BUS708 Statistics and Data Analysis: Tax Return Lodgement Report

VerifiedAdded on 2020/05/28

|11

|1933

|211

Report

AI Summary

This report analyzes tax return data, primarily focusing on the lodgement methods employed by Australians and international students. The study utilizes datasets from the Australian Taxation Office (ATO) and a survey of international students to assess the preferences for lodging tax returns through registered tax agents versus self-lodgement. Statistical analyses, including frequency tables, confidence intervals, and chi-square tests, are conducted to examine the relationship between lodgement methods, age groups, total income amounts, and total deduction amounts. The findings reveal a strong preference for tax agents across both datasets, with a positive correlation between total income and the use of tax agents. Furthermore, a positive relationship is identified between total income and total deduction amounts. The report concludes by highlighting the importance of these findings and suggests further investigation into the relationship between lodgement methods and gender.

Running Head: BUS708 STATISTICS AND DATA ANALYSIS

BUS708

Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

BUS708

Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUS708 STATISTICS AND DATA ANALYSIS

Table of Contents

Section 1: Introduction................................................................................................................................2

1.1 Introduction.......................................................................................................................................2

1.2 Explanation of the Tax Return Dataset..............................................................................................2

1.3 Explanation of the International Students Dataset............................................................................2

Section 2: Lodgment Method – Dataset 1...................................................................................................2

Section 3: Lodgement Method – Dataset 2.................................................................................................3

Section 4: Lodgement Method and Age Group...........................................................................................5

Section 5: Lodgement Method and Total Income Amount..........................................................................6

Section 6: Total Income Amount and Total Deduction Amount..................................................................7

Section 7: Conclusion..................................................................................................................................8

References...................................................................................................................................................9

Table of Contents

Section 1: Introduction................................................................................................................................2

1.1 Introduction.......................................................................................................................................2

1.2 Explanation of the Tax Return Dataset..............................................................................................2

1.3 Explanation of the International Students Dataset............................................................................2

Section 2: Lodgment Method – Dataset 1...................................................................................................2

Section 3: Lodgement Method – Dataset 2.................................................................................................3

Section 4: Lodgement Method and Age Group...........................................................................................5

Section 5: Lodgement Method and Total Income Amount..........................................................................6

Section 6: Total Income Amount and Total Deduction Amount..................................................................7

Section 7: Conclusion..................................................................................................................................8

References...................................................................................................................................................9

2BUS708 STATISTICS AND DATA ANALYSIS

Section 1: Introduction

1.1 Introduction

Lodging a tax return at the end of each financial year is important for a lot of people in Australia.

The people of Australia can do this by preparing and lodging their tax returns by themselves or get it

done by paying any registered tax agent. According to Kennedy et al. (2017), most of the people of

Australia prefer to get their lodgements done with the help of tax agents. This is a very vital work and

preparing their own tax returns might cause some errors which will be a problem for the individual in

the later years. So unless they are an expert in this matter, people prefer to get it done by agents. This

study mainly aims to find out the proportion of people who are lodging their tax returns by themselves

and with the help of agents. The relationships between total income, lodgement method and deduction

amount are also to be assessed. The preference of the international students on the lodgement

methods of tax return are also to be assessed.

1.2 Explanation of the Tax Return Dataset

The first dataset has been collected from the Australian Taxation Office (ATO). This is a subset of

1000 people of the 2013-2014 dataset available on their website. The variables that are involved in the

dataset are Gender, Age Range, Lodgement Method, Total income and total deduction. Here, the

variables Gender, Age Range and Lodgement Method are categorical variables and the variables total

income and total deductions are continuous variables. The data is secondary as it is collected from the

ATO website. The first five cases of the dataset are attached in table 1.1.

Table 1.1: First five cases of Tax Return Dataset

1.3 Explanation of the International Students Dataset

Data on the preference of international students were collected with the help of a survey. A

sample of 100 students were asked about their preferences of their tax return lodgement method. This

is a primary data as it has been collected directly from the students for the purpose of the study and

were not pre-recorded. This is a categorical variable.

Section 2: Lodgement Method – Dataset 1

For dataset 1, it can be seen that out of 1000 people, 738 people prefer lodging their tax returns

with the help of registered tax agents. Thus, it can be said that most of the people of Australia prefer

lodging tax returns with the help of agents.

Table 2.1: Frequency table for Lodgement Method of the People of Australia

Row Labels Count of Lodgement

A 738

S 262

Section 1: Introduction

1.1 Introduction

Lodging a tax return at the end of each financial year is important for a lot of people in Australia.

The people of Australia can do this by preparing and lodging their tax returns by themselves or get it

done by paying any registered tax agent. According to Kennedy et al. (2017), most of the people of

Australia prefer to get their lodgements done with the help of tax agents. This is a very vital work and

preparing their own tax returns might cause some errors which will be a problem for the individual in

the later years. So unless they are an expert in this matter, people prefer to get it done by agents. This

study mainly aims to find out the proportion of people who are lodging their tax returns by themselves

and with the help of agents. The relationships between total income, lodgement method and deduction

amount are also to be assessed. The preference of the international students on the lodgement

methods of tax return are also to be assessed.

1.2 Explanation of the Tax Return Dataset

The first dataset has been collected from the Australian Taxation Office (ATO). This is a subset of

1000 people of the 2013-2014 dataset available on their website. The variables that are involved in the

dataset are Gender, Age Range, Lodgement Method, Total income and total deduction. Here, the

variables Gender, Age Range and Lodgement Method are categorical variables and the variables total

income and total deductions are continuous variables. The data is secondary as it is collected from the

ATO website. The first five cases of the dataset are attached in table 1.1.

