Long-Run Purchasing Power Parity Test Report Analysis 2017

VerifiedAdded on 2020/03/13

|34

|6385

|168

Report

AI Summary

This report investigates the long-run Purchasing Power Parity (PPP) theory, a fundamental concept in international economics, by examining data from the European region, United Kingdom, and the United States from 1988 to 2010. It explores the relationship between exchange rates and price levels, utilizing co-integration techniques and unit root tests, including Augmented Dickey-Fuller and Philips-Perron tests, to assess the stationarity of real exchange rates. The study aims to validate the PPP hypothesis, which suggests that exchange rates adjust to equalize the purchasing power of different currencies. The methodology involves regression analysis, unit root tests, and co-integration methods to determine if the real exchange rate remains constant over time. The findings are discussed in relation to previous research, including the work of Huan and Yang, and the implications for understanding the competitiveness of countries and their trading partners. The report concludes with a summary of the results, limitations, and suggestions for future research, contributing to the ongoing debate on the validity of PPP in the long run. This report also reviews literature to provide context for the analysis.

Test for Long-run Purchasing Power Parity (PPP)

Name

University

22nd August 2017

Name

University

22nd August 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Purchasing power parity (PPP) is a balance condition that is frequently accepted in both

hypothetical and useful monetary examination. Observational testing of PPP has not, however,

gave clear proof that legitimizes its expansive application - despite what might be expected,

various examinations have achieved negative conclusions with respect to its validity. This paper

endeavors to accommodate the wide utilization of purchasing power equality and the

experimental confirmation, by utilizing more proper techniques to test the speculation, inside a

multivariate and multi-nation setting for European region, United Kingdom, and the United

States in the period 1988-2010.

In its supreme rendition, the theory of purchasing power parity builds up that the value levels of

two nations ought to be equivalent when expressed in a similar currency. In this manner,

P=SP∗¿

Where S is the nominal exchange rate of the currency of country A expressed in terms of the

currency of country B, and P and P* the price levels of countries A and B, respectively. This

version of PPP implies, therefore, that the logarithm of the real exchange rate is constant and

equal to zero.

The theory of long-run purchasing power parity (PPP) states that monetary standards of various

nations have a similar buying power within the sight of universal arbitrage. Testing the

hypothesis for the long-run PPP gives a valuable understanding into whether the country's

competitiveness and its trading partners, based on the real exchange rate, fluctuates or remains

steady after some time. Previous studies heavily depended upon standard econometric techniques

when it came to testing the long-run PPP. The disappointment experienced from these

procedures especially to consider the economic time series non-stationary behavior brings about

what has turned out to be known as "spurious regressions."

Modeling techniques such as co-integration have been able to detect the presence of long-run

equilibrium associations that exist between non-stationary variables, with this, the long-run PPP

theory has therefore been getting restored consideration.

Notwithstanding whether the theory of long-run PPP remains constant or not, the examiner's

decision of the co-integration approach, regardless of whether it is the Granger and Engle two

stage strategy or the Juselius and Johansen multivariate procedure, ought not have any

noteworthy effect upon the result of the hypothesis test. Notwithstanding, in one of the recent

studies, Huan and Yang (1996) concluded that when the Granger and Engle technique rejects the

long-run PPP theory the Juseliusand Johansen technique has a tendency to acknowledge

it.Through Monte Carlo simulations utilizing data from France, Canada, Switzerland, Germany,

Purchasing power parity (PPP) is a balance condition that is frequently accepted in both

hypothetical and useful monetary examination. Observational testing of PPP has not, however,

gave clear proof that legitimizes its expansive application - despite what might be expected,

various examinations have achieved negative conclusions with respect to its validity. This paper

endeavors to accommodate the wide utilization of purchasing power equality and the

experimental confirmation, by utilizing more proper techniques to test the speculation, inside a

multivariate and multi-nation setting for European region, United Kingdom, and the United

States in the period 1988-2010.

In its supreme rendition, the theory of purchasing power parity builds up that the value levels of

two nations ought to be equivalent when expressed in a similar currency. In this manner,

P=SP∗¿

Where S is the nominal exchange rate of the currency of country A expressed in terms of the

currency of country B, and P and P* the price levels of countries A and B, respectively. This

version of PPP implies, therefore, that the logarithm of the real exchange rate is constant and

equal to zero.

The theory of long-run purchasing power parity (PPP) states that monetary standards of various

nations have a similar buying power within the sight of universal arbitrage. Testing the

hypothesis for the long-run PPP gives a valuable understanding into whether the country's

competitiveness and its trading partners, based on the real exchange rate, fluctuates or remains

steady after some time. Previous studies heavily depended upon standard econometric techniques

when it came to testing the long-run PPP. The disappointment experienced from these

procedures especially to consider the economic time series non-stationary behavior brings about

what has turned out to be known as "spurious regressions."

Modeling techniques such as co-integration have been able to detect the presence of long-run

equilibrium associations that exist between non-stationary variables, with this, the long-run PPP

theory has therefore been getting restored consideration.

Notwithstanding whether the theory of long-run PPP remains constant or not, the examiner's

decision of the co-integration approach, regardless of whether it is the Granger and Engle two

stage strategy or the Juselius and Johansen multivariate procedure, ought not have any

noteworthy effect upon the result of the hypothesis test. Notwithstanding, in one of the recent

studies, Huan and Yang (1996) concluded that when the Granger and Engle technique rejects the

long-run PPP theory the Juseliusand Johansen technique has a tendency to acknowledge

it.Through Monte Carlo simulations utilizing data from France, Canada, Switzerland, Germany,

the U.S.A., and the U.K., Huan and Yang found that the Juselius and Johansen co-integration

strategy is one-sided toward supporting the long-run PPP under conditions in which the

presumption of ordinarily as well as autonomously and indistinguishably appropriated

aggravation term is violated.

This paper applies the two co-integration strategies to consumer price index (CPI) and exchange

rate data from three developed regions to test for the long-run PPP speculation. In particular, it

tests whether Huan and Yang's claim, that the two co-integration systems yield contradicting

outcomes, remains constant with regards to developed regions. The two co-integration

approaches are applied to a time series data spanning from 1988 to 2010. The paper utilizes

effective exchange rate as the measure of exchange rate. Most countries have more than one

exchanging partner, the effective exchange rate is the suitable measure of exchange rate (Officer

(1980)).

