Report on Advanced Financial Accounting: Impairment and Leases

VerifiedAdded on 2020/05/28

|13

|2574

|85

Report

AI Summary

This report provides an in-depth analysis of advanced financial accounting, focusing on impairment testing and lease accounting, particularly in the context of Virgin Australia. The report examines the company's approach to impairment testing, including the assessment of financial assets, the determination of cash-generating units, and the recognition of impairment losses. It also delves into the impact of the new lease accounting standard, discussing the shortcomings of the previous standard, the benefits of the new standard in terms of transparency and comparability, and the perspectives of stakeholders such as the IASB chairman. The report highlights the significance of the new rules in reflecting the correct financial state of lessees and enabling better decision-making among investors. Furthermore, it analyzes the potential impact of the new lease accounting standard on financial metrics and reporting, emphasizing the need for organizations to conduct preliminary assessments and establish robust internal control systems for its effective implementation. Overall, the report offers a comprehensive overview of these critical accounting topics, providing valuable insights into financial reporting practices and the implications of accounting standards.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

At each report date, Virgin Australia has assessed financial assets for impairment and it is

indicated by objective evidence that estimated future cash flow generated from assets are

negatively impacted by occurrence of any loss events. Assets having finite useful lives are tested

for impairment whenever there is an indication that assets might be impaired and it is done

annually. The management for estimating the impairment value requires significant judgment.

Virgin Australia has recognized impairment in relation to maintenance reserve deposits of

amount $ 28.5 million. Impairment loss has been recognized on assets of amount 118.1 million

that is associated with lease contracts (virginaustralia.com 2018).

Requirement ii)

Organization performs impairment testing on annual basis for determining if the

impairment loss is generated and potential impacts through sensitivity analysis. At each

reporting date, the group does assessment whether there is any indication that assets requires

impairment. Recoverable amount of assets is estimated when there is requirement of conducting

annual impairment testing. Inflow us nit generated by assets when recoverable amount of assets

are higher than assets. A cash-generating unit or an asset is considered impaired when their

recoverable amount is less than the carrying amount and after impairment, amount is written

down to its recoverable amount (virginaustralia.com 2018). Judgment is required for

determination of cash generating unit, regarding the way operations is monitored by

management.

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

At each report date, Virgin Australia has assessed financial assets for impairment and it is

indicated by objective evidence that estimated future cash flow generated from assets are

negatively impacted by occurrence of any loss events. Assets having finite useful lives are tested

for impairment whenever there is an indication that assets might be impaired and it is done

annually. The management for estimating the impairment value requires significant judgment.

Virgin Australia has recognized impairment in relation to maintenance reserve deposits of

amount $ 28.5 million. Impairment loss has been recognized on assets of amount 118.1 million

that is associated with lease contracts (virginaustralia.com 2018).

Requirement ii)

Organization performs impairment testing on annual basis for determining if the

impairment loss is generated and potential impacts through sensitivity analysis. At each

reporting date, the group does assessment whether there is any indication that assets requires

impairment. Recoverable amount of assets is estimated when there is requirement of conducting

annual impairment testing. Inflow us nit generated by assets when recoverable amount of assets

are higher than assets. A cash-generating unit or an asset is considered impaired when their

recoverable amount is less than the carrying amount and after impairment, amount is written

down to its recoverable amount (virginaustralia.com 2018). Judgment is required for

determination of cash generating unit, regarding the way operations is monitored by

