Accounting & Finance Report: Loan Options, Investment & Tax System

VerifiedAdded on 2023/04/20

|15

|1859

|381

Report

AI Summary

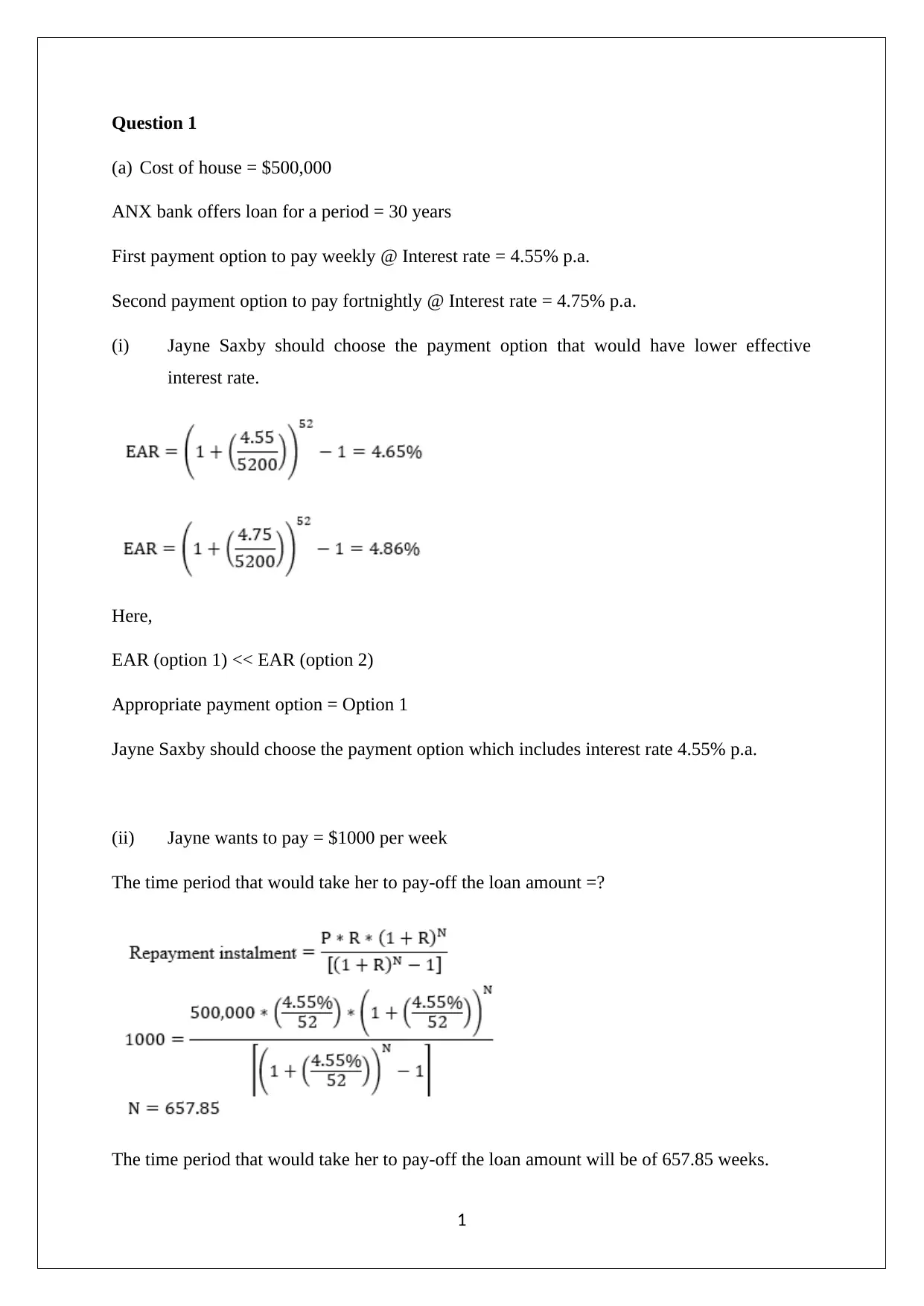

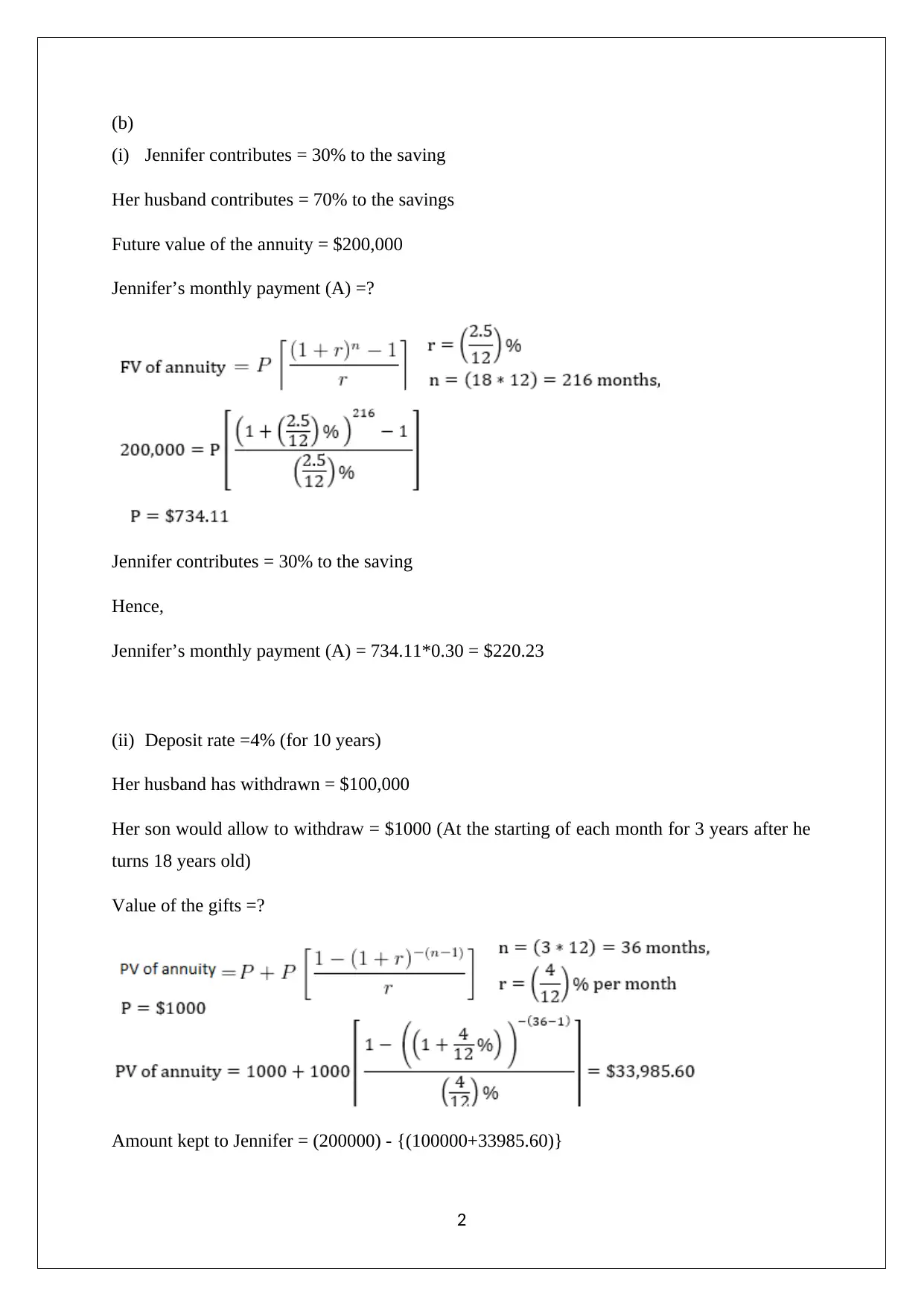

