Lovisa Holdings: Conceptual Framework & Financial Reporting Analysis

VerifiedAdded on 2023/06/09

|15

|2360

|159

Report

AI Summary

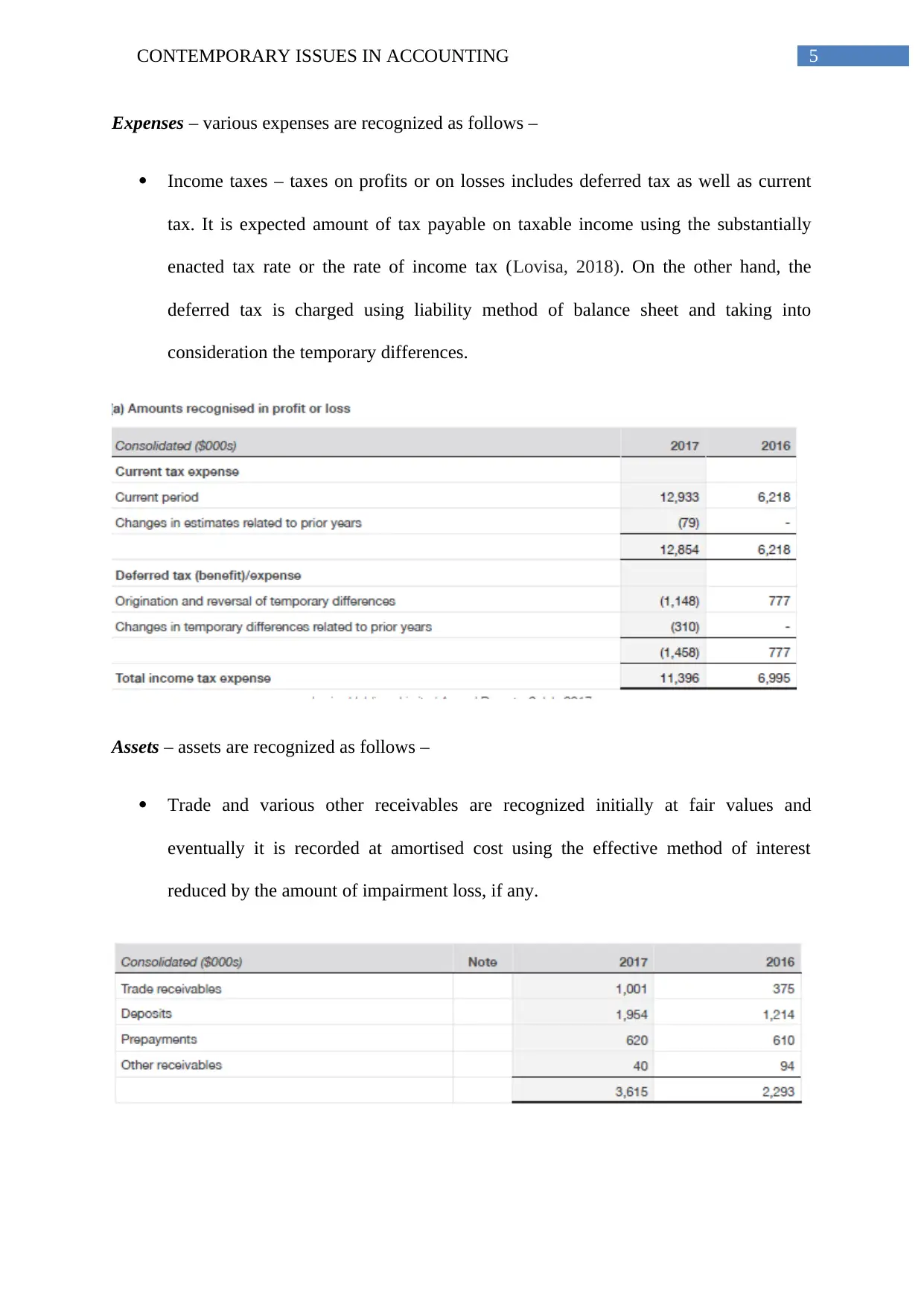

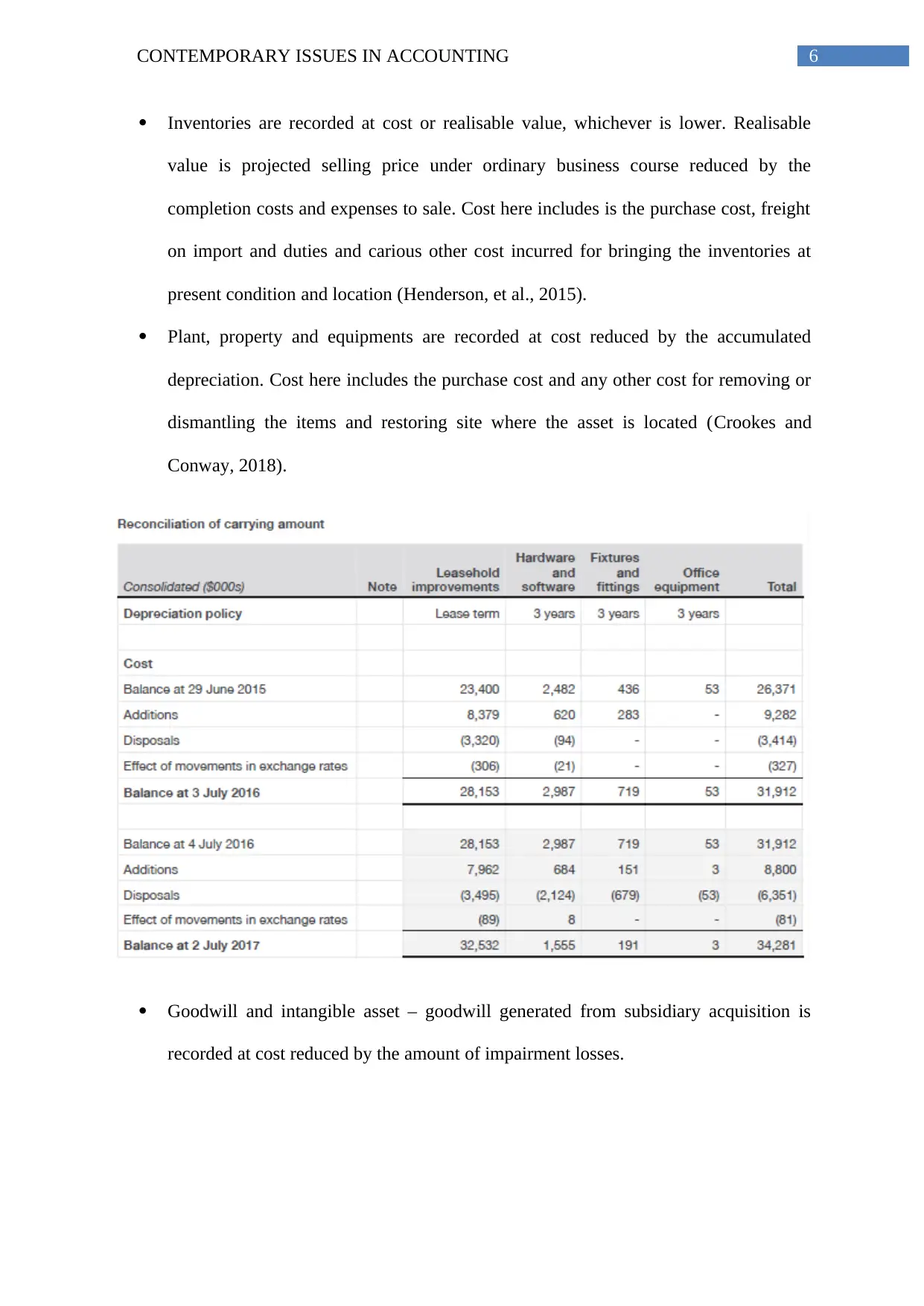

