Developing an Audit Program for Legend Corporation Limited: Report

VerifiedAdded on 2022/11/10

|21

|4777

|213

Report

AI Summary

This report provides a comprehensive audit analysis of Legend Corporation Limited, an Australian engineering services company. It begins with an executive summary and an introduction to the importance of auditing, followed by an identification of key business risks such as interest rate risk, foreign currency risk, liquidity risk, and credit risk. The report then delves into material misstatements, audit risk models, and analytical procedures, including ratio analysis to assess financial performance and position. It discusses the concept of materiality, identifies material accounts, and outlines corresponding assertions and audit procedures. The report emphasizes the use of sampling methods for testing material accounts and concludes with a summary of findings and recommendations. References are provided to support the analysis.

1

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

Auditing is an important process which is carried in all the companies. There is the

identification of the risk which is involved and the same is then reported in the reports. The

important elements in this respect have been provided in the report. There is the identification of

the risks which are there in the business process. In them there is the consideration of the audit

risk model which is involved. There is the ratio calculation and by that all of the aspects in

relation to the financial information have been considered. The performance of the business is

identified it is noted that there are adequate profitability and liquidity which is maintained by the

company. The assertions in relation to the material accounts have been identified and that will

help in carrying the proper procedure. The sampling method which will be used for the relayed

accounts has also been ascertained.

Executive summary

Auditing is an important process which is carried in all the companies. There is the

identification of the risk which is involved and the same is then reported in the reports. The

important elements in this respect have been provided in the report. There is the identification of

the risks which are there in the business process. In them there is the consideration of the audit

risk model which is involved. There is the ratio calculation and by that all of the aspects in

relation to the financial information have been considered. The performance of the business is

identified it is noted that there are adequate profitability and liquidity which is maintained by the

company. The assertions in relation to the material accounts have been identified and that will

help in carrying the proper procedure. The sampling method which will be used for the relayed

accounts has also been ascertained.

3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Key business risks............................................................................................................................5

Material misstatement......................................................................................................................6

Audit risk model..............................................................................................................................7

The analytical procedure..................................................................................................................8

Materiality......................................................................................................................................10

Material accounts, assertions, and audit procedures......................................................................11

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Key business risks............................................................................................................................5

Material misstatement......................................................................................................................6

Audit risk model..............................................................................................................................7

The analytical procedure..................................................................................................................8

Materiality......................................................................................................................................10

Material accounts, assertions, and audit procedures......................................................................11

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

Risk is an important aspect which is involved in all the businesses and will be required to

be taken into consideration. For this purpose, there is the undertaking of the audit in which all of

them are evaluated. In this report all of the aspects in this respect will be identified and covered

in an appropriate manner. This will be done with context to the legend corporation limited. There

are several business risks which are involved and with that there will be audit risk which will be

linked to it. There will be identification of them which exist in the company and then proper

evaluation of them will be made. There will be analyzation of the financial aspects and in that

there will be undertaking of the analytical procedure which is involved in auditing. There is the

ratio analysis which will be performed and with that there will be identification of the financial

position and performance.

The materiality concept will be discussed and with the help of that all of the material

account balances will be taken into account. They will be identified and then the assertions

which are available in their respect will be determined. The company is required to make the

proper testing and for that sampling is taken into use which will be performed. All of the

sampling methods which will be used by the company for the material accounts will be identified

and a plan will be formulated.

Introduction

Risk is an important aspect which is involved in all the businesses and will be required to

be taken into consideration. For this purpose, there is the undertaking of the audit in which all of

them are evaluated. In this report all of the aspects in this respect will be identified and covered

in an appropriate manner. This will be done with context to the legend corporation limited. There

are several business risks which are involved and with that there will be audit risk which will be

linked to it. There will be identification of them which exist in the company and then proper

evaluation of them will be made. There will be analyzation of the financial aspects and in that

there will be undertaking of the analytical procedure which is involved in auditing. There is the

ratio analysis which will be performed and with that there will be identification of the financial

position and performance.