management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

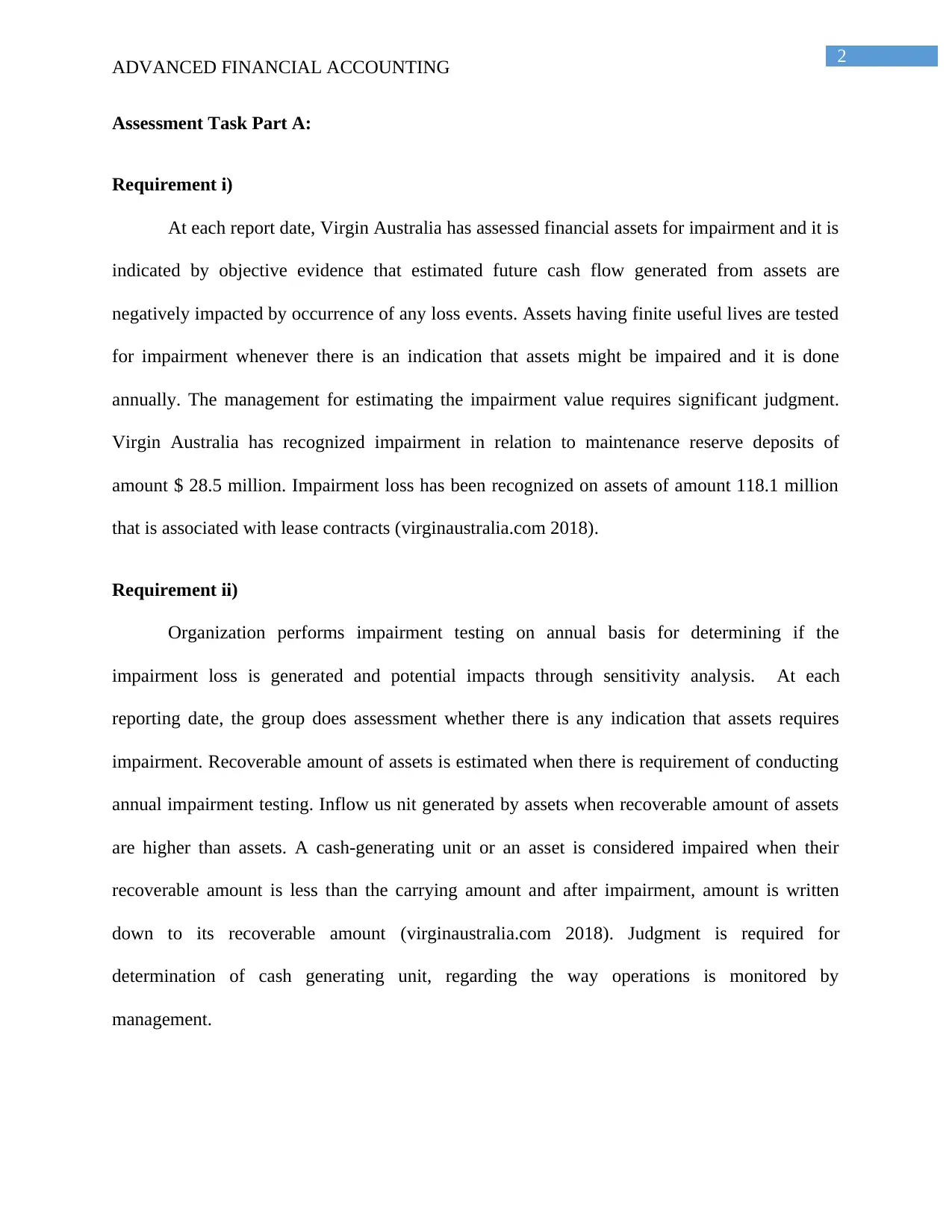

Carrying value of intangible assets and goodwill is allocated to each cash-generating unit

and there is no amortization of these balances and this result in impairment loss risks.

Determination of Cash generating unit is based on calculations of value in use. Financial budgets

form the basis of estimating future cash flow that is approved by senior management.

Requirement iii)

In the current reporting year, Virgin Australia airlines holding has recorded impairment

expenses on assets that are classified as held for sales and impairment losses on other assets.

Impairment assets on other assets are reported at $ 118.1 million and impairment losses on assets

that are classified as held for sale is reported at $ 107.3 million. Impairment loss in relation to

intangible assets is recorded at $ 4.6 million (virginaustralia.com 2018).

Requirement iv)

The calculation of impairment is done as the difference between present value of

estimated future cash flows and the carrying value of assets. Future cash flow is estimated at by

discounting at original effective interest rate of asset. Varying amount of assets and liabilities has

the possibility of carrying significant risks in light of assumptions that are made by management

and are likely to make material adjustments. Virgin Australia is required to use estimates that are

based on assumptions for calculation of unearned revenue. Historical trend of financial liabilities

ADVANCED FINANCIAL ACCOUNTING

Carrying value of intangible assets and goodwill is allocated to each cash-generating unit

and there is no amortization of these balances and this result in impairment loss risks.

Determination of Cash generating unit is based on calculations of value in use. Financial budgets

form the basis of estimating future cash flow that is approved by senior management.

Requirement iii)

In the current reporting year, Virgin Australia airlines holding has recorded impairment

expenses on assets that are classified as held for sales and impairment losses on other assets.

