Anura Fish Exporters: Live Crab Export Project from Sri Lanka to UK

VerifiedAdded on 2020/11/03

|25

|5749

|287

Project

AI Summary

This project comprehensively details the export of 907.185kg of live crabs from Batticaloa, Sri Lanka, to Billingsgate Market, London, UK, for Anura Fish Exporters (Pvt) Ltd. The project outlines step-by-step procedures, emphasizing air freight due to time sensitivity and the need for live delivery. It justifies the chosen steps, including crab handling, storage, packing, and air freight selection, while addressing risks like mortality and documentation requirements. The project includes detailed costing, Incoterms (DDP), labeling, and payment methods via Letter of Credit. It also covers necessary documents for both export from Sri Lanka and import to the UK, volumetric weight calculations, and a discussion on potential risks for the exporter. Relevant documentation, including the Lacey Act compliance and Srilankan Airlines' services are also included.

Contents

Task One..................................................................................................................................................3

All Procedures and steps for an Export of live crabs................................................................................4

Storage of Live crabs................................................................................................................................4

Packing crabs...........................................................................................................................................4

Why use air freight..................................................................................................................................6

Documents and approval needed for exports crabs from Srilanka..........................................................7

Documents needed for Import crabs to United Kingdom........................................................................7

Calculation of Volumetric Weight on Srilanka Airlines Cargo..................................................................8

Srilankan Airlines Route Map..................................................................................................................8

Srilankan Airlines Flight Schedules and Timing........................................................................................8

Costing.....................................................................................................................................................9

Delivered duty paid (DDP) Incoterms 2010..........................................................................................9

DDP Seller pays for:...............................................................................................................................10

DDP Buyer pays for:...............................................................................................................................10

Labeling / Marking.................................................................................................................................11

Carrier Acceptance by Air Mode............................................................................................................11

Payments for Seafood Shipments via Air mode.....................................................................................11

For the Exporter/Seller..........................................................................................................................12

For The Importer/Buyer.........................................................................................................................12

Risks that the exporter will face............................................................................................................13

Task 02,..................................................................................................................................................14

Packaging...............................................................................................................................................15

Labeling.................................................................................................................................................16

Preparing export declarations...............................................................................................................18

Preparing delivery orders or dock receipts............................................................................................19

The Costing............................................................................................................................................19

Ocean Freight charges LCL.....................................................................................................................19

Ocean Freight charges FCL.....................................................................................................................20

Air freight charges.................................................................................................................................20

1 | P a g e

Task One..................................................................................................................................................3

All Procedures and steps for an Export of live crabs................................................................................4

Storage of Live crabs................................................................................................................................4

Packing crabs...........................................................................................................................................4

Why use air freight..................................................................................................................................6

Documents and approval needed for exports crabs from Srilanka..........................................................7

Documents needed for Import crabs to United Kingdom........................................................................7

Calculation of Volumetric Weight on Srilanka Airlines Cargo..................................................................8

Srilankan Airlines Route Map..................................................................................................................8

Srilankan Airlines Flight Schedules and Timing........................................................................................8

Costing.....................................................................................................................................................9

Delivered duty paid (DDP) Incoterms 2010..........................................................................................9

DDP Seller pays for:...............................................................................................................................10

DDP Buyer pays for:...............................................................................................................................10

Labeling / Marking.................................................................................................................................11

Carrier Acceptance by Air Mode............................................................................................................11

Payments for Seafood Shipments via Air mode.....................................................................................11

For the Exporter/Seller..........................................................................................................................12

For The Importer/Buyer.........................................................................................................................12

Risks that the exporter will face............................................................................................................13

Task 02,..................................................................................................................................................14

Packaging...............................................................................................................................................15

Labeling.................................................................................................................................................16

Preparing export declarations...............................................................................................................18

Preparing delivery orders or dock receipts............................................................................................19

The Costing............................................................................................................................................19

Ocean Freight charges LCL.....................................................................................................................19

Ocean Freight charges FCL.....................................................................................................................20

Air freight charges.................................................................................................................................20

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Document need in MARINE transport...................................................................................................21

Document need in AIR transport...........................................................................................................21

Transportation insurance......................................................................................................................22

Limitation of Liability.............................................................................................................................22

Incoterms EX- Works (Exw)....................................................................................................................23

References.............................................................................................................................................24

2 | P a g e

Document need in AIR transport...........................................................................................................21

Transportation insurance......................................................................................................................22

Limitation of Liability.............................................................................................................................22

Incoterms EX- Works (Exw)....................................................................................................................23

References.............................................................................................................................................24

2 | P a g e

Task One

A commercial fisher has tasked you with transporting 907.185kg of Live Crabs from Batticaloa,

Sri Lanka to Bilingsgate Market, London.

- Explain step-by-step how you intend to do this.

- Justify your decision to take each of the steps you propose.

- Outline the risks the exporter will be taking.

- Offer costings

- Include relevant documents or explanations of these documents in an appendix.

