Dissertation: Loan Loss Experience of SIBs in Sri Lanka Over Ten Years

VerifiedAdded on 2023/06/10

|12

|3399

|446

Dissertation

AI Summary

This dissertation investigates the loan loss experience of Systemically Important Banks (SIBs) in Sri Lanka over the past ten years. It explores the magnitude of loan losses and their impact on bank profitability. The research includes an introduction to the Sri Lankan banking sector, a review of relevant literature on loan loss provisions, and a detailed methodology, including the adoption of a pragmatism research philosophy and a correlational research design. The study aims to answer research questions about the disadvantages of loan loss provisions, the loan loss scenario over the past decade, and the effect on SIBs' profitability. The research will employ both qualitative and quantitative methods to gain a comprehensive understanding of the issue. The study also includes a null and alternative hypothesis to determine the impact of loan loss experience on the SIBs’ profit levels. The findings are expected to provide valuable insights into the financial health of Sri Lankan banks and the broader economy.

Running head: RESEARCH PROPOSAL

Loan Loss Experience over the Last Ten Years in Systemically Important Banks in Sri Lanka

Name of the Student:

Name of the University:

Author note:

Loan Loss Experience over the Last Ten Years in Systemically Important Banks in Sri Lanka

Name of the Student:

Name of the University:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1DISSERTATION

Topic: Loan Loss Experience over the Last Ten Years in Systemically Important Banks in

Sri Lanka

Introduction

Sri Lanka is a developing agricultural country in the South Asian region. The banking

sector of the nation is supervised by the Bank Supervision Department of the Central Bank of Sri

Lanka. The Central Bank has categorized the banks into two different categories, namely,

Licensed Commercial Banks (LCBs) and Licensed Specialized banks (LSBs). However, the

LCBs play a significant role in shaping the financial condition of the Sri Lankan economy due to

their base of the assets and magnitude of the services provided. These LCBs dominate the

financial market of Sri Lanka and thus have successfully captured the greatest share of the entire

financial system of the nation by controlling the payment cycle. Therefore, the health of the

financial system of the Sri Lankan economy is dependent largely on the performance as well as

the financial strength of the six biggest LCBs and hence, they are referred to as the Systemically

Important Banks (SIBs). The LSBs do not have any major intermediary role in the payment cycle

and thus have relatively lower systemic importance, in terms of size and influence on the

financial system in the economy (Cbsl.gov.lk 2018).

It has been found that, the LCBs or SIBs have been facing a challenge in the past decade

that has been hampering their performances. The country’s economy is heavily burdened with

great amount of loan loss or non-performing loans for the last ten years. Due to this provision,

the LCBs suffer from fall in profit. According to a report by EconomyNext, in March 2017

quarter, the profits of the National Developmental Bank of Sri Lanka grew 35% than the

Topic: Loan Loss Experience over the Last Ten Years in Systemically Important Banks in

Sri Lanka

Introduction

Sri Lanka is a developing agricultural country in the South Asian region. The banking

sector of the nation is supervised by the Bank Supervision Department of the Central Bank of Sri

Lanka. The Central Bank has categorized the banks into two different categories, namely,

Licensed Commercial Banks (LCBs) and Licensed Specialized banks (LSBs). However, the

LCBs play a significant role in shaping the financial condition of the Sri Lankan economy due to

their base of the assets and magnitude of the services provided. These LCBs dominate the

financial market of Sri Lanka and thus have successfully captured the greatest share of the entire

financial system of the nation by controlling the payment cycle. Therefore, the health of the

financial system of the Sri Lankan economy is dependent largely on the performance as well as

the financial strength of the six biggest LCBs and hence, they are referred to as the Systemically

Important Banks (SIBs). The LSBs do not have any major intermediary role in the payment cycle

and thus have relatively lower systemic importance, in terms of size and influence on the

financial system in the economy (Cbsl.gov.lk 2018).

It has been found that, the LCBs or SIBs have been facing a challenge in the past decade

that has been hampering their performances. The country’s economy is heavily burdened with

great amount of loan loss or non-performing loans for the last ten years. Due to this provision,

the LCBs suffer from fall in profit. According to a report by EconomyNext, in March 2017

quarter, the profits of the National Developmental Bank of Sri Lanka grew 35% than the

2DISSERTATION

previous year due to lower provisioning for loan loss (Economynext.com 2017). It is also

reported that the loan loss provisions reduced to 80%, from 545 million rupees a year ago to 111

million rupees in March quarter 2017. Thus, the loan loss amount was extremely huge in the

2016 March quarter. The SIBs are greatly affected by this financial hurdle and this in turn affects

the financial system of the economy. This research project will explore the extent of loan loss in

the SIBs in Sri Lanka in the past 10 years and its effect on the profitability of the SIBs. The

researcher will conduct an extensive study on the factors of loan loss provisions in Sri Lanka, the

experience of the banks in the last decade to find out their impact on the profitability of the banks

as well as the economy’s performance.

