Mentor Education: Life Insurance Advice Assignment FNSASICX503A

VerifiedAdded on 2021/12/17

|36

|10368

|452

Homework Assignment

AI Summary

This assignment assesses the student's understanding of providing life insurance advice. It covers establishing relationships with clients, identifying their objectives, needs, and financial situations. The student demonstrates the ability to analyze client information, develop appropriate strategies, and present financial plans. The assignment also evaluates the student's knowledge of documentation, ongoing service provision, and relevant legal requirements. The assessment includes tasks on preparing for initial interviews, building rapport, explaining financial services guides, and outlining different insurance products and fees. The student's responses showcase their grasp of client needs assessment, information gathering techniques, and the application of fact-finding questions based on a provided case study. The assignment is designed to evaluate the student's competency in providing advice in life insurance, as per the FNSASICX503A unit requirements.

Insurance 1 of 36

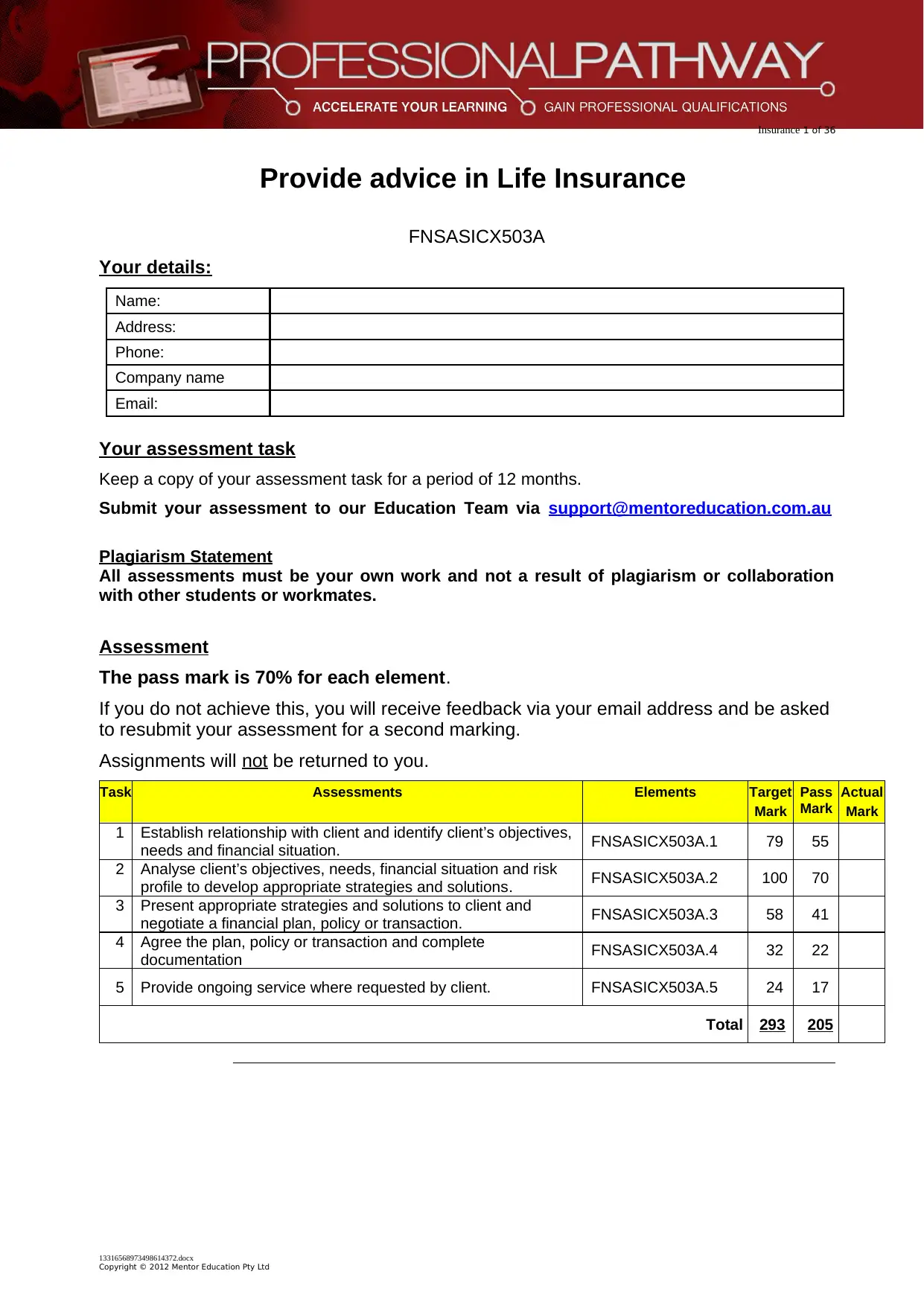

Provide advice in Life Insurance

FNSASICX503A

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

Keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via support@mentoreducation.com.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element.

If you do not achieve this, you will receive feedback via your email address and be asked

to resubmit your assessment for a second marking.

Assignments will not be returned to you.

Task Assessments Elements Target

Mark

Pass

Mark

Actual

Mark

1 Establish relationship with client and identify client’s objectives,

needs and financial situation. FNSASICX503A.1 79 55

2 Analyse client’s objectives, needs, financial situation and risk

profile to develop appropriate strategies and solutions. FNSASICX503A.2 100 70

3 Present appropriate strategies and solutions to client and

negotiate a financial plan, policy or transaction. FNSASICX503A.3 58 41

4 Agree the plan, policy or transaction and complete

documentation FNSASICX503A.4 32 22

5 Provide ongoing service where requested by client. FNSASICX503A.5 24 17

Total 293 205

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Provide advice in Life Insurance

FNSASICX503A

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

Keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via support@mentoreducation.com.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element.

If you do not achieve this, you will receive feedback via your email address and be asked

to resubmit your assessment for a second marking.

Assignments will not be returned to you.

