L'Oréal S.A. Financial Statement Analysis: Ratios, Valuation Model

VerifiedAdded on 2023/06/14

|26

|4604

|483

Report

AI Summary

This report provides a comprehensive financial statement analysis of L’Oréal S.A., including an analyst’s tear sheet with stock recommendations. It covers industry analysis using PEST, competitor analysis using Porter’s Five Forces, and an overview of L’Oréal’s business model and corporate strategy. The report examines key corporate events, such as the acquisition of a vegan skincare brand, and summarizes L’Oréal’s financial performance from 2016 to 2020. It includes a detailed financial ratio analysis comparing L’Oréal to Revlon, along with company valuation using both multiples and discounted cash flow models, ultimately providing insights into the financial health and investment potential of L’Oréal.

FINANCIAL STATEMENT

ANALYSIS - COMPONENT

B

ANALYSIS - COMPONENT

B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Analyst’s tear sheet......................................................................................................................3

Company Profile..........................................................................................................................5

Industry Analysis.........................................................................................................................5

Competitors analysis....................................................................................................................6

L’Oréal Business model and corporate strategy..........................................................................7

Analysis of L’Oréal key corporate events and activities.............................................................7

Summary Analysis of L’Oréal Financial statement.....................................................................8

Financial ratio calculation of L’Oréal and Revlon along its interpretation and comparison.......8

Company Valuation using multiples model..............................................................................11

Cash Flow Model.......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

Appendix..........................................................................................................................................3

Discounted cash flow value per share.........................................................................................3

INTRODUCTION...........................................................................................................................3

Analyst’s tear sheet......................................................................................................................3

Company Profile..........................................................................................................................5

Industry Analysis.........................................................................................................................5

Competitors analysis....................................................................................................................6

L’Oréal Business model and corporate strategy..........................................................................7

Analysis of L’Oréal key corporate events and activities.............................................................7

Summary Analysis of L’Oréal Financial statement.....................................................................8

Financial ratio calculation of L’Oréal and Revlon along its interpretation and comparison.......8

Company Valuation using multiples model..............................................................................11

Cash Flow Model.......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

Appendix..........................................................................................................................................3

Discounted cash flow value per share.........................................................................................3

INTRODUCTION

Financial statement analysis means the process of analysing and identifying the financial

health of the business using the financial ratio, free cash flow model, EBITDA multiples and

analyst tear sheet. The present report will be based on L’Oréal S.A. and will cover the tear sheet

of company along with the stock recommendation to investors. Further, the report will cover the

industry analysis, competitor analysis, business model, financial statement & ratio analysis of

company Lastly, the report will determine the valuation of L’Oréal business on the basis of free

cash flow model and multiples model.

Analyst’s tear sheet

Financial statement analysis means the process of analysing and identifying the financial

health of the business using the financial ratio, free cash flow model, EBITDA multiples and

analyst tear sheet. The present report will be based on L’Oréal S.A. and will cover the tear sheet

of company along with the stock recommendation to investors. Further, the report will cover the

industry analysis, competitor analysis, business model, financial statement & ratio analysis of

company Lastly, the report will determine the valuation of L’Oréal business on the basis of free

cash flow model and multiples model.

Analyst’s tear sheet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

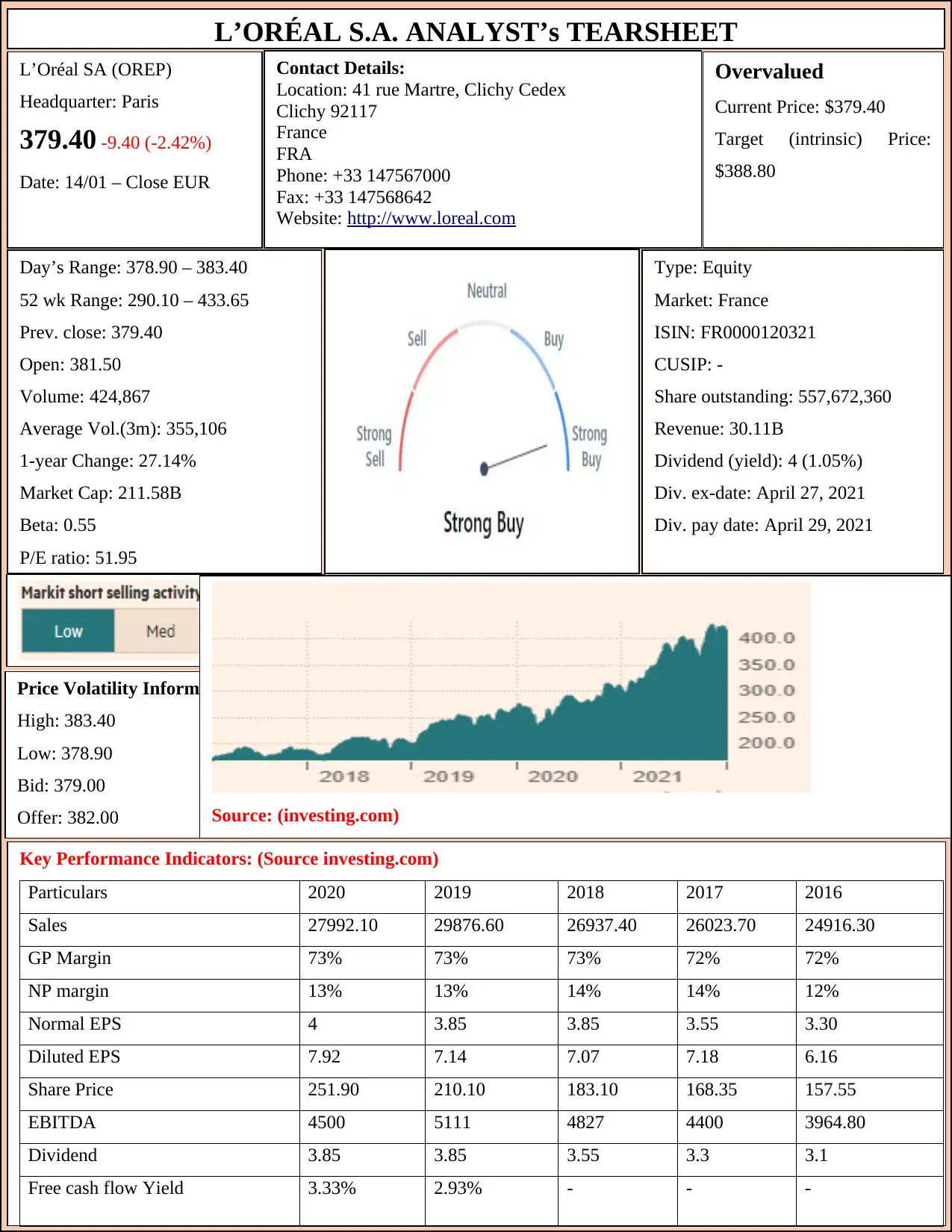

L’ORÉAL S.A. ANALYST’s TEARSHEET

L’Oréal SA (OREP)

