Lobelia Ltd: Cost Estimation, Budgeting, and Variance Analysis

VerifiedAdded on 2023/06/11

|12

|2814

|301

Case Study

AI Summary

This business finance case study analyzes cost estimation and variance analysis, focusing on Lobelia Ltd. Part A covers contribution per unit, break-even point calculations, margin of safety, and profit calculation using marginal and absorption costing, including reconciliation. A memo highlights the importance of contribution margin for business decisions. Part B emphasizes standard costing and variance analysis, calculating material and labor variances. It also discusses the preparation of a budget for controlling operations. The analysis provides insights into cost management and financial decision-making, offering practical applications for understanding and improving a company's financial performance. Desklib provides access to this and other solved assignments.

Business Finance

ASSESSMENT 1

ASSESSMENT 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of contribution per unit.............................................................................................3

Calculation of breakeven point in units and breakeven sales......................................................3

Calculation of margin of safety...................................................................................................4

Calculation of number of units sold.............................................................................................5

Preparation of memo suggesting the finance manager the importance of contribution:.............5

Calculation of profit using marginal and absorption costing and reconciliation between them. 6

PART B...........................................................................................................................................8

Importance of Standard Costing and Variance Analysis.............................................................8

Calculation of material and labour variance along with comment on them................................8

Preparation of budget for controlling the operations.................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of contribution per unit.............................................................................................3

Calculation of breakeven point in units and breakeven sales......................................................3

Calculation of margin of safety...................................................................................................4

Calculation of number of units sold.............................................................................................5

Preparation of memo suggesting the finance manager the importance of contribution:.............5

Calculation of profit using marginal and absorption costing and reconciliation between them. 6

PART B...........................................................................................................................................8

Importance of Standard Costing and Variance Analysis.............................................................8

Calculation of material and labour variance along with comment on them................................8

Preparation of budget for controlling the operations.................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Simply put, company finance is the process of effectively managing an organization's

finances so that its cash are not misappropriated. It is critical for the organisation to engage

clever financial experts with proper understanding of money and their treatment in order to carry

out optimal utilisation (Jiang, and et.al., 2020). This paper contains two case studies pertaining to

cost estimation and investment assessment approaches used to assess the project's feasibility. The

material and labour variations were estimated in order to better understand the disparity in those

areas.

PART A

Calculation of contribution per unit

It may also be described as profit on a single unit's sale, after all variable expenditures have

been deducted, the amount remaining is referred to as contribution. This information is useful in

determining the cheapest price at which to sell the item.

Contribution per unit = sales per unit – variable cost per unit

= £120 – £50

= £70 per unit

It can now be seen that revenues per unit are £120, variable expenses are £50 per unit, and

the Lobelia Ltd firm contributes £70 per unit.

Calculation of breakeven point in units and breakeven sales

This is the most crucial idea to understand since it weighs a new company's costs, goods,

and services against the unit of the selling price to determine when it will break even.

Essentially, it is the point in the sales process when the total of fixed and variable costs equals

total sales revenue (Ross, and et.al., 2019). On the other hand, the break-even point is a point at

which the firm makes neither a profit nor a loss. Simply said, the break-even point is the amount

of income required to cover all fixed and variable costs. If a company's sales are lower than

expected, the break-even point will be lower. However, if the company's income is substantial,

the break-even point is reached, and profit is generated, but only after all expenditures are taken

into account.

Simplification of Break- even point:

Simply put, company finance is the process of effectively managing an organization's

finances so that its cash are not misappropriated. It is critical for the organisation to engage

clever financial experts with proper understanding of money and their treatment in order to carry

out optimal utilisation (Jiang, and et.al., 2020). This paper contains two case studies pertaining to

cost estimation and investment assessment approaches used to assess the project's feasibility. The

material and labour variations were estimated in order to better understand the disparity in those

areas.

PART A

Calculation of contribution per unit

It may also be described as profit on a single unit's sale, after all variable expenditures have

been deducted, the amount remaining is referred to as contribution. This information is useful in

determining the cheapest price at which to sell the item.

Contribution per unit = sales per unit – variable cost per unit

= £120 – £50

= £70 per unit

It can now be seen that revenues per unit are £120, variable expenses are £50 per unit, and

the Lobelia Ltd firm contributes £70 per unit.

Calculation of breakeven point in units and breakeven sales

This is the most crucial idea to understand since it weighs a new company's costs, goods,

and services against the unit of the selling price to determine when it will break even.

Essentially, it is the point in the sales process when the total of fixed and variable costs equals

total sales revenue (Ross, and et.al., 2019). On the other hand, the break-even point is a point at

which the firm makes neither a profit nor a loss. Simply said, the break-even point is the amount

of income required to cover all fixed and variable costs. If a company's sales are lower than

expected, the break-even point will be lower. However, if the company's income is substantial,

the break-even point is reached, and profit is generated, but only after all expenditures are taken

into account.

Simplification of Break- even point:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The break-even point is a computation of sustenance, and the lower the break-even

quantity, the better for the firm.

