Comprehensive Report: Loan Application Process and Documentation

VerifiedAdded on 2022/12/29

|29

|4634

|54

Report

AI Summary

This report meticulously details the loan application process, starting from the initial contact with a client and proceeding through to settlement. It outlines the necessary documentation, including credit guides, privacy statements, client needs assessments, and combined credit quotes. The report also covers the process of application for credit, including serviceability calculations, income and savings verification, and valuation evidence. Furthermore, it examines anti-money laundering and counter-terrorism financing requirements, compliance checklists, and the completion of customer files and databases. The report emphasizes the importance of accurate documentation, credit assessment, and adherence to regulatory guidelines, providing a comprehensive overview of the loan application workflow.

Loan Application

Process Assessment

Process Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1: ...................................................................................................................................1

File notes from first contact through to settlement in chronological order............................1

Authorised Credit Representative Credit Guide and Licensee Credit Guide.........................2

Privacy Statement and Consent form.....................................................................................2

Client Needs Review or Fact Find..........................................................................................3

Combined Credit Quote and Proposal....................................................................................3

Product Comparison Report Preliminary Assessment...........................................................3

Costing sheet for Fees and Charges........................................................................................4

Fully completed Lender Loan Application or Copy of Online lodgement............................5

Lender’s loan Document Check List .....................................................................................6

Task 2: Process application for credit....................................................................................8

A completed serviceability calculator (refer to useful resources)

................................................................................................................................................8

Loan Comments/Lender Comments.......................................................................................8

Evidence of Income ...............................................................................................................8

Evidence of savings/equity and other loan commitments....................................................17

Evidence of Valuation successfully completed....................................................................17

Anti-Money Laundering/Counter Terrorism Financing ID requirements............................22

A Compliance file checklist.................................................................................................22

Task 3: Completing customer file........................................................................................24

Task 4: Customer /referrer data base ...................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

........................................................................................................................................................27

APPENDICES...............................................................................................................................28

AAMC TRAINING DOCUMENT CHECKLIST...............................................................28

.......................................................................................................................................................29

Task 1: ...................................................................................................................................1

File notes from first contact through to settlement in chronological order............................1

Authorised Credit Representative Credit Guide and Licensee Credit Guide.........................2

Privacy Statement and Consent form.....................................................................................2

Client Needs Review or Fact Find..........................................................................................3

Combined Credit Quote and Proposal....................................................................................3

Product Comparison Report Preliminary Assessment...........................................................3

Costing sheet for Fees and Charges........................................................................................4

Fully completed Lender Loan Application or Copy of Online lodgement............................5

Lender’s loan Document Check List .....................................................................................6

Task 2: Process application for credit....................................................................................8

A completed serviceability calculator (refer to useful resources)

................................................................................................................................................8

Loan Comments/Lender Comments.......................................................................................8

Evidence of Income ...............................................................................................................8

Evidence of savings/equity and other loan commitments....................................................17

Evidence of Valuation successfully completed....................................................................17

Anti-Money Laundering/Counter Terrorism Financing ID requirements............................22

A Compliance file checklist.................................................................................................22

Task 3: Completing customer file........................................................................................24

Task 4: Customer /referrer data base ...................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

........................................................................................................................................................27

APPENDICES...............................................................................................................................28

AAMC TRAINING DOCUMENT CHECKLIST...............................................................28

.......................................................................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Everybody in this world needs loan for something or the other in their life. This loan

taking process can be used to fulfil their needs. The individual has to verify various different

documents that the bank is asking if they don't fulfil it the bank will not give them loan. Another

major requirement that the banks nowadays are asking the credit score of the individual. In this

report the individual is needing the loan for building his house.

MAIN BODY

Task 1:

FHOGs is an abbreviation for First Home Owner Grant and it is a scheme that was

founded in 1 July 2000. This was set up in order to offset the effects of GST on Home

Ownership. It is to be considered as a national scheme that is funded by an accumulation of

territories and states and are being administered in accordance to their own legislature.

There has been a substantial decline in the affordability criteria in the housing market of

Australia. This problem of affordability is more excruciating for the first-time buyers and

therefore in order to mitigate this FHOGs are introduced. Any fluctuations in these criteria will

result in the hike of prices for the first-time buyers. And therefore, houses might exceed their

affordability criteria.

File notes from first contact through to settlement in chronological order

The notes taken in the first interaction by the broker associated with the eligible criteria of the

client will revolve around:

1. In order to check the eligibility criteria for loan the credit score of the concerned client

was 750 and therefore he as eligible for the loan.

2. The salary slip of client was taken into consideration in order to make sure that he has

frequent income flow.

3. In order to make sure that the client is eligible for paying the principal amount of the loan

along with the interest, his income was taken into consideration.

4. Client's legal record was also looked at.

Everybody in this world needs loan for something or the other in their life. This loan

taking process can be used to fulfil their needs. The individual has to verify various different

documents that the bank is asking if they don't fulfil it the bank will not give them loan. Another

major requirement that the banks nowadays are asking the credit score of the individual. In this

report the individual is needing the loan for building his house.

MAIN BODY

Task 1:

FHOGs is an abbreviation for First Home Owner Grant and it is a scheme that was

founded in 1 July 2000. This was set up in order to offset the effects of GST on Home

Ownership. It is to be considered as a national scheme that is funded by an accumulation of

territories and states and are being administered in accordance to their own legislature.

