Financial Management Report: Right Issue and Capital Budgeting

VerifiedAdded on 2023/01/13

|16

|3853

|92

Report

AI Summary

This financial management report delves into two key areas: right issues and capital budgeting. The report begins with an analysis of a right issue by Lexbel, examining the number of shares to be issued, the theoretical ex-rights price, the impact on earnings per share, the number of rights against the shares, and the best option for the company. The report also explores the concept of scrip dividends. The second part of the report focuses on capital budgeting techniques, specifically evaluating the feasibility of a project using methods such as payback period, accounting rate of return, net present value, and internal rate of return. The report also discusses the advantages and disadvantages of these capital budgeting tools, providing a comprehensive overview of financial decision-making processes.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 2...................................................................................................................................1

a) Number of share units to issue.................................................................................................2

b) Theoretical Ex rights price......................................................................................................3

c) Expected Earning per share ....................................................................................................3

d) Number of rights against the shares........................................................................................4

e) Best option ..............................................................................................................................5

QUESTION 3...................................................................................................................................6

a) Identifying feasibility of the project using techniques used in capital budgeting...................6

Payback period ............................................................................................................................7

Accounting rate of return ............................................................................................................8

Net Present Value .......................................................................................................................9

Internal Rate of Return ..............................................................................................................10

b) Advantages and dis-advantages of different tools use in capital budgeting..........................11

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

QUESTION 2...................................................................................................................................1

a) Number of share units to issue.................................................................................................2

b) Theoretical Ex rights price......................................................................................................3

c) Expected Earning per share ....................................................................................................3

d) Number of rights against the shares........................................................................................4

e) Best option ..............................................................................................................................5

QUESTION 3...................................................................................................................................6

a) Identifying feasibility of the project using techniques used in capital budgeting...................6

Payback period ............................................................................................................................7

Accounting rate of return ............................................................................................................8

Net Present Value .......................................................................................................................9

Internal Rate of Return ..............................................................................................................10

b) Advantages and dis-advantages of different tools use in capital budgeting..........................11

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management refers to plan, organize, direct and control financial activities

going on in a company like procurement & utilization of the funds of enterprise. This means

application of the general management principles over the financial resources of enterprise.

Money is needed for making money. Life blood of every business is finance and there should be

continuous inflow and outflow of money from business. Soundness of plans, efficiency in

production systems & excellent networks for marketing are hampered in absence of adequate &

timely funds supply. Financial management is having the same importance in business as

marketing and production. Present report will cover the concepts of raising finance. This will

provide an understanding about the raising of funds through right issue and the viability of

project in which company is planning to invest using the capital budgeting techniques. In the

present report question number 2 and 3 have been answered where 2 is related to right issue and

3 is concerned with capital budgeting techniques.

QUESTION 2

Right Issue

Right issue is concerned with raising additional capital by issuing new additional shares

to its existing shareholders. Existing shareholders have the right of subscribing the shares unless

certain special rights have reserved them for other individuals. Right offer or right issue is form

of dividend giving subscription rights for buying the additional securities in company given to

the existing shareholders. Where the right are related to equity securities like share in public

company, they are non-dilutive pro rata way of raising capital. Shares in right issue are sold

through prospectus. Existing shareholders in the issued rights have privilege of buying specified

number of the new securities at price specified within the period of subscription (Mazumdar,

2019). In public company right issue is type of public offering. In some cases privilege of right

issue is also given to individual such as employees directors, and other employees having

ownership in company.

Right issue can prove to be useful for most of the publicly traded entities as opposed to

the options of dilutive financing. Companies generally prefer equity issues over the debt issues

as from the viewpoint of company. Firms mostly go for right issue for minimizing the dilution &

maximizing useful life of the tax losses carry forwards. In right offerings control is not changed

1

Financial management refers to plan, organize, direct and control financial activities

going on in a company like procurement & utilization of the funds of enterprise. This means

application of the general management principles over the financial resources of enterprise.

Money is needed for making money. Life blood of every business is finance and there should be

continuous inflow and outflow of money from business. Soundness of plans, efficiency in

production systems & excellent networks for marketing are hampered in absence of adequate &

timely funds supply. Financial management is having the same importance in business as

marketing and production. Present report will cover the concepts of raising finance. This will

provide an understanding about the raising of funds through right issue and the viability of

project in which company is planning to invest using the capital budgeting techniques. In the

present report question number 2 and 3 have been answered where 2 is related to right issue and

3 is concerned with capital budgeting techniques.

QUESTION 2

Right Issue

Right issue is concerned with raising additional capital by issuing new additional shares

to its existing shareholders. Existing shareholders have the right of subscribing the shares unless

certain special rights have reserved them for other individuals. Right offer or right issue is form

of dividend giving subscription rights for buying the additional securities in company given to

the existing shareholders. Where the right are related to equity securities like share in public

company, they are non-dilutive pro rata way of raising capital. Shares in right issue are sold

through prospectus. Existing shareholders in the issued rights have privilege of buying specified

number of the new securities at price specified within the period of subscription (Mazumdar,

2019). In public company right issue is type of public offering. In some cases privilege of right

issue is also given to individual such as employees directors, and other employees having

ownership in company.

Right issue can prove to be useful for most of the publicly traded entities as opposed to

the options of dilutive financing. Companies generally prefer equity issues over the debt issues

as from the viewpoint of company. Firms mostly go for right issue for minimizing the dilution &

maximizing useful life of the tax losses carry forwards. In right offerings control is not changed

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and no-sale theory is applicable, corporations can preserve the carry forwards tax loss better than

any other offerings or dilutive financings (Kampanje, 2018).