Here's how to figure out your break-even point and sales:

Break-even point = Fixed cost / (sales per unit – variable cost per unit)

Break-even point

= £700000 / (£120 - £50)

= £700000 / £70

= £10000 units

It is evident that the above method calculates the break-even threshold when the fixed per

unit cost is divided by the contribution per unit, with the value of the fixed cost being £700000

and the contribution per unit being £70.

Break- even sales in % = Fixed cost / Contribution margin

Break- even sales

= £700000 / £2800000 *100

= 25 %

The above calculation clearly reveals that the break-even sales is 25%, and if it is

calculated in units, it displays the same breakeven point unit of £70.

Calculation of margin of safety

The difference between current sales and break-even sales is depicted in this idea of

margin of safety (Kong and Xin, 2019). It depicts the level of safety that the company achieves

before losses arise, implying a drop below the break-even point.

Clarification of Margin of Safety: It evaluates the company's risk and determines if a

bigger margin of safety is beneficial to the business.

The following is a formula for calculating the margin of safety:

Margin of safety (MOS) = Budgeted sales – Break-even point / budgeted sales * 100

= £40000 units - £10000 units / £40000 units *100

= £30000 units / £40000 units *100

= 75%

The foregoing calculation shows that the margin of safety is 75%, and the company's

planned sales are already £40,000, but the break-even threshold is calculated at £10,000.

quantity, the better for the firm.

Here's how to figure out your break-even point and sales:

Break-even point = Fixed cost / (sales per unit – variable cost per unit)

Break-even point

= £700000 / (£120 - £50)

= £700000 / £70

= £10000 units

It is evident that the above method calculates the break-even threshold when the fixed per

unit cost is divided by the contribution per unit, with the value of the fixed cost being £700000

and the contribution per unit being £70.

Break- even sales in % = Fixed cost / Contribution margin

Break- even sales

= £700000 / £2800000 *100

= 25 %

The above calculation clearly reveals that the break-even sales is 25%, and if it is

calculated in units, it displays the same breakeven point unit of £70.

Calculation of margin of safety

The difference between current sales and break-even sales is depicted in this idea of

margin of safety (Kong and Xin, 2019). It depicts the level of safety that the company achieves

before losses arise, implying a drop below the break-even point.

Clarification of Margin of Safety: It evaluates the company's risk and determines if a

bigger margin of safety is beneficial to the business.

The following is a formula for calculating the margin of safety:

Margin of safety (MOS) = Budgeted sales – Break-even point / budgeted sales * 100

= £40000 units - £10000 units / £40000 units *100

= £30000 units / £40000 units *100

= 75%

The foregoing calculation shows that the margin of safety is 75%, and the company's

planned sales are already £40,000, but the break-even threshold is calculated at £10,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

