Strategic Problem Solving and Decision Making in Lloyds Banking

VerifiedAdded on 2023/06/09

|10

|2664

|234

Report

AI Summary

This report examines the problems faced by Lloyds Banking Group, particularly concerning branch closures and the transition to digital banking. It uses SWOT and PESTLE analyses to evaluate internal and external factors impacting the bank. The report highlights the unrest among customers unfamiliar with digital banking, job losses, and the decline in shareholder value. Recommendations to resolve these issues include balancing digital services with maintaining physical branches, offering customer incentives, and engaging with local communities. A decision-making matrix is used to identify the best solution, emphasizing the importance of continuing digitalization while preserving high street banking. The report concludes by discussing the implementation and communication of these decisions, stressing the need for monitoring and feedback to ensure the effectiveness of the proposed solutions. Desklib offers a variety of resources, including similar solved assignments and past papers, to aid students in their studies.

Problem Solving and

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

SWOT analysis............................................................................................................................3

PESTLE analysis.........................................................................................................................5

Recommendations to resolve the problem...................................................................................6

Decision making matrix to identify the best solution for the problem........................................7

Implementation and communication of decisions.......................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

SWOT analysis............................................................................................................................3

PESTLE analysis.........................................................................................................................5

Recommendations to resolve the problem...................................................................................6

Decision making matrix to identify the best solution for the problem........................................7

Implementation and communication of decisions.......................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Working in an ever-changing and competitive environment, businesses face many problems

and challenges and understanding these problems is very essential in order to find solutions.

Understanding and dealing with these problems is also crucial for the survival of the business.

This report, in context of Lloyds banking group will highlight the nature, scope and impact of

one of the problems faced by the company(Tanda and Schena, 2019). As the lenders have been

declining, the banking group had to shut down many of its branches. The transition of the

business to digital banking also caused closing of several branches of the bank. The customers

had to shift to online banking and transactions due to this transition and also because of

pandemic of Covid19. This caused an unrest among the customers as not everyone was

familiar with the usage of digital marketing and the banking apps(Druhova, Hirna and Fostyak,

2021). Elders and customers from remote areas had a great difficulty in adaptation. The union

representatives started protesting to these closures as the bank neglected its corporate social

responsibility as many employees lost their jobs due to the shutting down of so many branches.

The customers are also likely shifting to the rival banks as they started providing incentives to

the new customers. The shareholders were also greatly affected as their investments diminished

due to the significant fall of the share prices of the bank. The operating cost of the bank also

increased and all these resulted in the reduction in the profitability of the banking group(Zabala

Aguayo and Ślusarczyk, 2020). The small shops adjacent to the bank branches were also

affected due to the shutting down of the branches in prime locations.

SWOT analysis

SWOT analysis is the evaluation of the factors like the organisation’s internal strengths and

weaknesses and the external opportunities and threats.

Strengths

Lloyds is one of the largest digital banks in UK which has multiple branches in places

that get high footfall of customers. The customer reach of the bank is also very high.

It is one of the leading provider of financial services and one of the largest corporate tax

payers in UK and thus plays an important role in the country’s economy.

Working in an ever-changing and competitive environment, businesses face many problems

and challenges and understanding these problems is very essential in order to find solutions.

Understanding and dealing with these problems is also crucial for the survival of the business.

This report, in context of Lloyds banking group will highlight the nature, scope and impact of

one of the problems faced by the company(Tanda and Schena, 2019). As the lenders have been

declining, the banking group had to shut down many of its branches. The transition of the

business to digital banking also caused closing of several branches of the bank. The customers

had to shift to online banking and transactions due to this transition and also because of

pandemic of Covid19. This caused an unrest among the customers as not everyone was

familiar with the usage of digital marketing and the banking apps(Druhova, Hirna and Fostyak,

2021). Elders and customers from remote areas had a great difficulty in adaptation. The union

representatives started protesting to these closures as the bank neglected its corporate social

responsibility as many employees lost their jobs due to the shutting down of so many branches.

