MBA51: Logicom Financial Performance and Risk Analysis Report

VerifiedAdded on 2022/12/17

|14

|2967

|91

Report

AI Summary

This report presents a comprehensive financial analysis of Logicom, evaluating its performance using key financial ratios. The analysis covers profitability, liquidity, efficiency, and gearing ratios, providing insights into the company's financial health and investment potential. The report investigates key performance indicators, interrelationships between ratios, and limitations of ratio analysis. It also identifies areas for further business growth and appraisal purposes, including credit risk, interest rate risk, and liquidity risk. Furthermore, the report examines various articles analyzing Logicom's financial performance, focusing on share performance, dividend attractiveness, and institutional ownership. The conclusion summarizes the findings, offering recommendations for investors regarding the company's investment viability and long-term prospects.

Interpretation

Of Accounts

Of Accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Analysis of key performing indicators...................................................................................3

Interrelationship between ratios.............................................................................................7

Limitation of ratio analysis.....................................................................................................7

PART B............................................................................................................................................8

Areas to be investigated for further business growth and appraisal purposes........................8

PART C............................................................................................................................................8

Various articles analysing financial performance of Logicom...............................................8

CONCLUSION..............................................................................................................................11

References......................................................................................................................................12

Appendix........................................................................................................................................13

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Analysis of key performing indicators...................................................................................3

Interrelationship between ratios.............................................................................................7

Limitation of ratio analysis.....................................................................................................7

PART B............................................................................................................................................8

Areas to be investigated for further business growth and appraisal purposes........................8

PART C............................................................................................................................................8

Various articles analysing financial performance of Logicom...............................................8

CONCLUSION..............................................................................................................................11

References......................................................................................................................................12

Appendix........................................................................................................................................13

INTRODUCTION

Financial analysis is described as measurement of financial statements and various activities of an

organisation in order to identify efficiency, performance, risk factors, returns, etc. Financial ratios

are determined in order to understand performance structure of an organisation. In order to identify

financial position of an enterprise, various ratios such as profitability ratios, liquidity ratios,

efficiency ratios and investors ratios in so that financial aspect will be determined of an

organisation. In this report, logicom financial statements are being analysed in order to analyse

financial performance in terms of revenue generation, sales volume, profitability and other related

factors. Also summary of relevant ratios will be provided by analysing each of the ratios in an

adequate manner. By analysis of such data, also relevant area of modification will be modified as

per the needs of organisation. Further, requirement of any other analysis of operation performance

in regard to company will be discussed later in the report.

Part A

Analysis of key performing indicators

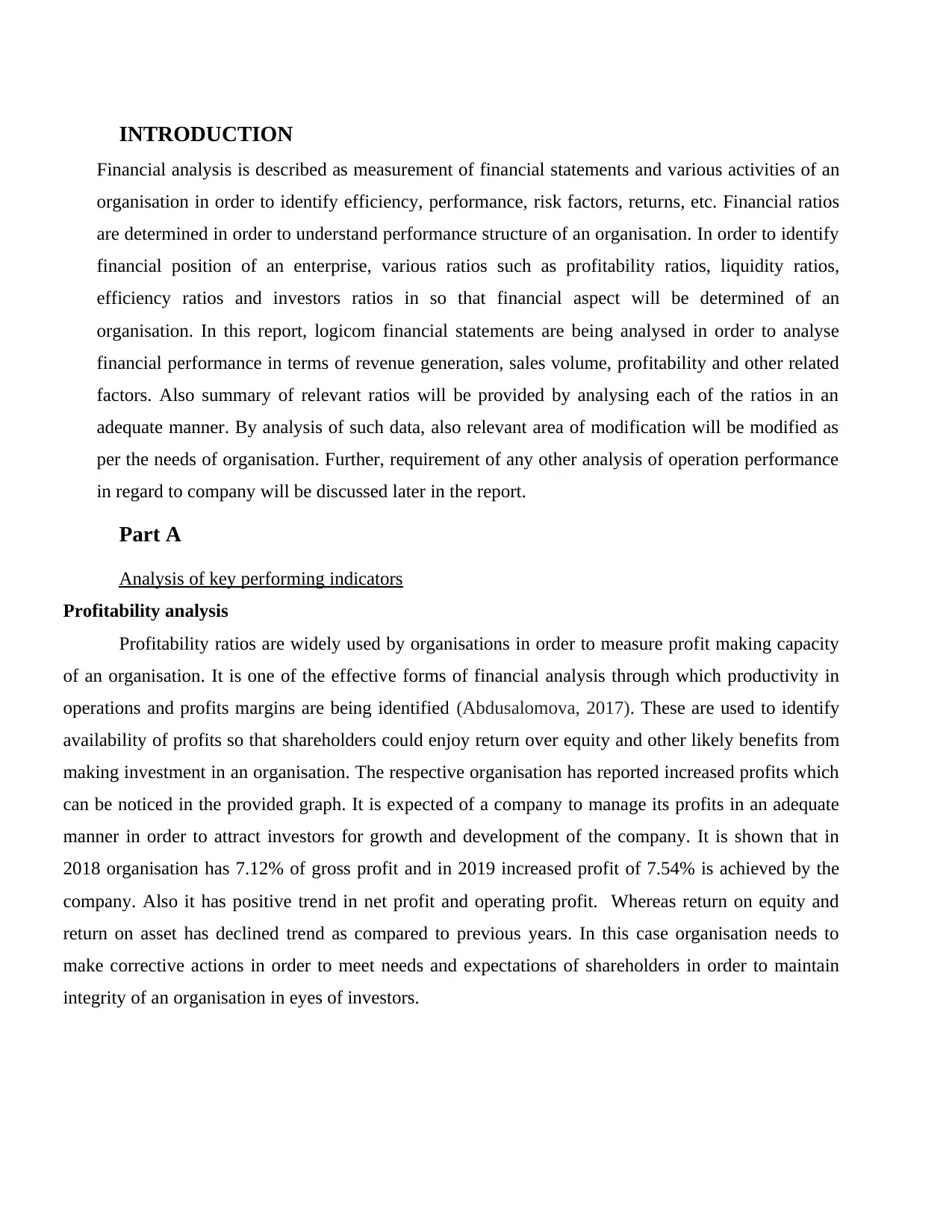

Profitability analysis

Profitability ratios are widely used by organisations in order to measure profit making capacity

of an organisation. It is one of the effective forms of financial analysis through which productivity in

operations and profits margins are being identified (Abdusalomova, 2017). These are used to identify

availability of profits so that shareholders could enjoy return over equity and other likely benefits from

making investment in an organisation. The respective organisation has reported increased profits which

can be noticed in the provided graph. It is expected of a company to manage its profits in an adequate

manner in order to attract investors for growth and development of the company. It is shown that in

2018 organisation has 7.12% of gross profit and in 2019 increased profit of 7.54% is achieved by the

company. Also it has positive trend in net profit and operating profit. Whereas return on equity and

return on asset has declined trend as compared to previous years. In this case organisation needs to

make corrective actions in order to meet needs and expectations of shareholders in order to maintain

integrity of an organisation in eyes of investors.