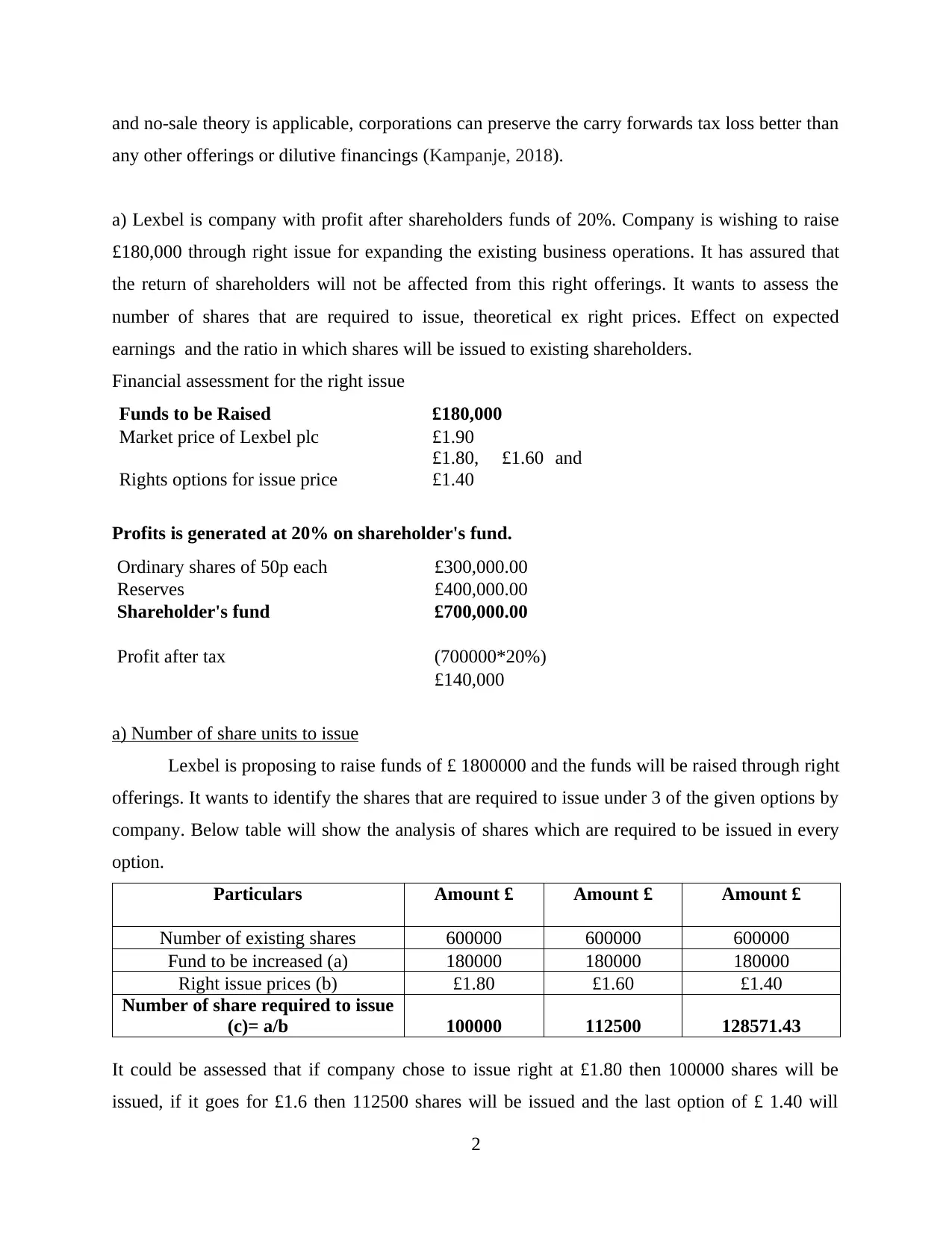

a) Lexbel is company with profit after shareholders funds of 20%. Company is wishing to raise

£180,000 through right issue for expanding the existing business operations. It has assured that

the return of shareholders will not be affected from this right offerings. It wants to assess the

number of shares that are required to issue, theoretical ex right prices. Effect on expected

earnings and the ratio in which shares will be issued to existing shareholders.

Financial assessment for the right issue

Funds to be Raised £180,000

Market price of Lexbel plc £1.90

Rights options for issue price

£1.80, £1.60 and

£1.40

Profits is generated at 20% on shareholder's fund.

Ordinary shares of 50p each £300,000.00

Reserves £400,000.00

Shareholder's fund £700,000.00

Profit after tax (700000*20%)

£140,000

a) Number of share units to issue

Lexbel is proposing to raise funds of £ 1800000 and the funds will be raised through right

offerings. It wants to identify the shares that are required to issue under 3 of the given options by

company. Below table will show the analysis of shares which are required to be issued in every

option.

Particulars Amount £ Amount £ Amount £

Number of existing shares 600000 600000 600000

Fund to be increased (a) 180000 180000 180000

Right issue prices (b) £1.80 £1.60 £1.40

Number of share required to issue

(c)= a/b 100000 112500 128571.43

It could be assessed that if company chose to issue right at £1.80 then 100000 shares will be

issued, if it goes for £1.6 then 112500 shares will be issued and the last option of £ 1.40 will

2

any other offerings or dilutive financings (Kampanje, 2018).

a) Lexbel is company with profit after shareholders funds of 20%. Company is wishing to raise

£180,000 through right issue for expanding the existing business operations. It has assured that

the return of shareholders will not be affected from this right offerings. It wants to assess the

number of shares that are required to issue, theoretical ex right prices. Effect on expected

earnings and the ratio in which shares will be issued to existing shareholders.

Financial assessment for the right issue

Funds to be Raised £180,000

Market price of Lexbel plc £1.90

Rights options for issue price

£1.80, £1.60 and

£1.40

Profits is generated at 20% on shareholder's fund.

Ordinary shares of 50p each £300,000.00

Reserves £400,000.00

Shareholder's fund £700,000.00

Profit after tax (700000*20%)

£140,000

a) Number of share units to issue

Lexbel is proposing to raise funds of £ 1800000 and the funds will be raised through right

offerings. It wants to identify the shares that are required to issue under 3 of the given options by

company. Below table will show the analysis of shares which are required to be issued in every

option.

Particulars Amount £ Amount £ Amount £

Number of existing shares 600000 600000 600000

Fund to be increased (a) 180000 180000 180000

Right issue prices (b) £1.80 £1.60 £1.40

Number of share required to issue

(c)= a/b 100000 112500 128571.43

It could be assessed that if company chose to issue right at £1.80 then 100000 shares will be

issued, if it goes for £1.6 then 112500 shares will be issued and the last option of £ 1.40 will

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

require 128572 shares for raising the required funds. As the prices of right issue decreases the

number of shares for raising the capital will be increasing.