Table 1.1: First five cases of Tax Return Dataset

1.3 Explanation of the International Students Dataset

Data on the preference of international students were collected with the help of a survey. A

sample of 100 students were asked about their preferences of their tax return lodgement method. This

is a primary data as it has been collected directly from the students for the purpose of the study and

were not pre-recorded. This is a categorical variable.

Section 2: Lodgement Method – Dataset 1

For dataset 1, it can be seen that out of 1000 people, 738 people prefer lodging their tax returns

with the help of registered tax agents. Thus, it can be said that most of the people of Australia prefer

lodging tax returns with the help of agents.

Table 2.1: Frequency table for Lodgement Method of the People of Australia

Row Labels Count of Lodgement

A 738

S 262

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUS708 STATISTICS AND DATA ANALYSIS

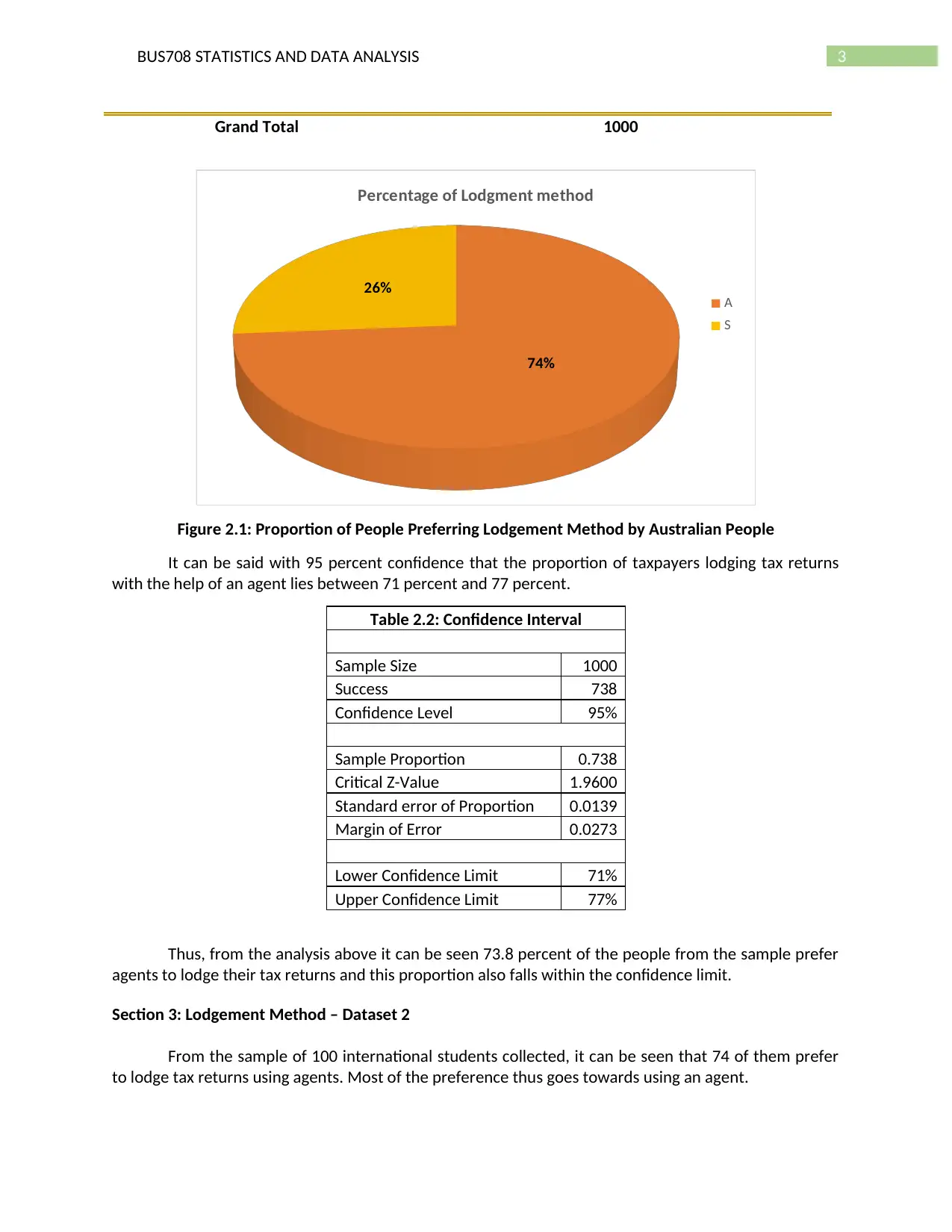

Grand Total 1000

74%

26%

Percentage of Lodgment method

A

S

Figure 2.1: Proportion of People Preferring Lodgement Method by Australian People

It can be said with 95 percent confidence that the proportion of taxpayers lodging tax returns

with the help of an agent lies between 71 percent and 77 percent.

Table 2.2: Confidence Interval

Sample Size 1000

Success 738

Confidence Level 95%

Sample Proportion 0.738

Critical Z-Value 1.9600

Standard error of Proportion 0.0139

Margin of Error 0.0273

Lower Confidence Limit 71%

Upper Confidence Limit 77%

Thus, from the analysis above it can be seen 73.8 percent of the people from the sample prefer

agents to lodge their tax returns and this proportion also falls within the confidence limit.