Research aim and objectives

The aim of this research study is to explore the magnitude of the loan loss experience

of the SIBs of Sri Lanka in the last 10 years and its impact on the profit level of the banks.

The research objectives are:

To explore the features of loan loss provision in the Systemically Important Banks (SIBs)

in Sri Lanka

To assess the last 10 years’ experience of the SIBs regarding the loan loss

To evaluate the impact of the loan loss experience on the Sri Lankan banks’ profit level

Research questions

1) What are the disadvantages of loan loss provisions in the Sri Lankan financial system?

2) What is the loan loss scenario in the Sri Lankan economy in the past 10 years?

3) How the loan loss has affected the profitability of the SIBs in Sri Lanka?

previous year due to lower provisioning for loan loss (Economynext.com 2017). It is also

reported that the loan loss provisions reduced to 80%, from 545 million rupees a year ago to 111

million rupees in March quarter 2017. Thus, the loan loss amount was extremely huge in the

2016 March quarter. The SIBs are greatly affected by this financial hurdle and this in turn affects

the financial system of the economy. This research project will explore the extent of loan loss in

the SIBs in Sri Lanka in the past 10 years and its effect on the profitability of the SIBs. The

researcher will conduct an extensive study on the factors of loan loss provisions in Sri Lanka, the

experience of the banks in the last decade to find out their impact on the profitability of the banks

as well as the economy’s performance.

Research aim and objectives

The aim of this research study is to explore the magnitude of the loan loss experience

of the SIBs of Sri Lanka in the last 10 years and its impact on the profit level of the banks.

The research objectives are:

To explore the features of loan loss provision in the Systemically Important Banks (SIBs)

in Sri Lanka

To assess the last 10 years’ experience of the SIBs regarding the loan loss

To evaluate the impact of the loan loss experience on the Sri Lankan banks’ profit level

Research questions

1) What are the disadvantages of loan loss provisions in the Sri Lankan financial system?

2) What is the loan loss scenario in the Sri Lankan economy in the past 10 years?

3) How the loan loss has affected the profitability of the SIBs in Sri Lanka?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3DISSERTATION

Research hypothesis

H0 (null hypothesis): loan loss experience has no significant impact on the SIBs’ profit level

H1 (alternative hypothesis): loan loss experience has significant impact on the SIBs’ profit level

Literature review

Loan loss provision (LLP) is an important feature of the commercial banks. These banks

set aside an expense as an allowance to compensate the uncollected loans and credits. As stated

by Dou, Ryan and Zou (2018), loan loss provision is a cost of the commercial banks, which they

keep reserved for the defaulted credits and loans. When the amount of defaulted loans gets

increased, it creates a pressure on the banks financial position as the loan loss provisions keeps

on getting increased. This is an important information as this indicates the stability of the bank’s

lending base. The amount of loans to be waved off is dependent on the bank’s discretion.

However, the loan loss incidences are not always the resultant impact of the bad or risky lending

decisions. The external economic conditions are often responsible to make the borrowers

defaulters.

According to Caporale et al. (2015), the major determinants of the loan loss provision

were classified into discretionary (capital management and income smoothing) and non-

discretionary (related to business cycle) factors. The study explored the panel data from 400

Italian banks within the time period of 2001 to 2012, and it was found that, in those Italian

banks, the LLP was mostly determined by the non-discretionary elements and consistent with the

countercyclical behavior of the LLP. However, as the loans of the local banks were mostly

collateralized, the activities and nature were more strongly affected by the supervisory activity of

the banks with initial coverage ratio being less than for the multinational banks. Hence, it can be

Research hypothesis

H0 (null hypothesis): loan loss experience has no significant impact on the SIBs’ profit level

H1 (alternative hypothesis): loan loss experience has significant impact on the SIBs’ profit level

Literature review

Loan loss provision (LLP) is an important feature of the commercial banks. These banks

set aside an expense as an allowance to compensate the uncollected loans and credits. As stated

by Dou, Ryan and Zou (2018), loan loss provision is a cost of the commercial banks, which they

keep reserved for the defaulted credits and loans. When the amount of defaulted loans gets

increased, it creates a pressure on the banks financial position as the loan loss provisions keeps

on getting increased. This is an important information as this indicates the stability of the bank’s

lending base. The amount of loans to be waved off is dependent on the bank’s discretion.