Task Assessments Elements Target

Mark

Pass

Mark

Actual

Mark

1 Establish relationship with client and identify client’s objectives,

needs and financial situation. FNSASICX503A.1 79 55

2 Analyse client’s objectives, needs, financial situation and risk

profile to develop appropriate strategies and solutions. FNSASICX503A.2 100 70

3 Present appropriate strategies and solutions to client and

negotiate a financial plan, policy or transaction. FNSASICX503A.3 58 41

4 Agree the plan, policy or transaction and complete

documentation FNSASICX503A.4 32 22

5 Provide ongoing service where requested by client. FNSASICX503A.5 24 17

Total 293 205

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insurance 2 of 36

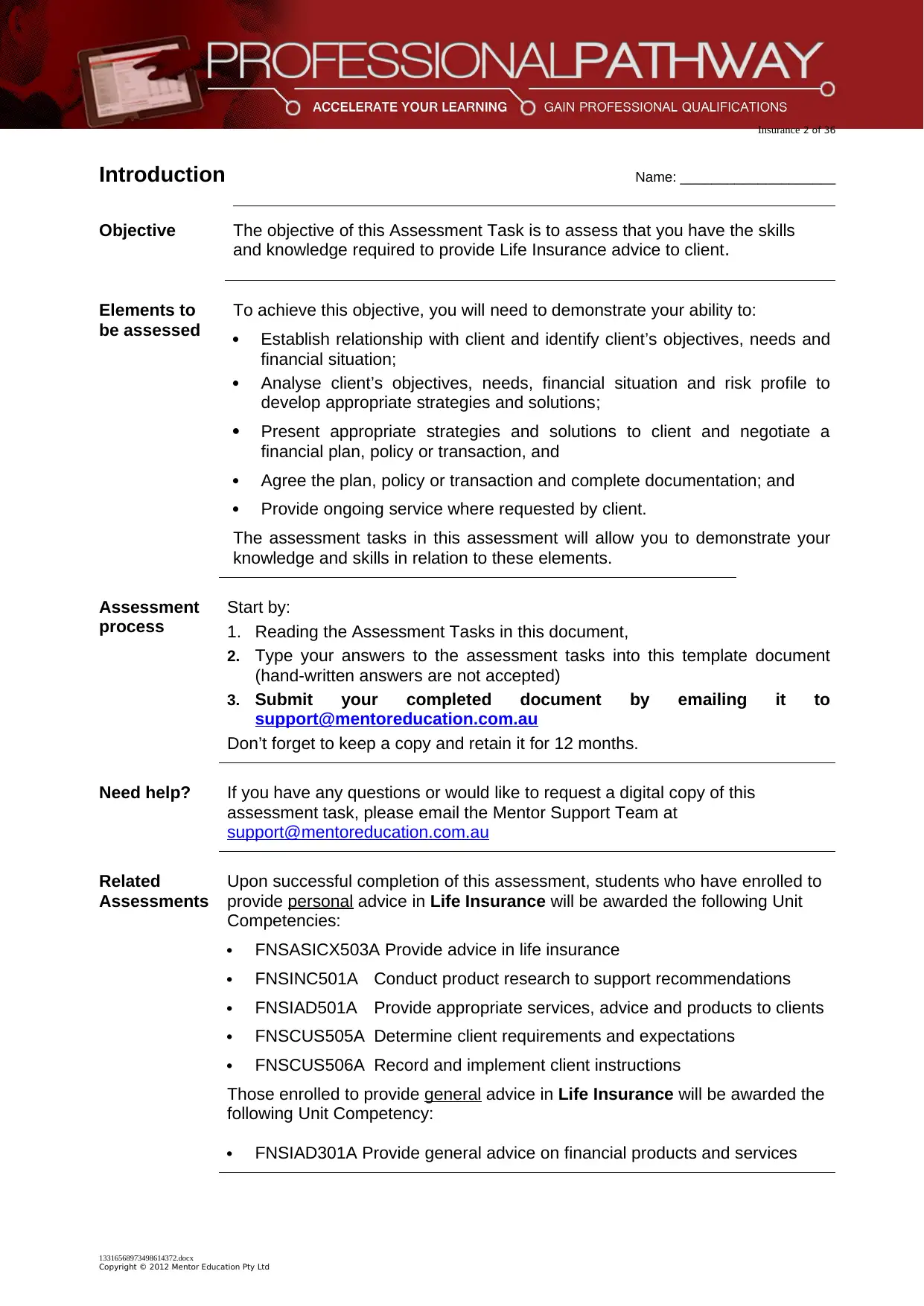

Introduction Name: ____________________

Objective The objective of this Assessment Task is to assess that you have the skills

and knowledge required to provide Life Insurance advice to client.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

Establish relationship with client and identify client’s objectives, needs and

financial situation;

Analyse client’s objectives, needs, financial situation and risk profile to

develop appropriate strategies and solutions;

Present appropriate strategies and solutions to client and negotiate a

financial plan, policy or transaction, and

Agree the plan, policy or transaction and complete documentation; and

Provide ongoing service where requested by client.

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Tasks in this document,

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by emailing it to

support@mentoreducation.com.au

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

support@mentoreducation.com.au

Related

Assessments

Upon successful completion of this assessment, students who have enrolled to

provide personal advice in Life Insurance will be awarded the following Unit

Competencies:

FNSASICX503A Provide advice in life insurance

FNSINC501A Conduct product research to support recommendations

FNSIAD501A Provide appropriate services, advice and products to clients

FNSCUS505A Determine client requirements and expectations

FNSCUS506A Record and implement client instructions

Those enrolled to provide general advice in Life Insurance will be awarded the

following Unit Competency:

FNSIAD301A Provide general advice on financial products and services

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Introduction Name: ____________________

Objective The objective of this Assessment Task is to assess that you have the skills

and knowledge required to provide Life Insurance advice to client.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

Establish relationship with client and identify client’s objectives, needs and

financial situation;

Analyse client’s objectives, needs, financial situation and risk profile to

develop appropriate strategies and solutions;

Present appropriate strategies and solutions to client and negotiate a

financial plan, policy or transaction, and

Agree the plan, policy or transaction and complete documentation; and

Provide ongoing service where requested by client.

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Tasks in this document,

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by emailing it to

support@mentoreducation.com.au

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

support@mentoreducation.com.au

Related

Assessments

Upon successful completion of this assessment, students who have enrolled to

provide personal advice in Life Insurance will be awarded the following Unit

Competencies:

FNSASICX503A Provide advice in life insurance

FNSINC501A Conduct product research to support recommendations

FNSIAD501A Provide appropriate services, advice and products to clients

FNSCUS505A Determine client requirements and expectations

FNSCUS506A Record and implement client instructions

Those enrolled to provide general advice in Life Insurance will be awarded the

following Unit Competency:

FNSIAD301A Provide general advice on financial products and services

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Insurance 3 of 36

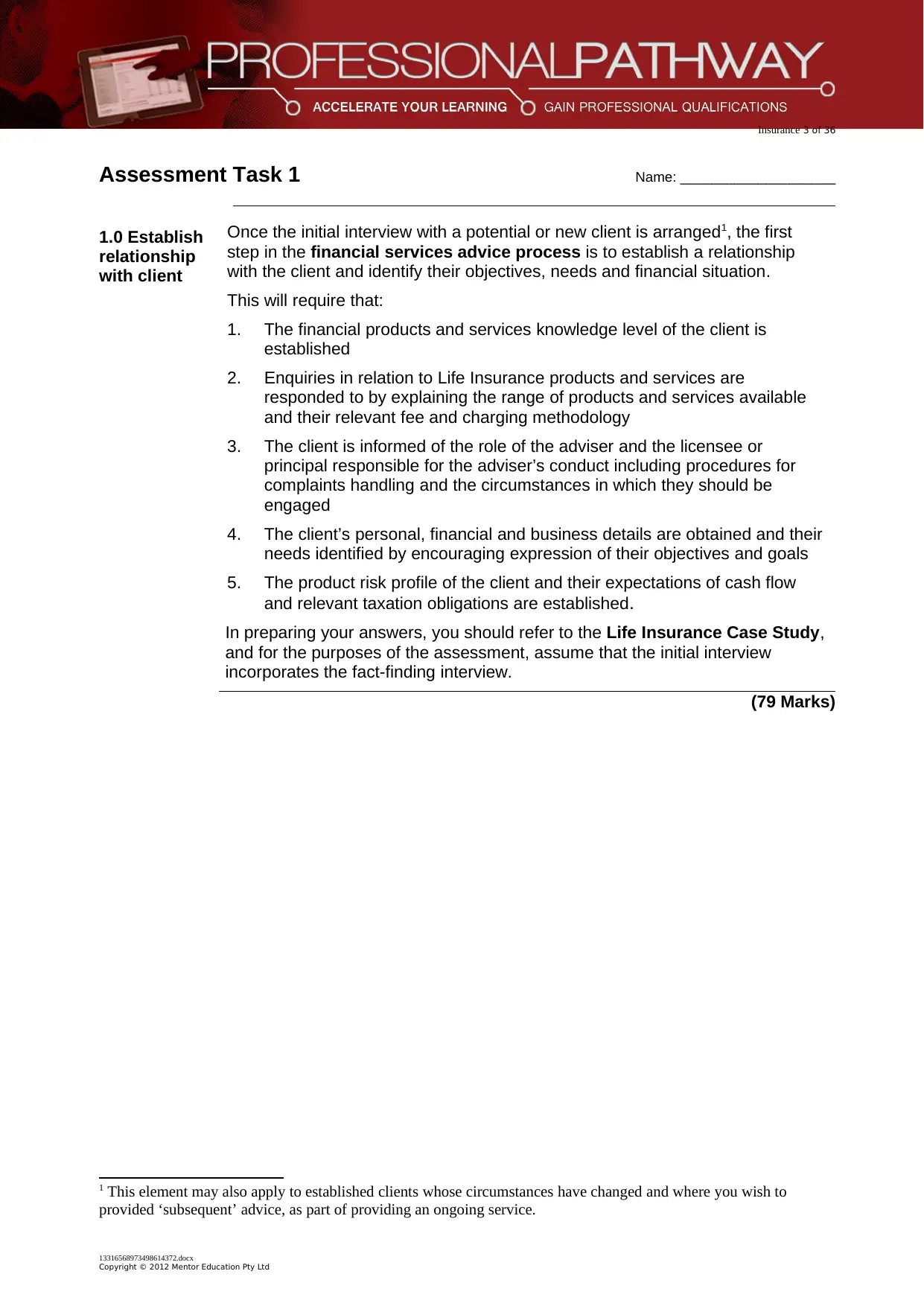

Assessment Task 1 Name: ____________________

1.0 Establish

relationship

with client

FNSASICX503A.1

Once the initial interview with a potential or new client is arranged1, the first

step in the financial services advice process is to establish a relationship

with the client and identify their objectives, needs and financial situation.

This will require that:

1. The financial products and services knowledge level of the client is

established

2. Enquiries in relation to Life Insurance products and services are

responded to by explaining the range of products and services available

and their relevant fee and charging methodology

3. The client is informed of the role of the adviser and the licensee or

principal responsible for the adviser’s conduct including procedures for

complaints handling and the circumstances in which they should be

engaged

4. The client’s personal, financial and business details are obtained and their

needs identified by encouraging expression of their objectives and goals

5. The product risk profile of the client and their expectations of cash flow

and relevant taxation obligations are established.