The materiality concept will be discussed and with the help of that all of the material

account balances will be taken into account. They will be identified and then the assertions

which are available in their respect will be determined. The company is required to make the

proper testing and for that sampling is taken into use which will be performed. All of the

sampling methods which will be used by the company for the material accounts will be identified

and a plan will be formulated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Key business risks

Legend Corporation Limited is an Australian company which is involved in the

engineering service providing. In addition to that various other operations are carried in relation

to the power, mining, rail, medical, semiconductor and information technology. The company is

carrying out the business from 1962 and is very successful by making the expansion in New

Zealand, Australia and Pacific regions (Legend Corporation Limited, 2019). There are export

services which are provided to various countries including China, USA, and Europe. The

company is expanding and for that, there are various products which are provided by it including

tools, consumables, components and measurement tests. There are certifications which have been

adopted by the company in relation to the standards which are applicable to them.

There are several processes and actions which are undertaken by the company and in the

various aspects are involved. There are the risks which are involved in this process and a

description of them is provided below. Most of them are due to the financial instruments which

are held by the company.

Interest rate risks: In the business, there are various financial assets and liabilities which

are involved and in relation to them there is the interest rate risk which is identified at the

reporting date. There will be change in the future which will be taking place and by that the cash

flows which will be involved in the future will be affected. There are floating rate instruments

which are involved in the company and they are experiencing the earnings volatility due to this.

The company has made the policy in this respect according to which all the interest rates risk

which is there in relation to the long term financing will be minimized (Zamboni & Litschig,

2018). For this the correct combination of the floating and fixed interest debt will be made.

Foreign currency risk: There are several overseas sales which are made by the company

and in that the fluctuation of the currency is faced which gives rise to this risk. In order to deal

with this, the proper monitoring is made for all the cash flows which are made in any other

currency. The risk management policy is taken into use and all the forward exchange contracts

are made in accordance with them. In order to minimize this risk there is the continuous

assessment which is made in relation to the financial instruments.

Key business risks

Legend Corporation Limited is an Australian company which is involved in the

engineering service providing. In addition to that various other operations are carried in relation

to the power, mining, rail, medical, semiconductor and information technology. The company is

carrying out the business from 1962 and is very successful by making the expansion in New

Zealand, Australia and Pacific regions (Legend Corporation Limited, 2019). There are export

services which are provided to various countries including China, USA, and Europe. The

company is expanding and for that, there are various products which are provided by it including

tools, consumables, components and measurement tests. There are certifications which have been

adopted by the company in relation to the standards which are applicable to them.

There are several processes and actions which are undertaken by the company and in the

various aspects are involved. There are the risks which are involved in this process and a

description of them is provided below. Most of them are due to the financial instruments which

are held by the company.

Interest rate risks: In the business, there are various financial assets and liabilities which

are involved and in relation to them there is the interest rate risk which is identified at the

reporting date. There will be change in the future which will be taking place and by that the cash

flows which will be involved in the future will be affected. There are floating rate instruments

which are involved in the company and they are experiencing the earnings volatility due to this.

The company has made the policy in this respect according to which all the interest rates risk

which is there in relation to the long term financing will be minimized (Zamboni & Litschig,

2018). For this the correct combination of the floating and fixed interest debt will be made.

Foreign currency risk: There are several overseas sales which are made by the company

and in that the fluctuation of the currency is faced which gives rise to this risk. In order to deal

with this, the proper monitoring is made for all the cash flows which are made in any other

currency. The risk management policy is taken into use and all the forward exchange contracts

are made in accordance with them. In order to minimize this risk there is the continuous

assessment which is made in relation to the financial instruments.

6

Liquidity risk: There are certain situations in which a company faces difficulty in meeting

with the debts and other liabilities. The possibility of the same will be identified as liquidity risk.

In order to make a control on the same there are various aspects which are used by the company

and they include making of the cash flow analysis for the coming period in which all of the

financial, operating and investing activities are undertaken. All of the credit risks which are

involved in relation to the financial assets are managed. The credit profile is kept at the reputable

position and the surplus funds which are available will be invested in the big financial

institutions.

Credit risk: This is the risk in relation to the obligations which are owed by the

counterparty and they will fail to meet them (Michelacci & Schivardi, 2013). The maximum

amount of the risk which can be faced in this category is till the carrying amount which is there

for the financial assets which are available at the reporting date.

Material misstatement

In the process of reporting which is followed in the company, there are various errors

which take place and that is identified as the misstatement. There is a need to identify as they are

considered as an important risk. All of the accounts in which this risk is involved will be

identified and then the action will be taken by which the risk can be eliminated and the financial

statements can be made free from any misstatement. By the help of this the true position of the

business will be reflected and that will help the investors and others in taking the proper

decisions.