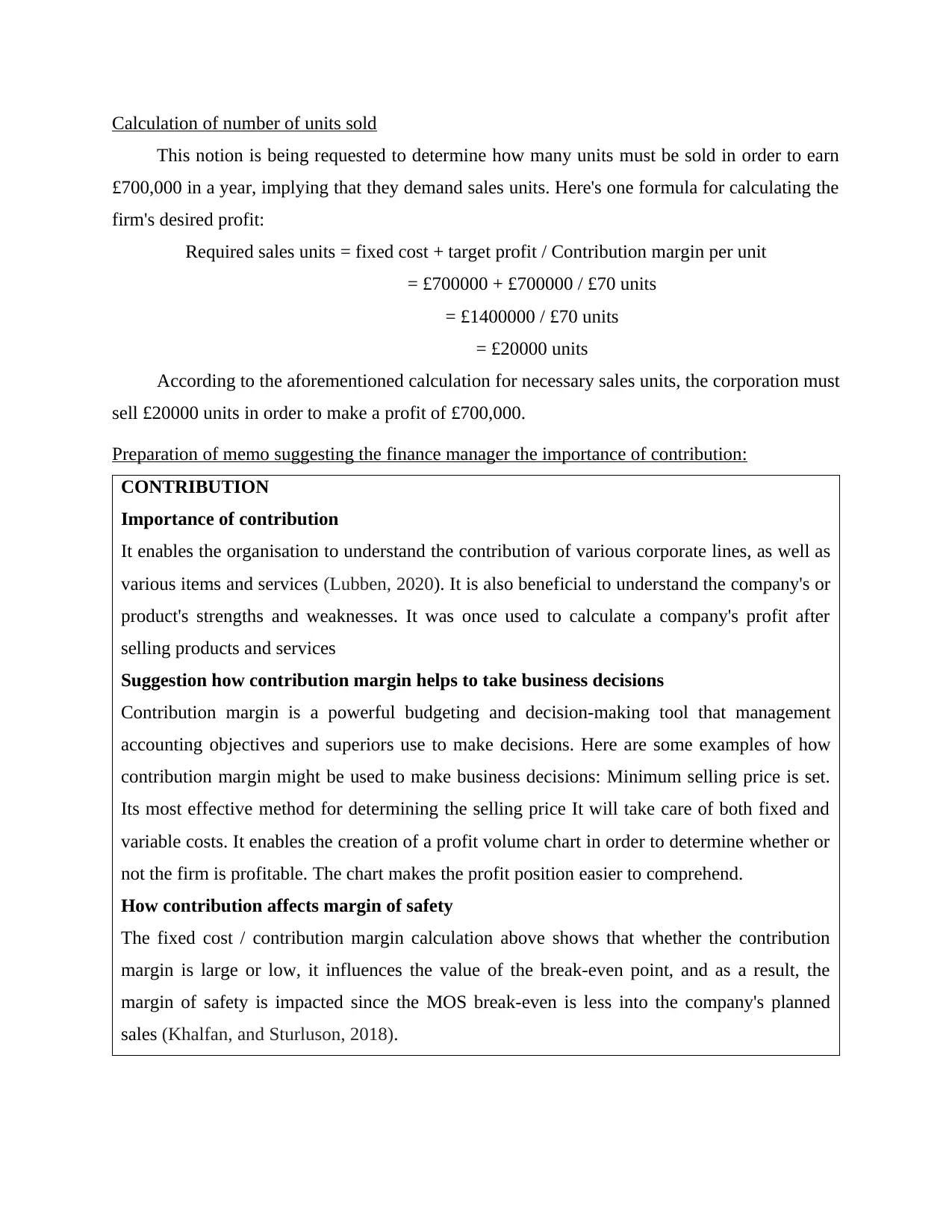

Calculation of number of units sold

This notion is being requested to determine how many units must be sold in order to earn

£700,000 in a year, implying that they demand sales units. Here's one formula for calculating the

firm's desired profit:

Required sales units = fixed cost + target profit / Contribution margin per unit

= £700000 + £700000 / £70 units

= £1400000 / £70 units

= £20000 units

According to the aforementioned calculation for necessary sales units, the corporation must

sell £20000 units in order to make a profit of £700,000.

Preparation of memo suggesting the finance manager the importance of contribution:

CONTRIBUTION

Importance of contribution

It enables the organisation to understand the contribution of various corporate lines, as well as

various items and services (Lubben, 2020). It is also beneficial to understand the company's or

product's strengths and weaknesses. It was once used to calculate a company's profit after

selling products and services

Suggestion how contribution margin helps to take business decisions

Contribution margin is a powerful budgeting and decision-making tool that management

accounting objectives and superiors use to make decisions. Here are some examples of how

contribution margin might be used to make business decisions: Minimum selling price is set.

Its most effective method for determining the selling price It will take care of both fixed and

variable costs. It enables the creation of a profit volume chart in order to determine whether or

not the firm is profitable. The chart makes the profit position easier to comprehend.

How contribution affects margin of safety

The fixed cost / contribution margin calculation above shows that whether the contribution

margin is large or low, it influences the value of the break-even point, and as a result, the

margin of safety is impacted since the MOS break-even is less into the company's planned

sales (Khalfan, and Sturluson, 2018).

This notion is being requested to determine how many units must be sold in order to earn

£700,000 in a year, implying that they demand sales units. Here's one formula for calculating the

firm's desired profit:

Required sales units = fixed cost + target profit / Contribution margin per unit

= £700000 + £700000 / £70 units

= £1400000 / £70 units

= £20000 units

According to the aforementioned calculation for necessary sales units, the corporation must

sell £20000 units in order to make a profit of £700,000.

Preparation of memo suggesting the finance manager the importance of contribution:

CONTRIBUTION

Importance of contribution

It enables the organisation to understand the contribution of various corporate lines, as well as

various items and services (Lubben, 2020). It is also beneficial to understand the company's or

product's strengths and weaknesses. It was once used to calculate a company's profit after

selling products and services

Suggestion how contribution margin helps to take business decisions

Contribution margin is a powerful budgeting and decision-making tool that management

accounting objectives and superiors use to make decisions. Here are some examples of how

contribution margin might be used to make business decisions: Minimum selling price is set.

Its most effective method for determining the selling price It will take care of both fixed and

variable costs. It enables the creation of a profit volume chart in order to determine whether or

not the firm is profitable. The chart makes the profit position easier to comprehend.

How contribution affects margin of safety

The fixed cost / contribution margin calculation above shows that whether the contribution

margin is large or low, it influences the value of the break-even point, and as a result, the

margin of safety is impacted since the MOS break-even is less into the company's planned

sales (Khalfan, and Sturluson, 2018).

