.

Answer E:

Under the section 104-15, ITAA 1997 CGT event B1 is mainly associated with the

enjoyment and use prior to the title passes. Accordingly, CGT event B1 is triggered when an

individual enters into the settlement with the one more entity, based on which;

a. The right of using and enjoying the title of CGT asset that under the ownership of a

person is passed to other entity;

b. The title of the asset might be passed to other entity before or prior to the agreement.

Answer F:

As per the section 4-10, ITAA 1997 it explains the method of working out the tax a

person should pay. The section requires a person to work out the income for the financial year by

using the below stated formula;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer G:

The judgement given in “FC of T v Day 2008 ATC 20-064” held that the legal

expenditure was not allowed for deductible purpose under the “section 8-1, ITAA 1997” because

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of

Business Taxation

5

TAXATION LAW

the legal expenditure was not allowed for deducible purpose since the conduct and the subject of

charges consisted of the acts which were unrelated to the duties to be carried out by the

respondent in the course of deriving taxable income3.

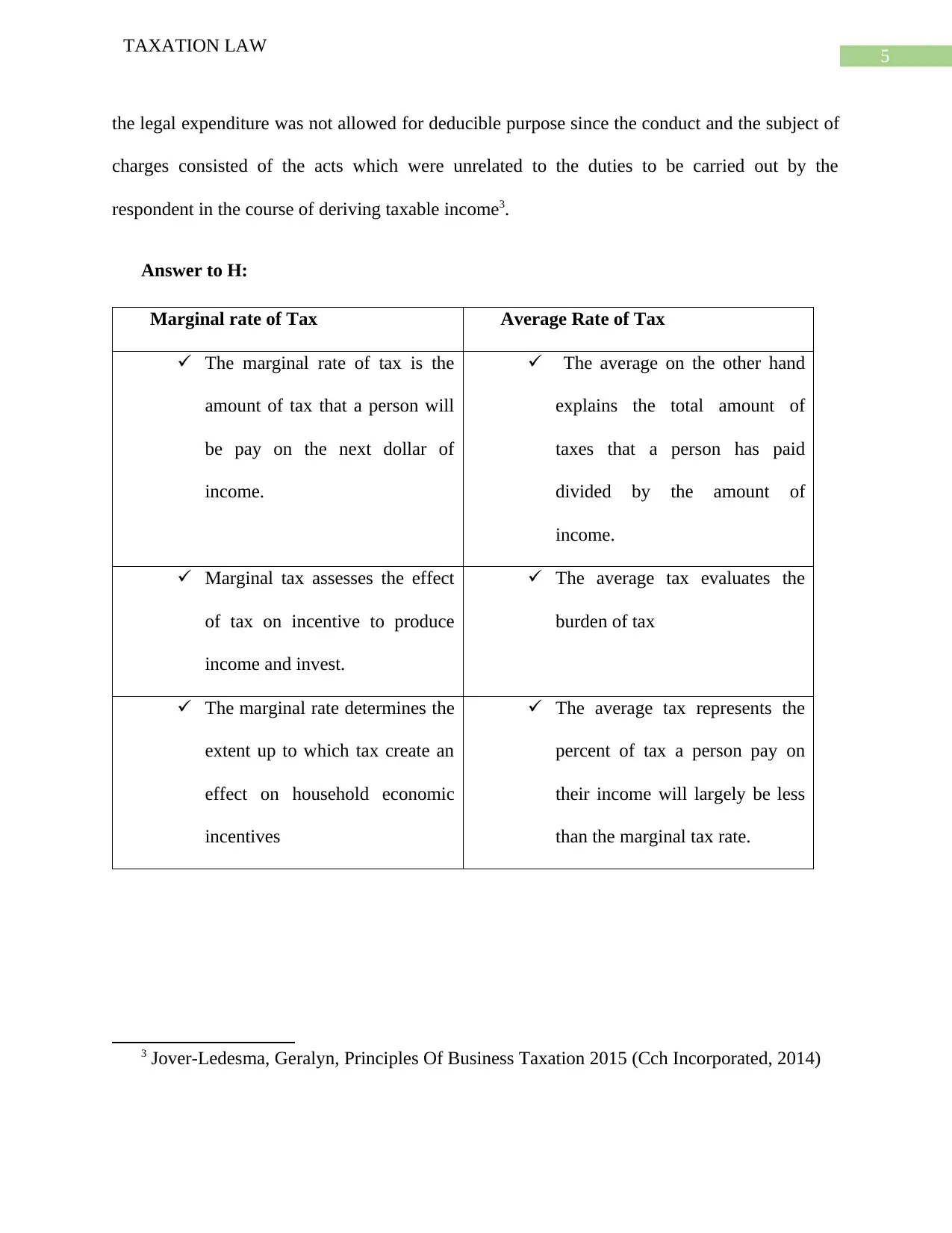

Answer to H:

Marginal rate of Tax Average Rate of Tax

The marginal rate of tax is the

amount of tax that a person will

be pay on the next dollar of

income.

The average on the other hand

explains the total amount of

taxes that a person has paid

divided by the amount of

income.

Marginal tax assesses the effect

of tax on incentive to produce

income and invest.

The average tax evaluates the

burden of tax

The marginal rate determines the

extent up to which tax create an

effect on household economic

incentives

The average tax represents the

percent of tax a person pay on

their income will largely be less

than the marginal tax rate.

3 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

TAXATION LAW

the legal expenditure was not allowed for deducible purpose since the conduct and the subject of

charges consisted of the acts which were unrelated to the duties to be carried out by the

respondent in the course of deriving taxable income3.

Answer to H:

Marginal rate of Tax Average Rate of Tax

The marginal rate of tax is the

amount of tax that a person will

be pay on the next dollar of

income.

The average on the other hand

explains the total amount of

taxes that a person has paid

divided by the amount of

income.

Marginal tax assesses the effect