The total risk will be consisting of the two main components which are inherent risk and

control risk. It will be required by the auditor to take them into consideration and for that there

will be undertaking of the proper procedure (Chugh, 2016). The risk which is involved in the

business strategy and will be incorporated in all of the activities will be considered as the

inherent risk. It is the risk which is difficult to be identified and controlled. The other is the

control risk which is related to the internal control of the company. The efficiency of the control

system is required to be evaluated and if the same will be weak then the determination of the

other risk will not be possible. This will be the situation in which there will be control risk which

will be involved.

Liquidity risk: There are certain situations in which a company faces difficulty in meeting

with the debts and other liabilities. The possibility of the same will be identified as liquidity risk.

In order to make a control on the same there are various aspects which are used by the company

and they include making of the cash flow analysis for the coming period in which all of the

financial, operating and investing activities are undertaken. All of the credit risks which are

involved in relation to the financial assets are managed. The credit profile is kept at the reputable

position and the surplus funds which are available will be invested in the big financial

institutions.

Credit risk: This is the risk in relation to the obligations which are owed by the

counterparty and they will fail to meet them (Michelacci & Schivardi, 2013). The maximum

amount of the risk which can be faced in this category is till the carrying amount which is there

for the financial assets which are available at the reporting date.

Material misstatement

In the process of reporting which is followed in the company, there are various errors

which take place and that is identified as the misstatement. There is a need to identify as they are

considered as an important risk. All of the accounts in which this risk is involved will be

identified and then the action will be taken by which the risk can be eliminated and the financial

statements can be made free from any misstatement. By the help of this the true position of the

business will be reflected and that will help the investors and others in taking the proper

decisions.

The total risk will be consisting of the two main components which are inherent risk and

control risk. It will be required by the auditor to take them into consideration and for that there

will be undertaking of the proper procedure (Chugh, 2016). The risk which is involved in the

business strategy and will be incorporated in all of the activities will be considered as the

inherent risk. It is the risk which is difficult to be identified and controlled. The other is the

control risk which is related to the internal control of the company. The efficiency of the control

system is required to be evaluated and if the same will be weak then the determination of the

other risk will not be possible. This will be the situation in which there will be control risk which

will be involved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

For the control risk, there is the need to take into consideration the internal policies and

procedures of the company. They will be identified so that the shortcoming in them can be

identified and then the steps for the resolving of them can be made possible. It is not possible to

identify some of the errors which are made in the accounts of the company and due to them the

arising of the inherent risk is made.

In addition to them, there is another risk which is involved and that is identified to be the

detection risk. This is involved in respect of the other risk. In the business there are various risks

which are involved and it is required that they shall be detected on time. If the same is not made

possible then it is known as the detection risk (van Veluw et al., 2017). It will be affecting the

company in an adverse manner and for that there shall be proper process which shall be

formulated in this respect.

The risk in the business is derived because of the various factors which are responsible

for them and in order to eliminate the risk they all shall be identified and considered in a proper

manner. All of the transactions which are taking place will be affected by the inherent risk and

due to that there will be need to control the same. In this there is the need to consider the

liquidity of the business and the complexity of the processes which are involved will also be

taken into account. If the processes will be complex then the issues will be faced to take them

into use and by that the risk will be increased as there will be errors which will be made. If the

control will not be made on them then the negative impact will be faced by the company. The

control process of the company will also be improved by which all the activities can be

controlled. The errors will be identified when the process used for monitoring is strong and by

that the detection risk will be decreased. Due to this it can be said that the risk of detection can

be reduced with the increase control system.

Audit risk model

All of the risks which will be the responsibility of the auditor and will be involved in the

process of the audit are identified as the audit risk. The main task of the auditors is to check all

the transactions so that if there is any error then it will be identified and reported. By this it will

be brought to the notice of all which will help in establishing the control on them. They will be

considering all of the risks and then the audit opinion which will be presented by the auditor will

For the control risk, there is the need to take into consideration the internal policies and

procedures of the company. They will be identified so that the shortcoming in them can be

identified and then the steps for the resolving of them can be made possible. It is not possible to

identify some of the errors which are made in the accounts of the company and due to them the

arising of the inherent risk is made.

