Budget Preparation and Analysis for Libertine Restaurant Pty Ltd

VerifiedAdded on 2020/10/22

|21

|7049

|341

Report

AI Summary

This report provides a detailed financial analysis of Libertine Restaurant Pty Ltd., encompassing budget preparation, sales projections, profit and loss statements, and cash flow analysis for the fiscal year 2017/18. The analysis includes quarterly sales budgets for food and beverages, along with corresponding cost of goods sold, leading to the calculation of gross profit. Expense breakdowns, including accounting fees, interest, depreciation, advertising, and various operational costs, are presented to determine net profit before and after tax. The report also addresses GST calculations, aged debtor summaries, and variance reports to assess financial performance. Key performance indicators (KPIs) are highlighted, and recommendations are offered for improving financial efficiency, including the use of financial software and adherence to relevant legislation. The report emphasizes strategies for cost efficiency, debt control, and profitability maximization, providing a comprehensive overview of the restaurant's financial health and future prospects. The report also covers topics such as tax liabilities, compliance requirements, financial analysis software, accounting principles, and implications of probity.

PREPARE BUDGET

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

ASSESSMENT: 1............................................................................................................................1

PART A...........................................................................................................................................1

Business Concept.........................................................................................................................1

Aim and Objectives.....................................................................................................................1

Strategies......................................................................................................................................2

Sales Budget for 2017/18 by quarter...........................................................................................2

Preparing budgeted profit and loss for 2017/18 quarterly...........................................................3

Preparing the cash flow analysis report with GST measurements..............................................5

Preparing the Budgeted aged Debtor’s summary by quarterly....................................................6

PART B...........................................................................................................................................7

1. Identification and measurement for tax liabilities in libertine restaurant group Pty ltd..........7

2. Determination of current compliance requirements and liabilities for business with the

influences of corporation act 2001..............................................................................................7

3. Reviewing the financial analysis software for Libertine restaurant group Pty ltd..................8

4.Explaining the principles of accounting in developing budgets...............................................8

5. Explaining implications of probity when preparing and revising budgets..............................9

6. Identifying most viable Financial Quarter for Libertine restaurant group Pty Ltd..................9

7. Listing any other items for inclusion in the budget for firm..................................................10

8. Listing internal controls that could improve risk management techniques including

maintenance of audit trails.........................................................................................................10

9. Discussing Australian legislations.........................................................................................11

ASSESMENT: 2............................................................................................................................12

Budget variance report...............................................................................................................12

Budgeted Financial outgoing.....................................................................................................13

Cashflow analysis variance report- 30th September 2017..........................................................13

Aged debtors variance report- 30th September 2017..................................................................14

Budgeted Aged Debtors report:.................................................................................................14

PERFORMANCE..........................................................................................................................14

Financial outgoings KPI’s Actuals – 30th September 2017.......................................................14

INTRODUCTION...........................................................................................................................1

ASSESSMENT: 1............................................................................................................................1

PART A...........................................................................................................................................1

Business Concept.........................................................................................................................1

Aim and Objectives.....................................................................................................................1

Strategies......................................................................................................................................2

Sales Budget for 2017/18 by quarter...........................................................................................2

Preparing budgeted profit and loss for 2017/18 quarterly...........................................................3

Preparing the cash flow analysis report with GST measurements..............................................5

Preparing the Budgeted aged Debtor’s summary by quarterly....................................................6

PART B...........................................................................................................................................7

1. Identification and measurement for tax liabilities in libertine restaurant group Pty ltd..........7

2. Determination of current compliance requirements and liabilities for business with the

influences of corporation act 2001..............................................................................................7

3. Reviewing the financial analysis software for Libertine restaurant group Pty ltd..................8

4.Explaining the principles of accounting in developing budgets...............................................8

5. Explaining implications of probity when preparing and revising budgets..............................9

6. Identifying most viable Financial Quarter for Libertine restaurant group Pty Ltd..................9

7. Listing any other items for inclusion in the budget for firm..................................................10

8. Listing internal controls that could improve risk management techniques including

maintenance of audit trails.........................................................................................................10

9. Discussing Australian legislations.........................................................................................11

ASSESMENT: 2............................................................................................................................12

Budget variance report...............................................................................................................12

Budgeted Financial outgoing.....................................................................................................13

Cashflow analysis variance report- 30th September 2017..........................................................13

Aged debtors variance report- 30th September 2017..................................................................14

Budgeted Aged Debtors report:.................................................................................................14

PERFORMANCE..........................................................................................................................14

Financial outgoings KPI’s Actuals – 30th September 2017.......................................................14

RECOMMENDATIONS...............................................................................................................15

EVALUATIONS...........................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

EVALUATIONS...........................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

To analyse the cost requirements in the business activities which will be based on

determining the accurate information regarding the past transactional records. The required

amount of fund will help professionals in an organisation to make further planning and

operational increment with helps in achieving the targets at the right time. In the present report,

there will be discussion based on various accounts of Libertine restaurant Pty Ltd. with

references to have effective financial stability. There will be preparation of various budget which

includes cash, sales, profit and loss, debtor ageing etc. along with this there will be variances

analysis among the actual and budgeted outcomes of quarterly observation.

Moreover, these are the key performance indicators which helps in analysing the outcomes

and making appropriate decision for organisational plans and policies. In addition, there will be

various suggestions to the professionals which arereleve4nta with the key legislations and the

future increment in the operational tactics. Implication of various financial software will be

suggested to them as they could have rise in the operational goals.

ASSESSMENT: 1

PART A

Business Concept

Libertine restaurant Pty Ltd has been engaged in operating in restaurant business which is

in approach for increasing the operational efficiency and business performance. there have been

use of various software and techniques in accounting practices and methods for resolving the

business issues. Therefore, there were various consequences have incurred which were affecting

the financial stability in the frim. The mismanagement of operational practices has been based on

centralising the business aspects. Managing the proper records and implication of several plans

and policies which will be helpful in governing the business tasks to bring stability in activities.

Aim and Objectives

Aim: To develop internal accounting and budgeting techniques which will help in

governing financial performance of Libertine restaurant Pty Ltd

Objectives:

To increase cost efficiency in the business and improving the financial stability.

To develop strategies for debt control, cost execution, improves equity funding as well as

maximisation of profitability.

1

To analyse the cost requirements in the business activities which will be based on

determining the accurate information regarding the past transactional records. The required

amount of fund will help professionals in an organisation to make further planning and

operational increment with helps in achieving the targets at the right time. In the present report,

there will be discussion based on various accounts of Libertine restaurant Pty Ltd. with

references to have effective financial stability. There will be preparation of various budget which

includes cash, sales, profit and loss, debtor ageing etc. along with this there will be variances

analysis among the actual and budgeted outcomes of quarterly observation.

Moreover, these are the key performance indicators which helps in analysing the outcomes

and making appropriate decision for organisational plans and policies. In addition, there will be

various suggestions to the professionals which arereleve4nta with the key legislations and the

future increment in the operational tactics. Implication of various financial software will be

suggested to them as they could have rise in the operational goals.

ASSESSMENT: 1

PART A

Business Concept

Libertine restaurant Pty Ltd has been engaged in operating in restaurant business which is

in approach for increasing the operational efficiency and business performance. there have been

use of various software and techniques in accounting practices and methods for resolving the

business issues. Therefore, there were various consequences have incurred which were affecting

the financial stability in the frim. The mismanagement of operational practices has been based on

centralising the business aspects. Managing the proper records and implication of several plans

and policies which will be helpful in governing the business tasks to bring stability in activities.

Aim and Objectives

Aim: To develop internal accounting and budgeting techniques which will help in

governing financial performance of Libertine restaurant Pty Ltd

Objectives:

To increase cost efficiency in the business and improving the financial stability.