Financial analysis is described as measurement of financial statements and various activities of an

organisation in order to identify efficiency, performance, risk factors, returns, etc. Financial ratios

are determined in order to understand performance structure of an organisation. In order to identify

financial position of an enterprise, various ratios such as profitability ratios, liquidity ratios,

efficiency ratios and investors ratios in so that financial aspect will be determined of an

organisation. In this report, logicom financial statements are being analysed in order to analyse

financial performance in terms of revenue generation, sales volume, profitability and other related

factors. Also summary of relevant ratios will be provided by analysing each of the ratios in an

adequate manner. By analysis of such data, also relevant area of modification will be modified as

per the needs of organisation. Further, requirement of any other analysis of operation performance

in regard to company will be discussed later in the report.

Part A

Analysis of key performing indicators

Profitability analysis

Profitability ratios are widely used by organisations in order to measure profit making capacity

of an organisation. It is one of the effective forms of financial analysis through which productivity in

operations and profits margins are being identified (Abdusalomova, 2017). These are used to identify

availability of profits so that shareholders could enjoy return over equity and other likely benefits from

making investment in an organisation. The respective organisation has reported increased profits which

can be noticed in the provided graph. It is expected of a company to manage its profits in an adequate

manner in order to attract investors for growth and development of the company. It is shown that in

2018 organisation has 7.12% of gross profit and in 2019 increased profit of 7.54% is achieved by the

company. Also it has positive trend in net profit and operating profit. Whereas return on equity and

return on asset has declined trend as compared to previous years. In this case organisation needs to

make corrective actions in order to meet needs and expectations of shareholders in order to maintain

integrity of an organisation in eyes of investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

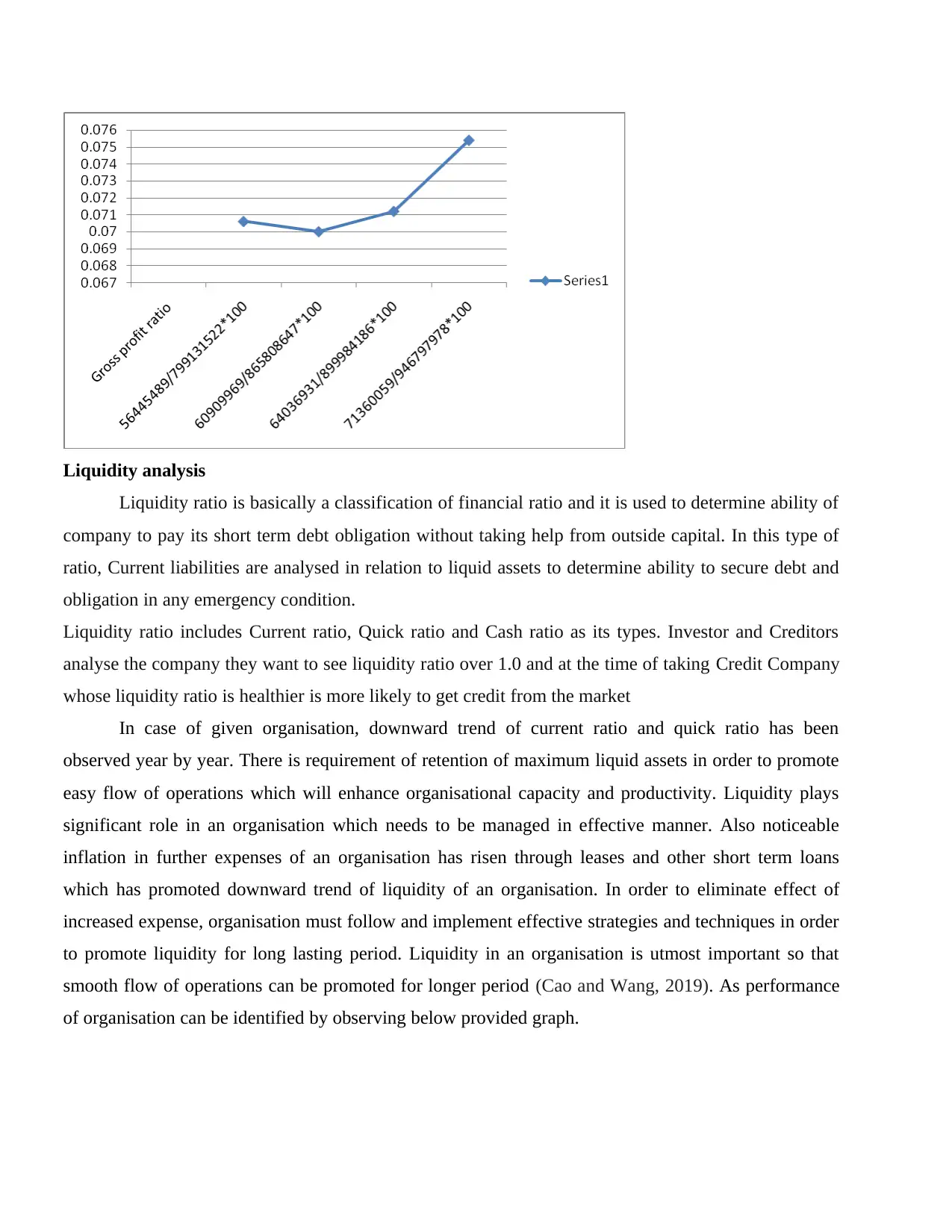

Liquidity analysis

Liquidity ratio is basically a classification of financial ratio and it is used to determine ability of

company to pay its short term debt obligation without taking help from outside capital. In this type of

ratio, Current liabilities are analysed in relation to liquid assets to determine ability to secure debt and

obligation in any emergency condition.