Headquarter: Paris

379.40 -9.40 (-2.42%)

Date: 14/01 – Close EUR

Overvalued

Current Price: $379.40

Target (intrinsic) Price:

$388.80

Day’s Range: 378.90 – 383.40

52 wk Range: 290.10 – 433.65

Prev. close: 379.40

Open: 381.50

Volume: 424,867

Average Vol.(3m): 355,106

1-year Change: 27.14%

Market Cap: 211.58B

Beta: 0.55

P/E ratio: 51.95

Type: Equity

Market: France

ISIN: FR0000120321

CUSIP: -

Share outstanding: 557,672,360

Revenue: 30.11B

Dividend (yield): 4 (1.05%)

Div. ex-date: April 27, 2021

Div. pay date: April 29, 2021

Price Volatility Information

High: 383.40

Low: 378.90

Bid: 379.00

Offer: 382.00 Source: (investing.com)

Key Performance Indicators: (Source investing.com)

Particulars 2020 2019 2018 2017 2016

Sales 27992.10 29876.60 26937.40 26023.70 24916.30

GP Margin 73% 73% 73% 72% 72%

NP margin 13% 13% 14% 14% 12%

Normal EPS 4 3.85 3.85 3.55 3.30

Diluted EPS 7.92 7.14 7.07 7.18 6.16

Share Price 251.90 210.10 183.10 168.35 157.55

EBITDA 4500 5111 4827 4400 3964.80

Dividend 3.85 3.85 3.55 3.3 3.1

Free cash flow Yield 3.33% 2.93% - - -

Contact Details:

Location: 41 rue Martre, Clichy Cedex

Clichy 92117

France

FRA

Phone: +33 147567000

Fax: +33 147568642

Website: http://www.loreal.com

L’Oréal SA (OREP)

Headquarter: Paris

379.40 -9.40 (-2.42%)

Date: 14/01 – Close EUR

Overvalued

Current Price: $379.40

Target (intrinsic) Price:

$388.80

Day’s Range: 378.90 – 383.40

52 wk Range: 290.10 – 433.65

Prev. close: 379.40

Open: 381.50

Volume: 424,867

Average Vol.(3m): 355,106

1-year Change: 27.14%

Market Cap: 211.58B

Beta: 0.55

P/E ratio: 51.95

Type: Equity

Market: France

ISIN: FR0000120321

CUSIP: -

Share outstanding: 557,672,360

Revenue: 30.11B

Dividend (yield): 4 (1.05%)

Div. ex-date: April 27, 2021

Div. pay date: April 29, 2021

Price Volatility Information

High: 383.40

Low: 378.90

Bid: 379.00

Offer: 382.00 Source: (investing.com)

Key Performance Indicators: (Source investing.com)

Particulars 2020 2019 2018 2017 2016

Sales 27992.10 29876.60 26937.40 26023.70 24916.30

GP Margin 73% 73% 73% 72% 72%

NP margin 13% 13% 14% 14% 12%

Normal EPS 4 3.85 3.85 3.55 3.30

Diluted EPS 7.92 7.14 7.07 7.18 6.16

Share Price 251.90 210.10 183.10 168.35 157.55

EBITDA 4500 5111 4827 4400 3964.80

Dividend 3.85 3.85 3.55 3.3 3.1

Free cash flow Yield 3.33% 2.93% - - -

Contact Details:

Location: 41 rue Martre, Clichy Cedex

Clichy 92117

France

FRA

Phone: +33 147567000

Fax: +33 147568642

Website: http://www.loreal.com

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company Profile

L’Oréal SA is one of the largest cosmetic company of UK having headquarter in Clichy,

France with a register office in Paris. The company is basically a French personal care company

that focus on various segment products such as hair colour, skin care, sun protection, make-up,

perfumes and hair care. The company operates in cosmetic industry and serve its both local as

well as international customers. Presently, the company operates in more than 150 countries

which is consider as their large geographical segment. The total number of employees work with

L’Oréal is around 88000 as per 2020 annual report. Further, in the year 2021, the company has

announced the acquisition of Vegan skin care brand in order to increase their business segment

and attract more and more customers. The financial health of the company is best and growing

day by day. The operating profit, revenue, net profit of the company in the year 2021 is €2672.80

million, 15196.60 million and 2362.60 million respectively which is higher than the previous

year i.e., 2020 figures (AREAS, 2018). This means that after Covid-19, company again come on

their growing track. The company have various mergers and acquisitions which help them

existing their business in the competitive market and taking advantage of higher sales and

customer base.

Industry Analysis

In order to analyse the industry in which L’Oréal company operates, the PEST analysis tool

is used. The PEST analysis of cosmetic industry is as follows:

Political: This factor denotes the political stability etc. impact over the cosmetic

industry. Different country has their own rules and regulation which affects the industry

as well as company. Because of brexit and Covid-19, the sales of the company has

showed vast decline which also affect its profitability and financial health. The political

factor is creating threat for the cosmetics industry and L’Oréal company (Gassama,

2020).

Economical: This includes the economic stability and people income factor impact over

industry and company. After covid-19, the income of the consumers has shifted their

purchasing criteria to basic goods from luxury and unnecessary goods. Along with the

trade war between China and USA has also causes decrease in the demand of L’Oréal

products.

