LCBB4001 Accounting Fundamentals: Kedison PLC Financial Report

VerifiedAdded on 2023/06/18

|9

|1822

|463

Report

AI Summary

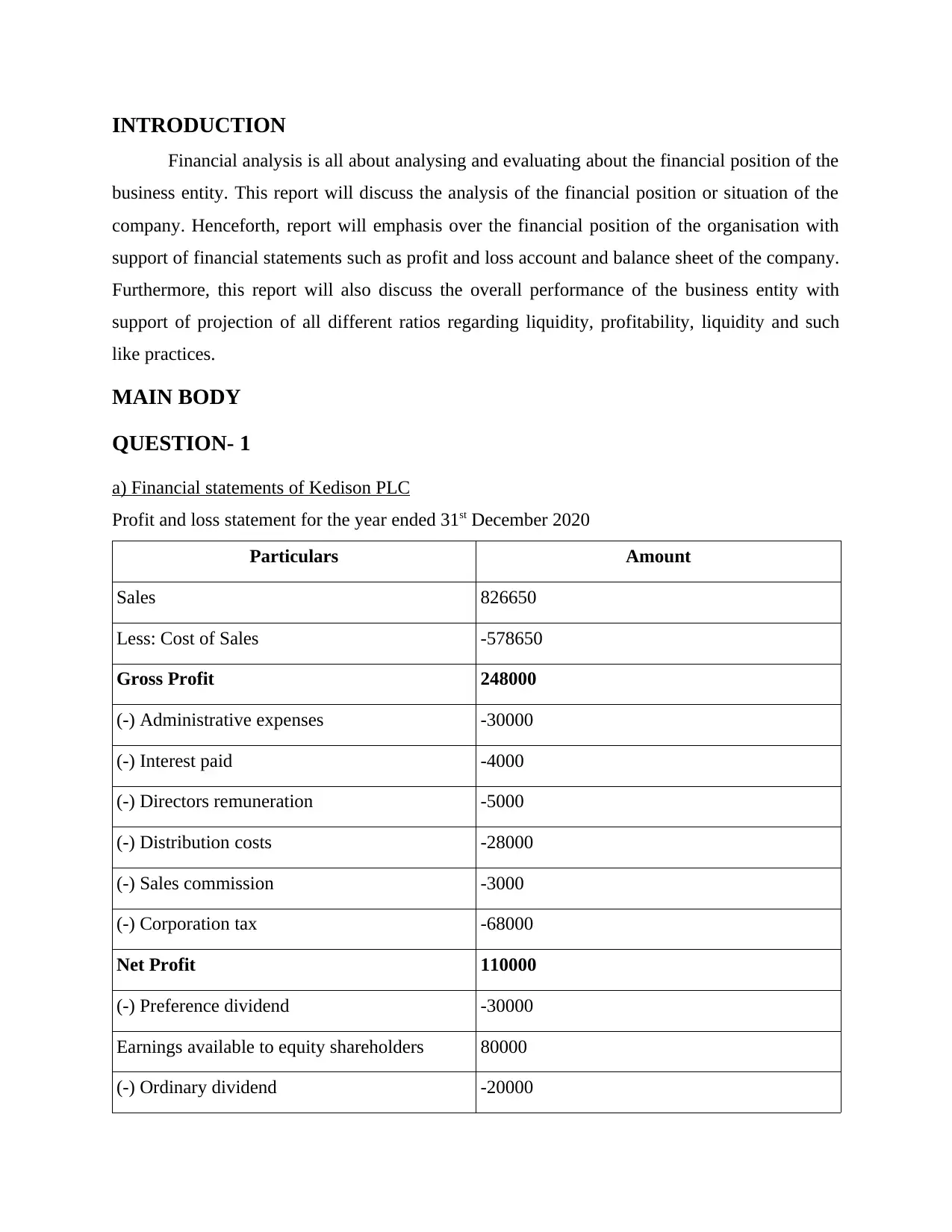

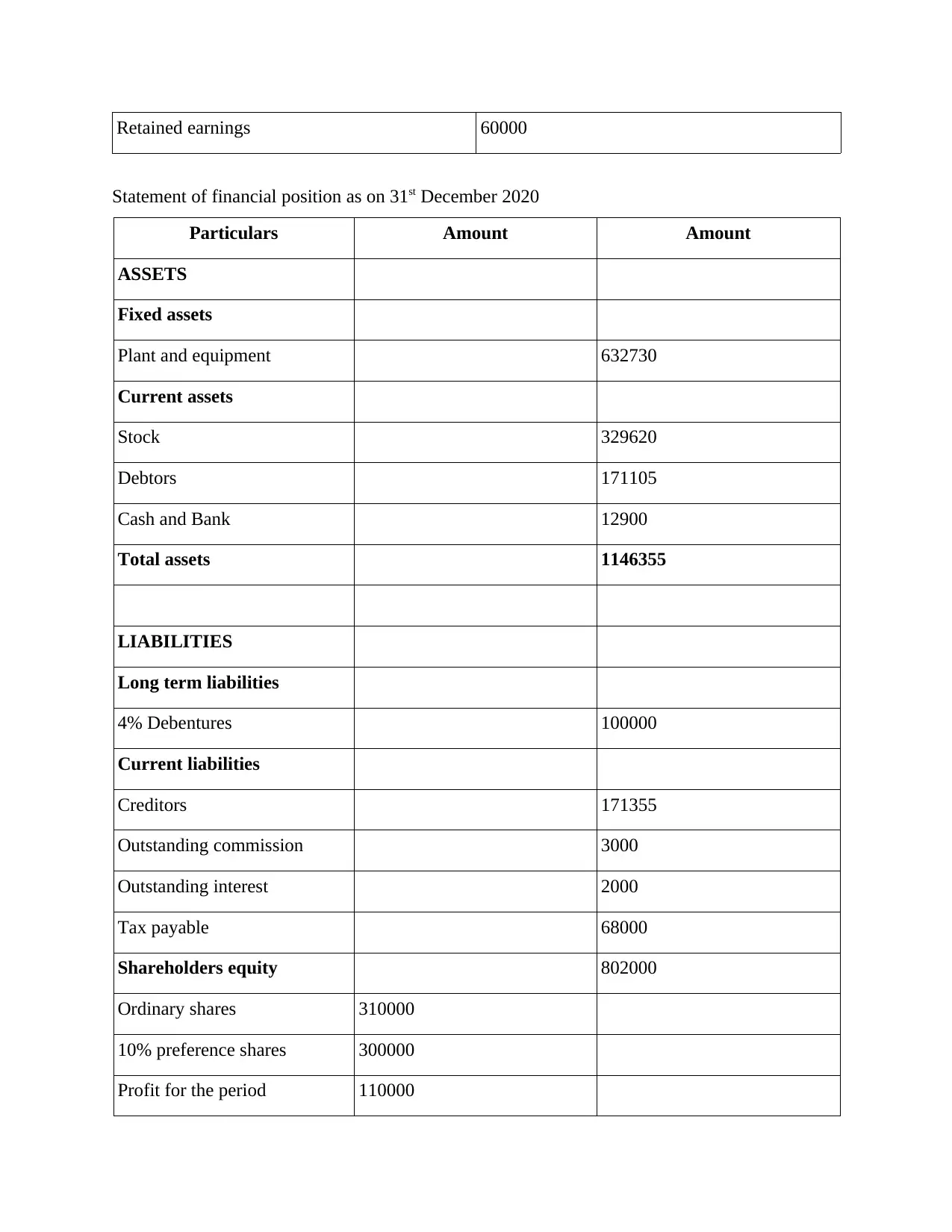