Liquidity ratio includes Current ratio, Quick ratio and Cash ratio as its types. Investor and Creditors

analyse the company they want to see liquidity ratio over 1.0 and at the time of taking Credit Company

whose liquidity ratio is healthier is more likely to get credit from the market

In case of given organisation, downward trend of current ratio and quick ratio has been

observed year by year. There is requirement of retention of maximum liquid assets in order to promote

easy flow of operations which will enhance organisational capacity and productivity. Liquidity plays

significant role in an organisation which needs to be managed in effective manner. Also noticeable

inflation in further expenses of an organisation has risen through leases and other short term loans

which has promoted downward trend of liquidity of an organisation. In order to eliminate effect of

increased expense, organisation must follow and implement effective strategies and techniques in order

to promote liquidity for long lasting period. Liquidity in an organisation is utmost important so that

smooth flow of operations can be promoted for longer period (Cao and Wang, 2019). As performance

of organisation can be identified by observing below provided graph.

Liquidity ratio is basically a classification of financial ratio and it is used to determine ability of

company to pay its short term debt obligation without taking help from outside capital. In this type of

ratio, Current liabilities are analysed in relation to liquid assets to determine ability to secure debt and

obligation in any emergency condition.

Liquidity ratio includes Current ratio, Quick ratio and Cash ratio as its types. Investor and Creditors

analyse the company they want to see liquidity ratio over 1.0 and at the time of taking Credit Company

whose liquidity ratio is healthier is more likely to get credit from the market

In case of given organisation, downward trend of current ratio and quick ratio has been

observed year by year. There is requirement of retention of maximum liquid assets in order to promote

easy flow of operations which will enhance organisational capacity and productivity. Liquidity plays

significant role in an organisation which needs to be managed in effective manner. Also noticeable

inflation in further expenses of an organisation has risen through leases and other short term loans

which has promoted downward trend of liquidity of an organisation. In order to eliminate effect of

increased expense, organisation must follow and implement effective strategies and techniques in order

to promote liquidity for long lasting period. Liquidity in an organisation is utmost important so that

smooth flow of operations can be promoted for longer period (Cao and Wang, 2019). As performance

of organisation can be identified by observing below provided graph.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