To develop strategies for debt control, cost execution, improves equity funding as well as

maximisation of profitability.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

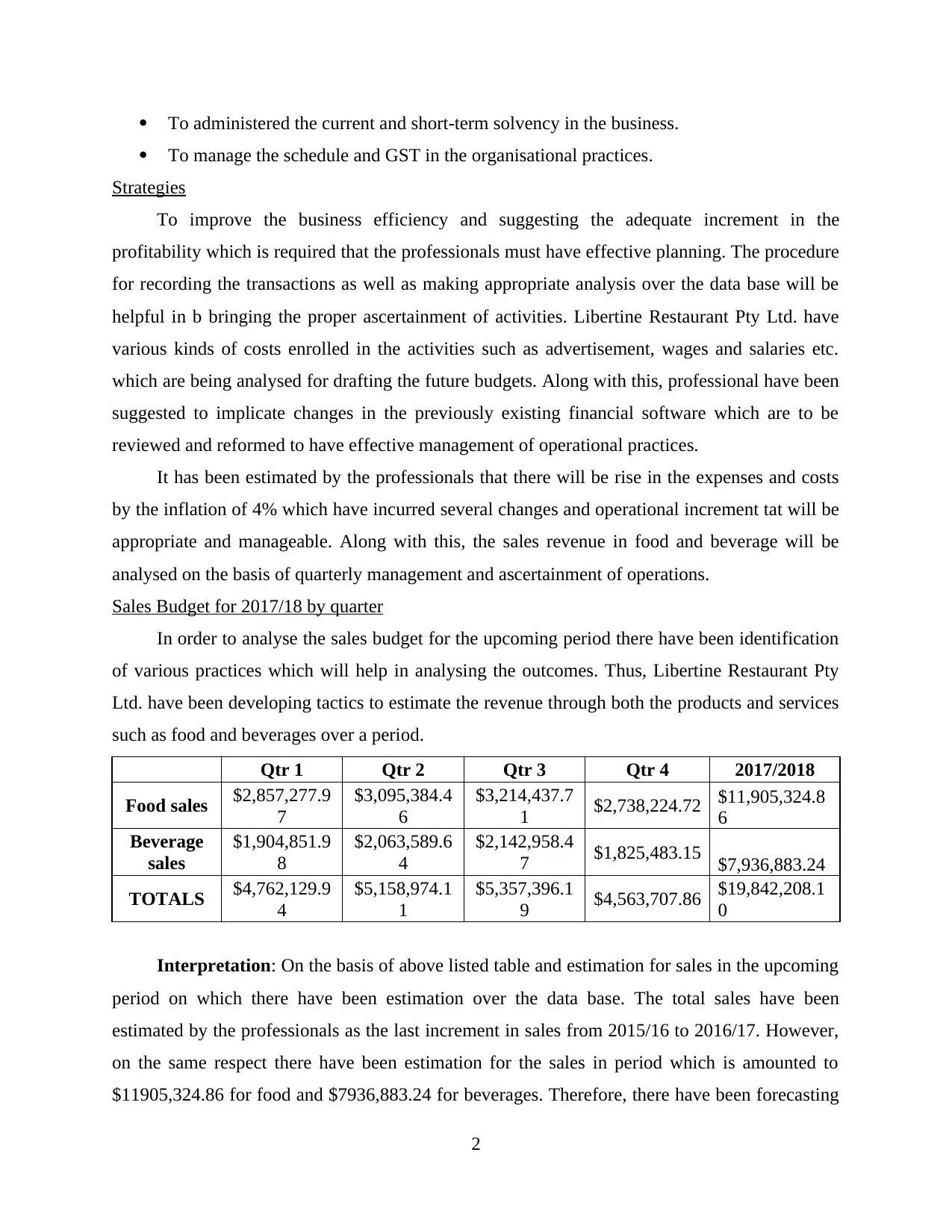

To administered the current and short-term solvency in the business.

To manage the schedule and GST in the organisational practices.

Strategies

To improve the business efficiency and suggesting the adequate increment in the

profitability which is required that the professionals must have effective planning. The procedure

for recording the transactions as well as making appropriate analysis over the data base will be

helpful in b bringing the proper ascertainment of activities. Libertine Restaurant Pty Ltd. have

various kinds of costs enrolled in the activities such as advertisement, wages and salaries etc.

which are being analysed for drafting the future budgets. Along with this, professional have been

suggested to implicate changes in the previously existing financial software which are to be

reviewed and reformed to have effective management of operational practices.

It has been estimated by the professionals that there will be rise in the expenses and costs

by the inflation of 4% which have incurred several changes and operational increment tat will be

appropriate and manageable. Along with this, the sales revenue in food and beverage will be

analysed on the basis of quarterly management and ascertainment of operations.

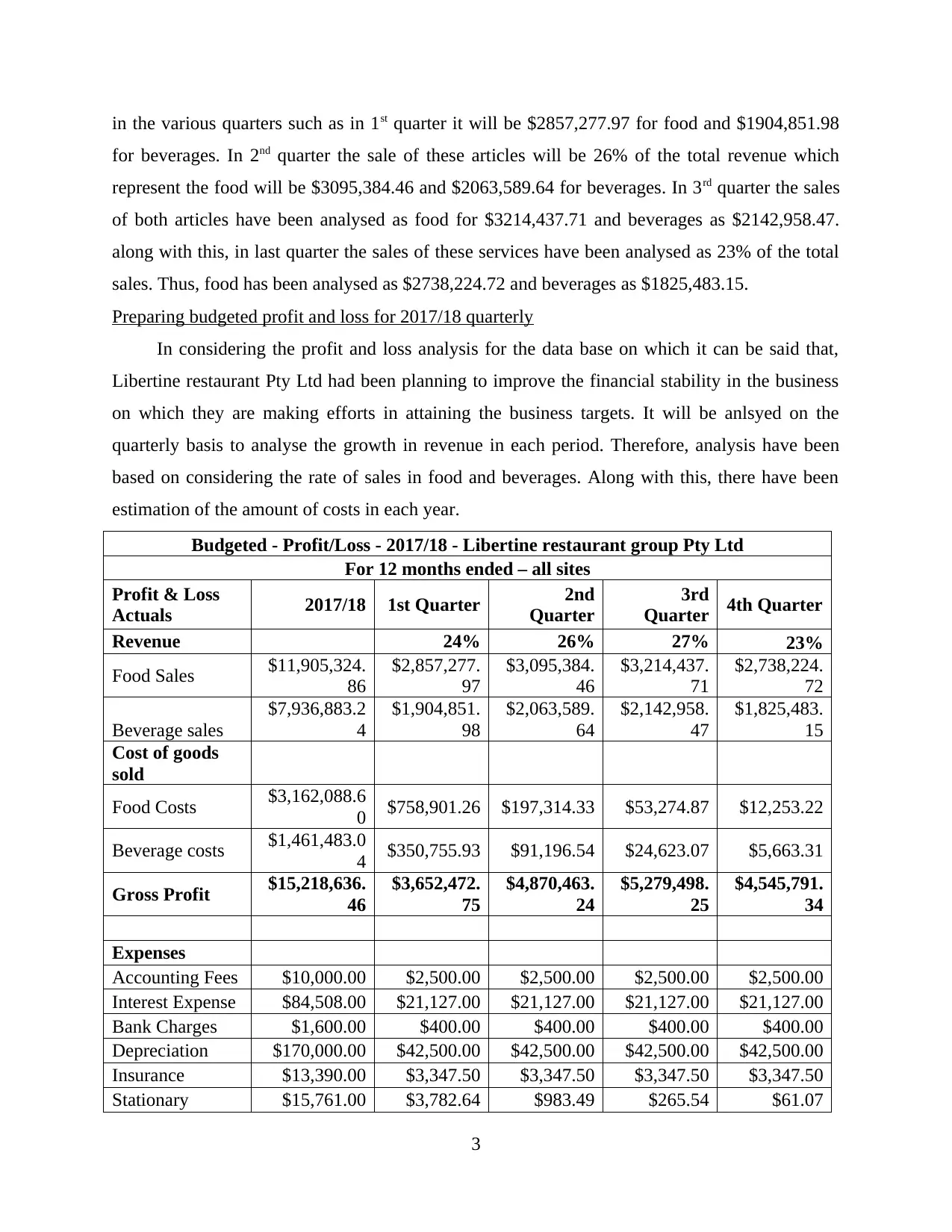

Sales Budget for 2017/18 by quarter

In order to analyse the sales budget for the upcoming period there have been identification

of various practices which will help in analysing the outcomes. Thus, Libertine Restaurant Pty

Ltd. have been developing tactics to estimate the revenue through both the products and services

such as food and beverages over a period.