L’Oréal SA is one of the largest cosmetic company of UK having headquarter in Clichy,

France with a register office in Paris. The company is basically a French personal care company

that focus on various segment products such as hair colour, skin care, sun protection, make-up,

perfumes and hair care. The company operates in cosmetic industry and serve its both local as

well as international customers. Presently, the company operates in more than 150 countries

which is consider as their large geographical segment. The total number of employees work with

L’Oréal is around 88000 as per 2020 annual report. Further, in the year 2021, the company has

announced the acquisition of Vegan skin care brand in order to increase their business segment

and attract more and more customers. The financial health of the company is best and growing

day by day. The operating profit, revenue, net profit of the company in the year 2021 is €2672.80

million, 15196.60 million and 2362.60 million respectively which is higher than the previous

year i.e., 2020 figures (AREAS, 2018). This means that after Covid-19, company again come on

their growing track. The company have various mergers and acquisitions which help them

existing their business in the competitive market and taking advantage of higher sales and

customer base.

Industry Analysis

In order to analyse the industry in which L’Oréal company operates, the PEST analysis tool

is used. The PEST analysis of cosmetic industry is as follows:

Political: This factor denotes the political stability etc. impact over the cosmetic

industry. Different country has their own rules and regulation which affects the industry

as well as company. Because of brexit and Covid-19, the sales of the company has

showed vast decline which also affect its profitability and financial health. The political

factor is creating threat for the cosmetics industry and L’Oréal company (Gassama,

2020).

Economical: This includes the economic stability and people income factor impact over

industry and company. After covid-19, the income of the consumers has shifted their

purchasing criteria to basic goods from luxury and unnecessary goods. Along with the

trade war between China and USA has also causes decrease in the demand of L’Oréal

products.

Social: In the present time, people all over the world love to show off which helps the

cosmetic industry in the increase of their demand. The impact of which the sales of the

L’Oréal company has also increase because company provides products as per the taste

and preference of consumers (Eriksrød, 2018).

Technological: The technology is increasing day by day and consumer prefer more

digital and online shopping rather than offline shopping. The industry and cosmetics

companies such as L’Oréal has adopted digital platform to connect with the customer is

an opportunity for them which leads to increase in customer base.

Competitors analysis

The competitor’s analysis of cosmetics industry using the Porter five forces model are as

follows:

Buyer Power: The power of buyer over cosmetics is weak because they have little

influence on price and products. Thus, L’Oréal are able to offer high price for the

products as well negotiate for pricing with other companies.

Supplier Power: The bargaining power of supplier over the supply of raw material to

cosmetics companies are also weak. It is because the number of suppliers of cosmetics

such as beauty and personal care products are high and switching cost is also expensive

(Ndirangu, 2019).

Threat of new Entrants: The number of firms that produces similar cosmetics products

are low in the market thus the threat of new entrants is also low. L’Oréal is highly

affected with this factor because their market share will get increase with low threat of

new entrants.

Threat of substitute: The threat of substitute products is high in cosmetics industry

because there are many firms which produces same personal and skin care products

which is produces by L’Oréal. The impact of which they are facing the risk of losing their

sales and customer base (Galetić and Požega, 2019).

Degree of rivalry: The degree of rivalry is high in the case of cosmetics industry because

the number of competitors in the industry are increasing day by day. As the switching

cost for consumer are quite low thus they can easily shift to new and other competitors

which is a risk for L’Oréal.

cosmetic industry in the increase of their demand. The impact of which the sales of the

L’Oréal company has also increase because company provides products as per the taste

and preference of consumers (Eriksrød, 2018).

Technological: The technology is increasing day by day and consumer prefer more

digital and online shopping rather than offline shopping. The industry and cosmetics

companies such as L’Oréal has adopted digital platform to connect with the customer is

an opportunity for them which leads to increase in customer base.

Competitors analysis

The competitor’s analysis of cosmetics industry using the Porter five forces model are as

follows:

Buyer Power: The power of buyer over cosmetics is weak because they have little

influence on price and products. Thus, L’Oréal are able to offer high price for the

products as well negotiate for pricing with other companies.

Supplier Power: The bargaining power of supplier over the supply of raw material to

cosmetics companies are also weak. It is because the number of suppliers of cosmetics

such as beauty and personal care products are high and switching cost is also expensive

(Ndirangu, 2019).

Threat of new Entrants: The number of firms that produces similar cosmetics products

are low in the market thus the threat of new entrants is also low. L’Oréal is highly

affected with this factor because their market share will get increase with low threat of

new entrants.

Threat of substitute: The threat of substitute products is high in cosmetics industry

because there are many firms which produces same personal and skin care products

which is produces by L’Oréal. The impact of which they are facing the risk of losing their

sales and customer base (Galetić and Požega, 2019).

Degree of rivalry: The degree of rivalry is high in the case of cosmetics industry because

the number of competitors in the industry are increasing day by day. As the switching

cost for consumer are quite low thus they can easily shift to new and other competitors

which is a risk for L’Oréal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

L’Oréal Business model and corporate strategy

The corporate strategy adopted by L’Oréal is unique which is known as Universalization

means the company uses the globalization and understand the needs, traditions, desires of its

customers before selling any product. The strategy of company is to help millions of women and

men in getting their desire skin via their five branches. The company generates 29.9 billion euro

sales which is from 35% skincare segment, 26% make-up, 15% hair care, 10% hair collaring and

5% fragrances (Leppänen, George and Alexy, 2021). The business model of L’Oréal is based on

five pillars which are as follows:

The R&D of company worth around 1 billion euros.

The innovation of company contributes 15% annual sales of business.

The company release every year a new product for its customers.

The company is one of the leading national and international brand.

It also focusses on e-commerce to increase its sales.

Analysis of L’Oréal key corporate events and activities

One of the key and significant event and activities of L’Oréal is announcement of

acquisition of vegan skin care brand in the December 2021. The company has signed an

agreement to acquire Youth to the People company of California skincare brand. This is an

important event for the company because with the help of this acquisition the company able to

attract US, Canada, Australia and other European countries customer (Albert and et.al., 2021).