The customers are also likely shifting to the rival banks as they started providing incentives to

the new customers. The shareholders were also greatly affected as their investments diminished

due to the significant fall of the share prices of the bank. The operating cost of the bank also

increased and all these resulted in the reduction in the profitability of the banking group(Zabala

Aguayo and Ślusarczyk, 2020). The small shops adjacent to the bank branches were also

affected due to the shutting down of the branches in prime locations.

SWOT analysis

SWOT analysis is the evaluation of the factors like the organisation’s internal strengths and

weaknesses and the external opportunities and threats.

Strengths

Lloyds is one of the largest digital banks in UK which has multiple branches in places

that get high footfall of customers. The customer reach of the bank is also very high.

It is one of the leading provider of financial services and one of the largest corporate tax

payers in UK and thus plays an important role in the country’s economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The bank has a solid capital generation and a high capital position in the industry which

gives it a competitive advantage. The bank’s operational efficiency which low risk

participation and cost advantage is beneficial for customers as well as stakeholders.

The bank offers numerous services and uses differentiated multichannel approach to

give seamless experience to the customers(SWOT analysis of Lloyds banking group,

2022). Understanding and supporting the customers’ needs by providing various

services like insurance, investments, commercial financing, etc. has strengthened its

footing in UK.

Weaknesses

The structural changes made after the crisis that created an absence of subsidiary on

future costs has had great impact on the financial stability and performance of the banks

and Lloyd is not an exception.

There have been many controversies regarding the bank for tax evasion and money

laundering that affected its brand image and dropped its credit ratings.

The dependency of the bank of UK economy makes it weak as when the economy

becomes unstable, the performance and operations of the bank will greatly be

affected(SWOT analysis of Lloyds banking group, 2022).

Although, digital banking has been a boon to banks as well as customers, but it also

brought along many issues with it as aged customers, people living in rural areas and

not having access to internet or other means are highly dissatisfied with it.

The closure of high number of branches is also affecting Lloyd’s business.

Opportunities

The economy and customers’ spending has been increasing after years of slow growth

and recession. This can be a great opportunity for the bank to attract more customers

and increase the market share of the bank.

The improved online channel through technology can help the bank to attract more

customers and serve them using big data analytics.

Free trade agreement with government can give an opportunity to the bank to enter new

emerging markets.

Threats

gives it a competitive advantage. The bank’s operational efficiency which low risk

participation and cost advantage is beneficial for customers as well as stakeholders.

The bank offers numerous services and uses differentiated multichannel approach to

give seamless experience to the customers(SWOT analysis of Lloyds banking group,

2022). Understanding and supporting the customers’ needs by providing various

services like insurance, investments, commercial financing, etc. has strengthened its

footing in UK.

Weaknesses

The structural changes made after the crisis that created an absence of subsidiary on

future costs has had great impact on the financial stability and performance of the banks

and Lloyd is not an exception.

There have been many controversies regarding the bank for tax evasion and money

laundering that affected its brand image and dropped its credit ratings.

The dependency of the bank of UK economy makes it weak as when the economy

becomes unstable, the performance and operations of the bank will greatly be

affected(SWOT analysis of Lloyds banking group, 2022).

Although, digital banking has been a boon to banks as well as customers, but it also

brought along many issues with it as aged customers, people living in rural areas and

not having access to internet or other means are highly dissatisfied with it.

The closure of high number of branches is also affecting Lloyd’s business.

Opportunities

The economy and customers’ spending has been increasing after years of slow growth

and recession. This can be a great opportunity for the bank to attract more customers

and increase the market share of the bank.

The improved online channel through technology can help the bank to attract more

customers and serve them using big data analytics.

Free trade agreement with government can give an opportunity to the bank to enter new

emerging markets.

Threats

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rise in competition and growing strengths of regional banks can become a threat to

Lloyds’ growth(SWOT analysis of Lloyds banking group, 2022).

The uncertainty and political and economical instability can affect the bank’s

profitability.

PESTLE analysis

PESTLE analysis is done to understand and evaluate the external factors that can affect the

organisation, its working and profitability. These factors include the Political, Economical,

Socio-cultural, Technological, Legal and Environmental aspects of the region the organisation

works in.