There has been a substantial decline in the affordability criteria in the housing market of

Australia. This problem of affordability is more excruciating for the first-time buyers and

therefore in order to mitigate this FHOGs are introduced. Any fluctuations in these criteria will

result in the hike of prices for the first-time buyers. And therefore, houses might exceed their

affordability criteria.

File notes from first contact through to settlement in chronological order

The notes taken in the first interaction by the broker associated with the eligible criteria of the

client will revolve around:

1. In order to check the eligibility criteria for loan the credit score of the concerned client

was 750 and therefore he as eligible for the loan.

2. The salary slip of client was taken into consideration in order to make sure that he has

frequent income flow.

3. In order to make sure that the client is eligible for paying the principal amount of the loan

along with the interest, his income was taken into consideration.

4. Client's legal record was also looked at.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Authorised Credit Representative Credit Guide and Licensee Credit Guide

The guide for the home loan revolves around the aforementioned steps.

Privacy Statement and Consent form

The privacy statement and content form are as follows:

Consent form revolves around making sure the client is compatible with the terms and

conditions of the loan provider. It helps in having a clarity in the contract.

Client Needs Review or Fact Find

1. Client needs the loan because the affordability structure of the marketplace is higher than

the client's savings.

2. The option of loan is taken into consideration because the client does not have to pay the

whole amount of loan at once. He can distribute that amount and pay it in instalments

over a fixed period of time.

3. Since the client is buying a house for the very first time, the prices of house is not

compatible with his pay-out structure.

The guide for the home loan revolves around the aforementioned steps.

Privacy Statement and Consent form

The privacy statement and content form are as follows:

Consent form revolves around making sure the client is compatible with the terms and

conditions of the loan provider. It helps in having a clarity in the contract.

Client Needs Review or Fact Find

1. Client needs the loan because the affordability structure of the marketplace is higher than

the client's savings.

2. The option of loan is taken into consideration because the client does not have to pay the

whole amount of loan at once. He can distribute that amount and pay it in instalments

over a fixed period of time.

3. Since the client is buying a house for the very first time, the prices of house is not

compatible with his pay-out structure.