The early experimental has grounded for a long time to look at the purchasing power parity

(PPP) exchange rates proved by statistical estimations and discovering versatility coefficients on

residential and foreign costs. Frankel (1978) conducted a study on relative and absolute PPP

convention amid the adaptable exchange rates. His outcome discovered causality relationship of

exchange rate on cost in the sense of granger. Most traditional econometric estimations such as

least square approach (GLS) in view of non-stationary time series results to spurious regression

and statistics may essentially show only correlated trends as opposed to a genuine relationship

(Granger and Newbold, 1974). Augmented Dickey-Fuller (1981) and Philips and Perron, (1988)

tests can help maintain a strategic distance from false outcomes through stationary tests of times

series.

Based on this, a number of observational studies present progression in the estimated equation of

PPP. Abuaf and Jorian (1990), conducted a unit-root test for non-stationary time series data.

Their results do not bolster PPP in long-run of the significant monetary forms. Taylor (1988)

utilized a co-integration of Johansen approach (1988) to conclude that there is a no connection

amongst costs and exchange rate. Patel (1990) utilized Engel-granger co-integration strategy to

affirm purchasing power parity prove. They pointed in their outcomes unfavorable proof to PPP

hypothesis amid the 1971-period assessed as ridiculing period after the Nixon (1993) inspected

long-run purchasing power parity utilizing a partial co-integration examination for the period

1914 - 1989. Their results upheld PPP as a long-run approach.

Johnson (1990) identified a solid and long-run U.S. - Canada data PPP idea. Philip (2001)

affirmed the confirmation of PPP in small-sample from yearly data spreading over 1973 through

1997 Nominal exchange rates for France, Canada, Japan, Italy, U.K and Switzerland are relative

to the U.S. dollar. Rogoff (1996)found out that PPP hypothesis did not hold amongst developing

and developed countries. Haug and Besher (2007) established a sort of mixed outcomes for non–

linear and linear co-integration in the PPP model utilizing monthly data from the post-Bretton

Woods period for G-10 nations. Ozdemir (2008), established bolster for PPP either over the long

strategy is one-sided toward supporting the long-run PPP under conditions in which the

presumption of ordinarily as well as autonomously and indistinguishably appropriated

aggravation term is violated.

This paper applies the two co-integration strategies to consumer price index (CPI) and exchange

rate data from three developed regions to test for the long-run PPP speculation. In particular, it

tests whether Huan and Yang's claim, that the two co-integration systems yield contradicting

outcomes, remains constant with regards to developed regions. The two co-integration

approaches are applied to a time series data spanning from 1988 to 2010. The paper utilizes

effective exchange rate as the measure of exchange rate. Most countries have more than one

exchanging partner, the effective exchange rate is the suitable measure of exchange rate (Officer

(1980)).

The early experimental has grounded for a long time to look at the purchasing power parity

(PPP) exchange rates proved by statistical estimations and discovering versatility coefficients on

residential and foreign costs. Frankel (1978) conducted a study on relative and absolute PPP

convention amid the adaptable exchange rates. His outcome discovered causality relationship of

exchange rate on cost in the sense of granger. Most traditional econometric estimations such as

least square approach (GLS) in view of non-stationary time series results to spurious regression

and statistics may essentially show only correlated trends as opposed to a genuine relationship

(Granger and Newbold, 1974). Augmented Dickey-Fuller (1981) and Philips and Perron, (1988)

tests can help maintain a strategic distance from false outcomes through stationary tests of times

series.

Based on this, a number of observational studies present progression in the estimated equation of

PPP. Abuaf and Jorian (1990), conducted a unit-root test for non-stationary time series data.

Their results do not bolster PPP in long-run of the significant monetary forms. Taylor (1988)

utilized a co-integration of Johansen approach (1988) to conclude that there is a no connection

amongst costs and exchange rate. Patel (1990) utilized Engel-granger co-integration strategy to

affirm purchasing power parity prove. They pointed in their outcomes unfavorable proof to PPP

hypothesis amid the 1971-period assessed as ridiculing period after the Nixon (1993) inspected

long-run purchasing power parity utilizing a partial co-integration examination for the period

1914 - 1989. Their results upheld PPP as a long-run approach.

Johnson (1990) identified a solid and long-run U.S. - Canada data PPP idea. Philip (2001)

affirmed the confirmation of PPP in small-sample from yearly data spreading over 1973 through

1997 Nominal exchange rates for France, Canada, Japan, Italy, U.K and Switzerland are relative

to the U.S. dollar. Rogoff (1996)found out that PPP hypothesis did not hold amongst developing

and developed countries. Haug and Besher (2007) established a sort of mixed outcomes for non–

linear and linear co-integration in the PPP model utilizing monthly data from the post-Bretton

Woods period for G-10 nations. Ozdemir (2008), established bolster for PPP either over the long

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

run. Hyrina and Serletis (2010) looked at various econometric strategies utilized in earlier and

later studies to verify PPP idea, where early experimental techniques failed to recognize PPP

presence contrasted with current investigations.

Hussein (2015) analyzed the long run development between US dollar and Canadian dollar

exchange rates upon month to month data for the period 1995 to 2008 utilizing the Engle-

Granger co-integration test. In his paper, he doesn't give the validity of PPP between US dollar

and Canadian dollar trade rates. Pedroni (2001) showed blended proof of PPP in view of panel

unit root tests. He showed the presence of weak PPP and rejected solid PPP idea. Robertson et al

(2014) utilized panel co-integration approach of month to month data from 1982 through to 2010

to explore the Purchasing Power Parity (PPP) between the Mexico and US.

The rest of the paper is organized in the following way. The literature review on the theory of

long-run PPP is presented in section II. Section III introduces the methodology used which

includes the approaches, philosophies, strategies and justification of the approaches used. Section

IV presents the empirical findings based on the analysis of data. Section V provides discussion of

the findings and interpretation of the results. Lastly, section VI provides the conclusions,

limitations of the study and a brief summary of the entire paper.

METHODOLOGY

This chapter presents the methodologies as well as testable hypothesis regarding the purchasing

power parity (PPP). Three stages as outlined by Froot and Rogoff (1995) have been employed.

The first step involves regression testing using the following equation model;

st =α +β ( pt + pt

¿

) +εt

Where st represents the logarithm of the nominal exchange rate, α represents the constant, pt and

pt

¿ represents the logarithms of domestic and foreign price levels and ε t is the error term. The

first step will mainly test whether β is close to one.

The next step would involve putting more emphasis on the properties of the logarithm of the real

exchange rate rx:

rx=st− ( pt− pt

¿

)

Here an assumption is made that PPP holds so long as the logarithm of the real exchange rate rx

is stationary.

In the third step, the focus is on both multivariate and univariate co-integration tests of PPP. The

model applied checks for stationarity in any of the constants μ¿ and μ

st − ( μ pt + μ¿ pt

¿

)

later studies to verify PPP idea, where early experimental techniques failed to recognize PPP

presence contrasted with current investigations.

