Analyzing Lease Transactions: Corporate Accounting and AASB 117 Impact

VerifiedAdded on 2023/06/11

|9

|1427

|99

Essay

AI Summary

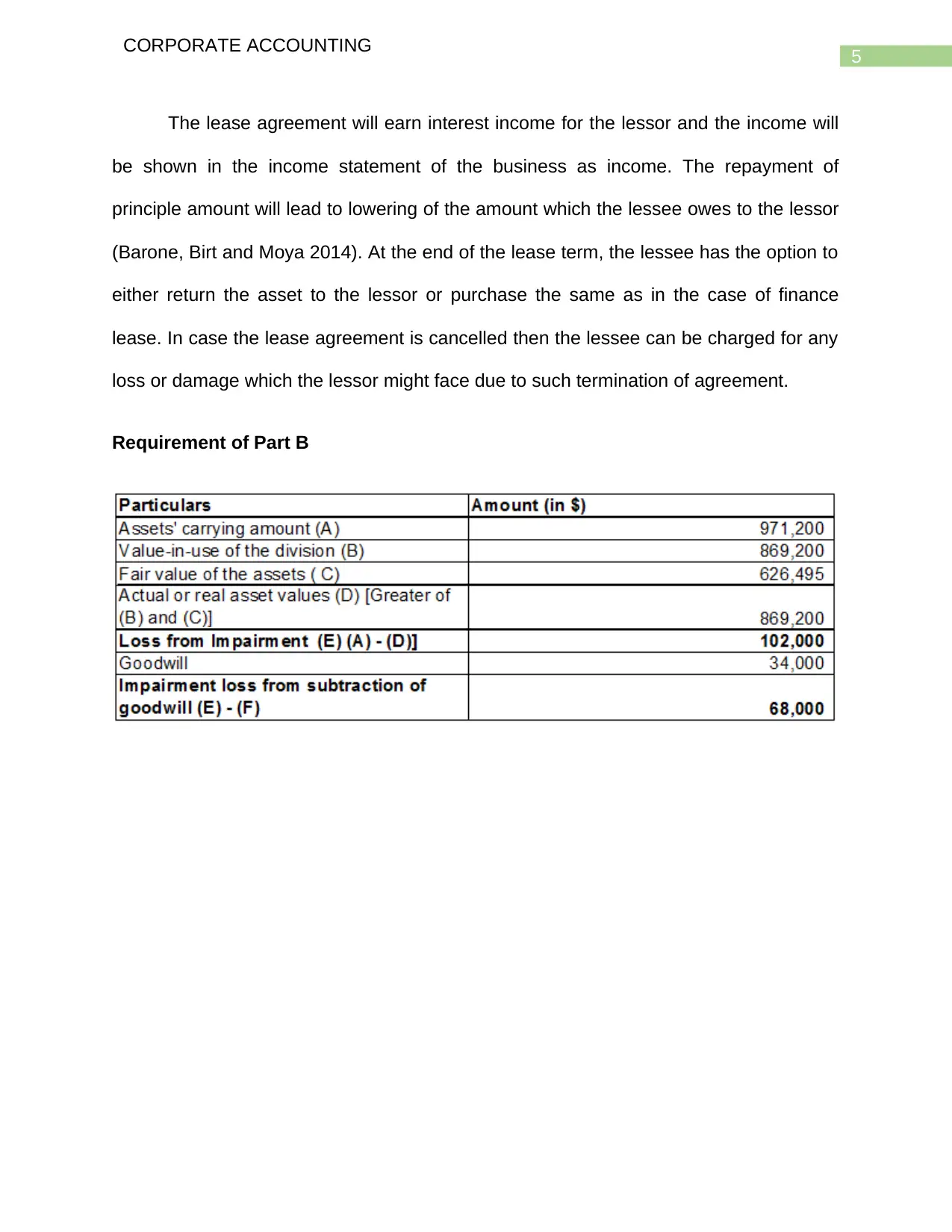

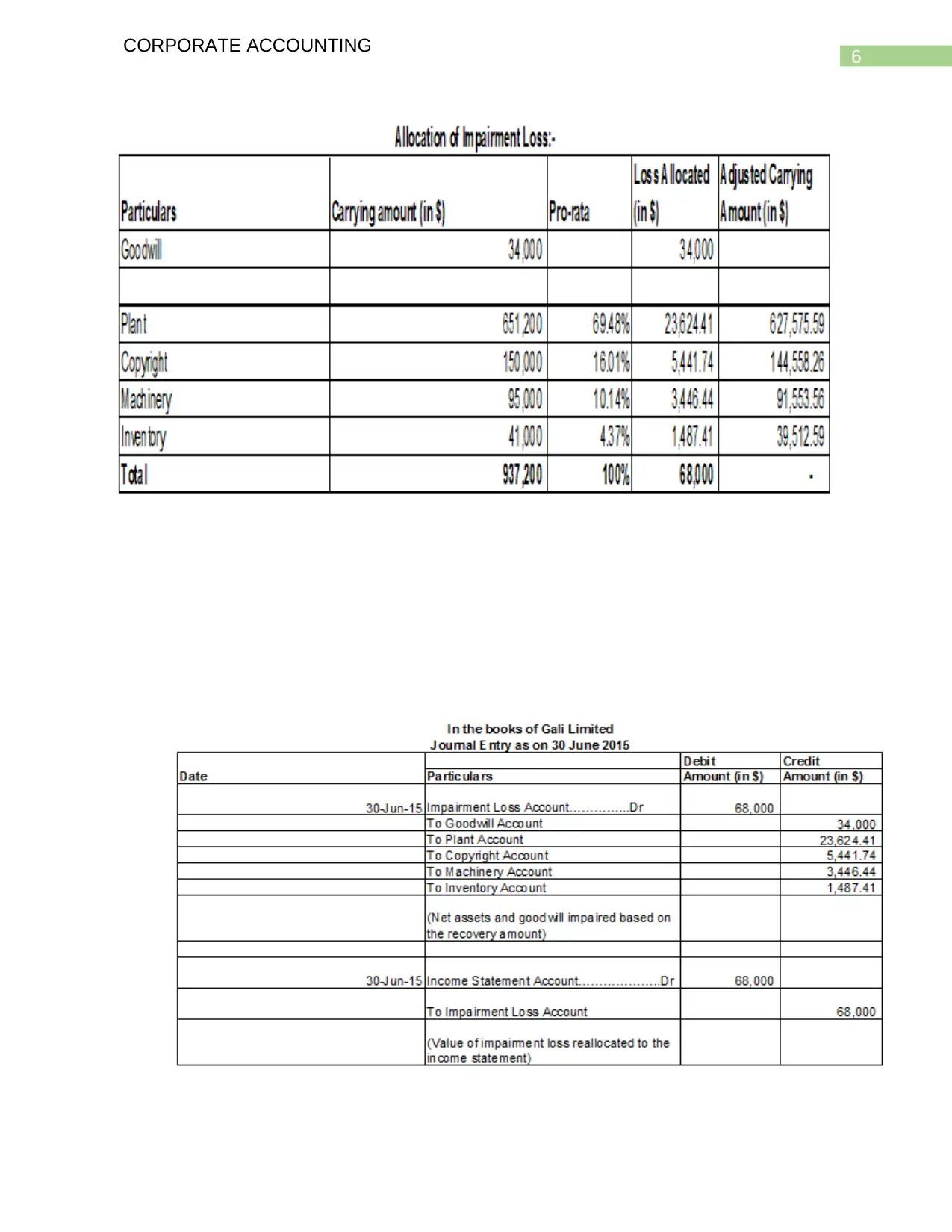

This essay delves into the intricacies of lease transactions within corporate accounting, focusing on the disclosure requirements stipulated by AASB 117 and IAS 17. It differentiates between operating and financial leases, highlighting that operating leases are short-term arrangements where the lessor retains asset risks and rewards, while financial leases transfer these aspects to the lessee, potentially including a purchase option at lease end. The essay also touches upon upcoming amendments with AASB 16 replacing AASB 117, primarily affecting operating lease disclosures. It outlines specific disclosure requirements for both lessors and lessees, including net carrying amounts, lease payment reconciliations, contingent rents, and terms associated with lease agreements, with a brief discussion on how these obligations are reflected as current and non-current liabilities, and how interest income is recognized by the lessor. The essay further discusses the implications of lease agreement cancellations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.