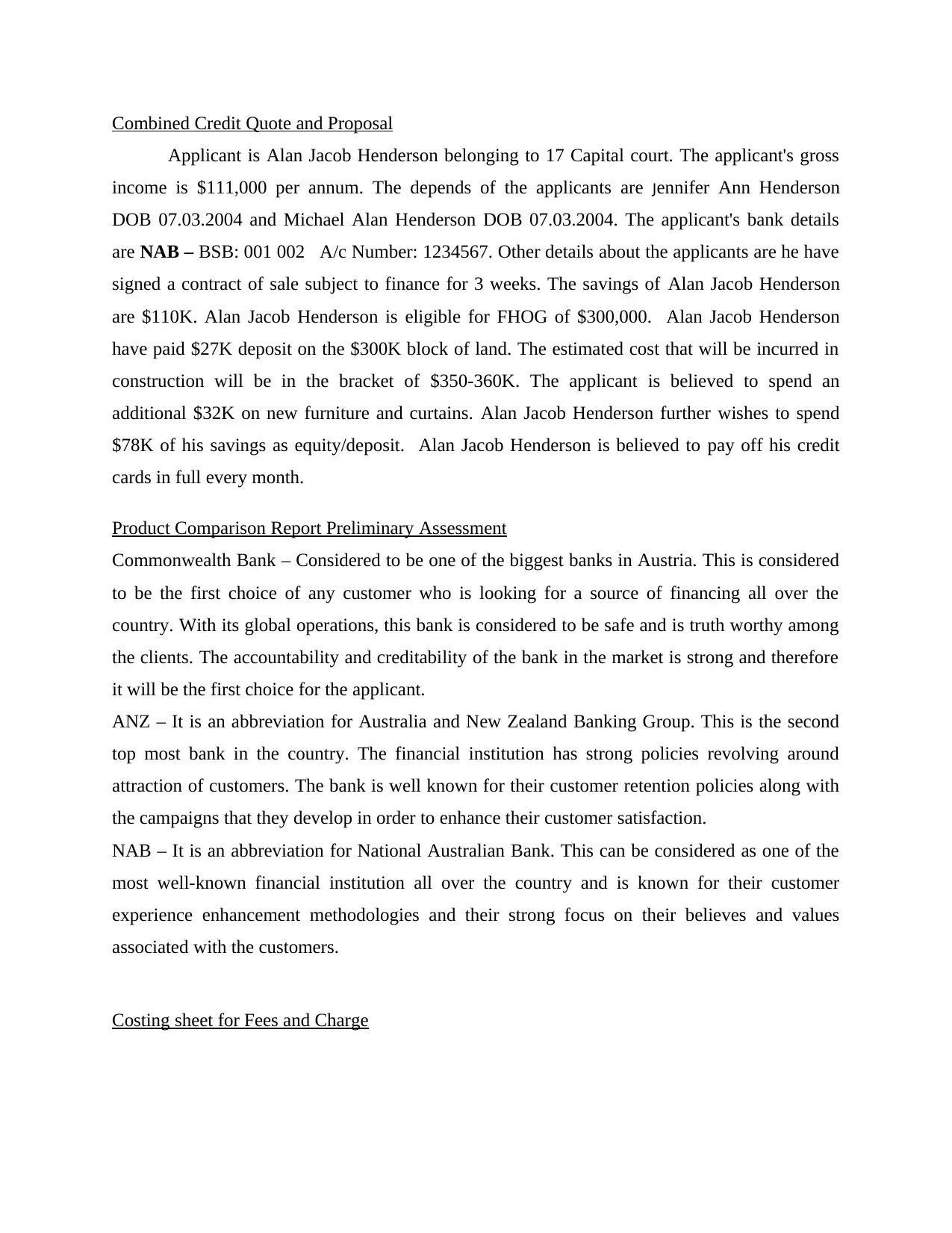

Combined Credit Quote and Proposal

Applicant is Alan Jacob Henderson belonging to 17 Capital court. The applicant's gross

income is $111,000 per annum. The depends of the applicants are Jennifer Ann Henderson

DOB 07.03.2004 and Michael Alan Henderson DOB 07.03.2004. The applicant's bank details

are NAB – BSB: 001 002 A/c Number: 1234567. Other details about the applicants are he have

signed a contract of sale subject to finance for 3 weeks. The savings of Alan Jacob Henderson

are $110K. Alan Jacob Henderson is eligible for FHOG of $300,000. Alan Jacob Henderson

have paid $27K deposit on the $300K block of land. The estimated cost that will be incurred in

construction will be in the bracket of $350-360K. The applicant is believed to spend an

additional $32K on new furniture and curtains. Alan Jacob Henderson further wishes to spend

$78K of his savings as equity/deposit. Alan Jacob Henderson is believed to pay off his credit

cards in full every month.

Product Comparison Report Preliminary Assessment

Commonwealth Bank – Considered to be one of the biggest banks in Austria. This is considered

to be the first choice of any customer who is looking for a source of financing all over the

country. With its global operations, this bank is considered to be safe and is truth worthy among

the clients. The accountability and creditability of the bank in the market is strong and therefore

it will be the first choice for the applicant.

ANZ – It is an abbreviation for Australia and New Zealand Banking Group. This is the second

top most bank in the country. The financial institution has strong policies revolving around

attraction of customers. The bank is well known for their customer retention policies along with

the campaigns that they develop in order to enhance their customer satisfaction.

NAB – It is an abbreviation for National Australian Bank. This can be considered as one of the

most well-known financial institution all over the country and is known for their customer

experience enhancement methodologies and their strong focus on their believes and values

associated with the customers.

Costing sheet for Fees and Charge

Applicant is Alan Jacob Henderson belonging to 17 Capital court. The applicant's gross

income is $111,000 per annum. The depends of the applicants are Jennifer Ann Henderson

DOB 07.03.2004 and Michael Alan Henderson DOB 07.03.2004. The applicant's bank details

are NAB – BSB: 001 002 A/c Number: 1234567. Other details about the applicants are he have

signed a contract of sale subject to finance for 3 weeks. The savings of Alan Jacob Henderson

are $110K. Alan Jacob Henderson is eligible for FHOG of $300,000. Alan Jacob Henderson

have paid $27K deposit on the $300K block of land. The estimated cost that will be incurred in

construction will be in the bracket of $350-360K. The applicant is believed to spend an

additional $32K on new furniture and curtains. Alan Jacob Henderson further wishes to spend

$78K of his savings as equity/deposit. Alan Jacob Henderson is believed to pay off his credit

cards in full every month.

Product Comparison Report Preliminary Assessment

Commonwealth Bank – Considered to be one of the biggest banks in Austria. This is considered

to be the first choice of any customer who is looking for a source of financing all over the

country. With its global operations, this bank is considered to be safe and is truth worthy among

the clients. The accountability and creditability of the bank in the market is strong and therefore

it will be the first choice for the applicant.

ANZ – It is an abbreviation for Australia and New Zealand Banking Group. This is the second

top most bank in the country. The financial institution has strong policies revolving around

attraction of customers. The bank is well known for their customer retention policies along with

the campaigns that they develop in order to enhance their customer satisfaction.

NAB – It is an abbreviation for National Australian Bank. This can be considered as one of the

most well-known financial institution all over the country and is known for their customer

experience enhancement methodologies and their strong focus on their believes and values

associated with the customers.

Costing sheet for Fees and Charge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