However, the loan loss incidences are not always the resultant impact of the bad or risky lending

decisions. The external economic conditions are often responsible to make the borrowers

defaulters.

According to Caporale et al. (2015), the major determinants of the loan loss provision

were classified into discretionary (capital management and income smoothing) and non-

discretionary (related to business cycle) factors. The study explored the panel data from 400

Italian banks within the time period of 2001 to 2012, and it was found that, in those Italian

banks, the LLP was mostly determined by the non-discretionary elements and consistent with the

countercyclical behavior of the LLP. However, as the loans of the local banks were mostly

collateralized, the activities and nature were more strongly affected by the supervisory activity of

the banks with initial coverage ratio being less than for the multinational banks. Hence, it can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4DISSERTATION

said that, the LLP is mostly dependent on the non-discretionary factors, which are mostly the

external macro-economic variables, affecting the financial system of the banks.

Another study by Pérez, Salas-Fumás and Saurina (2008) shows that, the Spanish banks

have been using the LLP for smoothing their earnings, however, the authors could not find any

evidence for capital management practice. Along with that, the credit risk variables were found

to be more important than the net operating income. Thus, as a summary the authors have

reported that usage of statistical provisions for accounting purpose improved the quality of the

accounting statements, which incorporated the cyclical and counter-cyclical impact of the LLP

that was made flexible to adjust with the upturn or downturn of the economy.

Kim, Liu and Rhee (2003) highlighted that the large and the small firms have different

objectives for earning management. The relationship between size of the firm and earnings

management was explored in their study. The authors excluded the banks, highly regulated firms

and financial institutions due to the capital structure and intensive government regulations and

found that the small firms smooth their earnings with a purpose of avoiding the reporting of loss

earning. On the other hand, the large and medium firms were more interested in reducing their

loss earnings. Thus, it can be said that, the banks would have a separate objective than other type

of firms for earning management.

Fernando and Ekanayake (2015) conducted a study on whether the commercial banks of

Sri Lanka use the loan loss provisions for smoothing their income. The authors have found that

the private sector LCBs use the loan loss provisions to smooth their income but not the public

sector LCBs. By using the panel data from 2003 to 2012 on eight bank specific variables, the

authors have found that the LLP in the Sri Lankan banks were highly dependent on the ratio of

said that, the LLP is mostly dependent on the non-discretionary factors, which are mostly the

external macro-economic variables, affecting the financial system of the banks.

Another study by Pérez, Salas-Fumás and Saurina (2008) shows that, the Spanish banks

have been using the LLP for smoothing their earnings, however, the authors could not find any

evidence for capital management practice. Along with that, the credit risk variables were found

to be more important than the net operating income. Thus, as a summary the authors have

reported that usage of statistical provisions for accounting purpose improved the quality of the

accounting statements, which incorporated the cyclical and counter-cyclical impact of the LLP

that was made flexible to adjust with the upturn or downturn of the economy.

Kim, Liu and Rhee (2003) highlighted that the large and the small firms have different

objectives for earning management. The relationship between size of the firm and earnings

management was explored in their study. The authors excluded the banks, highly regulated firms

and financial institutions due to the capital structure and intensive government regulations and

found that the small firms smooth their earnings with a purpose of avoiding the reporting of loss

earning. On the other hand, the large and medium firms were more interested in reducing their

loss earnings. Thus, it can be said that, the banks would have a separate objective than other type

of firms for earning management.

Fernando and Ekanayake (2015) conducted a study on whether the commercial banks of

Sri Lanka use the loan loss provisions for smoothing their income. The authors have found that

the private sector LCBs use the loan loss provisions to smooth their income but not the public

sector LCBs. By using the panel data from 2003 to 2012 on eight bank specific variables, the

authors have found that the LLP in the Sri Lankan banks were highly dependent on the ratio of

5DISSERTATION

loans and the deposits. In the private and SIBs, the relationship between the income before taxes

and the LLPs was found to be positive.

Bouvatier and Lepetit (2012) conducted a study on the impacts of loan loss provisions on

the growth of the bank lending and provided the outcome by comparing some international

companies. The authors investigated that if the backward-looking provision practices magnify

the rise in the bank lending and if that exists, if there are differences in the magnitude across the

countries. In this study, the authors found that the backward-looking provisioning system

influences the lending fluctuations in the banks’ operations in both the developed and developing

countries but in the emerging countries, it has a stronger effect.