Hussein (2015) analyzed the long run development between US dollar and Canadian dollar

exchange rates upon month to month data for the period 1995 to 2008 utilizing the Engle-

Granger co-integration test. In his paper, he doesn't give the validity of PPP between US dollar

and Canadian dollar trade rates. Pedroni (2001) showed blended proof of PPP in view of panel

unit root tests. He showed the presence of weak PPP and rejected solid PPP idea. Robertson et al

(2014) utilized panel co-integration approach of month to month data from 1982 through to 2010

to explore the Purchasing Power Parity (PPP) between the Mexico and US.

The rest of the paper is organized in the following way. The literature review on the theory of

long-run PPP is presented in section II. Section III introduces the methodology used which

includes the approaches, philosophies, strategies and justification of the approaches used. Section

IV presents the empirical findings based on the analysis of data. Section V provides discussion of

the findings and interpretation of the results. Lastly, section VI provides the conclusions,

limitations of the study and a brief summary of the entire paper.

METHODOLOGY

This chapter presents the methodologies as well as testable hypothesis regarding the purchasing

power parity (PPP). Three stages as outlined by Froot and Rogoff (1995) have been employed.

The first step involves regression testing using the following equation model;

st =α +β ( pt + pt

¿

) +εt

Where st represents the logarithm of the nominal exchange rate, α represents the constant, pt and

pt

¿ represents the logarithms of domestic and foreign price levels and ε t is the error term. The

first step will mainly test whether β is close to one.

The next step would involve putting more emphasis on the properties of the logarithm of the real

exchange rate rx:

rx=st− ( pt− pt

¿

)

Here an assumption is made that PPP holds so long as the logarithm of the real exchange rate rx

is stationary.

In the third step, the focus is on both multivariate and univariate co-integration tests of PPP. The

model applied checks for stationarity in any of the constants μ¿ and μ

st − ( μ pt + μ¿ pt

¿

)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This study will focus more on properties of the real exchange rates (using multivariate and

univariate approaches) as well as co-integration methods given that the series of the logarithms

of nominal exchange rates and consumer price index are normally non-stationary.

In testing for the unit root especially for the real exchange rates and consumer price index (CPI),

Augmented Dickey Fuller (ADF) tests is applied. The following equation models are used;

∆ yt =β yt−1 +∑ αi ∆ yt−i+1 + εt

∆ yt =c0 + β yt−1 +∑ α i ∆ yt−i+1 + εt

∆ yt =c0 + β yt−1 +c1 t +∑ α i ∆ yt−i+1 + εt

The final equation model is;

∆ yt =δ yt−1 +∑

i=1

k

δi ∆ yt−i +εt

Where yt is basically regressed on the lagged independent variable yt −1 and on yt −iso that it

could account for any possible autocorrelation of say order k that may occur in the error term ε t.

Rejecting the null hypothesis H0: δ=0 in favor of the alternative hypothesis HA: δ <0 would

imply that the given series is stationary.

For the case of Dickey-Fuller (1979), he suggested three different regression equations models to

be used in testing the presence or the absence of a unit root;

∆ yt =β yt−1 +εt

∆ yt =c0 + β yt−1 +εt

∆ yt =c0 + β yt−1 +c1 t +εt

The difference in the three regressions is based on the presence of the two deterministic elements

c0, c1 t. The first deterministic element (c0) presents a pure random walk model, while the second

one simply adds an intercept, and the last deterministic element includes both intercept and linear

time trend. The main concept behindDickey –Fuller test is the fact that the t-test normally

becomes inappropriate so long as the process is non-stationary, thus starting from yt =k yt −1 +εt

and if we subtract yt −1from both the RHS and the LHS we obtain;

∆ yt =β yt−1 +εt

In this case, testing whether β equals to 0 is similar to testing whether k equals to 1. This implies

that the parameter of interest in all the three regression equations is β, as such if β=0 then the

series ythas a unit root. OLS is used to estimate the above equations so as the value of β can be

univariate approaches) as well as co-integration methods given that the series of the logarithms

of nominal exchange rates and consumer price index are normally non-stationary.

In testing for the unit root especially for the real exchange rates and consumer price index (CPI),

Augmented Dickey Fuller (ADF) tests is applied. The following equation models are used;

∆ yt =β yt−1 +∑ αi ∆ yt−i+1 + εt

∆ yt =c0 + β yt−1 +∑ α i ∆ yt−i+1 + εt

∆ yt =c0 + β yt−1 +c1 t +∑ α i ∆ yt−i+1 + εt

The final equation model is;

∆ yt =δ yt−1 +∑

i=1

k

δi ∆ yt−i +εt

Where yt is basically regressed on the lagged independent variable yt −1 and on yt −iso that it

could account for any possible autocorrelation of say order k that may occur in the error term ε t.

Rejecting the null hypothesis H0: δ=0 in favor of the alternative hypothesis HA: δ <0 would

imply that the given series is stationary.

For the case of Dickey-Fuller (1979), he suggested three different regression equations models to

be used in testing the presence or the absence of a unit root;

∆ yt =β yt−1 +εt

∆ yt =c0 + β yt−1 +εt

∆ yt =c0 + β yt−1 +c1 t +εt

The difference in the three regressions is based on the presence of the two deterministic elements

c0, c1 t. The first deterministic element (c0) presents a pure random walk model, while the second

one simply adds an intercept, and the last deterministic element includes both intercept and linear

time trend. The main concept behindDickey –Fuller test is the fact that the t-test normally

becomes inappropriate so long as the process is non-stationary, thus starting from yt =k yt −1 +εt

and if we subtract yt −1from both the RHS and the LHS we obtain;

∆ yt =β yt−1 +εt

In this case, testing whether β equals to 0 is similar to testing whether k equals to 1. This implies

that the parameter of interest in all the three regression equations is β, as such if β=0 then the

series ythas a unit root. OLS is used to estimate the above equations so as the value of β can be

obtained as well as associated standard error. The t-statistic associated with testing for the null

hypothesis β=0 is gotten by dividing the estimated β value by its corresponding standard error (

β / Standard Error). A smaller critical value compared to the absolute t-statistic value implies that

test is significant hence the null hypothesis is rejected.

The Philips-Perron test supports the Dickey-Fuller test where it assumes that the errors are

significantly independent and that they follow homogeneity. The test is a generalization of the

Dickey-Fuller approach which permits for lighter assumptions regarding the error distributions.

The following regression equations are related to the Philips-Perron test;

yt =γ 0 +γ 1 yt −1+ μt

yt =λ0 + λ1 yt −1+ λ2 (t− T

2 )+μt

In the above equations, T denotes the number of observations while μt is the disturbance term

such that E ( μt )=0. The disturbance term need not to be homogeneous or serially uncorrelated.