In preparing your answers, you should refer to the Life Insurance Case Study,

and for the purposes of the assessment, assume that the initial interview

incorporates the fact-finding interview.

(79 Marks)

1 This element may also apply to established clients whose circumstances have changed and where you wish to

provided ‘subsequent’ advice, as part of providing an ongoing service.

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1 Name: ____________________

1.0 Establish

relationship

with client

FNSASICX503A.1

Once the initial interview with a potential or new client is arranged1, the first

step in the financial services advice process is to establish a relationship

with the client and identify their objectives, needs and financial situation.

This will require that:

1. The financial products and services knowledge level of the client is

established

2. Enquiries in relation to Life Insurance products and services are

responded to by explaining the range of products and services available

and their relevant fee and charging methodology

3. The client is informed of the role of the adviser and the licensee or

principal responsible for the adviser’s conduct including procedures for

complaints handling and the circumstances in which they should be

engaged

4. The client’s personal, financial and business details are obtained and their

needs identified by encouraging expression of their objectives and goals

5. The product risk profile of the client and their expectations of cash flow

and relevant taxation obligations are established.

In preparing your answers, you should refer to the Life Insurance Case Study,

and for the purposes of the assessment, assume that the initial interview

incorporates the fact-finding interview.

(79 Marks)

1 This element may also apply to established clients whose circumstances have changed and where you wish to

provided ‘subsequent’ advice, as part of providing an ongoing service.

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insurance 4 of 36

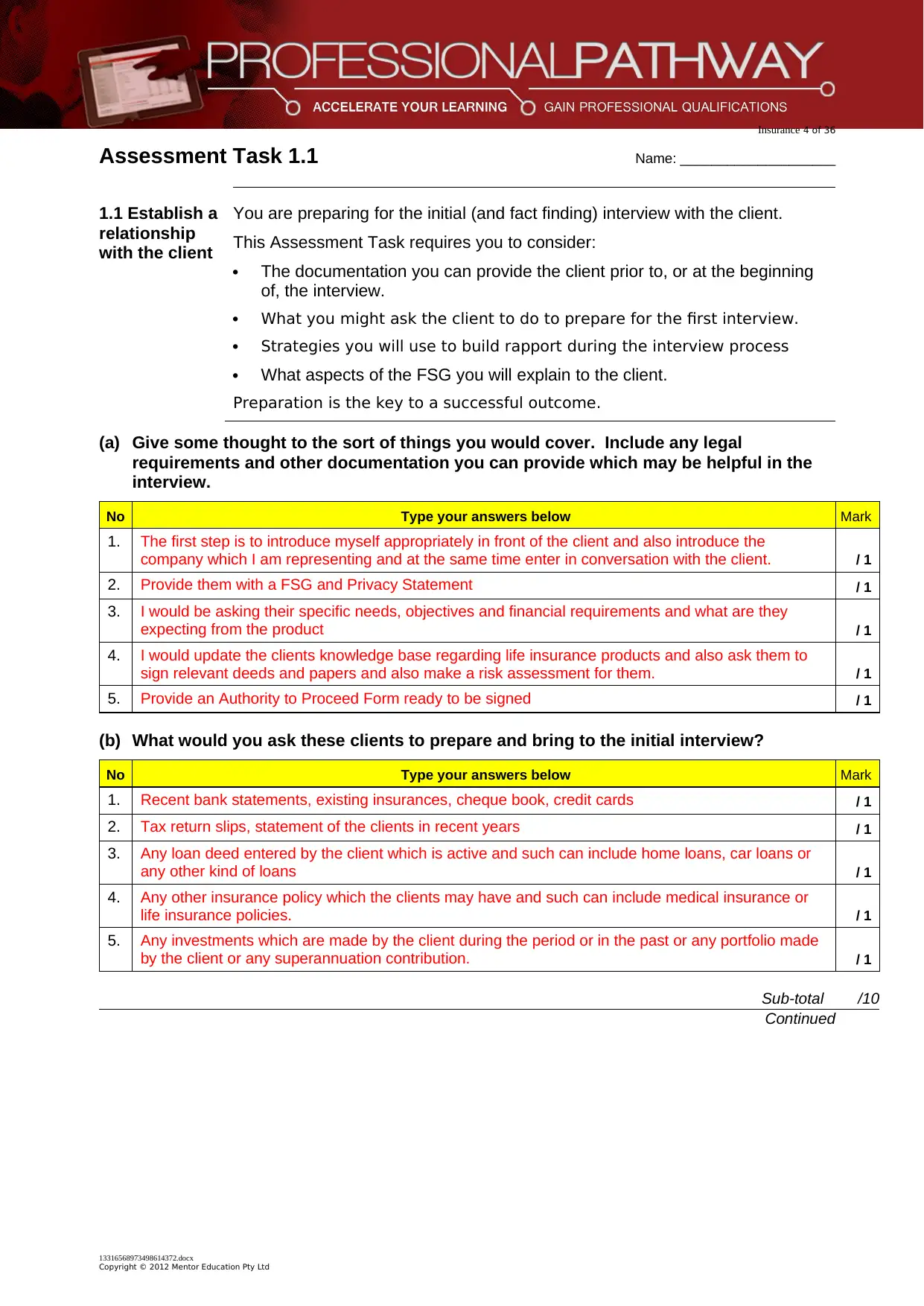

Assessment Task 1.1 Name: ____________________

1.1 Establish a

relationship

with the client

FNSASICX503A.1.1

FNSASICX503A.1.2

FNSASICX503A.1.3

You are preparing for the initial (and fact finding) interview with the client.

This Assessment Task requires you to consider:

The documentation you can provide the client prior to, or at the beginning

of, the interview.

What you might ask the client to do to prepare for the first interview.

Strategies you will use to build rapport during the interview process

What aspects of the FSG you will explain to the client.

Preparation is the key to a successful outcome.

(a) Give some thought to the sort of things you would cover. Include any legal

requirements and other documentation you can provide which may be helpful in the

interview.

No Type your answers below Mark

1. The first step is to introduce myself appropriately in front of the client and also introduce the

company which I am representing and at the same time enter in conversation with the client. / 1

2. Provide them with a FSG and Privacy Statement / 1

3. I would be asking their specific needs, objectives and financial requirements and what are they

expecting from the product / 1

4. I would update the clients knowledge base regarding life insurance products and also ask them to

sign relevant deeds and papers and also make a risk assessment for them. / 1

5. Provide an Authority to Proceed Form ready to be signed / 1

(b) What would you ask these clients to prepare and bring to the initial interview?

No Type your answers below Mark

1. Recent bank statements, existing insurances, cheque book, credit cards / 1

2. Tax return slips, statement of the clients in recent years / 1

3. Any loan deed entered by the client which is active and such can include home loans, car loans or

any other kind of loans / 1

4. Any other insurance policy which the clients may have and such can include medical insurance or

life insurance policies. / 1

5. Any investments which are made by the client during the period or in the past or any portfolio made

by the client or any superannuation contribution. / 1

Sub-total /10

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.1 Name: ____________________

1.1 Establish a

relationship

with the client

FNSASICX503A.1.1

FNSASICX503A.1.2

FNSASICX503A.1.3

You are preparing for the initial (and fact finding) interview with the client.

This Assessment Task requires you to consider:

The documentation you can provide the client prior to, or at the beginning

of, the interview.

What you might ask the client to do to prepare for the first interview.

Strategies you will use to build rapport during the interview process

What aspects of the FSG you will explain to the client.

Preparation is the key to a successful outcome.

(a) Give some thought to the sort of things you would cover. Include any legal

requirements and other documentation you can provide which may be helpful in the

interview.

No Type your answers below Mark

1. The first step is to introduce myself appropriately in front of the client and also introduce the

company which I am representing and at the same time enter in conversation with the client. / 1

2. Provide them with a FSG and Privacy Statement / 1

3. I would be asking their specific needs, objectives and financial requirements and what are they

expecting from the product / 1

4. I would update the clients knowledge base regarding life insurance products and also ask them to

sign relevant deeds and papers and also make a risk assessment for them. / 1

5. Provide an Authority to Proceed Form ready to be signed / 1

(b) What would you ask these clients to prepare and bring to the initial interview?