Details:

• Commodity: Live Crabs (Fresh Lagoon Crabs)

• Pickup point: Batticaloa, Sri Lanka

• Shipper: Anura Fish Exporters (Pvt) Ltd. - Batticaloa, Sri Lanka

• Consignee in UK: Fresh Fish Inc. Bilingsgate Market, London, UK

• Incoterm: DDP - Fresh Fish Inc. Bilingsgate Market, London, UK (Delivered Duty Paid)

• Cargo Gross weight: 907.185 Kg (including the weight of the cartons)

• Cargo Dimensions: Master carton size 40" x 35" x 35" --- 60 Nos of Master Cartons

• Payment Terms: Letter of credit (L/C)

• Origin Airport: Colombo (CMB) - Sri Lanka *if by Air

• Origin Sea Port: Colombo, Sri Lanka *if by Sea

• Destination Airport: Heathrow (LHR) - United Kingdom *if by Air

• Destination Sea Port: Felixtowe - UK *if by Sea

3 | P a g e

A commercial fisher has tasked you with transporting 907.185kg of Live Crabs from Batticaloa,

Sri Lanka to Bilingsgate Market, London.

- Explain step-by-step how you intend to do this.

- Justify your decision to take each of the steps you propose.

- Outline the risks the exporter will be taking.

- Offer costings

- Include relevant documents or explanations of these documents in an appendix.

Details:

• Commodity: Live Crabs (Fresh Lagoon Crabs)

• Pickup point: Batticaloa, Sri Lanka

• Shipper: Anura Fish Exporters (Pvt) Ltd. - Batticaloa, Sri Lanka

• Consignee in UK: Fresh Fish Inc. Bilingsgate Market, London, UK

• Incoterm: DDP - Fresh Fish Inc. Bilingsgate Market, London, UK (Delivered Duty Paid)

• Cargo Gross weight: 907.185 Kg (including the weight of the cartons)

• Cargo Dimensions: Master carton size 40" x 35" x 35" --- 60 Nos of Master Cartons

• Payment Terms: Letter of credit (L/C)

• Origin Airport: Colombo (CMB) - Sri Lanka *if by Air

• Origin Sea Port: Colombo, Sri Lanka *if by Sea

• Destination Airport: Heathrow (LHR) - United Kingdom *if by Air

• Destination Sea Port: Felixtowe - UK *if by Sea

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All Procedures and steps for an Export of live crabs

Key information on the handling, sorting and storage of live crabs for harvesters before transport.

Confirm legal size, sex and not berried as per state/territory regulations for export and

inspection.

Tie crab’s claws hard against the body to restrict movement as soon as possible. This minimizes

crab stress, aggression and damage to other crabs and handlers.

Apply care when legs are caught in basket. Pulling on legs can cause bleeding which increases

likelihood of death. Remove weak, slow or bleeding crabs. These may be revived using a

recovery procedure.

Put 5 to 7 crabs in one eskies/boxes and fill it with ¼ of salt water.

Storage of Live crabs

Temperature variation is a principal cause of mortality in the live transport of crabs and the Importance

of maintaining low water temperatures at about 8 degree C cannot be stressed too highly. The main

benefits are that at low temperatures crabs are less active. As such they produce less metabolic wastes

and require less oxygen to breathe, so putting a reduced demand on the water in which they are

travelling.

Avoid exposure to sunlight and breeze.

Transport vehicle cargo area should be cooled at 18ºC to 25ºC.

Packing crabs

Cool crabs to 18-25°C if possible prior to packaging. Provide air holes in eskies/boxes (2 in winter

or dry season, 4 in summer or wet season). If refrigerated transport is less than 15°C, reduce the

number of air holes.

Discard weak crabs - badly damaged, very slow or frothing crabs should be killed or removed

because these crabs will not survive further transportation.

Live crabs can be packed in layers separated by moistened material such as wood shavings,

newspapers or burlap. A layer of moistened materials can be placed on top. The box should

have ventilation holes on the top edge. Crabs should not be packed as high as the ventilation

holes.

4 | P a g e

Key information on the handling, sorting and storage of live crabs for harvesters before transport.

Confirm legal size, sex and not berried as per state/territory regulations for export and

inspection.

Tie crab’s claws hard against the body to restrict movement as soon as possible. This minimizes

crab stress, aggression and damage to other crabs and handlers.

Apply care when legs are caught in basket. Pulling on legs can cause bleeding which increases

likelihood of death. Remove weak, slow or bleeding crabs. These may be revived using a

recovery procedure.

Put 5 to 7 crabs in one eskies/boxes and fill it with ¼ of salt water.

Storage of Live crabs

Temperature variation is a principal cause of mortality in the live transport of crabs and the Importance

of maintaining low water temperatures at about 8 degree C cannot be stressed too highly. The main

benefits are that at low temperatures crabs are less active. As such they produce less metabolic wastes

and require less oxygen to breathe, so putting a reduced demand on the water in which they are

travelling.

Avoid exposure to sunlight and breeze.

Transport vehicle cargo area should be cooled at 18ºC to 25ºC.

Packing crabs

Cool crabs to 18-25°C if possible prior to packaging. Provide air holes in eskies/boxes (2 in winter

or dry season, 4 in summer or wet season). If refrigerated transport is less than 15°C, reduce the

number of air holes.

Discard weak crabs - badly damaged, very slow or frothing crabs should be killed or removed

because these crabs will not survive further transportation.

