Impact of AASB 16 on Lease Accounting, Tax Payment and Reporting

VerifiedAdded on 2023/06/03

|8

|875

|480

Homework Assignment

AI Summary

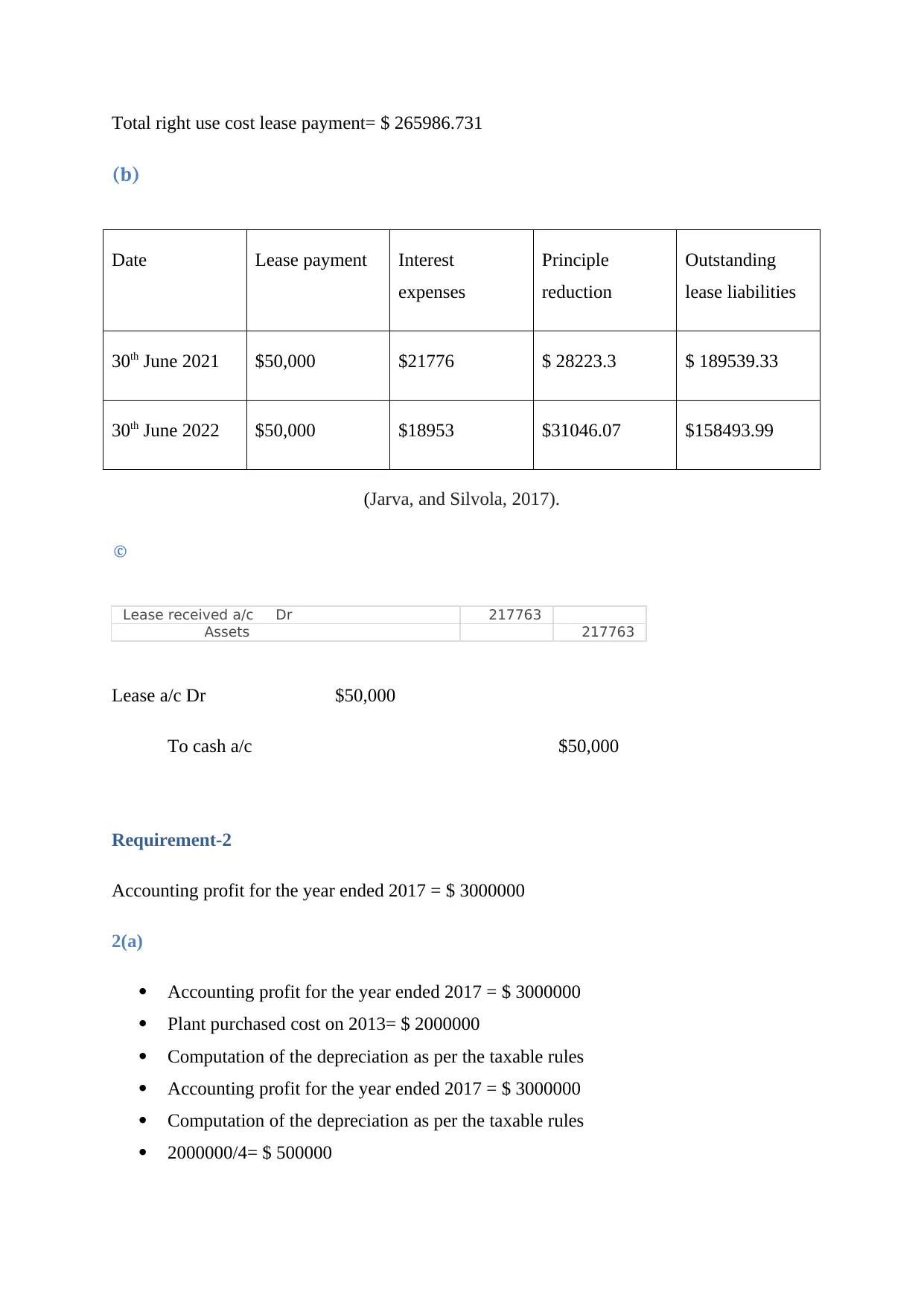

This assignment provides a detailed analysis of lease accounting, focusing on the calculation of lease liabilities and right-to-use assets in accordance with AASB 16. It includes computations of present values for lease payments and purchase options, along with journal entries for lease transactions. The assignment further delves into income tax calculations, addressing taxable profits, income tax expenses, and deferred tax implications. It presents a comprehensive overview of how accounting and tax rules interact, offering insights into deferred tax assets and liabilities arising from temporary differences. The journal entries for income tax, including deferred tax expenses and current income tax, are also provided, offering a complete picture of the financial and tax considerations in lease accounting. Desklib offers a variety of resources, including past papers and solved assignments, to aid students in their studies.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.