Political factors

The government sold off its shares of the Lloyds bank which accounted for 43%, this

removed the government’s influence and made Lloyds a privately owned business. This

can help the bank to rejuvenate and focus more on the customers.

The imposition of new policies by the government affects the revenue generation and

operations of the bank. The priorities of government for the financial sector might

change in the coming year, hence Lloyds bank should prepare for the same.

The political instability in the global environment might impact the economy of UK

too, affects the growth opportunities of the bank(PESTLE analysis of Lloyds banking

group, 2022).

The changes in the taxation policies by the government due to increasing inequality in

UK and also to reduce the carbon footprint of the financial sector, may lead to reduction

in revenue and profits of the bank which it used to enjoy earlier in terms of higher

profits that it used to invest in R&D.

Economic Factors

The growth of the bank is closely and directly related to the economic performance of

the economy of the country. As better economy in the country means more disposable

income of the citizens and more borrowings and lending, and this works in favour of

the bank.

The consumer spending behaviour will greatly be affected by the negative impacts of

the growing inequality on the consumer sentiments, this might cast a downwards

Lloyds’ growth(SWOT analysis of Lloyds banking group, 2022).

The uncertainty and political and economical instability can affect the bank’s

profitability.

PESTLE analysis

PESTLE analysis is done to understand and evaluate the external factors that can affect the

organisation, its working and profitability. These factors include the Political, Economical,

Socio-cultural, Technological, Legal and Environmental aspects of the region the organisation

works in.

Political factors

The government sold off its shares of the Lloyds bank which accounted for 43%, this

removed the government’s influence and made Lloyds a privately owned business. This

can help the bank to rejuvenate and focus more on the customers.

The imposition of new policies by the government affects the revenue generation and

operations of the bank. The priorities of government for the financial sector might

change in the coming year, hence Lloyds bank should prepare for the same.

The political instability in the global environment might impact the economy of UK

too, affects the growth opportunities of the bank(PESTLE analysis of Lloyds banking

group, 2022).

The changes in the taxation policies by the government due to increasing inequality in

UK and also to reduce the carbon footprint of the financial sector, may lead to reduction

in revenue and profits of the bank which it used to enjoy earlier in terms of higher

profits that it used to invest in R&D.

Economic Factors

The growth of the bank is closely and directly related to the economic performance of

the economy of the country. As better economy in the country means more disposable

income of the citizens and more borrowings and lending, and this works in favour of

the bank.

The consumer spending behaviour will greatly be affected by the negative impacts of

the growing inequality on the consumer sentiments, this might cast a downwards

pressure on the spending of the consumers even if the disposable income remains

stable.

Socio-cultural factors

The introduction of digitalisation and online banking which can be accessed at the

comfort of customers by the bank has improves the accessibility of the banking services

for customers with disability and has supported them greatly.

The workforce diversity in the bank that has employees without discriminating them on

the basis of caste, colour or religion is a great aspect of the bank.

Technological factors

The bank has made digital transformation by providing facilities like online banking,

etc. in order to improve customer experience. But this has also caused a chaos among

the customers and the bank had to close many of its branches(PESTLE analysis of

Lloyds bank, 2021).

Overall business of the bank has been transformed with the use of new technology.

Legal factors

The regulatory changes made by the UK government for ring-fencing has had several

impacts on Lloyds and the entire banking industry.

The HBOS reading fraud case has affected the brand image of the bank to a great

extent. The reputation of the bank has greatly suffered due to this case.

Environmental factors

The bank tries to keep its practices and operations more environment friendly and

sustainable.

The Lloyds bank has started a Clean Growth Finance Initiative in which it focuses on

reducing the emissions and carbon transport. It also tries to utilise its energy and water

efficiently and reduce waste and focus of recycling(PESTLE analysis of Lloyds banking

group, 2022). The bank does this by providing a scheme of offering lending at

discounted rates to the businesses who want to reduce their environmental impact.

