FINC 0300 - America Coffee House: Evaluating Leasing and Purchasing

VerifiedAdded on 2023/04/24

|13

|3074

|448

Case Study

AI Summary

This case study provides a detailed financial analysis of whether America Coffee House should lease or purchase an asset, applying capital investment principles for evaluation. It discusses the advantages and disadvantages of leasing, including perspectives from both lessor and lessee. The analysis includes calculating the weighted average cost of capital (WACC) and performing a net advantage to leasing (NAL) analysis under various scenarios, such as changes in payment timing, salvage value, and security deposits. Ultimately, the report recommends leasing the asset, considering the reduced risks and potential cost savings compared to purchasing, based on the present value of lease payments versus the cost of purchasing the asset. The classification of lease payments is also examined under different conditions, reflecting the varying values of the lease contract.

Running head: ACCOUNTING AND FINANCIAL MANAGEMENT

Purchase versus Lease

Name of the Student:

Name of the University:

Author’s Note:

Purchase versus Lease

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCIAL MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Leasing Of Assets..................................................................................................................2

Weighted Average Cost of Capital........................................................................................3

Net Advantage to Leasing Analysis.......................................................................................4

Leasing or Purchase...............................................................................................................5

Classification of Lease Payments...........................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

1) Weighted Average Cost of Capital...............................................................................10

2) Change in Payment at the beginning of each Period.....................................................10

3) Change in Payment at the End of Year.........................................................................11

4) Change in Salvage Value..............................................................................................11

5) Security Deposits..........................................................................................................12

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Leasing Of Assets..................................................................................................................2

Weighted Average Cost of Capital........................................................................................3

Net Advantage to Leasing Analysis.......................................................................................4

Leasing or Purchase...............................................................................................................5

Classification of Lease Payments...........................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

1) Weighted Average Cost of Capital...............................................................................10

2) Change in Payment at the beginning of each Period.....................................................10

3) Change in Payment at the End of Year.........................................................................11

4) Change in Salvage Value..............................................................................................11

5) Security Deposits..........................................................................................................12

2ACCOUNTING AND FINANCIAL MANAGEMENT

Introduction

Assets is an integral part of an organisation, which is used on a daily basis by the

organisation for their daily operational works. The principal of Capital Investment will be

applied for the purpose of evaluation and analysis of the financial viability of the project. The

Asset taken into consideration by the American Coffee house for including the same in

expanding the operations of the company 1.

Discussion

Leasing Of Assets

The process of financing the assets involves acquiring the necessary equipment’s and

assets for a business in order to operate where the company could not afford the assets.

American Coffee House could adopt various type of asset financing like

Leasing: the lessor lends Assets for a fixed period in exchange for a defined period of rental

payments by the lessee to lessor.

Hire Purchase Arrangements: The next best available option for financing the assets is in

the form of Hire Purchase where an initial deposit will be paid for the deposit of the asset and

the remaining balance of the asset will be paid in a fixed period. After making the full and

final payment of all the remaining balance of the asset, the ownership of the asset is

transferred from the lessor to the lessee (1).

The advantages of leasing or renting an equipment are:

In the case of asset financing or leasing the lessor, do not have to pay the full amount

of acquiring the asset rather they have to pay a minimum amount for using the same.

Introduction

Assets is an integral part of an organisation, which is used on a daily basis by the

organisation for their daily operational works. The principal of Capital Investment will be

applied for the purpose of evaluation and analysis of the financial viability of the project. The

Asset taken into consideration by the American Coffee house for including the same in

expanding the operations of the company 1.

Discussion

Leasing Of Assets

The process of financing the assets involves acquiring the necessary equipment’s and

assets for a business in order to operate where the company could not afford the assets.

American Coffee House could adopt various type of asset financing like

Leasing: the lessor lends Assets for a fixed period in exchange for a defined period of rental

payments by the lessee to lessor.

Hire Purchase Arrangements: The next best available option for financing the assets is in

the form of Hire Purchase where an initial deposit will be paid for the deposit of the asset and

the remaining balance of the asset will be paid in a fixed period. After making the full and

final payment of all the remaining balance of the asset, the ownership of the asset is

transferred from the lessor to the lessee (1).

The advantages of leasing or renting an equipment are:

In the case of asset financing or leasing the lessor, do not have to pay the full amount

of acquiring the asset rather they have to pay a minimum amount for using the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCIAL MANAGEMENT

Getting access to better and premium equipment can be well possible with the help of

leasing or asset financing where the initial investment in the asset would be

comparatively lower for the company.