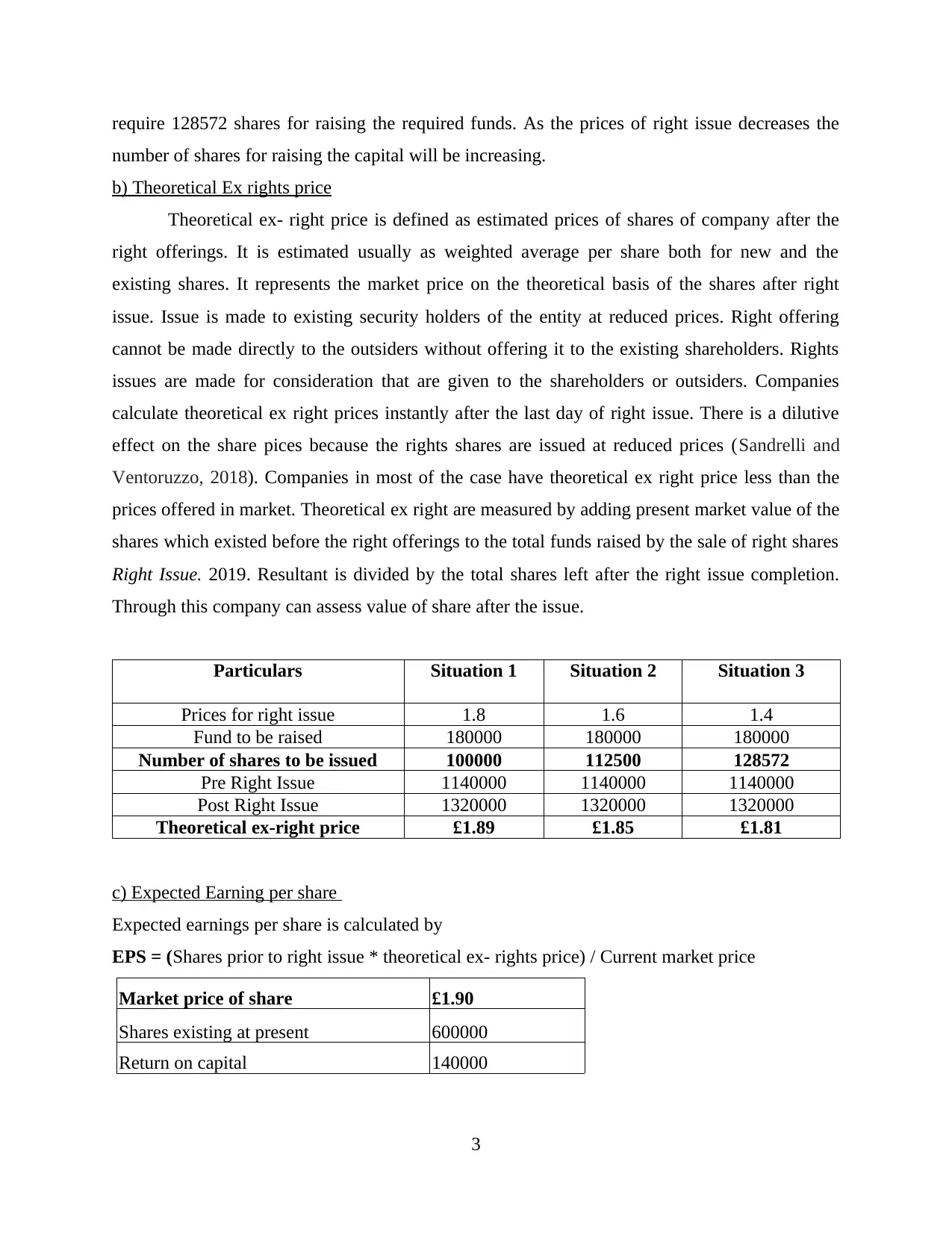

b) Theoretical Ex rights price

Theoretical ex- right price is defined as estimated prices of shares of company after the

right offerings. It is estimated usually as weighted average per share both for new and the

existing shares. It represents the market price on the theoretical basis of the shares after right

issue. Issue is made to existing security holders of the entity at reduced prices. Right offering

cannot be made directly to the outsiders without offering it to the existing shareholders. Rights

issues are made for consideration that are given to the shareholders or outsiders. Companies

calculate theoretical ex right prices instantly after the last day of right issue. There is a dilutive

effect on the share pices because the rights shares are issued at reduced prices (Sandrelli and

Ventoruzzo, 2018). Companies in most of the case have theoretical ex right price less than the

prices offered in market. Theoretical ex right are measured by adding present market value of the

shares which existed before the right offerings to the total funds raised by the sale of right shares

Right Issue. 2019. Resultant is divided by the total shares left after the right issue completion.

Through this company can assess value of share after the issue.

Particulars Situation 1 Situation 2 Situation 3

Prices for right issue 1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares to be issued 100000 112500 128572

Pre Right Issue 1140000 1140000 1140000

Post Right Issue 1320000 1320000 1320000

Theoretical ex-right price £1.89 £1.85 £1.81

c) Expected Earning per share

Expected earnings per share is calculated by

EPS = (Shares prior to right issue * theoretical ex- rights price) / Current market price

Market price of share £1.90

Shares existing at present 600000

Return on capital 140000

3

number of shares for raising the capital will be increasing.

b) Theoretical Ex rights price

Theoretical ex- right price is defined as estimated prices of shares of company after the

right offerings. It is estimated usually as weighted average per share both for new and the

existing shares. It represents the market price on the theoretical basis of the shares after right

issue. Issue is made to existing security holders of the entity at reduced prices. Right offering

cannot be made directly to the outsiders without offering it to the existing shareholders. Rights

issues are made for consideration that are given to the shareholders or outsiders. Companies

calculate theoretical ex right prices instantly after the last day of right issue. There is a dilutive

effect on the share pices because the rights shares are issued at reduced prices (Sandrelli and

Ventoruzzo, 2018). Companies in most of the case have theoretical ex right price less than the

prices offered in market. Theoretical ex right are measured by adding present market value of the

shares which existed before the right offerings to the total funds raised by the sale of right shares

Right Issue. 2019. Resultant is divided by the total shares left after the right issue completion.

Through this company can assess value of share after the issue.