According to a study by Alhadab and Alsahawneh (2016), it is seen that the LLP has a

negative influence on the profitability of the commercial banks in Jordan. 13 Jordanian banks,

which were listed on the Amman Stock Exchange (ASE) for the time period between 2004 and

2014, were studied by the authors by using Return on Equity (ROE) and Return on Assets

(ROA) as a proxy for the banks’ profitability and it was found that, LLP used by these banks for

various reasons had a negative impact on their profits. A similar study was conducted by ul

Mustafa, Ansari and Younis (2012) on the banks of Pakistan which also showed that, the LLP

has a magnificent importance in determining the profitability of the commercial banks of

Pakistan. The authors have shown that a well-maintained bank is supposed to have a lower LLP

and that leads to higher profitability. Apart from that, the deposits and advances also play a

significant role in determining the profitability of the commercial banks in Pakistan. However,

the authors also highlighted that political stability is another crucial factor affecting the banks’

profitability.

loans and the deposits. In the private and SIBs, the relationship between the income before taxes

and the LLPs was found to be positive.

Bouvatier and Lepetit (2012) conducted a study on the impacts of loan loss provisions on

the growth of the bank lending and provided the outcome by comparing some international

companies. The authors investigated that if the backward-looking provision practices magnify

the rise in the bank lending and if that exists, if there are differences in the magnitude across the

countries. In this study, the authors found that the backward-looking provisioning system

influences the lending fluctuations in the banks’ operations in both the developed and developing

countries but in the emerging countries, it has a stronger effect.

According to a study by Alhadab and Alsahawneh (2016), it is seen that the LLP has a

negative influence on the profitability of the commercial banks in Jordan. 13 Jordanian banks,

which were listed on the Amman Stock Exchange (ASE) for the time period between 2004 and

2014, were studied by the authors by using Return on Equity (ROE) and Return on Assets

(ROA) as a proxy for the banks’ profitability and it was found that, LLP used by these banks for

various reasons had a negative impact on their profits. A similar study was conducted by ul

Mustafa, Ansari and Younis (2012) on the banks of Pakistan which also showed that, the LLP

has a magnificent importance in determining the profitability of the commercial banks of

Pakistan. The authors have shown that a well-maintained bank is supposed to have a lower LLP

and that leads to higher profitability. Apart from that, the deposits and advances also play a

significant role in determining the profitability of the commercial banks in Pakistan. However,

the authors also highlighted that political stability is another crucial factor affecting the banks’

profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6DISSERTATION

Thus, from the above discussion on various literatures it can be inferred that LLP has an

important significance in the banking operations. The performance of the financial activities of

the SIBs depend on many internal as well as external factors and the loan loss provisions

influence the lending and credit accounting behavior. Through this research study, the researcher

will be investigating the impact of the LLP on the performance or the profit level of the SIBs in

Sri Lanka in the last 10 years, to find out if the profitability of the SIBs is influenced by the LLP.

According to a report by TheGlobalEconomy.com (2018), the data on the non-

performing loans in the Sri Lankan banks show the average value of the non-performing loans

was 3.86%, with minimum of 2.63% in 2016 and maximum of 5.58% in 2013. This percentage

of the non-performing loans indicates the health of the financial or banking system of Sri Lanka.

A high percent indicates that the SIBs face challenge in collecting the principal as well as the

interests on these loans, adding to their loan loss experience. This affects the profit levels of the

banks.

Research methodology

Research methodology refers to the procedures followed by the researcher to answer the

research questions in the most appropriate and reasonable manner (Mackey and Gass 2015). This

consists of the steps that are adopted in every stage of the study to get to the desired outcome.

Research methodology consists of research paradigm, approach, design, sampling, data

collection and analysis process.

In this study, the researcher aimed to investigate the loan loss experience of the SIBs in

Sri Lanka in the past 10 years. To conduct this study, the researcher will adopt the pragmatism

research philosophy or paradigm. This philosophy allows the researcher to apply both the

Thus, from the above discussion on various literatures it can be inferred that LLP has an

important significance in the banking operations. The performance of the financial activities of

the SIBs depend on many internal as well as external factors and the loan loss provisions

influence the lending and credit accounting behavior. Through this research study, the researcher

will be investigating the impact of the LLP on the performance or the profit level of the SIBs in

Sri Lanka in the last 10 years, to find out if the profitability of the SIBs is influenced by the LLP.