Live crabs can be packed in layers separated by moistened material such as wood shavings,

newspapers or burlap. A layer of moistened materials can be placed on top. The box should

have ventilation holes on the top edge. Crabs should not be packed as high as the ventilation

holes.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

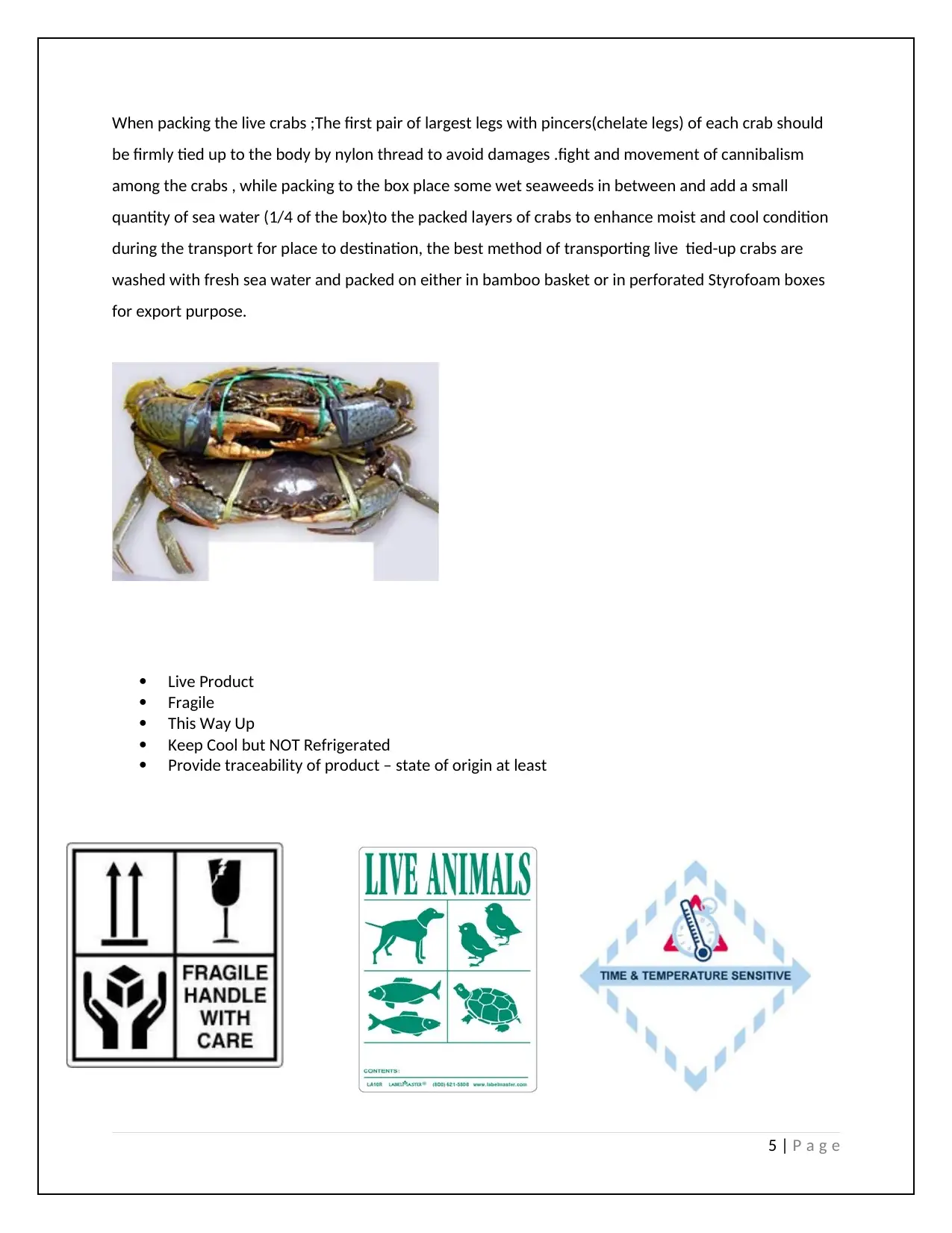

When packing the live crabs ;The first pair of largest legs with pincers(chelate legs) of each crab should

be firmly tied up to the body by nylon thread to avoid damages .fight and movement of cannibalism

among the crabs , while packing to the box place some wet seaweeds in between and add a small

quantity of sea water (1/4 of the box)to the packed layers of crabs to enhance moist and cool condition

during the transport for place to destination, the best method of transporting live tied-up crabs are

washed with fresh sea water and packed on either in bamboo basket or in perforated Styrofoam boxes

for export purpose.