Unlike the Dickey-Fuller test where the homogeneity and independence assumptions take a

center-stage, the Philips-Perron test gives room for disturbance term to be non-homogenously

distributed and weakly dependent.

hypothesis β=0 is gotten by dividing the estimated β value by its corresponding standard error (

β / Standard Error). A smaller critical value compared to the absolute t-statistic value implies that

test is significant hence the null hypothesis is rejected.

The Philips-Perron test supports the Dickey-Fuller test where it assumes that the errors are

significantly independent and that they follow homogeneity. The test is a generalization of the

Dickey-Fuller approach which permits for lighter assumptions regarding the error distributions.

The following regression equations are related to the Philips-Perron test;

yt =γ 0 +γ 1 yt −1+ μt

yt =λ0 + λ1 yt −1+ λ2 (t− T

2 )+μt

In the above equations, T denotes the number of observations while μt is the disturbance term

such that E ( μt )=0. The disturbance term need not to be homogeneous or serially uncorrelated.

Unlike the Dickey-Fuller test where the homogeneity and independence assumptions take a

center-stage, the Philips-Perron test gives room for disturbance term to be non-homogenously

distributed and weakly dependent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Results and Discussion

In this section, the test results for the PPP hypothesis are presented. The absolute version of PPP,

highlights that the nominal exchange rate computed between two currencies is the same as the

ratio of the general price levels that exists between two countries and this is formulated as

follows;

et =pt – pt

¿

Where pt, pt

¿ is the logarithm forms of the price levels for the three countries (United states,

United Kingdom and European Union) at time t respectively, and etis the logarithm of the

currency price for a unit of foreign currency observed at time t. The real exchange rate denotes a

price adjusted nominal exchange rate which is given as:

rt=et −( pt – pt

¿)

Therefore, in this paper, PPP hypothesis is being tested by evaluating the time series properties

of {rt} series. With this in mind, if { rt} series is stationary, then it can be said that would expect

the PPP to also hold; however, if {rt} series is non-stationary, for instance, if the series has unit

root then PPP does not hold.

Descriptive statistics

For the analysis purpose the time series data for inflation and the exchange rate was collected for

the three different region namely United States, United Kingdom and the European Union.

Descriptive results for the selected variable have been discussed below:

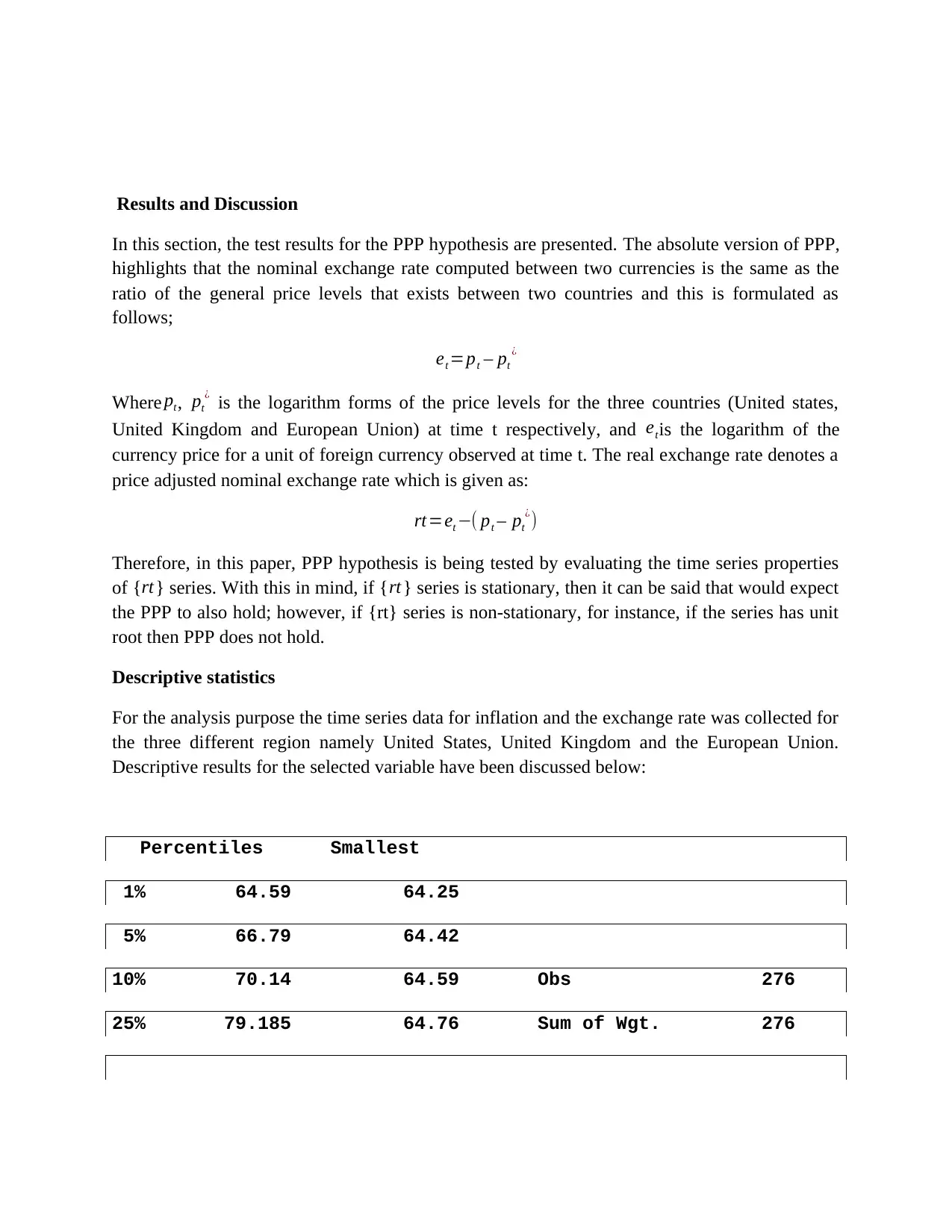

Percentiles Smallest

1% 64.59 64.25

5% 66.79 64.42

10% 70.14 64.59 Obs 276

25% 79.185 64.76 Sum of Wgt. 276

In this section, the test results for the PPP hypothesis are presented. The absolute version of PPP,

highlights that the nominal exchange rate computed between two currencies is the same as the

ratio of the general price levels that exists between two countries and this is formulated as

follows;

et =pt – pt

¿

Where pt, pt

¿ is the logarithm forms of the price levels for the three countries (United states,

United Kingdom and European Union) at time t respectively, and etis the logarithm of the

currency price for a unit of foreign currency observed at time t. The real exchange rate denotes a

price adjusted nominal exchange rate which is given as:

rt=et −( pt – pt

¿)

Therefore, in this paper, PPP hypothesis is being tested by evaluating the time series properties

of {rt} series. With this in mind, if { rt} series is stationary, then it can be said that would expect

the PPP to also hold; however, if {rt} series is non-stationary, for instance, if the series has unit

root then PPP does not hold.