According to a report by TheGlobalEconomy.com (2018), the data on the non-

performing loans in the Sri Lankan banks show the average value of the non-performing loans

was 3.86%, with minimum of 2.63% in 2016 and maximum of 5.58% in 2013. This percentage

of the non-performing loans indicates the health of the financial or banking system of Sri Lanka.

A high percent indicates that the SIBs face challenge in collecting the principal as well as the

interests on these loans, adding to their loan loss experience. This affects the profit levels of the

banks.

Research methodology

Research methodology refers to the procedures followed by the researcher to answer the

research questions in the most appropriate and reasonable manner (Mackey and Gass 2015). This

consists of the steps that are adopted in every stage of the study to get to the desired outcome.

Research methodology consists of research paradigm, approach, design, sampling, data

collection and analysis process.

In this study, the researcher aimed to investigate the loan loss experience of the SIBs in

Sri Lanka in the past 10 years. To conduct this study, the researcher will adopt the pragmatism

research philosophy or paradigm. This philosophy allows the researcher to apply both the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7DISSERTATION

qualitative and quantitative research method. This method will be applied to get a wider

perspective on the research topic. Following this philosophy, the researcher will apply deductive

research approach. Under this research approach, the researcher will explain the findings by

exploring and analyzing the data, against the previous literatures. This is unlike the inductive

approach, in which the researcher is required to develop a new theory from the data. In the given

study, there is no need to generate new theories, rather, based on the previous literature, the

researcher will explain the impact of the loan loss experience on the profitability of the SIBs in

Sri Lanka.

Regarding the research design, the researcher will adopt the correlational research

design. In this design, the researcher will establish a relationship between the dependent and

independent variable, depicting the research problem. This research design enables the

researcher to frame a research hypothesis and then test it to get the outcome. This research

design aims to establish a causal relationship between the variables. As in this study, through the

correlational study, the researcher will examine if there is any cause and effect relationship

between the dependent and independent variables.

Following this design, the researcher will apply case study research strategy. There are

six SIBs in Sri Lanka and the researcher will explore the reports of these banks regarding the

loan loss experience to write the thesis. Thus, this strategy will beneficial as this enables the

researcher to narrow down the research horizon and put focus on a specific aspect. This yields

more specific results, based on which, a generalized conclusion can be made.

The researcher will collect both the primary and secondary data for this study. The

primary data will be collected from few employees of the SIBs to get information regarding the

qualitative and quantitative research method. This method will be applied to get a wider

perspective on the research topic. Following this philosophy, the researcher will apply deductive

research approach. Under this research approach, the researcher will explain the findings by

exploring and analyzing the data, against the previous literatures. This is unlike the inductive

approach, in which the researcher is required to develop a new theory from the data. In the given

study, there is no need to generate new theories, rather, based on the previous literature, the

researcher will explain the impact of the loan loss experience on the profitability of the SIBs in

Sri Lanka.

Regarding the research design, the researcher will adopt the correlational research

design. In this design, the researcher will establish a relationship between the dependent and

independent variable, depicting the research problem. This research design enables the

researcher to frame a research hypothesis and then test it to get the outcome. This research

design aims to establish a causal relationship between the variables. As in this study, through the

correlational study, the researcher will examine if there is any cause and effect relationship

between the dependent and independent variables.

Following this design, the researcher will apply case study research strategy. There are

six SIBs in Sri Lanka and the researcher will explore the reports of these banks regarding the

loan loss experience to write the thesis. Thus, this strategy will beneficial as this enables the

researcher to narrow down the research horizon and put focus on a specific aspect. This yields

more specific results, based on which, a generalized conclusion can be made.

The researcher will collect both the primary and secondary data for this study. The

primary data will be collected from few employees of the SIBs to get information regarding the

8DISSERTATION

loan loss provisions in the banks and its impact on the banks’ profit level. A survey will be

conducted to collect primary data. Few of the employees from each bank will be chosen using

appropriate sampling technique and the survey questionnaire will be sent to them via their

emails. Secondary data on the banks’ profits, Return on Equity (ROE), Return on Assets (ROA)

and LLP experience for the past 10 years will be gathered from their annual reports, collected

from their official websites. Various newspaper and journal articles will be consulted for further

information.

Sampling is essential for primary data collection. As it is not possible to study the entire

population, the researcher will draw a smaller subset from the large population containing the

same characteristics, so that, they yield similar result as the population. The researcher will apply

the simple random sampling technique to select the employees from each bank. This technique

falls under the category of probability sampling. Under this technique, each of the samples has

equal probability of being chosen and the choice is random. This helps in reducing the biasness

and sampling fluctuations in the data (Peck, Olsen and Devore 2015). Non-probability samplings

will not be used as there can be biasness in choosing the sample, based on the researcher’s

judgment, which can yield biased outcome.