of tax on incentive to produce

income and invest.

The average tax evaluates the

burden of tax

The marginal rate determines the

extent up to which tax create an

effect on household economic

incentives

The average tax represents the

percent of tax a person pay on

their income will largely be less

than the marginal tax rate.

3 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

Answer to I:

The consumption can be defined as the tax on the spending by the consumers namely the

sales tax or the value added tax. This tax is generally levied on the consumption expenditure

such as goods and services. The tax base of consumption tax is the amount of money that is

spend on the consumption and this tax is generally indirect tax.

Answer to question 2:

Answer A:

“Section 8-1, ITAA 1997” permits taxpayers to deduct from their taxable income any

amount of loss or outgoing till the extent that it is occurred in performing the business activities

for obtaining assessable income. As held in “Amalgamated Zinc Ltd v FCT (1935)” expenses

are deductible occurred in producing taxable income4.

Brett took out the loan so that he can pay the outstanding employee wages. Brett occurred

interest on loan for the loan taken out paying employee wages. Mentioning “Amalgamated Zinc

Ltd v FCT (1935)” the interest on occurred by Brett is in the business course of producing

taxable income. Therefore, it is allowed as deduction under “Section 8-1, ITAA 1997”.

Answer B:

Where the deductibility of dual expenditure is involved a loss or outgoing is only allowed

for deduction under “section 8-1, ITAA 1997” by apportioning the expenses that is occurred in

producing taxable income. In “Ronpibon Tin v FCT (1949)” it is necessary to apportionment of

expenses that involves dual purpose.

4 Sadiq, Kerrie, Principles Of Taxation Law 2014

TAXATION LAW

Answer to I:

The consumption can be defined as the tax on the spending by the consumers namely the

sales tax or the value added tax. This tax is generally levied on the consumption expenditure

such as goods and services. The tax base of consumption tax is the amount of money that is

spend on the consumption and this tax is generally indirect tax.

Answer to question 2:

Answer A:

“Section 8-1, ITAA 1997” permits taxpayers to deduct from their taxable income any

amount of loss or outgoing till the extent that it is occurred in performing the business activities

for obtaining assessable income. As held in “Amalgamated Zinc Ltd v FCT (1935)” expenses

are deductible occurred in producing taxable income4.