In addition to them, there is another risk which is involved and that is identified to be the

detection risk. This is involved in respect of the other risk. In the business there are various risks

which are involved and it is required that they shall be detected on time. If the same is not made

possible then it is known as the detection risk (van Veluw et al., 2017). It will be affecting the

company in an adverse manner and for that there shall be proper process which shall be

formulated in this respect.

The risk in the business is derived because of the various factors which are responsible

for them and in order to eliminate the risk they all shall be identified and considered in a proper

manner. All of the transactions which are taking place will be affected by the inherent risk and

due to that there will be need to control the same. In this there is the need to consider the

liquidity of the business and the complexity of the processes which are involved will also be

taken into account. If the processes will be complex then the issues will be faced to take them

into use and by that the risk will be increased as there will be errors which will be made. If the

control will not be made on them then the negative impact will be faced by the company. The

control process of the company will also be improved by which all the activities can be

controlled. The errors will be identified when the process used for monitoring is strong and by

that the detection risk will be decreased. Due to this it can be said that the risk of detection can

be reduced with the increase control system.

Audit risk model

All of the risks which will be the responsibility of the auditor and will be involved in the

process of the audit are identified as the audit risk. The main task of the auditors is to check all

the transactions so that if there is any error then it will be identified and reported. By this it will

be brought to the notice of all which will help in establishing the control on them. They will be

considering all of the risks and then the audit opinion which will be presented by the auditor will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

be based on them. There will be audit risk model which will be followed in which all of the

elements will be taken into account. The model will be as follows:

Audit risk model = control risk X inherent risk X detection risk

The two main risks which are involved have been identified and they are the inherent and

control risk. The inherent risk which is involved is due to the error or can be said that all of the

material misstatements which are taken place will be responsible for the same. There is the need

to establish the process by which control will be made otherwise the control risk will also exist.

The third risk is in relation to the identification of them and this will be the responsibility of the

auditor (Huang et al., 2017). They will be required to detect all the risks and misstatements

which are taking place. If they fail to do so then the same will be resulting in the detection risk.

There will be need have the appropriate audit plan for the same in which all of the actions which

will be taken are specified and that will be making the elimination of the risk which is most

important. There will be evaluation process which will be involved in which all of the tasks will

be checked and if any issue is there then the reporting of the same will be made in the audit

report. They all are related to one another and with the strong internal control the inherent risk

will be reduced and also the detection will be made appropriately which will be reducing the

detection risk.

In case of the legend corporation, there are various risks which are involved. This is

because of the vast expansion of the company. There are several activities which are undertaken

and that involves the possibility of the errors being made. Due to this it can be said that there is

the involvement of the risk in the company. There are high fluctuations which are made in the

currencies and due to that the risk is faced (Jans et al., 2013). The risk management policy is

maintained and carried in effective manner by which the proper steps are taken in his respect.

The risks are identified and reported in adequate manner which shows that detection risk is low

in the company.

The analytical procedure

The financial aspects of the business are covered with the help of the financial statements

in which all of the information is collected in an adequate manner. The position of the company

be based on them. There will be audit risk model which will be followed in which all of the

elements will be taken into account. The model will be as follows:

Audit risk model = control risk X inherent risk X detection risk

The two main risks which are involved have been identified and they are the inherent and

control risk. The inherent risk which is involved is due to the error or can be said that all of the

material misstatements which are taken place will be responsible for the same. There is the need

to establish the process by which control will be made otherwise the control risk will also exist.

The third risk is in relation to the identification of them and this will be the responsibility of the

auditor (Huang et al., 2017). They will be required to detect all the risks and misstatements

which are taking place. If they fail to do so then the same will be resulting in the detection risk.

There will be need have the appropriate audit plan for the same in which all of the actions which

will be taken are specified and that will be making the elimination of the risk which is most

important. There will be evaluation process which will be involved in which all of the tasks will

be checked and if any issue is there then the reporting of the same will be made in the audit

report. They all are related to one another and with the strong internal control the inherent risk

will be reduced and also the detection will be made appropriately which will be reducing the

detection risk.

In case of the legend corporation, there are various risks which are involved. This is

because of the vast expansion of the company. There are several activities which are undertaken

and that involves the possibility of the errors being made. Due to this it can be said that there is

the involvement of the risk in the company. There are high fluctuations which are made in the

currencies and due to that the risk is faced (Jans et al., 2013). The risk management policy is

maintained and carried in effective manner by which the proper steps are taken in his respect.

The risks are identified and reported in adequate manner which shows that detection risk is low

in the company.