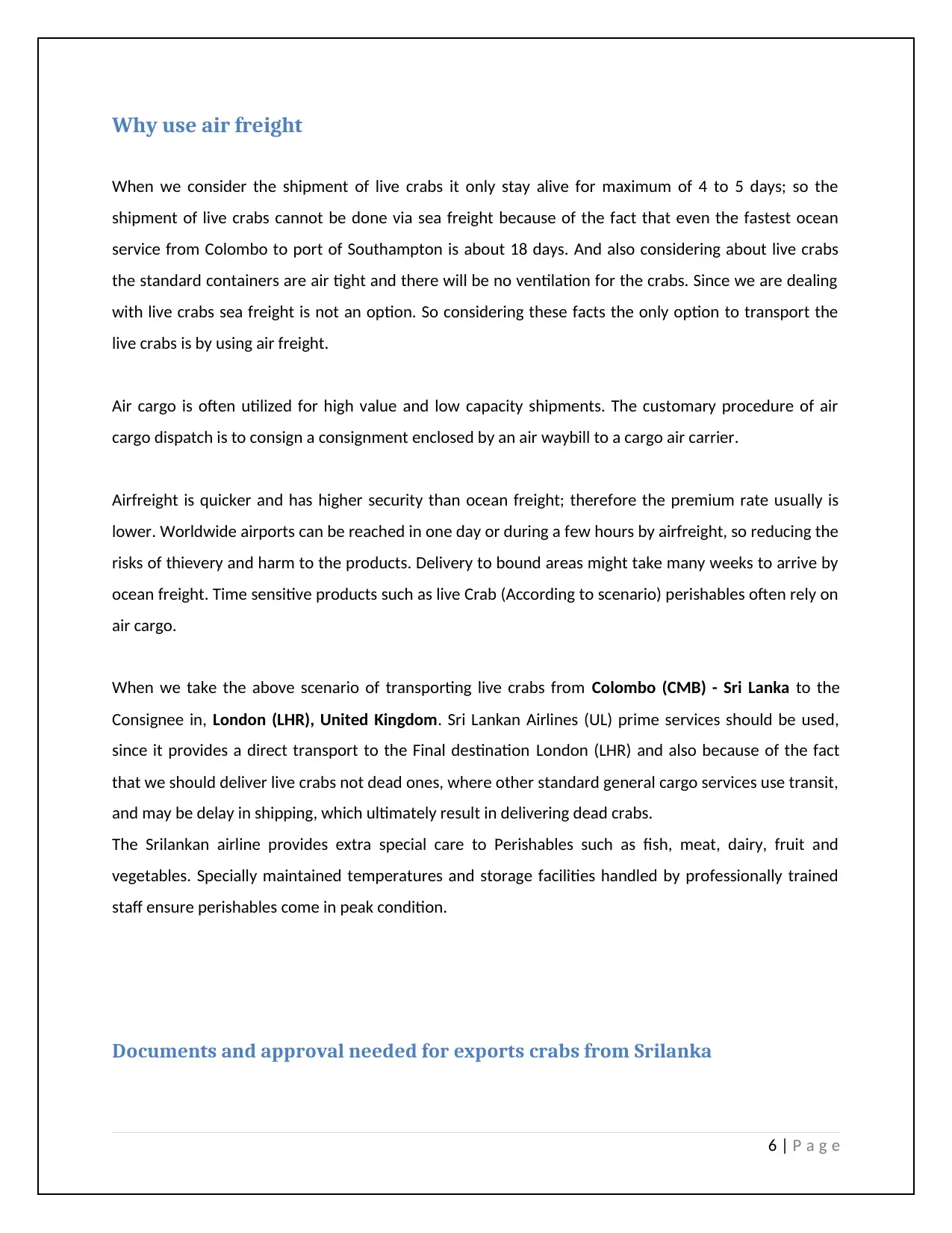

Live Product

Fragile

This Way Up

Keep Cool but NOT Refrigerated

Provide traceability of product – state of origin at least

5 | P a g e

be firmly tied up to the body by nylon thread to avoid damages .fight and movement of cannibalism

among the crabs , while packing to the box place some wet seaweeds in between and add a small

quantity of sea water (1/4 of the box)to the packed layers of crabs to enhance moist and cool condition

during the transport for place to destination, the best method of transporting live tied-up crabs are

washed with fresh sea water and packed on either in bamboo basket or in perforated Styrofoam boxes

for export purpose.

Live Product

Fragile

This Way Up

Keep Cool but NOT Refrigerated

Provide traceability of product – state of origin at least

5 | P a g e

Why use air freight

When we consider the shipment of live crabs it only stay alive for maximum of 4 to 5 days; so the

shipment of live crabs cannot be done via sea freight because of the fact that even the fastest ocean

service from Colombo to port of Southampton is about 18 days. And also considering about live crabs

the standard containers are air tight and there will be no ventilation for the crabs. Since we are dealing

with live crabs sea freight is not an option. So considering these facts the only option to transport the

live crabs is by using air freight.

Air cargo is often utilized for high value and low capacity shipments. The customary procedure of air

cargo dispatch is to consign a consignment enclosed by an air waybill to a cargo air carrier.

Airfreight is quicker and has higher security than ocean freight; therefore the premium rate usually is

lower. Worldwide airports can be reached in one day or during a few hours by airfreight, so reducing the

risks of thievery and harm to the products. Delivery to bound areas might take many weeks to arrive by

ocean freight. Time sensitive products such as live Crab (According to scenario) perishables often rely on

air cargo.

When we take the above scenario of transporting live crabs from Colombo (CMB) - Sri Lanka to the

Consignee in, London (LHR), United Kingdom. Sri Lankan Airlines (UL) prime services should be used,

since it provides a direct transport to the Final destination London (LHR) and also because of the fact

that we should deliver live crabs not dead ones, where other standard general cargo services use transit,

and may be delay in shipping, which ultimately result in delivering dead crabs.

The Srilankan airline provides extra special care to Perishables such as fish, meat, dairy, fruit and

vegetables. Specially maintained temperatures and storage facilities handled by professionally trained

staff ensure perishables come in peak condition.

Documents and approval needed for exports crabs from Srilanka

6 | P a g e

When we consider the shipment of live crabs it only stay alive for maximum of 4 to 5 days; so the

shipment of live crabs cannot be done via sea freight because of the fact that even the fastest ocean

service from Colombo to port of Southampton is about 18 days. And also considering about live crabs

the standard containers are air tight and there will be no ventilation for the crabs. Since we are dealing

with live crabs sea freight is not an option. So considering these facts the only option to transport the

live crabs is by using air freight.

Air cargo is often utilized for high value and low capacity shipments. The customary procedure of air

cargo dispatch is to consign a consignment enclosed by an air waybill to a cargo air carrier.