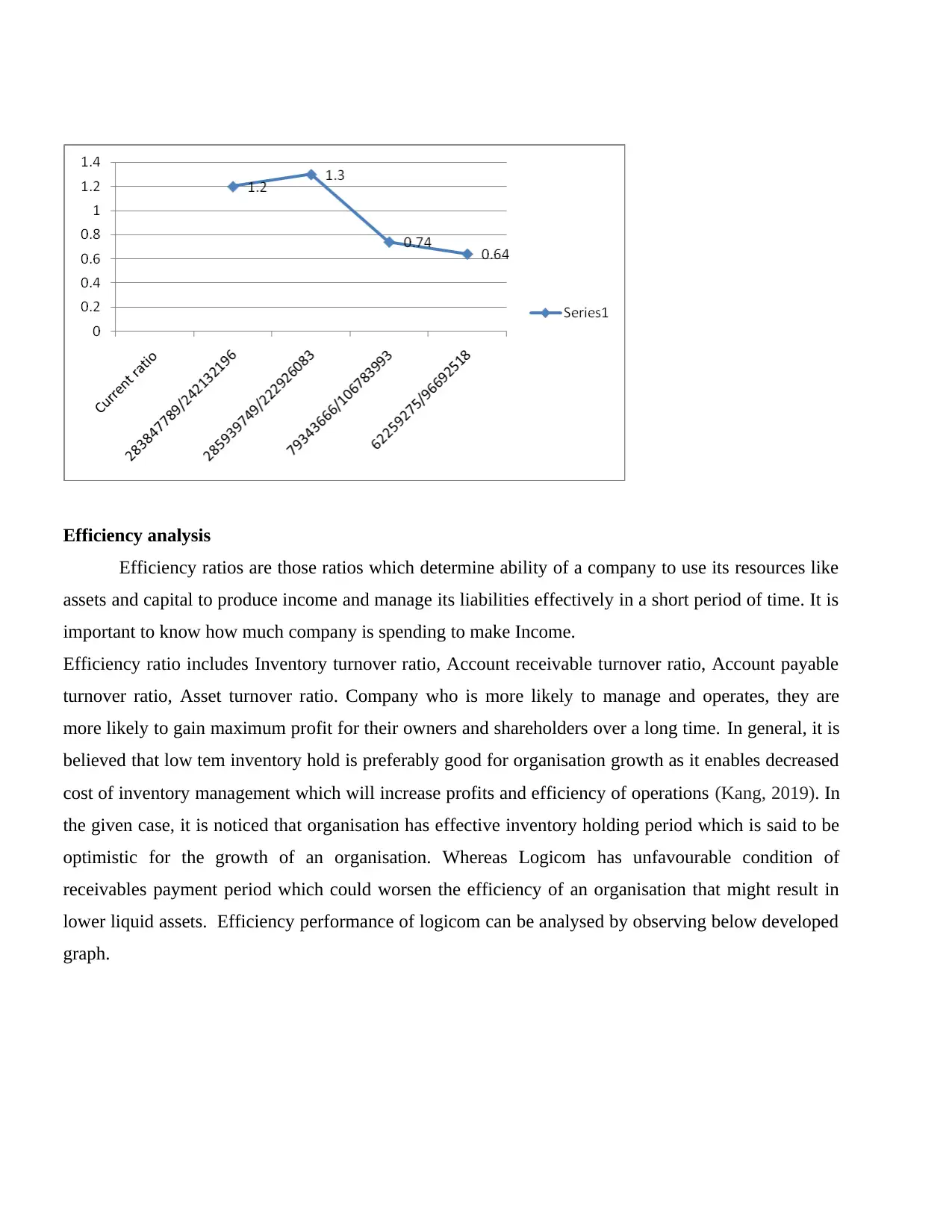

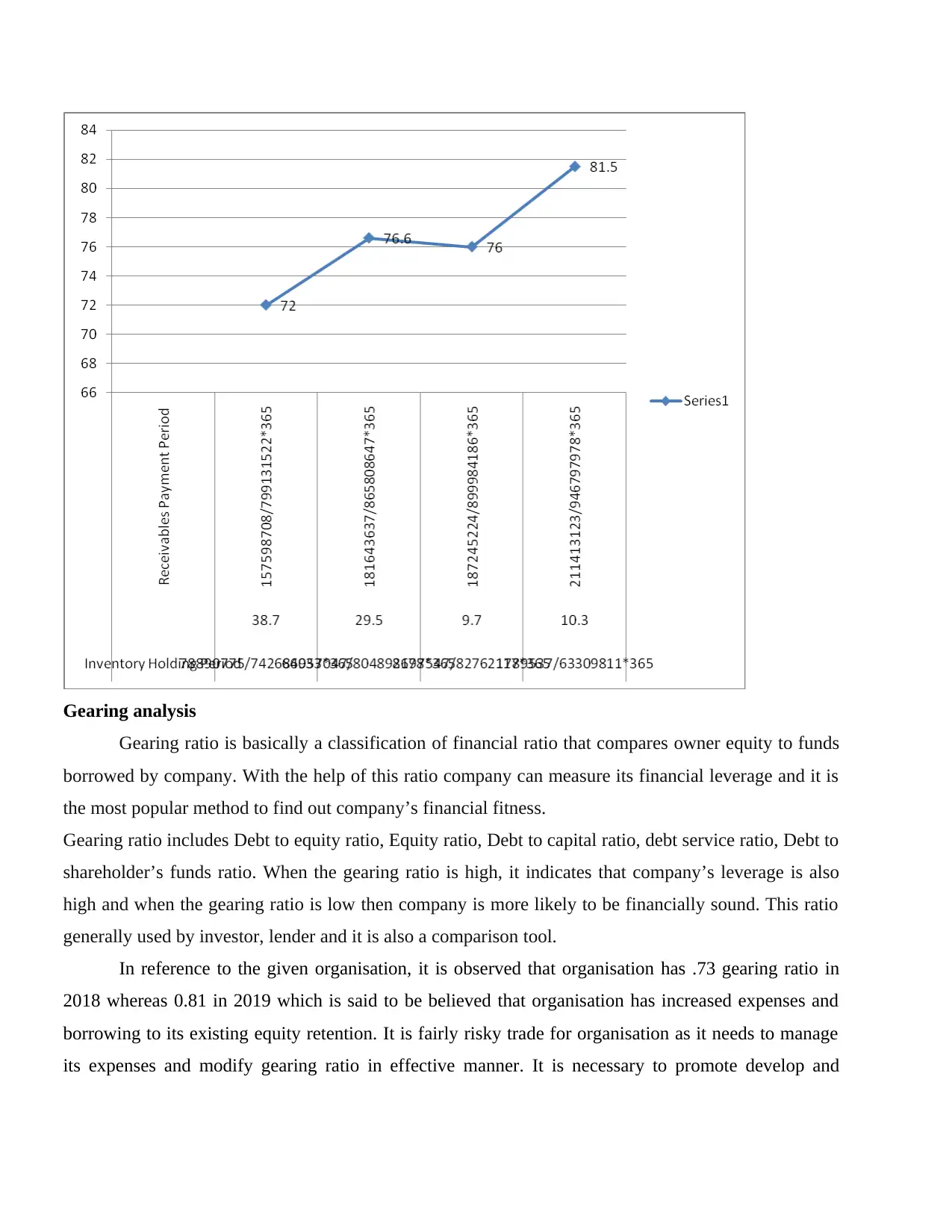

Efficiency analysis

Efficiency ratios are those ratios which determine ability of a company to use its resources like

assets and capital to produce income and manage its liabilities effectively in a short period of time. It is

important to know how much company is spending to make Income.

Efficiency ratio includes Inventory turnover ratio, Account receivable turnover ratio, Account payable

turnover ratio, Asset turnover ratio. Company who is more likely to manage and operates, they are

more likely to gain maximum profit for their owners and shareholders over a long time. In general, it is

believed that low tem inventory hold is preferably good for organisation growth as it enables decreased

cost of inventory management which will increase profits and efficiency of operations (Kang, 2019). In

the given case, it is noticed that organisation has effective inventory holding period which is said to be

optimistic for the growth of an organisation. Whereas Logicom has unfavourable condition of

receivables payment period which could worsen the efficiency of an organisation that might result in

lower liquid assets. Efficiency performance of logicom can be analysed by observing below developed

graph.

Efficiency ratios are those ratios which determine ability of a company to use its resources like

assets and capital to produce income and manage its liabilities effectively in a short period of time. It is

important to know how much company is spending to make Income.

Efficiency ratio includes Inventory turnover ratio, Account receivable turnover ratio, Account payable

turnover ratio, Asset turnover ratio. Company who is more likely to manage and operates, they are

more likely to gain maximum profit for their owners and shareholders over a long time. In general, it is

believed that low tem inventory hold is preferably good for organisation growth as it enables decreased

cost of inventory management which will increase profits and efficiency of operations (Kang, 2019). In

the given case, it is noticed that organisation has effective inventory holding period which is said to be

optimistic for the growth of an organisation. Whereas Logicom has unfavourable condition of

receivables payment period which could worsen the efficiency of an organisation that might result in

lower liquid assets. Efficiency performance of logicom can be analysed by observing below developed

graph.