Particulars Situation 1 Situation 2 Situation 3

Prices for right issue 1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares to be issued 100000 112500 128572

Pre Right Issue 1140000 1140000 1140000

Post Right Issue 1320000 1320000 1320000

Theoretical ex-right price £1.89 £1.85 £1.81

c) Expected Earning per share

Expected earnings per share is calculated by

EPS = (Shares prior to right issue * theoretical ex- rights price) / Current market price

Market price of share £1.90

Shares existing at present 600000

Return on capital 140000

3

Particulars Amount £ Amount £ Amount £

Prices for right issue £1.80 £1.60 £1.40

Fund to be raised £180,000.00 £180,000.00 £180,000.00

Number of shares to be issued 100000 112500 128572

Pre Right Issue 1140000 1140000 1140000

Post Right Issue 1320000 1320000 1320000

Theoretical ex-right price £1.89 £1.85 £1.81

Value of one right 0.01 0.05 0.09

Fair value per share 95454.55 97159.09 99350.65

Bonus fractions 50619.83 52443.83 54836.4

Earning per share or Eps 595488.72 585041.55 572136.22

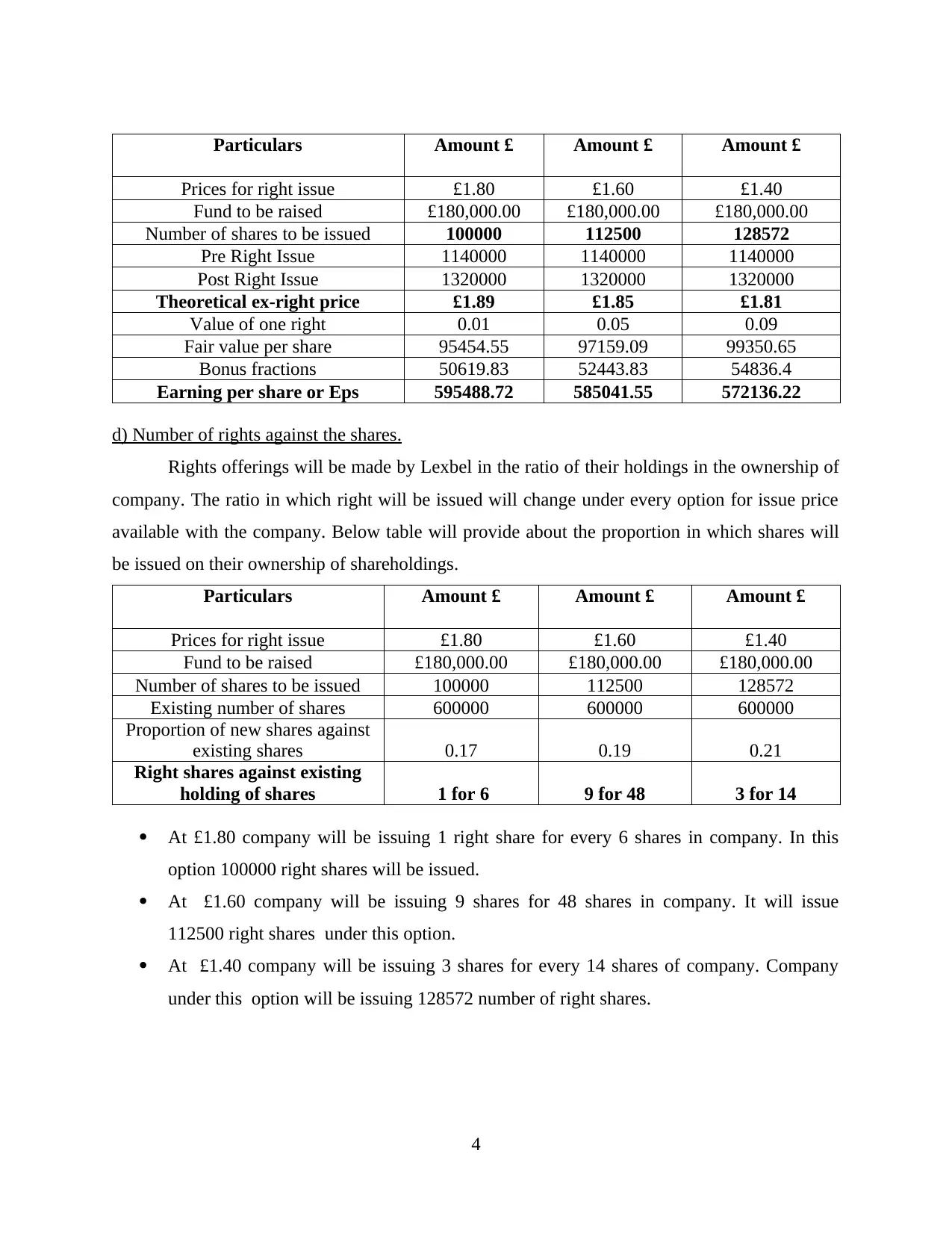

d) Number of rights against the shares.

Rights offerings will be made by Lexbel in the ratio of their holdings in the ownership of

company. The ratio in which right will be issued will change under every option for issue price

available with the company. Below table will provide about the proportion in which shares will

be issued on their ownership of shareholdings.

Particulars Amount £ Amount £ Amount £

Prices for right issue £1.80 £1.60 £1.40

Fund to be raised £180,000.00 £180,000.00 £180,000.00

Number of shares to be issued 100000 112500 128572

Existing number of shares 600000 600000 600000

Proportion of new shares against

existing shares 0.17 0.19 0.21

Right shares against existing

holding of shares 1 for 6 9 for 48 3 for 14

At £1.80 company will be issuing 1 right share for every 6 shares in company. In this

option 100000 right shares will be issued.

At £1.60 company will be issuing 9 shares for 48 shares in company. It will issue

112500 right shares under this option.

At £1.40 company will be issuing 3 shares for every 14 shares of company. Company

under this option will be issuing 128572 number of right shares.

4

Prices for right issue £1.80 £1.60 £1.40

Fund to be raised £180,000.00 £180,000.00 £180,000.00

Number of shares to be issued 100000 112500 128572

Pre Right Issue 1140000 1140000 1140000

Post Right Issue 1320000 1320000 1320000

Theoretical ex-right price £1.89 £1.85 £1.81

Value of one right 0.01 0.05 0.09

Fair value per share 95454.55 97159.09 99350.65

Bonus fractions 50619.83 52443.83 54836.4

Earning per share or Eps 595488.72 585041.55 572136.22

d) Number of rights against the shares.

