Loan Application Process: Case Study, Guidelines, and Database

VerifiedAdded on 2020/07/23

|11

|1407

|194

Report

AI Summary

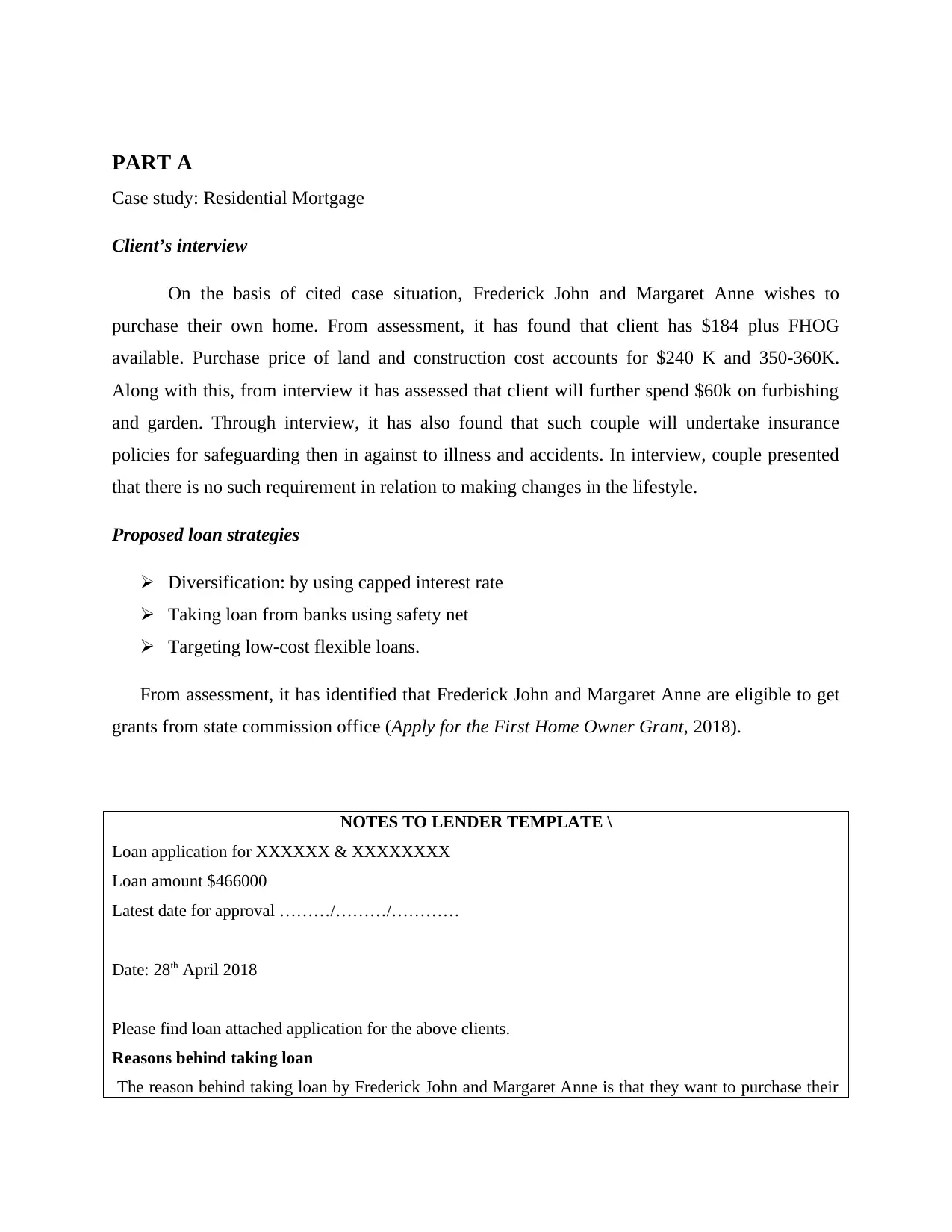

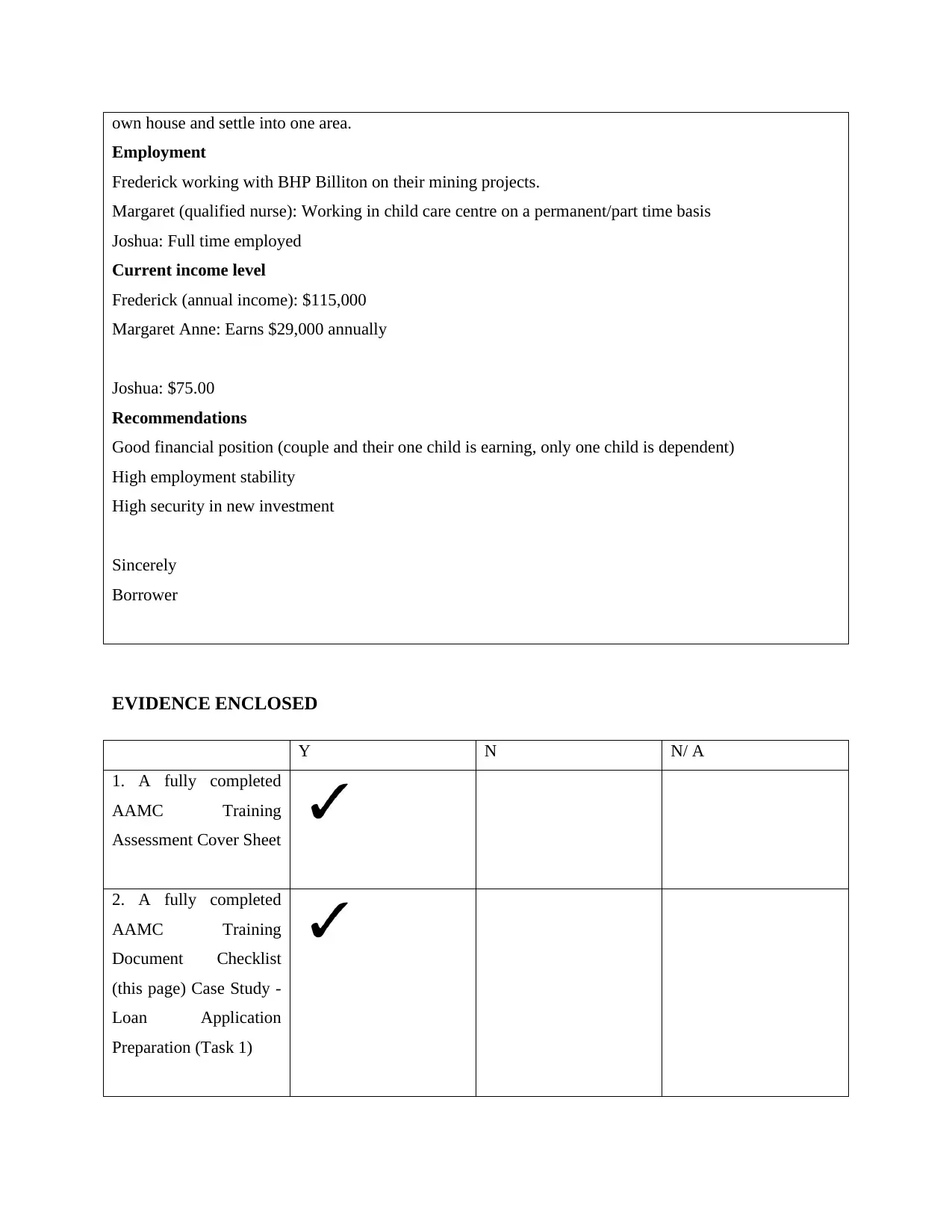

This report provides a comprehensive overview of the loan application process, utilizing a case study involving a couple seeking a residential mortgage. It details the couple's financial situation, loan strategies, and eligibility for grants. The report includes a notes to lender template, outlining loan details and required documentation. Furthermore, it examines lender mortgage insurer guidelines, specifically loan-to-value ratios and maximum loan amounts. The report emphasizes the importance of responsible lending conduct, referencing the National Consumer Credit Protection Act 2009. It also covers the completion of a customer file, including contact records, advice of loan approval, document sign-up, and advice of transaction completion. Finally, the report discusses database management, professional relationship development, and promotional strategies for business growth. The report is well-structured, providing a clear understanding of the loan application process from start to finish, including all necessary documentation and regulatory considerations.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.