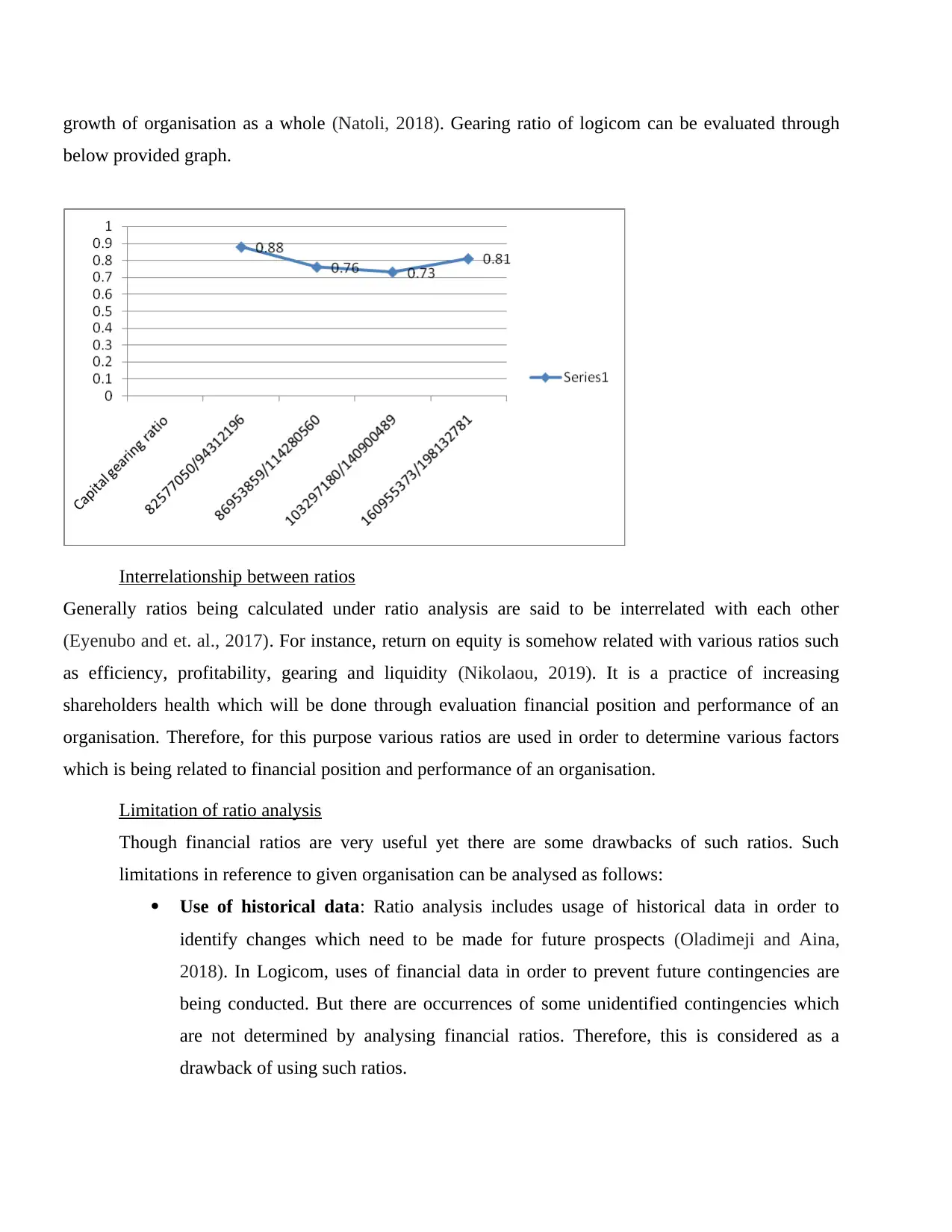

Gearing analysis

Gearing ratio is basically a classification of financial ratio that compares owner equity to funds

borrowed by company. With the help of this ratio company can measure its financial leverage and it is

the most popular method to find out company’s financial fitness.

Gearing ratio includes Debt to equity ratio, Equity ratio, Debt to capital ratio, debt service ratio, Debt to

shareholder’s funds ratio. When the gearing ratio is high, it indicates that company’s leverage is also

high and when the gearing ratio is low then company is more likely to be financially sound. This ratio

generally used by investor, lender and it is also a comparison tool.

In reference to the given organisation, it is observed that organisation has .73 gearing ratio in

2018 whereas 0.81 in 2019 which is said to be believed that organisation has increased expenses and

borrowing to its existing equity retention. It is fairly risky trade for organisation as it needs to manage

its expenses and modify gearing ratio in effective manner. It is necessary to promote develop and

Gearing ratio is basically a classification of financial ratio that compares owner equity to funds

borrowed by company. With the help of this ratio company can measure its financial leverage and it is

the most popular method to find out company’s financial fitness.

Gearing ratio includes Debt to equity ratio, Equity ratio, Debt to capital ratio, debt service ratio, Debt to

shareholder’s funds ratio. When the gearing ratio is high, it indicates that company’s leverage is also

high and when the gearing ratio is low then company is more likely to be financially sound. This ratio

generally used by investor, lender and it is also a comparison tool.

In reference to the given organisation, it is observed that organisation has .73 gearing ratio in

2018 whereas 0.81 in 2019 which is said to be believed that organisation has increased expenses and

borrowing to its existing equity retention. It is fairly risky trade for organisation as it needs to manage

its expenses and modify gearing ratio in effective manner. It is necessary to promote develop and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

growth of organisation as a whole (Natoli, 2018). Gearing ratio of logicom can be evaluated through

below provided graph.

Interrelationship between ratios

Generally ratios being calculated under ratio analysis are said to be interrelated with each other

(Eyenubo and et. al., 2017). For instance, return on equity is somehow related with various ratios such

as efficiency, profitability, gearing and liquidity (Nikolaou, 2019). It is a practice of increasing

shareholders health which will be done through evaluation financial position and performance of an

organisation. Therefore, for this purpose various ratios are used in order to determine various factors

which is being related to financial position and performance of an organisation.

Limitation of ratio analysis

Though financial ratios are very useful yet there are some drawbacks of such ratios. Such

limitations in reference to given organisation can be analysed as follows:

Use of historical data: Ratio analysis includes usage of historical data in order to

identify changes which need to be made for future prospects (Oladimeji and Aina,

2018). In Logicom, uses of financial data in order to prevent future contingencies are

being conducted. But there are occurrences of some unidentified contingencies which

are not determined by analysing financial ratios. Therefore, this is considered as a

drawback of using such ratios.

below provided graph.

Interrelationship between ratios

Generally ratios being calculated under ratio analysis are said to be interrelated with each other

(Eyenubo and et. al., 2017). For instance, return on equity is somehow related with various ratios such

as efficiency, profitability, gearing and liquidity (Nikolaou, 2019). It is a practice of increasing

shareholders health which will be done through evaluation financial position and performance of an

organisation. Therefore, for this purpose various ratios are used in order to determine various factors

which is being related to financial position and performance of an organisation.

Limitation of ratio analysis

Though financial ratios are very useful yet there are some drawbacks of such ratios. Such

limitations in reference to given organisation can be analysed as follows:

Use of historical data: Ratio analysis includes usage of historical data in order to

identify changes which need to be made for future prospects (Oladimeji and Aina,

2018). In Logicom, uses of financial data in order to prevent future contingencies are

being conducted. But there are occurrences of some unidentified contingencies which

are not determined by analysing financial ratios. Therefore, this is considered as a

drawback of using such ratios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Change in accounting policies: Such changes might affect the analysed information

and there may be difficulty in identification of actual changes which needs to be kept in

mind in respect of organisational growth and future prospects (Moon and Min, 2020.

Therefore such factors should be given preference while formulation of such ratios in

order to determine financial performance and position of organisation.

PART B

Areas to be investigated for further business growth and appraisal purposes

Credit risk: It is type risk which involves delayed recovery of receivables which could

cause huge difference in actual efficiency and forecasted efficiency. In order to

overcome this issue, Logicom needs to manage relevant receivables collection period so

that long term efficiency of an organisation can be promoted.