The rental amount that would be paid by the lessor to the lessee for the financing of

the asset is usually fixed which makes it easy for both the party to value the contract

in terms of present value.

The lease payment that would be paid by the company or the lessor would be treated

as a taxable expense, which in turn reduces the effective tax rate of the lessor.

Risk and maintenance of the asset would not be borne by the lessor, which reduces the

risk associated with an asset in terms of breakdown or replacement of the assets (2).

Disadvantages of leasing or renting and equipment are:

The lessor would not be able to claim capital allowances on the leased assets if the

lease period under which the asset will be leased is less than for a sum of five

years of period or seven years in some cases.

The leasing policies and the fixed amount payable by the company would not also

be in the best interest of the lessor.

The option of buying the assets is not always applicable in the case of the leasing

where the lessor might actually want to purchase the same.

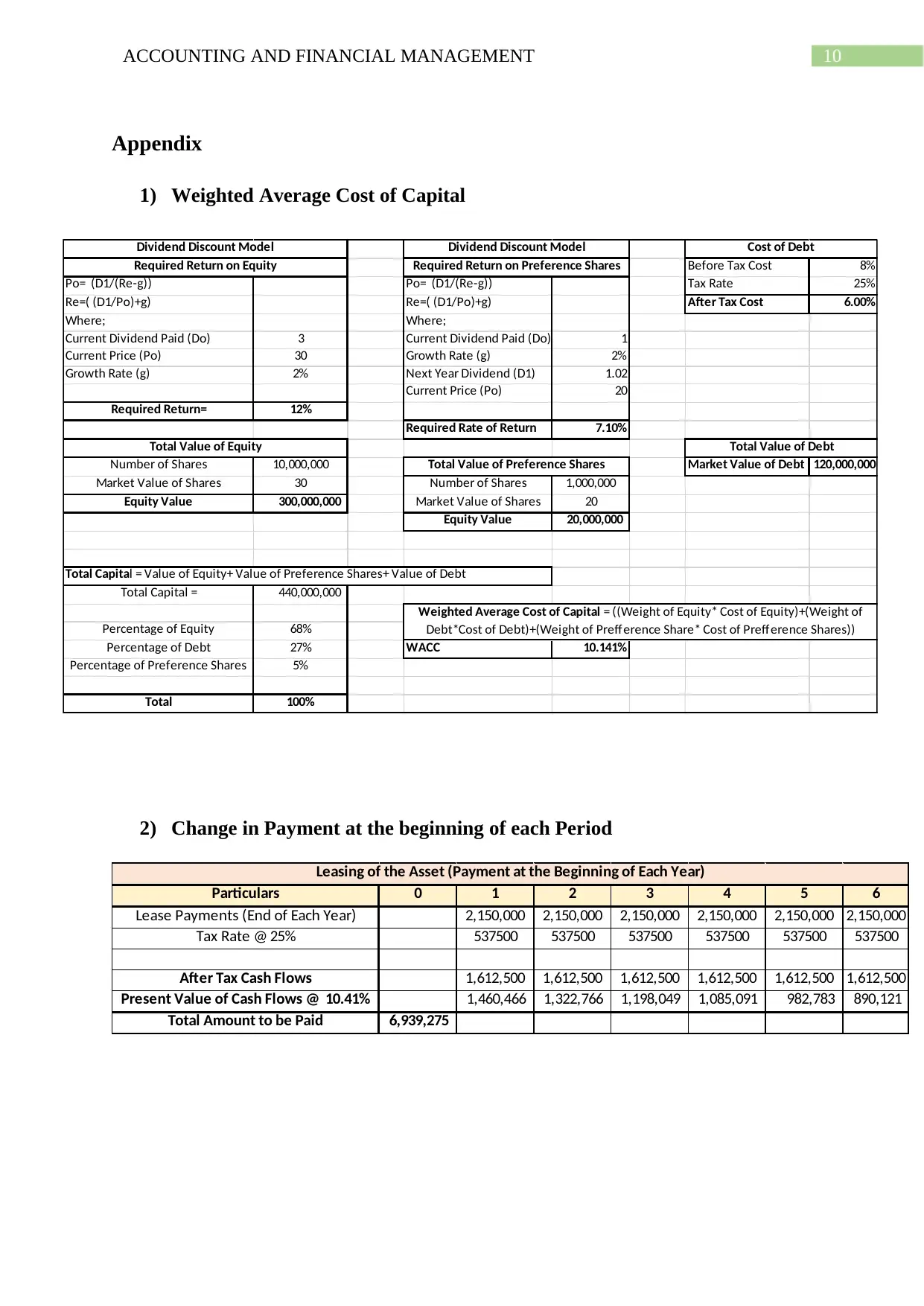

Weighted Average Cost of Capital

The weighted average cost of capital shows the minimum rate of return required by

the company for financing the operations and the various activities of the company. The

weighted average cost of capital is calculated with the help of the debt, equity and preference

share financing of the company and the various rates (2). The weighted average of each of

the sources of capital was done with the help of the following formula:

Getting access to better and premium equipment can be well possible with the help of

leasing or asset financing where the initial investment in the asset would be

comparatively lower for the company.

The rental amount that would be paid by the lessor to the lessee for the financing of

the asset is usually fixed which makes it easy for both the party to value the contract

in terms of present value.

The lease payment that would be paid by the company or the lessor would be treated

as a taxable expense, which in turn reduces the effective tax rate of the lessor.

Risk and maintenance of the asset would not be borne by the lessor, which reduces the

risk associated with an asset in terms of breakdown or replacement of the assets (2).

Disadvantages of leasing or renting and equipment are:

The lessor would not be able to claim capital allowances on the leased assets if the

lease period under which the asset will be leased is less than for a sum of five

years of period or seven years in some cases.

The leasing policies and the fixed amount payable by the company would not also

be in the best interest of the lessor.

The option of buying the assets is not always applicable in the case of the leasing

where the lessor might actually want to purchase the same.

Weighted Average Cost of Capital

The weighted average cost of capital shows the minimum rate of return required by

the company for financing the operations and the various activities of the company. The

weighted average cost of capital is calculated with the help of the debt, equity and preference

share financing of the company and the various rates (2). The weighted average of each of

the sources of capital was done with the help of the following formula:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCIAL MANAGEMENT

Weighted Average Cost of Capital = ((Weight of Equity* Cost of Equity) + (Weight of

Debt*Cost of Debt) + (Weight of Preference Share* Cost of Preference Shares)).

The return/rate on equity was calculated with the help of the dividend discount model

where the formula applied was:

Required Return of Equity: (D1/Po) + Growth Rate.

The required return on equity was calculated to be around 12% and the return on

preference share was calculated to be around 7.10%. The after tax cost of debt was calculated

to be around 6% taking the tax rate at 25%. The weighted average cost of capital was

calculated to be around 10.141% and the same has been calculated by using the relevant

weight of the capital and the relevant cost involved in the same (Appendix 1).

Net Advantage to Leasing Analysis

The leasing method will be analysed based on the annual payment of $2.15 million

that would be paid for a sum of six years of period. The payment was discounted with the

help of the weighted average cost of capital that was determined for the company, which was

around 10.141%, and the same was used for discounting the cash flows that would be paid by

the company for getting the actual sum of investment that is paid by the company for using

the assets (3).

Changes in Value when Payment is done at the End of Period: The net value determined

for the asset was around $7,661,654 million (4). The annual lease payment was taken into

consideration for a sum of six years of time and the same was taxed at the taxation rate of

25% for determining the actual value to be paid by the lessor (Appendix 2).

Changes in Value when Payment is done at the Beginning of Period: The net value

determined for the asset was around $6,939,275 million (5). The annual lease payment was

Weighted Average Cost of Capital = ((Weight of Equity* Cost of Equity) + (Weight of

Debt*Cost of Debt) + (Weight of Preference Share* Cost of Preference Shares)).

The return/rate on equity was calculated with the help of the dividend discount model

where the formula applied was:

Required Return of Equity: (D1/Po) + Growth Rate.

The required return on equity was calculated to be around 12% and the return on

preference share was calculated to be around 7.10%. The after tax cost of debt was calculated

to be around 6% taking the tax rate at 25%. The weighted average cost of capital was

calculated to be around 10.141% and the same has been calculated by using the relevant

weight of the capital and the relevant cost involved in the same (Appendix 1).

Net Advantage to Leasing Analysis

The leasing method will be analysed based on the annual payment of $2.15 million

that would be paid for a sum of six years of period. The payment was discounted with the

help of the weighted average cost of capital that was determined for the company, which was

around 10.141%, and the same was used for discounting the cash flows that would be paid by

the company for getting the actual sum of investment that is paid by the company for using

the assets (3).