Regarding the data analysis process, the researcher will apply both the qualitative and

quantitative method of data analysis. Thereby, the mixed methodology will be followed for

this research. The primary data, that is, the survey response will be collected through the Google

form link and the data will be converted into numeric values to perform the statistical functions

under quantitative analysis. The secondary data, that is, the 10 years’ reports on LLP data and the

banks’ profit level will be analyzed using descriptive method under qualitative analysis. The

loan loss provisions in the banks and its impact on the banks’ profit level. A survey will be

conducted to collect primary data. Few of the employees from each bank will be chosen using

appropriate sampling technique and the survey questionnaire will be sent to them via their

emails. Secondary data on the banks’ profits, Return on Equity (ROE), Return on Assets (ROA)

and LLP experience for the past 10 years will be gathered from their annual reports, collected

from their official websites. Various newspaper and journal articles will be consulted for further

information.

Sampling is essential for primary data collection. As it is not possible to study the entire

population, the researcher will draw a smaller subset from the large population containing the

same characteristics, so that, they yield similar result as the population. The researcher will apply

the simple random sampling technique to select the employees from each bank. This technique

falls under the category of probability sampling. Under this technique, each of the samples has

equal probability of being chosen and the choice is random. This helps in reducing the biasness

and sampling fluctuations in the data (Peck, Olsen and Devore 2015). Non-probability samplings

will not be used as there can be biasness in choosing the sample, based on the researcher’s

judgment, which can yield biased outcome.

Regarding the data analysis process, the researcher will apply both the qualitative and

quantitative method of data analysis. Thereby, the mixed methodology will be followed for

this research. The primary data, that is, the survey response will be collected through the Google

form link and the data will be converted into numeric values to perform the statistical functions

under quantitative analysis. The secondary data, that is, the 10 years’ reports on LLP data and the

banks’ profit level will be analyzed using descriptive method under qualitative analysis. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9DISSERTATION

outcome of the secondary data analysis will be used to compare the findings from the primary

data analysis. This would make the findings more strong.