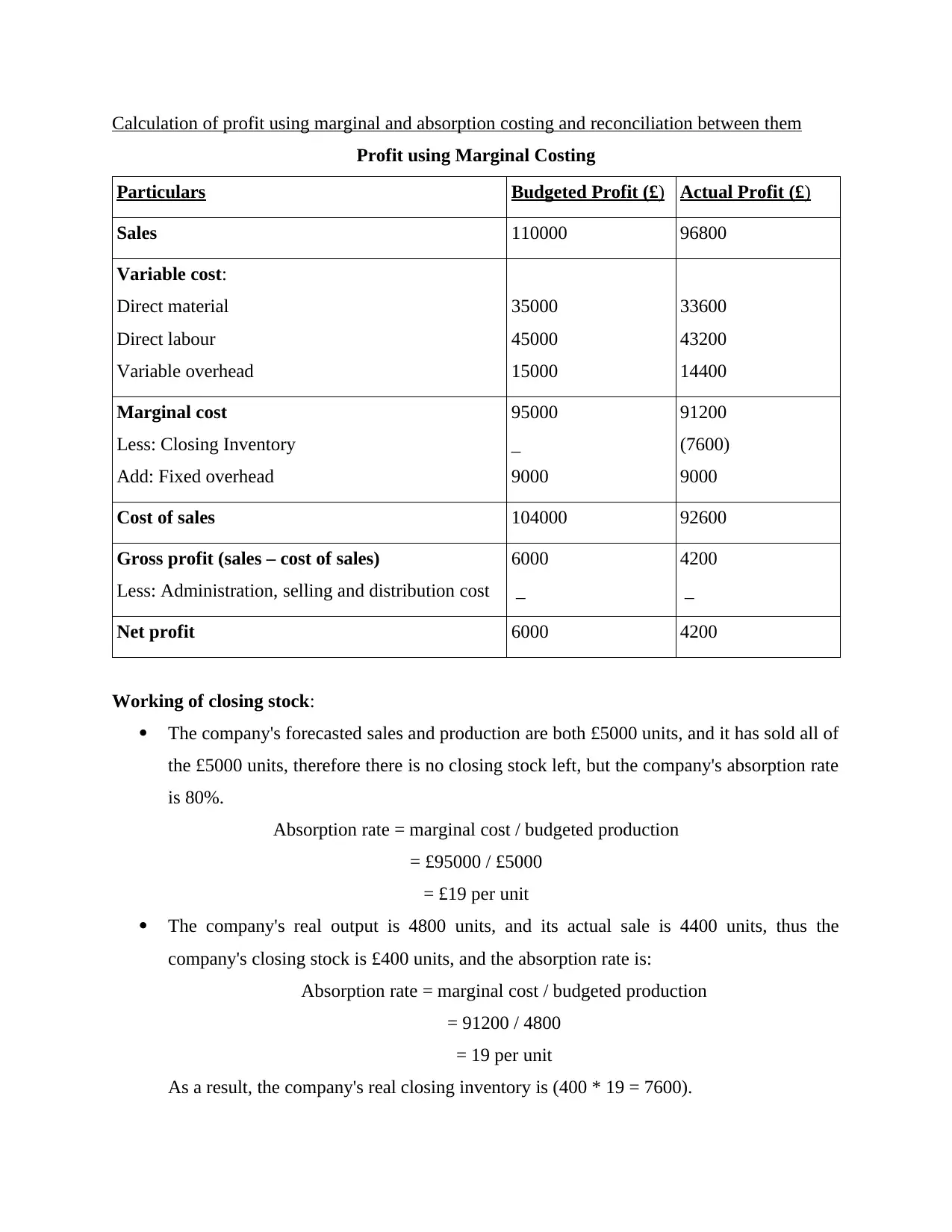

Calculation of profit using marginal and absorption costing and reconciliation between them

Profit using Marginal Costing

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Variable overhead

35000

45000

15000

33600

43200

14400

Marginal cost

Less: Closing Inventory

Add: Fixed overhead

95000

_

9000

91200

(7600)

9000

Cost of sales 104000 92600

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4200

_

Net profit 6000 4200

Working of closing stock:

The company's forecasted sales and production are both £5000 units, and it has sold all of

the £5000 units, therefore there is no closing stock left, but the company's absorption rate

is 80%.

Absorption rate = marginal cost / budgeted production

= £95000 / £5000

= £19 per unit

The company's real output is 4800 units, and its actual sale is 4400 units, thus the

company's closing stock is £400 units, and the absorption rate is:

Absorption rate = marginal cost / budgeted production

= 91200 / 4800

= 19 per unit

As a result, the company's real closing inventory is (400 * 19 = 7600).

Profit using Marginal Costing

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Variable overhead

35000

45000

15000

33600

43200

14400

Marginal cost

Less: Closing Inventory

Add: Fixed overhead

95000

_

9000

91200

(7600)

9000

Cost of sales 104000 92600

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4200

_

Net profit 6000 4200

Working of closing stock:

The company's forecasted sales and production are both £5000 units, and it has sold all of

the £5000 units, therefore there is no closing stock left, but the company's absorption rate

is 80%.