Airfreight is quicker and has higher security than ocean freight; therefore the premium rate usually is

lower. Worldwide airports can be reached in one day or during a few hours by airfreight, so reducing the

risks of thievery and harm to the products. Delivery to bound areas might take many weeks to arrive by

ocean freight. Time sensitive products such as live Crab (According to scenario) perishables often rely on

air cargo.

When we take the above scenario of transporting live crabs from Colombo (CMB) - Sri Lanka to the

Consignee in, London (LHR), United Kingdom. Sri Lankan Airlines (UL) prime services should be used,

since it provides a direct transport to the Final destination London (LHR) and also because of the fact

that we should deliver live crabs not dead ones, where other standard general cargo services use transit,

and may be delay in shipping, which ultimately result in delivering dead crabs.

The Srilankan airline provides extra special care to Perishables such as fish, meat, dairy, fruit and

vegetables. Specially maintained temperatures and storage facilities handled by professionally trained

staff ensure perishables come in peak condition.

Documents and approval needed for exports crabs from Srilanka

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sri Lanka National Plan of Action to Prevent, Deter and Eliminate IUU Fishing (SLNPOA-IUU)

contains measures that are being implemented and those proposed to be adopted for

implementation to combat IUU fishing activities conducted by local fishing in Sri Lanka waters,

and waters of national jurisdictions of other coastal States and high-seas Sri Lanka waters. It has

been prepared in accordance with the guidelines stipulated in the International Plan of Action to

Prevent, Deter and Eliminate Illegal, Unreported and Unregulated Fishing (IPOA-IUU) and

exporting live aquatics.

Fisheries of Sri Lanka are governed by Fisheries and Aquatic Resources Act, No. 2 of 1996 as

amended by Acts No. 4 of 2000, 4 of 2004 and 22 of 2006 (FARA), provisions of which are

administered by the Department of Fisheries and Aquatic Resources (DFAR). FARA does not

include provisions to implement measures on illegal fishing of aquatics and exporting services.

There for the relevant document should be submitted to provide the approval of local

government to catch aquatics and to export them to market.

Documents needed for Import crabs to United Kingdom

Import license is requires when importing live aquatics (crab, fish lobster etc.) because of

negative list.

A CARICOM Area Invoice (this is provided by the supplier and is necessary for any goods entering

the CARICOM region).

The supplier’s invoice. A copy of the Airway Bill (for items transported by air) or Bill of Lading

(for items transported by sea).

Import license for those items that are on the negative. information on obtaining an import

license, should be registered to the relevant fishery department

A declaration on the C75 or C76 form (used only when there is an ongoing demand-supply

relationship between the importer and the supplier) signed by the importer. A certificate of

origin (provided by the supplier).

7 | P a g e

contains measures that are being implemented and those proposed to be adopted for

implementation to combat IUU fishing activities conducted by local fishing in Sri Lanka waters,

and waters of national jurisdictions of other coastal States and high-seas Sri Lanka waters. It has

been prepared in accordance with the guidelines stipulated in the International Plan of Action to

Prevent, Deter and Eliminate Illegal, Unreported and Unregulated Fishing (IPOA-IUU) and

exporting live aquatics.

Fisheries of Sri Lanka are governed by Fisheries and Aquatic Resources Act, No. 2 of 1996 as

amended by Acts No. 4 of 2000, 4 of 2004 and 22 of 2006 (FARA), provisions of which are

administered by the Department of Fisheries and Aquatic Resources (DFAR). FARA does not

include provisions to implement measures on illegal fishing of aquatics and exporting services.

There for the relevant document should be submitted to provide the approval of local

government to catch aquatics and to export them to market.

Documents needed for Import crabs to United Kingdom

Import license is requires when importing live aquatics (crab, fish lobster etc.) because of

negative list.

A CARICOM Area Invoice (this is provided by the supplier and is necessary for any goods entering

the CARICOM region).

The supplier’s invoice. A copy of the Airway Bill (for items transported by air) or Bill of Lading

(for items transported by sea).

Import license for those items that are on the negative. information on obtaining an import

license, should be registered to the relevant fishery department

A declaration on the C75 or C76 form (used only when there is an ongoing demand-supply

relationship between the importer and the supplier) signed by the importer. A certificate of

origin (provided by the supplier).