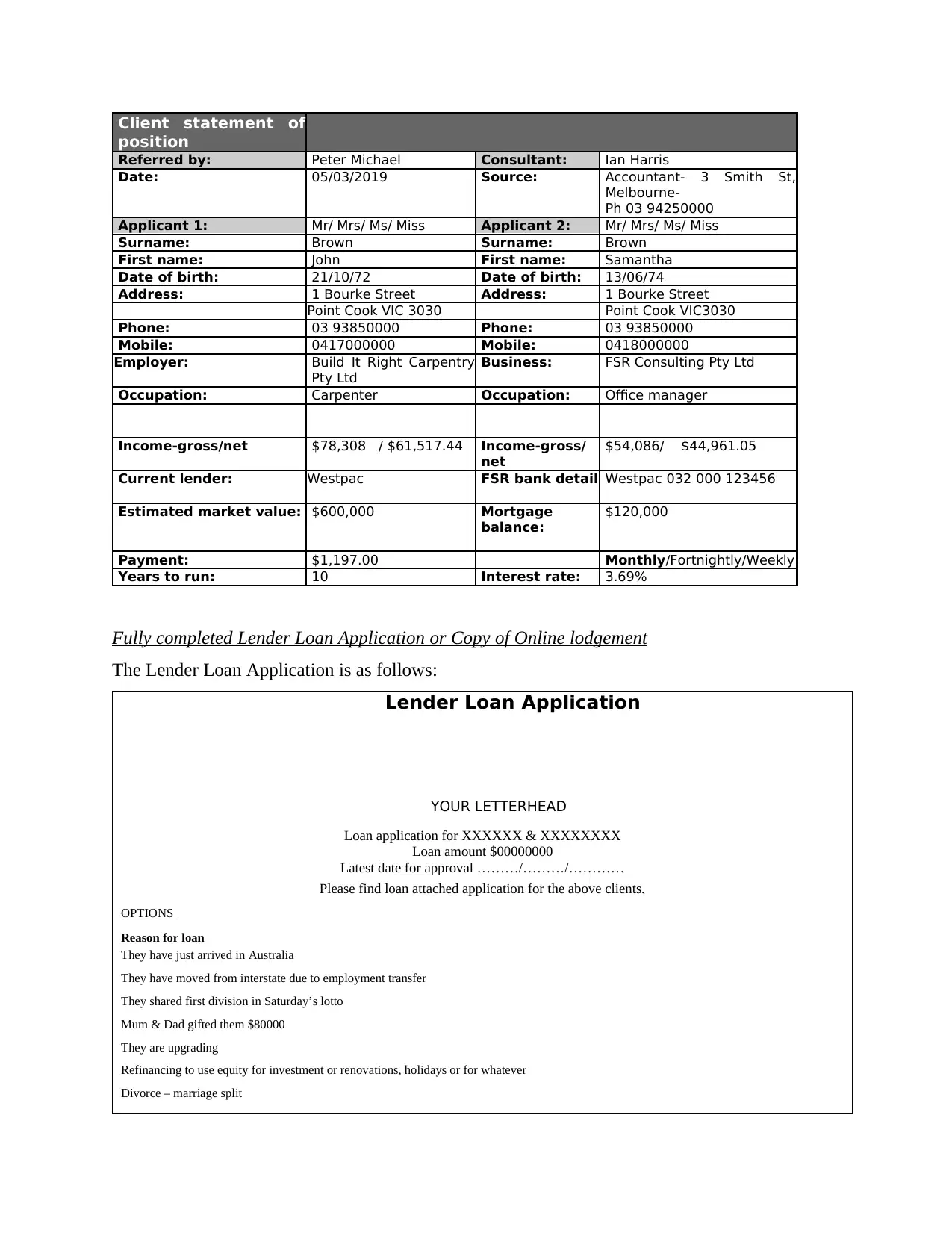

Client statement of

position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/

net

$54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market value: $600,000 Mortgage

balance:

$120,000

Payment: $1,197.00 Monthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Fully completed Lender Loan Application or Copy of Online lodgement

The Lender Loan Application is as follows:

Lender Loan Application

YOUR LETTERHEAD

Loan application for XXXXXX & XXXXXXXX

Loan amount $00000000

Latest date for approval ………/………/…………

Please find loan attached application for the above clients.

OPTIONS

Reason for loan

They have just arrived in Australia

They have moved from interstate due to employment transfer

They shared first division in Saturday’s lotto

Mum & Dad gifted them $80000

They are upgrading

Refinancing to use equity for investment or renovations, holidays or for whatever

Divorce – marriage split

position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/

net

$54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market value: $600,000 Mortgage

balance:

$120,000

Payment: $1,197.00 Monthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Fully completed Lender Loan Application or Copy of Online lodgement

The Lender Loan Application is as follows:

Lender Loan Application

YOUR LETTERHEAD

Loan application for XXXXXX & XXXXXXXX

Loan amount $00000000

Latest date for approval ………/………/…………

Please find loan attached application for the above clients.

OPTIONS

Reason for loan

They have just arrived in Australia

They have moved from interstate due to employment transfer

They shared first division in Saturday’s lotto

Mum & Dad gifted them $80000

They are upgrading

Refinancing to use equity for investment or renovations, holidays or for whatever