Brett took out the loan so that he can pay the outstanding employee wages. Brett occurred

interest on loan for the loan taken out paying employee wages. Mentioning “Amalgamated Zinc

Ltd v FCT (1935)” the interest on occurred by Brett is in the business course of producing

taxable income. Therefore, it is allowed as deduction under “Section 8-1, ITAA 1997”.

Answer B:

Where the deductibility of dual expenditure is involved a loss or outgoing is only allowed

for deduction under “section 8-1, ITAA 1997” by apportioning the expenses that is occurred in

producing taxable income. In “Ronpibon Tin v FCT (1949)” it is necessary to apportionment of

expenses that involves dual purpose.

4 Sadiq, Kerrie, Principles Of Taxation Law 2014

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

A dual purpose mobile phone bill was occurred by Julie that comprised of 60% for work

related calls while 40% was associated to private purpose. Reciting “Ronpibon Tin v FCT

(1949)” only 60% of the mobile phone bill is allowed for deduction purpose under “section 8-1,

ITAA 1997”.

Answer C:

No general deduction is allowable for the child care expenses under “section 8-1, ITAA

1997”. As held in “Lodge v FCT (1972)” child care expenses that was incurred by the taxpayer

was denied deduction since the expenses were not relevant nor incidental in producing taxable

income5.

Sally reports the babysitter expenses of $1,200 so that she can go to work. Denoting

decision of court in “Lodge v FCT (1972)” the child care expenses is not allowed for deduction

under “section 8-1, ITAA 1997” since the expenses were not relevant nor incidental in

producing taxable income.

Answer D:

The general provision of “section 8-1, ITAA 1997” is applied for both the loss and

outgoings. As held in “Charles Moore & Co Pty Ltd v FCT (1956)” deduction was allowed to

taxpayer for depletion in the financial position due to theft of money from the business.

The taxpayer here Sally reports a loss of $20,000 as the goods were stolen by his long

term employee from his business. Quoting “Charles Moore & Co Pty Ltd v FCT (1956)”

5 Stevens, Matthew A, Taxation Of Financial Products And Transactions, 2014

TAXATION LAW

A dual purpose mobile phone bill was occurred by Julie that comprised of 60% for work

related calls while 40% was associated to private purpose. Reciting “Ronpibon Tin v FCT

(1949)” only 60% of the mobile phone bill is allowed for deduction purpose under “section 8-1,

ITAA 1997”.

Answer C:

No general deduction is allowable for the child care expenses under “section 8-1, ITAA

1997”. As held in “Lodge v FCT (1972)” child care expenses that was incurred by the taxpayer

was denied deduction since the expenses were not relevant nor incidental in producing taxable

income5.

Sally reports the babysitter expenses of $1,200 so that she can go to work. Denoting

decision of court in “Lodge v FCT (1972)” the child care expenses is not allowed for deduction

under “section 8-1, ITAA 1997” since the expenses were not relevant nor incidental in

producing taxable income.

Answer D:

The general provision of “section 8-1, ITAA 1997” is applied for both the loss and

outgoings. As held in “Charles Moore & Co Pty Ltd v FCT (1956)” deduction was allowed to

taxpayer for depletion in the financial position due to theft of money from the business.

The taxpayer here Sally reports a loss of $20,000 as the goods were stolen by his long

term employee from his business. Quoting “Charles Moore & Co Pty Ltd v FCT (1956)”

5 Stevens, Matthew A, Taxation Of Financial Products And Transactions, 2014

8

TAXATION LAW

deduction for stolen goods is allowed to Sally under “section 8-1, ITAA 1997” as it amounts to

depletion in the financial position due to theft of goods from the business.

Answer E:

The taxpayer is not allowed to claim deduction under “section 8-1, ITAA 1997” for

expenses that are considered preliminary to begin the income generating activities. As held in

“FCT v Maddalena (1971)” the expenditure that was occurred by taxpayer in travelling to the

second club for negotiating the contract were non-deductible because the expenses occurred at a

point too soon6.

Similarly, the expenses occurred in contesting the local council election and spending in the

big party election is considered preliminary to begin the income generating activities. Citing the

case of “FCT v Maddalena (1971)” the expenditure that was occurred by taxpayer in contesting

local council election is non-deductible under “section 8-1, ITAA 1997” because the expenses

occurred at a point too soon.