The bank’s increased renewable portfolio also shows its contribution for the

sustainability of the environment.

stable.

Socio-cultural factors

The introduction of digitalisation and online banking which can be accessed at the

comfort of customers by the bank has improves the accessibility of the banking services

for customers with disability and has supported them greatly.

The workforce diversity in the bank that has employees without discriminating them on

the basis of caste, colour or religion is a great aspect of the bank.

Technological factors

The bank has made digital transformation by providing facilities like online banking,

etc. in order to improve customer experience. But this has also caused a chaos among

the customers and the bank had to close many of its branches(PESTLE analysis of

Lloyds bank, 2021).

Overall business of the bank has been transformed with the use of new technology.

Legal factors

The regulatory changes made by the UK government for ring-fencing has had several

impacts on Lloyds and the entire banking industry.

The HBOS reading fraud case has affected the brand image of the bank to a great

extent. The reputation of the bank has greatly suffered due to this case.

Environmental factors

The bank tries to keep its practices and operations more environment friendly and

sustainable.

The Lloyds bank has started a Clean Growth Finance Initiative in which it focuses on

reducing the emissions and carbon transport. It also tries to utilise its energy and water

efficiently and reduce waste and focus of recycling(PESTLE analysis of Lloyds banking

group, 2022). The bank does this by providing a scheme of offering lending at

discounted rates to the businesses who want to reduce their environmental impact.

The bank’s increased renewable portfolio also shows its contribution for the

sustainability of the environment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendations to resolve the problem

As it can be seen that digitalisation of the Lloyds bank’s services might be a great step towards

the future of automation and technological advancements, but it also brought along many

problems and challenges, not only for the banking group, but for its customers, shareholders,

employees and even many communities. The digital banking and transactions have provided

many customers with the comfort of managing their transactions from anywhere and at

anytime they like. But, it also caused many issues with people who are not much familiar with

the use of internet, mobile apps, etc. and even for people who have limited or no access to

these facilities(Abbasov, Mamedov and Aliev, 2019). Aged people, people from small towns

and remote areas, etc. have difficulty in managing their transactions digitally. Closure of

branches also impacted the lives of many employees as they lost their jobs which also invoked

its CSR. Hence, the bank should keep in mind the interest of all such customers and the

employees by managing the digitalisation of its banking services along with the running of its

bank branches at more locations. Branches at remote areas should not be shut down. The

banking group should maintain high street banking along with the online banking facilities so

that the interests of all categories of customers can be kept. The banks should also offer

incentives to its customers to stop them from switching to the rival banks. The bank should

also consider consulting with the local authorities and communities to understand their

perspective and opinion and try to act accordingly. Proper seminars and online sessions should

be organised to make the customers understand the effectiveness of online baking and also

sessions should be held for teaching the customers how to use the digital banking. These

tutorials should not be time limited as in these should be made available to the customers all

the time so that they can watch these anytime they need.