Impairment assets on other assets are reported at $ 118.1 million and impairment losses on assets

that are classified as held for sale is reported at $ 107.3 million. Impairment loss in relation to

intangible assets is recorded at $ 4.6 million (virginaustralia.com 2018).

Requirement iv)

The calculation of impairment is done as the difference between present value of

estimated future cash flows and the carrying value of assets. Future cash flow is estimated at by

discounting at original effective interest rate of asset. Varying amount of assets and liabilities has

the possibility of carrying significant risks in light of assumptions that are made by management

and are likely to make material adjustments. Virgin Australia is required to use estimates that are

based on assumptions for calculation of unearned revenue. Historical trend of financial liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

and assets form the basis of assumptions. Any change in assumptions for determining

recoverable amount of assets leads to reversal of recognized impairment loss. Projections of cash

flow are based on assumptions such as expectation of management regarding revenue, market,

costs, fuel price, load factors and exchange rate.

Requirement v)

Accuracy of impairment testing by organization can be improved if there is any existence

of subjectivity in determining the estimates. Management of group is required to make judgment

about assets recoverable amount and in terms of inputs and parameters. Significant judgment is

required for determining the estimation of impairment value. In the current year, it was

recognized by the management of group that there was no requirement of conducting impairment

testing and there was no triggering of impairment and recognition of goodwill

(virginaustralia.com 2018). Therefore, the assumptions, framing judgment, making estimates are

all accounted by exercising subjectivity and enabling management to act opportunistically.

Requirement vi)

The impairment testing methodology of virgin Australia airline holding seems to be

interesting as depicted from the analysis of annual report. Management has done impairment

testing by considering relevant facts and figures and determining whether impairment has

triggered in any particular reporting year. Assumptions of management regarding impairment

testing might reasonably change if they are identified. It has been found that other variables

determining impairment have been held constant as mentioned in the sensitivity analysis.

Another interesting fact that has been gained about impairment testing by analyzing the report of

Airline Company that it conducts sensitivity analysis by making several assumptions and

ADVANCED FINANCIAL ACCOUNTING

and assets form the basis of assumptions. Any change in assumptions for determining

recoverable amount of assets leads to reversal of recognized impairment loss. Projections of cash

flow are based on assumptions such as expectation of management regarding revenue, market,

costs, fuel price, load factors and exchange rate.

Requirement v)

Accuracy of impairment testing by organization can be improved if there is any existence

of subjectivity in determining the estimates. Management of group is required to make judgment

about assets recoverable amount and in terms of inputs and parameters. Significant judgment is

required for determining the estimation of impairment value. In the current year, it was

recognized by the management of group that there was no requirement of conducting impairment

testing and there was no triggering of impairment and recognition of goodwill

(virginaustralia.com 2018). Therefore, the assumptions, framing judgment, making estimates are

all accounted by exercising subjectivity and enabling management to act opportunistically.

Requirement vi)

The impairment testing methodology of virgin Australia airline holding seems to be

interesting as depicted from the analysis of annual report. Management has done impairment

testing by considering relevant facts and figures and determining whether impairment has

triggered in any particular reporting year. Assumptions of management regarding impairment

testing might reasonably change if they are identified. It has been found that other variables

determining impairment have been held constant as mentioned in the sensitivity analysis.

Another interesting fact that has been gained about impairment testing by analyzing the report of

Airline Company that it conducts sensitivity analysis by making several assumptions and

5

ADVANCED FINANCIAL ACCOUNTING

changing the assumptions for recoverable amount estimation so that it becomes equal to carrying

amount (virginaustralia.com 2018).