Qtr 1 Qtr 2 Qtr 3 Qtr 4 2017/2018

Food sales $2,857,277.9

7

$3,095,384.4

6

$3,214,437.7

1 $2,738,224.72 $11,905,324.8

6

Beverage

sales

$1,904,851.9

8

$2,063,589.6

4

$2,142,958.4

7 $1,825,483.15 $7,936,883.24

TOTALS $4,762,129.9

4

$5,158,974.1

1

$5,357,396.1

9 $4,563,707.86 $19,842,208.1

0

Interpretation: On the basis of above listed table and estimation for sales in the upcoming

period on which there have been estimation over the data base. The total sales have been

estimated by the professionals as the last increment in sales from 2015/16 to 2016/17. However,

on the same respect there have been estimation for the sales in period which is amounted to

$11905,324.86 for food and $7936,883.24 for beverages. Therefore, there have been forecasting

2

To manage the schedule and GST in the organisational practices.

Strategies

To improve the business efficiency and suggesting the adequate increment in the

profitability which is required that the professionals must have effective planning. The procedure

for recording the transactions as well as making appropriate analysis over the data base will be

helpful in b bringing the proper ascertainment of activities. Libertine Restaurant Pty Ltd. have

various kinds of costs enrolled in the activities such as advertisement, wages and salaries etc.

which are being analysed for drafting the future budgets. Along with this, professional have been

suggested to implicate changes in the previously existing financial software which are to be

reviewed and reformed to have effective management of operational practices.

It has been estimated by the professionals that there will be rise in the expenses and costs

by the inflation of 4% which have incurred several changes and operational increment tat will be

appropriate and manageable. Along with this, the sales revenue in food and beverage will be

analysed on the basis of quarterly management and ascertainment of operations.

Sales Budget for 2017/18 by quarter

In order to analyse the sales budget for the upcoming period there have been identification

of various practices which will help in analysing the outcomes. Thus, Libertine Restaurant Pty

Ltd. have been developing tactics to estimate the revenue through both the products and services

such as food and beverages over a period.

Qtr 1 Qtr 2 Qtr 3 Qtr 4 2017/2018

Food sales $2,857,277.9

7

$3,095,384.4

6

$3,214,437.7

1 $2,738,224.72 $11,905,324.8

6

Beverage

sales

$1,904,851.9

8

$2,063,589.6

4

$2,142,958.4

7 $1,825,483.15 $7,936,883.24

TOTALS $4,762,129.9

4

$5,158,974.1

1

$5,357,396.1

9 $4,563,707.86 $19,842,208.1

0

Interpretation: On the basis of above listed table and estimation for sales in the upcoming

period on which there have been estimation over the data base. The total sales have been

estimated by the professionals as the last increment in sales from 2015/16 to 2016/17. However,

on the same respect there have been estimation for the sales in period which is amounted to

$11905,324.86 for food and $7936,883.24 for beverages. Therefore, there have been forecasting

2

in the various quarters such as in 1st quarter it will be $2857,277.97 for food and $1904,851.98

for beverages. In 2nd quarter the sale of these articles will be 26% of the total revenue which

represent the food will be $3095,384.46 and $2063,589.64 for beverages. In 3rd quarter the sales

of both articles have been analysed as food for $3214,437.71 and beverages as $2142,958.47.

along with this, in last quarter the sales of these services have been analysed as 23% of the total

sales. Thus, food has been analysed as $2738,224.72 and beverages as $1825,483.15.

Preparing budgeted profit and loss for 2017/18 quarterly

In considering the profit and loss analysis for the data base on which it can be said that,

Libertine restaurant Pty Ltd had been planning to improve the financial stability in the business

on which they are making efforts in attaining the business targets. It will be anlsyed on the

quarterly basis to analyse the growth in revenue in each period. Therefore, analysis have been

based on considering the rate of sales in food and beverages. Along with this, there have been

estimation of the amount of costs in each year.

Budgeted - Profit/Loss - 2017/18 - Libertine restaurant group Pty Ltd

For 12 months ended – all sites

Profit & Loss

Actuals 2017/18 1st Quarter 2nd

Quarter

3rd

Quarter 4th Quarter

Revenue 24% 26% 27% 23%

Food Sales $11,905,324.

86

$2,857,277.

97

$3,095,384.

46

$3,214,437.

71

$2,738,224.

72

Beverage sales

$7,936,883.2

4

$1,904,851.

98

$2,063,589.

64

$2,142,958.

47

$1,825,483.

15

Cost of goods

sold

Food Costs $3,162,088.6

0 $758,901.26 $197,314.33 $53,274.87 $12,253.22

Beverage costs $1,461,483.0

4 $350,755.93 $91,196.54 $24,623.07 $5,663.31

Gross Profit $15,218,636.

46

$3,652,472.

75

$4,870,463.

24

$5,279,498.

25

$4,545,791.

34

Expenses

Accounting Fees $10,000.00 $2,500.00 $2,500.00 $2,500.00 $2,500.00

Interest Expense $84,508.00 $21,127.00 $21,127.00 $21,127.00 $21,127.00

Bank Charges $1,600.00 $400.00 $400.00 $400.00 $400.00

Depreciation $170,000.00 $42,500.00 $42,500.00 $42,500.00 $42,500.00

Insurance $13,390.00 $3,347.50 $3,347.50 $3,347.50 $3,347.50

Stationary $15,761.00 $3,782.64 $983.49 $265.54 $61.07

3

for beverages. In 2nd quarter the sale of these articles will be 26% of the total revenue which

represent the food will be $3095,384.46 and $2063,589.64 for beverages. In 3rd quarter the sales

of both articles have been analysed as food for $3214,437.71 and beverages as $2142,958.47.

along with this, in last quarter the sales of these services have been analysed as 23% of the total

sales. Thus, food has been analysed as $2738,224.72 and beverages as $1825,483.15.

Preparing budgeted profit and loss for 2017/18 quarterly

In considering the profit and loss analysis for the data base on which it can be said that,

Libertine restaurant Pty Ltd had been planning to improve the financial stability in the business

on which they are making efforts in attaining the business targets. It will be anlsyed on the

quarterly basis to analyse the growth in revenue in each period. Therefore, analysis have been

based on considering the rate of sales in food and beverages. Along with this, there have been

estimation of the amount of costs in each year.

Budgeted - Profit/Loss - 2017/18 - Libertine restaurant group Pty Ltd

For 12 months ended – all sites

Profit & Loss

Actuals 2017/18 1st Quarter 2nd

Quarter

3rd

Quarter 4th Quarter

Revenue 24% 26% 27% 23%

Food Sales $11,905,324.

86

$2,857,277.

97

$3,095,384.

46

$3,214,437.

71

$2,738,224.

72

Beverage sales

$7,936,883.2

4

$1,904,851.

98

$2,063,589.

64

$2,142,958.

47

$1,825,483.

15

Cost of goods

sold

Food Costs $3,162,088.6

0 $758,901.26 $197,314.33 $53,274.87 $12,253.22

Beverage costs $1,461,483.0

4 $350,755.93 $91,196.54 $24,623.07 $5,663.31

Gross Profit $15,218,636.

46

$3,652,472.

75

$4,870,463.

24

$5,279,498.

25

$4,545,791.