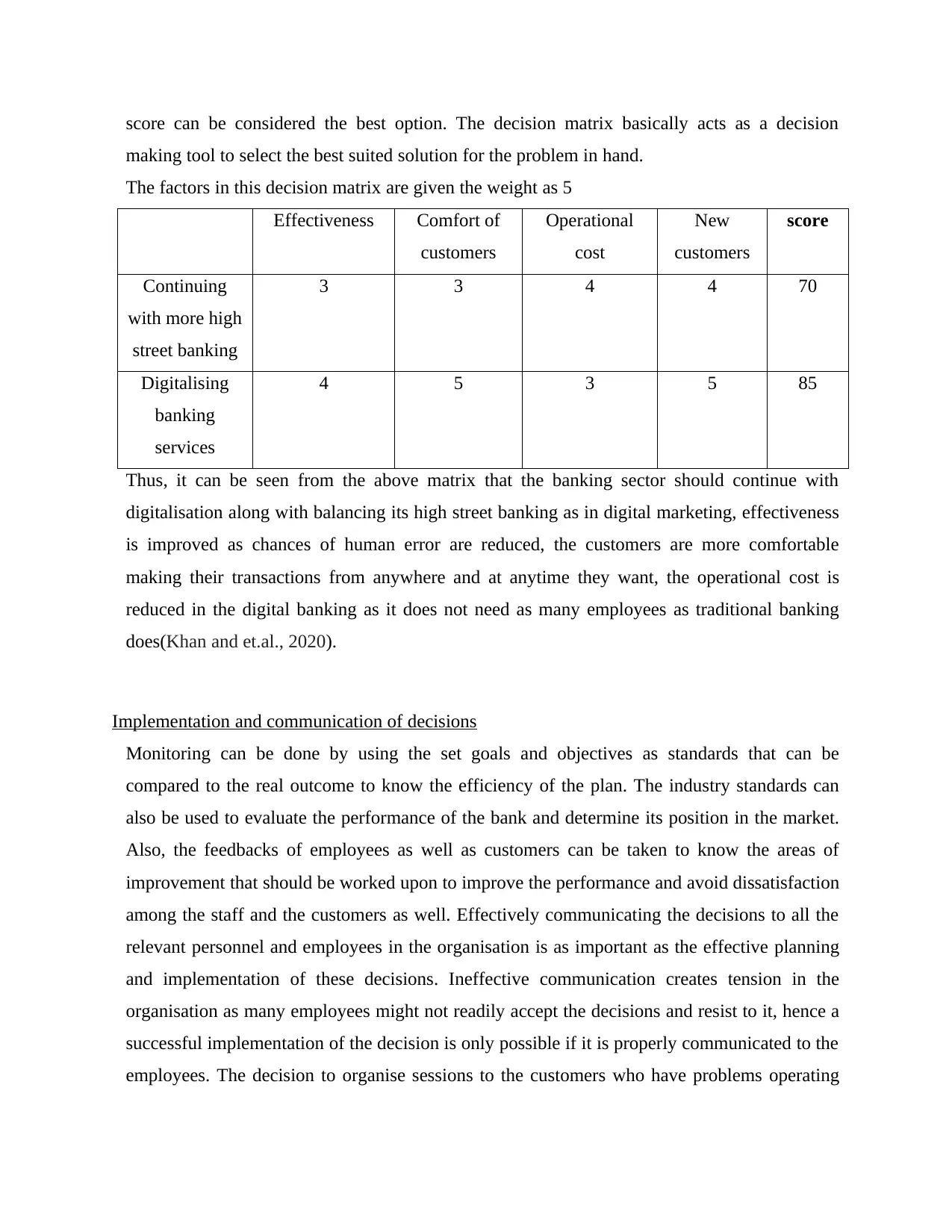

Decision making matrix to identify the best solution for the problem

A decision matrix helps to evaluate various options available as solutions and prioritize them

by identifying various factors and considering these factors using which scores are assigned to

the options and the best one among them is chosen to resolve the problem(Biasetti and De

Mori, 2021). This is done by assigning a weight to the various identified factors and then

ranking them using scores on the basis of their suitability. These scores are then multiplied

with the weights to calculate the weighted score. The weighted scores of all the factors are

summed up to reach the total score of the alternative. The alternative with the highest total

As it can be seen that digitalisation of the Lloyds bank’s services might be a great step towards

the future of automation and technological advancements, but it also brought along many

problems and challenges, not only for the banking group, but for its customers, shareholders,

employees and even many communities. The digital banking and transactions have provided

many customers with the comfort of managing their transactions from anywhere and at

anytime they like. But, it also caused many issues with people who are not much familiar with

the use of internet, mobile apps, etc. and even for people who have limited or no access to

these facilities(Abbasov, Mamedov and Aliev, 2019). Aged people, people from small towns

and remote areas, etc. have difficulty in managing their transactions digitally. Closure of

branches also impacted the lives of many employees as they lost their jobs which also invoked

its CSR. Hence, the bank should keep in mind the interest of all such customers and the

employees by managing the digitalisation of its banking services along with the running of its

bank branches at more locations. Branches at remote areas should not be shut down. The

banking group should maintain high street banking along with the online banking facilities so

that the interests of all categories of customers can be kept. The banks should also offer

incentives to its customers to stop them from switching to the rival banks. The bank should

also consider consulting with the local authorities and communities to understand their

perspective and opinion and try to act accordingly. Proper seminars and online sessions should

be organised to make the customers understand the effectiveness of online baking and also

sessions should be held for teaching the customers how to use the digital banking. These

tutorials should not be time limited as in these should be made available to the customers all

the time so that they can watch these anytime they need.