Answer to Question 3

Answer A

The provisions of capital gain taxes show that a “CGT event F2” is applicable when an

individual review, grants or extends long-term leases. As per the case which is provided in the

assessment, Andy is an owner of a land which he grants to Brain for a lease of five years and the

premium on the same is $ 5,000. This results in “CGT event F2” taking place and therefore

6 Weltman, Barbara, J.K. Lasser's Small Business Taxes 2014 (Wiley, 2014)

TAXATION LAW

deduction for stolen goods is allowed to Sally under “section 8-1, ITAA 1997” as it amounts to

depletion in the financial position due to theft of goods from the business.

Answer E:

The taxpayer is not allowed to claim deduction under “section 8-1, ITAA 1997” for

expenses that are considered preliminary to begin the income generating activities. As held in

“FCT v Maddalena (1971)” the expenditure that was occurred by taxpayer in travelling to the

second club for negotiating the contract were non-deductible because the expenses occurred at a

point too soon6.

Similarly, the expenses occurred in contesting the local council election and spending in the

big party election is considered preliminary to begin the income generating activities. Citing the

case of “FCT v Maddalena (1971)” the expenditure that was occurred by taxpayer in contesting

local council election is non-deductible under “section 8-1, ITAA 1997” because the expenses

occurred at a point too soon.

Answer to Question 3

Answer A

The provisions of capital gain taxes show that a “CGT event F2” is applicable when an

individual review, grants or extends long-term leases. As per the case which is provided in the

assessment, Andy is an owner of a land which he grants to Brain for a lease of five years and the

premium on the same is $ 5,000. This results in “CGT event F2” taking place and therefore

6 Weltman, Barbara, J.K. Lasser's Small Business Taxes 2014 (Wiley, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Andy would not be eligible for 50% CGT discount as the same is not available in case of “CGT

event F2”.

Answer B

As per the direction of Australian Tax office (ATO) “CGT event B1” occurs when a land is

acquired by a new owner. In details, the right of enjoyment and use of the land would be

considered to be viable if the ownership is acquired by the new owner along with the permit to

receive rents and profits associated with the land. As per the case, in exchange of $ 40,000 Farm

land an offer was provided of purchasing a 100-acre land which was of the sum of $ 800,000.

This resulted in attraction of CGT event B1 which has an eligibility of 50% CGT discount for the

transaction.

Answer C

The opinion which was given by ATO in case a taxpayer’s dwelling is the not the main

residence considering the full period of ownership and the same is used for generation of income

then in such a case partial residency exemption would be applicable to the taxpayer. The case

shows that a property was purchased by Jaime and Olivia which was rented for a two-year

period. The property was let out for generating income and was also utilized as main residence

until the same was sold off. The taxpayers would eligible for partial residency exemption for the

property. Therefore, Jaime and Olivia would be eligible for 50% CGT to ascertain the net

amount of capitals gains tax.

TAXATION LAW

Andy would not be eligible for 50% CGT discount as the same is not available in case of “CGT

event F2”.

Answer B

As per the direction of Australian Tax office (ATO) “CGT event B1” occurs when a land is

acquired by a new owner. In details, the right of enjoyment and use of the land would be

considered to be viable if the ownership is acquired by the new owner along with the permit to

receive rents and profits associated with the land. As per the case, in exchange of $ 40,000 Farm

land an offer was provided of purchasing a 100-acre land which was of the sum of $ 800,000.

This resulted in attraction of CGT event B1 which has an eligibility of 50% CGT discount for the

transaction.