34

Expenses

Accounting Fees $10,000.00 $2,500.00 $2,500.00 $2,500.00 $2,500.00

Interest Expense $84,508.00 $21,127.00 $21,127.00 $21,127.00 $21,127.00

Bank Charges $1,600.00 $400.00 $400.00 $400.00 $400.00

Depreciation $170,000.00 $42,500.00 $42,500.00 $42,500.00 $42,500.00

Insurance $13,390.00 $3,347.50 $3,347.50 $3,347.50 $3,347.50

Stationary $15,761.00 $3,782.64 $983.49 $265.54 $61.07

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

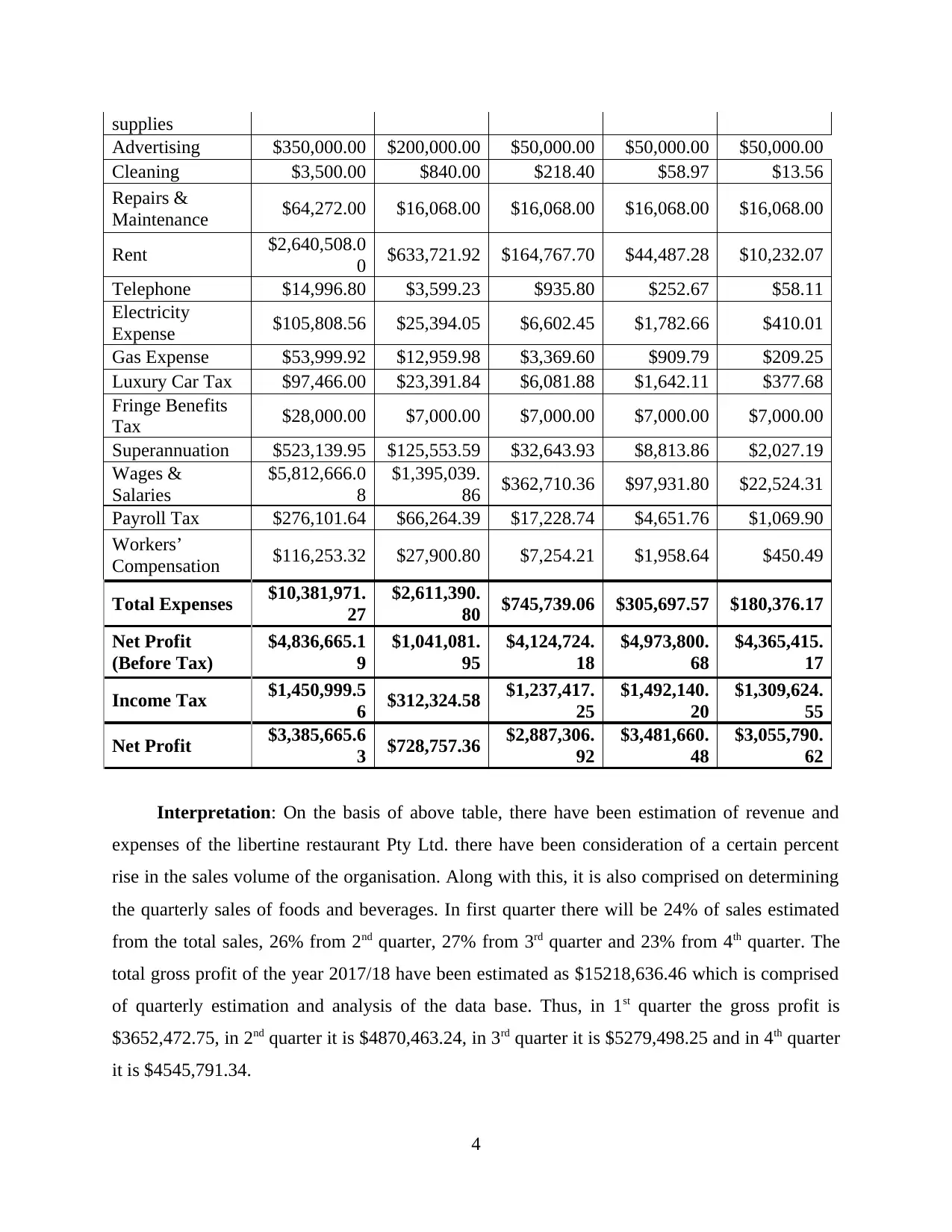

supplies

Advertising $350,000.00 $200,000.00 $50,000.00 $50,000.00 $50,000.00

Cleaning $3,500.00 $840.00 $218.40 $58.97 $13.56

Repairs &

Maintenance $64,272.00 $16,068.00 $16,068.00 $16,068.00 $16,068.00

Rent $2,640,508.0

0 $633,721.92 $164,767.70 $44,487.28 $10,232.07

Telephone $14,996.80 $3,599.23 $935.80 $252.67 $58.11

Electricity

Expense $105,808.56 $25,394.05 $6,602.45 $1,782.66 $410.01

Gas Expense $53,999.92 $12,959.98 $3,369.60 $909.79 $209.25

Luxury Car Tax $97,466.00 $23,391.84 $6,081.88 $1,642.11 $377.68

Fringe Benefits

Tax $28,000.00 $7,000.00 $7,000.00 $7,000.00 $7,000.00

Superannuation $523,139.95 $125,553.59 $32,643.93 $8,813.86 $2,027.19

Wages &

Salaries

$5,812,666.0

8

$1,395,039.

86 $362,710.36 $97,931.80 $22,524.31

Payroll Tax $276,101.64 $66,264.39 $17,228.74 $4,651.76 $1,069.90

Workers’

Compensation $116,253.32 $27,900.80 $7,254.21 $1,958.64 $450.49

Total Expenses $10,381,971.

27

$2,611,390.

80 $745,739.06 $305,697.57 $180,376.17

Net Profit

(Before Tax)

$4,836,665.1

9

$1,041,081.

95

$4,124,724.

18

$4,973,800.

68

$4,365,415.

17

Income Tax $1,450,999.5

6 $312,324.58 $1,237,417.

25

$1,492,140.

20

$1,309,624.

55

Net Profit $3,385,665.6

3 $728,757.36 $2,887,306.

92

$3,481,660.

48

$3,055,790.

62

Interpretation: On the basis of above table, there have been estimation of revenue and

expenses of the libertine restaurant Pty Ltd. there have been consideration of a certain percent

rise in the sales volume of the organisation. Along with this, it is also comprised on determining

the quarterly sales of foods and beverages. In first quarter there will be 24% of sales estimated

from the total sales, 26% from 2nd quarter, 27% from 3rd quarter and 23% from 4th quarter. The

total gross profit of the year 2017/18 have been estimated as $15218,636.46 which is comprised

of quarterly estimation and analysis of the data base. Thus, in 1st quarter the gross profit is

$3652,472.75, in 2nd quarter it is $4870,463.24, in 3rd quarter it is $5279,498.25 and in 4th quarter

it is $4545,791.34.

4

Advertising $350,000.00 $200,000.00 $50,000.00 $50,000.00 $50,000.00

Cleaning $3,500.00 $840.00 $218.40 $58.97 $13.56

Repairs &

Maintenance $64,272.00 $16,068.00 $16,068.00 $16,068.00 $16,068.00

Rent $2,640,508.0

0 $633,721.92 $164,767.70 $44,487.28 $10,232.07

Telephone $14,996.80 $3,599.23 $935.80 $252.67 $58.11

Electricity

Expense $105,808.56 $25,394.05 $6,602.45 $1,782.66 $410.01

Gas Expense $53,999.92 $12,959.98 $3,369.60 $909.79 $209.25

Luxury Car Tax $97,466.00 $23,391.84 $6,081.88 $1,642.11 $377.68

Fringe Benefits

Tax $28,000.00 $7,000.00 $7,000.00 $7,000.00 $7,000.00

Superannuation $523,139.95 $125,553.59 $32,643.93 $8,813.86 $2,027.19

Wages &

Salaries

$5,812,666.0

8

$1,395,039.

86 $362,710.36 $97,931.80 $22,524.31

Payroll Tax $276,101.64 $66,264.39 $17,228.74 $4,651.76 $1,069.90

Workers’

Compensation $116,253.32 $27,900.80 $7,254.21 $1,958.64 $450.49

Total Expenses $10,381,971.

27

$2,611,390.

80 $745,739.06 $305,697.57 $180,376.17

Net Profit

(Before Tax)

$4,836,665.1

9

$1,041,081.