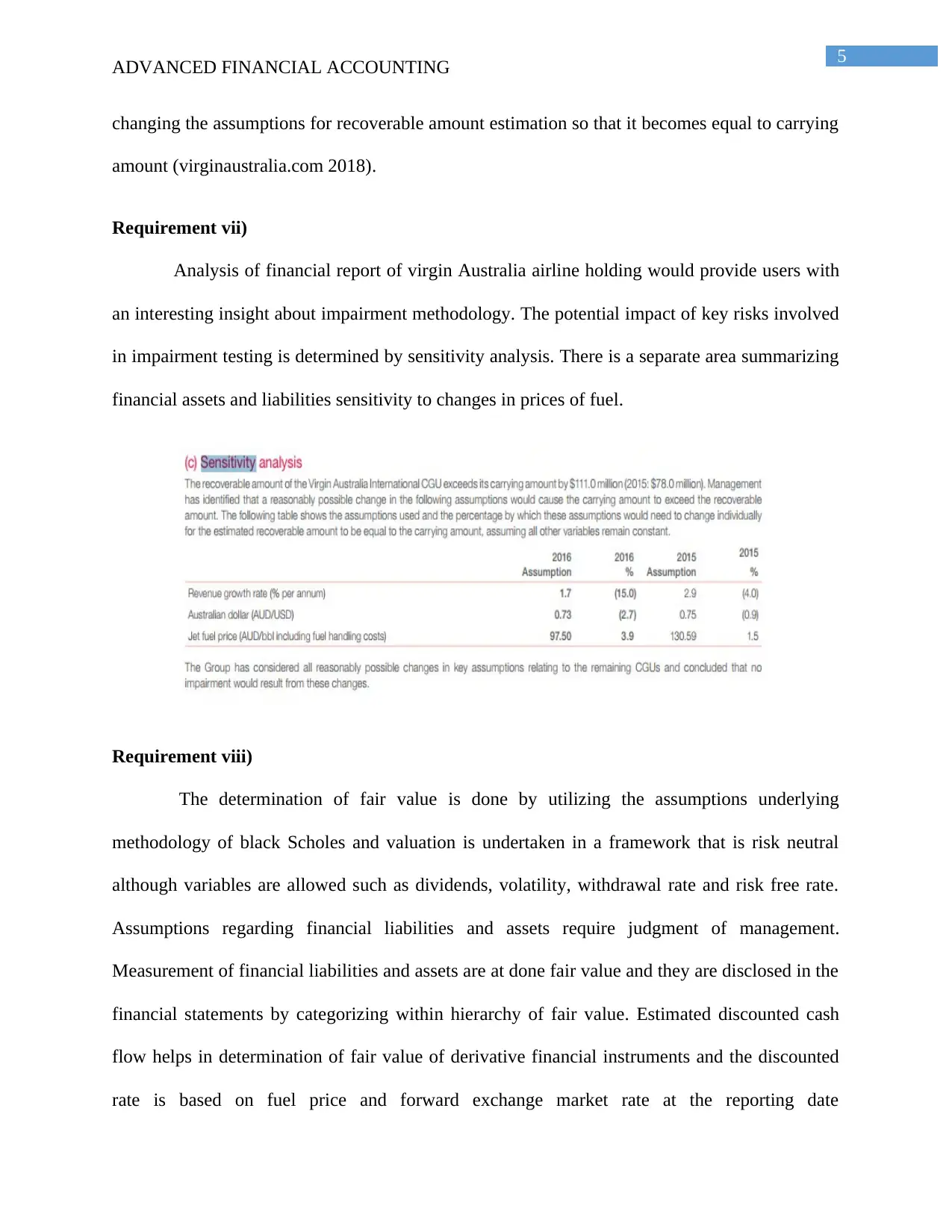

Requirement vii)

Analysis of financial report of virgin Australia airline holding would provide users with

an interesting insight about impairment methodology. The potential impact of key risks involved

in impairment testing is determined by sensitivity analysis. There is a separate area summarizing

financial assets and liabilities sensitivity to changes in prices of fuel.

Requirement viii)

The determination of fair value is done by utilizing the assumptions underlying

methodology of black Scholes and valuation is undertaken in a framework that is risk neutral

although variables are allowed such as dividends, volatility, withdrawal rate and risk free rate.

Assumptions regarding financial liabilities and assets require judgment of management.

Measurement of financial liabilities and assets are at done fair value and they are disclosed in the

financial statements by categorizing within hierarchy of fair value. Estimated discounted cash

flow helps in determination of fair value of derivative financial instruments and the discounted

rate is based on fuel price and forward exchange market rate at the reporting date

ADVANCED FINANCIAL ACCOUNTING

changing the assumptions for recoverable amount estimation so that it becomes equal to carrying

amount (virginaustralia.com 2018).

Requirement vii)

Analysis of financial report of virgin Australia airline holding would provide users with

an interesting insight about impairment methodology. The potential impact of key risks involved

in impairment testing is determined by sensitivity analysis. There is a separate area summarizing

financial assets and liabilities sensitivity to changes in prices of fuel.

Requirement viii)

The determination of fair value is done by utilizing the assumptions underlying

methodology of black Scholes and valuation is undertaken in a framework that is risk neutral

although variables are allowed such as dividends, volatility, withdrawal rate and risk free rate.