Descriptive statistics

For the analysis purpose the time series data for inflation and the exchange rate was collected for

the three different region namely United States, United Kingdom and the European Union.

Descriptive results for the selected variable have been discussed below:

Percentiles Smallest

1% 64.59 64.25

5% 66.79 64.42

10% 70.14 64.59 Obs 276

25% 79.185 64.76 Sum of Wgt. 276

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

50% 87.905 Mean 88.79076

Largest Std. Dev. 12.96434

75% 99.535 110.19

90% 107.88 110.52 Variance 168.0741

95% 108.54 110.62 Skewness -.0715355

99% 110.52 111.29 Kurtosis 2.022907

Table 1 Descriptive statistics for inflation in United States

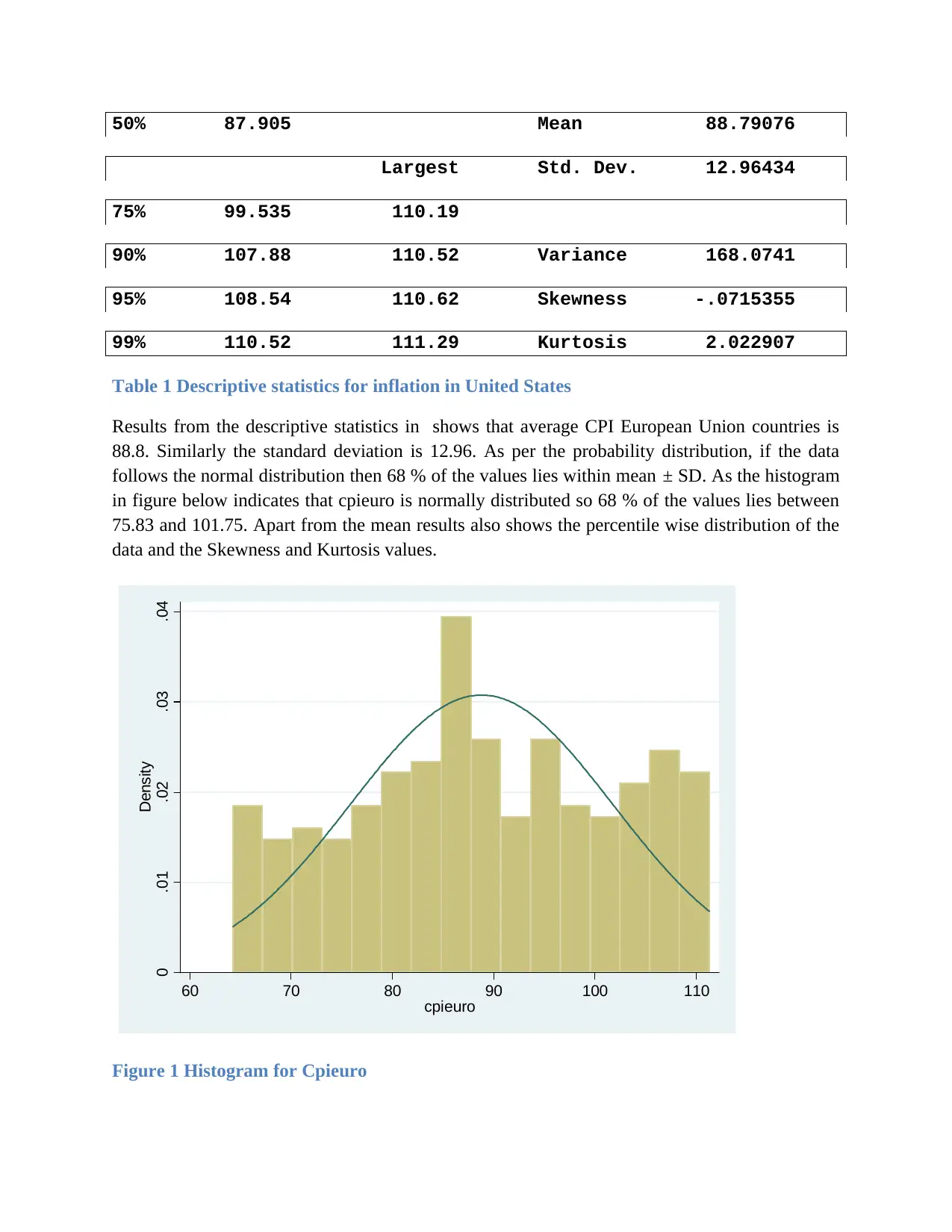

Results from the descriptive statistics in shows that average CPI European Union countries is

88.8. Similarly the standard deviation is 12.96. As per the probability distribution, if the data

follows the normal distribution then 68 % of the values lies within mean ± SD. As the histogram

in figure below indicates that cpieuro is normally distributed so 68 % of the values lies between

75.83 and 101.75. Apart from the mean results also shows the percentile wise distribution of the

data and the Skewness and Kurtosis values.

0 .01 .02 .03 .04

Density

60 70 80 90 100 110

cpieuro

Figure 1 Histogram for Cpieuro

Largest Std. Dev. 12.96434

75% 99.535 110.19

90% 107.88 110.52 Variance 168.0741

95% 108.54 110.62 Skewness -.0715355

99% 110.52 111.29 Kurtosis 2.022907

Table 1 Descriptive statistics for inflation in United States

Results from the descriptive statistics in shows that average CPI European Union countries is

88.8. Similarly the standard deviation is 12.96. As per the probability distribution, if the data

follows the normal distribution then 68 % of the values lies within mean ± SD. As the histogram

in figure below indicates that cpieuro is normally distributed so 68 % of the values lies between

75.83 and 101.75. Apart from the mean results also shows the percentile wise distribution of the

data and the Skewness and Kurtosis values.

0 .01 .02 .03 .04

Density

60 70 80 90 100 110

cpieuro

Figure 1 Histogram for Cpieuro

Similarly the descriptive statistics for remaining 5 variables has also been shown the following

table. Histogram for other variable is shown in the appendix.