95

$4,124,724.

18

$4,973,800.

68

$4,365,415.

17

Income Tax $1,450,999.5

6 $312,324.58 $1,237,417.

25

$1,492,140.

20

$1,309,624.

55

Net Profit $3,385,665.6

3 $728,757.36 $2,887,306.

92

$3,481,660.

48

$3,055,790.

62

Interpretation: On the basis of above table, there have been estimation of revenue and

expenses of the libertine restaurant Pty Ltd. there have been consideration of a certain percent

rise in the sales volume of the organisation. Along with this, it is also comprised on determining

the quarterly sales of foods and beverages. In first quarter there will be 24% of sales estimated

from the total sales, 26% from 2nd quarter, 27% from 3rd quarter and 23% from 4th quarter. The

total gross profit of the year 2017/18 have been estimated as $15218,636.46 which is comprised

of quarterly estimation and analysis of the data base. Thus, in 1st quarter the gross profit is

$3652,472.75, in 2nd quarter it is $4870,463.24, in 3rd quarter it is $5279,498.25 and in 4th quarter

it is $4545,791.34.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Additionally, there have been ascertainment of costs and expenses in the operational

activities which are being determined by implicating several techniques. the fixed costs have

been categorised in a manner that it will equally charged in each quarter. Therefore, to estimate

the variable costs for the upcoming period on which there have been use of sales revenue

percentage. Moreover, there have been several charges based on taxation which are have to be

bare by the organisation. The corporate tax of 30% have been analysed and charges as per having

appropriate ascertainment of data base.

As per analysing the profitability of the organisation ion which it has been estimated by the

professionals that 3385,665.63 as the total profit retained by the business which determines the

NP margin as 17%. Therefore, to categorise the profitability on the quarterly basis on which the

net profit has been generated by the professionals as 728,757.36 which is 15%, in 2nd quarter it is

2887,306.92 which is 56%, in 3rd quarter it is 3481,660.48 that is 65% and in 4th quarter it will be

3055790.62 which is 67%. However, as per analysing such outcomes on which it can be said that

the last quarter will be profitable to the industry in terms of having appropriate outcomes.

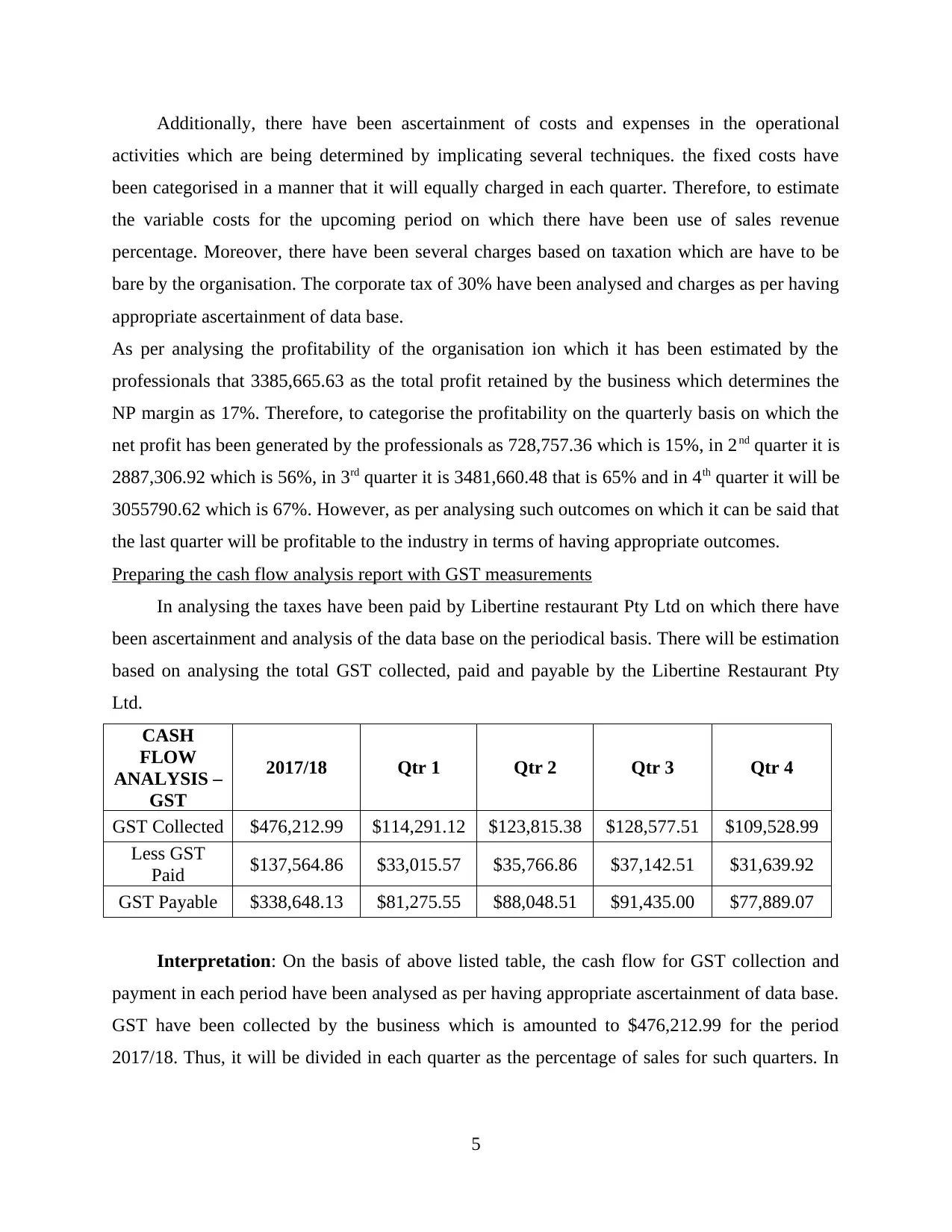

Preparing the cash flow analysis report with GST measurements

In analysing the taxes have been paid by Libertine restaurant Pty Ltd on which there have

been ascertainment and analysis of the data base on the periodical basis. There will be estimation

based on analysing the total GST collected, paid and payable by the Libertine Restaurant Pty

Ltd.

CASH

FLOW

ANALYSIS –

GST

2017/18 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $476,212.99 $114,291.12 $123,815.38 $128,577.51 $109,528.99

Less GST

Paid $137,564.86 $33,015.57 $35,766.86 $37,142.51 $31,639.92

GST Payable $338,648.13 $81,275.55 $88,048.51 $91,435.00 $77,889.07

Interpretation: On the basis of above listed table, the cash flow for GST collection and

payment in each period have been analysed as per having appropriate ascertainment of data base.

GST have been collected by the business which is amounted to $476,212.99 for the period

2017/18. Thus, it will be divided in each quarter as the percentage of sales for such quarters. In

5

activities which are being determined by implicating several techniques. the fixed costs have

been categorised in a manner that it will equally charged in each quarter. Therefore, to estimate

the variable costs for the upcoming period on which there have been use of sales revenue

percentage. Moreover, there have been several charges based on taxation which are have to be

bare by the organisation. The corporate tax of 30% have been analysed and charges as per having

appropriate ascertainment of data base.

As per analysing the profitability of the organisation ion which it has been estimated by the

professionals that 3385,665.63 as the total profit retained by the business which determines the

NP margin as 17%. Therefore, to categorise the profitability on the quarterly basis on which the

net profit has been generated by the professionals as 728,757.36 which is 15%, in 2nd quarter it is

2887,306.92 which is 56%, in 3rd quarter it is 3481,660.48 that is 65% and in 4th quarter it will be

3055790.62 which is 67%. However, as per analysing such outcomes on which it can be said that

the last quarter will be profitable to the industry in terms of having appropriate outcomes.

Preparing the cash flow analysis report with GST measurements

In analysing the taxes have been paid by Libertine restaurant Pty Ltd on which there have

been ascertainment and analysis of the data base on the periodical basis. There will be estimation

based on analysing the total GST collected, paid and payable by the Libertine Restaurant Pty

Ltd.