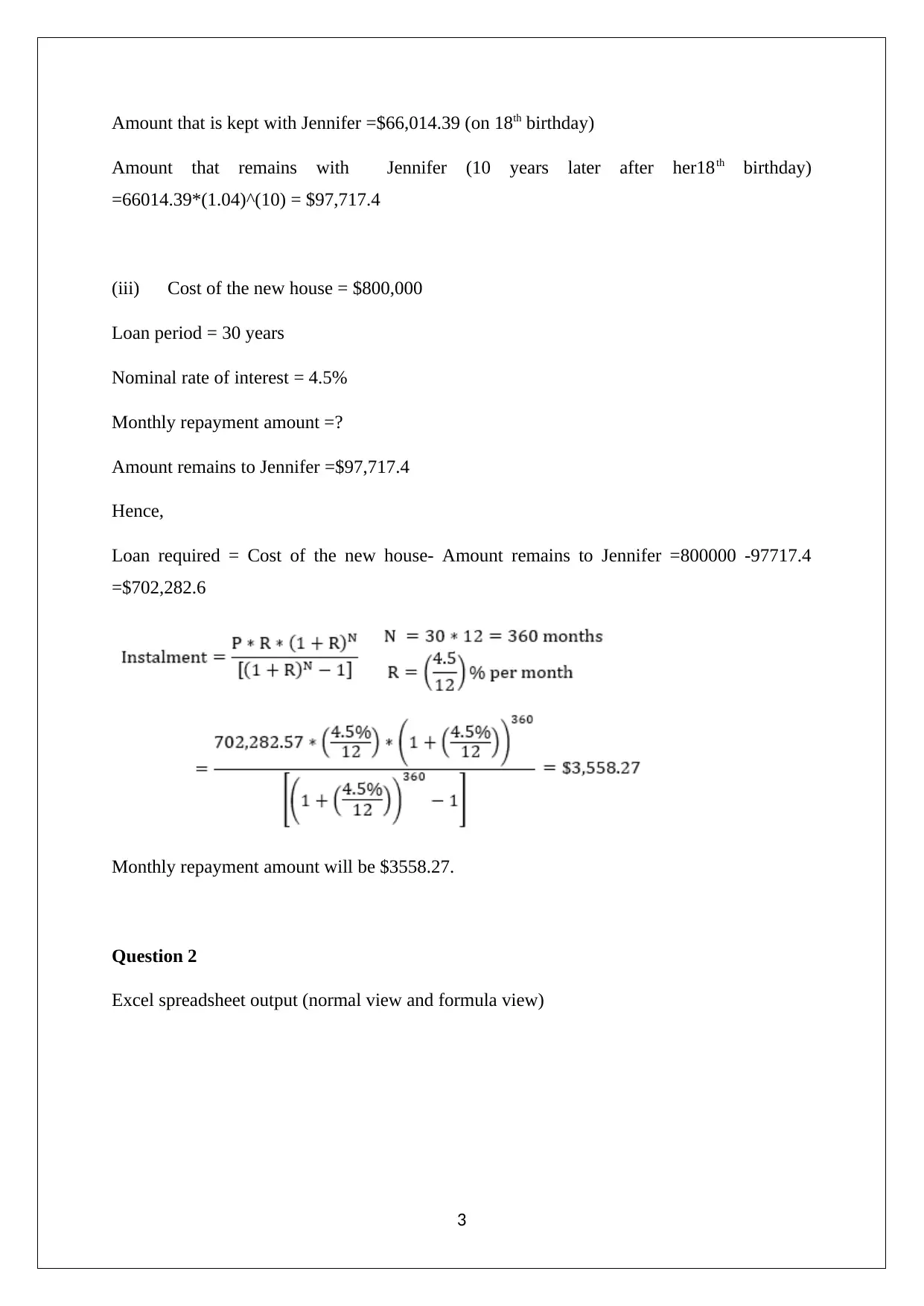

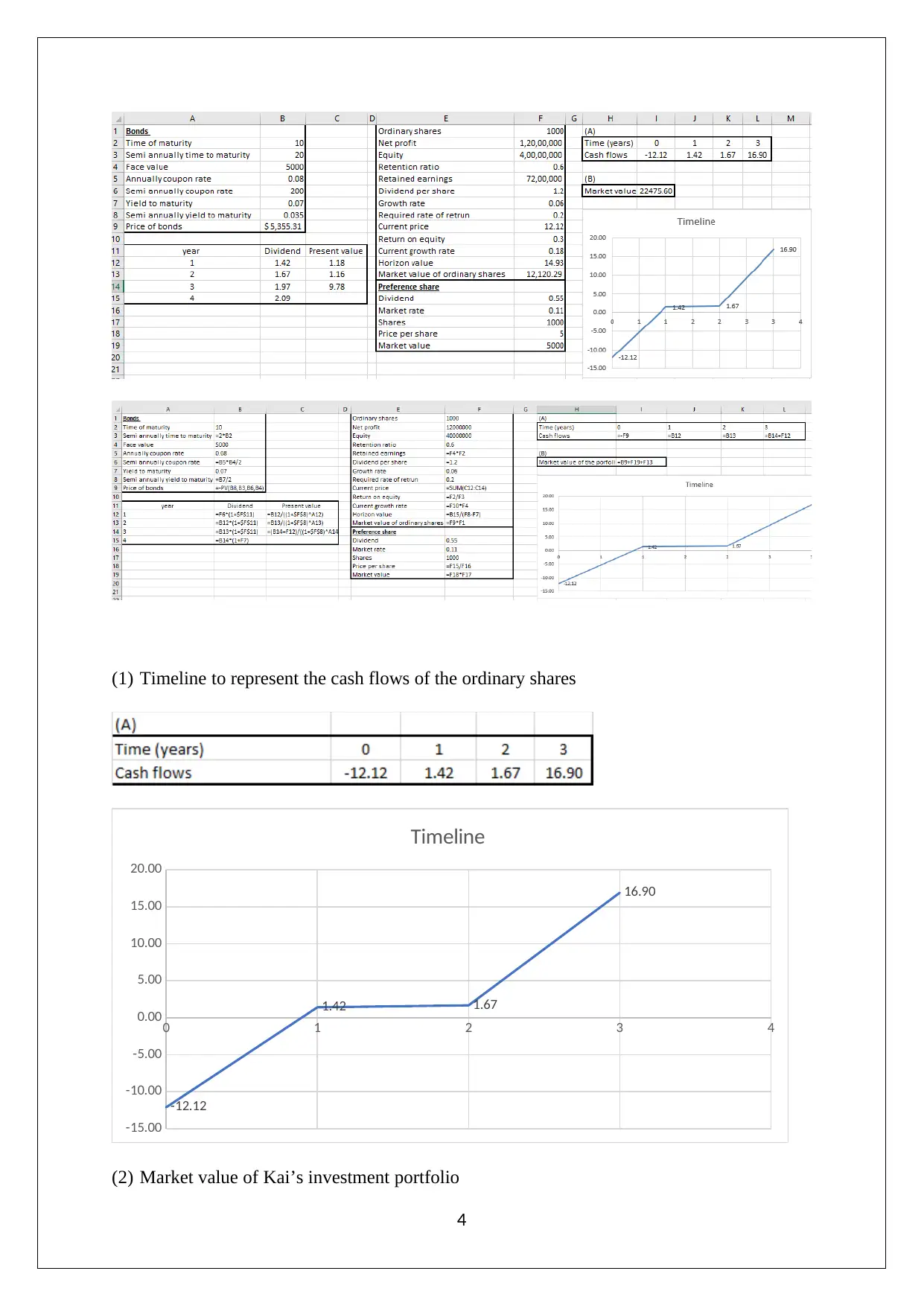

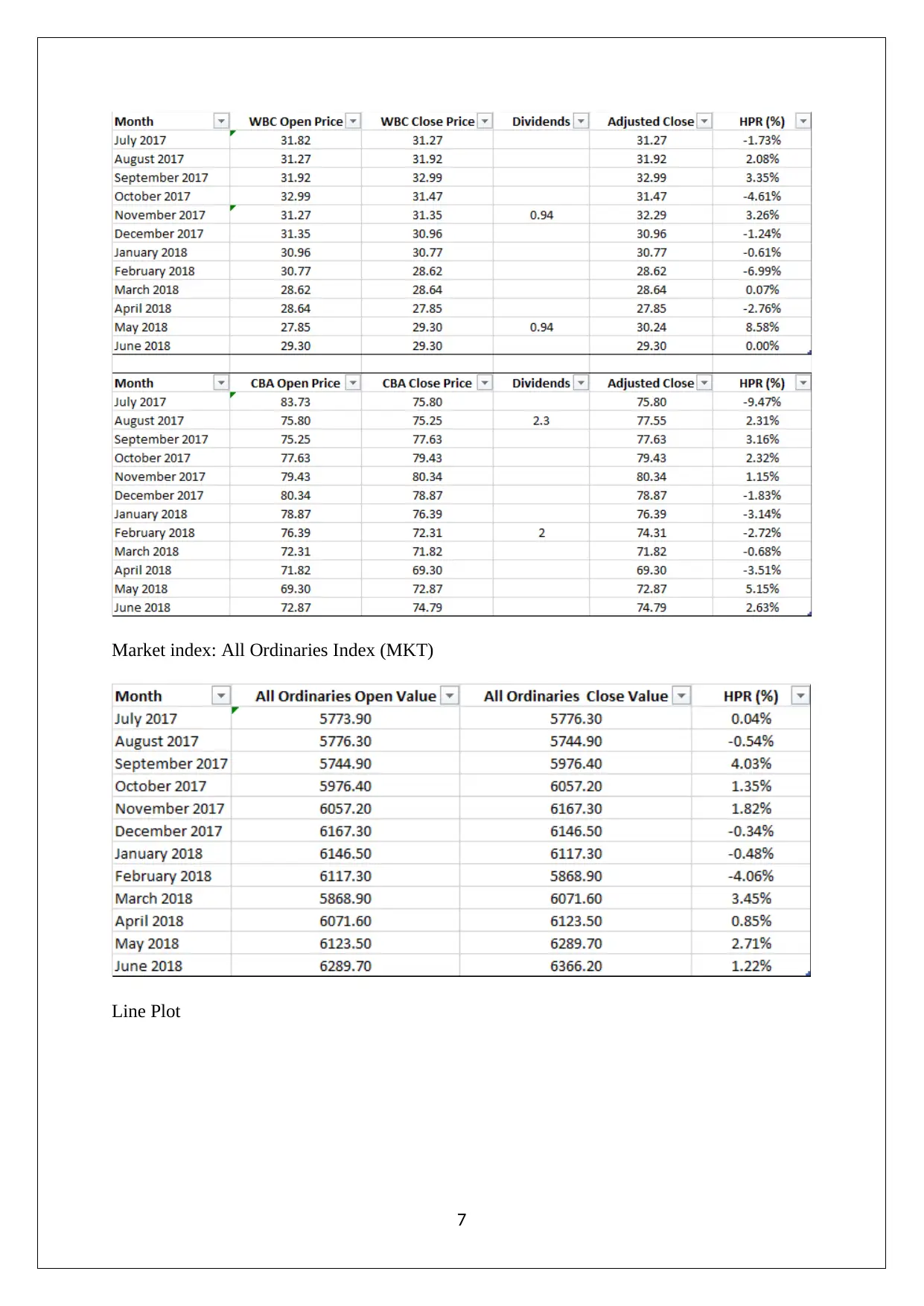

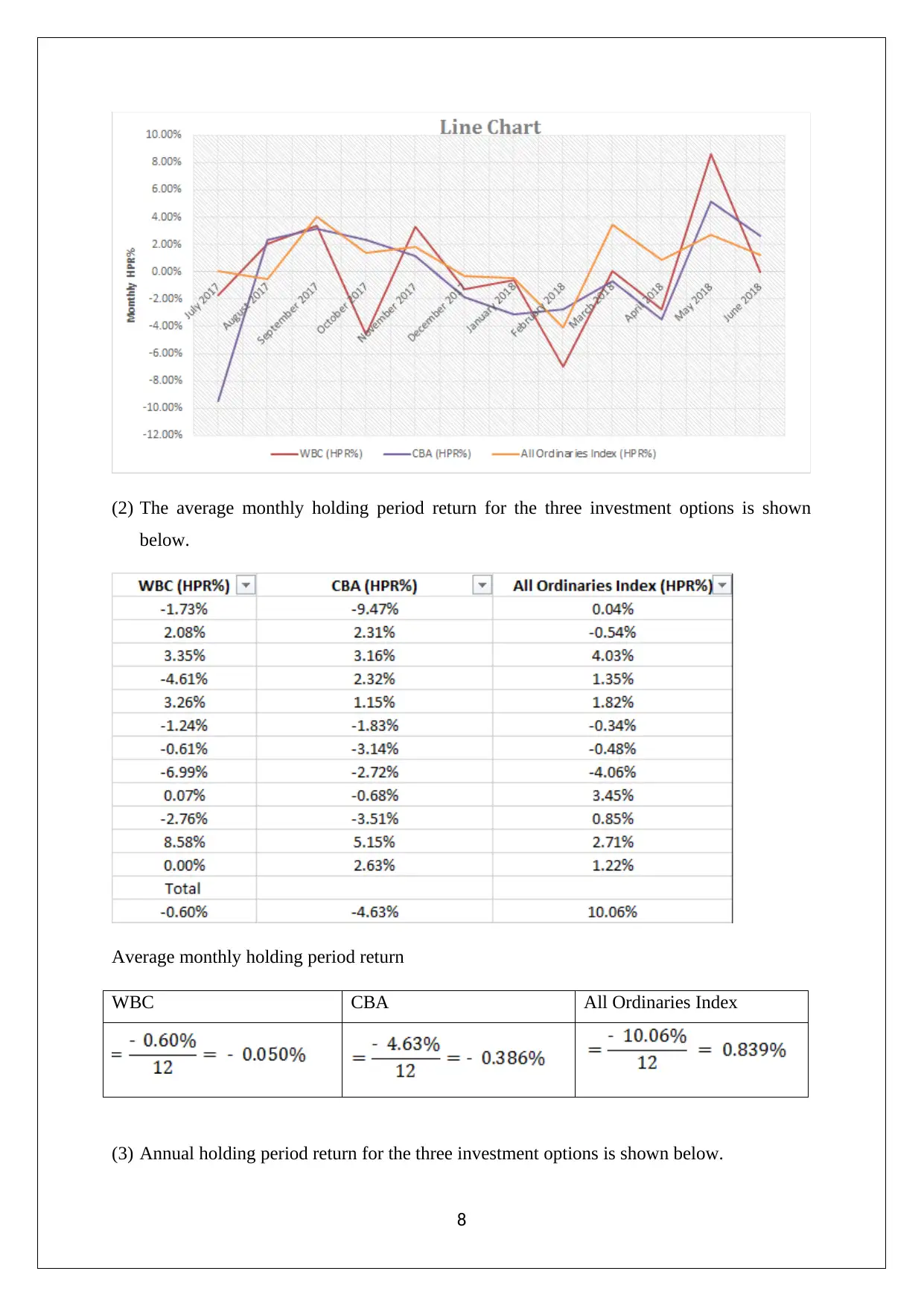

