Comprehensive Financial Analysis: Linda's Toy Business Transactions

VerifiedAdded on 2022/12/29

|15

|2474

|53

Homework Assignment

AI Summary

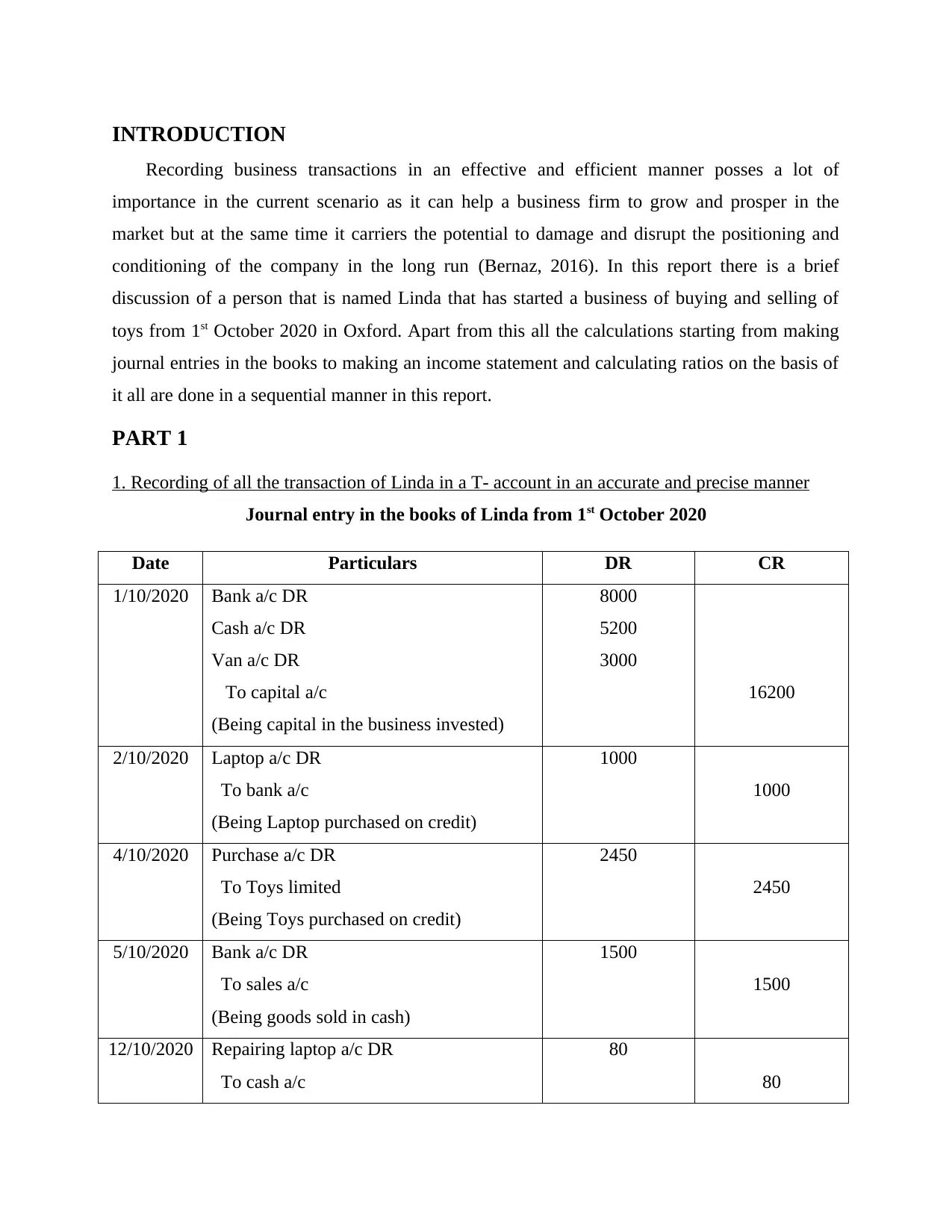