Rights offerings will be made by Lexbel in the ratio of their holdings in the ownership of

company. The ratio in which right will be issued will change under every option for issue price

available with the company. Below table will provide about the proportion in which shares will

be issued on their ownership of shareholdings.

Particulars Amount £ Amount £ Amount £

Prices for right issue £1.80 £1.60 £1.40

Fund to be raised £180,000.00 £180,000.00 £180,000.00

Number of shares to be issued 100000 112500 128572

Existing number of shares 600000 600000 600000

Proportion of new shares against

existing shares 0.17 0.19 0.21

Right shares against existing

holding of shares 1 for 6 9 for 48 3 for 14

At £1.80 company will be issuing 1 right share for every 6 shares in company. In this

option 100000 right shares will be issued.

At £1.60 company will be issuing 9 shares for 48 shares in company. It will issue

112500 right shares under this option.

At £1.40 company will be issuing 3 shares for every 14 shares of company. Company

under this option will be issuing 128572 number of right shares.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

e) Best option

The above analysis shows that the option that is most beneficial and suitable for the

company is of issuing shares at £1.80. This would be the best option from all the three options

available to the company. It will have maximum earnings in comparison with the other available

option to the company. Also the number of shares are also less that prevents the spread of profits

between increased number of shares (Brown, 2018). Also the share price tends to reduce with

the increase in number of shares. Therefore choosing this option will least affect the share price

after the right offering and the earnings per share. Other two options will not prove to be as

beneficial as the above option.

c) Shareholders adopting scrip dividends in place of cash dividends.

Every listed company is required to pay dividend over their shareholdings. Investors

invest their funds in company for generating adequate returns over their investments. Dividends

is form of return to the shareholders for their investments. It is distribution of profits earned by

company during the year. Dividends are paid at specified percentage by the corporations. Before

the dividends are decided approval of shareholders is required to be taken. Board of directors

decide the dividend to be declared to its shareholders. Company can pay dividends in many

forms like in cash, stocks, any other form. It is paid out of earnings or reserves and unless

specified it is not mandatory for company to declare dividend every year. In event of inadequate

funds or the expansion plan company can forgo payment of dividends.

Scrip Dividends

In scrip dividend shareholders are given the choice of receiving dividends either in cash

or common stocks or at future on specified time. Scrip dividends are generally issued by

company when it is not having sufficient funds for distribution. They are paid when company

wants to give it shareholder return for their investment. It is made for giving the shareholders a

chance for increasing their share of ownership without having to pay in addition (Hornuf and

Neuenkirch, 2017). In this shareholders are given options to receive common stocks of company.

Investors are showing interested in receiving scrip dividends rather than the cash dividends.

Cash Dividends

Cash dividend refers to the dividend received by investors in cash. Cash dividends are

paid at specified percentage as decided by the board of directors of company. This refers to

5

The above analysis shows that the option that is most beneficial and suitable for the

company is of issuing shares at £1.80. This would be the best option from all the three options

available to the company. It will have maximum earnings in comparison with the other available

option to the company. Also the number of shares are also less that prevents the spread of profits

between increased number of shares (Brown, 2018). Also the share price tends to reduce with

the increase in number of shares. Therefore choosing this option will least affect the share price

after the right offering and the earnings per share. Other two options will not prove to be as

beneficial as the above option.

c) Shareholders adopting scrip dividends in place of cash dividends.

Every listed company is required to pay dividend over their shareholdings. Investors

invest their funds in company for generating adequate returns over their investments. Dividends

is form of return to the shareholders for their investments. It is distribution of profits earned by

company during the year. Dividends are paid at specified percentage by the corporations. Before

the dividends are decided approval of shareholders is required to be taken. Board of directors

decide the dividend to be declared to its shareholders. Company can pay dividends in many

forms like in cash, stocks, any other form. It is paid out of earnings or reserves and unless

specified it is not mandatory for company to declare dividend every year. In event of inadequate

funds or the expansion plan company can forgo payment of dividends.

Scrip Dividends

In scrip dividend shareholders are given the choice of receiving dividends either in cash

or common stocks or at future on specified time. Scrip dividends are generally issued by

company when it is not having sufficient funds for distribution. They are paid when company

wants to give it shareholder return for their investment. It is made for giving the shareholders a

chance for increasing their share of ownership without having to pay in addition (Hornuf and

Neuenkirch, 2017). In this shareholders are given options to receive common stocks of company.

Investors are showing interested in receiving scrip dividends rather than the cash dividends.

Cash Dividends

Cash dividend refers to the dividend received by investors in cash. Cash dividends are

paid at specified percentage as decided by the board of directors of company. This refers to

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transfer of economic value from the company to the shareholders, instead of using the funds for

business operations. Cash dividends lower the share prices of companies.

Benefits of scrip dividend to company

Companies are saving their funds through issue of shares in place of cash dividends by

giving them choice to receive shares of company.

Liquidation risk can be minimised in this option of the firms. Companies increase their

market capitalisation over the stock exchange due to increase in number of shareholders.

In the event of insufficiency of monetary funds shareholders can be offered stocks in

place of cash.

Companies are not required to pay dividend tax over scrip dividends like in cash

dividend.

Benefits of scrip dividend to shareholders

Shareholders receiving shares in scrip dividends are not required to pay any brokerage

commission or tax in personal returns.

It provides the security holders with more yields of capital and financial gains compared

with the cash dividends (Kampanje, 2018).

Ownership in the company is increased of the shareholders without any additional

payment for shares.

Retaining powers and increase in value of assets is provided to the investors.

QUESTION 3

Techniques used in investment appraisals

a) Identifying feasibility of the project using techniques used in capital budgeting.

Company Lowell limited is proposing to buy new machine of £275,000 for food

manufacturing. For calculating whether the project is viable or not various investment appraisal

techniques will be used. Project involves signifiant investments of funds therefore to check the

viability of project is essential. The techniques used are payback period, ARR, net present value

and internal rate of return

Project under different techniques

6

business operations. Cash dividends lower the share prices of companies.

Benefits of scrip dividend to company

Companies are saving their funds through issue of shares in place of cash dividends by

giving them choice to receive shares of company.

Liquidation risk can be minimised in this option of the firms. Companies increase their

market capitalisation over the stock exchange due to increase in number of shareholders.

In the event of insufficiency of monetary funds shareholders can be offered stocks in

place of cash.