Assumptions regarding financial liabilities and assets require judgment of management.

Measurement of financial liabilities and assets are at done fair value and they are disclosed in the

financial statements by categorizing within hierarchy of fair value. Estimated discounted cash

flow helps in determination of fair value of derivative financial instruments and the discounted

rate is based on fuel price and forward exchange market rate at the reporting date

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

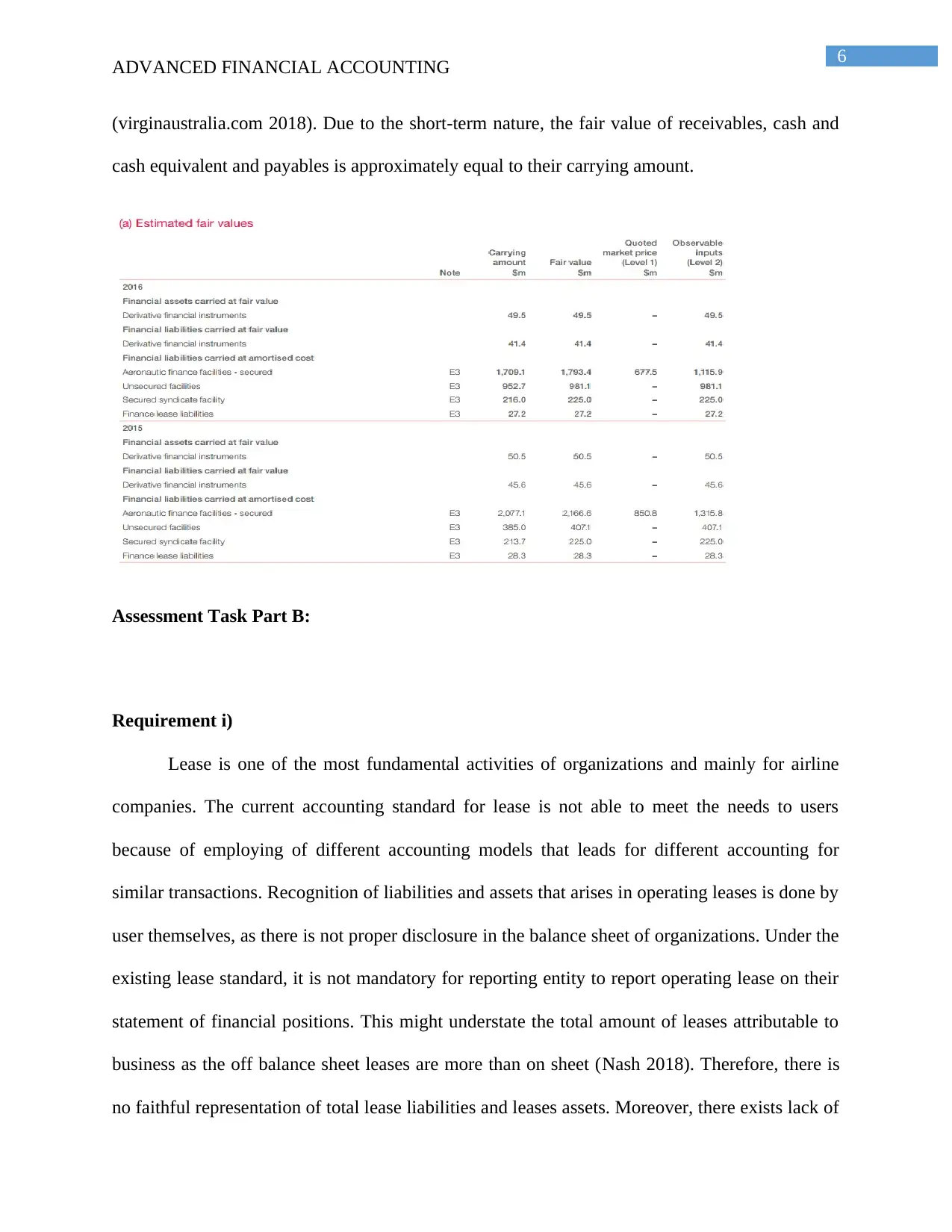

ADVANCED FINANCIAL ACCOUNTING

(virginaustralia.com 2018). Due to the short-term nature, the fair value of receivables, cash and

cash equivalent and payables is approximately equal to their carrying amount.