Section 3: Lodgement Method – Dataset 2

From the sample of 100 international students collected, it can be seen that 74 of them prefer

to lodge tax returns using agents. Most of the preference thus goes towards using an agent.

Grand Total 1000

74%

26%

Percentage of Lodgment method

A

S

Figure 2.1: Proportion of People Preferring Lodgement Method by Australian People

It can be said with 95 percent confidence that the proportion of taxpayers lodging tax returns

with the help of an agent lies between 71 percent and 77 percent.

Table 2.2: Confidence Interval

Sample Size 1000

Success 738

Confidence Level 95%

Sample Proportion 0.738

Critical Z-Value 1.9600

Standard error of Proportion 0.0139

Margin of Error 0.0273

Lower Confidence Limit 71%

Upper Confidence Limit 77%

Thus, from the analysis above it can be seen 73.8 percent of the people from the sample prefer

agents to lodge their tax returns and this proportion also falls within the confidence limit.

Section 3: Lodgement Method – Dataset 2

From the sample of 100 international students collected, it can be seen that 74 of them prefer

to lodge tax returns using agents. Most of the preference thus goes towards using an agent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUS708 STATISTICS AND DATA ANALYSIS

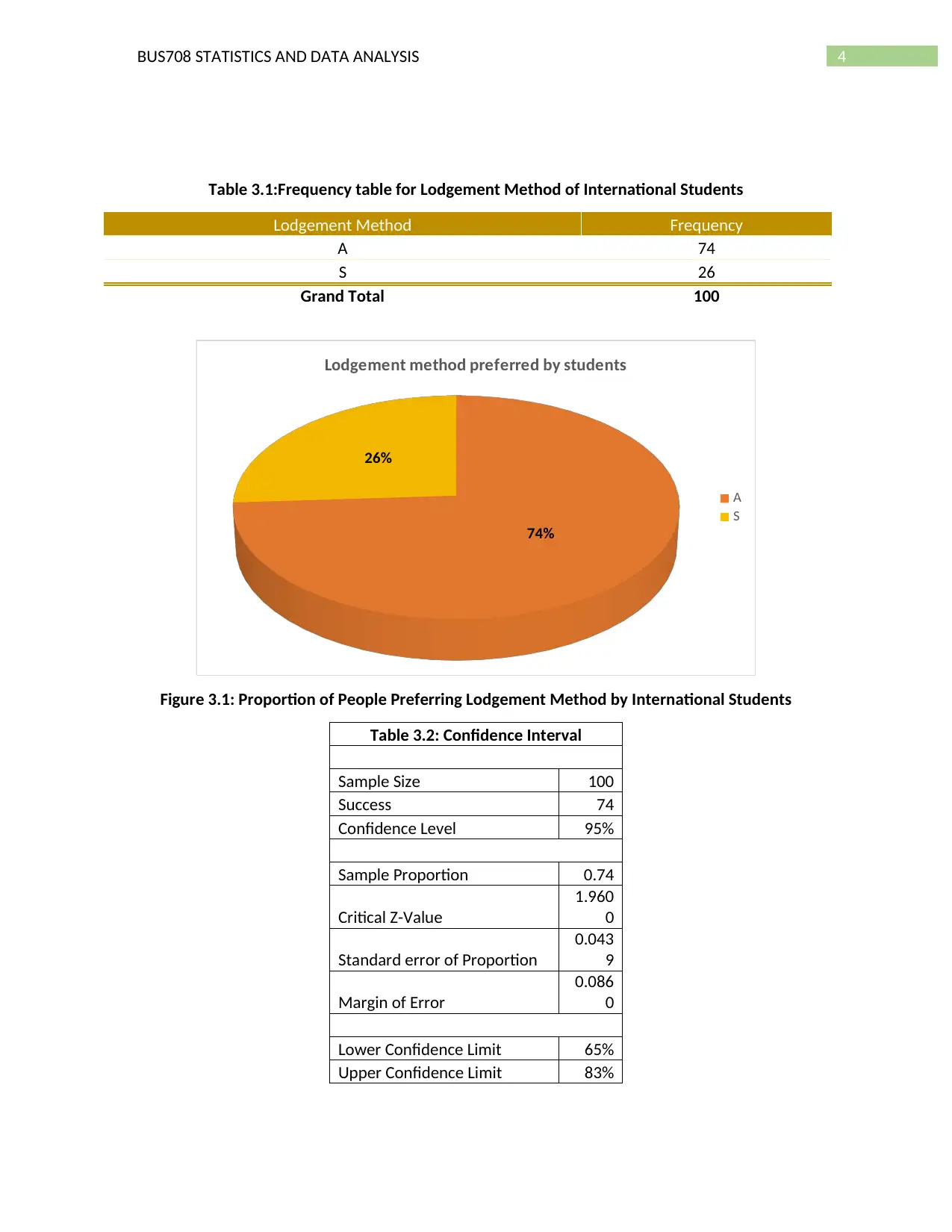

Table 3.1:Frequency table for Lodgement Method of International Students

Lodgement Method Frequency

A 74

S 26

Grand Total 100

74%

26%

Lodgement method preferred by students

A

S

Figure 3.1: Proportion of People Preferring Lodgement Method by International Students

Table 3.2: Confidence Interval

Sample Size 100

Success 74

Confidence Level 95%

Sample Proportion 0.74

Critical Z-Value

1.960

0

Standard error of Proportion

0.043

9

Margin of Error

0.086

0

Lower Confidence Limit 65%

Upper Confidence Limit 83%

Table 3.1:Frequency table for Lodgement Method of International Students

Lodgement Method Frequency

A 74

S 26

Grand Total 100

74%

26%

Lodgement method preferred by students

A

S

Figure 3.1: Proportion of People Preferring Lodgement Method by International Students

Table 3.2: Confidence Interval

Sample Size 100

Success 74

Confidence Level 95%

Sample Proportion 0.74

Critical Z-Value

1.960

0

Standard error of Proportion

0.043

9

Margin of Error

0.086

0

Lower Confidence Limit 65%

Upper Confidence Limit 83%

5BUS708 STATISTICS AND DATA ANALYSIS

It can be said with 95 percent confidence that that the proportion of students preferring agents

over themselves on lodging tax returns lies between 65 percent and 83 percent.