The analytical procedure

The financial aspects of the business are covered with the help of the financial statements

in which all of the information is collected in an adequate manner. The position of the company

9

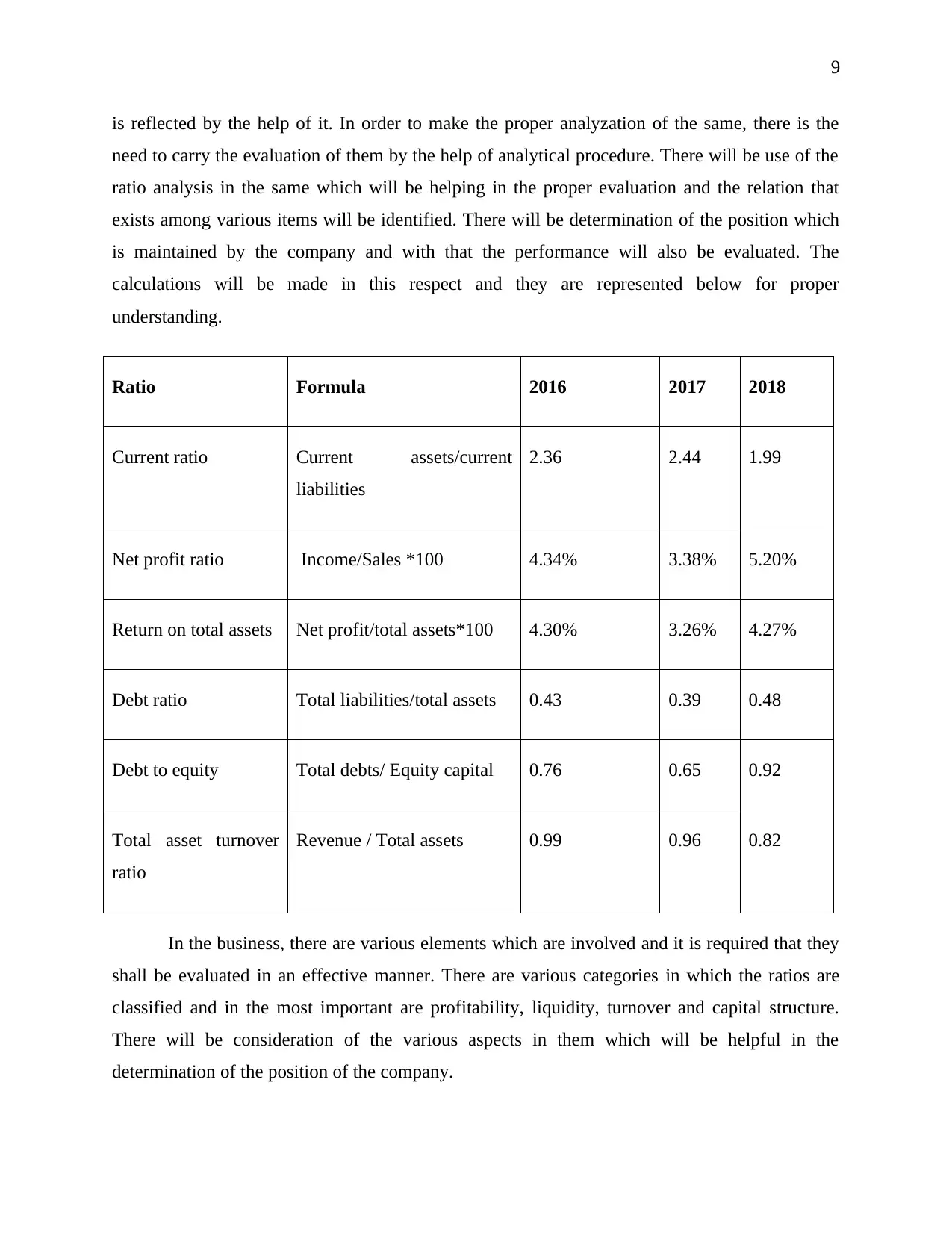

is reflected by the help of it. In order to make the proper analyzation of the same, there is the

need to carry the evaluation of them by the help of analytical procedure. There will be use of the

ratio analysis in the same which will be helping in the proper evaluation and the relation that

exists among various items will be identified. There will be determination of the position which

is maintained by the company and with that the performance will also be evaluated. The

calculations will be made in this respect and they are represented below for proper

understanding.