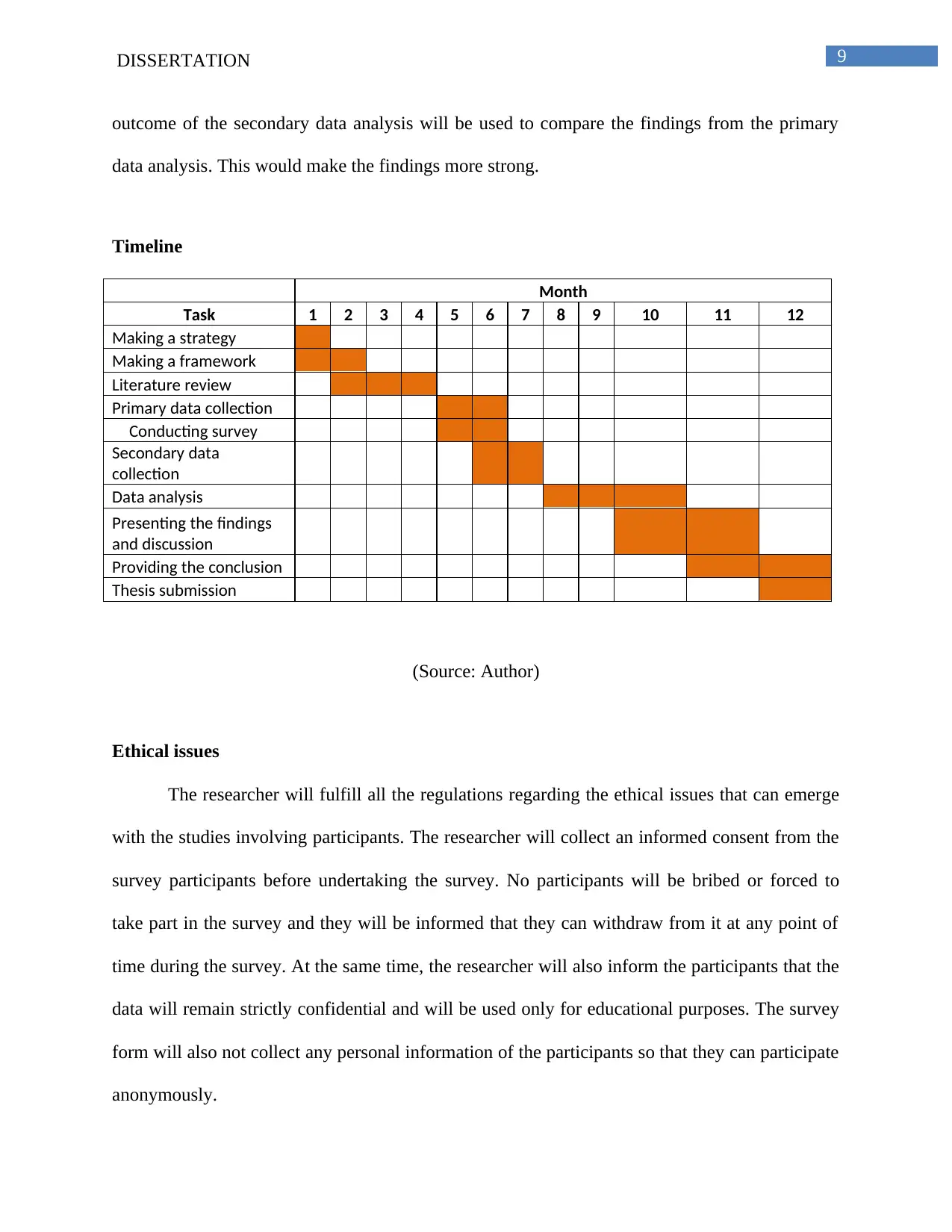

Timeline

Month

Task 1 2 3 4 5 6 7 8 9 10 11 12

Making a strategy

Making a framework

Literature review

Primary data collection

Conducting survey

Secondary data

collection

Data analysis

Presenting the findings

and discussion

Providing the conclusion

Thesis submission

(Source: Author)

Ethical issues

The researcher will fulfill all the regulations regarding the ethical issues that can emerge

with the studies involving participants. The researcher will collect an informed consent from the

survey participants before undertaking the survey. No participants will be bribed or forced to

take part in the survey and they will be informed that they can withdraw from it at any point of

time during the survey. At the same time, the researcher will also inform the participants that the

data will remain strictly confidential and will be used only for educational purposes. The survey

form will also not collect any personal information of the participants so that they can participate

anonymously.

outcome of the secondary data analysis will be used to compare the findings from the primary

data analysis. This would make the findings more strong.

Timeline

Month

Task 1 2 3 4 5 6 7 8 9 10 11 12

Making a strategy

Making a framework

Literature review

Primary data collection

Conducting survey

Secondary data

collection

Data analysis

Presenting the findings

and discussion

Providing the conclusion

Thesis submission

(Source: Author)

Ethical issues

The researcher will fulfill all the regulations regarding the ethical issues that can emerge

with the studies involving participants. The researcher will collect an informed consent from the

survey participants before undertaking the survey. No participants will be bribed or forced to

take part in the survey and they will be informed that they can withdraw from it at any point of

time during the survey. At the same time, the researcher will also inform the participants that the

data will remain strictly confidential and will be used only for educational purposes. The survey

form will also not collect any personal information of the participants so that they can participate

anonymously.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10DISSERTATION

References

Alhadab, M. and Alsahawneh, S., 2016. Loan Loss Provision and the Profitability of

Commercial Banks: Evidence from Jordan. International Journal of Business and

Management, 11(12), p.242.

Bouvatier, V. and Lepetit, L., 2012. Effects of loan loss provisions on growth in bank lending:

some international comparisons. Economie internationale, (4), pp.91-116.

Caporale, G., Alessi, M., Di Colli, S. and Lopez, J., 2015. Loan loss Provision: Some empirical

evidence for Italian banks.

Cbsl.gov.lk, 2018. Banking Sector | Central Bank of Sri Lanka. [online] Cbsl.gov.lk. Available

at: https://www.cbsl.gov.lk/en/financial-system/financial-system-stability/banking-sector

[Accessed 23 Jul. 2018].

Dailymirror.lk, 2018. NDB eyes systemically important private bank status by 2020. [online]

Dailymirror.lk. Available at: http://www.dailymirror.lk/article/NDB-eyes-systemically-

important-private-bank-status-by--147244.html [Accessed 23 Jul. 2018].

Dou, Y., Ryan, S.G. and Zou, Y., 2018. The Effect of Credit Competition on Banks’ Loan-Loss

Provisions. Journal of Financial and Quantitative Analysis, pp.1-32.