Decision making matrix to identify the best solution for the problem

A decision matrix helps to evaluate various options available as solutions and prioritize them

by identifying various factors and considering these factors using which scores are assigned to

the options and the best one among them is chosen to resolve the problem(Biasetti and De

Mori, 2021). This is done by assigning a weight to the various identified factors and then

ranking them using scores on the basis of their suitability. These scores are then multiplied

with the weights to calculate the weighted score. The weighted scores of all the factors are

summed up to reach the total score of the alternative. The alternative with the highest total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

score can be considered the best option. The decision matrix basically acts as a decision

making tool to select the best suited solution for the problem in hand.

The factors in this decision matrix are given the weight as 5

Effectiveness Comfort of

customers

Operational

cost

New

customers

score

Continuing

with more high

street banking

3 3 4 4 70

Digitalising

banking

services

4 5 3 5 85

Thus, it can be seen from the above matrix that the banking sector should continue with

digitalisation along with balancing its high street banking as in digital marketing, effectiveness

is improved as chances of human error are reduced, the customers are more comfortable

making their transactions from anywhere and at anytime they want, the operational cost is

reduced in the digital banking as it does not need as many employees as traditional banking

does(Khan and et.al., 2020).

Implementation and communication of decisions

Monitoring can be done by using the set goals and objectives as standards that can be

compared to the real outcome to know the efficiency of the plan. The industry standards can

also be used to evaluate the performance of the bank and determine its position in the market.

Also, the feedbacks of employees as well as customers can be taken to know the areas of

improvement that should be worked upon to improve the performance and avoid dissatisfaction

among the staff and the customers as well. Effectively communicating the decisions to all the

relevant personnel and employees in the organisation is as important as the effective planning

and implementation of these decisions. Ineffective communication creates tension in the

organisation as many employees might not readily accept the decisions and resist to it, hence a

successful implementation of the decision is only possible if it is properly communicated to the

employees. The decision to organise sessions to the customers who have problems operating

making tool to select the best suited solution for the problem in hand.

The factors in this decision matrix are given the weight as 5

Effectiveness Comfort of

customers

Operational

cost

New

customers

score

Continuing

with more high

street banking

3 3 4 4 70

Digitalising

banking

services

4 5 3 5 85

Thus, it can be seen from the above matrix that the banking sector should continue with

digitalisation along with balancing its high street banking as in digital marketing, effectiveness

is improved as chances of human error are reduced, the customers are more comfortable

making their transactions from anywhere and at anytime they want, the operational cost is

reduced in the digital banking as it does not need as many employees as traditional banking

does(Khan and et.al., 2020).

Implementation and communication of decisions

Monitoring can be done by using the set goals and objectives as standards that can be

compared to the real outcome to know the efficiency of the plan. The industry standards can

also be used to evaluate the performance of the bank and determine its position in the market.

Also, the feedbacks of employees as well as customers can be taken to know the areas of

improvement that should be worked upon to improve the performance and avoid dissatisfaction

among the staff and the customers as well. Effectively communicating the decisions to all the

relevant personnel and employees in the organisation is as important as the effective planning

and implementation of these decisions. Ineffective communication creates tension in the

organisation as many employees might not readily accept the decisions and resist to it, hence a

successful implementation of the decision is only possible if it is properly communicated to the

employees. The decision to organise sessions to the customers who have problems operating

the digital banking and recording various videos that could be used by these customers

whenever needed should be communicated to the employees.

whenever needed should be communicated to the employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abbasov, A. M., Mamedov, Z. F. and Aliev, S. A., 2019. Digitalization of the banking sector:

new challenges and prospects. Economics and Management. (6). pp.81-89.