Percentiles Smallest

1% 62.3 61.9

5% 65.2 62.1

10% 70.6 62.3 Obs 276

25% 82.55 63.1 Sum of Wgt. 276

50% 92.35 Mean 90.86739

Largest Std. Dev. 13.19832

75% 99.5 114.9

90% 109.5 115.2 Variance 174.1957

95% 112 115.6 Skewness -.2829012

99% 115.2 116.8 Kurtosis 2.546003

Table 2 Descriptive results for cpiuk

Results show that average cpi in United Kingdom is 90.86 which is higher than the average cpi

in European region. Similarly the standard deviation in this case is 13.19. In terms of range the

highest cpi is116.8 whereas the lowest is 61.9. The mean value is often being criticized as the

mean value is affected by the extreme values and some scholars preferred median over mean as a

measure of central tendency.

-------------------------------------------------------------

Percentiles Smallest

1% 116.5 115.7

5% 121.6 116

10% 128.9 116.5 Obs 276

table. Histogram for other variable is shown in the appendix.

Percentiles Smallest

1% 62.3 61.9

5% 65.2 62.1

10% 70.6 62.3 Obs 276

25% 82.55 63.1 Sum of Wgt. 276

50% 92.35 Mean 90.86739

Largest Std. Dev. 13.19832

75% 99.5 114.9

90% 109.5 115.2 Variance 174.1957

95% 112 115.6 Skewness -.2829012

99% 115.2 116.8 Kurtosis 2.546003

Table 2 Descriptive results for cpiuk

Results show that average cpi in United Kingdom is 90.86 which is higher than the average cpi

in European region. Similarly the standard deviation in this case is 13.19. In terms of range the

highest cpi is116.8 whereas the lowest is 61.9. The mean value is often being criticized as the

mean value is affected by the extreme values and some scholars preferred median over mean as a

measure of central tendency.

-------------------------------------------------------------

Percentiles Smallest

1% 116.5 115.7

5% 121.6 116

10% 128.9 116.5 Obs 276

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

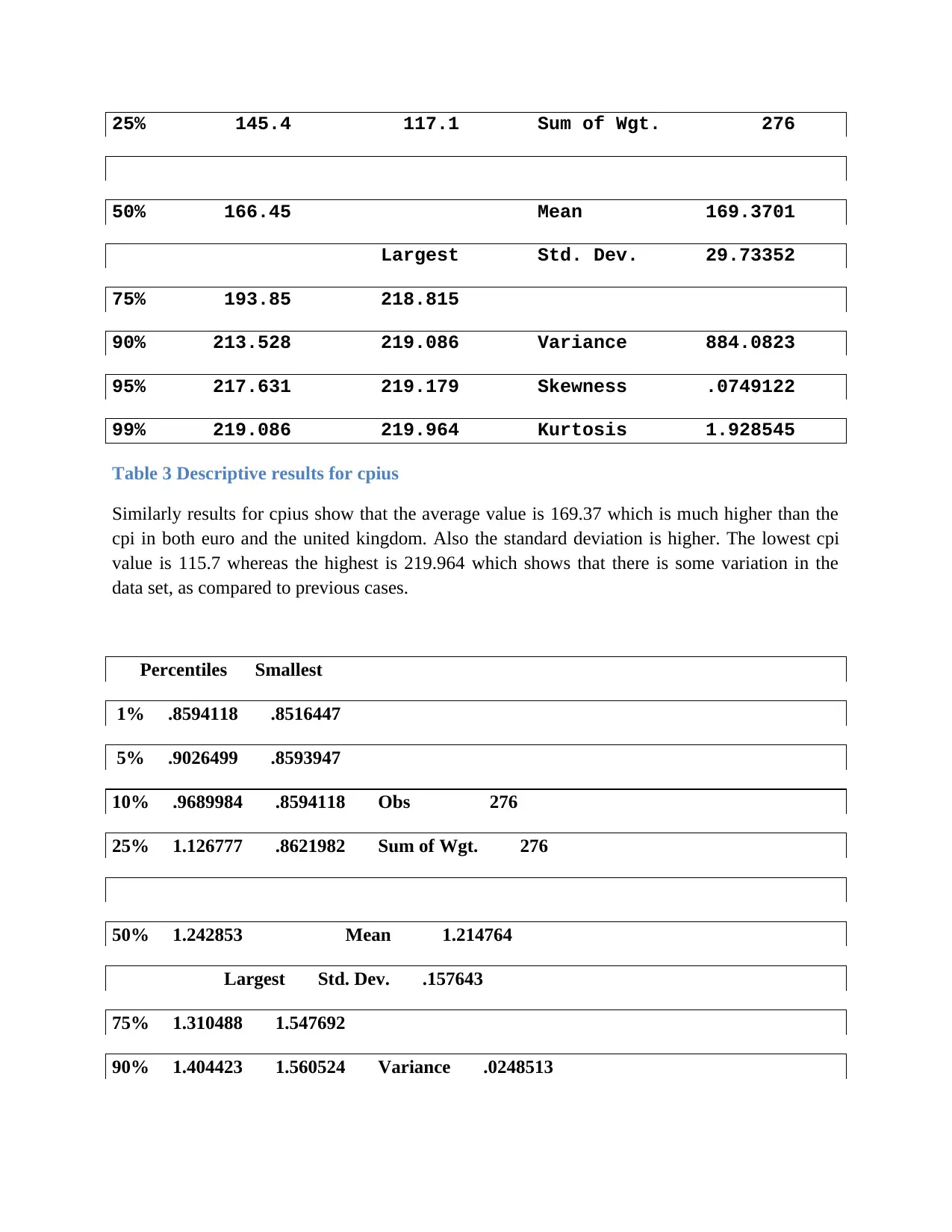

25% 145.4 117.1 Sum of Wgt. 276

50% 166.45 Mean 169.3701

Largest Std. Dev. 29.73352

75% 193.85 218.815

90% 213.528 219.086 Variance 884.0823

95% 217.631 219.179 Skewness .0749122

99% 219.086 219.964 Kurtosis 1.928545

Table 3 Descriptive results for cpius

Similarly results for cpius show that the average value is 169.37 which is much higher than the

cpi in both euro and the united kingdom. Also the standard deviation is higher. The lowest cpi

value is 115.7 whereas the highest is 219.964 which shows that there is some variation in the

data set, as compared to previous cases.

Percentiles Smallest

1% .8594118 .8516447

5% .9026499 .8593947

10% .9689984 .8594118 Obs 276

25% 1.126777 .8621982 Sum of Wgt. 276

50% 1.242853 Mean 1.214764

Largest Std. Dev. .157643

75% 1.310488 1.547692

90% 1.404423 1.560524 Variance .0248513

50% 166.45 Mean 169.3701

Largest Std. Dev. 29.73352

75% 193.85 218.815

90% 213.528 219.086 Variance 884.0823

95% 217.631 219.179 Skewness .0749122

99% 219.086 219.964 Kurtosis 1.928545

Table 3 Descriptive results for cpius

Similarly results for cpius show that the average value is 169.37 which is much higher than the

cpi in both euro and the united kingdom. Also the standard deviation is higher. The lowest cpi

value is 115.7 whereas the highest is 219.964 which shows that there is some variation in the

data set, as compared to previous cases.

