Lending Club Case Study: Securitization of Promissory Notes Analysis

VerifiedAdded on 2022/10/13

|9

|788

|497

Case Study

AI Summary

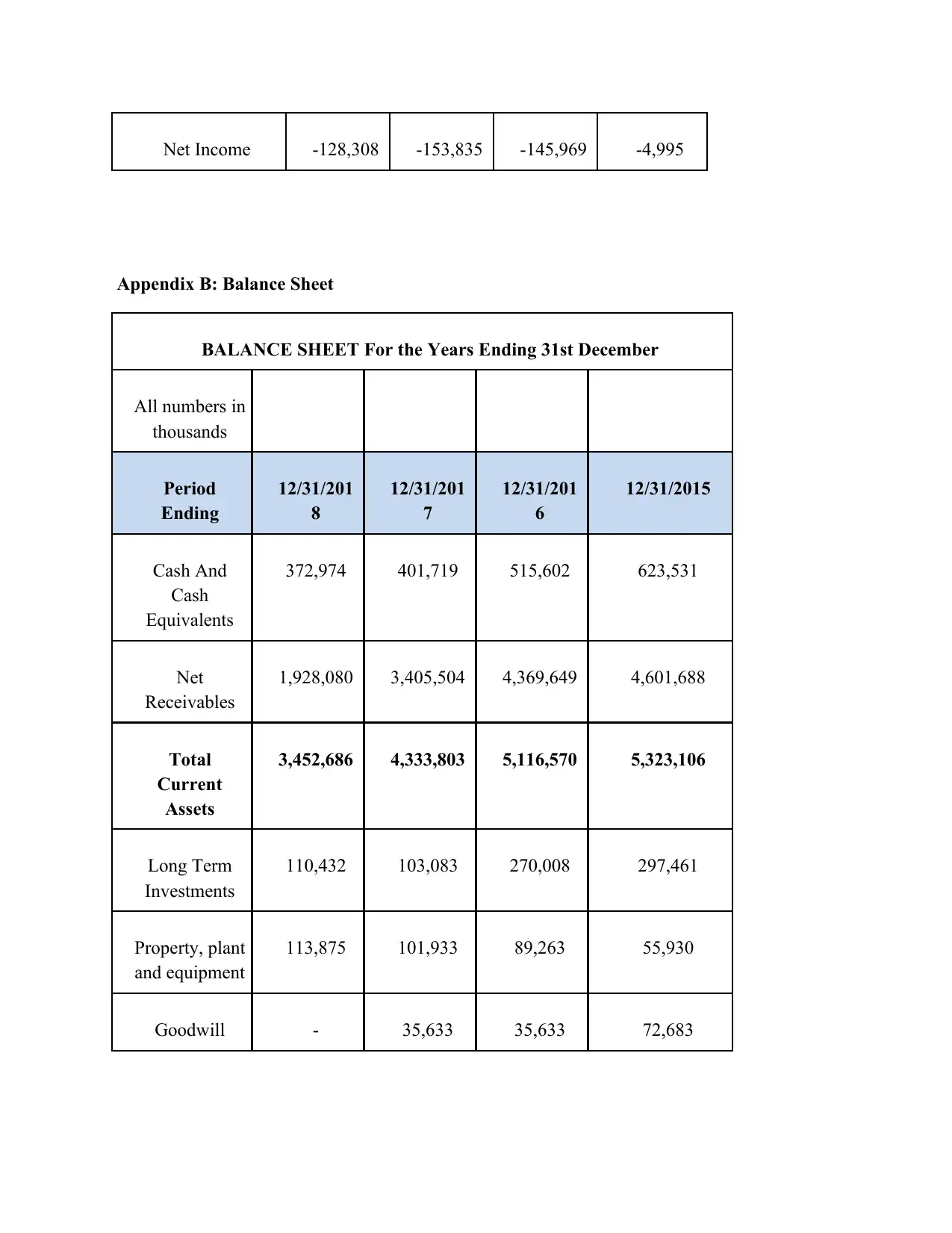

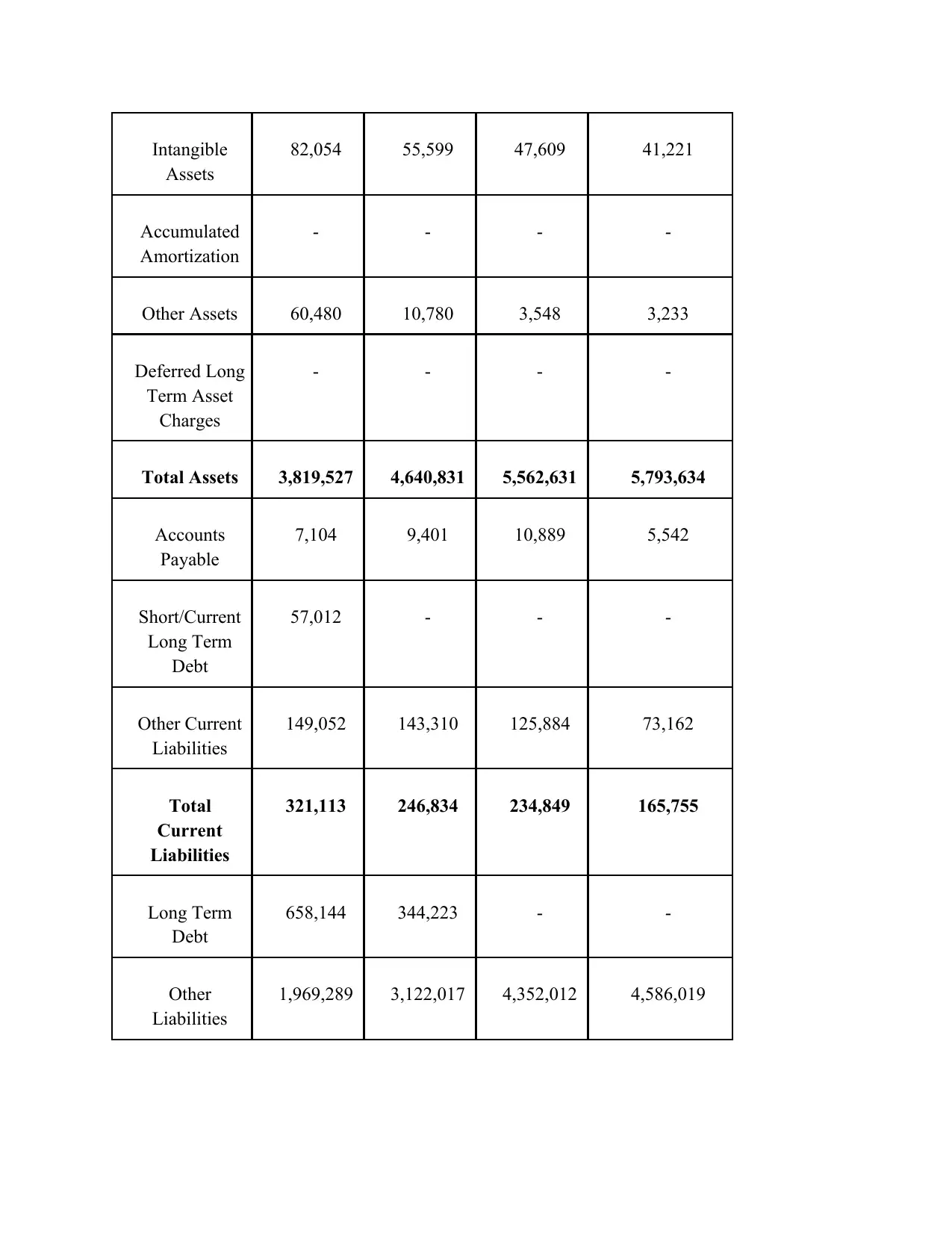

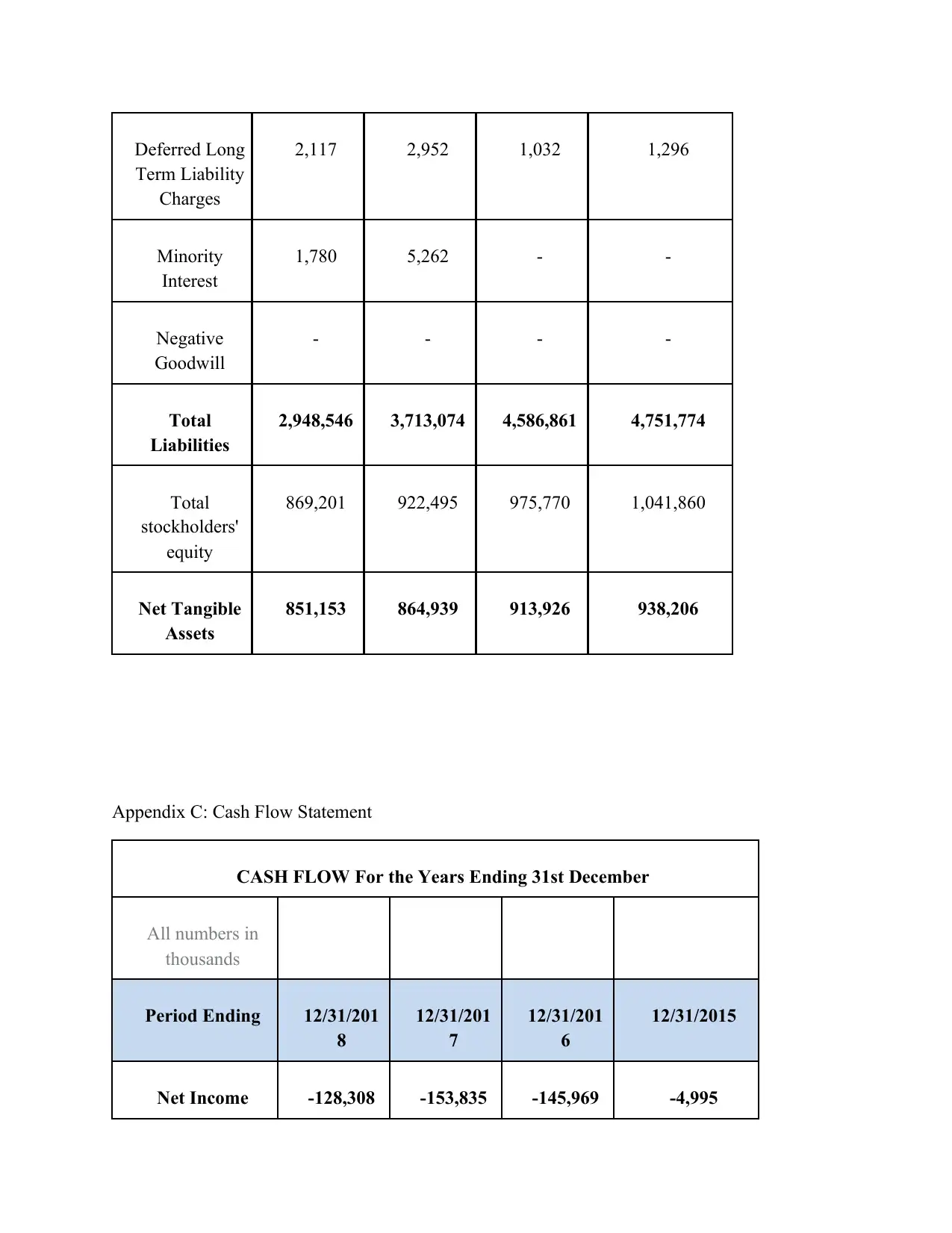

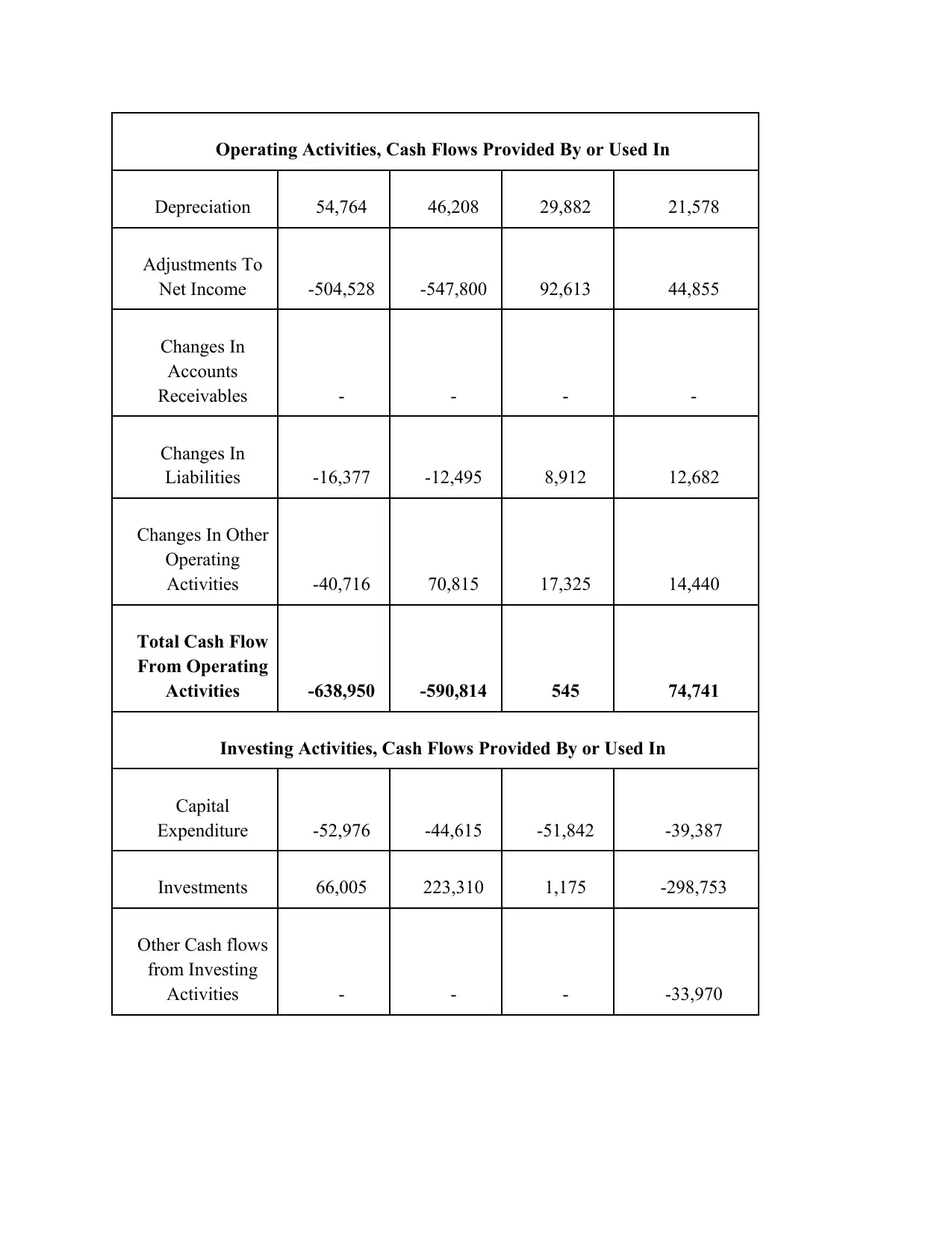

This case study analyzes Lending Club's strategic decision to securitize its promissory notes to enhance liquidity and expand investor access. The case explores the company's business model, the peer-to-peer lending system, and the challenges posed by the lack of a secondary market for its loans. It examines the financial performance of Lending Club, including revenue growth and share price fluctuations, and the potential impact of SEC regulations on its operations. The study highlights the complexities of securitization, the need for regulatory compliance, and the importance of considering the size of investment offerings. The analysis provides recommendations for Lending Club regarding its registration with the SEC and the structuring of its investment offerings. The case study uses financial data from 2015 to 2018 and relevant references to support its findings, offering insights into the financial and regulatory aspects of securitizing personal loans.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.