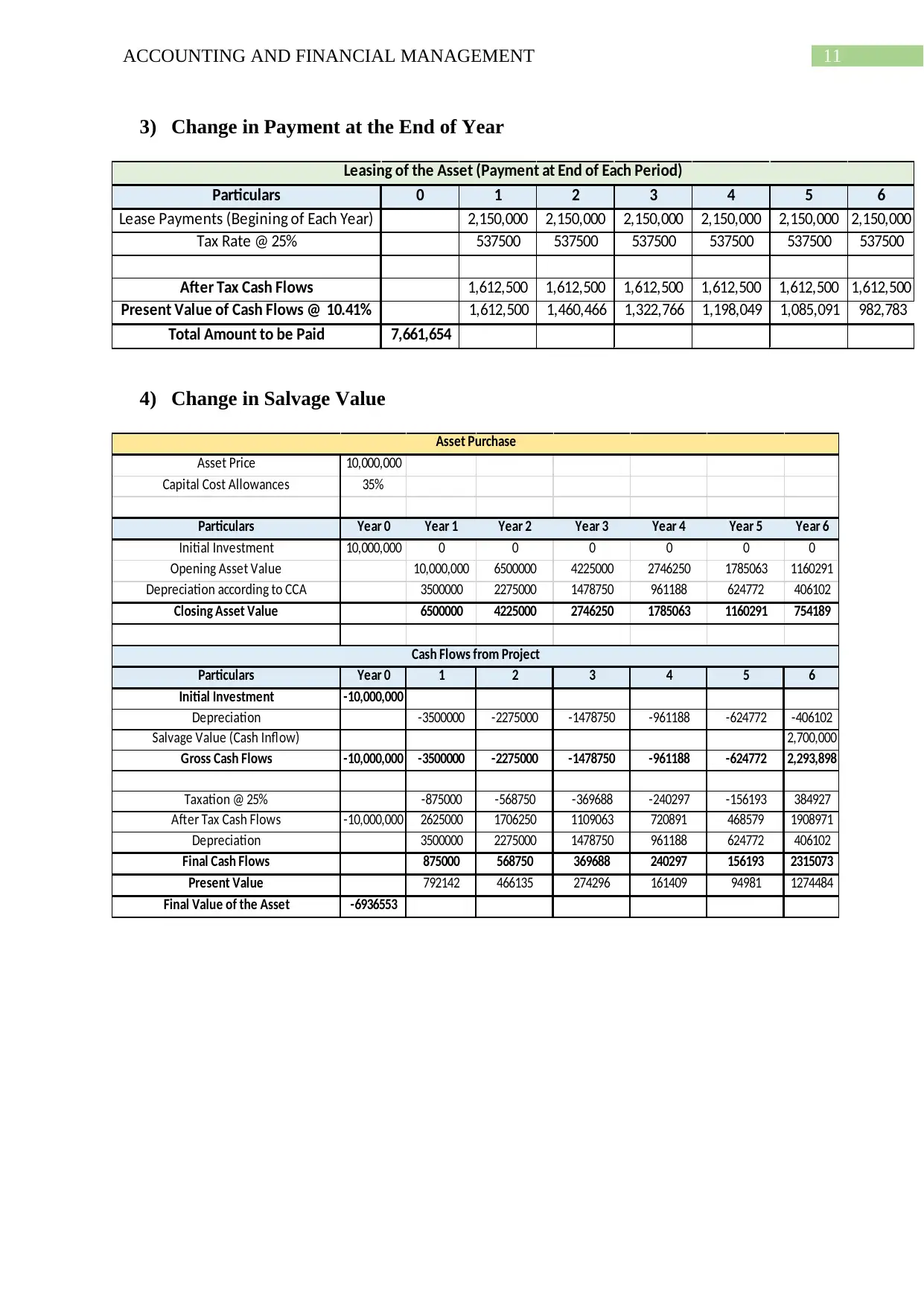

Changes in Value when Payment is done at the End of Period: The net value determined

for the asset was around $7,661,654 million (4). The annual lease payment was taken into

consideration for a sum of six years of time and the same was taxed at the taxation rate of

25% for determining the actual value to be paid by the lessor (Appendix 2).

Changes in Value when Payment is done at the Beginning of Period: The net value

determined for the asset was around $6,939,275 million (5). The annual lease payment was

5ACCOUNTING AND FINANCIAL MANAGEMENT

taken into consideration for a sum of six years of time and the same was taxed at the taxation

rate of 25% for determining the actual value to be paid by the lessor. The value determined is

much lower than the above value reflecting the impact of time value of money (Appendix 3).