The acquisition event is quite profitable to company as they able to provide vegan skin care

products to its customers which are highly demanded by customers.

Summary Analysis of L’Oréal Financial statement

On the basis of the analysis of L’Oréal financial statement, it is identified that company are

performing well in the market because from 2016 to 2019, the sales, operating profit as well as

net profit of company in increasing. But in the year 2020, the financial health of business is

reducing which might be because of Covid-19 and lockdown. But this loss is temporary for the

company because as the government lift the lock-down, the sales of company will again increase

because of its online presence. With the help of E-commerce, the company have managed its

The corporate strategy adopted by L’Oréal is unique which is known as Universalization

means the company uses the globalization and understand the needs, traditions, desires of its

customers before selling any product. The strategy of company is to help millions of women and

men in getting their desire skin via their five branches. The company generates 29.9 billion euro

sales which is from 35% skincare segment, 26% make-up, 15% hair care, 10% hair collaring and

5% fragrances (Leppänen, George and Alexy, 2021). The business model of L’Oréal is based on

five pillars which are as follows:

The R&D of company worth around 1 billion euros.

The innovation of company contributes 15% annual sales of business.

The company release every year a new product for its customers.

The company is one of the leading national and international brand.

It also focusses on e-commerce to increase its sales.

Analysis of L’Oréal key corporate events and activities

One of the key and significant event and activities of L’Oréal is announcement of

acquisition of vegan skin care brand in the December 2021. The company has signed an

agreement to acquire Youth to the People company of California skincare brand. This is an

important event for the company because with the help of this acquisition the company able to

attract US, Canada, Australia and other European countries customer (Albert and et.al., 2021).

The acquisition event is quite profitable to company as they able to provide vegan skin care

products to its customers which are highly demanded by customers.

Summary Analysis of L’Oréal Financial statement

On the basis of the analysis of L’Oréal financial statement, it is identified that company are

performing well in the market because from 2016 to 2019, the sales, operating profit as well as

net profit of company in increasing. But in the year 2020, the financial health of business is

reducing which might be because of Covid-19 and lockdown. But this loss is temporary for the

company because as the government lift the lock-down, the sales of company will again increase

because of its online presence. With the help of E-commerce, the company have managed its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operations even in this pandemic situation (AREAS, 2018). Thus, overall financial statement of

the company is good.

Financial ratio calculation of L’Oréal and Revlon along its interpretation and comparison

the company is good.

Financial ratio calculation of L’Oréal and Revlon along its interpretation and comparison

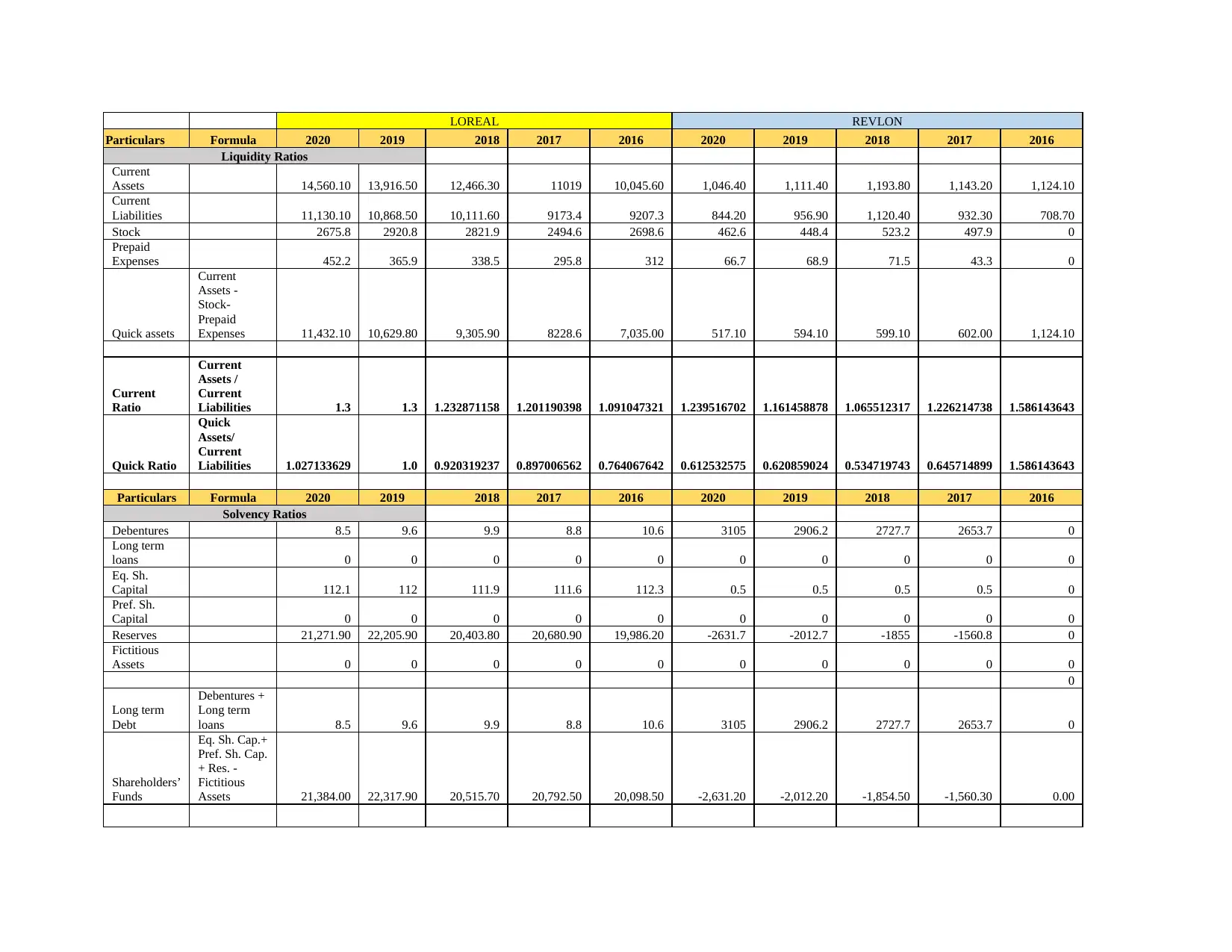

LOREAL REVLON

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Liquidity Ratios

Current

Assets 14,560.10 13,916.50 12,466.30 11019 10,045.60 1,046.40 1,111.40 1,193.80 1,143.20 1,124.10