Economynext.com, 2017. Sri Lanka's NDB net up 35-pct lower loan loss provisions. [online]

Economynext.com. Available at:

https://economynext.com/Sri_Lanka_s_NDB_net_up_35_pct_lower_loan_loss_provisions-3-

7869-17.html [Accessed 23 Jul. 2018].

References

Alhadab, M. and Alsahawneh, S., 2016. Loan Loss Provision and the Profitability of

Commercial Banks: Evidence from Jordan. International Journal of Business and

Management, 11(12), p.242.

Bouvatier, V. and Lepetit, L., 2012. Effects of loan loss provisions on growth in bank lending:

some international comparisons. Economie internationale, (4), pp.91-116.

Caporale, G., Alessi, M., Di Colli, S. and Lopez, J., 2015. Loan loss Provision: Some empirical

evidence for Italian banks.

Cbsl.gov.lk, 2018. Banking Sector | Central Bank of Sri Lanka. [online] Cbsl.gov.lk. Available

at: https://www.cbsl.gov.lk/en/financial-system/financial-system-stability/banking-sector

[Accessed 23 Jul. 2018].

Dailymirror.lk, 2018. NDB eyes systemically important private bank status by 2020. [online]

Dailymirror.lk. Available at: http://www.dailymirror.lk/article/NDB-eyes-systemically-

important-private-bank-status-by--147244.html [Accessed 23 Jul. 2018].

Dou, Y., Ryan, S.G. and Zou, Y., 2018. The Effect of Credit Competition on Banks’ Loan-Loss

Provisions. Journal of Financial and Quantitative Analysis, pp.1-32.

Economynext.com, 2017. Sri Lanka's NDB net up 35-pct lower loan loss provisions. [online]

Economynext.com. Available at:

https://economynext.com/Sri_Lanka_s_NDB_net_up_35_pct_lower_loan_loss_provisions-3-

7869-17.html [Accessed 23 Jul. 2018].

11DISSERTATION

Fernando, W.D.I. and Ekanayake, E.M.N.N., 2015. Do commercial banks use loan loss

provisions to smooth their income? Empirical evidence from Sri Lankan commercial

banks. Journal of Finance and Bank Management, 3(1), pp.167-179.

Kim, Y., Liu, C. and Rhee, S.G., 2003. The relation of earnings management to firm

size. Journal of Management Research, 4, pp.81-88.

Mackey, A. and Gass, S.M., 2015. Second language research: Methodology and design.

Routledge.

Peck, R., Olsen, C. and Devore, J.L., 2015. Introduction to statistics and data analysis. Cengage

Learning.

Pérez, D., Salas-Fumás, V. and Saurina, J. (2008). Earnings and Capital Management in

Alternative Loan Loss Provision Regulatory Regimes. European Accounting Review, 17(3),

pp.423-445.

TheGlobalEconomy.com, 2018. Sri Lanka Non-performing loans - data, chart. [online]

TheGlobalEconomy.com. Available at:

https://www.theglobaleconomy.com/Sri-Lanka/Nonperforming_loans/ [Accessed 23 Jul. 2018].

ul Mustafa, A.R., Ansari, R.H. and Younis, M.U., 2012. Does the Loan Loss Provision Affect

the Banking Profitability in Case of Pakistan?. Asian Economic and Financial Review, 2(7),

p.772.

Fernando, W.D.I. and Ekanayake, E.M.N.N., 2015. Do commercial banks use loan loss

provisions to smooth their income? Empirical evidence from Sri Lankan commercial

banks. Journal of Finance and Bank Management, 3(1), pp.167-179.

Kim, Y., Liu, C. and Rhee, S.G., 2003. The relation of earnings management to firm

size. Journal of Management Research, 4, pp.81-88.

Mackey, A. and Gass, S.M., 2015. Second language research: Methodology and design.

Routledge.

Peck, R., Olsen, C. and Devore, J.L., 2015. Introduction to statistics and data analysis. Cengage

Learning.

Pérez, D., Salas-Fumás, V. and Saurina, J. (2008). Earnings and Capital Management in

Alternative Loan Loss Provision Regulatory Regimes. European Accounting Review, 17(3),

pp.423-445.

TheGlobalEconomy.com, 2018. Sri Lanka Non-performing loans - data, chart. [online]

TheGlobalEconomy.com. Available at:

https://www.theglobaleconomy.com/Sri-Lanka/Nonperforming_loans/ [Accessed 23 Jul. 2018].

ul Mustafa, A.R., Ansari, R.H. and Younis, M.U., 2012. Does the Loan Loss Provision Affect

the Banking Profitability in Case of Pakistan?. Asian Economic and Financial Review, 2(7),

p.772.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.