Absorption rate = marginal cost / budgeted production

= £95000 / £5000

= £19 per unit

The company's real output is 4800 units, and its actual sale is 4400 units, thus the

company's closing stock is £400 units, and the absorption rate is:

Absorption rate = marginal cost / budgeted production

= 91200 / 4800

= 19 per unit

As a result, the company's real closing inventory is (400 * 19 = 7600).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

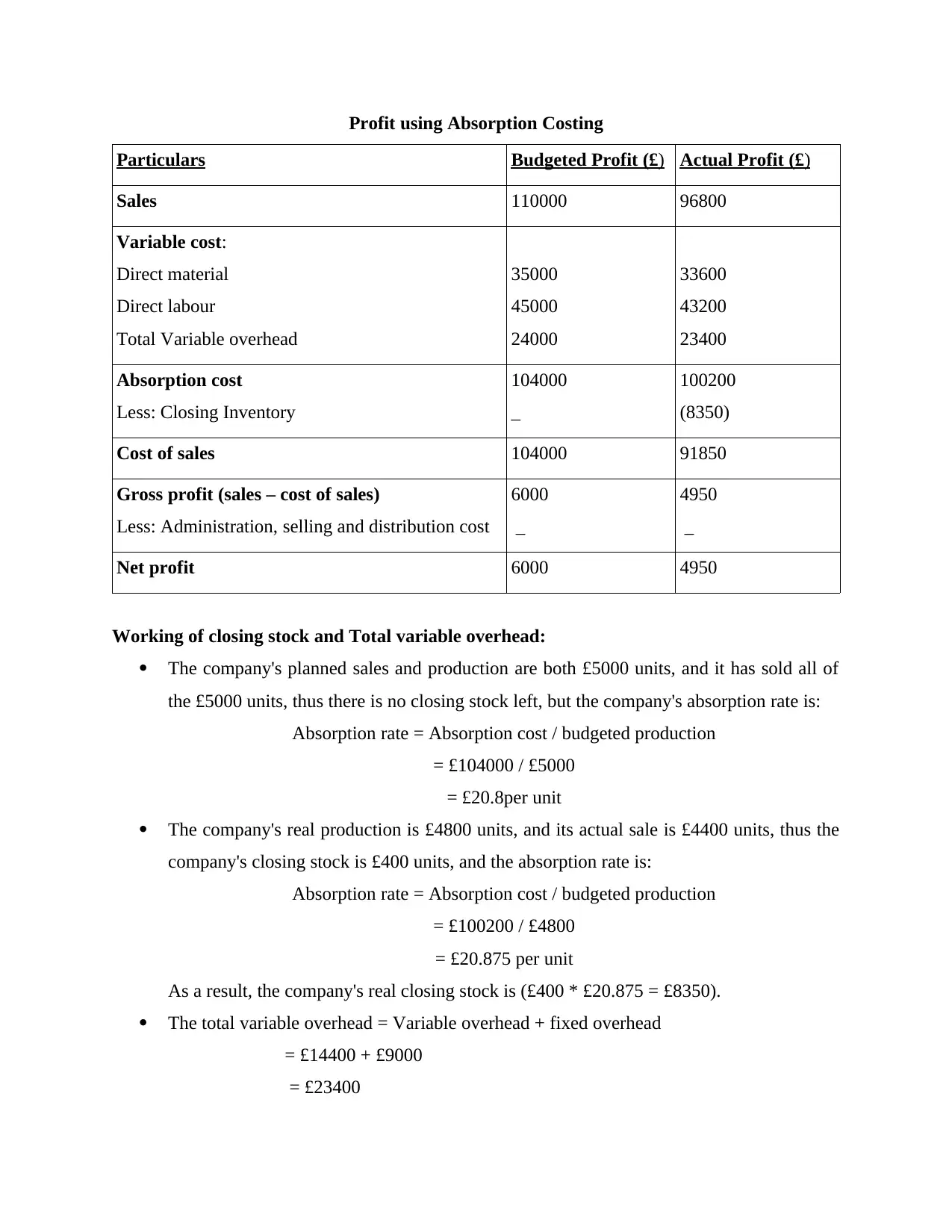

Profit using Absorption Costing

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Total Variable overhead

35000

45000

24000

33600

43200

23400

Absorption cost

Less: Closing Inventory

104000

_

100200

(8350)

Cost of sales 104000 91850

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4950

_

Net profit 6000 4950

Working of closing stock and Total variable overhead:

The company's planned sales and production are both £5000 units, and it has sold all of

the £5000 units, thus there is no closing stock left, but the company's absorption rate is:

Absorption rate = Absorption cost / budgeted production

= £104000 / £5000

= £20.8per unit

The company's real production is £4800 units, and its actual sale is £4400 units, thus the

company's closing stock is £400 units, and the absorption rate is:

Absorption rate = Absorption cost / budgeted production

= £100200 / £4800

= £20.875 per unit

As a result, the company's real closing stock is (£400 * £20.875 = £8350).

The total variable overhead = Variable overhead + fixed overhead

= £14400 + £9000

= £23400

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Total Variable overhead

35000

45000

24000

33600

43200

23400

Absorption cost

Less: Closing Inventory

104000

_

100200

(8350)

Cost of sales 104000 91850

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4950

_

Net profit 6000 4950

Working of closing stock and Total variable overhead:

The company's planned sales and production are both £5000 units, and it has sold all of

the £5000 units, thus there is no closing stock left, but the company's absorption rate is:

Absorption rate = Absorption cost / budgeted production

= £104000 / £5000

= £20.8per unit

The company's real production is £4800 units, and its actual sale is £4400 units, thus the

company's closing stock is £400 units, and the absorption rate is:

Absorption rate = Absorption cost / budgeted production

= £100200 / £4800

= £20.875 per unit

As a result, the company's real closing stock is (£400 * £20.875 = £8350).