Current

Liabilities 11,130.10 10,868.50 10,111.60 9173.4 9207.3 844.20 956.90 1,120.40 932.30 708.70

Stock 2675.8 2920.8 2821.9 2494.6 2698.6 462.6 448.4 523.2 497.9 0

Prepaid

Expenses 452.2 365.9 338.5 295.8 312 66.7 68.9 71.5 43.3 0

Quick assets

Current

Assets -

Stock-

Prepaid

Expenses 11,432.10 10,629.80 9,305.90 8228.6 7,035.00 517.10 594.10 599.10 602.00 1,124.10

Current

Ratio

Current

Assets /

Current

Liabilities 1.3 1.3 1.232871158 1.201190398 1.091047321 1.239516702 1.161458878 1.065512317 1.226214738 1.586143643

Quick Ratio

Quick

Assets/

Current

Liabilities 1.027133629 1.0 0.920319237 0.897006562 0.764067642 0.612532575 0.620859024 0.534719743 0.645714899 1.586143643

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Solvency Ratios

Debentures 8.5 9.6 9.9 8.8 10.6 3105 2906.2 2727.7 2653.7 0

Long term

loans 0 0 0 0 0 0 0 0 0 0

Eq. Sh.

Capital 112.1 112 111.9 111.6 112.3 0.5 0.5 0.5 0.5 0

Pref. Sh.

Capital 0 0 0 0 0 0 0 0 0 0

Reserves 21,271.90 22,205.90 20,403.80 20,680.90 19,986.20 -2631.7 -2012.7 -1855 -1560.8 0

Fictitious

Assets 0 0 0 0 0 0 0 0 0 0

0

Long term

Debt

Debentures +

Long term

loans 8.5 9.6 9.9 8.8 10.6 3105 2906.2 2727.7 2653.7 0

Shareholders’

Funds

Eq. Sh. Cap.+

Pref. Sh. Cap.

+ Res. -

Fictitious

Assets 21,384.00 22,317.90 20,515.70 20,792.50 20,098.50 -2,631.20 -2,012.20 -1,854.50 -1,560.30 0.00

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Liquidity Ratios

Current

Assets 14,560.10 13,916.50 12,466.30 11019 10,045.60 1,046.40 1,111.40 1,193.80 1,143.20 1,124.10

Current

Liabilities 11,130.10 10,868.50 10,111.60 9173.4 9207.3 844.20 956.90 1,120.40 932.30 708.70

Stock 2675.8 2920.8 2821.9 2494.6 2698.6 462.6 448.4 523.2 497.9 0

Prepaid

Expenses 452.2 365.9 338.5 295.8 312 66.7 68.9 71.5 43.3 0

Quick assets

Current

Assets -

Stock-

Prepaid

Expenses 11,432.10 10,629.80 9,305.90 8228.6 7,035.00 517.10 594.10 599.10 602.00 1,124.10

Current

Ratio

Current

Assets /

Current

Liabilities 1.3 1.3 1.232871158 1.201190398 1.091047321 1.239516702 1.161458878 1.065512317 1.226214738 1.586143643

Quick Ratio

Quick

Assets/

Current

Liabilities 1.027133629 1.0 0.920319237 0.897006562 0.764067642 0.612532575 0.620859024 0.534719743 0.645714899 1.586143643

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Solvency Ratios

Debentures 8.5 9.6 9.9 8.8 10.6 3105 2906.2 2727.7 2653.7 0

Long term

loans 0 0 0 0 0 0 0 0 0 0

Eq. Sh.

Capital 112.1 112 111.9 111.6 112.3 0.5 0.5 0.5 0.5 0

Pref. Sh.

Capital 0 0 0 0 0 0 0 0 0 0

Reserves 21,271.90 22,205.90 20,403.80 20,680.90 19,986.20 -2631.7 -2012.7 -1855 -1560.8 0

Fictitious

Assets 0 0 0 0 0 0 0 0 0 0

0

Long term

Debt

Debentures +

Long term

loans 8.5 9.6 9.9 8.8 10.6 3105 2906.2 2727.7 2653.7 0

Shareholders’

Funds

Eq. Sh. Cap.+

Pref. Sh. Cap.

+ Res. -

Fictitious

Assets 21,384.00 22,317.90 20,515.70 20,792.50 20,098.50 -2,631.20 -2,012.20 -1,854.50 -1,560.30 0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