Biasetti, P. and De Mori, B., 2021. The ethical matrix as a tool for decision-making process in

conservation. Frontiers in Environmental Science. 9. p.584636.

Druhova, V., Hirna, O. and Fostyak, V., 2021. A factor analysis of the impact of digitalisation

on the banking industry. Zeszyty Naukowe Uniwersytetu Ekonomicznego w

Krakowie/Cracow Review of Economics and Management. (1 (991)). pp.9-22.

Khan, M. J. and et.al., 2020. An adjustable weighted soft discernibility matrix based on

generalized picture fuzzy soft set and its applications in decision making. Journal of

Intelligent & Fuzzy Systems. 38(2). pp.2103-2118.

Tanda, A. and Schena, C. M., 2019. FinTech, BigTech and banks: Digitalisation and its impact

on banking business models. Springer.

Zabala Aguayo, F. and Ślusarczyk, B., 2020. Risks of banking services’ digitalization: The

practice of diversification and sustainable development goals. Sustainability. 12(10).

p.4040.

Online

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.swotandpestle.com/lloyds-banking-group/ >

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.mbaskool.com/brandguide/banking-and-financial-services/1273-lloyds-

tsb-bank.html>

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.marketresearch.com/MarketLine-v3883/Lloyds-Bank-Plc-Strategy-

SWOT-31478947/>

PESTLE analysis of Lloyds banking group. 2022. Available through:<

https://www.case48.com/pestel-analysis/3182-Lloyds-Banking-Group-plc >

PESTLE analysis of Lloyds banking group. 2022. Available through:<

https://embapro.com/frontpage/pestelcoanalysis/17667-lloyds-banking >

PESTLE analysis of Lloyds bank. 2021. Available through:<

https://www.bartleby.com/essay/Pestle-Raport-Lloyds-Banking-Group-FKE7MS8K86VA>

Books and Journals

Abbasov, A. M., Mamedov, Z. F. and Aliev, S. A., 2019. Digitalization of the banking sector:

new challenges and prospects. Economics and Management. (6). pp.81-89.

Biasetti, P. and De Mori, B., 2021. The ethical matrix as a tool for decision-making process in

conservation. Frontiers in Environmental Science. 9. p.584636.

Druhova, V., Hirna, O. and Fostyak, V., 2021. A factor analysis of the impact of digitalisation

on the banking industry. Zeszyty Naukowe Uniwersytetu Ekonomicznego w

Krakowie/Cracow Review of Economics and Management. (1 (991)). pp.9-22.

Khan, M. J. and et.al., 2020. An adjustable weighted soft discernibility matrix based on

generalized picture fuzzy soft set and its applications in decision making. Journal of

Intelligent & Fuzzy Systems. 38(2). pp.2103-2118.

Tanda, A. and Schena, C. M., 2019. FinTech, BigTech and banks: Digitalisation and its impact

on banking business models. Springer.

Zabala Aguayo, F. and Ślusarczyk, B., 2020. Risks of banking services’ digitalization: The

practice of diversification and sustainable development goals. Sustainability. 12(10).

p.4040.

Online

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.swotandpestle.com/lloyds-banking-group/ >

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.mbaskool.com/brandguide/banking-and-financial-services/1273-lloyds-

tsb-bank.html>

SWOT analysis of Lloyds banking group. 2022. Available through:<

https://www.marketresearch.com/MarketLine-v3883/Lloyds-Bank-Plc-Strategy-

SWOT-31478947/>

PESTLE analysis of Lloyds banking group. 2022. Available through:<

https://www.case48.com/pestel-analysis/3182-Lloyds-Banking-Group-plc >

PESTLE analysis of Lloyds banking group. 2022. Available through:<

https://embapro.com/frontpage/pestelcoanalysis/17667-lloyds-banking >

PESTLE analysis of Lloyds bank. 2021. Available through:<

https://www.bartleby.com/essay/Pestle-Raport-Lloyds-Banking-Group-FKE7MS8K86VA>

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.