Ratio Formula 2016 2017 2018

Current ratio Current assets/current

liabilities

2.36 2.44 1.99

Net profit ratio Income/Sales *100 4.34% 3.38% 5.20%

Return on total assets Net profit/total assets*100 4.30% 3.26% 4.27%

Debt ratio Total liabilities/total assets 0.43 0.39 0.48

Debt to equity Total debts/ Equity capital 0.76 0.65 0.92

Total asset turnover

ratio

Revenue / Total assets 0.99 0.96 0.82

In the business, there are various elements which are involved and it is required that they

shall be evaluated in an effective manner. There are various categories in which the ratios are

classified and in the most important are profitability, liquidity, turnover and capital structure.

There will be consideration of the various aspects in them which will be helpful in the

determination of the position of the company.

is reflected by the help of it. In order to make the proper analyzation of the same, there is the

need to carry the evaluation of them by the help of analytical procedure. There will be use of the

ratio analysis in the same which will be helping in the proper evaluation and the relation that

exists among various items will be identified. There will be determination of the position which

is maintained by the company and with that the performance will also be evaluated. The

calculations will be made in this respect and they are represented below for proper

understanding.

Ratio Formula 2016 2017 2018

Current ratio Current assets/current

liabilities

2.36 2.44 1.99

Net profit ratio Income/Sales *100 4.34% 3.38% 5.20%

Return on total assets Net profit/total assets*100 4.30% 3.26% 4.27%

Debt ratio Total liabilities/total assets 0.43 0.39 0.48

Debt to equity Total debts/ Equity capital 0.76 0.65 0.92

Total asset turnover

ratio

Revenue / Total assets 0.99 0.96 0.82

In the business, there are various elements which are involved and it is required that they

shall be evaluated in an effective manner. There are various categories in which the ratios are

classified and in the most important are profitability, liquidity, turnover and capital structure.

There will be consideration of the various aspects in them which will be helpful in the

determination of the position of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

The liquidity of the company has been analyzed and in that there is the consideration of

the current ratio. The ratio is calculated by the help of current assets and current liabilities. There

will be comparison which will be made and it will ensure the ability of the company to repay its

debts. In this, it is analyzed that company will be able to pay off the liabilities on time or not. For

this the calculation is made and it is identified that the same is increasing from 2.36 to 2.44 in

2017 and after that there is some decline which is faced and it declined to 1.99 (Legend

Corporation Limited, 2017). After this also the company is in good position and there is adequate

liquidity which is maintained. It can be said that company is efficient in maintaining the liquidity

and will be paying all of the liabilities on time.

The profitability position of the company has been analyzed and it is identified that there

are improvements which are made in the same. The ratio has increased and this is because of the

rise in the income which made in spite of the decline which is made in the sales. The net profit

margin is maintained and there is a good amount of the return which has been earned by the

company on the total assets which are involved. The position of the debt in the company is

maintained at adequate level. There is a debt ratio of 0.43 in 2016 and it has increased to 0.48 in

2018. This is the level at which company will be able to meet with the expenses which are

incurred in relation to the debts. There will be proper position which will be maintained and no

issue will be faced in dealing with the liabilities. The turnover of the company is required to be

maintained with the help of the available resources (Legend Corporation Limited, 2018). There

are total assets which are involved in the company and there is more investment which has been

made in the company and the assets are increasing with time. The ratio which has been identified

is decreasing and it shows that company is not maintained the proper ratio between the available

resources and sales which is made. This shows that proper utilization of the assets is not made in

the company and it is required to improve the process by which the growth can be gained in the

coming time.

Materiality

The materiality is an important concept which is specified in the auditing standard ASA

320. According to this, there are several such accounts which are material and will be in the

position to affect the other accounts and results that are obtained in the company. There are

The liquidity of the company has been analyzed and in that there is the consideration of

the current ratio. The ratio is calculated by the help of current assets and current liabilities. There

will be comparison which will be made and it will ensure the ability of the company to repay its

debts. In this, it is analyzed that company will be able to pay off the liabilities on time or not. For

this the calculation is made and it is identified that the same is increasing from 2.36 to 2.44 in

2017 and after that there is some decline which is faced and it declined to 1.99 (Legend

Corporation Limited, 2017). After this also the company is in good position and there is adequate

liquidity which is maintained. It can be said that company is efficient in maintaining the liquidity

and will be paying all of the liabilities on time.