Divorce – marriage split

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

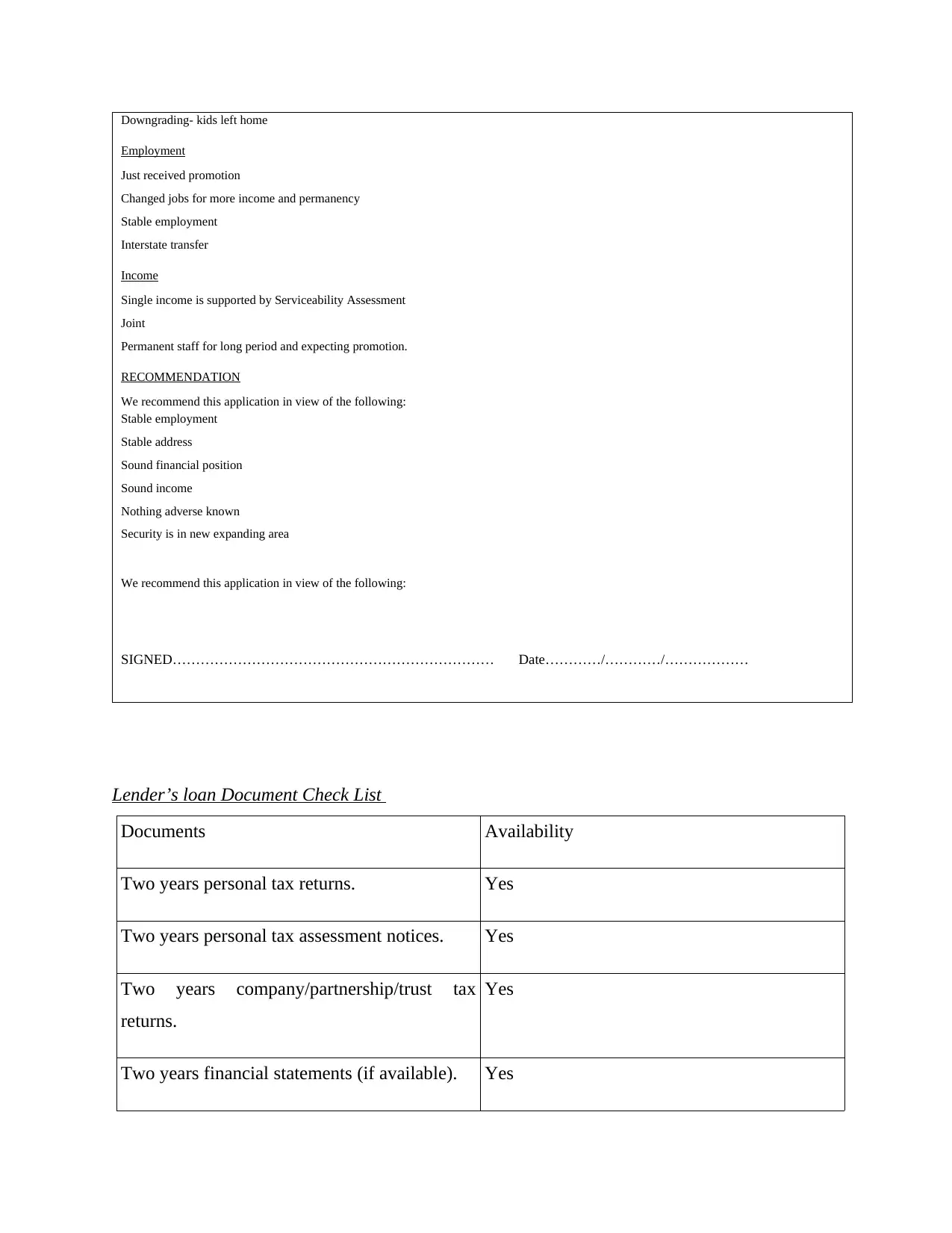

Downgrading- kids left home

Employment

Just received promotion

Changed jobs for more income and permanency

Stable employment

Interstate transfer

Income

Single income is supported by Serviceability Assessment

Joint

Permanent staff for long period and expecting promotion.

RECOMMENDATION

We recommend this application in view of the following:

Stable employment

Stable address

Sound financial position

Sound income

Nothing adverse known

Security is in new expanding area

We recommend this application in view of the following:

SIGNED…………………………………………………………… Date…………/…………/………………

Lender’s loan Document Check List

Documents Availability

Two years personal tax returns. Yes

Two years personal tax assessment notices. Yes

Two years company/partnership/trust tax

returns.

Yes

Two years financial statements (if available). Yes

Employment

Just received promotion

Changed jobs for more income and permanency

Stable employment

Interstate transfer

Income

Single income is supported by Serviceability Assessment

Joint

Permanent staff for long period and expecting promotion.

RECOMMENDATION

We recommend this application in view of the following:

Stable employment

Stable address

Sound financial position

Sound income

Nothing adverse known

Security is in new expanding area

We recommend this application in view of the following:

SIGNED…………………………………………………………… Date…………/…………/………………

Lender’s loan Document Check List

Documents Availability

Two years personal tax returns. Yes

Two years personal tax assessment notices. Yes

Two years company/partnership/trust tax

returns.