No Type your answers below Mark

1. Recent bank statements, existing insurances, cheque book, credit cards / 1

2. Tax return slips, statement of the clients in recent years / 1

3. Any loan deed entered by the client which is active and such can include home loans, car loans or

any other kind of loans / 1

4. Any other insurance policy which the clients may have and such can include medical insurance or

life insurance policies. / 1

5. Any investments which are made by the client during the period or in the past or any portfolio made

by the client or any superannuation contribution. / 1

Sub-total /10

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insurance 5 of 36

Assessment Task 1.1, continued Name: ____________________

(c) To establish a relationship with the client, what strategies or approaches might you

use to build rapport and trust during the interview process?

No Type your answers below Mark

1. The questions asked would be informal in nature and the same can be associated with the work,

personal life of the client. / 1

2. Ask about the hobbies of the client and bring out a common interest point which can be sports, book

reading, boating or adventure. / 1

3. Ask the client about his future endeavors and provide a positive view of the plan and if possible,

make certain suggestions to further improve the scope of the plan. / 1

4. Assure the client that the company I have dealt with such a situation in the past and have helped out

many clients and would do so for the present client as well / 1

5. Listen carefully to what are the issues, concerns and expectation of the clients and address every

feedback appropriately for the client. / 1

(d) What are the four points you must cover when presenting an FSG?

FNSASICX503A.1.1

No Type your answers below Mark

1. Make an introduction to the product or services of dealer group along with their attributes to the

clients. / 1

2. Explain all fees and charges, particularly any commissions or any other benefits that I might receive

from product suppliers / 1

3. Explain any relationships that might influence the range of products and services being provided,

e.g. links with profit providers. / 1

4. Explain the process about customer complaint resolutions and give them contact details for the

ombudsman / 1

(e) What types of personal insurance strategies/products do you expect to provide advice

on?

FNSASICX503A.1.2

No Type your answers below Mark

1. Income Protection / 1

2. Trauma / 1

3. Life Insurance / 1

4. Total Permanent Disability / 1

Sub-total /13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.1, continued Name: ____________________

(c) To establish a relationship with the client, what strategies or approaches might you

use to build rapport and trust during the interview process?

No Type your answers below Mark

1. The questions asked would be informal in nature and the same can be associated with the work,

personal life of the client. / 1

2. Ask about the hobbies of the client and bring out a common interest point which can be sports, book

reading, boating or adventure. / 1

3. Ask the client about his future endeavors and provide a positive view of the plan and if possible,

make certain suggestions to further improve the scope of the plan. / 1

4. Assure the client that the company I have dealt with such a situation in the past and have helped out

many clients and would do so for the present client as well / 1

5. Listen carefully to what are the issues, concerns and expectation of the clients and address every

feedback appropriately for the client. / 1

(d) What are the four points you must cover when presenting an FSG?

FNSASICX503A.1.1

No Type your answers below Mark

1. Make an introduction to the product or services of dealer group along with their attributes to the

clients. / 1

2. Explain all fees and charges, particularly any commissions or any other benefits that I might receive

from product suppliers / 1

3. Explain any relationships that might influence the range of products and services being provided,

e.g. links with profit providers. / 1

4. Explain the process about customer complaint resolutions and give them contact details for the

ombudsman / 1

(e) What types of personal insurance strategies/products do you expect to provide advice

on?

FNSASICX503A.1.2

No Type your answers below Mark

1. Income Protection / 1

2. Trauma / 1

3. Life Insurance / 1

4. Total Permanent Disability / 1

Sub-total /13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Insurance 6 of 36

Assessment Task 1.1, continued Name: ____________________

(f) What are the benefits of explaining these products and strategies to your clients?

FNSASICX503A.1.1 and 1.2 (a)

No Type your answers below Mark

1. On the basis of the objectives and goals which are set out by the client, I am able to appropriately

explain the features of the products point out how such products can lead to fulfillment of the

objectives of the client. The client would be able to take his decisions appropriately due to the

discussion regarding the product. / 1

2. Due to expertise and knowledge in the field I would be able to provide the clients with appropriate

advise regarding which product would give the maximum benefits and meet the expectations of the

clients. / 1

3. This helps the client by not being overloaded with excess information and getting mixed up. / 1

(g) List the different types of fees you could charge these clients.

FNSASICX503A.1.2 (b)

No Type your answers below Mark

1. Commissions / 1

2. Hourly rate / 1

3. Referral Fees / 1

(h) What are the benefits of explaining these fees to the clients?

FNSASICX503A.1.2 (b)

No Type your answers below Mark

1. Have a clear contract and explaining the fees structure would help in building trust / 1

2. The cost element of services would become known to the client / 1

3. Client would be explained the breakup of fees charged which would ensure that there is fairness in

the approach / 1

4. Conforms with rules and regulations set under the Corporations Act Documentary Requirements,

and ASIC / 1

(i) Outline the three steps your clients should take if they have a complaint or dispute

prior to contacting the ASIC.

FNSASICX503A.1.3 (b)

No Type your answers below Mark

1. They can contact the company to make a formal complaint to the free internal disputes resolution

process / 1

2. Contact the disputes Officer / 1

3. If they are still not happy with the result within the first 45 days, they can refer it to Insurance

Ombudsman / 1

Sub-total / 13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.1, continued Name: ____________________

(f) What are the benefits of explaining these products and strategies to your clients?

FNSASICX503A.1.1 and 1.2 (a)

No Type your answers below Mark

1. On the basis of the objectives and goals which are set out by the client, I am able to appropriately

explain the features of the products point out how such products can lead to fulfillment of the

objectives of the client. The client would be able to take his decisions appropriately due to the

discussion regarding the product. / 1

2. Due to expertise and knowledge in the field I would be able to provide the clients with appropriate

advise regarding which product would give the maximum benefits and meet the expectations of the

clients. / 1

3. This helps the client by not being overloaded with excess information and getting mixed up. / 1

(g) List the different types of fees you could charge these clients.

FNSASICX503A.1.2 (b)

No Type your answers below Mark

1. Commissions / 1

2. Hourly rate / 1

3. Referral Fees / 1

(h) What are the benefits of explaining these fees to the clients?

FNSASICX503A.1.2 (b)

No Type your answers below Mark

1. Have a clear contract and explaining the fees structure would help in building trust / 1

2. The cost element of services would become known to the client / 1

3. Client would be explained the breakup of fees charged which would ensure that there is fairness in

the approach / 1

4. Conforms with rules and regulations set under the Corporations Act Documentary Requirements,

and ASIC / 1

(i) Outline the three steps your clients should take if they have a complaint or dispute

prior to contacting the ASIC.

FNSASICX503A.1.3 (b)

No Type your answers below Mark

1. They can contact the company to make a formal complaint to the free internal disputes resolution

process / 1

2. Contact the disputes Officer / 1

3. If they are still not happy with the result within the first 45 days, they can refer it to Insurance

Ombudsman / 1

Sub-total / 13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insurance 7 of 36

Assessment Task 1.2 Name: ____________________

1.2 Identify

your client’s

objectives,

needs and

financial

situation

FNSASICX503A.1.1

FNSASICX503A.1.4

FNSASICX503A.1.5

You can now begin identifying the clients objectives, needs and financial

situation.

This Assessment Task requires that the:

Client’s personal, financial and business details are obtained and their

needs identified by encouraging expression of their objectives and goals

Product risk profile of the client and their expectations of cash flow and

relevant taxation obligations are established.

Attention to detail, methodical enquiry and documentation are required.

(a) What techniques or tools could you use to gather information about your clients?

No Type your answers below Mark

1. Ask open ended questions Who, What ,when, where, why / 1

2. Client’s Personal details and what insurances they have in place, Mortgage, Loans, Income

inheritances, Bank Accounts. / 1

3. Bank Statements from their Business Expenses, Loans, Turn over, etc. / 1

4. Fact Find Document / 1

(b) Using the information about the client provided in the case study, answer the fact

finding questions in the table below about the client’s personal and business details.

FNSASICX503A.1.4 (a)

No Fact Finding Questions Type your answers below Mark

1. What are the clients’

names and their ages?

Bill Smith 42 Mary Smith 40

/ 1

2. What are the names and

ages of the clients’

dependants?

Harry Smith 8 Diana Smith 4

/ 1

3. What are the clients’

occupations or

employment status?

Bill is a partner in a heavy engineering business

Mary works part time as a fitness instructor.

/ 1

4. What are the clients’

career or business plans

for the future?

Bill would like to investigate ways to grow the company and increase

profits

Mary intends to return to full time employment when her daughter goes

to primary school. She will use the extra money to pay for the children’s’

private school fees for their secondary education. / 1

5. Do the clients have any

health issues? What is

their health status?

No, both are in good health

/ 1

6. Are the client’s smokers

or non-smokers?