Change in Salvage Value: If the salvage value of the asset changes from 1.5 million dollar

to about 2.7 million dollar then the same would be affecting the cost involved in the purchase

of the assets (6). The net value of the assets that would be paid by the lessor would ultimately

be reduced for the company in the form of the higher salvage value of the assets. The net cost

that would be paid by the American Coffee house if the salvage value changes and after

accounting for all the tax shield the company would be getting would be around $6,936,553

million (Appendix 4).

Security Deposit: The value of the asset would change if there would be an initial

investment of $800,000 in the first year in the case of lease payment scenario (7). The lease

payment would be $2.15 million as it is in the six years of period. The after tax cash flows

were discounted at a rate of 10.141% where the value of the asset at today’s times was around

$6,861,654.

Breakeven Lease Payment: The breakeven lease payment for the company where the

payment requested on a lease agreement by a party to a potential agreement is indifferent in

regards to either entering or non-entering into the lease agreements (8). In the above various

case analysed for the company it was found that the American Coffee House would be paying

the lowest in the case of first scenario when the payment is made at the beginning of each

year when the company will be able to receive and utilize the asset in the lowest possible

value, which is around $6,939,275.

taken into consideration for a sum of six years of time and the same was taxed at the taxation

rate of 25% for determining the actual value to be paid by the lessor. The value determined is

much lower than the above value reflecting the impact of time value of money (Appendix 3).

Change in Salvage Value: If the salvage value of the asset changes from 1.5 million dollar

to about 2.7 million dollar then the same would be affecting the cost involved in the purchase

of the assets (6). The net value of the assets that would be paid by the lessor would ultimately

be reduced for the company in the form of the higher salvage value of the assets. The net cost

that would be paid by the American Coffee house if the salvage value changes and after

accounting for all the tax shield the company would be getting would be around $6,936,553

million (Appendix 4).

Security Deposit: The value of the asset would change if there would be an initial

investment of $800,000 in the first year in the case of lease payment scenario (7). The lease

payment would be $2.15 million as it is in the six years of period. The after tax cash flows

were discounted at a rate of 10.141% where the value of the asset at today’s times was around

$6,861,654.

Breakeven Lease Payment: The breakeven lease payment for the company where the

payment requested on a lease agreement by a party to a potential agreement is indifferent in

regards to either entering or non-entering into the lease agreements (8). In the above various

case analysed for the company it was found that the American Coffee House would be paying

the lowest in the case of first scenario when the payment is made at the beginning of each

year when the company will be able to receive and utilize the asset in the lowest possible

value, which is around $6,939,275.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCIAL MANAGEMENT

Leasing or Purchase

The analysis from the perspective of the company would be based on the case that the

financial viability and the cost involved in the same would be the key factor that will be taken

into analysis for the purpose of evaluation (9). The assets of the company would be leased if

the present value of the asset were certainly less in the case of lease payment then the

purchase of assets. In the case of leasing an asset it would be certain that in the base case

where payment are made at the beginning of each year the total value of the asset would be

around $7,432,018 million. The salvage value of the asset was taken at 1.5 million in the

evaluation of the project. On the other hand, if the American Coffee House leased the asset

then the value of the asset or the total payment that the company needs to pay would be

around $6,939,275. The same was done by taking an assumption that the payment will be

done at the beginning of each year. However, it is recommended that the company goes for

leasing the asset as the company would be enjoying the benefits of leasing where the

company would not be having the risks associated with the asset such as wear and tear,

maintenance risk and various other problems (10).

Classification of Lease Payments

The classification of the lease payment would be done in accordance with the various

factors and scenarios taken into consideration for the analysis of the project. The sensitivity

analysis from the project could be taken into consideration when payment of the lease will be

at a different point of time if the payment is made at the beginning of each year the value of

the contract or the lease would be worth around $6,939,275. On the other hand, if the value of

the lease changes to payment made at the end of period then the value of the contract or lease

would be around $7,661,654. The same is higher due to payment, which will be made at the

end of the year. Leasing of the asset would differs in different condition reflecting the value

Leasing or Purchase

The analysis from the perspective of the company would be based on the case that the

financial viability and the cost involved in the same would be the key factor that will be taken

into analysis for the purpose of evaluation (9). The assets of the company would be leased if

the present value of the asset were certainly less in the case of lease payment then the

purchase of assets. In the case of leasing an asset it would be certain that in the base case

where payment are made at the beginning of each year the total value of the asset would be

around $7,432,018 million. The salvage value of the asset was taken at 1.5 million in the

evaluation of the project. On the other hand, if the American Coffee House leased the asset

then the value of the asset or the total payment that the company needs to pay would be

around $6,939,275. The same was done by taking an assumption that the payment will be

done at the beginning of each year. However, it is recommended that the company goes for

leasing the asset as the company would be enjoying the benefits of leasing where the

company would not be having the risks associated with the asset such as wear and tear,

maintenance risk and various other problems (10).