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

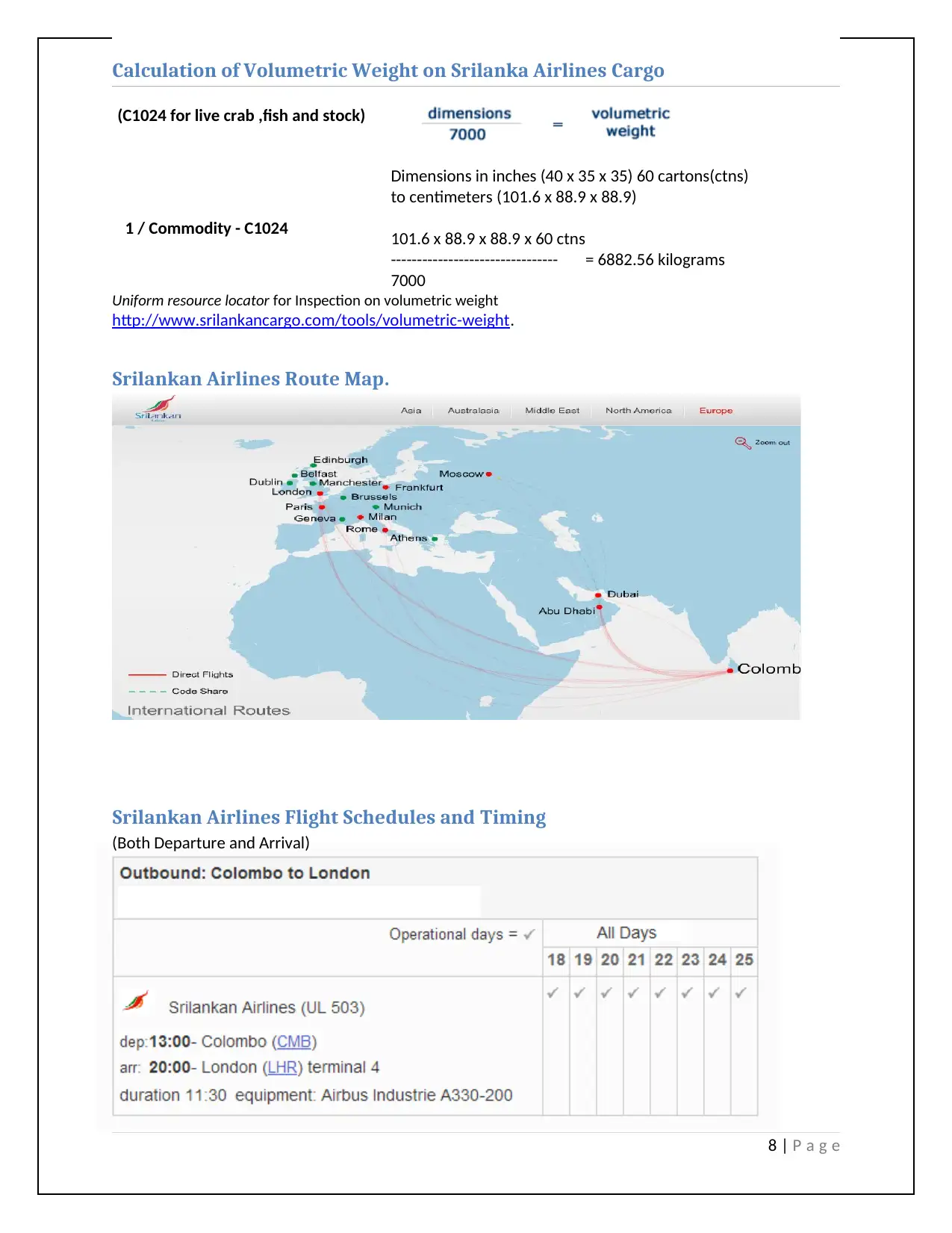

Uniform resource locator for Inspection on volumetric weight

http://www.srilankancargo.com/tools/volumetric-weight.

Srilankan Airlines Route Map.

Srilankan Airlines Flight Schedules and Timing

(Both Departure and Arrival)

8 | P a g e

Calculation of Volumetric Weight on Srilanka Airlines Cargo

(C1024 for live crab ,fish and stock)

1 / Commodity - C1024

Dimensions in inches (40 x 35 x 35) 60 cartons(ctns)

to centimeters (101.6 x 88.9 x 88.9)

101.6 x 88.9 x 88.9 x 60 ctns

-------------------------------- = 6882.56 kilograms

7000

http://www.srilankancargo.com/tools/volumetric-weight.

Srilankan Airlines Route Map.

Srilankan Airlines Flight Schedules and Timing

(Both Departure and Arrival)

8 | P a g e

Calculation of Volumetric Weight on Srilanka Airlines Cargo

(C1024 for live crab ,fish and stock)

1 / Commodity - C1024

Dimensions in inches (40 x 35 x 35) 60 cartons(ctns)

to centimeters (101.6 x 88.9 x 88.9)