Yes

Two years financial statements (if available). Yes

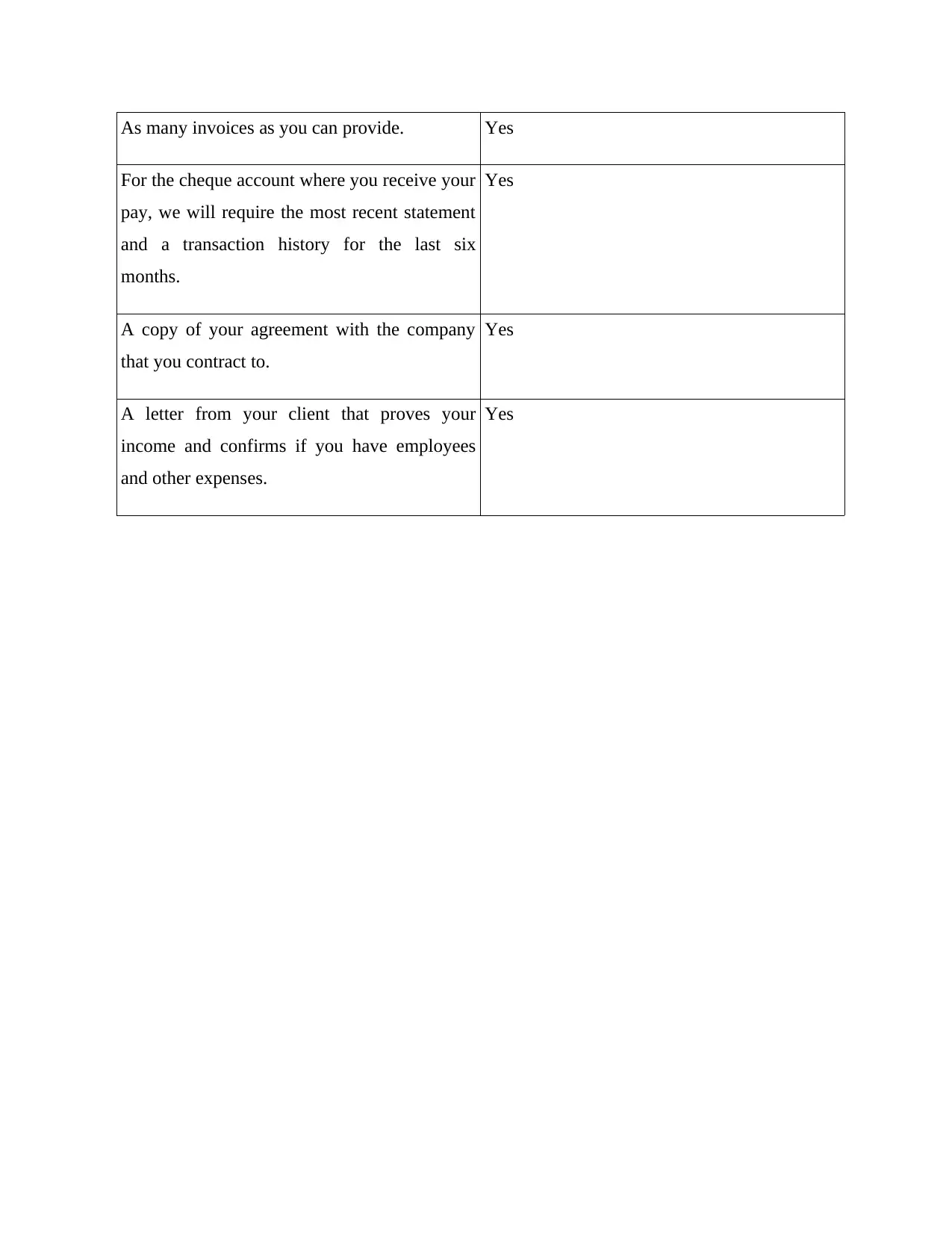

As many invoices as you can provide. Yes

For the cheque account where you receive your

pay, we will require the most recent statement

and a transaction history for the last six

months.

Yes

A copy of your agreement with the company

that you contract to.

Yes

A letter from your client that proves your

income and confirms if you have employees

and other expenses.

Yes

For the cheque account where you receive your

pay, we will require the most recent statement

and a transaction history for the last six

months.

Yes

A copy of your agreement with the company

that you contract to.

Yes

A letter from your client that proves your

income and confirms if you have employees

and other expenses.

Yes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2: Process application for credit.

Loan Comments/Lender Comments

This part covers the information about the loan comments from the manager as the

documents needed for the loan application is complete and applicant is eligible for taking the

loan. The procedure of the loan includes several documents such as the bank statement or income

statement and the information regarding the nationality of the applicant to make sure that

applicant belongs to the Australia and applicant is the citizen of Australia (Chuang et al 2018).

In order to complete the loan procedure these documents in particular is needed first of all the

document which is needed to apply for the housing loan is the amount of loan which is required

by the applicant after that applicant have to mention its income and provide its annual income

statement to the bank which helps bank to determine that applicant is capable or not to repay the

loan. Next document which is important to complete the procedure is the identity of the applicant

in order to make sure that the applicant belongs from Australia and not committing any type of

fraud with the bank. There are documents required by the bank for the current property of

applicant and the proof of residence is also mandatory for the applicant to submit to the bank.

The other documents which is needed by the bank is the proof of age and the photographs of the

applicant in order to prepare the application (Ebekozien et al 2018). At last the employee of the

member checks all the mandatory documents and it's authenticity and after cross checking all the

documents loan is sanctioned to the applicant and provided to the applicant in the instalments.

Evidence of Income

The applicant's pay slip is as follows:

FSR Consulting PVT Ltd

PAYSLIP

ABN: 11 123 456 789

ACN: 123 456 789

1 King Street, Melbourne VIC 3000

Employee ID: 5245 Bookkeeper

Loan Comments/Lender Comments

This part covers the information about the loan comments from the manager as the

documents needed for the loan application is complete and applicant is eligible for taking the

loan. The procedure of the loan includes several documents such as the bank statement or income

statement and the information regarding the nationality of the applicant to make sure that

applicant belongs to the Australia and applicant is the citizen of Australia (Chuang et al 2018).