Percentiles Smallest

1% .8594118 .8516447

5% .9026499 .8593947

10% .9689984 .8594118 Obs 276

25% 1.126777 .8621982 Sum of Wgt. 276

50% 1.242853 Mean 1.214764

Largest Std. Dev. .157643

75% 1.310488 1.547692

90% 1.404423 1.560524 Variance .0248513

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

95% 1.461457 1.580327 Skewness -.3843775

99% 1.560524 1.597132 Kurtosis 2.853423

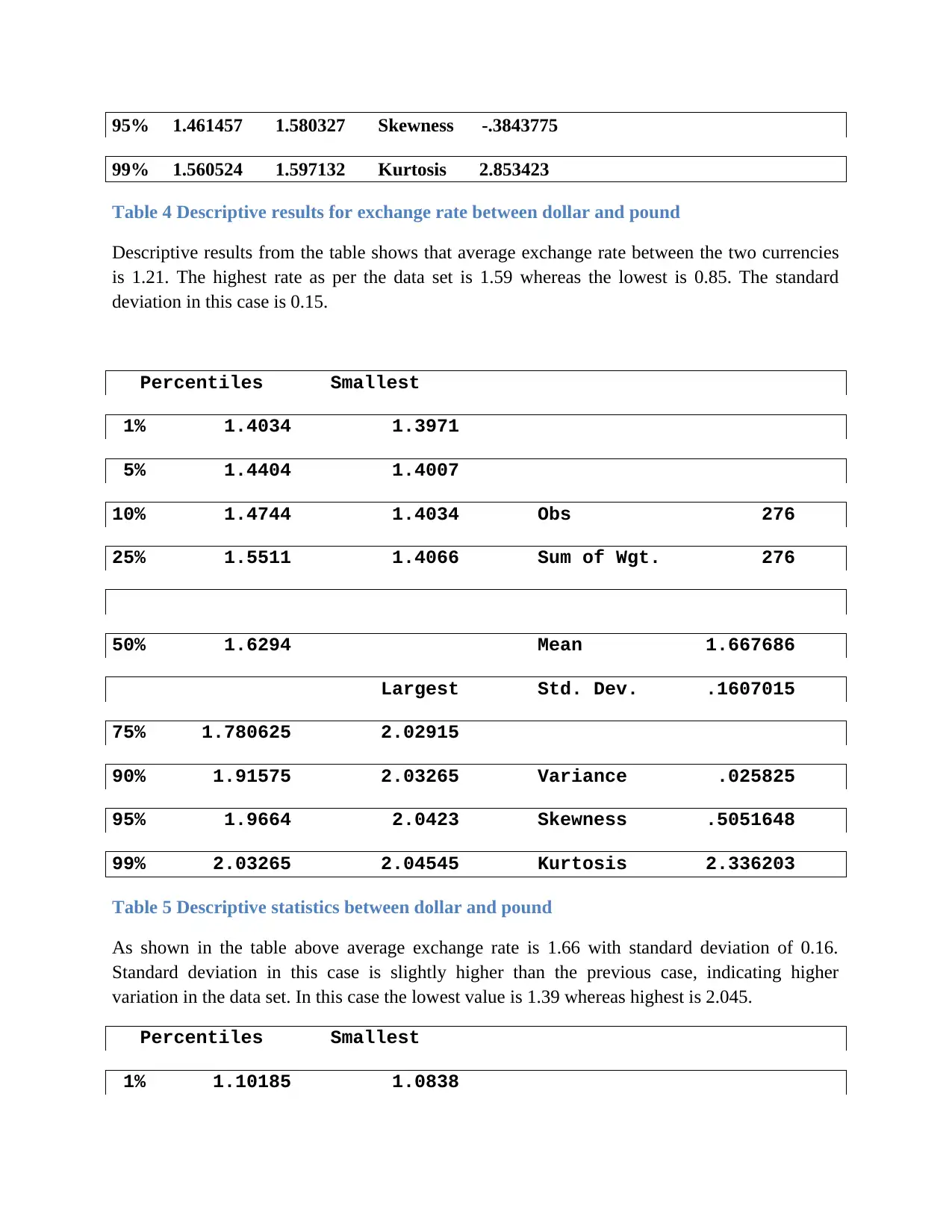

Table 4 Descriptive results for exchange rate between dollar and pound

Descriptive results from the table shows that average exchange rate between the two currencies

is 1.21. The highest rate as per the data set is 1.59 whereas the lowest is 0.85. The standard

deviation in this case is 0.15.

Percentiles Smallest

1% 1.4034 1.3971

5% 1.4404 1.4007

10% 1.4744 1.4034 Obs 276

25% 1.5511 1.4066 Sum of Wgt. 276

50% 1.6294 Mean 1.667686

Largest Std. Dev. .1607015

75% 1.780625 2.02915

90% 1.91575 2.03265 Variance .025825

95% 1.9664 2.0423 Skewness .5051648

99% 2.03265 2.04545 Kurtosis 2.336203

Table 5 Descriptive statistics between dollar and pound

As shown in the table above average exchange rate is 1.66 with standard deviation of 0.16.

Standard deviation in this case is slightly higher than the previous case, indicating higher

variation in the data set. In this case the lowest value is 1.39 whereas highest is 2.045.

Percentiles Smallest

1% 1.10185 1.0838

99% 1.560524 1.597132 Kurtosis 2.853423

Table 4 Descriptive results for exchange rate between dollar and pound

Descriptive results from the table shows that average exchange rate between the two currencies

is 1.21. The highest rate as per the data set is 1.59 whereas the lowest is 0.85. The standard

deviation in this case is 0.15.

Percentiles Smallest

1% 1.4034 1.3971

5% 1.4404 1.4007

10% 1.4744 1.4034 Obs 276

25% 1.5511 1.4066 Sum of Wgt. 276

50% 1.6294 Mean 1.667686

Largest Std. Dev. .1607015

75% 1.780625 2.02915

90% 1.91575 2.03265 Variance .025825

95% 1.9664 2.0423 Skewness .5051648

99% 2.03265 2.04545 Kurtosis 2.336203

Table 5 Descriptive statistics between dollar and pound

As shown in the table above average exchange rate is 1.66 with standard deviation of 0.16.