The profitability position of the company has been analyzed and it is identified that there

are improvements which are made in the same. The ratio has increased and this is because of the

rise in the income which made in spite of the decline which is made in the sales. The net profit

margin is maintained and there is a good amount of the return which has been earned by the

company on the total assets which are involved. The position of the debt in the company is

maintained at adequate level. There is a debt ratio of 0.43 in 2016 and it has increased to 0.48 in

2018. This is the level at which company will be able to meet with the expenses which are

incurred in relation to the debts. There will be proper position which will be maintained and no

issue will be faced in dealing with the liabilities. The turnover of the company is required to be

maintained with the help of the available resources (Legend Corporation Limited, 2018). There

are total assets which are involved in the company and there is more investment which has been

made in the company and the assets are increasing with time. The ratio which has been identified

is decreasing and it shows that company is not maintained the proper ratio between the available

resources and sales which is made. This shows that proper utilization of the assets is not made in

the company and it is required to improve the process by which the growth can be gained in the

coming time.

Materiality

The materiality is an important concept which is specified in the auditing standard ASA

320. According to this, there are several such accounts which are material and will be in the

position to affect the other accounts and results that are obtained in the company. There are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

chances of modification in them and by that the position of the business will be affected. There

will be continuous monitoring which will be made and with the help of that the errors which

have been involved will be identified and improvement will be made (Eilifsen & Messier Jr,

2014). There will be elimination of the errors and that will be improving the position of the

business. There are certain aspects which will be used in the determination of the materiality

such as the size of the account and its value. All of the factors which determine the materiality

will have to be taken into account in an appropriate manner. The material accounts are of big size

and by the change in them complete position of the business will be affected. Some times

modifications are made so that the overall reflection of the business can be improved and this

will be against the rules and regulations (Keune & Johnstone, 2012). The company will be

following the process and determining all of the material accounts so that further process in

relation to them can be made possible.