Assessment Task Part B:

Requirement i)

Lease is one of the most fundamental activities of organizations and mainly for airline

companies. The current accounting standard for lease is not able to meet the needs to users

because of employing of different accounting models that leads for different accounting for

similar transactions. Recognition of liabilities and assets that arises in operating leases is done by

user themselves, as there is not proper disclosure in the balance sheet of organizations. Under the

existing lease standard, it is not mandatory for reporting entity to report operating lease on their

statement of financial positions. This might understate the total amount of leases attributable to

business as the off balance sheet leases are more than on sheet (Nash 2018). Therefore, there is

no faithful representation of total lease liabilities and leases assets. Moreover, there exists lack of

ADVANCED FINANCIAL ACCOUNTING

(virginaustralia.com 2018). Due to the short-term nature, the fair value of receivables, cash and

cash equivalent and payables is approximately equal to their carrying amount.

Assessment Task Part B:

Requirement i)

Lease is one of the most fundamental activities of organizations and mainly for airline

companies. The current accounting standard for lease is not able to meet the needs to users

because of employing of different accounting models that leads for different accounting for

similar transactions. Recognition of liabilities and assets that arises in operating leases is done by

user themselves, as there is not proper disclosure in the balance sheet of organizations. Under the

existing lease standard, it is not mandatory for reporting entity to report operating lease on their

statement of financial positions. This might understate the total amount of leases attributable to

business as the off balance sheet leases are more than on sheet (Nash 2018). Therefore, there is

no faithful representation of total lease liabilities and leases assets. Moreover, there exists lack of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

transparency that makes it difficult for users to evaluate the total amount of leased assets and

liabilities, an organization has. In different lease transactions, different economics are involved

and in the absence of their disclosures, users of financial statement are not provided with

economic reality pertaining to leases.

Requirement ii)

Under the existing lease accounting standard, organizations are required to only make

disclosure of capital lease assets and liabilities. However, they are not required to disclose

operating leased assets and liabilities as their disclosure is not mandatory. There exists possibility

that a reporting entity might have thousands leases liabilities and assets that are not incorporated

in the financial metrics. Most of the organizations have majority of leased liabilities and assets in

the form of operating leases and are not disclosed in the statement of financial position leading to

underestimation of actual operating lease amount (Huber et al. 2017). This would contribute in

making total leases reported in the balance sheets significantly lower than off balance sheet.

Although, there is no disclosure of such leasing amounts in the financial statements, organization

are committed to duly meet their long-term commitments arising from such operating leases.

Many retail organizations have gone bankrupt at the time of financial crisis on part of

their failure to make adjustments to reflect economic reality. Financial position of such reporting

entities are perceived deceptively as their obligations to meet or repay their long-term liabilities

arising from operating leases despite they are not disclosed in the financial statements in

accordance with the existing or current lease standard.

ADVANCED FINANCIAL ACCOUNTING

transparency that makes it difficult for users to evaluate the total amount of leased assets and

liabilities, an organization has. In different lease transactions, different economics are involved

and in the absence of their disclosures, users of financial statement are not provided with

economic reality pertaining to leases.

Requirement ii)

Under the existing lease accounting standard, organizations are required to only make

disclosure of capital lease assets and liabilities. However, they are not required to disclose

operating leased assets and liabilities as their disclosure is not mandatory. There exists possibility

that a reporting entity might have thousands leases liabilities and assets that are not incorporated

in the financial metrics. Most of the organizations have majority of leased liabilities and assets in

the form of operating leases and are not disclosed in the statement of financial position leading to

underestimation of actual operating lease amount (Huber et al. 2017). This would contribute in

making total leases reported in the balance sheets significantly lower than off balance sheet.

Although, there is no disclosure of such leasing amounts in the financial statements, organization

are committed to duly meet their long-term commitments arising from such operating leases.

Many retail organizations have gone bankrupt at the time of financial crisis on part of

their failure to make adjustments to reflect economic reality. Financial position of such reporting

entities are perceived deceptively as their obligations to meet or repay their long-term liabilities

arising from operating leases despite they are not disclosed in the financial statements in

accordance with the existing or current lease standard.

8

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Former accounting standard of leasing was criticized due to its complexity in defining

and dividing line between operating and financing. This makes it difficult for investors to make

comparison between the financial positions of different entities. Majority of leases of aviation

companies are acquired in the form of operating leases and their disclosures are not done in the

balance sheets. Hence, there exists dissimilarity between organizations who are buying most of

its fleet and organizations who are leasing most of their aircraft fleets. However, in reality there

exist considerable differences between financial position of such companies. It is indicative of

the fact that there is no level-playing field between some of airline companies. All the leases for

airline companies will be accounted in the form of assets with the adoption of this standard and it

would be recorded in the form of liabilities (Edwards 2015). Therefore, the introduction of new

lease standard will help in resolving the issue of level playing field between airline companies.