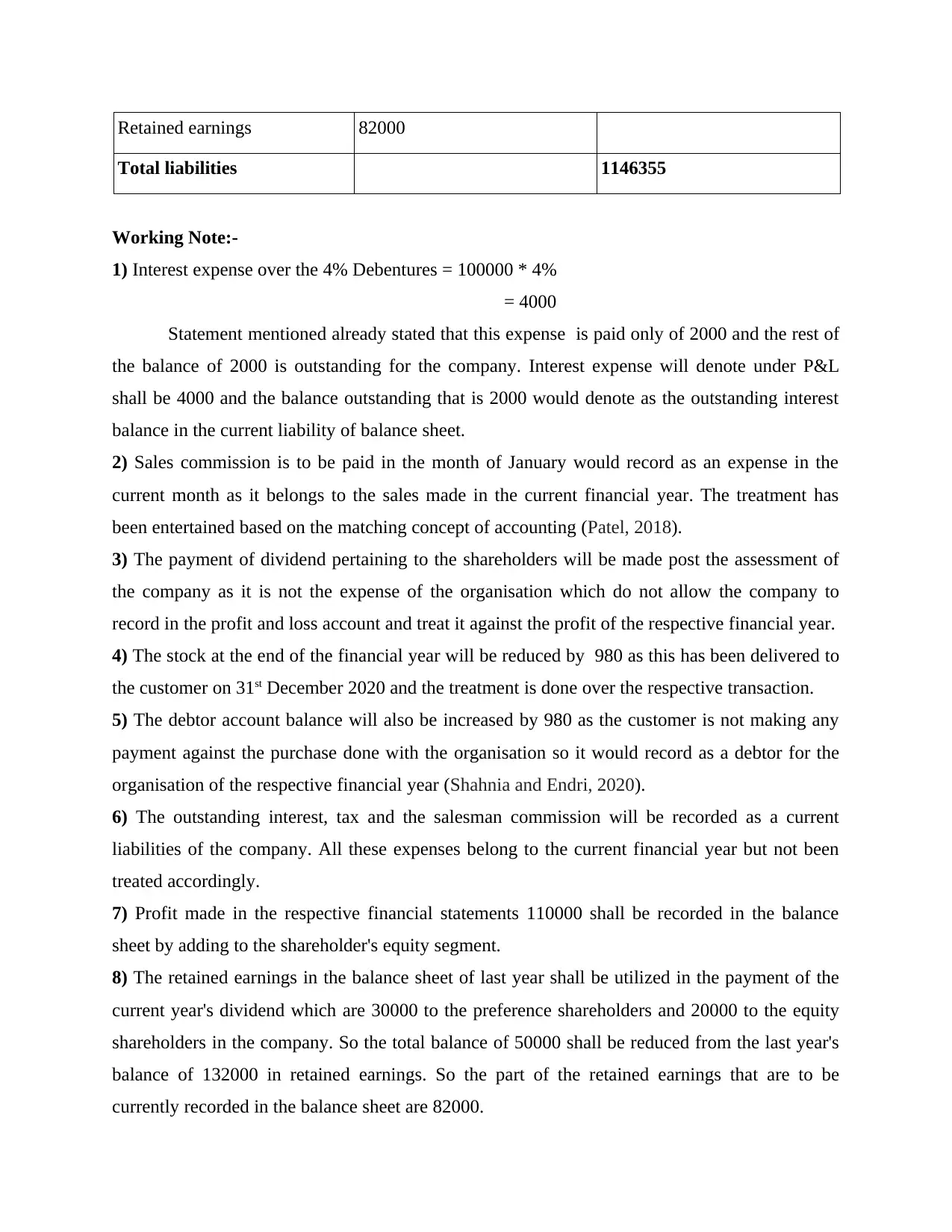

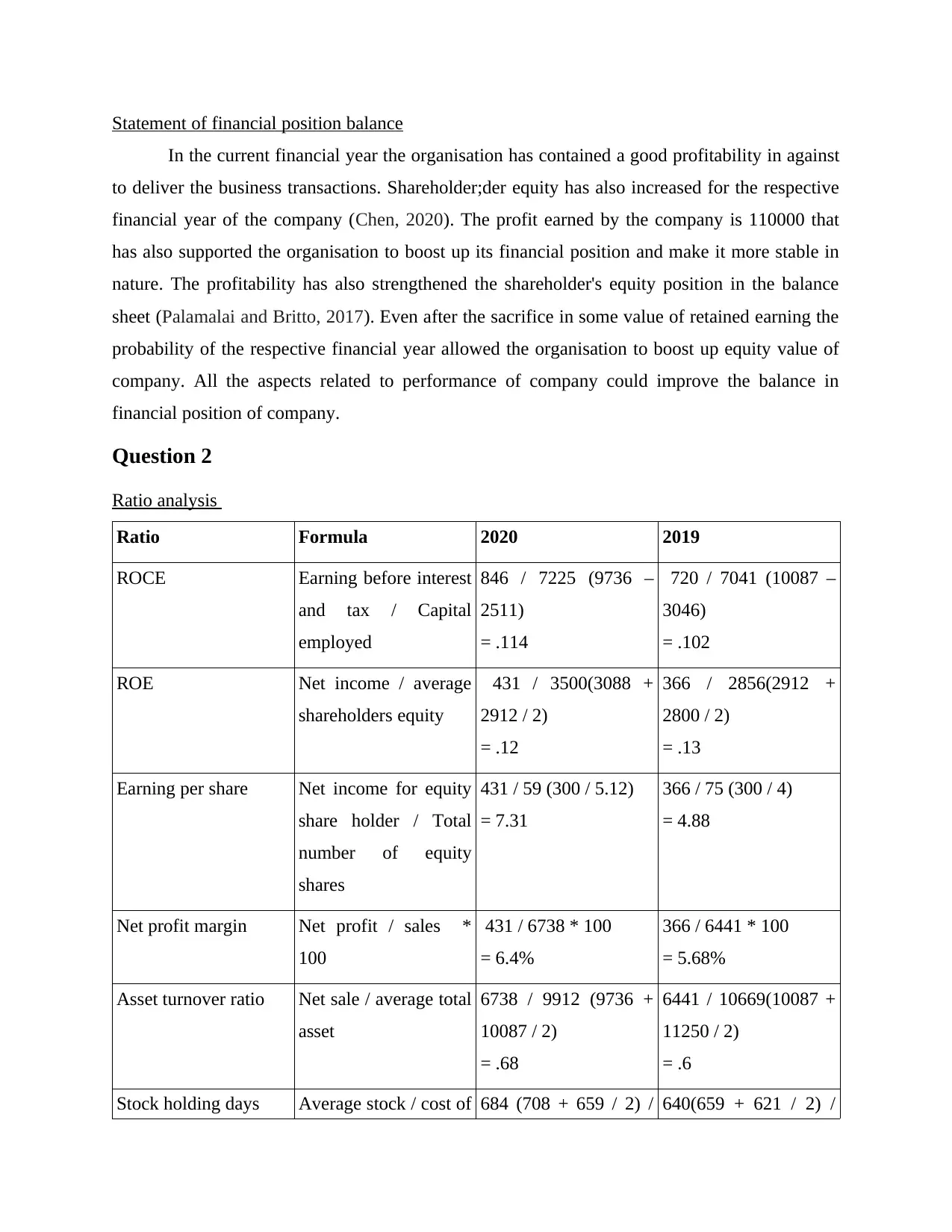

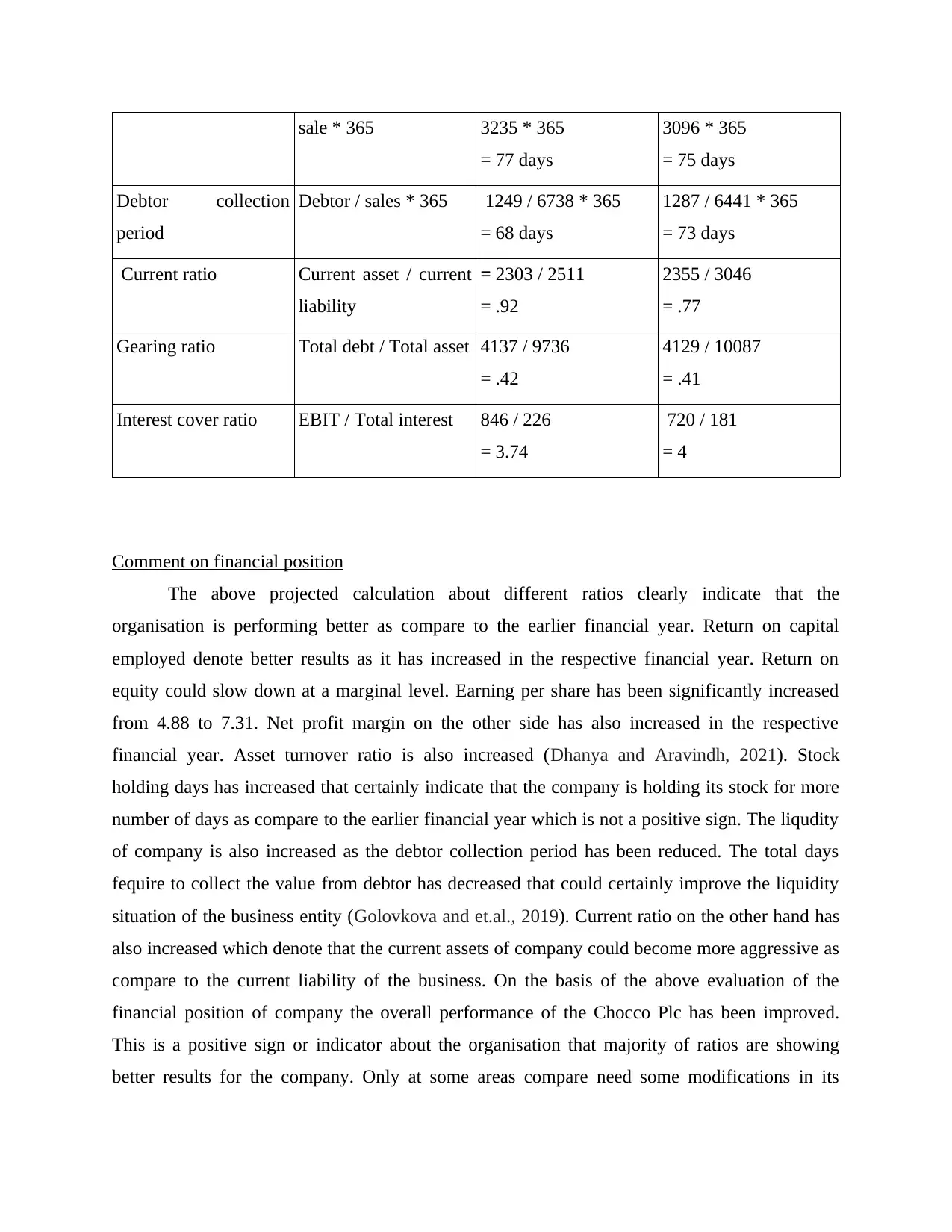

This report provides a comprehensive financial analysis of Kedison PLC, utilizing financial statements such as the profit and loss account and balance sheet to evaluate the company's financial health. The analysis includes a detailed examination of various financial ratios, including ROCE, ROE, net profit margin, and asset turnover, to assess the company's liquidity, profitability, and overall performance. The report also discusses the implications of these ratios, highlighting areas of improvement and strengths in Kedison PLC's financial strategies. The conclusion summarizes the key findings and emphasizes the importance of ratio analysis in evaluating the financial position of a business entity, noting Chocco Plc favorable results in reflecting its financial position. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.