Answer C

The opinion which was given by ATO in case a taxpayer’s dwelling is the not the main

residence considering the full period of ownership and the same is used for generation of income

then in such a case partial residency exemption would be applicable to the taxpayer. The case

shows that a property was purchased by Jaime and Olivia which was rented for a two-year

period. The property was let out for generating income and was also utilized as main residence

until the same was sold off. The taxpayers would eligible for partial residency exemption for the

property. Therefore, Jaime and Olivia would be eligible for 50% CGT to ascertain the net

amount of capitals gains tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

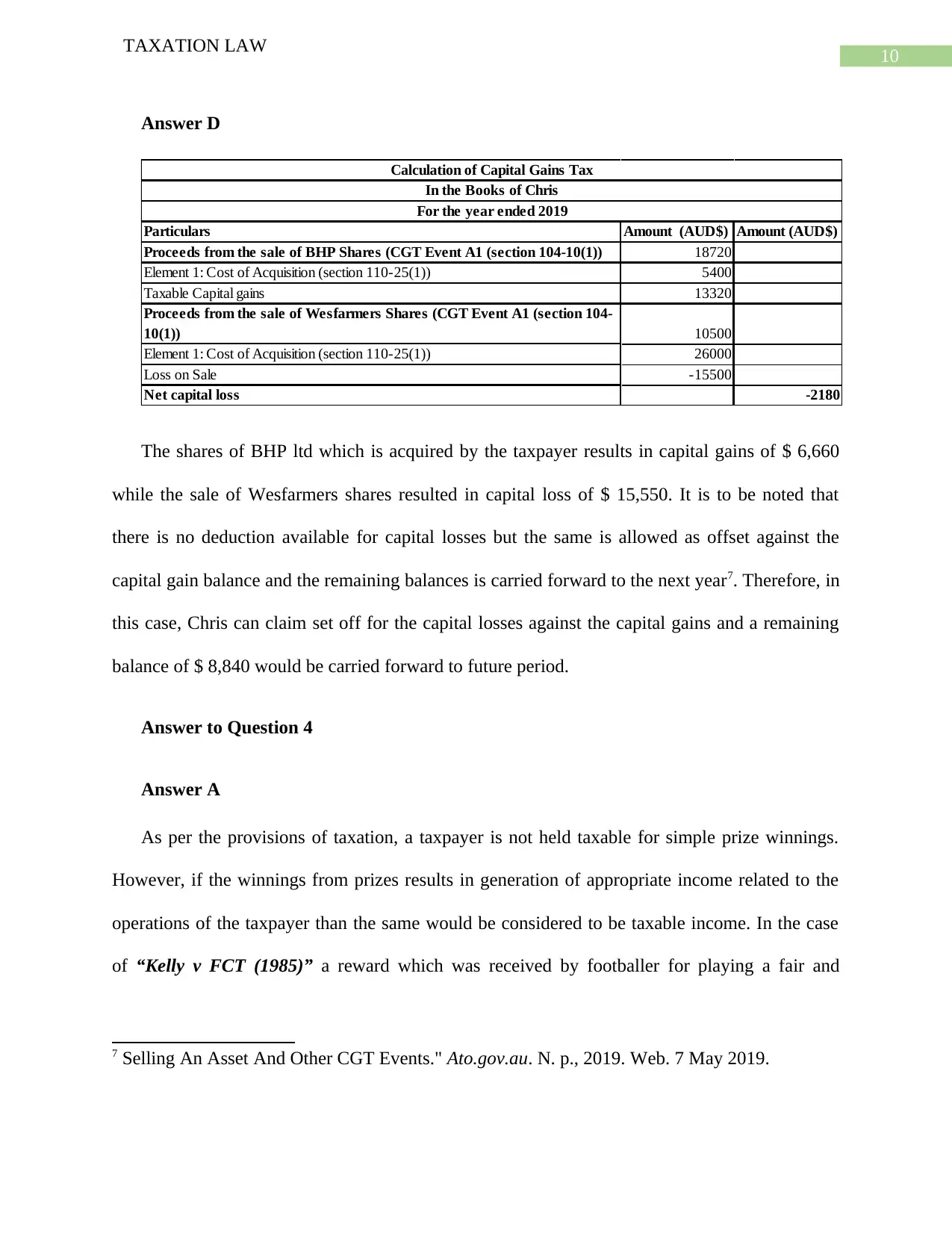

Answer D

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The shares of BHP ltd which is acquired by the taxpayer results in capital gains of $ 6,660

while the sale of Wesfarmers shares resulted in capital loss of $ 15,550. It is to be noted that

there is no deduction available for capital losses but the same is allowed as offset against the

capital gain balance and the remaining balances is carried forward to the next year7. Therefore, in

this case, Chris can claim set off for the capital losses against the capital gains and a remaining

balance of $ 8,840 would be carried forward to future period.