Interest rate risk: It is considered as fluctuations in relevant value of financial elements

because of up and down in market rate of interests (Kumari and Pattanayak, 2017). As

income and other operations are being dependent on market changes and other relevant

factors it is required to manage business operations in such a manner which will help

organisation in order to meet future fluctuations in such rates. As borrowings are

considered as variables rate which puts organisation at risk that might affect cash

inflows and outflows.

Liquidity risk: In order to eliminate this risk, organisation needs to focus over retention

of adequate amount of bank and cash balance so that business operations flow can be

maintained (Chowdhury and et. al., 2018).

PART C

Various articles analysing financial performance of Logicom

1. Quality & value will play key element for shares in Logicom Public

Company?

It is believed that generally high quality and cheap shares are tend to perform in an

effective manner as compared to low quality and high priced shares. Therefore, Logicom

has achieved growth of 1.98% in share performance which is considered as beneficial for

long term prospects. It contains two influential factors such as high quality and lower

and there may be difficulty in identification of actual changes which needs to be kept in

mind in respect of organisational growth and future prospects (Moon and Min, 2020.

Therefore such factors should be given preference while formulation of such ratios in

order to determine financial performance and position of organisation.

PART B

Areas to be investigated for further business growth and appraisal purposes

Credit risk: It is type risk which involves delayed recovery of receivables which could

cause huge difference in actual efficiency and forecasted efficiency. In order to

overcome this issue, Logicom needs to manage relevant receivables collection period so

that long term efficiency of an organisation can be promoted.

Interest rate risk: It is considered as fluctuations in relevant value of financial elements

because of up and down in market rate of interests (Kumari and Pattanayak, 2017). As

income and other operations are being dependent on market changes and other relevant

factors it is required to manage business operations in such a manner which will help

organisation in order to meet future fluctuations in such rates. As borrowings are

considered as variables rate which puts organisation at risk that might affect cash

inflows and outflows.

Liquidity risk: In order to eliminate this risk, organisation needs to focus over retention

of adequate amount of bank and cash balance so that business operations flow can be

maintained (Chowdhury and et. al., 2018).

PART C

Various articles analysing financial performance of Logicom

1. Quality & value will play key element for shares in Logicom Public

Company?

It is believed that generally high quality and cheap shares are tend to perform in an

effective manner as compared to low quality and high priced shares. Therefore, Logicom

has achieved growth of 1.98% in share performance which is considered as beneficial for

long term prospects. It contains two influential factors such as high quality and lower

valued shares which will be helpful in creation of optimum investment returns Could

(quality and value be the key for shares in Logicom Public?, 2020).

Source: Could quality and value be the key for shares in Logicom Public?

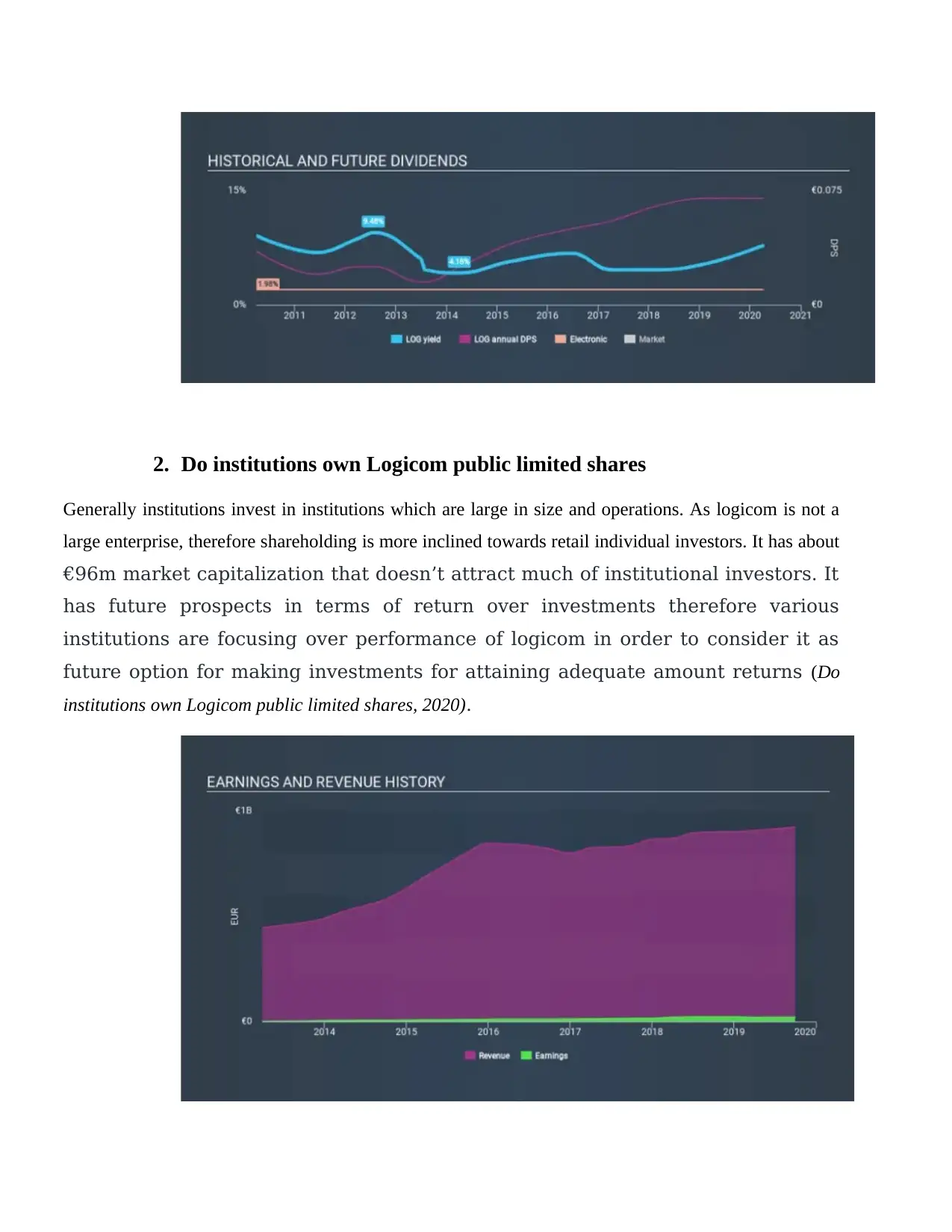

1. Why Dividend Hunters love Logicom Public Limited

It is observed that Logicom has been effective and efficient market leader who is dedicated towards

providing appropriate amount of dividends to its shareholders which has made it famous among

investors which will be helpful for its long term growth. It is identified that logicom has yielding

capacity of about 7.8% and has good image among investors. Various investments are being provided

by the company in order to attract maximum number of investors for attaining profitability and

productivity (Why Dividend Hunters love Logicom Public Limited, 2020) .