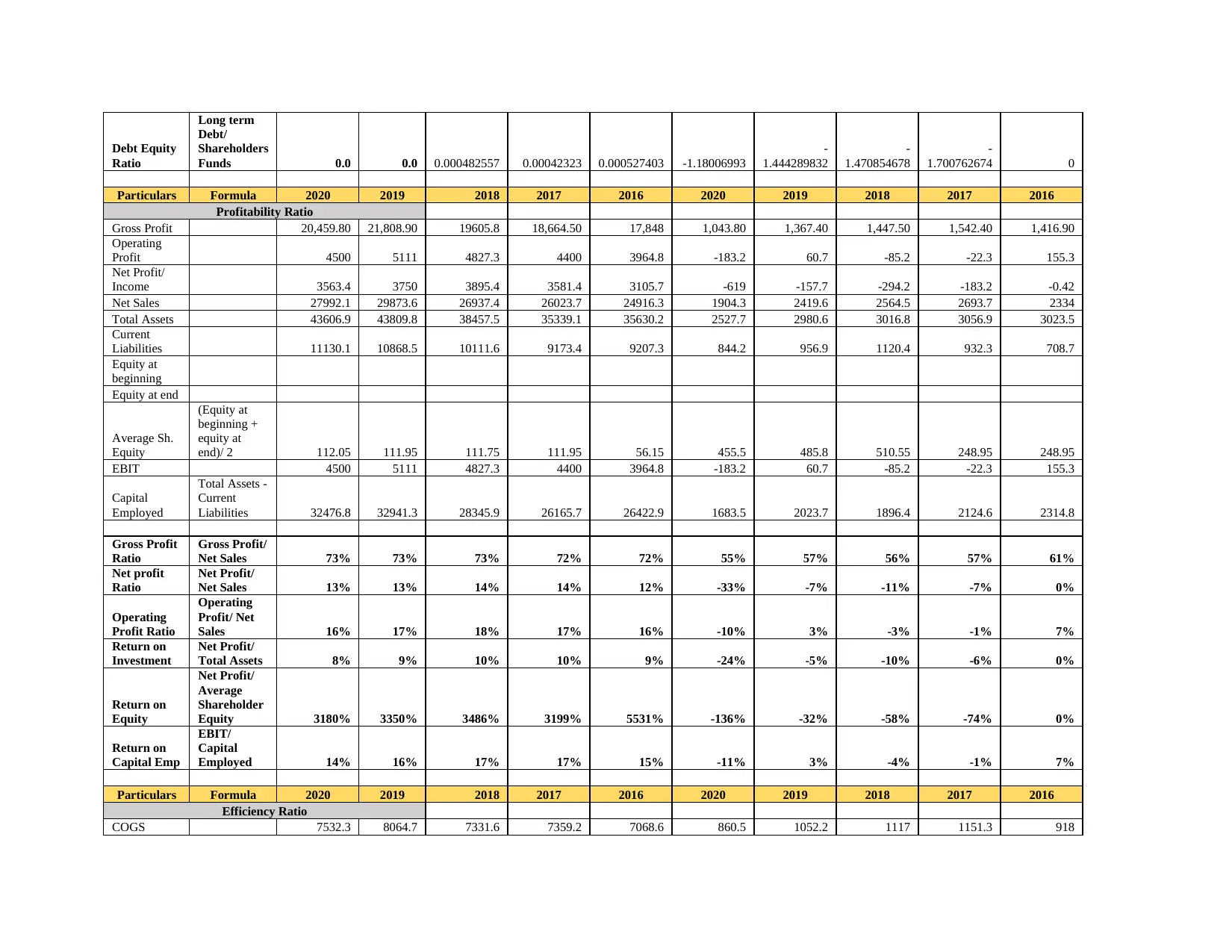

Debt Equity

Ratio

Long term

Debt/

Shareholders

Funds 0.0 0.0 0.000482557 0.00042323 0.000527403 -1.18006993

-

1.444289832

-

1.470854678

-

1.700762674 0

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Profitability Ratio

Gross Profit 20,459.80 21,808.90 19605.8 18,664.50 17,848 1,043.80 1,367.40 1,447.50 1,542.40 1,416.90

Operating

Profit 4500 5111 4827.3 4400 3964.8 -183.2 60.7 -85.2 -22.3 155.3

Net Profit/

Income 3563.4 3750 3895.4 3581.4 3105.7 -619 -157.7 -294.2 -183.2 -0.42

Net Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2564.5 2693.7 2334

Total Assets 43606.9 43809.8 38457.5 35339.1 35630.2 2527.7 2980.6 3016.8 3056.9 3023.5

Current

Liabilities 11130.1 10868.5 10111.6 9173.4 9207.3 844.2 956.9 1120.4 932.3 708.7

Equity at

beginning

Equity at end

Average Sh.

Equity

(Equity at

beginning +

equity at

end)/ 2 112.05 111.95 111.75 111.95 56.15 455.5 485.8 510.55 248.95 248.95

EBIT 4500 5111 4827.3 4400 3964.8 -183.2 60.7 -85.2 -22.3 155.3

Capital

Employed

Total Assets -

Current

Liabilities 32476.8 32941.3 28345.9 26165.7 26422.9 1683.5 2023.7 1896.4 2124.6 2314.8

Gross Profit

Ratio

Gross Profit/

Net Sales 73% 73% 73% 72% 72% 55% 57% 56% 57% 61%

Net profit

Ratio

Net Profit/

Net Sales 13% 13% 14% 14% 12% -33% -7% -11% -7% 0%

Operating

Profit Ratio

Operating

Profit/ Net

Sales 16% 17% 18% 17% 16% -10% 3% -3% -1% 7%

Return on

Investment

Net Profit/

Total Assets 8% 9% 10% 10% 9% -24% -5% -10% -6% 0%

Return on

Equity

Net Profit/

Average

Shareholder

Equity 3180% 3350% 3486% 3199% 5531% -136% -32% -58% -74% 0%

Return on

Capital Emp

EBIT/

Capital

Employed 14% 16% 17% 17% 15% -11% 3% -4% -1% 7%

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Efficiency Ratio

COGS 7532.3 8064.7 7331.6 7359.2 7068.6 860.5 1052.2 1117 1151.3 918

Ratio

Long term

Debt/

Shareholders

Funds 0.0 0.0 0.000482557 0.00042323 0.000527403 -1.18006993

-

1.444289832

-

1.470854678

-

1.700762674 0

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Profitability Ratio

Gross Profit 20,459.80 21,808.90 19605.8 18,664.50 17,848 1,043.80 1,367.40 1,447.50 1,542.40 1,416.90

Operating

Profit 4500 5111 4827.3 4400 3964.8 -183.2 60.7 -85.2 -22.3 155.3

Net Profit/

Income 3563.4 3750 3895.4 3581.4 3105.7 -619 -157.7 -294.2 -183.2 -0.42

Net Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2564.5 2693.7 2334

Total Assets 43606.9 43809.8 38457.5 35339.1 35630.2 2527.7 2980.6 3016.8 3056.9 3023.5

Current

Liabilities 11130.1 10868.5 10111.6 9173.4 9207.3 844.2 956.9 1120.4 932.3 708.7

Equity at

beginning

Equity at end

Average Sh.