The total variable overhead = Variable overhead + fixed overhead

= £14400 + £9000

= £23400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

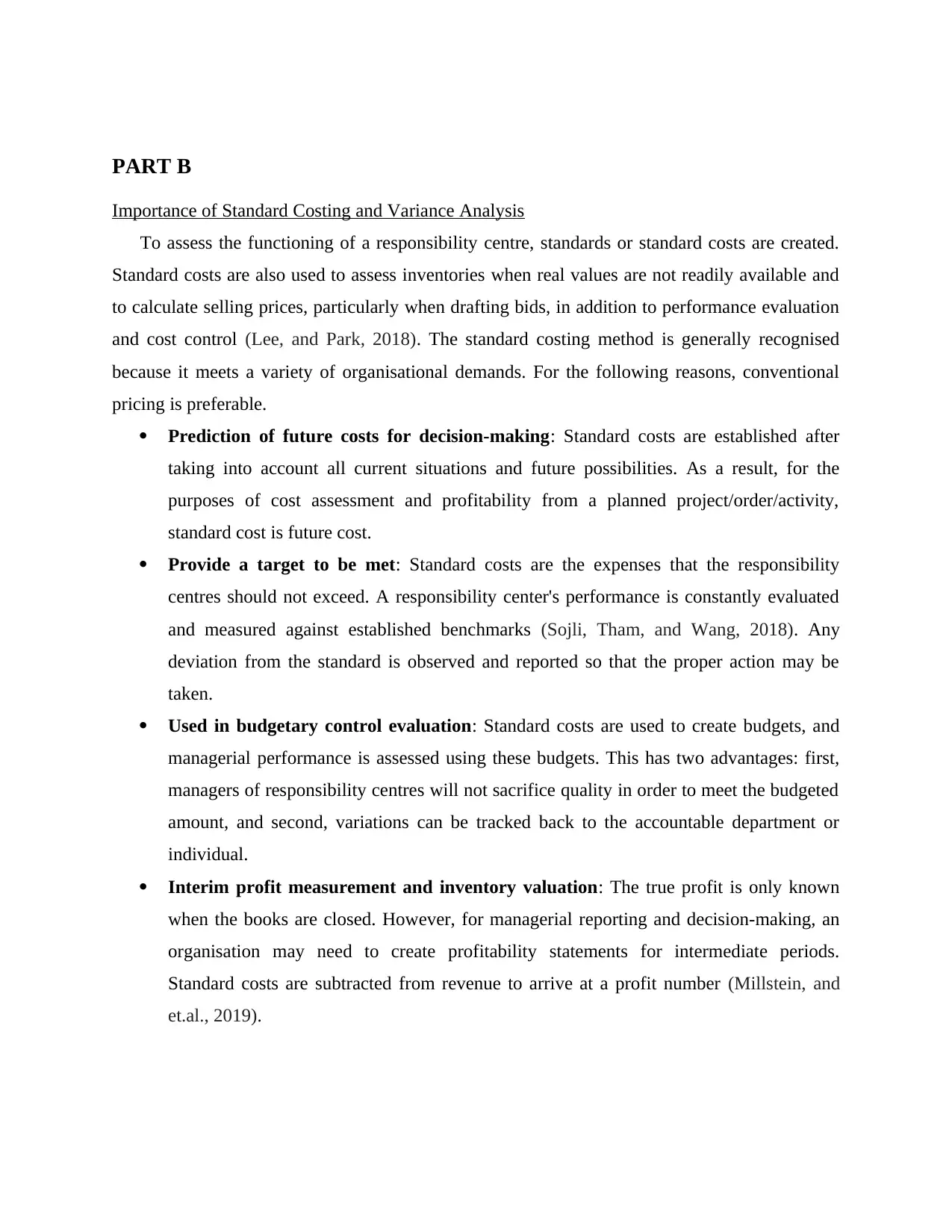

Importance of Standard Costing and Variance Analysis

To assess the functioning of a responsibility centre, standards or standard costs are created.

Standard costs are also used to assess inventories when real values are not readily available and

to calculate selling prices, particularly when drafting bids, in addition to performance evaluation

and cost control (Lee, and Park, 2018). The standard costing method is generally recognised

because it meets a variety of organisational demands. For the following reasons, conventional

pricing is preferable.

Prediction of future costs for decision-making: Standard costs are established after

taking into account all current situations and future possibilities. As a result, for the

purposes of cost assessment and profitability from a planned project/order/activity,

standard cost is future cost.

Provide a target to be met: Standard costs are the expenses that the responsibility

centres should not exceed. A responsibility center's performance is constantly evaluated

and measured against established benchmarks (Sojli, Tham, and Wang, 2018). Any

deviation from the standard is observed and reported so that the proper action may be

taken.

Used in budgetary control evaluation: Standard costs are used to create budgets, and

managerial performance is assessed using these budgets. This has two advantages: first,

managers of responsibility centres will not sacrifice quality in order to meet the budgeted

amount, and second, variations can be tracked back to the accountable department or

individual.