Non Smokers

/ 1

Sub-total /10

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.2 Name: ____________________

1.2 Identify

your client’s

objectives,

needs and

financial

situation

FNSASICX503A.1.1

FNSASICX503A.1.4

FNSASICX503A.1.5

You can now begin identifying the clients objectives, needs and financial

situation.

This Assessment Task requires that the:

Client’s personal, financial and business details are obtained and their

needs identified by encouraging expression of their objectives and goals

Product risk profile of the client and their expectations of cash flow and

relevant taxation obligations are established.

Attention to detail, methodical enquiry and documentation are required.

(a) What techniques or tools could you use to gather information about your clients?

No Type your answers below Mark

1. Ask open ended questions Who, What ,when, where, why / 1

2. Client’s Personal details and what insurances they have in place, Mortgage, Loans, Income

inheritances, Bank Accounts. / 1

3. Bank Statements from their Business Expenses, Loans, Turn over, etc. / 1

4. Fact Find Document / 1

(b) Using the information about the client provided in the case study, answer the fact

finding questions in the table below about the client’s personal and business details.

FNSASICX503A.1.4 (a)

No Fact Finding Questions Type your answers below Mark

1. What are the clients’

names and their ages?

Bill Smith 42 Mary Smith 40

/ 1

2. What are the names and

ages of the clients’

dependants?

Harry Smith 8 Diana Smith 4

/ 1

3. What are the clients’

occupations or

employment status?

Bill is a partner in a heavy engineering business

Mary works part time as a fitness instructor.

/ 1

4. What are the clients’

career or business plans

for the future?

Bill would like to investigate ways to grow the company and increase

profits

Mary intends to return to full time employment when her daughter goes

to primary school. She will use the extra money to pay for the children’s’

private school fees for their secondary education. / 1

5. Do the clients have any

health issues? What is

their health status?

No, both are in good health

/ 1

6. Are the client’s smokers

or non-smokers?

Non Smokers

/ 1

Sub-total /10

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insurance 8 of 36

Assessment Task 1.2 Name: ____________________

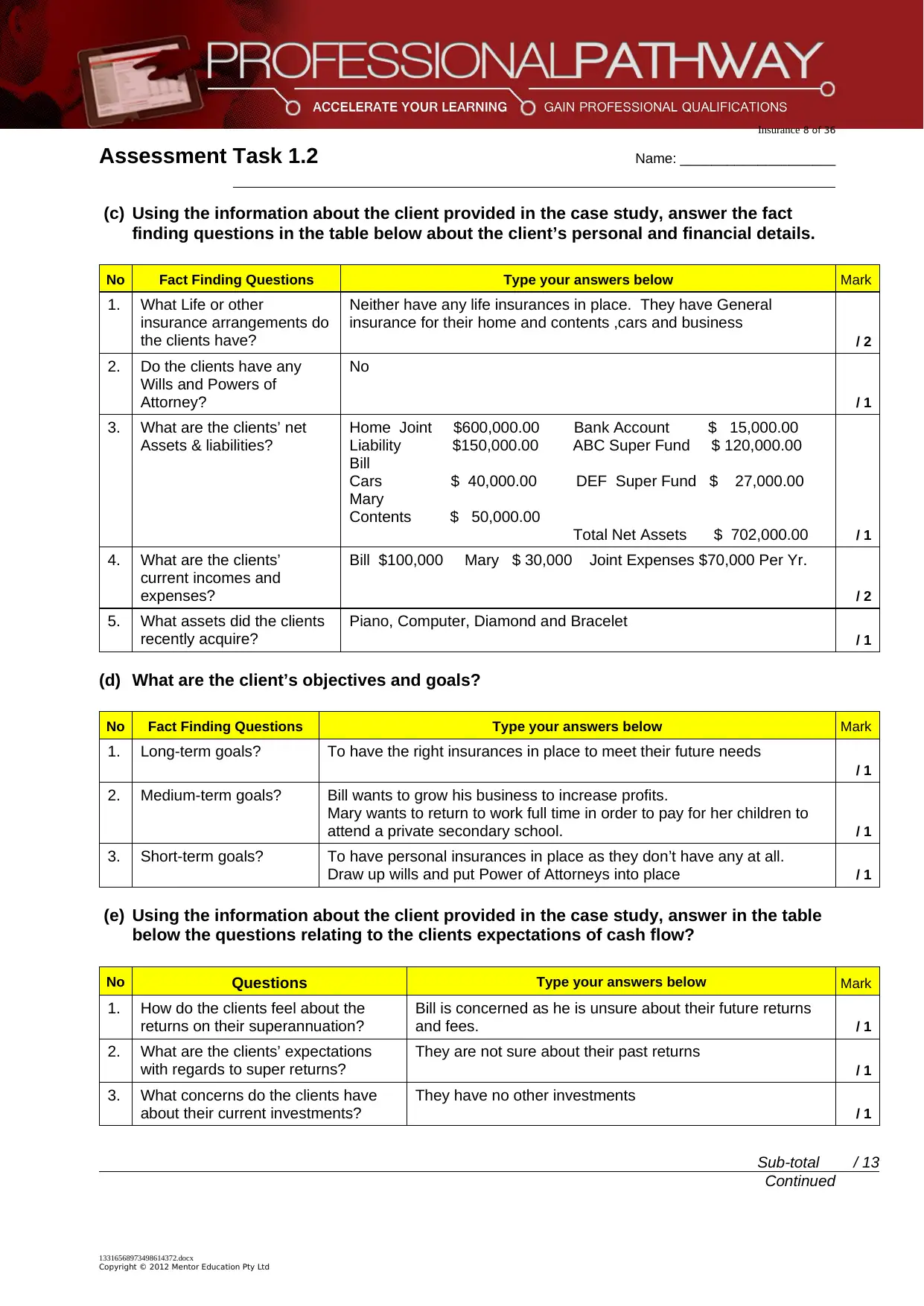

(c) Using the information about the client provided in the case study, answer the fact

finding questions in the table below about the client’s personal and financial details.

FNSASICX503A.1.4 (a)

No Fact Finding Questions Type your answers below Mark

1. What Life or other

insurance arrangements do

the clients have?

Neither have any life insurances in place. They have General

insurance for their home and contents ,cars and business

/ 2

2. Do the clients have any

Wills and Powers of

Attorney?

No

/ 1

3. What are the clients’ net

Assets & liabilities?

Home Joint $600,000.00 Bank Account $ 15,000.00

Liability $150,000.00 ABC Super Fund $ 120,000.00

Bill

Cars $ 40,000.00 DEF Super Fund $ 27,000.00

Mary

Contents $ 50,000.00

Total Net Assets $ 702,000.00 / 1

4. What are the clients’

current incomes and

expenses?

Bill $100,000 Mary $ 30,000 Joint Expenses $70,000 Per Yr.

/ 2

5. What assets did the clients

recently acquire?

Piano, Computer, Diamond and Bracelet

/ 1

(d) What are the client’s objectives and goals?

FNSASICX503A.1.4 (b)

No Fact Finding Questions Type your answers below Mark

1. Long-term goals? To have the right insurances in place to meet their future needs

/ 1

2. Medium-term goals? Bill wants to grow his business to increase profits.

Mary wants to return to work full time in order to pay for her children to

attend a private secondary school. / 1

3. Short-term goals? To have personal insurances in place as they don’t have any at all.

Draw up wills and put Power of Attorneys into place / 1

(e) Using the information about the client provided in the case study, answer in the table

below the questions relating to the clients expectations of cash flow?

FNSASICX503A.1.5

No Questions Type your answers below Mark

1. How do the clients feel about the

returns on their superannuation?

Bill is concerned as he is unsure about their future returns

and fees. / 1

2. What are the clients’ expectations

with regards to super returns?

They are not sure about their past returns

/ 1

3. What concerns do the clients have

about their current investments?

They have no other investments

/ 1

Sub-total / 13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.2 Name: ____________________

(c) Using the information about the client provided in the case study, answer the fact

finding questions in the table below about the client’s personal and financial details.

FNSASICX503A.1.4 (a)

No Fact Finding Questions Type your answers below Mark

1. What Life or other

insurance arrangements do

the clients have?

Neither have any life insurances in place. They have General

insurance for their home and contents ,cars and business

/ 2

2. Do the clients have any

Wills and Powers of

Attorney?

No

/ 1

3. What are the clients’ net

Assets & liabilities?

Home Joint $600,000.00 Bank Account $ 15,000.00

Liability $150,000.00 ABC Super Fund $ 120,000.00

Bill

Cars $ 40,000.00 DEF Super Fund $ 27,000.00

Mary

Contents $ 50,000.00

Total Net Assets $ 702,000.00 / 1

4. What are the clients’

current incomes and

expenses?