101.6 x 88.9 x 88.9 x 60 ctns

-------------------------------- = 6882.56 kilograms

7000

Costing

Transport charges from Batticaloa to Airport -

Export custom documentation -

Handling charges -

Export corantime clearance -

Prime service charges -

Import custom clearance -

Import corantime charges -

VAT or possible taxes -

Transport charges from Heathrow to Billingsgate Market -

9 | P a g e

Transport charges from Batticaloa to Airport -

Export custom documentation -

Handling charges -

Export corantime clearance -

Prime service charges -

Import custom clearance -

Import corantime charges -

VAT or possible taxes -

Transport charges from Heathrow to Billingsgate Market -

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

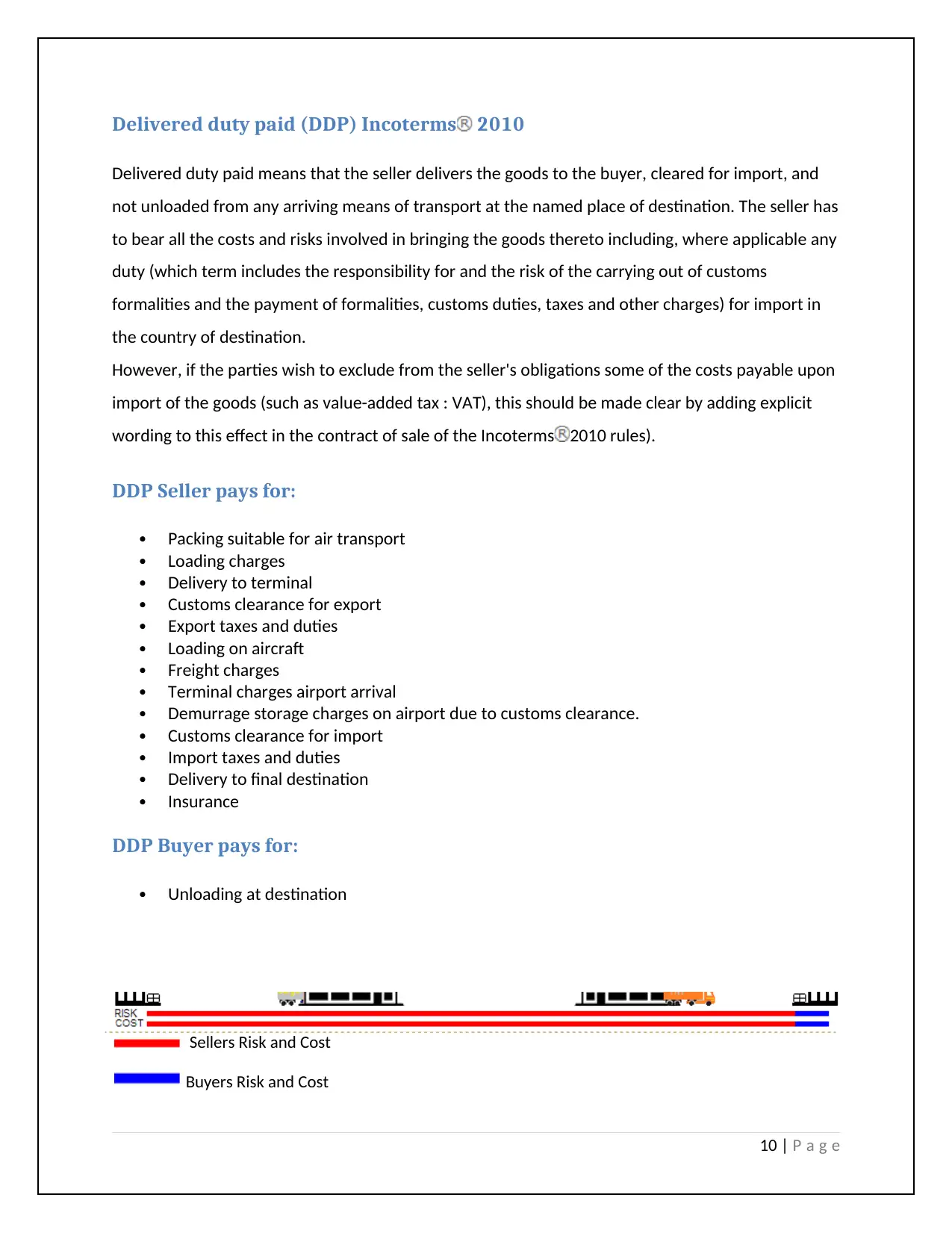

Delivered duty paid (DDP) Incoterms 2010

Delivered duty paid means that the seller delivers the goods to the buyer, cleared for import, and

not unloaded from any arriving means of transport at the named place of destination. The seller has

to bear all the costs and risks involved in bringing the goods thereto including, where applicable any

duty (which term includes the responsibility for and the risk of the carrying out of customs

formalities and the payment of formalities, customs duties, taxes and other charges) for import in

the country of destination.

However, if the parties wish to exclude from the seller's obligations some of the costs payable upon

import of the goods (such as value-added tax : VAT), this should be made clear by adding explicit

wording to this effect in the contract of sale of the Incoterms 2010 rules).

DDP Seller pays for:

Packing suitable for air transport

Loading charges

Delivery to terminal

Customs clearance for export

Export taxes and duties

Loading on aircraft

Freight charges

Terminal charges airport arrival

Demurrage storage charges on airport due to customs clearance.

Customs clearance for import

Import taxes and duties

Delivery to final destination

Insurance

DDP Buyer pays for:

Unloading at destination

Sellers Risk and Cost

Buyers Risk and Cost

10 | P a g e

Delivered duty paid means that the seller delivers the goods to the buyer, cleared for import, and

not unloaded from any arriving means of transport at the named place of destination. The seller has

to bear all the costs and risks involved in bringing the goods thereto including, where applicable any

duty (which term includes the responsibility for and the risk of the carrying out of customs

formalities and the payment of formalities, customs duties, taxes and other charges) for import in

the country of destination.

However, if the parties wish to exclude from the seller's obligations some of the costs payable upon

import of the goods (such as value-added tax : VAT), this should be made clear by adding explicit

wording to this effect in the contract of sale of the Incoterms 2010 rules).

DDP Seller pays for:

Packing suitable for air transport

Loading charges

Delivery to terminal

Customs clearance for export

Export taxes and duties

Loading on aircraft

Freight charges

Terminal charges airport arrival

Demurrage storage charges on airport due to customs clearance.

Customs clearance for import

Import taxes and duties

Delivery to final destination

Insurance

DDP Buyer pays for:

Unloading at destination

Sellers Risk and Cost

Buyers Risk and Cost

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Labeling / Marking

All containers of seafood being shipped interstate must be marked according to the 1988 Lacey Act.

A Fish/Wildlife Sticker may be used by the shipper to provide required information. The following six

items to be prominently displayed on each shipment:

Name and address of shipper and consignee, or passenger.

24-hour phone number of the consignee or passenger.

Commodity note as Fish or Wildlife.

Specifies species name: such as live Crab

Number of each species or the weight of each type species.

Each container must be marked Live, Fresh or Frozen.