Interim profit measurement and inventory valuation: The true profit is only known

when the books are closed. However, for managerial reporting and decision-making, an

organisation may need to create profitability statements for intermediate periods.

Standard costs are subtracted from revenue to arrive at a profit number (Millstein, and

et.al., 2019).

Importance of Standard Costing and Variance Analysis

To assess the functioning of a responsibility centre, standards or standard costs are created.

Standard costs are also used to assess inventories when real values are not readily available and

to calculate selling prices, particularly when drafting bids, in addition to performance evaluation

and cost control (Lee, and Park, 2018). The standard costing method is generally recognised

because it meets a variety of organisational demands. For the following reasons, conventional

pricing is preferable.

Prediction of future costs for decision-making: Standard costs are established after

taking into account all current situations and future possibilities. As a result, for the

purposes of cost assessment and profitability from a planned project/order/activity,

standard cost is future cost.

Provide a target to be met: Standard costs are the expenses that the responsibility

centres should not exceed. A responsibility center's performance is constantly evaluated

and measured against established benchmarks (Sojli, Tham, and Wang, 2018). Any

deviation from the standard is observed and reported so that the proper action may be

taken.

Used in budgetary control evaluation: Standard costs are used to create budgets, and

managerial performance is assessed using these budgets. This has two advantages: first,

managers of responsibility centres will not sacrifice quality in order to meet the budgeted

amount, and second, variations can be tracked back to the accountable department or

individual.

Interim profit measurement and inventory valuation: The true profit is only known

when the books are closed. However, for managerial reporting and decision-making, an

organisation may need to create profitability statements for intermediate periods.

Standard costs are subtracted from revenue to arrive at a profit number (Millstein, and

et.al., 2019).

Calculation of material and labour variance along with comment on them

Material price variance: It calculates the variation in material costs caused by the

difference between the actual material purchase price and the standard material price. The

following is the formula for calculating the same:

= Actual Quantity * (Standard Price – Actual Price)

= (5 * 10000) * (4 -6)

= 100000 Adverse

This indicates that expenditures have been exceeded in comparison to budgets, which

must be monitored and kept under control in order to keep the price of final goods under

control.

Material usage variance: It calculates the cost of materials as a function of their

use/consumption. The following is the formula for calculating the same:

= Standard Price * (Standard Quantity – Actual Quantity)

= 4 * {(10000*4 – 5*10000)}

= 4 * (40000 – 50000)

= 40000 Adverse

This indicates that more raw material was utilised in the end goods than was budgeted,

indicating that the cost of inputs used by the business must be managed.

Labour rate variance: The discrepancy between the actual rate paid and the standard

rate causes labour rate variation. It's a lot like material price variation (Safiullah, and

Shamsuddin, 2019). The following is the formula for determining the labour rate

variance.

= Actual Time * (Standard Rate - Actual Rate)

= (10000 * 3) * (27 – 30)

= 90000 Adverse

This demonstrates that the labour price is higher than the industry standard, resulting in a

90000 Pound rise in the company's costs.

Labour efficiency variance: The difference in working hours from the conventional

working hour causes labour efficiency variance (Daher, and Ismail, 2018). Below is the

formula for calculating the efficiency variance.

= Standard rate * (Standard time – Actual time)

Material price variance: It calculates the variation in material costs caused by the

difference between the actual material purchase price and the standard material price. The

following is the formula for calculating the same:

= Actual Quantity * (Standard Price – Actual Price)

= (5 * 10000) * (4 -6)

= 100000 Adverse

This indicates that expenditures have been exceeded in comparison to budgets, which

must be monitored and kept under control in order to keep the price of final goods under

control.

Material usage variance: It calculates the cost of materials as a function of their

use/consumption. The following is the formula for calculating the same:

= Standard Price * (Standard Quantity – Actual Quantity)

= 4 * {(10000*4 – 5*10000)}

= 4 * (40000 – 50000)

= 40000 Adverse

This indicates that more raw material was utilised in the end goods than was budgeted,

indicating that the cost of inputs used by the business must be managed.

Labour rate variance: The discrepancy between the actual rate paid and the standard

rate causes labour rate variation. It's a lot like material price variation (Safiullah, and

Shamsuddin, 2019). The following is the formula for determining the labour rate

variance.

= Actual Time * (Standard Rate - Actual Rate)

= (10000 * 3) * (27 – 30)

= 90000 Adverse

This demonstrates that the labour price is higher than the industry standard, resulting in a

90000 Pound rise in the company's costs.

Labour efficiency variance: The difference in working hours from the conventional

working hour causes labour efficiency variance (Daher, and Ismail, 2018). Below is the

formula for calculating the efficiency variance.

= Standard rate * (Standard time – Actual time)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 27 * (3 -3)

= Nil

This demonstrates that the actual and predicted time to create one unit are the same,

implying that labour has been operating at maximum efficiency.

Fixed overhead efficiency variance: This is the distinction between absorbed fixed

overhead and conventional fixed overhead (Bu, and et.al., 2021). The following is the

formula for computing the above variance:

= (Recovered overhead – Standard overhead)

= (15000- 20000)

= 5000 Adverse

This demonstrates that the organisation is incurring additional overhead, which should be

avoided because it has an impact on their company and productivity.