Answer to Question 4

Answer A

As per the provisions of taxation, a taxpayer is not held taxable for simple prize winnings.

However, if the winnings from prizes results in generation of appropriate income related to the

operations of the taxpayer than the same would be considered to be taxable income. In the case

of “Kelly v FCT (1985)” a reward which was received by footballer for playing a fair and

7 Selling An Asset And Other CGT Events." Ato.gov.au. N. p., 2019. Web. 7 May 2019.

TAXATION LAW

Answer D

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The shares of BHP ltd which is acquired by the taxpayer results in capital gains of $ 6,660

while the sale of Wesfarmers shares resulted in capital loss of $ 15,550. It is to be noted that

there is no deduction available for capital losses but the same is allowed as offset against the

capital gain balance and the remaining balances is carried forward to the next year7. Therefore, in

this case, Chris can claim set off for the capital losses against the capital gains and a remaining

balance of $ 8,840 would be carried forward to future period.

Answer to Question 4

Answer A

As per the provisions of taxation, a taxpayer is not held taxable for simple prize winnings.

However, if the winnings from prizes results in generation of appropriate income related to the

operations of the taxpayer than the same would be considered to be taxable income. In the case

of “Kelly v FCT (1985)” a reward which was received by footballer for playing a fair and

7 Selling An Asset And Other CGT Events." Ato.gov.au. N. p., 2019. Web. 7 May 2019.

11

TAXATION LAW

excellent sport was considered to be ordinary income as the same was related to the profession of

the footballer and it also required employment of skills.

The case shows that the taxpayer receives $ 2,000 by the taxpayer for best advertisement

campaign for the year8. This would be considered as ordinary income under “section 6-5, ITAA

1997”. The amount received would be held taxable as the same is incidental to the line of work

performed by the taxpayer.

Answer B

As per the provisions which is stated in “section 6-1 of the ITAA 1936” personal exertion

income consists of wages, gratuities, remunerations etc and the same is received by the employee

for the services which is rendered by the employee or as proceeds for carrying on operations of a

business9.

In this case, the employee received the amount of $ 500 as travelling expenses provided by

employer for travel from Sydney to place of work. The amount would be considered as income

as the same is allowances received for the work which is done by the employee.

Answer C

A gain which is in the nature of simple gift would not be considered as income as the same

does not contains the characteristics of an income. In the case of “FCT v Scott (1966)” verdict

was given by the court that receipt of 10,000 pounds as the gift from wife out of the estate of the

8 Gashenko, Irina V., Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods of

Taxation." Optimization of the Taxation System: Preconditions, Tendencies and Perspectives. Springer, Cham,

2019. 33-39.

9 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

TAXATION LAW

excellent sport was considered to be ordinary income as the same was related to the profession of

the footballer and it also required employment of skills.

The case shows that the taxpayer receives $ 2,000 by the taxpayer for best advertisement

campaign for the year8. This would be considered as ordinary income under “section 6-5, ITAA

1997”. The amount received would be held taxable as the same is incidental to the line of work

performed by the taxpayer.

Answer B

As per the provisions which is stated in “section 6-1 of the ITAA 1936” personal exertion

income consists of wages, gratuities, remunerations etc and the same is received by the employee

for the services which is rendered by the employee or as proceeds for carrying on operations of a

business9.

In this case, the employee received the amount of $ 500 as travelling expenses provided by

employer for travel from Sydney to place of work. The amount would be considered as income

as the same is allowances received for the work which is done by the employee.

Answer C

A gain which is in the nature of simple gift would not be considered as income as the same

does not contains the characteristics of an income. In the case of “FCT v Scott (1966)” verdict

was given by the court that receipt of 10,000 pounds as the gift from wife out of the estate of the

8 Gashenko, Irina V., Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods of

Taxation." Optimization of the Taxation System: Preconditions, Tendencies and Perspectives. Springer, Cham,

2019. 33-39.

9 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.