(quality and value be the key for shares in Logicom Public?, 2020).

Source: Could quality and value be the key for shares in Logicom Public?

1. Why Dividend Hunters love Logicom Public Limited

It is observed that Logicom has been effective and efficient market leader who is dedicated towards

providing appropriate amount of dividends to its shareholders which has made it famous among

investors which will be helpful for its long term growth. It is identified that logicom has yielding

capacity of about 7.8% and has good image among investors. Various investments are being provided

by the company in order to attract maximum number of investors for attaining profitability and

productivity (Why Dividend Hunters love Logicom Public Limited, 2020) .

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

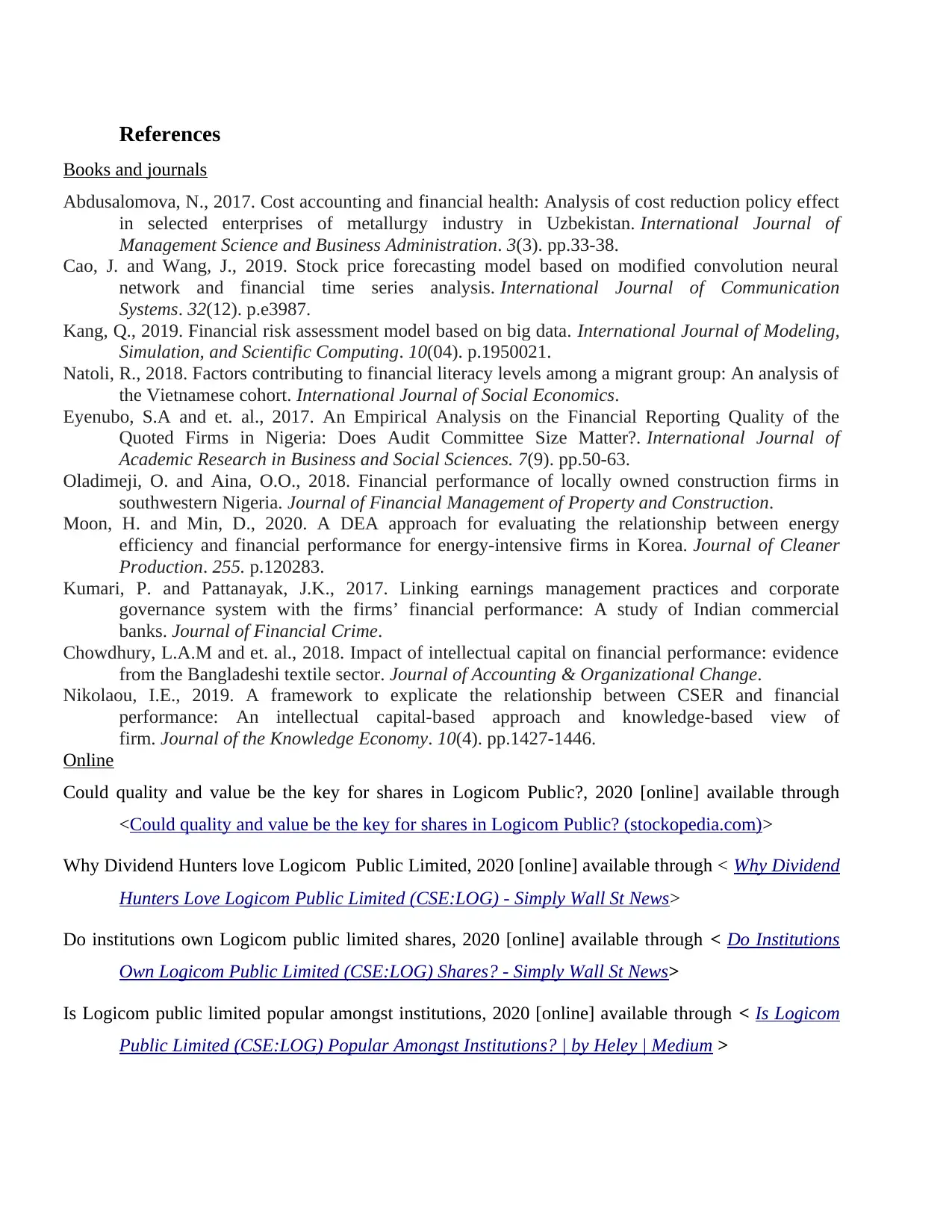

2. Do institutions own Logicom public limited shares

Generally institutions invest in institutions which are large in size and operations. As logicom is not a

large enterprise, therefore shareholding is more inclined towards retail individual investors. It has about

€96m market capitalization that doesn’t attract much of institutional investors. It

has future prospects in terms of return over investments therefore various

institutions are focusing over performance of logicom in order to consider it as

future option for making investments for attaining adequate amount returns (Do

institutions own Logicom public limited shares, 2020).

Generally institutions invest in institutions which are large in size and operations. As logicom is not a

large enterprise, therefore shareholding is more inclined towards retail individual investors. It has about

€96m market capitalization that doesn’t attract much of institutional investors. It

has future prospects in terms of return over investments therefore various

institutions are focusing over performance of logicom in order to consider it as

future option for making investments for attaining adequate amount returns (Do

institutions own Logicom public limited shares, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Is Logicom public limited popular amongst institutions?

It is fairly popular among institutions from point making investments. By analysing below graph it is

observed that the organisation has appropriate number of institutional investors as compared to

individuals. It is one of the most effective performing organisations which is operating over a large

platform. It has attracted interest of various institutions as logicom is considered as profit earning

organisation. Yet it needs to make modification in expense structure in order to continue earning profits

for long period (Is Logicom public limited popular amongst institutions, 2020).

CONCLUSION

Financial analysis is very important for an identification of financial growth of an organisation.

It is analysed from the above report that Logicom is one of good performing organisation in terms of

financial terms which is making it popular among investors in order to make adequate investments. By

analysing various financial ratios, it is suggested to investors that logicom is a profit making company

and adequate amount of investments can be made in the organisation through purchase of shares. Also

it is identified that existing shareholders needs to hold their shareholding in order to gain adequate

amount of returns from such organisation in long term. It is also at discretion of investors to whether

hold shares of the company or sale them as to gain profits from the markets. It is recommended that

investors needs to retain their shares in order to enjoy long term return over such shareholdings in the

respective organisation.