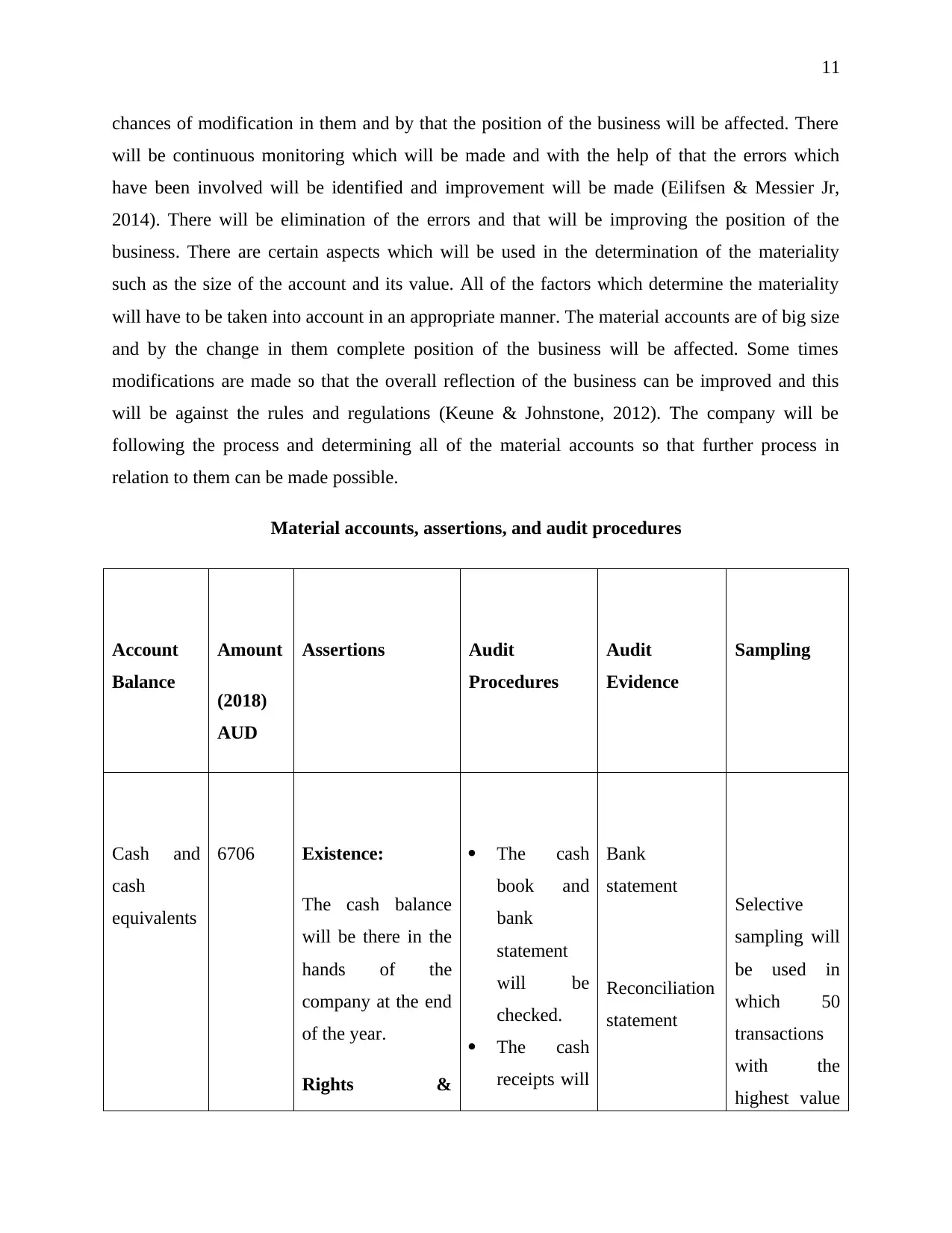

Material accounts, assertions, and audit procedures

Account

Balance

Amount

(2018)

AUD

Assertions Audit

Procedures

Audit

Evidence

Sampling

Cash and

cash

equivalents

6706 Existence:

The cash balance

will be there in the

hands of the

company at the end

of the year.

Rights &

The cash

book and

bank

statement

will be

checked.

The cash

receipts will

Bank

statement

Reconciliation

statement

Selective

sampling will

be used in

which 50

transactions

with the

highest value

chances of modification in them and by that the position of the business will be affected. There

will be continuous monitoring which will be made and with the help of that the errors which

have been involved will be identified and improvement will be made (Eilifsen & Messier Jr,

2014). There will be elimination of the errors and that will be improving the position of the

business. There are certain aspects which will be used in the determination of the materiality

such as the size of the account and its value. All of the factors which determine the materiality

will have to be taken into account in an appropriate manner. The material accounts are of big size

and by the change in them complete position of the business will be affected. Some times

modifications are made so that the overall reflection of the business can be improved and this

will be against the rules and regulations (Keune & Johnstone, 2012). The company will be

following the process and determining all of the material accounts so that further process in

relation to them can be made possible.

Material accounts, assertions, and audit procedures

Account

Balance

Amount

(2018)

AUD

Assertions Audit

Procedures

Audit

Evidence

Sampling

Cash and

cash

equivalents

6706 Existence:

The cash balance

will be there in the

hands of the

company at the end

of the year.

Rights &

The cash

book and

bank

statement

will be

checked.

The cash

receipts will

Bank

statement

Reconciliation

statement

Selective

sampling will

be used in

which 50

transactions

with the

highest value

12

Obligations

The company will

be having the rights

on the asset which

will make the

applicability of this

assertion.

be checked

with the

cash book

and by that

confirmatio

n will be

made.

will be used.

Inventories 32522 Completeness:

The total of all the

values in relation to

the inventory is

taken into

consideration

Valuation

The valuation

standard which is

available will be

used to calculate

the correct value.

The

inventory

records are

checked

with the

sheet that is

prepared for

the same.

The

physical

verification

will be

made for

the

confirmatio

n.

The cost

will be

calculated

by using the

Inventory

sheet

Stock register

Cycle

counting

method will

be used in

which 20

samples will

be selected.

Obligations

The company will

be having the rights

on the asset which

will make the

applicability of this

assertion.

be checked

with the

cash book

and by that

confirmatio

n will be

made.

will be used.

Inventories 32522 Completeness:

The total of all the

values in relation to

the inventory is

taken into

consideration

Valuation

The valuation

standard which is

available will be

used to calculate

the correct value.

The

inventory

records are

checked

with the

sheet that is

prepared for

the same.

The

physical

verification

will be

made for

the

confirmatio

n.

The cost

will be

calculated

by using the

Inventory

sheet

Stock register

Cycle

counting

method will

be used in

which 20

samples will

be selected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.