Bill $100,000 Mary $ 30,000 Joint Expenses $70,000 Per Yr.

/ 2

5. What assets did the clients

recently acquire?

Piano, Computer, Diamond and Bracelet

/ 1

(d) What are the client’s objectives and goals?

FNSASICX503A.1.4 (b)

No Fact Finding Questions Type your answers below Mark

1. Long-term goals? To have the right insurances in place to meet their future needs

/ 1

2. Medium-term goals? Bill wants to grow his business to increase profits.

Mary wants to return to work full time in order to pay for her children to

attend a private secondary school. / 1

3. Short-term goals? To have personal insurances in place as they don’t have any at all.

Draw up wills and put Power of Attorneys into place / 1

(e) Using the information about the client provided in the case study, answer in the table

below the questions relating to the clients expectations of cash flow?

FNSASICX503A.1.5

No Questions Type your answers below Mark

1. How do the clients feel about the

returns on their superannuation?

Bill is concerned as he is unsure about their future returns

and fees. / 1

2. What are the clients’ expectations

with regards to super returns?

They are not sure about their past returns

/ 1

3. What concerns do the clients have

about their current investments?

They have no other investments

/ 1

Sub-total / 13

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Insurance 9 of 36

Assessment Task 1.2, continued Name: ____________________

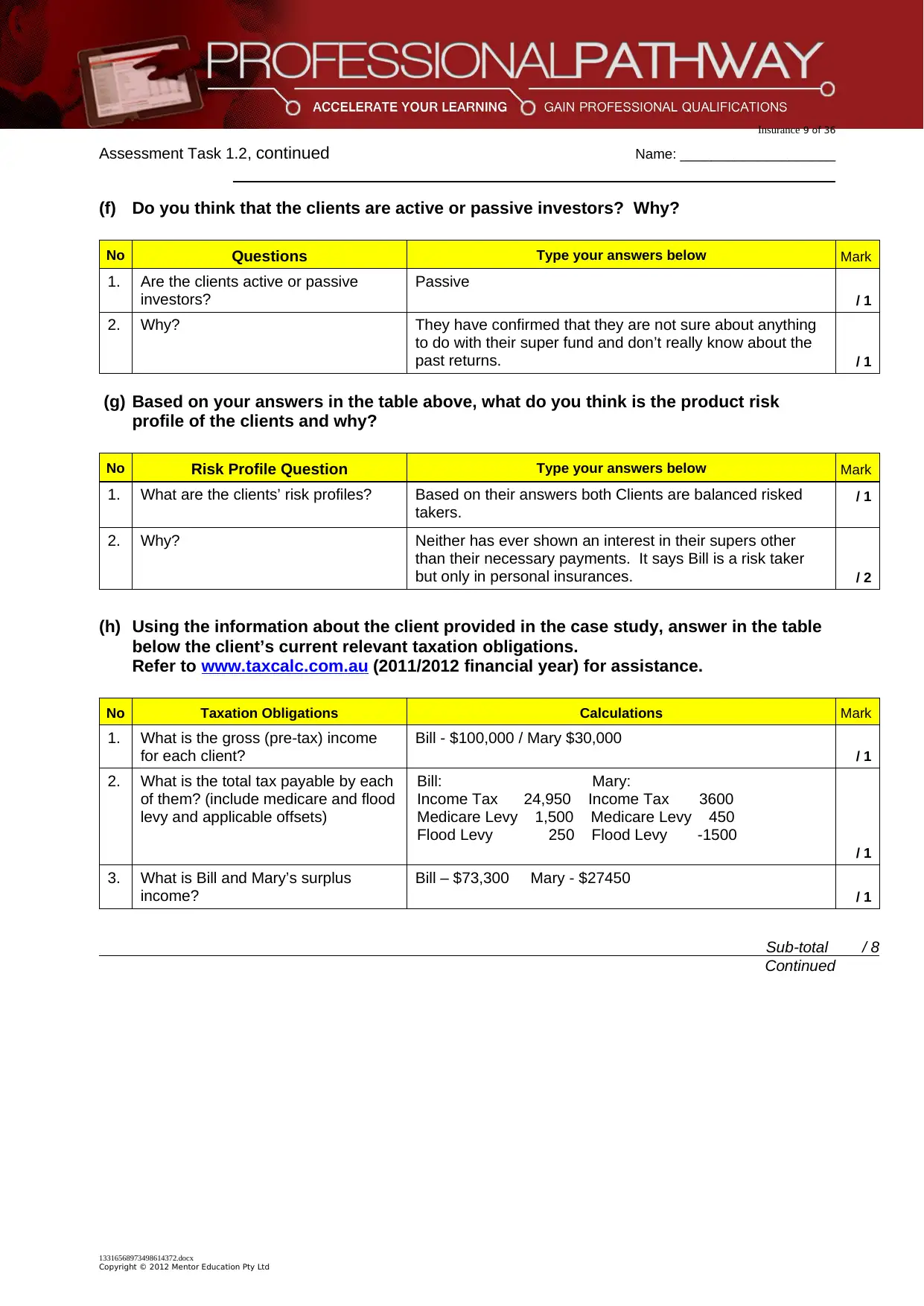

(f) Do you think that the clients are active or passive investors? Why?

FNSASICX503A.1.5 (i) (a)

No Questions Type your answers below Mark

1. Are the clients active or passive

investors?

Passive

/ 1

2. Why? They have confirmed that they are not sure about anything

to do with their super fund and don’t really know about the

past returns. / 1

(g) Based on your answers in the table above, what do you think is the product risk

profile of the clients and why?

FNSASICX503A.1.5 (ii) (b)

No Risk Profile Question Type your answers below Mark

1. What are the clients’ risk profiles? Based on their answers both Clients are balanced risked

takers.

/ 1

2. Why? Neither has ever shown an interest in their supers other

than their necessary payments. It says Bill is a risk taker

but only in personal insurances. / 2

(h) Using the information about the client provided in the case study, answer in the table

below the client’s current relevant taxation obligations.

Refer to www.taxcalc.com.au (2011/2012 financial year) for assistance.

FNSASICX503A.1.4 (f)

No Taxation Obligations Calculations Mark

1. What is the gross (pre-tax) income

for each client?

Bill - $100,000 / Mary $30,000

/ 1

2. What is the total tax payable by each

of them? (include medicare and flood

levy and applicable offsets)

Bill: Mary:

Income Tax 24,950 Income Tax 3600

Medicare Levy 1,500 Medicare Levy 450

Flood Levy 250 Flood Levy -1500

/ 1

3. What is Bill and Mary’s surplus

income?

Bill – $73,300 Mary - $27450

/ 1

Sub-total / 8

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.2, continued Name: ____________________

(f) Do you think that the clients are active or passive investors? Why?

FNSASICX503A.1.5 (i) (a)

No Questions Type your answers below Mark

1. Are the clients active or passive

investors?

Passive

/ 1

2. Why? They have confirmed that they are not sure about anything

to do with their super fund and don’t really know about the

past returns. / 1

(g) Based on your answers in the table above, what do you think is the product risk

profile of the clients and why?

FNSASICX503A.1.5 (ii) (b)

No Risk Profile Question Type your answers below Mark

1. What are the clients’ risk profiles? Based on their answers both Clients are balanced risked

takers.

/ 1

2. Why? Neither has ever shown an interest in their supers other

than their necessary payments. It says Bill is a risk taker

but only in personal insurances. / 2

(h) Using the information about the client provided in the case study, answer in the table

below the client’s current relevant taxation obligations.

Refer to www.taxcalc.com.au (2011/2012 financial year) for assistance.

FNSASICX503A.1.4 (f)

No Taxation Obligations Calculations Mark

1. What is the gross (pre-tax) income

for each client?

Bill - $100,000 / Mary $30,000

/ 1

2. What is the total tax payable by each

of them? (include medicare and flood

levy and applicable offsets)

Bill: Mary:

Income Tax 24,950 Income Tax 3600

Medicare Levy 1,500 Medicare Levy 450

Flood Levy 250 Flood Levy -1500

/ 1

3. What is Bill and Mary’s surplus

income?