Equity

(Equity at

beginning +

equity at

end)/ 2 112.05 111.95 111.75 111.95 56.15 455.5 485.8 510.55 248.95 248.95

EBIT 4500 5111 4827.3 4400 3964.8 -183.2 60.7 -85.2 -22.3 155.3

Capital

Employed

Total Assets -

Current

Liabilities 32476.8 32941.3 28345.9 26165.7 26422.9 1683.5 2023.7 1896.4 2124.6 2314.8

Gross Profit

Ratio

Gross Profit/

Net Sales 73% 73% 73% 72% 72% 55% 57% 56% 57% 61%

Net profit

Ratio

Net Profit/

Net Sales 13% 13% 14% 14% 12% -33% -7% -11% -7% 0%

Operating

Profit Ratio

Operating

Profit/ Net

Sales 16% 17% 18% 17% 16% -10% 3% -3% -1% 7%

Return on

Investment

Net Profit/

Total Assets 8% 9% 10% 10% 9% -24% -5% -10% -6% 0%

Return on

Equity

Net Profit/

Average

Shareholder

Equity 3180% 3350% 3486% 3199% 5531% -136% -32% -58% -74% 0%

Return on

Capital Emp

EBIT/

Capital

Employed 14% 16% 17% 17% 15% -11% 3% -4% -1% 7%

Particulars Formula 2020 2019 2018 2017 2016 2020 2019 2018 2017 2016

Efficiency Ratio

COGS 7532.3 8064.7 7331.6 7359.2 7068.6 860.5 1052.2 1117 1151.3 918

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

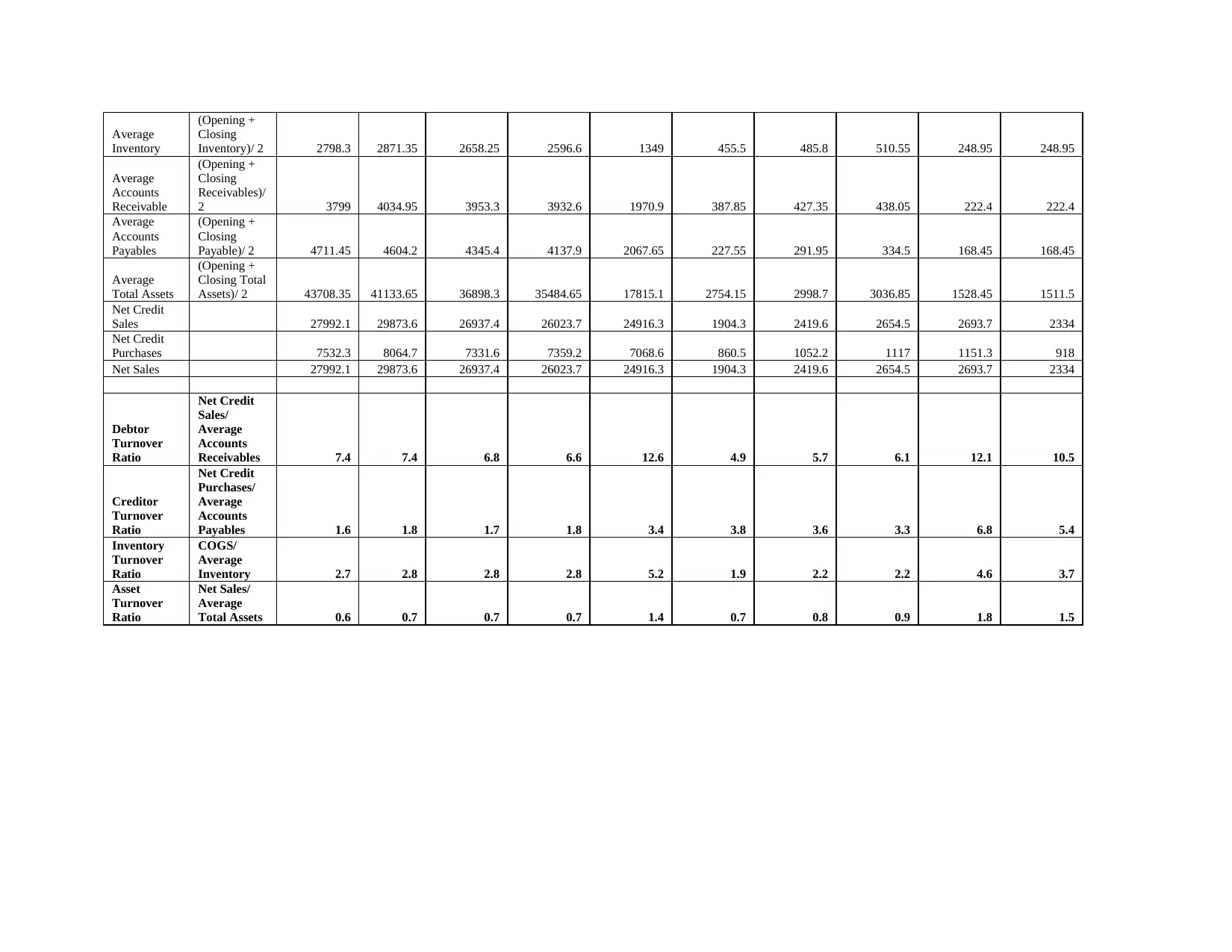

Average

Inventory

(Opening +

Closing

Inventory)/ 2 2798.3 2871.35 2658.25 2596.6 1349 455.5 485.8 510.55 248.95 248.95

Average

Accounts

Receivable

(Opening +

Closing

Receivables)/

2 3799 4034.95 3953.3 3932.6 1970.9 387.85 427.35 438.05 222.4 222.4

Average

Accounts

Payables

(Opening +

Closing

Payable)/ 2 4711.45 4604.2 4345.4 4137.9 2067.65 227.55 291.95 334.5 168.45 168.45

Average

Total Assets

(Opening +

Closing Total

Assets)/ 2 43708.35 41133.65 36898.3 35484.65 17815.1 2754.15 2998.7 3036.85 1528.45 1511.5