Thus, from the analysis above, it can be seen clearly that most of the students also prefer to give

the responsibility to some experts and not work on their own just like the people of Australia.65 to 83

percent of the students prefer agents. Hence, there is no difference in dataset 1 and dataset 2 in terms

of lodgement method.

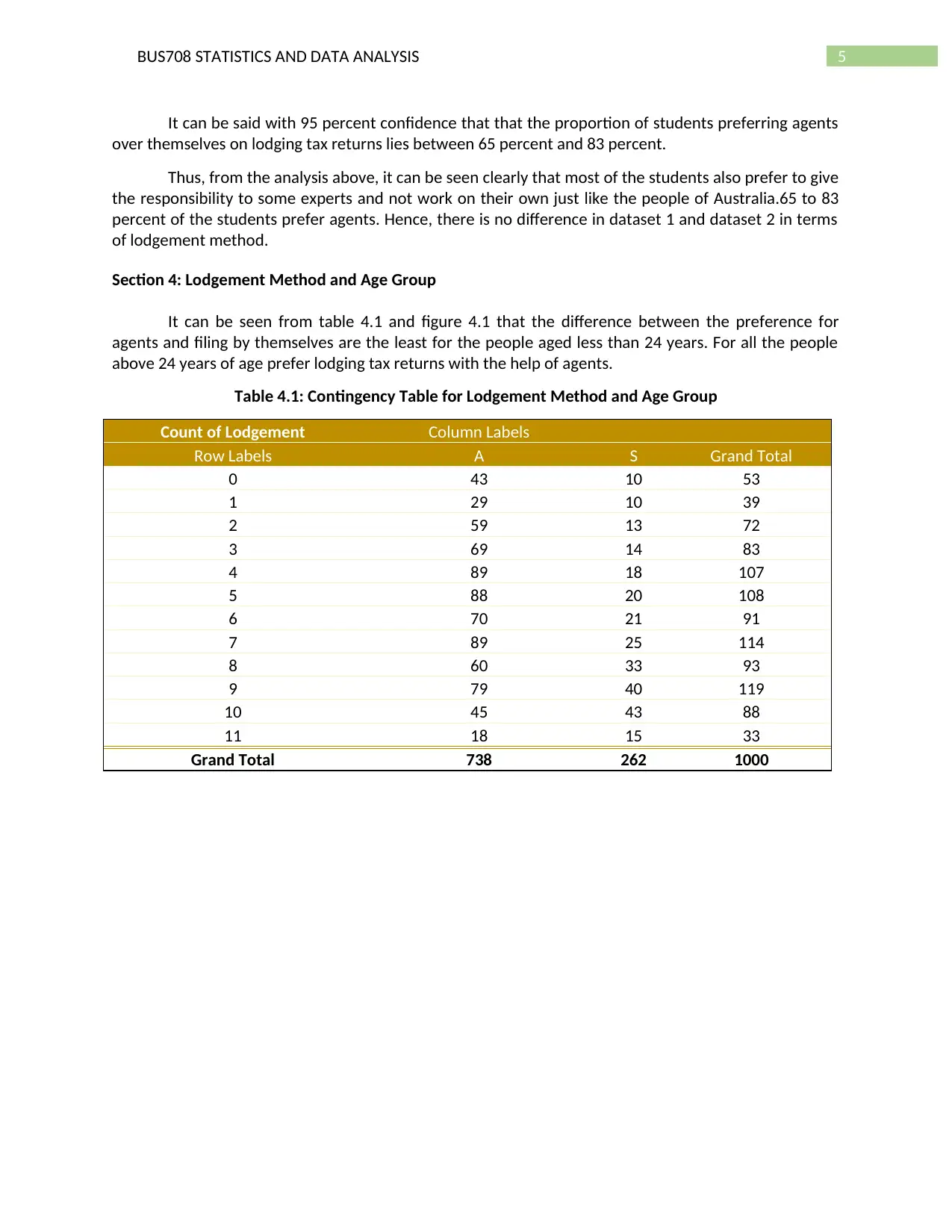

Section 4: Lodgement Method and Age Group

It can be seen from table 4.1 and figure 4.1 that the difference between the preference for

agents and filing by themselves are the least for the people aged less than 24 years. For all the people

above 24 years of age prefer lodging tax returns with the help of agents.

Table 4.1: Contingency Table for Lodgement Method and Age Group

Count of Lodgement Column Labels

Row Labels A S Grand Total

0 43 10 53

1 29 10 39

2 59 13 72

3 69 14 83

4 89 18 107

5 88 20 108

6 70 21 91

7 89 25 114

8 60 33 93

9 79 40 119

10 45 43 88

11 18 15 33

Grand Total 738 262 1000

It can be said with 95 percent confidence that that the proportion of students preferring agents

over themselves on lodging tax returns lies between 65 percent and 83 percent.