Bill – $73,300 Mary - $27450

/ 1

Sub-total / 8

Continued

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insurance 10 of 36

Assessment Task 1.2, continued Name: ____________________

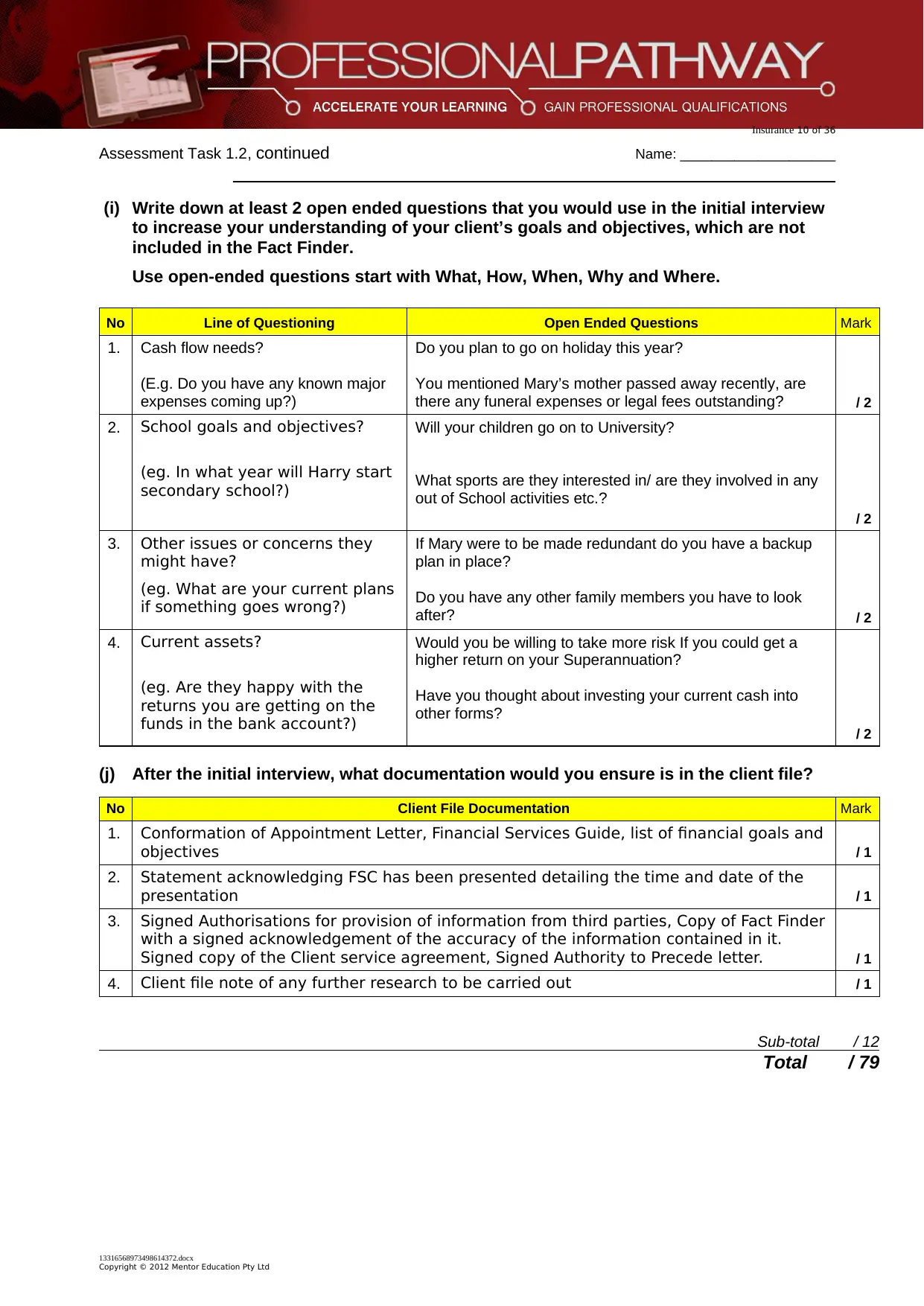

(i) Write down at least 2 open ended questions that you would use in the initial interview

to increase your understanding of your client’s goals and objectives, which are not

included in the Fact Finder.

Use open-ended questions start with What, How, When, Why and Where.

FNSASICX503A.1.5 (ii) (d)

No Line of Questioning Open Ended Questions Mark

1. Cash flow needs?

(E.g. Do you have any known major

expenses coming up?)

Do you plan to go on holiday this year?

You mentioned Mary’s mother passed away recently, are

there any funeral expenses or legal fees outstanding? / 2

2. School goals and objectives?

(eg. In what year will Harry start

secondary school?)

Will your children go on to University?

What sports are they interested in/ are they involved in any

out of School activities etc.?

/ 2

3. Other issues or concerns they

might have?

(eg. What are your current plans

if something goes wrong?)

If Mary were to be made redundant do you have a backup

plan in place?

Do you have any other family members you have to look

after? / 2

4. Current assets?

(eg. Are they happy with the

returns you are getting on the

funds in the bank account?)

Would you be willing to take more risk If you could get a

higher return on your Superannuation?

Have you thought about investing your current cash into

other forms?

/ 2

(j) After the initial interview, what documentation would you ensure is in the client file?

FNSASICX503A.1.3

No Client File Documentation Mark

1. Conformation of Appointment Letter, Financial Services Guide, list of financial goals and

objectives / 1

2. Statement acknowledging FSC has been presented detailing the time and date of the

presentation / 1

3. Signed Authorisations for provision of information from third parties, Copy of Fact Finder

with a signed acknowledgement of the accuracy of the information contained in it.

Signed copy of the Client service agreement, Signed Authority to Precede letter. / 1

4. Client file note of any further research to be carried out / 1

Sub-total / 12

Total / 79

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 1.2, continued Name: ____________________

(i) Write down at least 2 open ended questions that you would use in the initial interview

to increase your understanding of your client’s goals and objectives, which are not

included in the Fact Finder.

Use open-ended questions start with What, How, When, Why and Where.

FNSASICX503A.1.5 (ii) (d)

No Line of Questioning Open Ended Questions Mark

1. Cash flow needs?

(E.g. Do you have any known major

expenses coming up?)

Do you plan to go on holiday this year?

You mentioned Mary’s mother passed away recently, are

there any funeral expenses or legal fees outstanding? / 2

2. School goals and objectives?

(eg. In what year will Harry start

secondary school?)

Will your children go on to University?

What sports are they interested in/ are they involved in any

out of School activities etc.?

/ 2

3. Other issues or concerns they

might have?

(eg. What are your current plans

if something goes wrong?)

If Mary were to be made redundant do you have a backup

plan in place?

Do you have any other family members you have to look

after? / 2

4. Current assets?

(eg. Are they happy with the

returns you are getting on the

funds in the bank account?)

Would you be willing to take more risk If you could get a

higher return on your Superannuation?

Have you thought about investing your current cash into

other forms?

/ 2

(j) After the initial interview, what documentation would you ensure is in the client file?

FNSASICX503A.1.3

No Client File Documentation Mark

1. Conformation of Appointment Letter, Financial Services Guide, list of financial goals and

objectives / 1

2. Statement acknowledging FSC has been presented detailing the time and date of the

presentation / 1

3. Signed Authorisations for provision of information from third parties, Copy of Fact Finder

with a signed acknowledgement of the accuracy of the information contained in it.

Signed copy of the Client service agreement, Signed Authority to Precede letter. / 1

4. Client file note of any further research to be carried out / 1

Sub-total / 12

Total / 79

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insurance 11 of 36

Assessment Task 2 Name: ____________________

2.0 Analyse

client’s

objectives,

needs,

financial

situation and

risk profile to

develop

appropriate

strategies

and solutions

FNSASICX503A.2

The next step in the financial services advice process is to analyse client's

objectives, needs, financial situation and risk profile to develop appropriate

strategies and solutions.

This will require that:

1. An assessment of client’s needs is undertaken, utilising all information

gathered and taking into account client’s product expectations and specific

needs

2. Client is consulted throughout the analysis for further clarification where

necessary

3. The need for specialist advice is analysed and the client is referred to an

appropriate adviser for higher level or specialist advice if required

4. Product risk profile of the client is assessed and agreed demonstrating

understanding of the ASIC identified generic and specialist knowledge

relevant to the products being offered

5. An appropriate strategy to provide for identified needs and outcomes is

determined from analysis of products, client risk profile and assessment of

their needs

6. Relevant research, analysis and product modeling is conducted and an

appropriate solution, plan, policy or transaction drafted for presentation to

the client.

(100 Marks)

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 2 Name: ____________________

2.0 Analyse

client’s

objectives,

needs,

financial

situation and

risk profile to

develop

appropriate

strategies

and solutions

FNSASICX503A.2

The next step in the financial services advice process is to analyse client's

objectives, needs, financial situation and risk profile to develop appropriate

strategies and solutions.