Classification of Lease Payments

The classification of the lease payment would be done in accordance with the various

factors and scenarios taken into consideration for the analysis of the project. The sensitivity

analysis from the project could be taken into consideration when payment of the lease will be

at a different point of time if the payment is made at the beginning of each year the value of

the contract or the lease would be worth around $6,939,275. On the other hand, if the value of

the lease changes to payment made at the end of period then the value of the contract or lease

would be around $7,661,654. The same is higher due to payment, which will be made at the

end of the year. Leasing of the asset would differs in different condition reflecting the value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCIAL MANAGEMENT

of the contract. The lease payment would also change if the value of the asset changes from

one year to another when the payment of lease would change (11).

Conclusion

The evaluation and analysis of the asset were done in the case of American Coffee

house were the value of the asset would differ in different condition. The value of the asset

and lease analysis was done in different condition where the evaluation of the company was

done from the investor’s perspective. It was observed from the above case that the value of

the asset in the case of leasing and purchase was analysed reflecting the value of the contract

in the case of lease and the value of the asset in case of purchase.

of the contract. The lease payment would also change if the value of the asset changes from

one year to another when the payment of lease would change (11).

Conclusion

The evaluation and analysis of the asset were done in the case of American Coffee

house were the value of the asset would differ in different condition. The value of the asset

and lease analysis was done in different condition where the evaluation of the company was

done from the investor’s perspective. It was observed from the above case that the value of

the asset in the case of leasing and purchase was analysed reflecting the value of the contract

in the case of lease and the value of the asset in case of purchase.

8ACCOUNTING AND FINANCIAL MANAGEMENT

References

1. Saunders A, Brynjolfsson E. Valuing Information Technology Related Intangible

Assets. Mis Quarterly. 2016 Mar 1;40(1).

2. Cosci S, Guida R, Meliciani V. Leasing decisions and credit constraints: Empirical

analysis on a sample of Italian firms. European Financial Management. 2015

Mar;21(2):377-98.

3. Propheter G, Hatch ME. Evaluating lease-purchase financing for professional sports

facilities. Urban Affairs Review. 2015 Nov;51(6):905-25.

4. Gao SS. International leasing: strategy and decision. Routledge; 2018 Dec 20.

5. Fatima M. Differences and similarities between Ijara and conventional operating lease

contracts. Market Forces. 2016 Jun 26;1(4).

6. Li T, Karim R, Munir Q. The determinants of leasing decisions: an empirical analysis

from Chinese listed SMEs. Managerial Finance. 2016 Aug 8;42(8):763-80.

7. Nuryani N, Heng TT, Juliesta N. Capitalization of Operating Lease and Its Impact on

Firm's Financial Ratios. Procedia-Social and Behavioral Sciences. 2015 Nov

25;211:268-76.

8. André C, Boulet D, Rey-Valette H, Rulleau B. Protection by hard defence structures

or relocation of assets exposed to coastal risks: Contributions and drawbacks of cost-

benefit analysis for long-term adaptation choices to climate change. Ocean & coastal

management. 2016 Dec 1;134:173-82.

9. Bourjade S, Huc R, Muller-Vibes C. Leasing and profitability: Empirical evidence

from the airline industry. Transportation Research Part A: Policy and Practice. 2017

Mar 1;97:30-46.

10. Kolpak EP, Gorynya EV, Shaposhnikova AI, Khasenova KE, Zemlyakova NS.

Special aspects of leasing activities and its meaning in conditions of enterprise

References

1. Saunders A, Brynjolfsson E. Valuing Information Technology Related Intangible

Assets. Mis Quarterly. 2016 Mar 1;40(1).

2. Cosci S, Guida R, Meliciani V. Leasing decisions and credit constraints: Empirical

analysis on a sample of Italian firms. European Financial Management. 2015

Mar;21(2):377-98.

3. Propheter G, Hatch ME. Evaluating lease-purchase financing for professional sports

facilities. Urban Affairs Review. 2015 Nov;51(6):905-25.

4. Gao SS. International leasing: strategy and decision. Routledge; 2018 Dec 20.

5. Fatima M. Differences and similarities between Ijara and conventional operating lease

contracts. Market Forces. 2016 Jun 26;1(4).