Thus, from the analysis above, it can be seen clearly that most of the students also prefer to give

the responsibility to some experts and not work on their own just like the people of Australia.65 to 83

percent of the students prefer agents. Hence, there is no difference in dataset 1 and dataset 2 in terms

of lodgement method.

Section 4: Lodgement Method and Age Group

It can be seen from table 4.1 and figure 4.1 that the difference between the preference for

agents and filing by themselves are the least for the people aged less than 24 years. For all the people

above 24 years of age prefer lodging tax returns with the help of agents.

Table 4.1: Contingency Table for Lodgement Method and Age Group

Count of Lodgement Column Labels

Row Labels A S Grand Total

0 43 10 53

1 29 10 39

2 59 13 72

3 69 14 83

4 89 18 107

5 88 20 108

6 70 21 91

7 89 25 114

8 60 33 93

9 79 40 119

10 45 43 88

11 18 15 33

Grand Total 738 262 1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUS708 STATISTICS AND DATA ANALYSIS

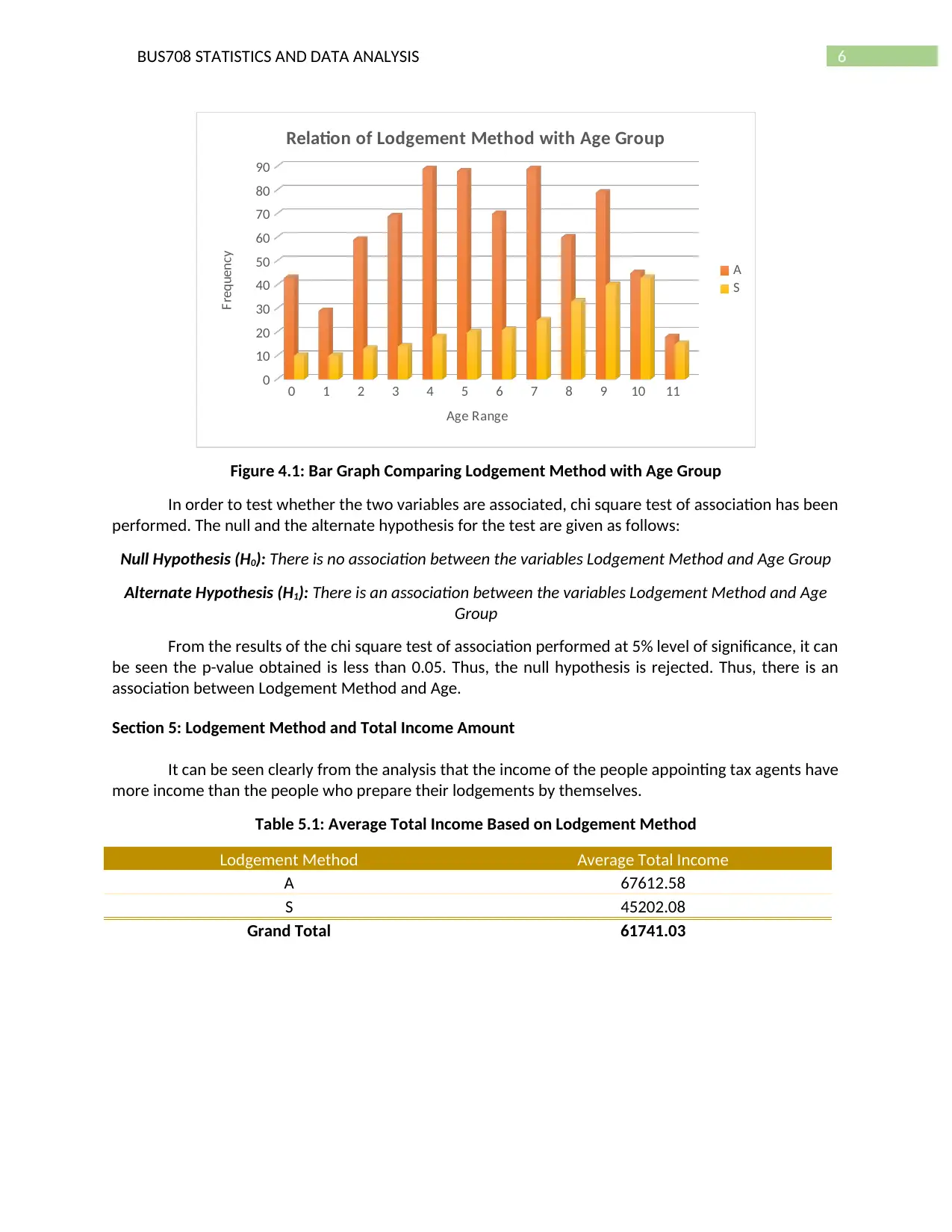

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

Relation of Lodgement Method with Age Group

A

S

Age Range

Frequency

Figure 4.1: Bar Graph Comparing Lodgement Method with Age Group

In order to test whether the two variables are associated, chi square test of association has been

performed. The null and the alternate hypothesis for the test are given as follows:

Null Hypothesis (H0): There is no association between the variables Lodgement Method and Age Group

Alternate Hypothesis (H1): There is an association between the variables Lodgement Method and Age

Group

From the results of the chi square test of association performed at 5% level of significance, it can

be seen the p-value obtained is less than 0.05. Thus, the null hypothesis is rejected. Thus, there is an

association between Lodgement Method and Age.