This will require that:

1. An assessment of client’s needs is undertaken, utilising all information

gathered and taking into account client’s product expectations and specific

needs

2. Client is consulted throughout the analysis for further clarification where

necessary

3. The need for specialist advice is analysed and the client is referred to an

appropriate adviser for higher level or specialist advice if required

4. Product risk profile of the client is assessed and agreed demonstrating

understanding of the ASIC identified generic and specialist knowledge

relevant to the products being offered

5. An appropriate strategy to provide for identified needs and outcomes is

determined from analysis of products, client risk profile and assessment of

their needs

6. Relevant research, analysis and product modeling is conducted and an

appropriate solution, plan, policy or transaction drafted for presentation to

the client.

(100 Marks)

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Insurance 12 of 36

Assessment Task 2.1 Name: ____________________

2.1 Analyse

client

objectives,

financial

situation and

risk profile

FNSASICX503A.2.1

After the initial interview, you will conduct research to analyse the clients’

insurance needs.

Consideration needs to be given to seeking specialist advice and consulting

the client as required.

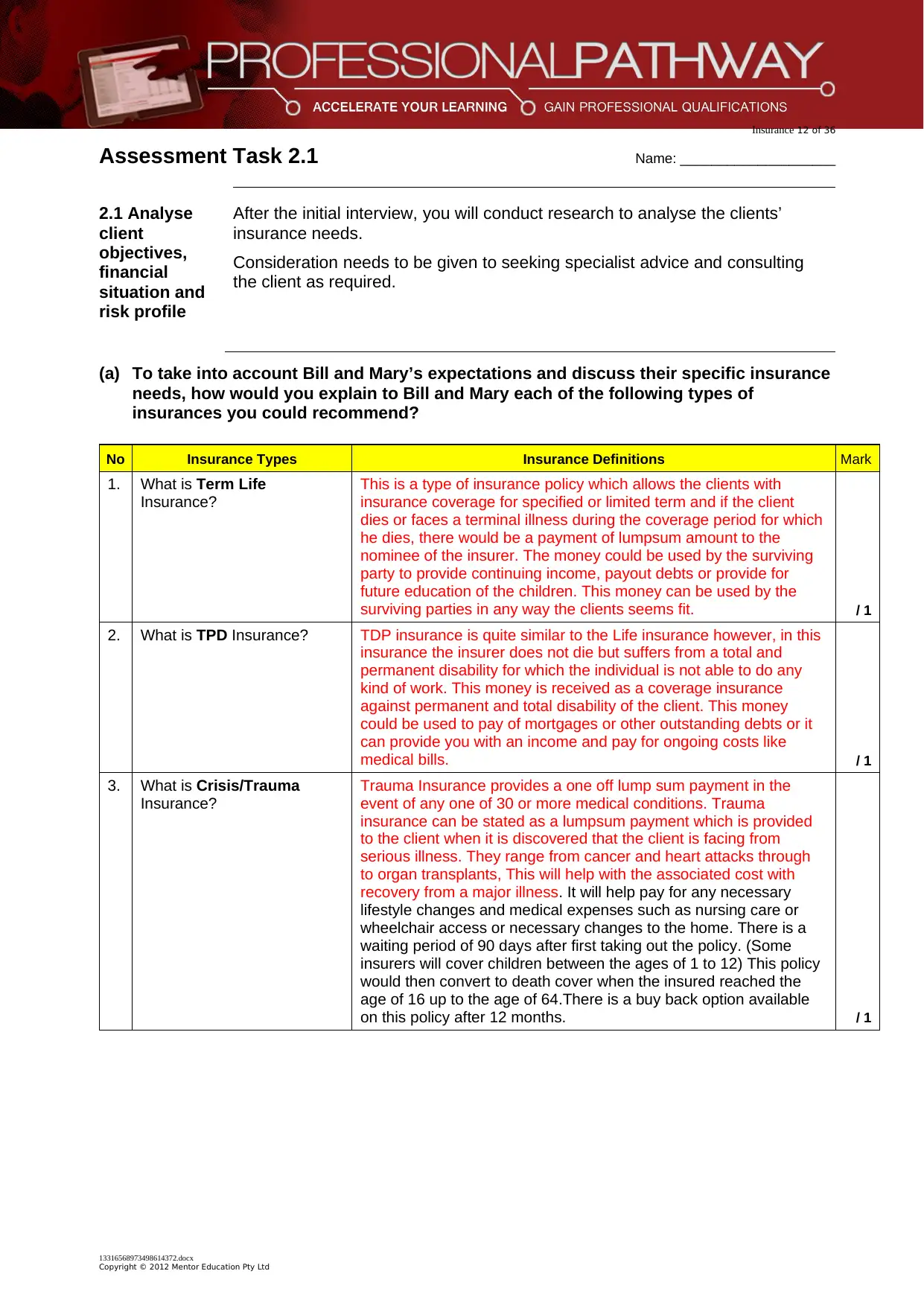

(a) To take into account Bill and Mary’s expectations and discuss their specific insurance

needs, how would you explain to Bill and Mary each of the following types of

insurances you could recommend?

FNSASICX503A.2.1 (b & c & d) and 1.5(i) (f)

No Insurance Types Insurance Definitions Mark

1. What is Term Life

Insurance?

This is a type of insurance policy which allows the clients with

insurance coverage for specified or limited term and if the client

dies or faces a terminal illness during the coverage period for which

he dies, there would be a payment of lumpsum amount to the

nominee of the insurer. The money could be used by the surviving

party to provide continuing income, payout debts or provide for

future education of the children. This money can be used by the

surviving parties in any way the clients seems fit. / 1

2. What is TPD Insurance? TDP insurance is quite similar to the Life insurance however, in this

insurance the insurer does not die but suffers from a total and

permanent disability for which the individual is not able to do any

kind of work. This money is received as a coverage insurance

against permanent and total disability of the client. This money

could be used to pay of mortgages or other outstanding debts or it

can provide you with an income and pay for ongoing costs like

medical bills. / 1

3. What is Crisis/Trauma

Insurance?

Trauma Insurance provides a one off lump sum payment in the

event of any one of 30 or more medical conditions. Trauma

insurance can be stated as a lumpsum payment which is provided

to the client when it is discovered that the client is facing from

serious illness. They range from cancer and heart attacks through

to organ transplants, This will help with the associated cost with

recovery from a major illness. It will help pay for any necessary

lifestyle changes and medical expenses such as nursing care or

wheelchair access or necessary changes to the home. There is a

waiting period of 90 days after first taking out the policy. (Some

insurers will cover children between the ages of 1 to 12) This policy

would then convert to death cover when the insured reached the

age of 16 up to the age of 64.There is a buy back option available

on this policy after 12 months. / 1

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

Assessment Task 2.1 Name: ____________________

2.1 Analyse

client

objectives,

financial

situation and

risk profile

FNSASICX503A.2.1

After the initial interview, you will conduct research to analyse the clients’

insurance needs.

Consideration needs to be given to seeking specialist advice and consulting

the client as required.

(a) To take into account Bill and Mary’s expectations and discuss their specific insurance

needs, how would you explain to Bill and Mary each of the following types of

insurances you could recommend?

FNSASICX503A.2.1 (b & c & d) and 1.5(i) (f)

No Insurance Types Insurance Definitions Mark

1. What is Term Life

Insurance?

This is a type of insurance policy which allows the clients with

insurance coverage for specified or limited term and if the client

dies or faces a terminal illness during the coverage period for which

he dies, there would be a payment of lumpsum amount to the

nominee of the insurer. The money could be used by the surviving

party to provide continuing income, payout debts or provide for

future education of the children. This money can be used by the

surviving parties in any way the clients seems fit. / 1

2. What is TPD Insurance? TDP insurance is quite similar to the Life insurance however, in this

insurance the insurer does not die but suffers from a total and

permanent disability for which the individual is not able to do any

kind of work. This money is received as a coverage insurance

against permanent and total disability of the client. This money

could be used to pay of mortgages or other outstanding debts or it

can provide you with an income and pay for ongoing costs like

medical bills. / 1

3. What is Crisis/Trauma

Insurance?

Trauma Insurance provides a one off lump sum payment in the

event of any one of 30 or more medical conditions. Trauma

insurance can be stated as a lumpsum payment which is provided

to the client when it is discovered that the client is facing from

serious illness. They range from cancer and heart attacks through

to organ transplants, This will help with the associated cost with

recovery from a major illness. It will help pay for any necessary

lifestyle changes and medical expenses such as nursing care or

wheelchair access or necessary changes to the home. There is a

waiting period of 90 days after first taking out the policy. (Some

insurers will cover children between the ages of 1 to 12) This policy

would then convert to death cover when the insured reached the

age of 16 up to the age of 64.There is a buy back option available

on this policy after 12 months. / 1

13316568973498614372.docx

Copyright © 2012 Mentor Education Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.