6. Li T, Karim R, Munir Q. The determinants of leasing decisions: an empirical analysis

from Chinese listed SMEs. Managerial Finance. 2016 Aug 8;42(8):763-80.

7. Nuryani N, Heng TT, Juliesta N. Capitalization of Operating Lease and Its Impact on

Firm's Financial Ratios. Procedia-Social and Behavioral Sciences. 2015 Nov

25;211:268-76.

8. André C, Boulet D, Rey-Valette H, Rulleau B. Protection by hard defence structures

or relocation of assets exposed to coastal risks: Contributions and drawbacks of cost-

benefit analysis for long-term adaptation choices to climate change. Ocean & coastal

management. 2016 Dec 1;134:173-82.

9. Bourjade S, Huc R, Muller-Vibes C. Leasing and profitability: Empirical evidence

from the airline industry. Transportation Research Part A: Policy and Practice. 2017

Mar 1;97:30-46.

10. Kolpak EP, Gorynya EV, Shaposhnikova AI, Khasenova KE, Zemlyakova NS.

Special aspects of leasing activities and its meaning in conditions of enterprise

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCIAL MANAGEMENT

competitiveness. International Review of Management and Marketing. 2016 Aug

18;6(6S):126-33.

11. Rampini AA. Financing durable assets. American Economic Review. 2019

Feb;109(2):664-701.

competitiveness. International Review of Management and Marketing. 2016 Aug

18;6(6S):126-33.

11. Rampini AA. Financing durable assets. American Economic Review. 2019

Feb;109(2):664-701.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCIAL MANAGEMENT

Appendix

1) Weighted Average Cost of Capital

2) Change in Payment at the beginning of each Period

Particulars 0 1 2 3 4 5 6

Lease Payments (End of Each Year) 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000

Tax Rate @ 25% 537500 537500 537500 537500 537500 537500

After Tax Cash Flows 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500

Present Value of Cash Flows @ 10.41% 1,460,466 1,322,766 1,198,049 1,085,091 982,783 890,121

Total Amount to be Paid 6,939,275

Leasing of the Asset (Payment at the Beginning of Each Year)

Before Tax Cost 8%

Po= (D1/(Re-g)) Po= (D1/(Re-g)) Tax Rate 25%

Re=( (D1/Po)+g) Re=( (D1/Po)+g) After Tax Cost 6.00%

Where; Where;

Current Dividend Paid (Do) 3 Current Dividend Paid (Do) 1

Current Price (Po) 30 Growth Rate (g) 2%

Growth Rate (g) 2% Next Year Dividend (D1) 1.02

Current Price (Po) 20

Required Return= 12%

Required Rate of Return 7.10%

Number of Shares 10,000,000 Market Value of Debt 120,000,000

Market Value of Shares 30 Number of Shares 1,000,000

Equity Value 300,000,000 Market Value of Shares 20

Equity Value 20,000,000

Total Capital = Value of Equity+ Value of Preference Shares+ Value of Debt

Total Capital = 440,000,000

Percentage of Equity 68%

Percentage of Debt 27% WACC 10.141%

Percentage of Preference Shares 5%

Total 100%

Total Value of Equity

Total Value of Preference Shares

Total Value of Debt

Weighted Average Cost of Capital = ((Weight of Equity* Cost of Equity)+(Weight of

Debt*Cost of Debt)+(Weight of Prefference Share* Cost of Prefference Shares))

Required Return on Equity

Dividend Discount Model Dividend Discount Model

Required Return on Preference Shares

Cost of Debt

Appendix

1) Weighted Average Cost of Capital

2) Change in Payment at the beginning of each Period

Particulars 0 1 2 3 4 5 6

Lease Payments (End of Each Year) 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000

Tax Rate @ 25% 537500 537500 537500 537500 537500 537500

After Tax Cash Flows 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500

Present Value of Cash Flows @ 10.41% 1,460,466 1,322,766 1,198,049 1,085,091 982,783 890,121

Total Amount to be Paid 6,939,275

Leasing of the Asset (Payment at the Beginning of Each Year)

Before Tax Cost 8%

Po= (D1/(Re-g)) Po= (D1/(Re-g)) Tax Rate 25%

Re=( (D1/Po)+g) Re=( (D1/Po)+g) After Tax Cost 6.00%

Where; Where;