Section 5: Lodgement Method and Total Income Amount

It can be seen clearly from the analysis that the income of the people appointing tax agents have

more income than the people who prepare their lodgements by themselves.

Table 5.1: Average Total Income Based on Lodgement Method

Lodgement Method Average Total Income

A 67612.58

S 45202.08

Grand Total 61741.03

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

Relation of Lodgement Method with Age Group

A

S

Age Range

Frequency

Figure 4.1: Bar Graph Comparing Lodgement Method with Age Group

In order to test whether the two variables are associated, chi square test of association has been

performed. The null and the alternate hypothesis for the test are given as follows:

Null Hypothesis (H0): There is no association between the variables Lodgement Method and Age Group

Alternate Hypothesis (H1): There is an association between the variables Lodgement Method and Age

Group

From the results of the chi square test of association performed at 5% level of significance, it can

be seen the p-value obtained is less than 0.05. Thus, the null hypothesis is rejected. Thus, there is an

association between Lodgement Method and Age.

Section 5: Lodgement Method and Total Income Amount

It can be seen clearly from the analysis that the income of the people appointing tax agents have

more income than the people who prepare their lodgements by themselves.

Table 5.1: Average Total Income Based on Lodgement Method

Lodgement Method Average Total Income

A 67612.58

S 45202.08

Grand Total 61741.03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUS708 STATISTICS AND DATA ANALYSIS

A

S

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

Average Total Income of Lodgement Method

Lodgement Method

Average Income

Figure 5.1: Average total income of different tax lodgement methods

The average income of the people who appoint tax agents are $67612.58 and that of the people

who prepare by themselves are $45202.08. 50 percent of the people who appoint tax agents earn more

than $46353 and 50 percent of the people who prepare their tax reports by themselves earn below

$35726. The standard deviation of the incomes for both lodgement methods are extremely high. Thus,

the values are not close to the mean income and are scattered a lot from the mean. Moreover, most of

the people earn less than the mean income. There are a lot of outliers to the data.