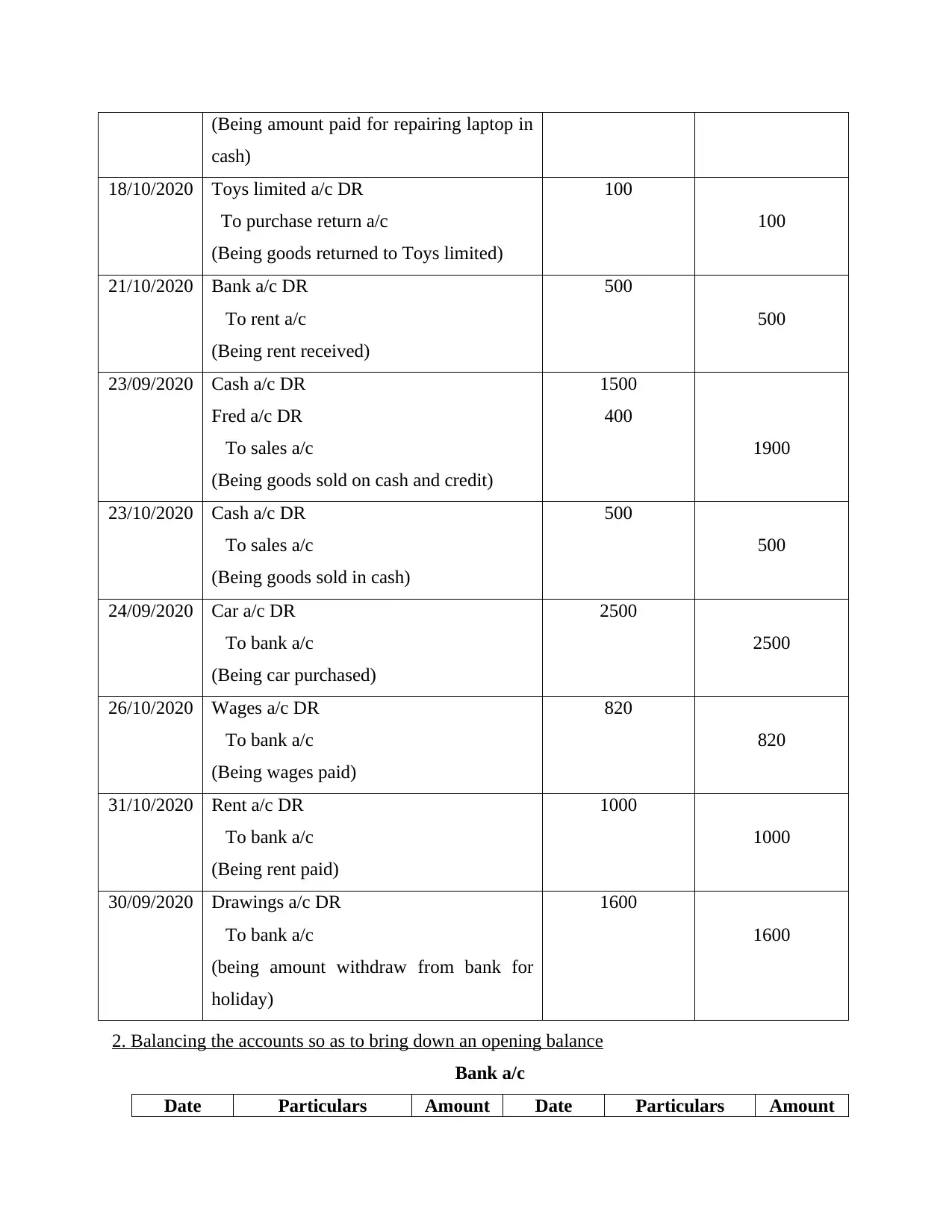

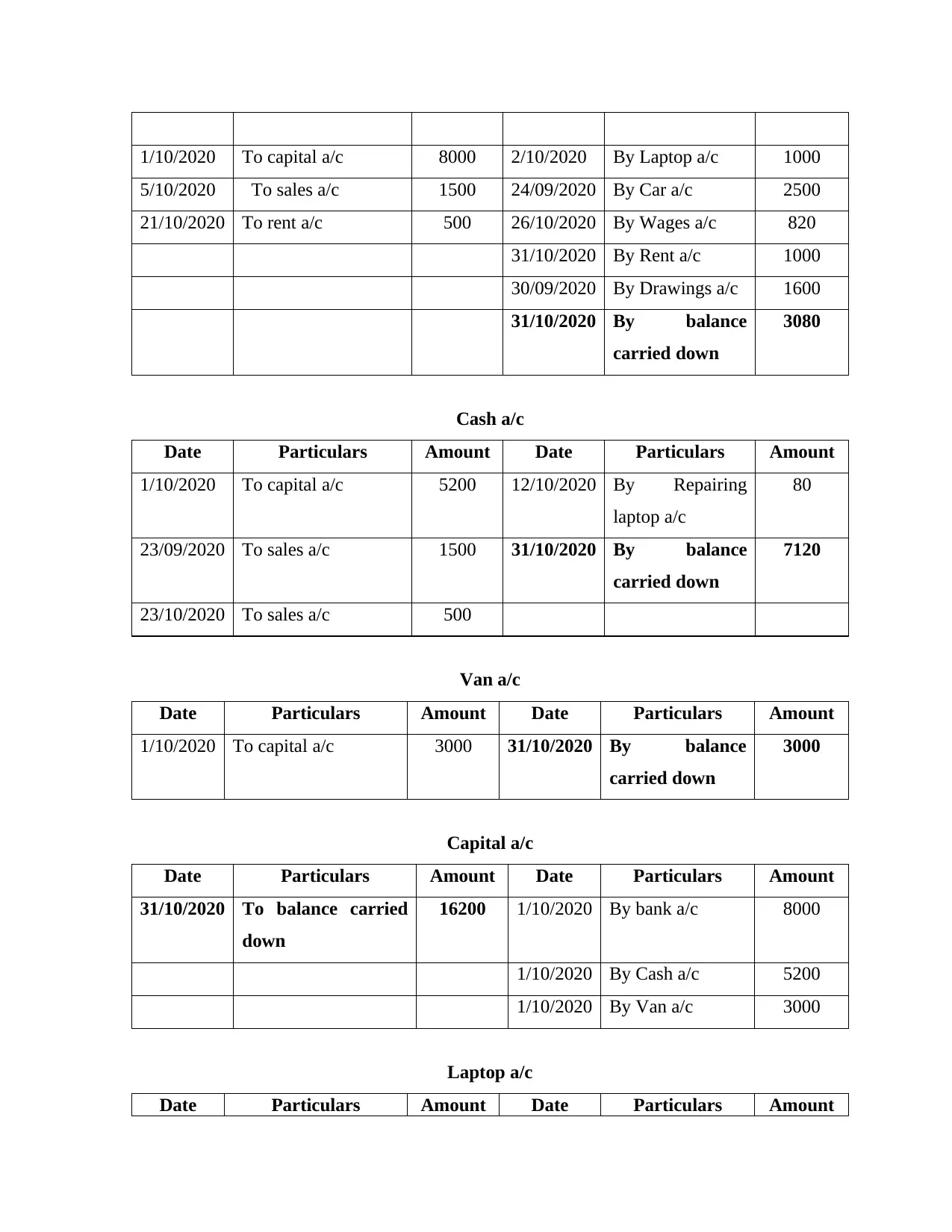

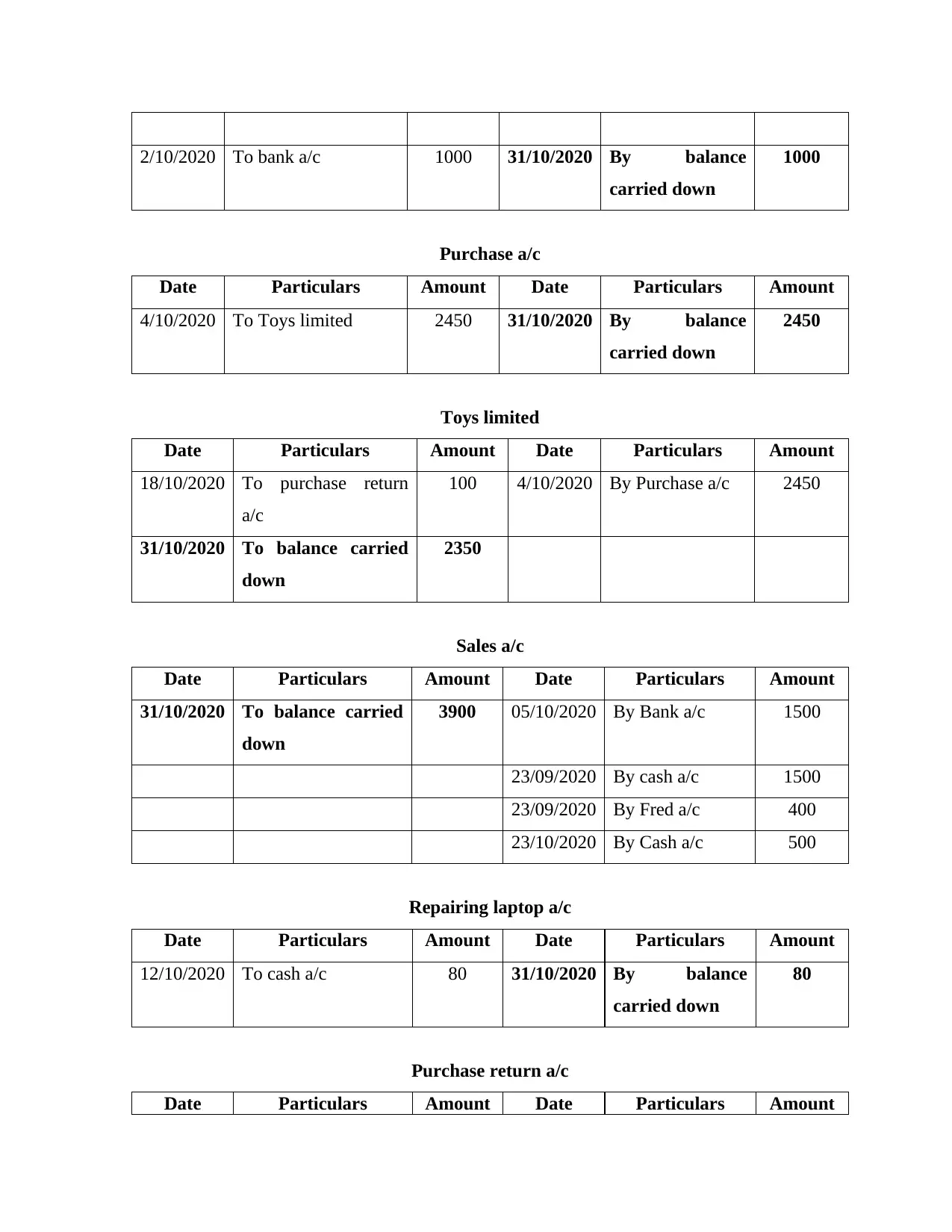

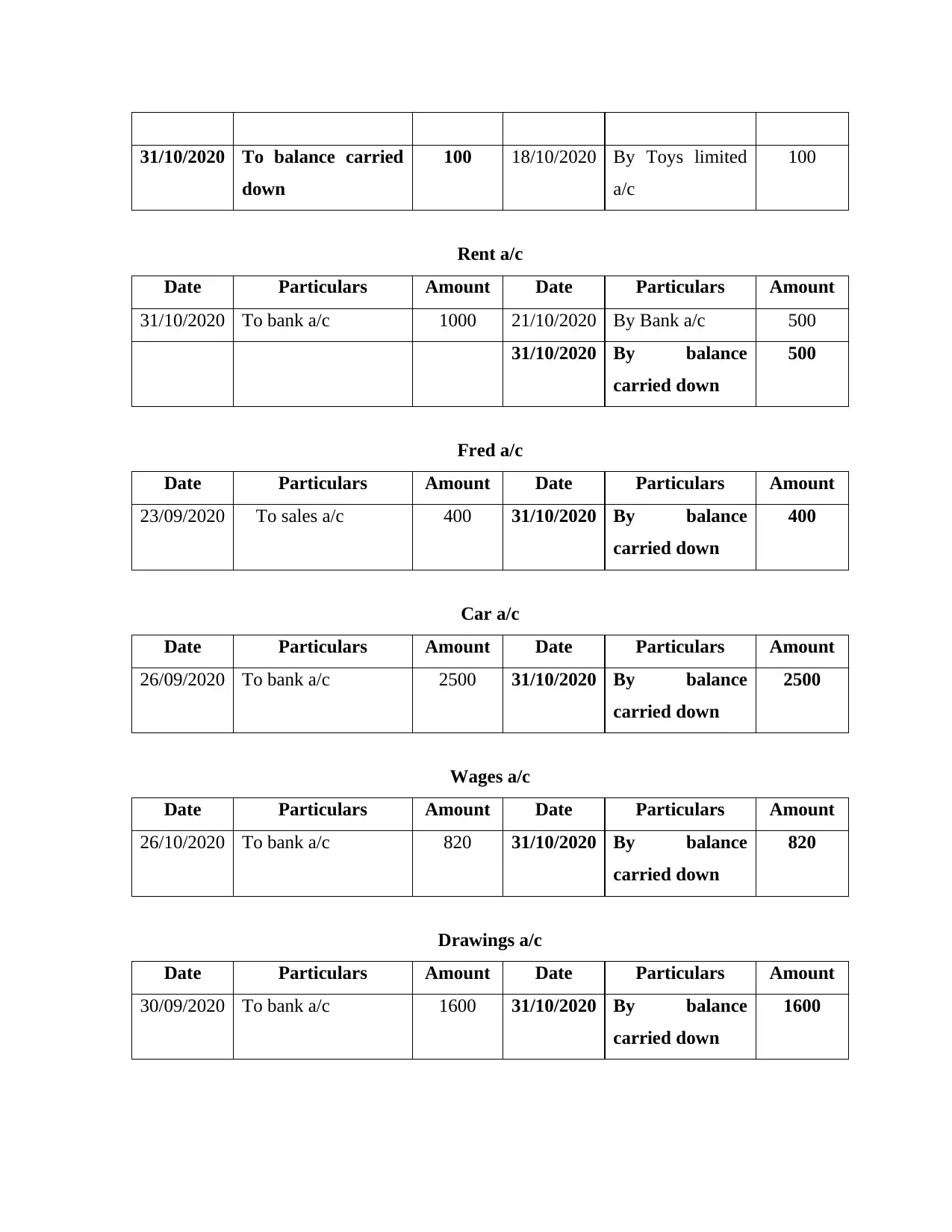