CASH

FLOW

ANALYSIS –

GST

2017/18 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $476,212.99 $114,291.12 $123,815.38 $128,577.51 $109,528.99

Less GST

Paid $137,564.86 $33,015.57 $35,766.86 $37,142.51 $31,639.92

GST Payable $338,648.13 $81,275.55 $88,048.51 $91,435.00 $77,889.07

Interpretation: On the basis of above listed table, the cash flow for GST collection and

payment in each period have been analysed as per having appropriate ascertainment of data base.

GST have been collected by the business which is amounted to $476,212.99 for the period

2017/18. Thus, it will be divided in each quarter as the percentage of sales for such quarters. In

5

1st qtr the GST collected was $114291,.12, in 2nd qtr it was $123,815.38, in 3rd qtr it was

$128,577.51 and in 4th qtr it was $109,528.99.

GST have been paid by the organisation in 2017/18 $137,564.86. Thus, in 1st quarter it was

$33015.57, in 2nd quarter it had been analysed as $35,766.86, in 3rd quarter it will be $37142.51

and in 4th quarter it will be around $31639.92. Therefore, the GST for the period have been

payable by the professionals as $338,648.13 that is in 1st quarter it will be around $81275.55, in

2nd quarter it will be around $88,048.51, in 3rd quarter it will be around $91435.00 and in last

quarter it will be $77889.07.

Preparing the Budgeted aged Debtor’s summary by quarterly

In accordance with the operational practices and tactics of business in analysing the costs

which have been impacted in determining the gains. The accounts receivable gaining is the

report which brings appropriate information among the professionals which is relevant with

ascertaining the information regarding the time utilise to recover the debtors. Thus, in

accordance with determining the invoices which are overdue and the amount payment which is

yet to be recovered. On the other side, it also defined the efficiency of the firm and professionals

in collecting such overdue payments in the required deadline.

AGED

DEBTORS

BUDGET

2017/18

TOTAL Qtr 1 Qtr 2 Qtr 3 Qtr 4

Sales $4,762,129.94 $4,762,129.9

4

$5,158,974.1

1

$5,357,396.1

9

$4,563,707.8

6

% Debtors

Sales 1.00% 1.00% 1.00% 1.00% 1.00%

Total

Debtors $47,621.30 $47,621.30 $51,589.74 $53,573.96 $45,637.08

Current $40,001.89 $40,001.89 $43,335.38 $45,002.13 $38,335.15

30 Days $4,762.13 $4,762.13 $5,158.97 $5,357.40 $4,563.71

60 Days $2,381.06 $2,381.06 $2,579.49 $2,678.70 $2,281.85

90 Days $476.21 $476.21 $515.90 $535.74 $456.37

Interpretation: In accordance with the above listed table on which it can be said that, the

sale over the period was $4762,129.94 is been analysed annually. In 1st quarter the sales revenue

has been analysed as $4762,1229.94, in 2nd quarter it is 5158,974.11, in 3rd quarter it was

$5357,396.19 and in 4th quarter it was $4563,707.86. Thus, it has been estimated by the

6

$128,577.51 and in 4th qtr it was $109,528.99.

GST have been paid by the organisation in 2017/18 $137,564.86. Thus, in 1st quarter it was

$33015.57, in 2nd quarter it had been analysed as $35,766.86, in 3rd quarter it will be $37142.51

and in 4th quarter it will be around $31639.92. Therefore, the GST for the period have been

payable by the professionals as $338,648.13 that is in 1st quarter it will be around $81275.55, in

2nd quarter it will be around $88,048.51, in 3rd quarter it will be around $91435.00 and in last

quarter it will be $77889.07.

Preparing the Budgeted aged Debtor’s summary by quarterly

In accordance with the operational practices and tactics of business in analysing the costs

which have been impacted in determining the gains. The accounts receivable gaining is the

report which brings appropriate information among the professionals which is relevant with

ascertaining the information regarding the time utilise to recover the debtors. Thus, in

accordance with determining the invoices which are overdue and the amount payment which is

yet to be recovered. On the other side, it also defined the efficiency of the firm and professionals

in collecting such overdue payments in the required deadline.

AGED

DEBTORS

BUDGET

2017/18

TOTAL Qtr 1 Qtr 2 Qtr 3 Qtr 4

Sales $4,762,129.94 $4,762,129.9

4

$5,158,974.1

1

$5,357,396.1

9

$4,563,707.8

6

% Debtors

Sales 1.00% 1.00% 1.00% 1.00% 1.00%

Total

Debtors $47,621.30 $47,621.30 $51,589.74 $53,573.96 $45,637.08

Current $40,001.89 $40,001.89 $43,335.38 $45,002.13 $38,335.15

30 Days $4,762.13 $4,762.13 $5,158.97 $5,357.40 $4,563.71

60 Days $2,381.06 $2,381.06 $2,579.49 $2,678.70 $2,281.85

90 Days $476.21 $476.21 $515.90 $535.74 $456.37

Interpretation: In accordance with the above listed table on which it can be said that, the

sale over the period was $4762,129.94 is been analysed annually. In 1st quarter the sales revenue

has been analysed as $4762,1229.94, in 2nd quarter it is 5158,974.11, in 3rd quarter it was

$5357,396.19 and in 4th quarter it was $4563,707.86. Thus, it has been estimated by the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

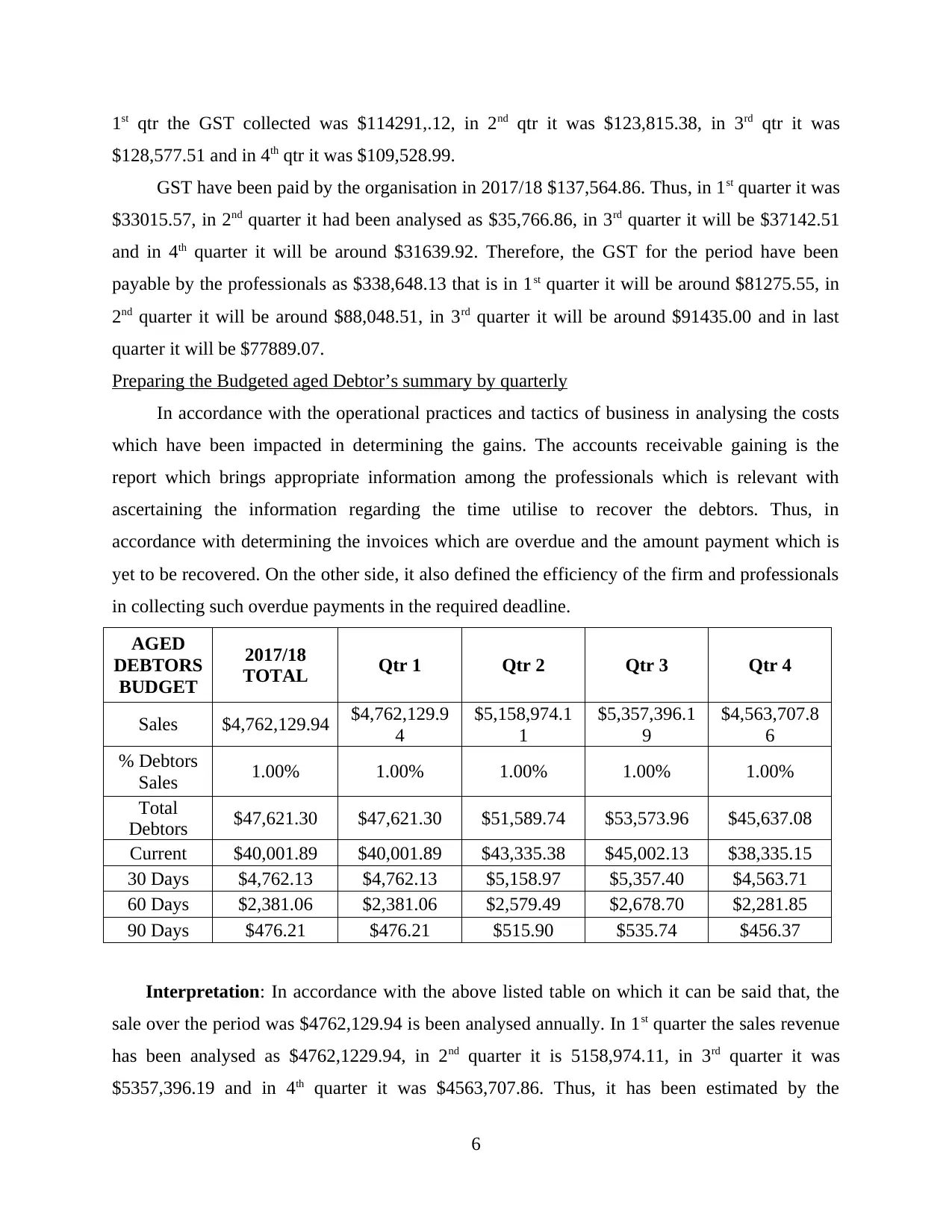

professionals that, the total debtors over the period will be 1% of the revenue therefore, it has

