Comprehensive Financial Ratio Analysis and Business Performance Report

VerifiedAdded on 2022/12/28

|8

|1265

|25

Report

AI Summary

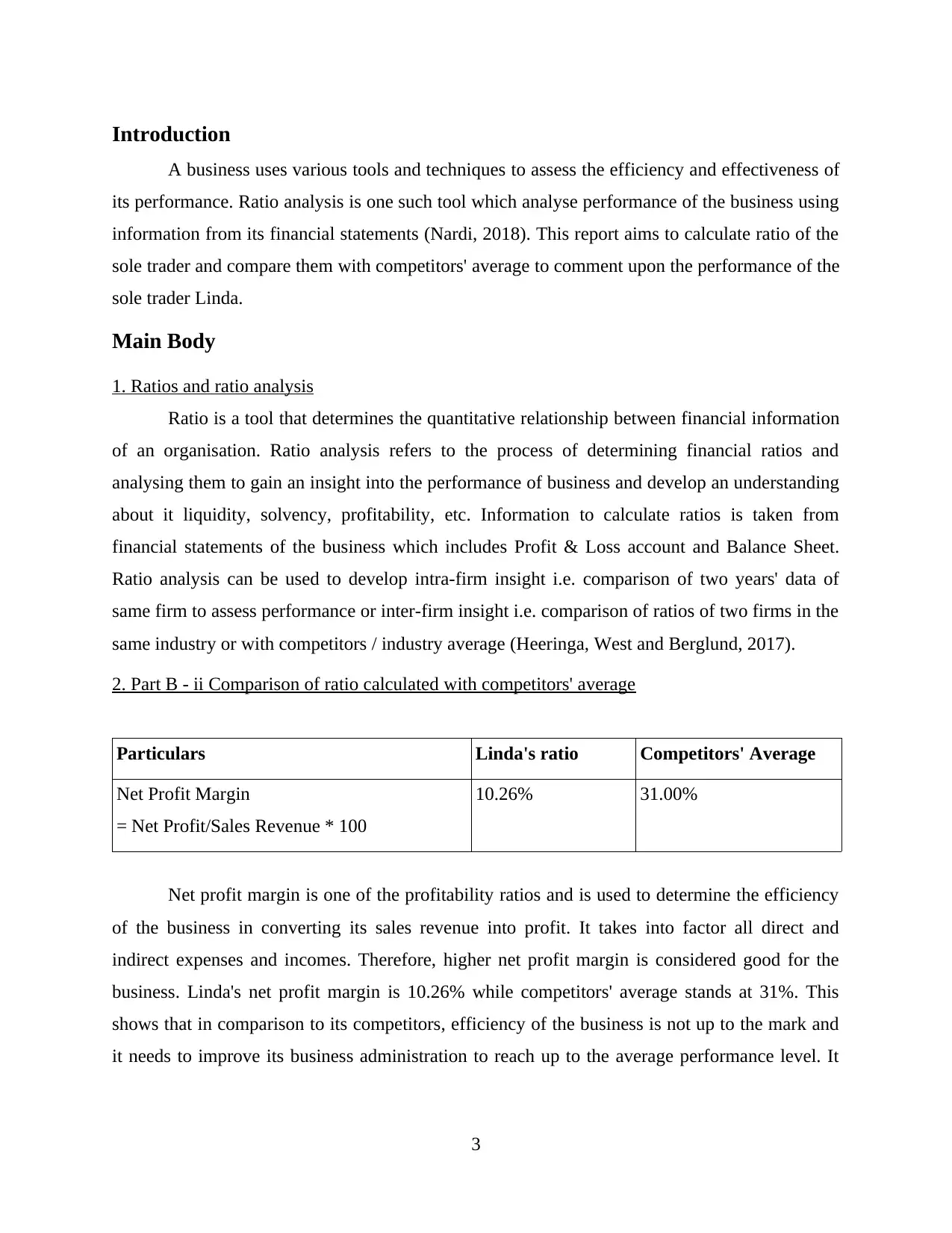

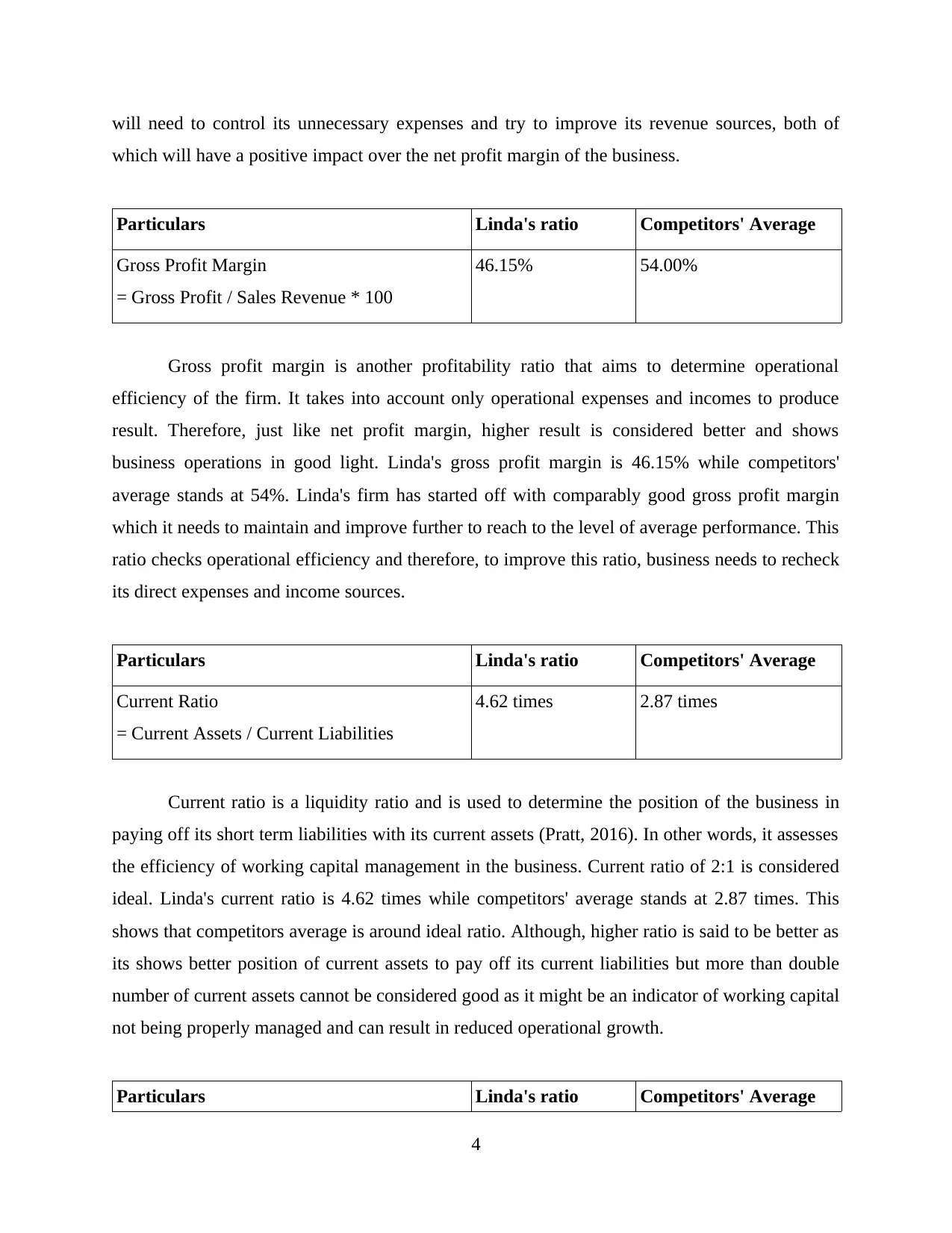

This report presents a financial ratio analysis of a sole trader named Linda, comparing her business's performance against industry averages. The analysis includes the calculation and interpretation of key financial ratios such as net profit margin, gross profit margin, current ratio, quick ratio, accounts receivables collection period, and accounts payables payment period. The report highlights Linda's strengths and weaknesses by comparing her ratios to those of her competitors. The findings indicate areas where Linda's business excels, such as accounts receivable management, and areas where improvement is needed, particularly in profitability ratios. The report concludes that ratio analysis is a valuable tool for assessing business performance, providing insights into liquidity, solvency, and profitability, and facilitating comparisons with competitors.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.