In order to complete the loan procedure these documents in particular is needed first of all the

document which is needed to apply for the housing loan is the amount of loan which is required

by the applicant after that applicant have to mention its income and provide its annual income

statement to the bank which helps bank to determine that applicant is capable or not to repay the

loan. Next document which is important to complete the procedure is the identity of the applicant

in order to make sure that the applicant belongs from Australia and not committing any type of

fraud with the bank. There are documents required by the bank for the current property of

applicant and the proof of residence is also mandatory for the applicant to submit to the bank.

The other documents which is needed by the bank is the proof of age and the photographs of the

applicant in order to prepare the application (Ebekozien et al 2018). At last the employee of the

member checks all the mandatory documents and it's authenticity and after cross checking all the

documents loan is sanctioned to the applicant and provided to the applicant in the instalments.

Evidence of Income

The applicant's pay slip is as follows:

FSR Consulting PVT Ltd

PAYSLIP

ABN: 11 123 456 789

ACN: 123 456 789

1 King Street, Melbourne VIC 3000

Employee ID: 5245 Bookkeeper

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

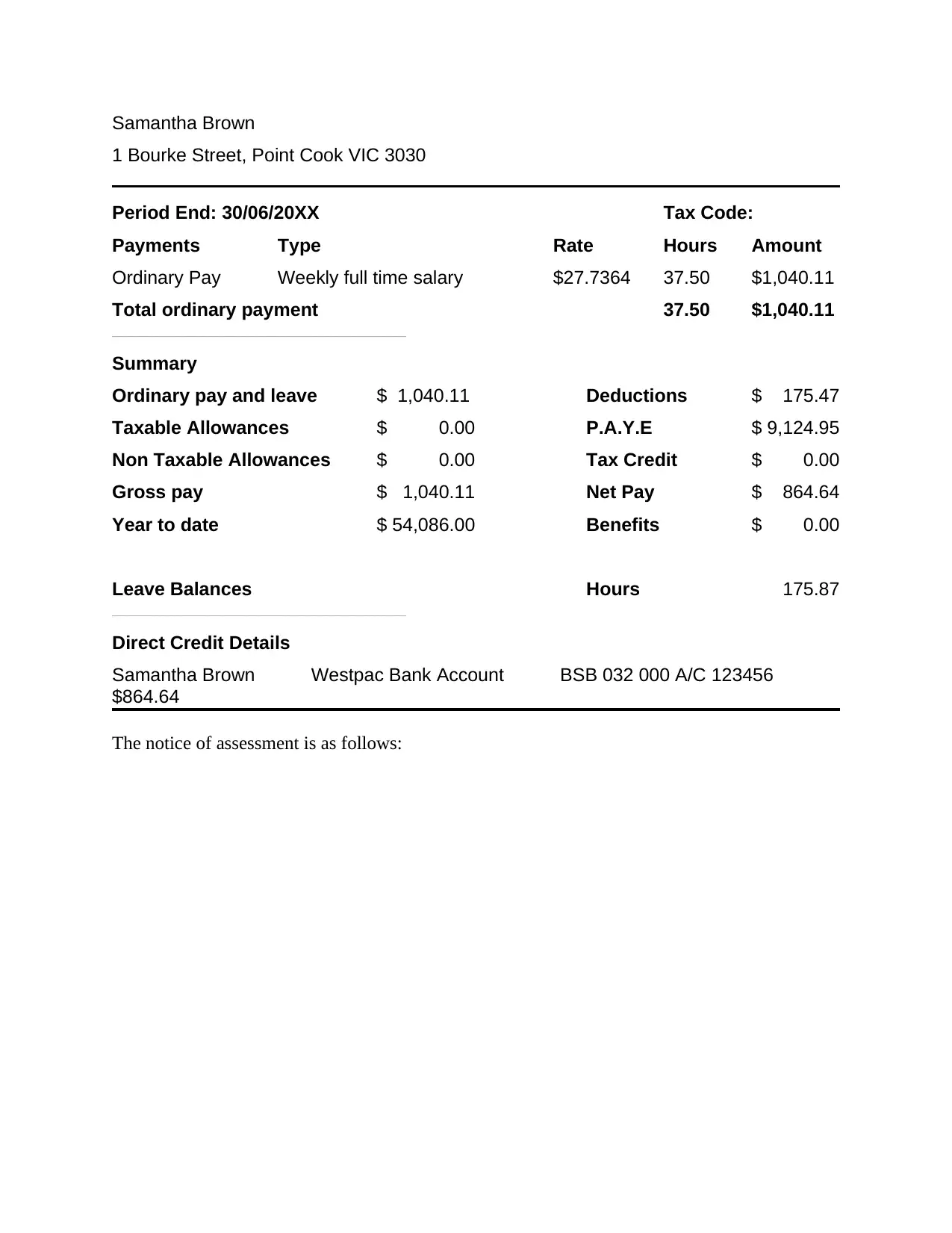

Samantha Brown

1 Bourke Street, Point Cook VIC 3030

Period End: 30/06/20XX Tax Code:

Payments Type Rate Hours Amount

Ordinary Pay Weekly full time salary $27.7364 37.50 $1,040.11

Total ordinary payment 37.50 $1,040.11

_____________________________________________________________________________________

Summary

Ordinary pay and leave $ 1,040.11 Deductions $ 175.47

Taxable Allowances $ 0.00 P.A.Y.E $ 9,124.95

Non Taxable Allowances $ 0.00 Tax Credit $ 0.00

Gross pay $ 1,040.11 Net Pay $ 864.64

Year to date $ 54,086.00 Benefits $ 0.00

Leave Balances Hours 175.87

_____________________________________________________________________________________

Direct Credit Details

Samantha Brown Westpac Bank Account BSB 032 000 A/C 123456

$864.64

The notice of assessment is as follows:

1 Bourke Street, Point Cook VIC 3030

Period End: 30/06/20XX Tax Code:

Payments Type Rate Hours Amount

Ordinary Pay Weekly full time salary $27.7364 37.50 $1,040.11

Total ordinary payment 37.50 $1,040.11

_____________________________________________________________________________________

Summary

Ordinary pay and leave $ 1,040.11 Deductions $ 175.47

Taxable Allowances $ 0.00 P.A.Y.E $ 9,124.95

Non Taxable Allowances $ 0.00 Tax Credit $ 0.00

Gross pay $ 1,040.11 Net Pay $ 864.64

Year to date $ 54,086.00 Benefits $ 0.00

Leave Balances Hours 175.87

_____________________________________________________________________________________

Direct Credit Details

Samantha Brown Westpac Bank Account BSB 032 000 A/C 123456

$864.64

The notice of assessment is as follows:

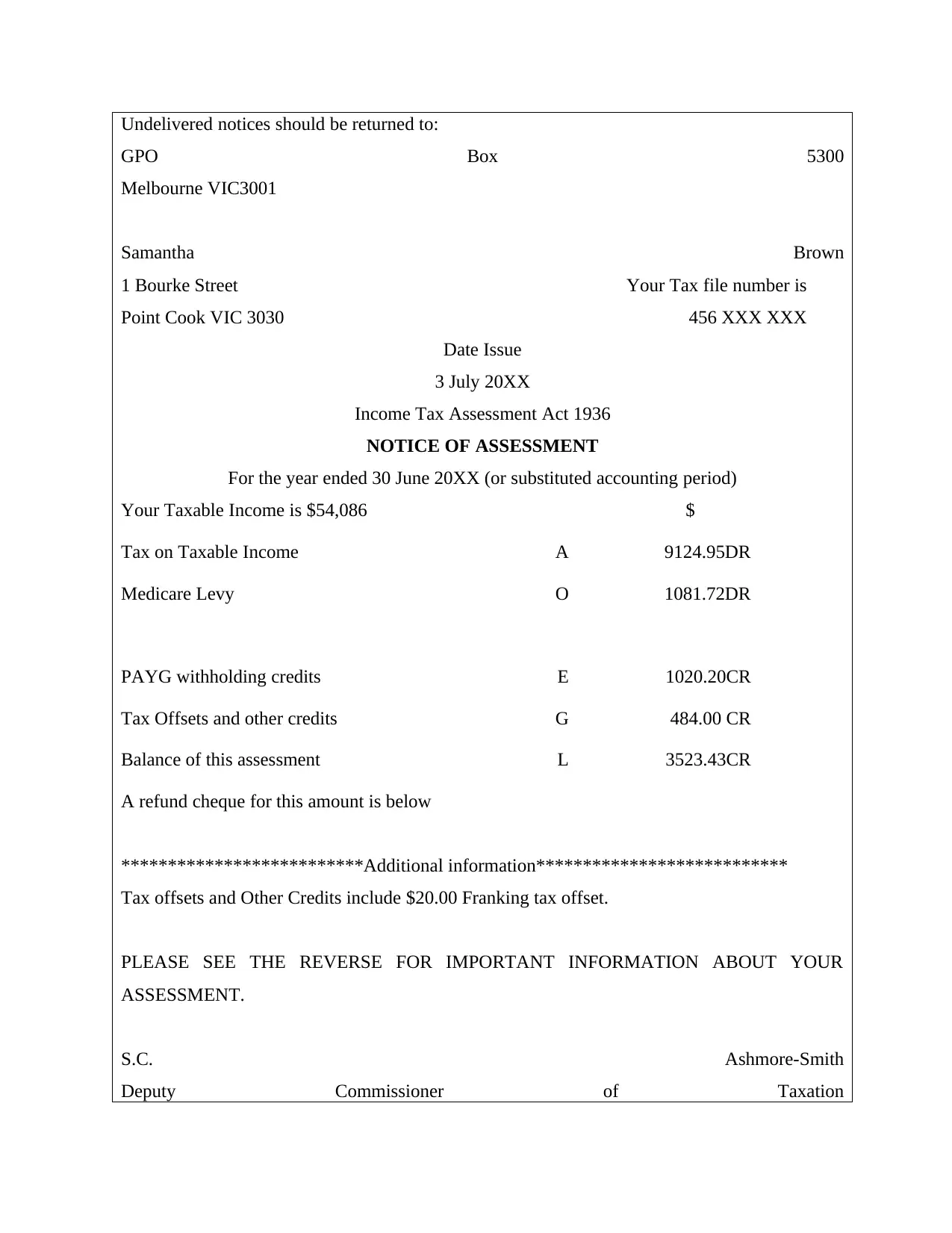

Undelivered notices should be returned to:

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR

ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR

ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.