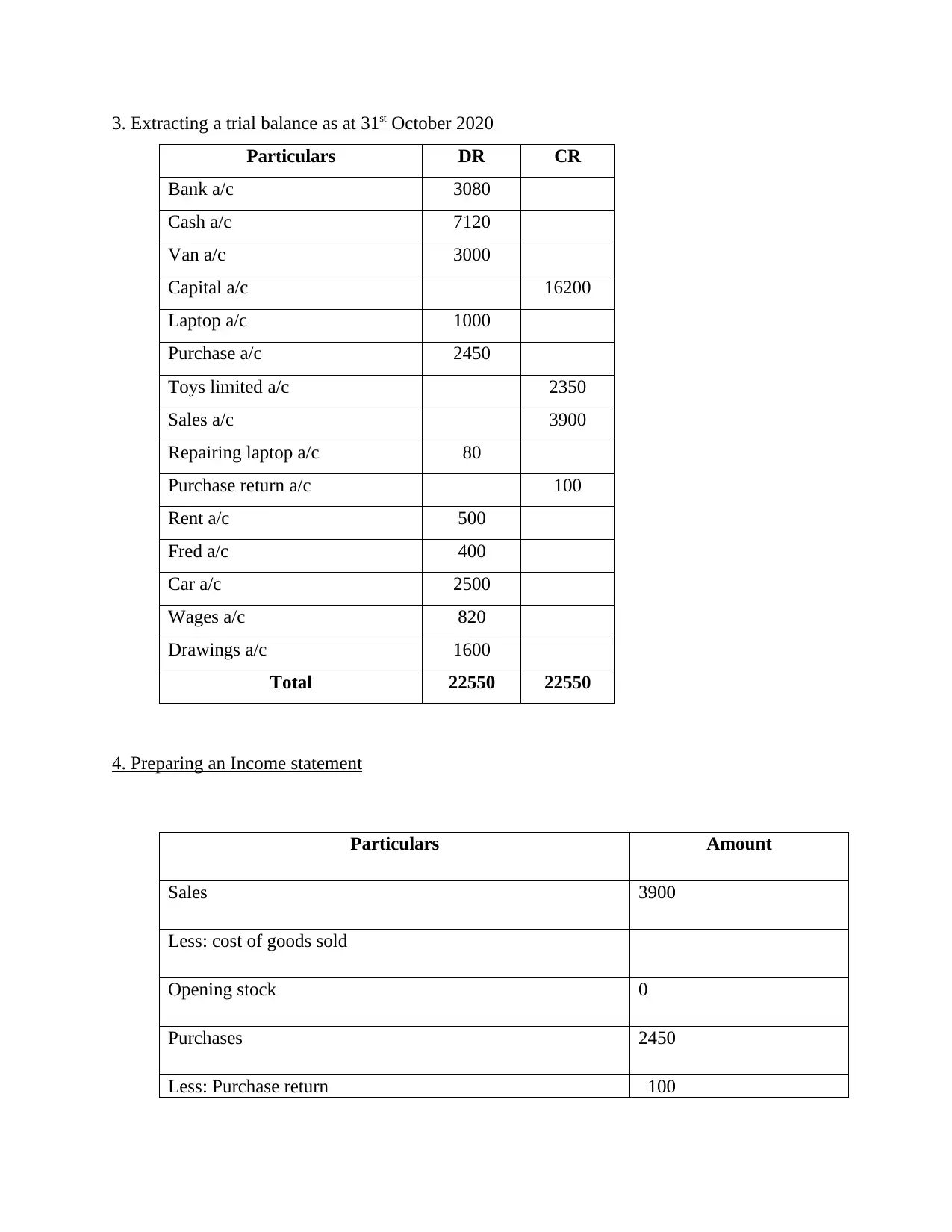

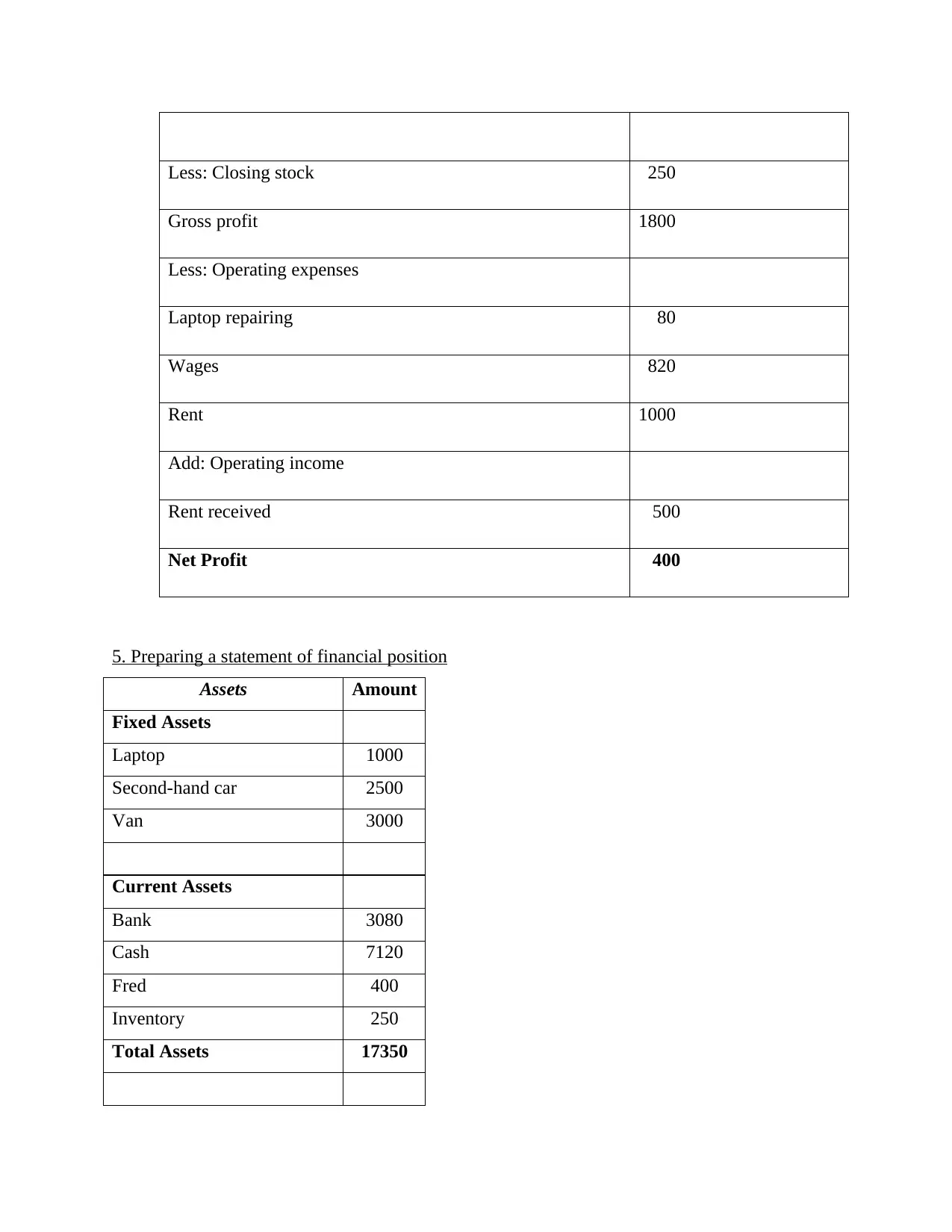

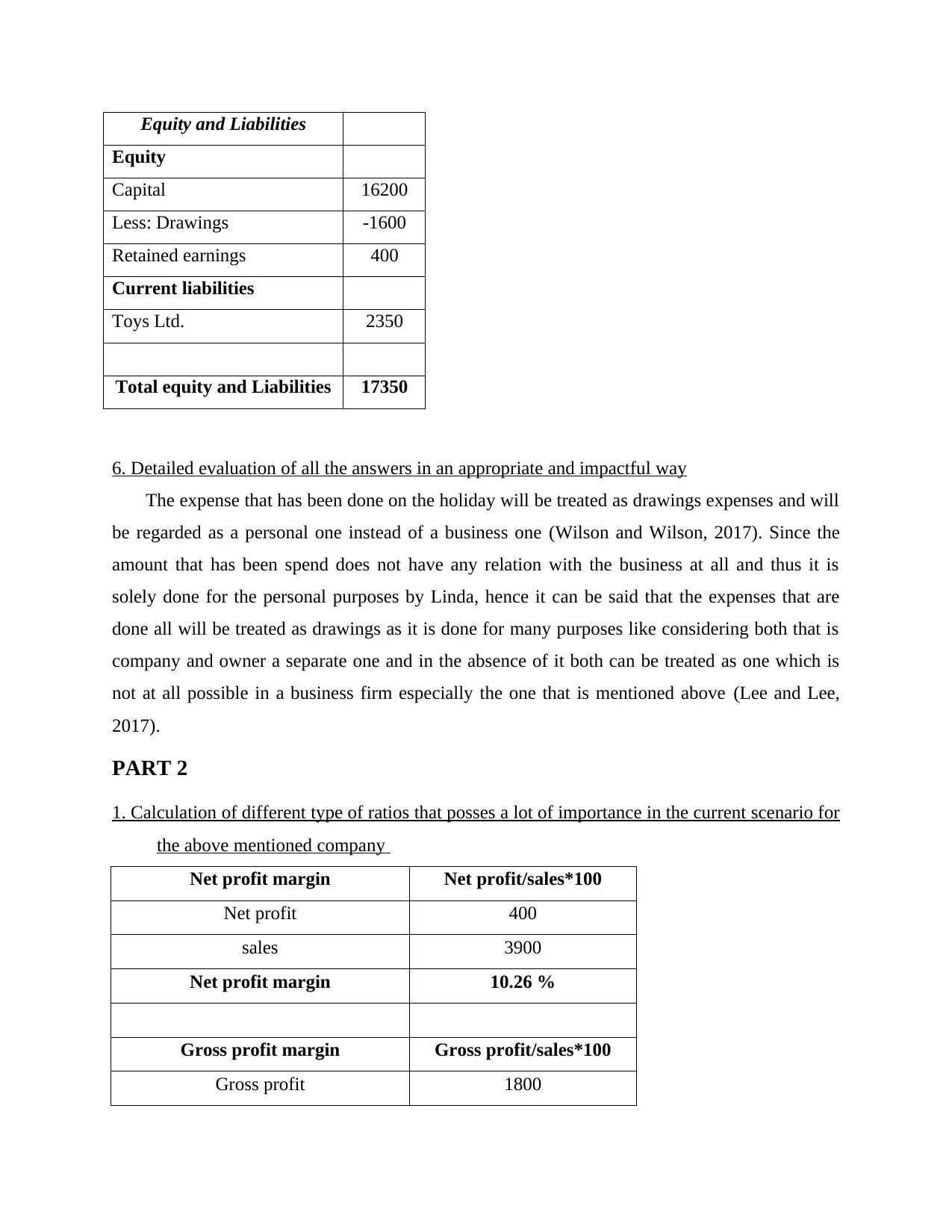

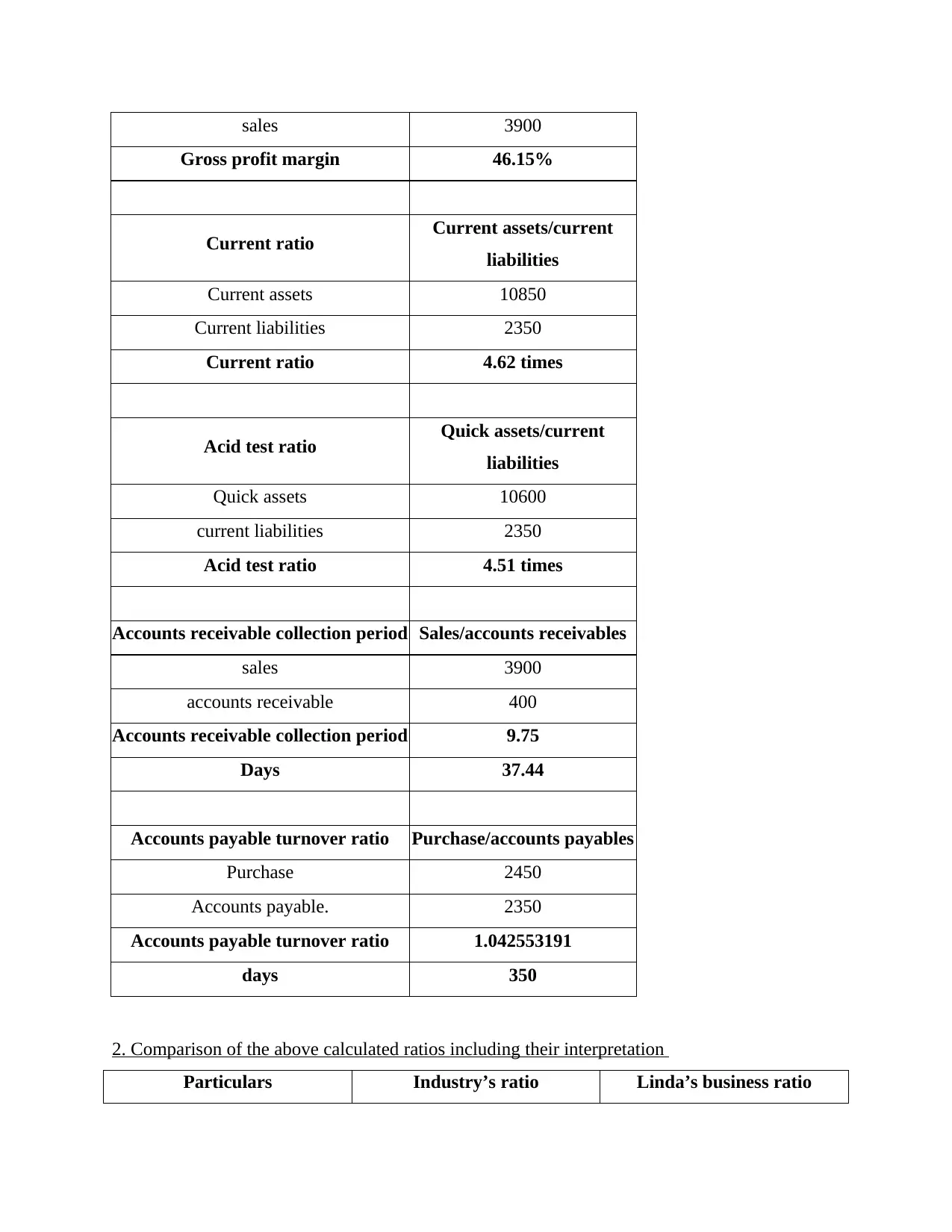

This assignment provides a detailed financial analysis of Linda's toy business, starting with the recording of transactions in T-accounts, preparing a trial balance, and constructing an income statement and a statement of financial position. The solution includes journal entries, balanced accounts, and the extraction of a trial balance. Furthermore, the assignment delves into ratio analysis, calculating net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivable collection period, and accounts payable turnover ratio. The solution compares Linda's business ratios with industry standards, offering interpretations of the financial performance and identifying areas for improvement. The analysis highlights the importance of effective financial recording and its impact on business growth and profitability.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.