Companies are not required to pay dividend tax over scrip dividends like in cash

dividend.

Benefits of scrip dividend to shareholders

Shareholders receiving shares in scrip dividends are not required to pay any brokerage

commission or tax in personal returns.

It provides the security holders with more yields of capital and financial gains compared

with the cash dividends (Kampanje, 2018).

Ownership in the company is increased of the shareholders without any additional

payment for shares.

Retaining powers and increase in value of assets is provided to the investors.

QUESTION 3

Techniques used in investment appraisals

a) Identifying feasibility of the project using techniques used in capital budgeting.

Company Lowell limited is proposing to buy new machine of £275,000 for food

manufacturing. For calculating whether the project is viable or not various investment appraisal

techniques will be used. Project involves signifiant investments of funds therefore to check the

viability of project is essential. The techniques used are payback period, ARR, net present value

and internal rate of return

Project under different techniques

6

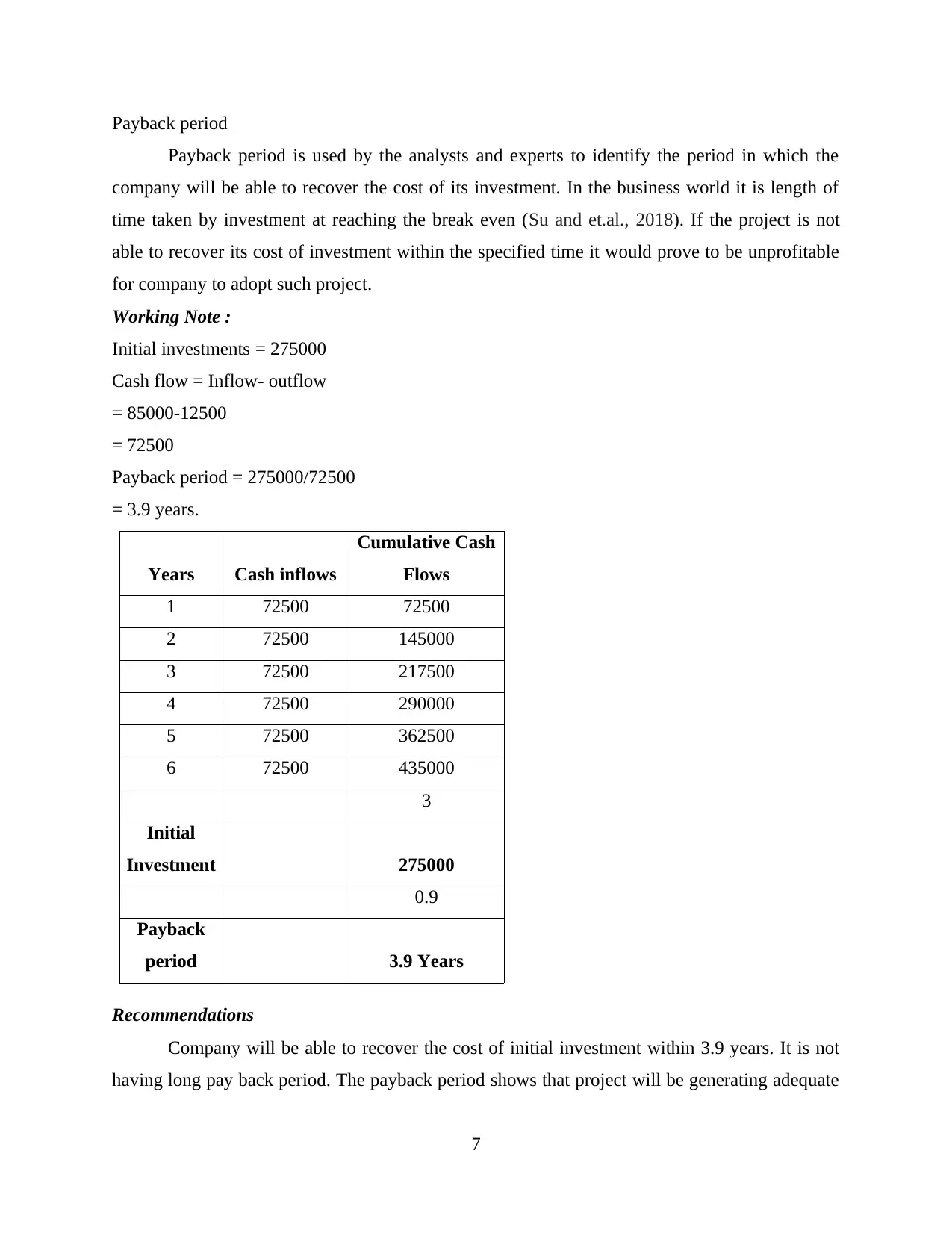

Payback period

Payback period is used by the analysts and experts to identify the period in which the

company will be able to recover the cost of its investment. In the business world it is length of

time taken by investment at reaching the break even (Su and et.al., 2018). If the project is not

able to recover its cost of investment within the specified time it would prove to be unprofitable

for company to adopt such project.

Working Note :

Initial investments = 275000

Cash flow = Inflow- outflow

= 85000-12500

= 72500

Payback period = 275000/72500

= 3.9 years.

Years Cash inflows

Cumulative Cash

Flows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

3

Initial

Investment 275000

0.9

Payback

period 3.9 Years

Recommendations

Company will be able to recover the cost of initial investment within 3.9 years. It is not

having long pay back period. The payback period shows that project will be generating adequate

7

Payback period is used by the analysts and experts to identify the period in which the

company will be able to recover the cost of its investment. In the business world it is length of

time taken by investment at reaching the break even (Su and et.al., 2018). If the project is not

able to recover its cost of investment within the specified time it would prove to be unprofitable

for company to adopt such project.

Working Note :

Initial investments = 275000

Cash flow = Inflow- outflow

= 85000-12500

= 72500

Payback period = 275000/72500

= 3.9 years.

Years Cash inflows

Cumulative Cash

Flows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

3

Initial

Investment 275000

0.9

Payback

period 3.9 Years

Recommendations

Company will be able to recover the cost of initial investment within 3.9 years. It is not

having long pay back period. The payback period shows that project will be generating adequate

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cash flows for the company through which the cost of investment will be recovered. The cash

flows are even through out the year and company should adopt the project as per the pay back

period.