Current Dividend Paid (Do) 3 Current Dividend Paid (Do) 1

Current Price (Po) 30 Growth Rate (g) 2%

Growth Rate (g) 2% Next Year Dividend (D1) 1.02

Current Price (Po) 20

Required Return= 12%

Required Rate of Return 7.10%

Number of Shares 10,000,000 Market Value of Debt 120,000,000

Market Value of Shares 30 Number of Shares 1,000,000

Equity Value 300,000,000 Market Value of Shares 20

Equity Value 20,000,000

Total Capital = Value of Equity+ Value of Preference Shares+ Value of Debt

Total Capital = 440,000,000

Percentage of Equity 68%

Percentage of Debt 27% WACC 10.141%

Percentage of Preference Shares 5%

Total 100%

Total Value of Equity

Total Value of Preference Shares

Total Value of Debt

Weighted Average Cost of Capital = ((Weight of Equity* Cost of Equity)+(Weight of

Debt*Cost of Debt)+(Weight of Prefference Share* Cost of Prefference Shares))

Required Return on Equity

Dividend Discount Model Dividend Discount Model

Required Return on Preference Shares

Cost of Debt

11ACCOUNTING AND FINANCIAL MANAGEMENT

3) Change in Payment at the End of Year

Particulars 0 1 2 3 4 5 6

Lease Payments (Begining of Each Year) 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000

Tax Rate @ 25% 537500 537500 537500 537500 537500 537500

After Tax Cash Flows 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500

Present Value of Cash Flows @ 10.41% 1,612,500 1,460,466 1,322,766 1,198,049 1,085,091 982,783

Total Amount to be Paid 7,661,654

Leasing of the Asset (Payment at End of Each Period)

4) Change in Salvage Value

Asset Price 10,000,000

Capital Cost Allowances 35%

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Initial Investment 10,000,000 0 0 0 0 0 0

Opening Asset Value 10,000,000 6500000 4225000 2746250 1785063 1160291

Depreciation according to CCA 3500000 2275000 1478750 961188 624772 406102

Closing Asset Value 6500000 4225000 2746250 1785063 1160291 754189

Particulars Year 0 1 2 3 4 5 6

Initial Investment -10,000,000

Depreciation -3500000 -2275000 -1478750 -961188 -624772 -406102

Salvage Value (Cash Inflow) 2,700,000

Gross Cash Flows -10,000,000 -3500000 -2275000 -1478750 -961188 -624772 2,293,898

Taxation @ 25% -875000 -568750 -369688 -240297 -156193 384927

After Tax Cash Flows -10,000,000 2625000 1706250 1109063 720891 468579 1908971

Depreciation 3500000 2275000 1478750 961188 624772 406102

Final Cash Flows 875000 568750 369688 240297 156193 2315073

Present Value 792142 466135 274296 161409 94981 1274484

Final Value of the Asset -6936553

Asset Purchase

Cash Flows from Project

3) Change in Payment at the End of Year

Particulars 0 1 2 3 4 5 6

Lease Payments (Begining of Each Year) 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000 2,150,000

Tax Rate @ 25% 537500 537500 537500 537500 537500 537500

After Tax Cash Flows 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500 1,612,500

Present Value of Cash Flows @ 10.41% 1,612,500 1,460,466 1,322,766 1,198,049 1,085,091 982,783

Total Amount to be Paid 7,661,654

Leasing of the Asset (Payment at End of Each Period)

4) Change in Salvage Value

Asset Price 10,000,000

Capital Cost Allowances 35%

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Initial Investment 10,000,000 0 0 0 0 0 0

Opening Asset Value 10,000,000 6500000 4225000 2746250 1785063 1160291

Depreciation according to CCA 3500000 2275000 1478750 961188 624772 406102

Closing Asset Value 6500000 4225000 2746250 1785063 1160291 754189

Particulars Year 0 1 2 3 4 5 6

Initial Investment -10,000,000

Depreciation -3500000 -2275000 -1478750 -961188 -624772 -406102

Salvage Value (Cash Inflow) 2,700,000

Gross Cash Flows -10,000,000 -3500000 -2275000 -1478750 -961188 -624772 2,293,898

Taxation @ 25% -875000 -568750 -369688 -240297 -156193 384927

After Tax Cash Flows -10,000,000 2625000 1706250 1109063 720891 468579 1908971

Depreciation 3500000 2275000 1478750 961188 624772 406102

Final Cash Flows 875000 568750 369688 240297 156193 2315073

Present Value 792142 466135 274296 161409 94981 1274484

Final Value of the Asset -6936553

Asset Purchase

Cash Flows from Project

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.