Requirement iv)

Views of chairman of IASB that new lease accounting standard will not be popular

among everyone is because of several criticisms that are leveled against it and they are listed

below:

It is perceived that new accounting standard for lease will increase complexities and costs

of reporting relating to large volume of small assets in relation to leases.

Balance sheet profiles of lessee will change significantly that would make them looks

more leveraged than they actually are (Waybright et al. 2015). This would have an

impact on lessees borrowing costs and making it reason for becoming unpopular among

lessees.

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Former accounting standard of leasing was criticized due to its complexity in defining

and dividing line between operating and financing. This makes it difficult for investors to make

comparison between the financial positions of different entities. Majority of leases of aviation

companies are acquired in the form of operating leases and their disclosures are not done in the

balance sheets. Hence, there exists dissimilarity between organizations who are buying most of

its fleet and organizations who are leasing most of their aircraft fleets. However, in reality there

exist considerable differences between financial position of such companies. It is indicative of

the fact that there is no level-playing field between some of airline companies. All the leases for

airline companies will be accounted in the form of assets with the adoption of this standard and it

would be recorded in the form of liabilities (Edwards 2015). Therefore, the introduction of new

lease standard will help in resolving the issue of level playing field between airline companies.

Requirement iv)

Views of chairman of IASB that new lease accounting standard will not be popular

among everyone is because of several criticisms that are leveled against it and they are listed

below:

It is perceived that new accounting standard for lease will increase complexities and costs

of reporting relating to large volume of small assets in relation to leases.

Balance sheet profiles of lessee will change significantly that would make them looks

more leveraged than they actually are (Waybright et al. 2015). This would have an

impact on lessees borrowing costs and making it reason for becoming unpopular among

lessees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

Some sophisticated lenders when lending to lessee already estimate the effect of leases

that are off balance sheet on leverage. Hence, reporting entity is not required to bring

them on balance sheets.

One of the factors is adequacy of knowledge on part of management for implementing

new lease standard. An organization is required to gather relevant facts and information

and make changes accordingly so that they get adapted to new system (Mader et al.

2015). However, existing financial metrics of organization will also be altered by the

implementation of this new leasing standard.

Requirement v)

The new rules that are framed for leasing as per new accounting standard will ensure that

balance sheets reflect lessees correct financial state of affairs. Moreover, lenders will be able to

get detailed and true information on credit risks of lessee and therefore, they will be well

equipped with understanding about pricing the risk of lending. For determining how lease

accounting will be affected by this new standard, it is required by reporting entity to conduct

preliminary assessment. It is also required to be ensured by entities that they have adequate

internal control system in place so that they are able to collect necessary information for

implementation of new standard. A detailed guidance is provided to organizations for

determining whether contract is service contract or lease contract (Eng et al. 2014).

Organizations working heavily with operating leases will be considerably impacted by this new

lease standard. There will be reasonable uncertainty by exercising leasing options relating to

economic reality. Moreover, lease accounting will enable better and informed decision among

investors in terms of determining contract terms, calculations and leasing practice that leads to

identification of relevant leased assets relating to leasing operations. Investors under new

ADVANCED FINANCIAL ACCOUNTING

Some sophisticated lenders when lending to lessee already estimate the effect of leases

that are off balance sheet on leverage. Hence, reporting entity is not required to bring

them on balance sheets.

One of the factors is adequacy of knowledge on part of management for implementing

new lease standard. An organization is required to gather relevant facts and information

and make changes accordingly so that they get adapted to new system (Mader et al.

2015). However, existing financial metrics of organization will also be altered by the

implementation of this new leasing standard.

Requirement v)

The new rules that are framed for leasing as per new accounting standard will ensure that

balance sheets reflect lessees correct financial state of affairs. Moreover, lenders will be able to

get detailed and true information on credit risks of lessee and therefore, they will be well

equipped with understanding about pricing the risk of lending. For determining how lease

accounting will be affected by this new standard, it is required by reporting entity to conduct

preliminary assessment. It is also required to be ensured by entities that they have adequate

internal control system in place so that they are able to collect necessary information for

implementation of new standard. A detailed guidance is provided to organizations for

determining whether contract is service contract or lease contract (Eng et al. 2014).