Net Credit

Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2654.5 2693.7 2334

Net Credit

Purchases 7532.3 8064.7 7331.6 7359.2 7068.6 860.5 1052.2 1117 1151.3 918

Net Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2654.5 2693.7 2334

Debtor

Turnover

Ratio

Net Credit

Sales/

Average

Accounts

Receivables 7.4 7.4 6.8 6.6 12.6 4.9 5.7 6.1 12.1 10.5

Creditor

Turnover

Ratio

Net Credit

Purchases/

Average

Accounts

Payables 1.6 1.8 1.7 1.8 3.4 3.8 3.6 3.3 6.8 5.4

Inventory

Turnover

Ratio

COGS/

Average

Inventory 2.7 2.8 2.8 2.8 5.2 1.9 2.2 2.2 4.6 3.7

Asset

Turnover

Ratio

Net Sales/

Average

Total Assets 0.6 0.7 0.7 0.7 1.4 0.7 0.8 0.9 1.8 1.5

Inventory

(Opening +

Closing

Inventory)/ 2 2798.3 2871.35 2658.25 2596.6 1349 455.5 485.8 510.55 248.95 248.95

Average

Accounts

Receivable

(Opening +

Closing

Receivables)/

2 3799 4034.95 3953.3 3932.6 1970.9 387.85 427.35 438.05 222.4 222.4

Average

Accounts

Payables

(Opening +

Closing

Payable)/ 2 4711.45 4604.2 4345.4 4137.9 2067.65 227.55 291.95 334.5 168.45 168.45

Average

Total Assets

(Opening +

Closing Total

Assets)/ 2 43708.35 41133.65 36898.3 35484.65 17815.1 2754.15 2998.7 3036.85 1528.45 1511.5

Net Credit

Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2654.5 2693.7 2334

Net Credit

Purchases 7532.3 8064.7 7331.6 7359.2 7068.6 860.5 1052.2 1117 1151.3 918

Net Sales 27992.1 29873.6 26937.4 26023.7 24916.3 1904.3 2419.6 2654.5 2693.7 2334

Debtor

Turnover

Ratio

Net Credit

Sales/

Average

Accounts

Receivables 7.4 7.4 6.8 6.6 12.6 4.9 5.7 6.1 12.1 10.5

Creditor

Turnover

Ratio

Net Credit

Purchases/

Average

Accounts

Payables 1.6 1.8 1.7 1.8 3.4 3.8 3.6 3.3 6.8 5.4

Inventory

Turnover

Ratio

COGS/

Average

Inventory 2.7 2.8 2.8 2.8 5.2 1.9 2.2 2.2 4.6 3.7

Asset

Turnover

Ratio

Net Sales/

Average

Total Assets 0.6 0.7 0.7 0.7 1.4 0.7 0.8 0.9 1.8 1.5

Interpretation

Liquidity Ratios

Liquidity ratios are a form of financial ratios, used by different companies in order to analyse the

liquidity state of a company. These ratios are used to determine if the company has sufficient

assets which can be used to meet its short-term obligations.

From the above calculations of Loreal Paris, it can be stated that the liquidity of the company is

increasing little by little, which is a good indicator. The Current ratio of Loreal Paris were

recorded to be 1.091 in 2016 which increased to 1.2328 in 2018 and further reaching 1.3 in 2020.

Similarly, The Quick ratio of Loreal Paris was 0.764 which increased to 0.9203 in 2018 and

reach to 1.027 in 2020. The increasing liquidity ratio gives a feeling of contentment to the

shareholders of the company as the company is capable of repaying its short-term liabilities on

time. But Loreal Paris can still work on making its liquidity better by repaying its short terms

before time, cutting overhead expenses like rent, labour, marketing expenses (Haralayya, 2021).

The Loreal Paris is doing better than Revlon as the liquidity ratios of Revlon are constantly

decreasing.

Solvency Ratios

The ratios which helps an organization in identifying its capacity to pay long term debts are

known as Solvency ratios. Solvency ratios determines the amount of shareholder’s fund in

relation to the long-term debt owned by the company. It can be seen from the above table that the

solvency ratio of Loreal Paris is below 1. The debt equity ratio of the company in 2016 was

recorded as 0.0005274 and since then it is constantly deteriorating and in the year 2020 it came

down to zero. A debt equity ratio lower than 1 states that the company does not trust external

borrowings for financing. The ideal debt equity ratio is between 1 to 2. But it can be stated that

Loreal Paris has a better debt equity ratio than Revlon as negative debt equity ratio refers more

debt than assets (Pascal and et.al., 2021).

Profitability ratio

The profitability ratio of the company disclose the fact that company could govern an

increase rend in its profits. The net profit of the Loreal company could go down in the year 2019

Liquidity Ratios

Liquidity ratios are a form of financial ratios, used by different companies in order to analyse the

liquidity state of a company. These ratios are used to determine if the company has sufficient

assets which can be used to meet its short-term obligations.

From the above calculations of Loreal Paris, it can be stated that the liquidity of the company is

increasing little by little, which is a good indicator. The Current ratio of Loreal Paris were

recorded to be 1.091 in 2016 which increased to 1.2328 in 2018 and further reaching 1.3 in 2020.

Similarly, The Quick ratio of Loreal Paris was 0.764 which increased to 0.9203 in 2018 and

reach to 1.027 in 2020. The increasing liquidity ratio gives a feeling of contentment to the

shareholders of the company as the company is capable of repaying its short-term liabilities on

time. But Loreal Paris can still work on making its liquidity better by repaying its short terms

before time, cutting overhead expenses like rent, labour, marketing expenses (Haralayya, 2021).

The Loreal Paris is doing better than Revlon as the liquidity ratios of Revlon are constantly

decreasing.

Solvency Ratios

The ratios which helps an organization in identifying its capacity to pay long term debts are

known as Solvency ratios. Solvency ratios determines the amount of shareholder’s fund in

relation to the long-term debt owned by the company. It can be seen from the above table that the

solvency ratio of Loreal Paris is below 1. The debt equity ratio of the company in 2016 was

recorded as 0.0005274 and since then it is constantly deteriorating and in the year 2020 it came

down to zero. A debt equity ratio lower than 1 states that the company does not trust external

borrowings for financing. The ideal debt equity ratio is between 1 to 2. But it can be stated that

Loreal Paris has a better debt equity ratio than Revlon as negative debt equity ratio refers more

debt than assets (Pascal and et.al., 2021).

Profitability ratio

The profitability ratio of the company disclose the fact that company could govern an

increase rend in its profits. The net profit of the Loreal company could go down in the year 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.