Preparation of budget for controlling the operations

The following is the financial statement for Apparel Plc.

Particular Budget

Direct Material (4 * 4 * 10000) 160000

Add: Direct Labour (3 * 9 * 10000) 270000

Prime Cost 430000

Add: Variable Overhead (2 * 3 * 10000) 60000

Add: Fixed budget Cost 20000

Total Budgeted Cost of Apparel Plc 510000

CONCLUSION

Two alternative case situations with different firms have been shown in the preceding report.

It consists of two companies: Lobelia ltd, for which the margin of safety, contribution per unit,

and other metrics were computed; and Apparel plc, for which the material and labour variances

were calculated using cost data to analyse and interpret the deviation.

= Nil

This demonstrates that the actual and predicted time to create one unit are the same,

implying that labour has been operating at maximum efficiency.

Fixed overhead efficiency variance: This is the distinction between absorbed fixed

overhead and conventional fixed overhead (Bu, and et.al., 2021). The following is the

formula for computing the above variance:

= (Recovered overhead – Standard overhead)

= (15000- 20000)

= 5000 Adverse

This demonstrates that the organisation is incurring additional overhead, which should be

avoided because it has an impact on their company and productivity.

Preparation of budget for controlling the operations

The following is the financial statement for Apparel Plc.

Particular Budget

Direct Material (4 * 4 * 10000) 160000

Add: Direct Labour (3 * 9 * 10000) 270000

Prime Cost 430000

Add: Variable Overhead (2 * 3 * 10000) 60000

Add: Fixed budget Cost 20000

Total Budgeted Cost of Apparel Plc 510000

CONCLUSION

Two alternative case situations with different firms have been shown in the preceding report.

It consists of two companies: Lobelia ltd, for which the margin of safety, contribution per unit,

and other metrics were computed; and Apparel plc, for which the material and labour variances

were calculated using cost data to analyse and interpret the deviation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Jiang, F., and et.al., 2020. Capital markets, financial institutions, and corporate finance in

China. Journal of Corporate Finance, 63, p.101309.

Ross, S.A., and et.al., 2019. Corporate finance (pp. 880-86). McGraw-Hill Education.

Kong, D. and Xin, Q., 2019. Corporate finance in China. China Finance Review International.

Lubben, S.J., 2020. Corporate Finance. Wolters Kluwer Law & Business.

Khalfan, T. and Sturluson, J.Þ., 2018. Corporate finance approaches of Icelandic private firms

after the financial crisis. Managerial Finance.

Lee, H. and Park, K., 2018. Advances in the corporate finance literature: a survey of recent

studies on Korea. Managerial Finance.

Sojli, E., Tham, W.W. and Wang, W., 2018. Time-varying Group Unobserved Heterogeneity in

Finance. Available at SSRN 3258048.

Millstein, I., and et.al., 2019. Session I: corporate purpose and governance. Journal of Applied

Corporate Finance, 31(3), pp.10-25.

Safiullah, M. and Shamsuddin, A., 2019. Risk-adjusted efficiency and corporate governance:

Evidence from Islamic and conventional banks. Journal of Corporate Finance, 55,

pp.105-140.

Bu, L., and et.al., 2021. Talented inside directors and corporate social responsibility: A tale of

two roles. Journal of Corporate Finance, 70, p.102044.

Daher, M.M. and Ismail, A.K., 2018. Debt covenants and corporate acquisitions. Journal of

Corporate Finance, 53, pp.174-201.

Books and Journals

Jiang, F., and et.al., 2020. Capital markets, financial institutions, and corporate finance in

China. Journal of Corporate Finance, 63, p.101309.

Ross, S.A., and et.al., 2019. Corporate finance (pp. 880-86). McGraw-Hill Education.

Kong, D. and Xin, Q., 2019. Corporate finance in China. China Finance Review International.

Lubben, S.J., 2020. Corporate Finance. Wolters Kluwer Law & Business.

Khalfan, T. and Sturluson, J.Þ., 2018. Corporate finance approaches of Icelandic private firms

after the financial crisis. Managerial Finance.

Lee, H. and Park, K., 2018. Advances in the corporate finance literature: a survey of recent

studies on Korea. Managerial Finance.

Sojli, E., Tham, W.W. and Wang, W., 2018. Time-varying Group Unobserved Heterogeneity in

Finance. Available at SSRN 3258048.

Millstein, I., and et.al., 2019. Session I: corporate purpose and governance. Journal of Applied

Corporate Finance, 31(3), pp.10-25.

Safiullah, M. and Shamsuddin, A., 2019. Risk-adjusted efficiency and corporate governance:

Evidence from Islamic and conventional banks. Journal of Corporate Finance, 55,

pp.105-140.

Bu, L., and et.al., 2021. Talented inside directors and corporate social responsibility: A tale of

two roles. Journal of Corporate Finance, 70, p.102044.

Daher, M.M. and Ismail, A.K., 2018. Debt covenants and corporate acquisitions. Journal of

Corporate Finance, 53, pp.174-201.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.