Table 5.2: Summary measures of total income on different lodgement methods

Descriptive Measures Tax Agent Self-Preparer

Mean 67612.58 45202.08

Standard Error 6398.62 2732.93

Median 46353 35726

Mode 0 0

Standard Deviation 173826.03 44236.40

Sample Variance 30215489951 1956859121

Kurtosis 484.054 18.679

Skewness 20.361 3.408

Range 4308305 380484

Minimum -1942 -7

Maximum 4306363 380477

Sum 49898083 11842946

Count 738 262

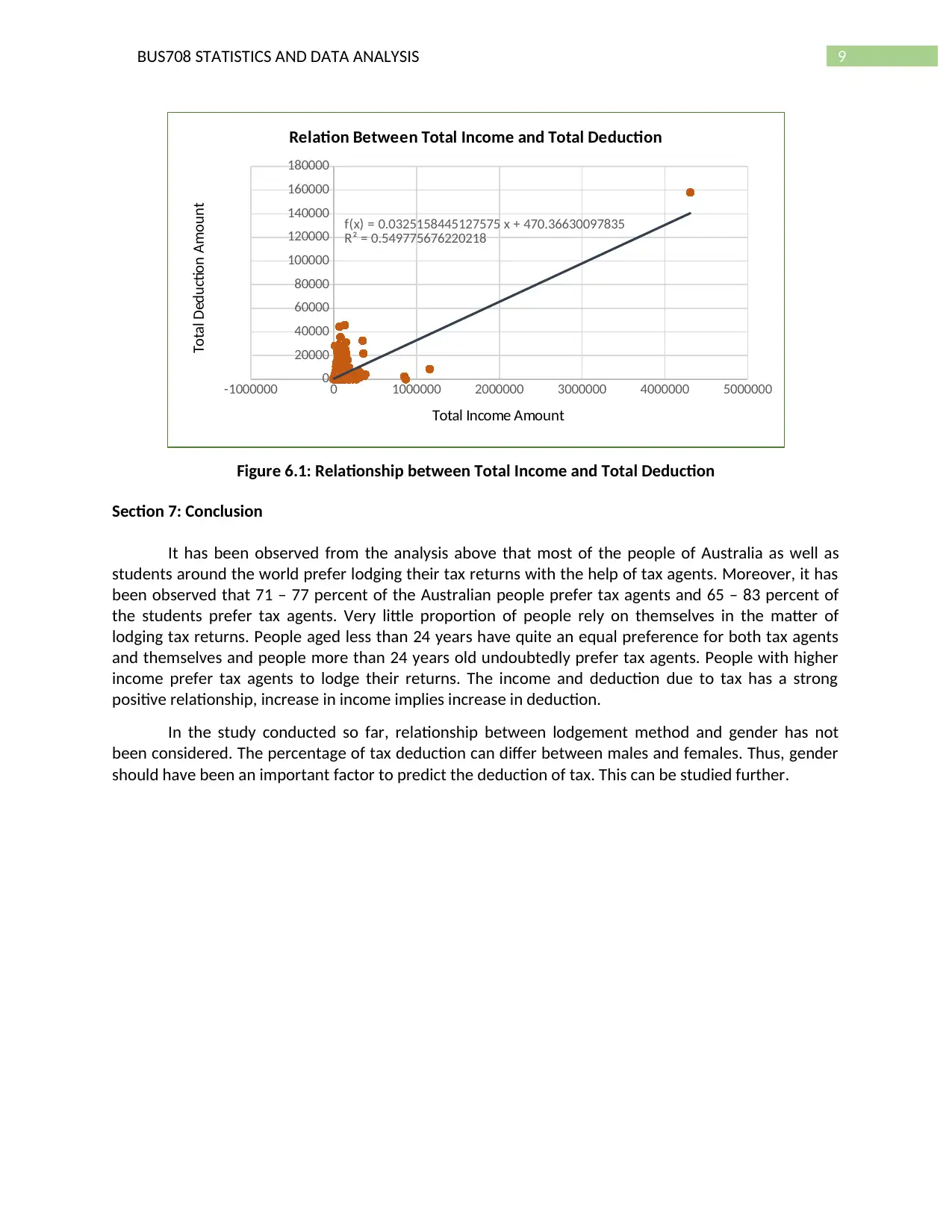

Section 6: Total Income Amount and Total Deduction Amount

The relationship between total income and total deduction are shown diagrammatically with the

help of a scatter diagram. It can be seen clearly from figure 6.1 that the total deduction amount is

A

S

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

Average Total Income of Lodgement Method

Lodgement Method

Average Income

Figure 5.1: Average total income of different tax lodgement methods

The average income of the people who appoint tax agents are $67612.58 and that of the people

who prepare by themselves are $45202.08. 50 percent of the people who appoint tax agents earn more

than $46353 and 50 percent of the people who prepare their tax reports by themselves earn below

$35726. The standard deviation of the incomes for both lodgement methods are extremely high. Thus,

the values are not close to the mean income and are scattered a lot from the mean. Moreover, most of

the people earn less than the mean income. There are a lot of outliers to the data.

Table 5.2: Summary measures of total income on different lodgement methods

Descriptive Measures Tax Agent Self-Preparer

Mean 67612.58 45202.08

Standard Error 6398.62 2732.93

Median 46353 35726

Mode 0 0

Standard Deviation 173826.03 44236.40

Sample Variance 30215489951 1956859121

Kurtosis 484.054 18.679

Skewness 20.361 3.408

Range 4308305 380484

Minimum -1942 -7

Maximum 4306363 380477

Sum 49898083 11842946

Count 738 262

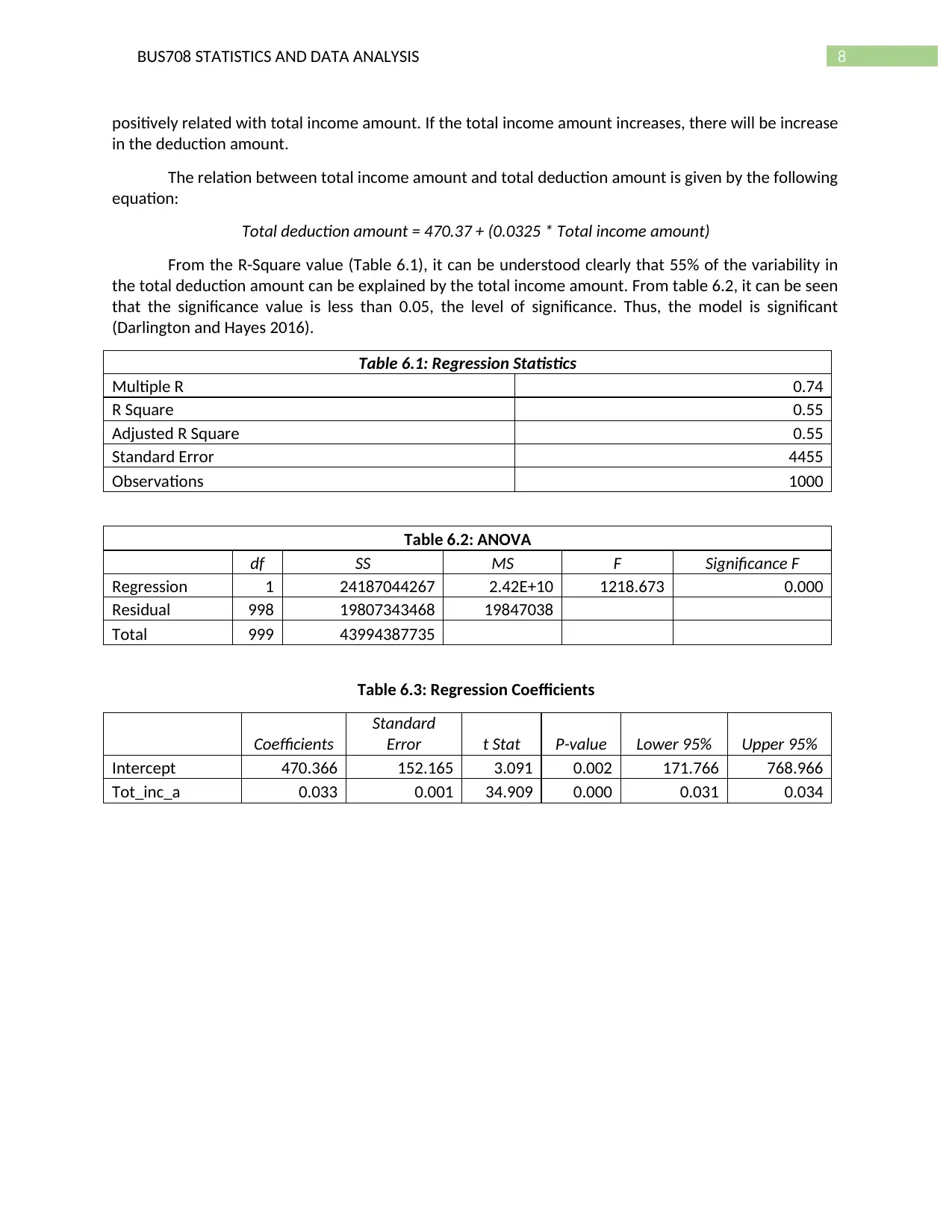

Section 6: Total Income Amount and Total Deduction Amount

The relationship between total income and total deduction are shown diagrammatically with the

help of a scatter diagram. It can be seen clearly from figure 6.1 that the total deduction amount is

8BUS708 STATISTICS AND DATA ANALYSIS

positively related with total income amount. If the total income amount increases, there will be increase

in the deduction amount.