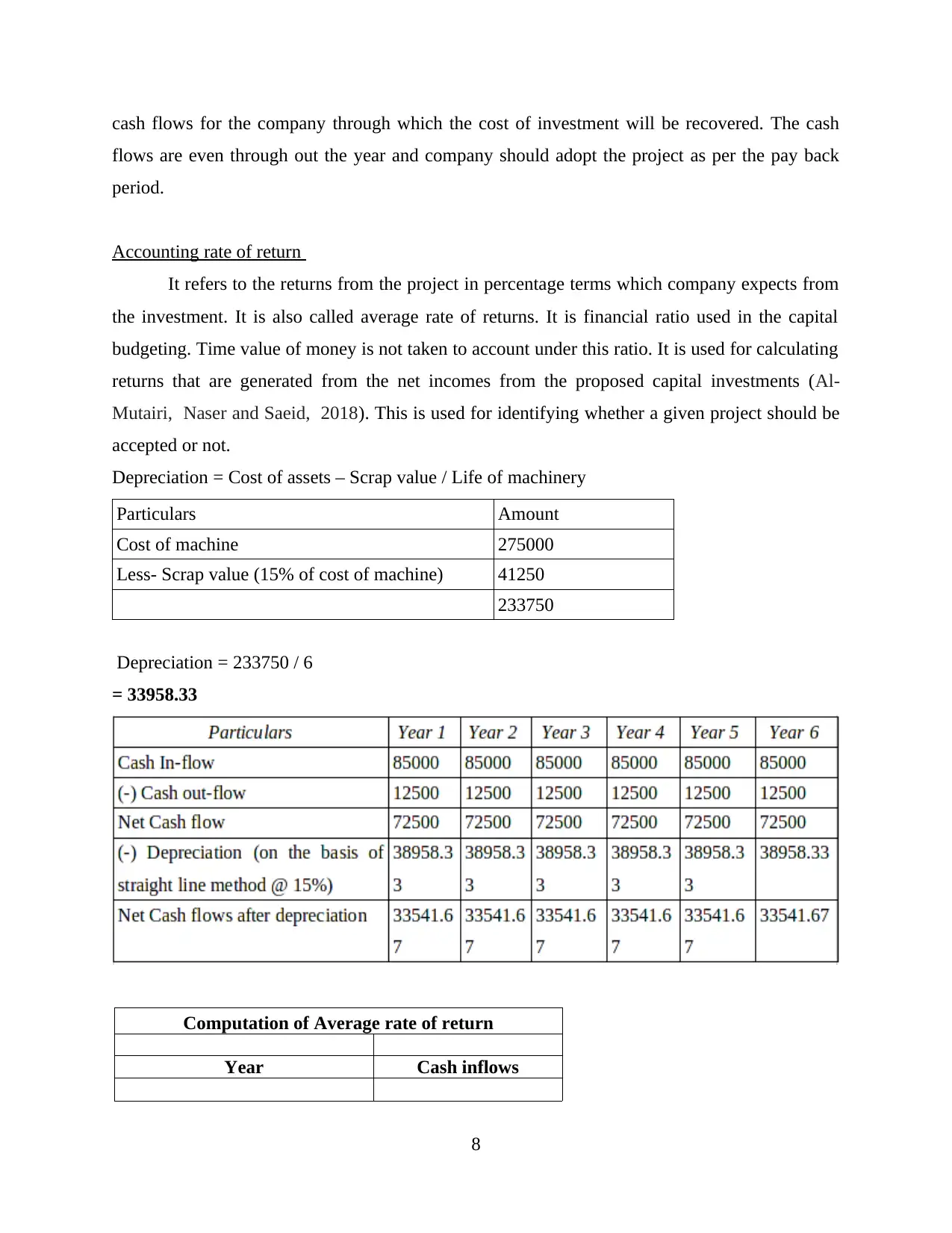

Accounting rate of return

It refers to the returns from the project in percentage terms which company expects from

the investment. It is also called average rate of returns. It is financial ratio used in the capital

budgeting. Time value of money is not taken to account under this ratio. It is used for calculating

returns that are generated from the net incomes from the proposed capital investments (Al-

Mutairi, Naser and Saeid, 2018). This is used for identifying whether a given project should be

accepted or not.

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

233750

Depreciation = 233750 / 6

= 33958.33

Computation of Average rate of return

Year Cash inflows

8

flows are even through out the year and company should adopt the project as per the pay back

period.

Accounting rate of return

It refers to the returns from the project in percentage terms which company expects from

the investment. It is also called average rate of returns. It is financial ratio used in the capital

budgeting. Time value of money is not taken to account under this ratio. It is used for calculating

returns that are generated from the net incomes from the proposed capital investments (Al-

Mutairi, Naser and Saeid, 2018). This is used for identifying whether a given project should be

accepted or not.

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

233750

Depreciation = 233750 / 6

= 33958.33

Computation of Average rate of return

Year Cash inflows

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 33541.67

2 33541.67

3 33541.67

4 33541.67

5 33541.67

6 33541.67

Average profit or cash inflow 33541.67

Average initial investment 275000

average initial investment

[(initial investment + scrap value)

/ 2]

ARR 12.19%

ARR = (33541 /275000)*100 =>12.19%

Recommendations

The above study shows that adopting this machine will give the company return of

12.19%. As compared with other projects returns is comparatively low. Company makes

investments for having adequate rate of return. The machine is providing the rate at which it

would not be beneficial to have the machine. The technique is not suggesting to adopt the project

further assessment will be made for knowing the viability of project.

Net Present Value

Analysts and experts measure NPV for knowing the present value of future cash flows. It

shows whether the future inflows will be able to recover the present outflows. It is calculated to

make the comparisons on same scale. Project is considered as profitable if it is left with the

positive NPV (Chadha and Sharma, 2019). It is derived when the present value of future cash

flows is more than the present outflow.

Computation of NPV

Year Cash inflows

PV factor @

12%

Discounted cash

inflows

1 72500 0.893 64732.14

2 72500 0.797 57797

9

2 33541.67

3 33541.67

4 33541.67

5 33541.67

6 33541.67

Average profit or cash inflow 33541.67

Average initial investment 275000

average initial investment

[(initial investment + scrap value)

/ 2]

ARR 12.19%

ARR = (33541 /275000)*100 =>12.19%

Recommendations

The above study shows that adopting this machine will give the company return of

12.19%. As compared with other projects returns is comparatively low. Company makes

investments for having adequate rate of return. The machine is providing the rate at which it

would not be beneficial to have the machine. The technique is not suggesting to adopt the project

further assessment will be made for knowing the viability of project.