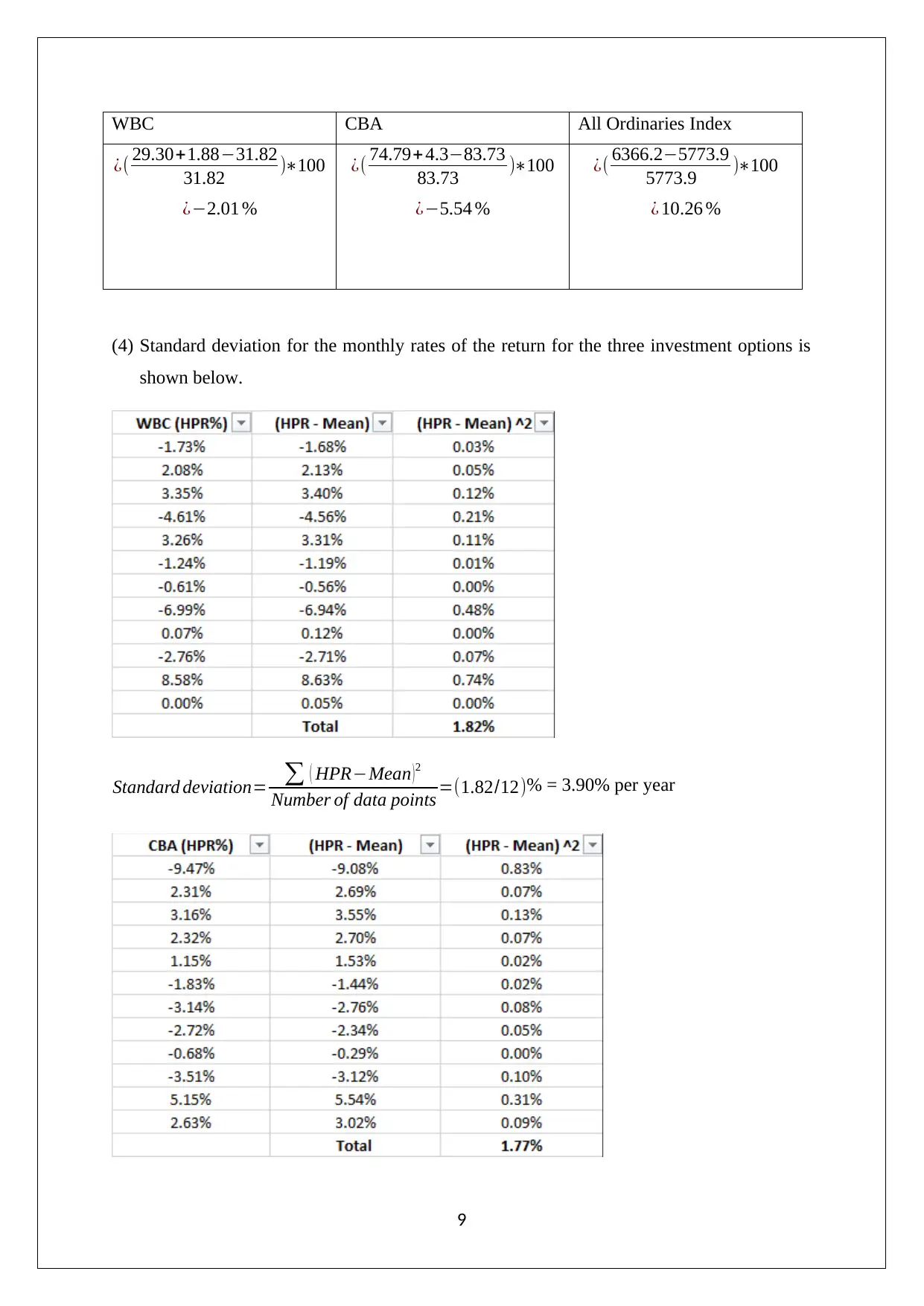

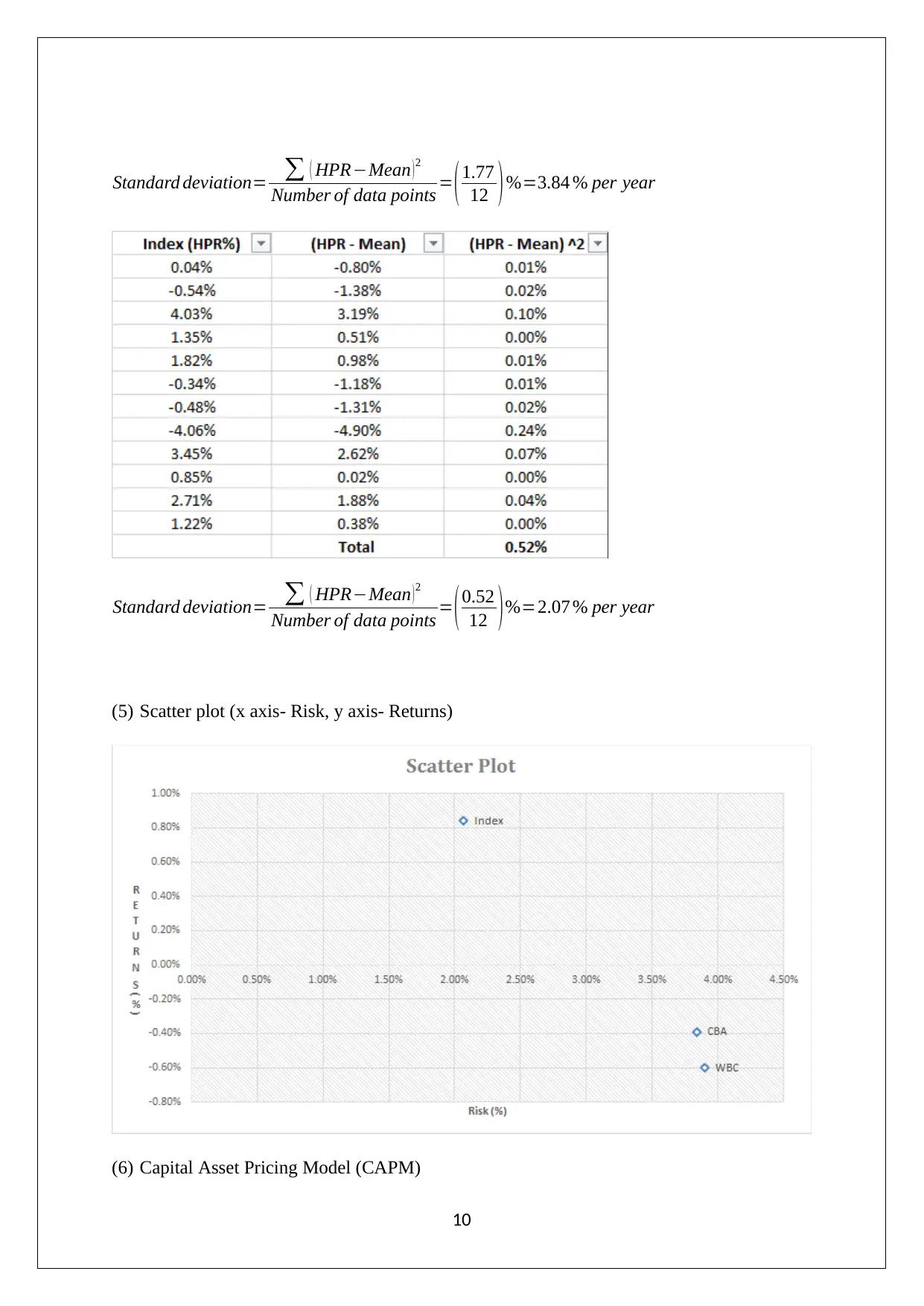

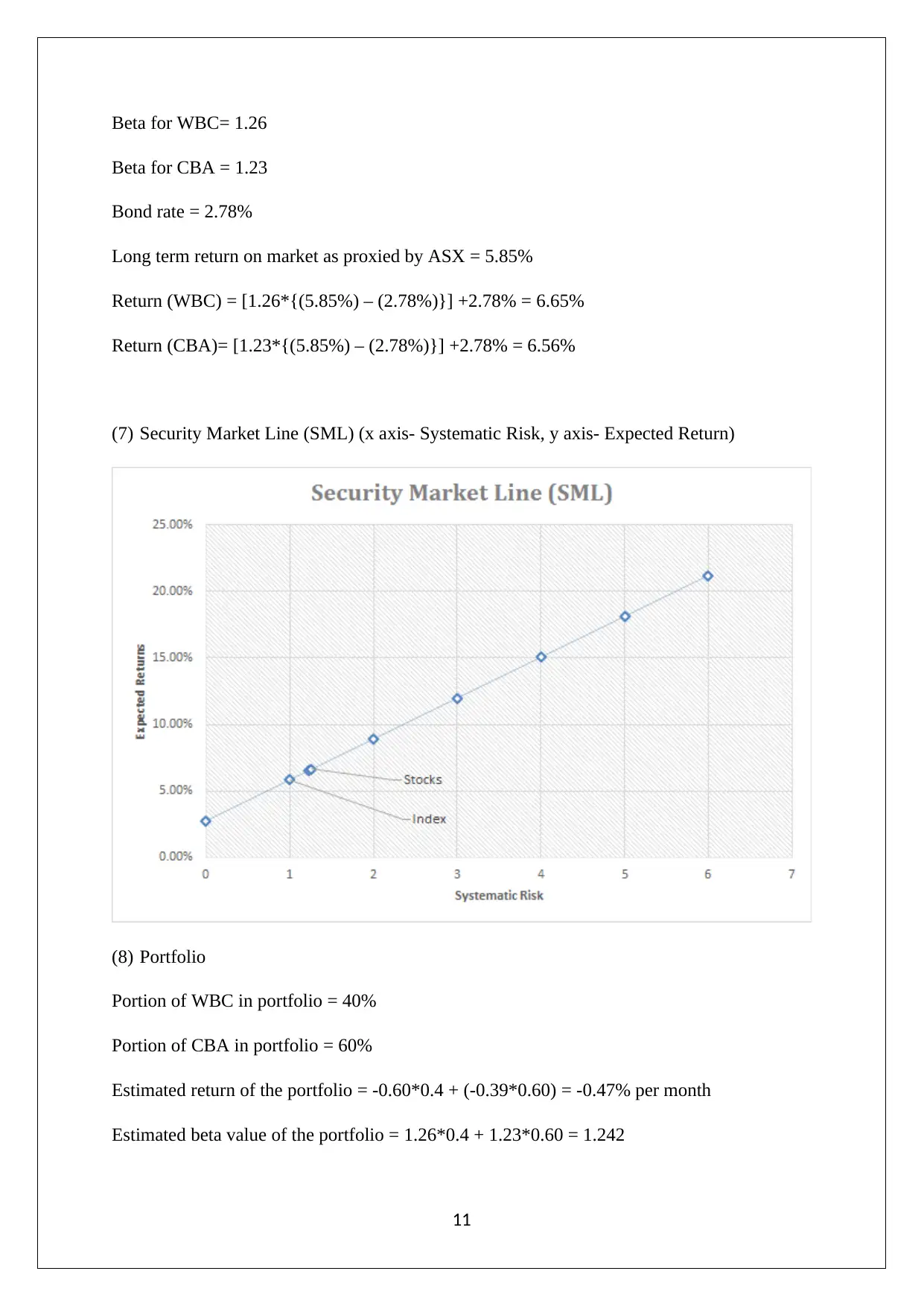

This assignment solution provides a comprehensive analysis of various finance-related topics. It begins with an evaluation of loan options for purchasing a house, comparing weekly and fortnightly payment plans and calculating the time required to pay off a loan with a specific weekly payment. Furthermore, it examines investment strategies, including calculating monthly payments for savings, the future value of annuities, and the impact of withdrawals on investment accounts. The report also delves into the Australian taxation system, contrasting it with classical taxation systems and illustrating the benefits of imputation credits through numerical examples. Lastly, the solution includes an investment portfolio analysis, calculating monthly and annual holding period returns, standard deviation, beta values, and applying the Capital Asset Pricing Model (CAPM) to assess investment options, concluding with a preferred investment choice based on risk and return, all of which can be found with more resources on Desklib.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.