The relation between total income amount and total deduction amount is given by the following

equation:

Total deduction amount = 470.37 + (0.0325 * Total income amount)

From the R-Square value (Table 6.1), it can be understood clearly that 55% of the variability in

the total deduction amount can be explained by the total income amount. From table 6.2, it can be seen

that the significance value is less than 0.05, the level of significance. Thus, the model is significant

(Darlington and Hayes 2016).

Table 6.1: Regression Statistics

Multiple R 0.74

R Square 0.55

Adjusted R Square 0.55

Standard Error 4455

Observations 1000

Table 6.2: ANOVA

df SS MS F Significance F

Regression 1 24187044267 2.42E+10 1218.673 0.000

Residual 998 19807343468 19847038

Total 999 43994387735

Table 6.3: Regression Coefficients

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 470.366 152.165 3.091 0.002 171.766 768.966

Tot_inc_a 0.033 0.001 34.909 0.000 0.031 0.034

positively related with total income amount. If the total income amount increases, there will be increase

in the deduction amount.

The relation between total income amount and total deduction amount is given by the following

equation:

Total deduction amount = 470.37 + (0.0325 * Total income amount)

From the R-Square value (Table 6.1), it can be understood clearly that 55% of the variability in

the total deduction amount can be explained by the total income amount. From table 6.2, it can be seen

that the significance value is less than 0.05, the level of significance. Thus, the model is significant

(Darlington and Hayes 2016).

Table 6.1: Regression Statistics

Multiple R 0.74

R Square 0.55

Adjusted R Square 0.55

Standard Error 4455

Observations 1000

Table 6.2: ANOVA

df SS MS F Significance F

Regression 1 24187044267 2.42E+10 1218.673 0.000

Residual 998 19807343468 19847038

Total 999 43994387735

Table 6.3: Regression Coefficients

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 470.366 152.165 3.091 0.002 171.766 768.966

Tot_inc_a 0.033 0.001 34.909 0.000 0.031 0.034

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUS708 STATISTICS AND DATA ANALYSIS

-1000000 0 1000000 2000000 3000000 4000000 5000000

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

f(x) = 0.0325158445127575 x + 470.36630097835

R² = 0.549775676220218

Relation Between Total Income and Total Deduction

Total Income Amount

Total Deduction Amount

Figure 6.1: Relationship between Total Income and Total Deduction

Section 7: Conclusion

It has been observed from the analysis above that most of the people of Australia as well as

students around the world prefer lodging their tax returns with the help of tax agents. Moreover, it has

been observed that 71 – 77 percent of the Australian people prefer tax agents and 65 – 83 percent of

the students prefer tax agents. Very little proportion of people rely on themselves in the matter of

lodging tax returns. People aged less than 24 years have quite an equal preference for both tax agents

and themselves and people more than 24 years old undoubtedly prefer tax agents. People with higher

income prefer tax agents to lodge their returns. The income and deduction due to tax has a strong

positive relationship, increase in income implies increase in deduction.

In the study conducted so far, relationship between lodgement method and gender has not

been considered. The percentage of tax deduction can differ between males and females. Thus, gender

should have been an important factor to predict the deduction of tax. This can be studied further.

-1000000 0 1000000 2000000 3000000 4000000 5000000

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

f(x) = 0.0325158445127575 x + 470.36630097835

R² = 0.549775676220218

Relation Between Total Income and Total Deduction

Total Income Amount

Total Deduction Amount

Figure 6.1: Relationship between Total Income and Total Deduction

Section 7: Conclusion

It has been observed from the analysis above that most of the people of Australia as well as

students around the world prefer lodging their tax returns with the help of tax agents. Moreover, it has

been observed that 71 – 77 percent of the Australian people prefer tax agents and 65 – 83 percent of

the students prefer tax agents. Very little proportion of people rely on themselves in the matter of

lodging tax returns. People aged less than 24 years have quite an equal preference for both tax agents

and themselves and people more than 24 years old undoubtedly prefer tax agents. People with higher

income prefer tax agents to lodge their returns. The income and deduction due to tax has a strong

positive relationship, increase in income implies increase in deduction.

In the study conducted so far, relationship between lodgement method and gender has not

been considered. The percentage of tax deduction can differ between males and females. Thus, gender

should have been an important factor to predict the deduction of tax. This can be studied further.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUS708 STATISTICS AND DATA ANALYSIS

References

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality hinder economic

growth? New evidence using Australian taxation statistics. Economic Modelling.

Darlington, R.B. and Hayes, A.F., 2016. Regression analysis and linear models: Concepts, applications,

and implementation. Guilford Publications.

References

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality hinder economic

growth? New evidence using Australian taxation statistics. Economic Modelling.

Darlington, R.B. and Hayes, A.F., 2016. Regression analysis and linear models: Concepts, applications,

and implementation. Guilford Publications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.