been forecasted by the professionals in respect with the same percentage. In 1st quarter the sales

revenue has been analysed as $47621.30, in 2nd quarter it is 51589.74, in 3rd quarter it was

$53573.96 and in 4th quarter it was $45637.08.

Moreover, the period of 30 days, 60 days and 90 days have been measured on the basis of

proportionate analysis. The 1% of charges have been estimated for the 90 days of the total debts,

5% for the 60 days of period and 10% for the 30 days of period. Therefore, it can be said that the

debtor has to be recorded in less than 30 days of time as it will help in bringing the more funds

than compared to other periods.

PART B

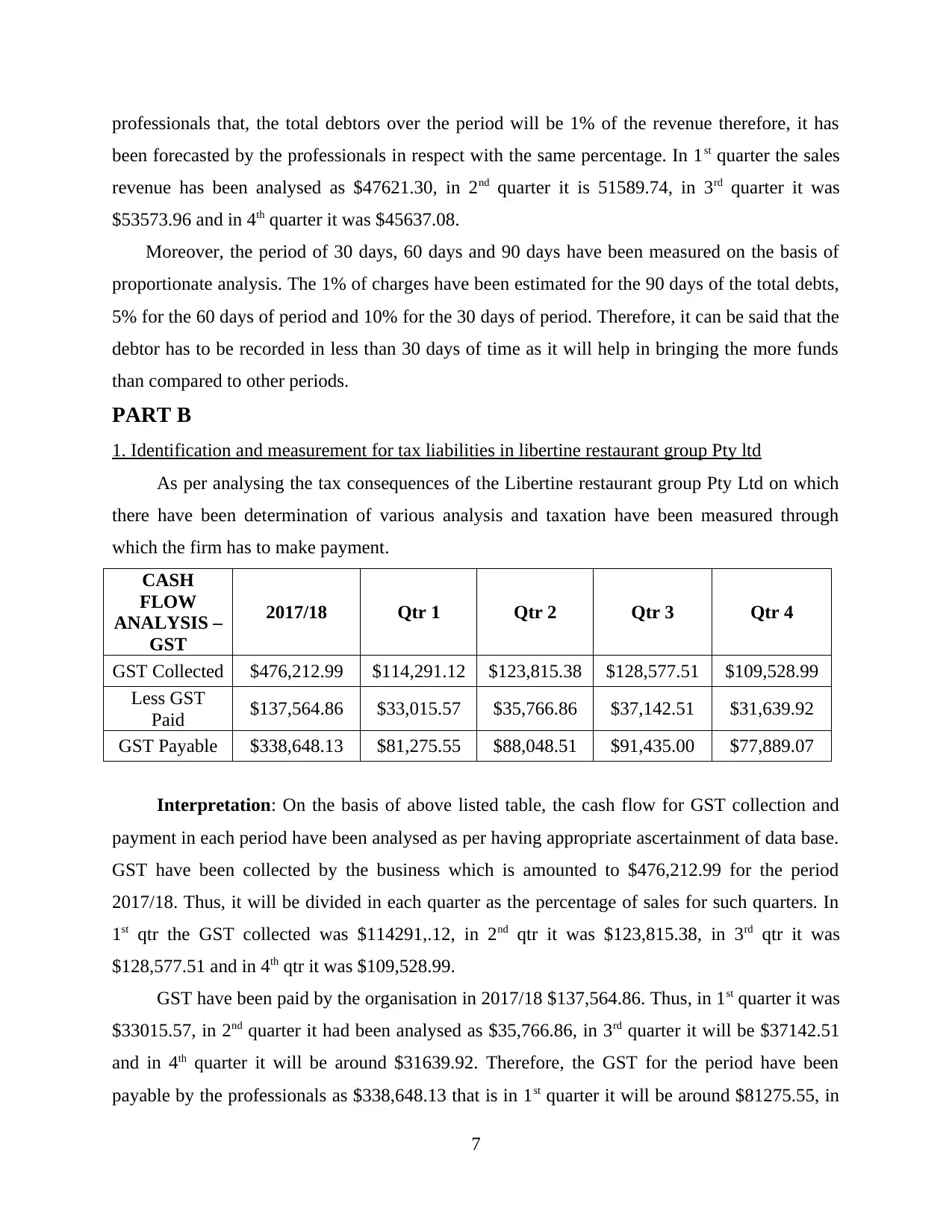

1. Identification and measurement for tax liabilities in libertine restaurant group Pty ltd

As per analysing the tax consequences of the Libertine restaurant group Pty Ltd on which

there have been determination of various analysis and taxation have been measured through

which the firm has to make payment.

CASH

FLOW

ANALYSIS –

GST

2017/18 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $476,212.99 $114,291.12 $123,815.38 $128,577.51 $109,528.99

Less GST

Paid $137,564.86 $33,015.57 $35,766.86 $37,142.51 $31,639.92

GST Payable $338,648.13 $81,275.55 $88,048.51 $91,435.00 $77,889.07

Interpretation: On the basis of above listed table, the cash flow for GST collection and

payment in each period have been analysed as per having appropriate ascertainment of data base.

GST have been collected by the business which is amounted to $476,212.99 for the period

2017/18. Thus, it will be divided in each quarter as the percentage of sales for such quarters. In

1st qtr the GST collected was $114291,.12, in 2nd qtr it was $123,815.38, in 3rd qtr it was

$128,577.51 and in 4th qtr it was $109,528.99.

GST have been paid by the organisation in 2017/18 $137,564.86. Thus, in 1st quarter it was

$33015.57, in 2nd quarter it had been analysed as $35,766.86, in 3rd quarter it will be $37142.51

and in 4th quarter it will be around $31639.92. Therefore, the GST for the period have been

payable by the professionals as $338,648.13 that is in 1st quarter it will be around $81275.55, in

7

been forecasted by the professionals in respect with the same percentage. In 1st quarter the sales

revenue has been analysed as $47621.30, in 2nd quarter it is 51589.74, in 3rd quarter it was

$53573.96 and in 4th quarter it was $45637.08.

Moreover, the period of 30 days, 60 days and 90 days have been measured on the basis of

proportionate analysis. The 1% of charges have been estimated for the 90 days of the total debts,

5% for the 60 days of period and 10% for the 30 days of period. Therefore, it can be said that the

debtor has to be recorded in less than 30 days of time as it will help in bringing the more funds

than compared to other periods.

PART B

1. Identification and measurement for tax liabilities in libertine restaurant group Pty ltd

As per analysing the tax consequences of the Libertine restaurant group Pty Ltd on which

there have been determination of various analysis and taxation have been measured through

which the firm has to make payment.

CASH

FLOW

ANALYSIS –

GST

2017/18 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $476,212.99 $114,291.12 $123,815.38 $128,577.51 $109,528.99

Less GST

Paid $137,564.86 $33,015.57 $35,766.86 $37,142.51 $31,639.92

GST Payable $338,648.13 $81,275.55 $88,048.51 $91,435.00 $77,889.07

Interpretation: On the basis of above listed table, the cash flow for GST collection and

payment in each period have been analysed as per having appropriate ascertainment of data base.