Net Present Value

Analysts and experts measure NPV for knowing the present value of future cash flows. It

shows whether the future inflows will be able to recover the present outflows. It is calculated to

make the comparisons on same scale. Project is considered as profitable if it is left with the

positive NPV (Chadha and Sharma, 2019). It is derived when the present value of future cash

flows is more than the present outflow.

Computation of NPV

Year Cash inflows

PV factor @

12%

Discounted cash

inflows

1 72500 0.893 64732.14

2 72500 0.797 57797

9

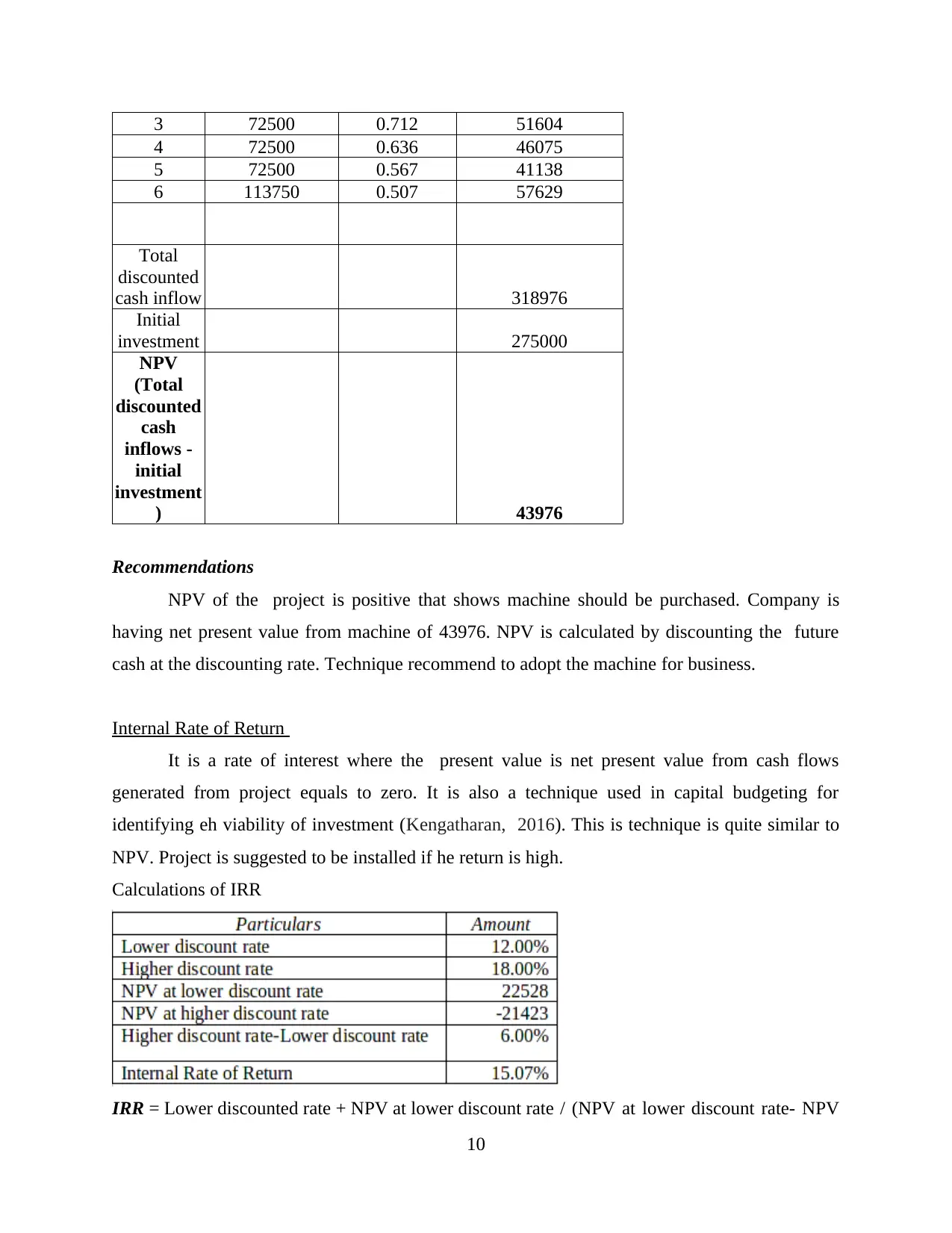

3 72500 0.712 51604

4 72500 0.636 46075

5 72500 0.567 41138

6 113750 0.507 57629

Total

discounted

cash inflow 318976

Initial

investment 275000

NPV

(Total

discounted

cash

inflows -

initial

investment

) 43976

Recommendations

NPV of the project is positive that shows machine should be purchased. Company is

having net present value from machine of 43976. NPV is calculated by discounting the future

cash at the discounting rate. Technique recommend to adopt the machine for business.

Internal Rate of Return

It is a rate of interest where the present value is net present value from cash flows

generated from project equals to zero. It is also a technique used in capital budgeting for

identifying eh viability of investment (Kengatharan, 2016). This is technique is quite similar to

NPV. Project is suggested to be installed if he return is high.

Calculations of IRR

IRR = Lower discounted rate + NPV at lower discount rate / (NPV at lower discount rate- NPV

10

4 72500 0.636 46075

5 72500 0.567 41138

6 113750 0.507 57629

Total

discounted

cash inflow 318976

Initial

investment 275000

NPV

(Total

discounted

cash

inflows -

initial

investment

) 43976

Recommendations

NPV of the project is positive that shows machine should be purchased. Company is

having net present value from machine of 43976. NPV is calculated by discounting the future

cash at the discounting rate. Technique recommend to adopt the machine for business.

Internal Rate of Return

It is a rate of interest where the present value is net present value from cash flows

generated from project equals to zero. It is also a technique used in capital budgeting for

identifying eh viability of investment (Kengatharan, 2016). This is technique is quite similar to

NPV. Project is suggested to be installed if he return is high.

Calculations of IRR

IRR = Lower discounted rate + NPV at lower discount rate / (NPV at lower discount rate- NPV

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.