Carrier Acceptance by Air Mode

Compliance with the Lacey Act and its packaging requirements are mandatory where the

containers must be free of leaks and odors, random "tip tests" shall be conducted, with the

option of refusing an entire shipment should there be an excessive number of cartons leaking of

Indelible inks and waterproof labels must be used. Sequential numbering of multiple packages is

recommended (1 of 4, 2 of 4, 3 of 4, etc.).

Payments for Seafood Shipments via Air mode

Most Airlines does not accept COD (Cash on Delivery) payments because of Noncommercial

perishable goods must be prepaid. So airway bills like Letter of credit are being used, these Air

Waybills are never negotiable. They are always straight consignments even if “TO ORDER” is typed

in the Consignee block. Not being a title document, but merely a receipt for shipment, the

importing buyer can pick up the merchandise at the airport simply by providing proper identification

to the carrier.

11 | P a g e

All containers of seafood being shipped interstate must be marked according to the 1988 Lacey Act.

A Fish/Wildlife Sticker may be used by the shipper to provide required information. The following six

items to be prominently displayed on each shipment:

Name and address of shipper and consignee, or passenger.

24-hour phone number of the consignee or passenger.

Commodity note as Fish or Wildlife.

Specifies species name: such as live Crab

Number of each species or the weight of each type species.

Each container must be marked Live, Fresh or Frozen.

Carrier Acceptance by Air Mode

Compliance with the Lacey Act and its packaging requirements are mandatory where the

containers must be free of leaks and odors, random "tip tests" shall be conducted, with the

option of refusing an entire shipment should there be an excessive number of cartons leaking of

Indelible inks and waterproof labels must be used. Sequential numbering of multiple packages is

recommended (1 of 4, 2 of 4, 3 of 4, etc.).

Payments for Seafood Shipments via Air mode

Most Airlines does not accept COD (Cash on Delivery) payments because of Noncommercial

perishable goods must be prepaid. So airway bills like Letter of credit are being used, these Air

Waybills are never negotiable. They are always straight consignments even if “TO ORDER” is typed

in the Consignee block. Not being a title document, but merely a receipt for shipment, the

importing buyer can pick up the merchandise at the airport simply by providing proper identification

to the carrier.

11 | P a g e

(Q)When a letter of credit is used, how does the exporter prevent the buyer from getting

the merchandise without paying for it?

Answer: The Air Waybill consignee should be listed as the buyer’s bank. The bank will

transfer the goods to the buyer through an “Air Release”, but only after the buyer has paid or

obligated himself to pay for the merchandise. Air Waybills only be consigned to the order of the

buyer’s bank with that bank’s permission.

The fact is that Letter of Credit can be a very useful financial tool for both the buyer/importer and the

seller/exporter. While Letters of Credit are particularly well suited for high transactions,

For the Exporter/Seller

Upon presentation of the specified documents (in strict conformance) the Seller/Exporter is

guaranteed payment (the exception is if the Issuing Bank folds)

Eliminates risk of the buyer canceling the order and therefore reduces production risk

Makes it easier for the Seller/Exporter to secure order/production financing-pre-export

financing

Easier to secure receivable financing (in case where the L/C is not payable At Sight)

Buyer cannot refuse payment by raising a complaint about the goods. Any complaints must be

settled between the Buyer and Seller outside of the L/C.

For The Importer/Buyer

In most cases the Importer/Buyer avoids partial pre-payments or deposits

Helps reduce the risk of non-performance of the Exporter/Seller. If the Exporter/Seller doesn’t

ship the goods they don’t get paid.

Certainty that payment will only be make to the Exporter/Seller upon presentation of

documents in strict compliance with the L/C evidencing the shipment of goods.

Documents are received quickly, expediting customs clearance and ultimate delivery

Makes structuring an advantageous payment schedule easy

Importer/Buyer will receive timely delivery or the goods because the L/C terms dictate latest

acceptable shipment date.

12 | P a g e

the merchandise without paying for it?

Answer: The Air Waybill consignee should be listed as the buyer’s bank. The bank will

transfer the goods to the buyer through an “Air Release”, but only after the buyer has paid or

obligated himself to pay for the merchandise. Air Waybills only be consigned to the order of the

buyer’s bank with that bank’s permission.

The fact is that Letter of Credit can be a very useful financial tool for both the buyer/importer and the

seller/exporter. While Letters of Credit are particularly well suited for high transactions,

For the Exporter/Seller

Upon presentation of the specified documents (in strict conformance) the Seller/Exporter is

guaranteed payment (the exception is if the Issuing Bank folds)

Eliminates risk of the buyer canceling the order and therefore reduces production risk

Makes it easier for the Seller/Exporter to secure order/production financing-pre-export

financing

Easier to secure receivable financing (in case where the L/C is not payable At Sight)

Buyer cannot refuse payment by raising a complaint about the goods. Any complaints must be

settled between the Buyer and Seller outside of the L/C.

For The Importer/Buyer

In most cases the Importer/Buyer avoids partial pre-payments or deposits

Helps reduce the risk of non-performance of the Exporter/Seller. If the Exporter/Seller doesn’t

ship the goods they don’t get paid.

Certainty that payment will only be make to the Exporter/Seller upon presentation of

documents in strict compliance with the L/C evidencing the shipment of goods.

Documents are received quickly, expediting customs clearance and ultimate delivery

Makes structuring an advantageous payment schedule easy

Importer/Buyer will receive timely delivery or the goods because the L/C terms dictate latest

acceptable shipment date.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.