It is fairly popular among institutions from point making investments. By analysing below graph it is

observed that the organisation has appropriate number of institutional investors as compared to

individuals. It is one of the most effective performing organisations which is operating over a large

platform. It has attracted interest of various institutions as logicom is considered as profit earning

organisation. Yet it needs to make modification in expense structure in order to continue earning profits

for long period (Is Logicom public limited popular amongst institutions, 2020).

CONCLUSION

Financial analysis is very important for an identification of financial growth of an organisation.

It is analysed from the above report that Logicom is one of good performing organisation in terms of

financial terms which is making it popular among investors in order to make adequate investments. By

analysing various financial ratios, it is suggested to investors that logicom is a profit making company

and adequate amount of investments can be made in the organisation through purchase of shares. Also

it is identified that existing shareholders needs to hold their shareholding in order to gain adequate

amount of returns from such organisation in long term. It is also at discretion of investors to whether

hold shares of the company or sale them as to gain profits from the markets. It is recommended that

investors needs to retain their shares in order to enjoy long term return over such shareholdings in the

respective organisation.

References

Books and journals

Abdusalomova, N., 2017. Cost accounting and financial health: Analysis of cost reduction policy effect

in selected enterprises of metallurgy industry in Uzbekistan. International Journal of

Management Science and Business Administration. 3(3). pp.33-38.

Cao, J. and Wang, J., 2019. Stock price forecasting model based on modified convolution neural

network and financial time series analysis. International Journal of Communication

Systems. 32(12). p.e3987.

Kang, Q., 2019. Financial risk assessment model based on big data. International Journal of Modeling,

Simulation, and Scientific Computing. 10(04). p.1950021.

Natoli, R., 2018. Factors contributing to financial literacy levels among a migrant group: An analysis of

the Vietnamese cohort. International Journal of Social Economics.

Eyenubo, S.A and et. al., 2017. An Empirical Analysis on the Financial Reporting Quality of the

Quoted Firms in Nigeria: Does Audit Committee Size Matter?. International Journal of

Academic Research in Business and Social Sciences. 7(9). pp.50-63.

Oladimeji, O. and Aina, O.O., 2018. Financial performance of locally owned construction firms in

southwestern Nigeria. Journal of Financial Management of Property and Construction.

Moon, H. and Min, D., 2020. A DEA approach for evaluating the relationship between energy

efficiency and financial performance for energy-intensive firms in Korea. Journal of Cleaner

Production. 255. p.120283.

Kumari, P. and Pattanayak, J.K., 2017. Linking earnings management practices and corporate

governance system with the firms’ financial performance: A study of Indian commercial

banks. Journal of Financial Crime.

Chowdhury, L.A.M and et. al., 2018. Impact of intellectual capital on financial performance: evidence

from the Bangladeshi textile sector. Journal of Accounting & Organizational Change.

Nikolaou, I.E., 2019. A framework to explicate the relationship between CSER and financial

performance: An intellectual capital-based approach and knowledge-based view of

firm. Journal of the Knowledge Economy. 10(4). pp.1427-1446.

Online

Could quality and value be the key for shares in Logicom Public?, 2020 [online] available through

<Could quality and value be the key for shares in Logicom Public? (stockopedia.com)>

Why Dividend Hunters love Logicom Public Limited, 2020 [online] available through < Why Dividend

Hunters Love Logicom Public Limited (CSE:LOG) - Simply Wall St News>

Do institutions own Logicom public limited shares, 2020 [online] available through < Do Institutions

Own Logicom Public Limited (CSE:LOG) Shares? - Simply Wall St News>

Is Logicom public limited popular amongst institutions, 2020 [online] available through < Is Logicom

Public Limited (CSE:LOG) Popular Amongst Institutions? | by Heley | Medium >

Books and journals

Abdusalomova, N., 2017. Cost accounting and financial health: Analysis of cost reduction policy effect

in selected enterprises of metallurgy industry in Uzbekistan. International Journal of

Management Science and Business Administration. 3(3). pp.33-38.

Cao, J. and Wang, J., 2019. Stock price forecasting model based on modified convolution neural

network and financial time series analysis. International Journal of Communication

Systems. 32(12). p.e3987.

Kang, Q., 2019. Financial risk assessment model based on big data. International Journal of Modeling,

Simulation, and Scientific Computing. 10(04). p.1950021.

Natoli, R., 2018. Factors contributing to financial literacy levels among a migrant group: An analysis of

the Vietnamese cohort. International Journal of Social Economics.

Eyenubo, S.A and et. al., 2017. An Empirical Analysis on the Financial Reporting Quality of the

Quoted Firms in Nigeria: Does Audit Committee Size Matter?. International Journal of

Academic Research in Business and Social Sciences. 7(9). pp.50-63.

Oladimeji, O. and Aina, O.O., 2018. Financial performance of locally owned construction firms in

southwestern Nigeria. Journal of Financial Management of Property and Construction.

Moon, H. and Min, D., 2020. A DEA approach for evaluating the relationship between energy

efficiency and financial performance for energy-intensive firms in Korea. Journal of Cleaner

Production. 255. p.120283.

Kumari, P. and Pattanayak, J.K., 2017. Linking earnings management practices and corporate

governance system with the firms’ financial performance: A study of Indian commercial

banks. Journal of Financial Crime.

Chowdhury, L.A.M and et. al., 2018. Impact of intellectual capital on financial performance: evidence

from the Bangladeshi textile sector. Journal of Accounting & Organizational Change.

Nikolaou, I.E., 2019. A framework to explicate the relationship between CSER and financial

performance: An intellectual capital-based approach and knowledge-based view of

firm. Journal of the Knowledge Economy. 10(4). pp.1427-1446.

Online

Could quality and value be the key for shares in Logicom Public?, 2020 [online] available through

<Could quality and value be the key for shares in Logicom Public? (stockopedia.com)>

Why Dividend Hunters love Logicom Public Limited, 2020 [online] available through < Why Dividend

Hunters Love Logicom Public Limited (CSE:LOG) - Simply Wall St News>

Do institutions own Logicom public limited shares, 2020 [online] available through < Do Institutions

Own Logicom Public Limited (CSE:LOG) Shares? - Simply Wall St News>

Is Logicom public limited popular amongst institutions, 2020 [online] available through < Is Logicom

Public Limited (CSE:LOG) Popular Amongst Institutions? | by Heley | Medium >

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.