Organizations working heavily with operating leases will be considerably impacted by this new

lease standard. There will be reasonable uncertainty by exercising leasing options relating to

economic reality. Moreover, lease accounting will enable better and informed decision among

investors in terms of determining contract terms, calculations and leasing practice that leads to

identification of relevant leased assets relating to leasing operations. Investors under new

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

standard are not required to perform any rough calculations for estimating the amount of leased

assets and liabilities to add back them on balance sheets (Antle and Garstka 2014). It will

facilitate making comparison between different companies and assist investors in leading to more

balanced lease versus better buy decisions by management and making informed decisions.

ADVANCED FINANCIAL ACCOUNTING

standard are not required to perform any rough calculations for estimating the amount of leased

assets and liabilities to add back them on balance sheets (Antle and Garstka 2014). It will

facilitate making comparison between different companies and assist investors in leading to more

balanced lease versus better buy decisions by management and making informed decisions.

11

ADVANCED FINANCIAL ACCOUNTING

References list:

Allen, J., 2016. ACCT 200-08-09 Introductory Financial Accounting

Andrew, A. and Ward, A.M., 2015. Introduction to Financial Accounting.

Antle, R. and Garstka, S.J., 2014. Financial accounting with questions, exercises, problems, case

problems, cases and thomson analytics. Hardcover, South-Western College.

Cockrell, C., 2015. ACCT 500-W26 Foundations of Financial Accounting.

Edwards, J.R., 2015. History of financial accounting theory in Britain1. The Routledge

Companion to Financial Accounting Theory, p.12.

Eng, L.L., Lea, B.R. and Cai, R., 2014. Use of clickers for assurance of learning in introductory

financial accounting. In Advances in Accounting Education: Teaching and Curriculum

Innovations (pp. 269-291). Emerald Group Publishing Limited.

Glover, J., 2014. Have Academic Accountants and Financial Accounting Standard Setters

Traded Places?. Accounting, Economics and Law Account. Econ. Law, 4(1), pp.17-26.

Huber, M., Law, D. and Khallaf, A., 2017. Active Learning Innovations In Introductory

Financial Accounting. In Advances in Accounting Education: Teaching and Curriculum

Innovations (pp. 125-167). Emerald Publishing Limited.

Mader, G.A., Mader, R.J., Campbell, J., Kannan, B. and Carnes, R., 2015. Financial Accounting

with Odoo: Versions 6, 7, and 8.

Malak, S.S.D.A., 2015. Cooperative learning: Buddy system in an advanced accounting subject.

May, I., 2014. the Financial Accounting Standards Board (“FASB”) issued.

ADVANCED FINANCIAL ACCOUNTING

References list:

Allen, J., 2016. ACCT 200-08-09 Introductory Financial Accounting

Andrew, A. and Ward, A.M., 2015. Introduction to Financial Accounting.

Antle, R. and Garstka, S.J., 2014. Financial accounting with questions, exercises, problems, case

problems, cases and thomson analytics. Hardcover, South-Western College.

Cockrell, C., 2015. ACCT 500-W26 Foundations of Financial Accounting.

Edwards, J.R., 2015. History of financial accounting theory in Britain1. The Routledge

Companion to Financial Accounting Theory, p.12.

Eng, L.L., Lea, B.R. and Cai, R., 2014. Use of clickers for assurance of learning in introductory

financial accounting. In Advances in Accounting Education: Teaching and Curriculum

Innovations (pp. 269-291). Emerald Group Publishing Limited.

Glover, J., 2014. Have Academic Accountants and Financial Accounting Standard Setters

Traded Places?. Accounting, Economics and Law Account. Econ. Law, 4(1), pp.17-26.

Huber, M., Law, D. and Khallaf, A., 2017. Active Learning Innovations In Introductory

Financial Accounting. In Advances in Accounting Education: Teaching and Curriculum

Innovations (pp. 125-167). Emerald Publishing Limited.

Mader, G.A., Mader, R.J., Campbell, J., Kannan, B. and Carnes, R., 2015. Financial Accounting

with Odoo: Versions 6, 7, and 8.

Malak, S.S.D.A., 2015. Cooperative learning: Buddy system in an advanced accounting subject.

May, I., 2014. the Financial Accounting Standards Board (“FASB”) issued.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.