Standard deviation in this case is slightly higher than the previous case, indicating higher

variation in the data set. In this case the lowest value is 1.39 whereas highest is 2.045.

Percentiles Smallest

1% 1.10185 1.0838

5% 1.1428 1.08875

10% 1.18136 1.10185 Obs 276

25% 1.263585 1.11495 Sum of Wgt. 276

50% 1.417225 Mean 1.386635

Largest Std. Dev. .1458609

75% 1.48465 1.6529

90% 1.5929 1.6602 Variance .0212754

95% 1.6225 1.6621 Skewness -.114234

99% 1.6602 1.7 Kurtosis 2.095064

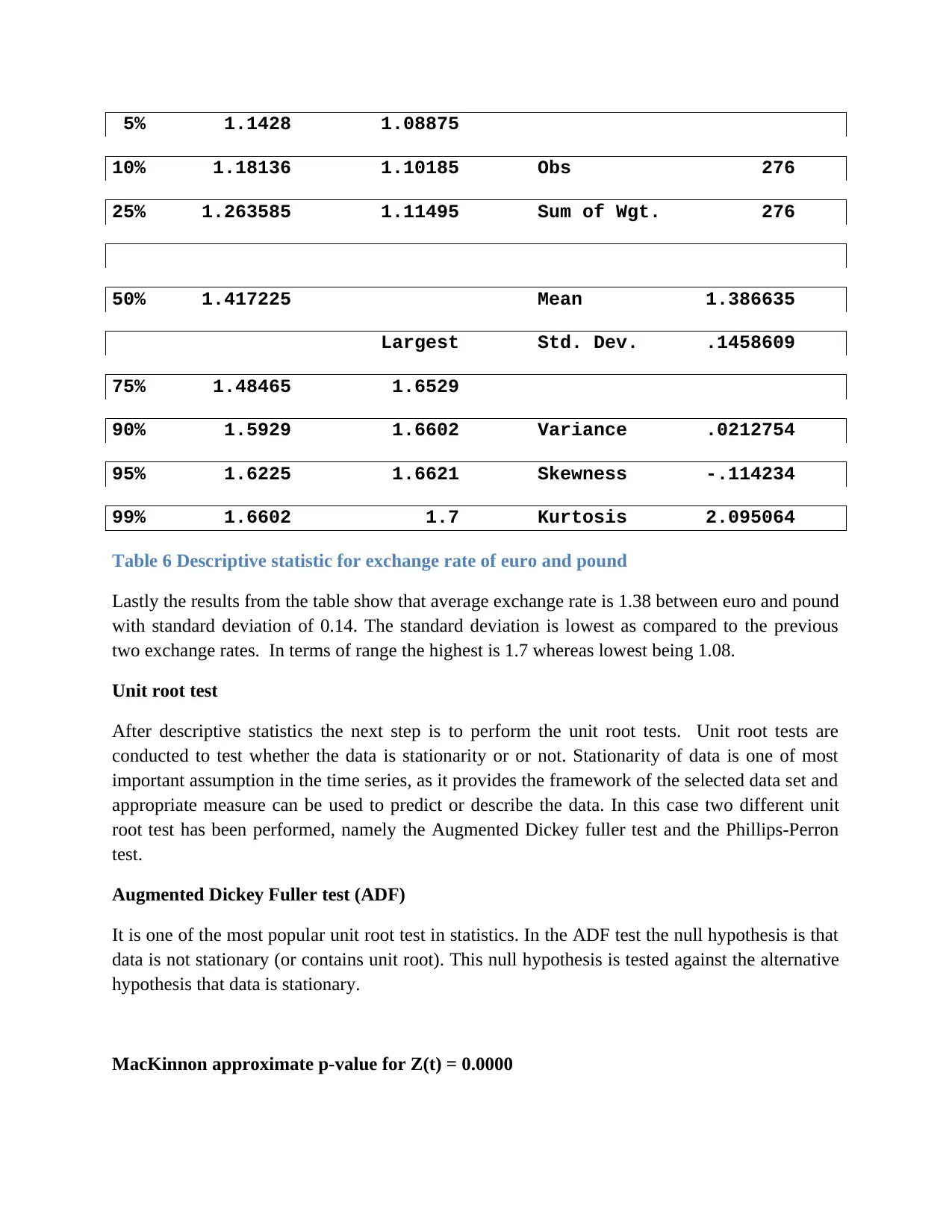

Table 6 Descriptive statistic for exchange rate of euro and pound

Lastly the results from the table show that average exchange rate is 1.38 between euro and pound

with standard deviation of 0.14. The standard deviation is lowest as compared to the previous

two exchange rates. In terms of range the highest is 1.7 whereas lowest being 1.08.

Unit root test

After descriptive statistics the next step is to perform the unit root tests. Unit root tests are

conducted to test whether the data is stationarity or or not. Stationarity of data is one of most

important assumption in the time series, as it provides the framework of the selected data set and

appropriate measure can be used to predict or describe the data. In this case two different unit

root test has been performed, namely the Augmented Dickey fuller test and the Phillips-Perron

test.

Augmented Dickey Fuller test (ADF)

It is one of the most popular unit root test in statistics. In the ADF test the null hypothesis is that

data is not stationary (or contains unit root). This null hypothesis is tested against the alternative

hypothesis that data is stationary.

MacKinnon approximate p-value for Z(t) = 0.0000

10% 1.18136 1.10185 Obs 276

25% 1.263585 1.11495 Sum of Wgt. 276

50% 1.417225 Mean 1.386635

Largest Std. Dev. .1458609

75% 1.48465 1.6529

90% 1.5929 1.6602 Variance .0212754

95% 1.6225 1.6621 Skewness -.114234

99% 1.6602 1.7 Kurtosis 2.095064

Table 6 Descriptive statistic for exchange rate of euro and pound

Lastly the results from the table show that average exchange rate is 1.38 between euro and pound

with standard deviation of 0.14. The standard deviation is lowest as compared to the previous

two exchange rates. In terms of range the highest is 1.7 whereas lowest being 1.08.

Unit root test

After descriptive statistics the next step is to perform the unit root tests. Unit root tests are

conducted to test whether the data is stationarity or or not. Stationarity of data is one of most

important assumption in the time series, as it provides the framework of the selected data set and

appropriate measure can be used to predict or describe the data. In this case two different unit

root test has been performed, namely the Augmented Dickey fuller test and the Phillips-Perron

test.

Augmented Dickey Fuller test (ADF)

It is one of the most popular unit root test in statistics. In the ADF test the null hypothesis is that

data is not stationary (or contains unit root). This null hypothesis is tested against the alternative

hypothesis that data is stationary.

MacKinnon approximate p-value for Z(t) = 0.0000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.