GST have been collected by the business which is amounted to $476,212.99 for the period

2017/18. Thus, it will be divided in each quarter as the percentage of sales for such quarters. In

1st qtr the GST collected was $114291,.12, in 2nd qtr it was $123,815.38, in 3rd qtr it was

$128,577.51 and in 4th qtr it was $109,528.99.

GST have been paid by the organisation in 2017/18 $137,564.86. Thus, in 1st quarter it was

$33015.57, in 2nd quarter it had been analysed as $35,766.86, in 3rd quarter it will be $37142.51

and in 4th quarter it will be around $31639.92. Therefore, the GST for the period have been

payable by the professionals as $338,648.13 that is in 1st quarter it will be around $81275.55, in

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2nd quarter it will be around $88,048.51, in 3rd quarter it will be around $91435.00 and in last

quarter it will be $77889.07.

2. Determination of current compliance requirements and liabilities for business with the

influences of corporation act 2001

To govern the business with the influences of legislative requirement and operations of the firm.

There are various laws and regulation which have been imposed by the Australian government

with an approach towards developing fair trade practices in the economy. Thus, with the

influences of corporate act 2001 there will be analysis over various operational aspects.

However, there have been influences of various rules and guidelines which are imposed by the

federal registrar of legislation which will be helpful in creating the operational encouragement

for business development.

3. Reviewing the financial analysis software for Libertine restaurant group Pty ltd

As per reviewing the previously existed financial analyses software on which financial

information have been gathered and analysed to have adequate outcomes. The point of sales

system has been used by Libertine restaurant group Pty ltd which have been used to analyze the

financial data. It has facilitated the adequate information on which organization is making

appropriate operational analysis. The accuracy of this software in analyzing the profitability on

the basis of revenue and costs which is not adequate and up-to the expectations.

However, there have been various information which have been generated through such

software which is not being reliable or accurate. Thus, it will be suggested to the professionals

that they must make necessary increment and development of plans which will help them in

analyzing the outcomes. Along with this, it can be said that, there is need to make development

in the plans and policies which will help in governing operations. There are requirements for

making changes in policies and techniques to measure the performance of the business.

therefore, installation of ERP software SPSS etc. will be adequate in demonstrating the

operational gains for the business.

4.Explaining the principles of accounting in developing budgets

Matching Principle: This accounting concept have determined that the transaction which

are recorded in the business have to be summaries in the final accounts. Therefore, the relevancy

of the data will be based on matching the information through invoices or the origin of

8

quarter it will be $77889.07.

2. Determination of current compliance requirements and liabilities for business with the

influences of corporation act 2001

To govern the business with the influences of legislative requirement and operations of the firm.

There are various laws and regulation which have been imposed by the Australian government

with an approach towards developing fair trade practices in the economy. Thus, with the

influences of corporate act 2001 there will be analysis over various operational aspects.

However, there have been influences of various rules and guidelines which are imposed by the

federal registrar of legislation which will be helpful in creating the operational encouragement

for business development.

3. Reviewing the financial analysis software for Libertine restaurant group Pty ltd

As per reviewing the previously existed financial analyses software on which financial

information have been gathered and analysed to have adequate outcomes. The point of sales

system has been used by Libertine restaurant group Pty ltd which have been used to analyze the

financial data. It has facilitated the adequate information on which organization is making

appropriate operational analysis. The accuracy of this software in analyzing the profitability on

the basis of revenue and costs which is not adequate and up-to the expectations.

However, there have been various information which have been generated through such

software which is not being reliable or accurate. Thus, it will be suggested to the professionals

that they must make necessary increment and development of plans which will help them in

analyzing the outcomes. Along with this, it can be said that, there is need to make development

in the plans and policies which will help in governing operations. There are requirements for

making changes in policies and techniques to measure the performance of the business.

therefore, installation of ERP software SPSS etc. will be adequate in demonstrating the

operational gains for the business.

4.Explaining the principles of accounting in developing budgets

Matching Principle: This accounting concept have determined that the transaction which

are recorded in the business have to be summaries in the final accounts. Therefore, the relevancy

of the data will be based on matching the information through invoices or the origin of

8

transactions. Along with this this the golden rule of balance sheet is that, there must be matching

amount for total liabilities and total assets.

Account Groups: This concept of accounting has been enacted by GAAP which define

that all the transactions are required to be addressed in several books. Thus, after such recording,

these all are required to be summarized in a summarized account. Thus, the group of accounts

will be helpful in making appropriate analysis over gains of the business.

Time Periods: The disclosure of accounts has to be based on considering the time limit

which insist communicating the performance of business among external parties.

5. Explaining implications of probity when preparing and revising budgets

The financial probity is one of the important aspect in making budgets so as to ethically

follow guidelines and prepare budgets with ease. It can be analysed that firm should be able to

enhance its position by sticking to budget prepared by which it may not get deviate from its

actual performance in effectual manner. The firm should be able to demonstrate to suppliers and

community with regards to procurement studies with high standards of probity and

accountability.

The implications of probity when preparation or revising budgets is that appropriate

checks and balances related to variance if any are analysed for making revision. Concept of

conflict interest is effectively understood and as a result, firm is able to attain clarity regarding

the differences in a better way. Confidentiality of suppliers and related stakeholders are secured

in the best way possible which leads to attainment of reliability in budgeted figures and no

information is overlooked. Moreover, expected behaviours are articulated in a better manner by

which information gets clear in a better manner and budgets are revised by personnels with ease.

Furthermore, when ethics are not conducted while preparation of budgets, it is required

that efficiencies may be implemented so that proper budgets may be revised and implications

may be altered quite effectually. On the other hand, Libertine restaurant group Pty Ltd is

required to conduct accounting as per the financial probity as governed by Australian

government.

6. Identifying most viable Financial Quarter for Libertine restaurant group Pty Ltd

Libertine restaurant group Pty Ltd is able to provide better services in effective manner.

There are two quarters which provides clarity that for 2017/18, it is performing good. From the

analysis of Budgeted Profit and Loss account, it can be analysed that most viable quarter for

9

amount for total liabilities and total assets.

Account Groups: This concept of accounting has been enacted by GAAP which define

that all the transactions are required to be addressed in several books. Thus, after such recording,

these all are required to be summarized in a summarized account. Thus, the group of accounts

will be helpful in making appropriate analysis over gains of the business.

Time Periods: The disclosure of accounts has to be based on considering the time limit

which insist communicating the performance of business among external parties.

5. Explaining implications of probity when preparing and revising budgets

The financial probity is one of the important aspect in making budgets so as to ethically

follow guidelines and prepare budgets with ease. It can be analysed that firm should be able to

enhance its position by sticking to budget prepared by which it may not get deviate from its

actual performance in effectual manner. The firm should be able to demonstrate to suppliers and

community with regards to procurement studies with high standards of probity and

accountability.

The implications of probity when preparation or revising budgets is that appropriate

checks and balances related to variance if any are analysed for making revision. Concept of

conflict interest is effectively understood and as a result, firm is able to attain clarity regarding

the differences in a better way. Confidentiality of suppliers and related stakeholders are secured

in the best way possible which leads to attainment of reliability in budgeted figures and no

information is overlooked. Moreover, expected behaviours are articulated in a better manner by

which information gets clear in a better manner and budgets are revised by personnels with ease.

Furthermore, when ethics are not conducted while preparation of budgets, it is required

that efficiencies may be implemented so that proper budgets may be revised and implications

may be altered quite effectually. On the other hand, Libertine restaurant group Pty Ltd is

required to conduct accounting as per the financial probity as governed by Australian

government.

6. Identifying most viable Financial Quarter for Libertine restaurant group Pty Ltd

Libertine restaurant group Pty Ltd is able to provide better services in effective manner.

There are two quarters which provides clarity that for 2017/18, it is performing good. From the

analysis of Budgeted Profit and Loss account, it can be analysed that most viable quarter for

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.