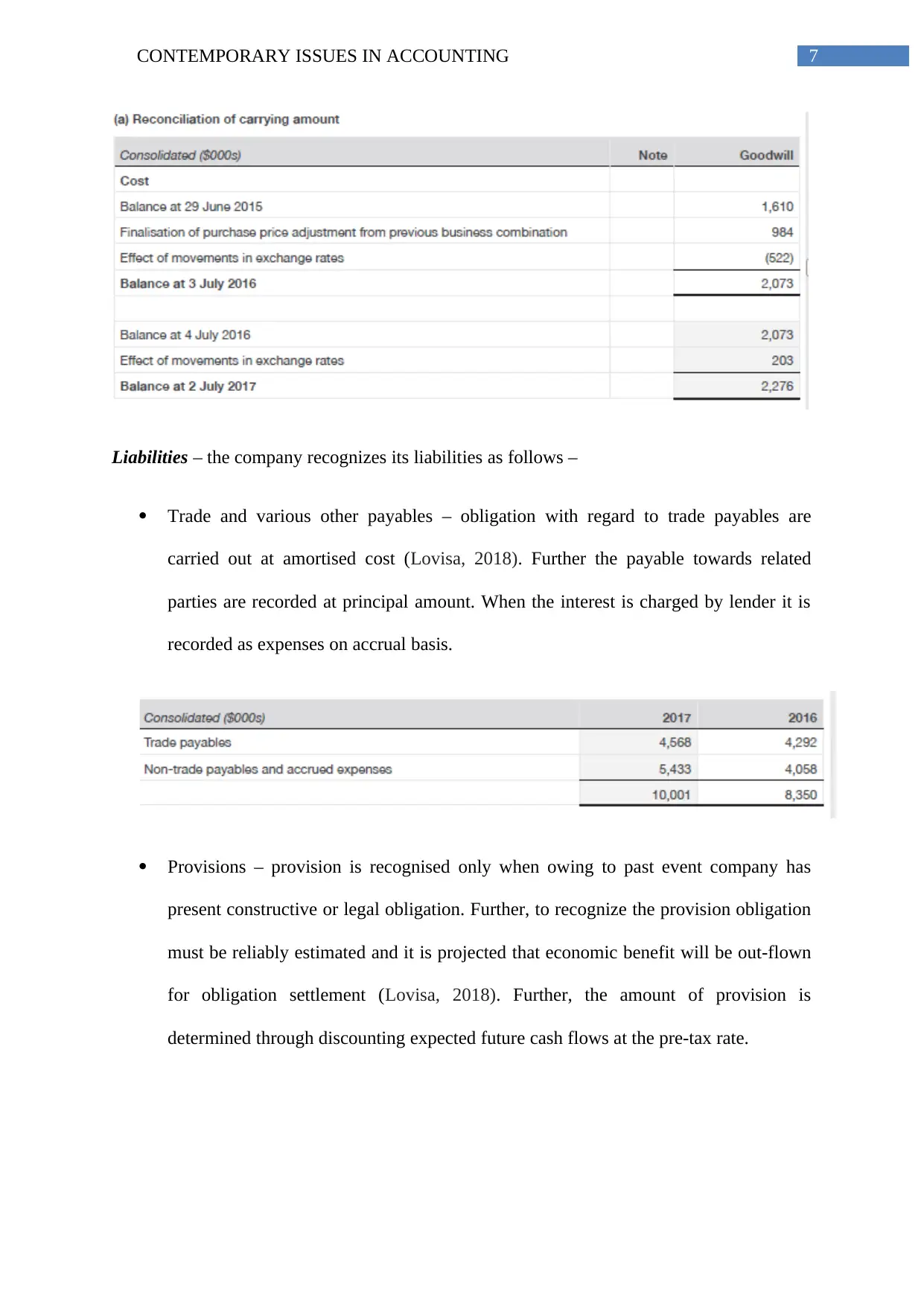

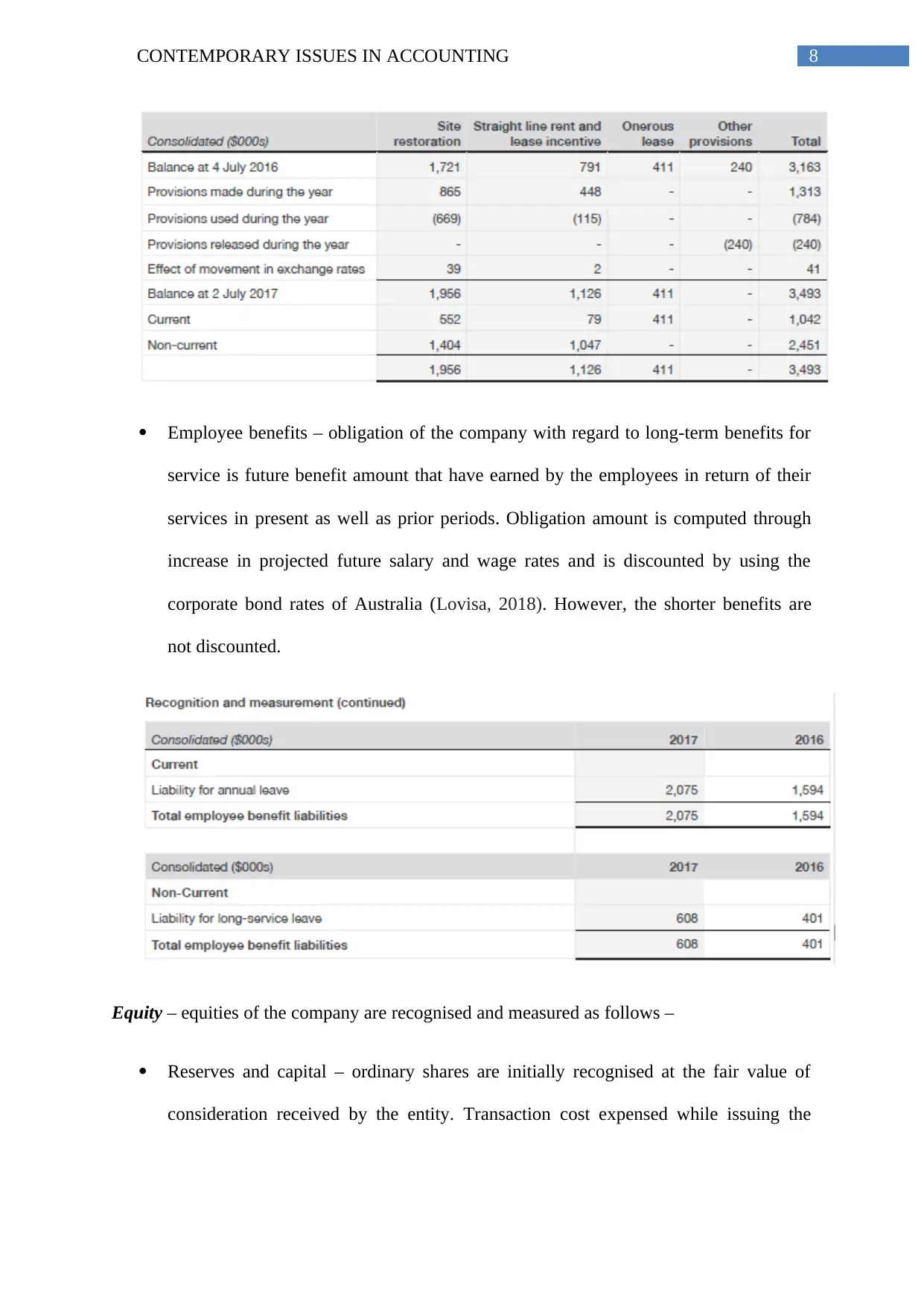

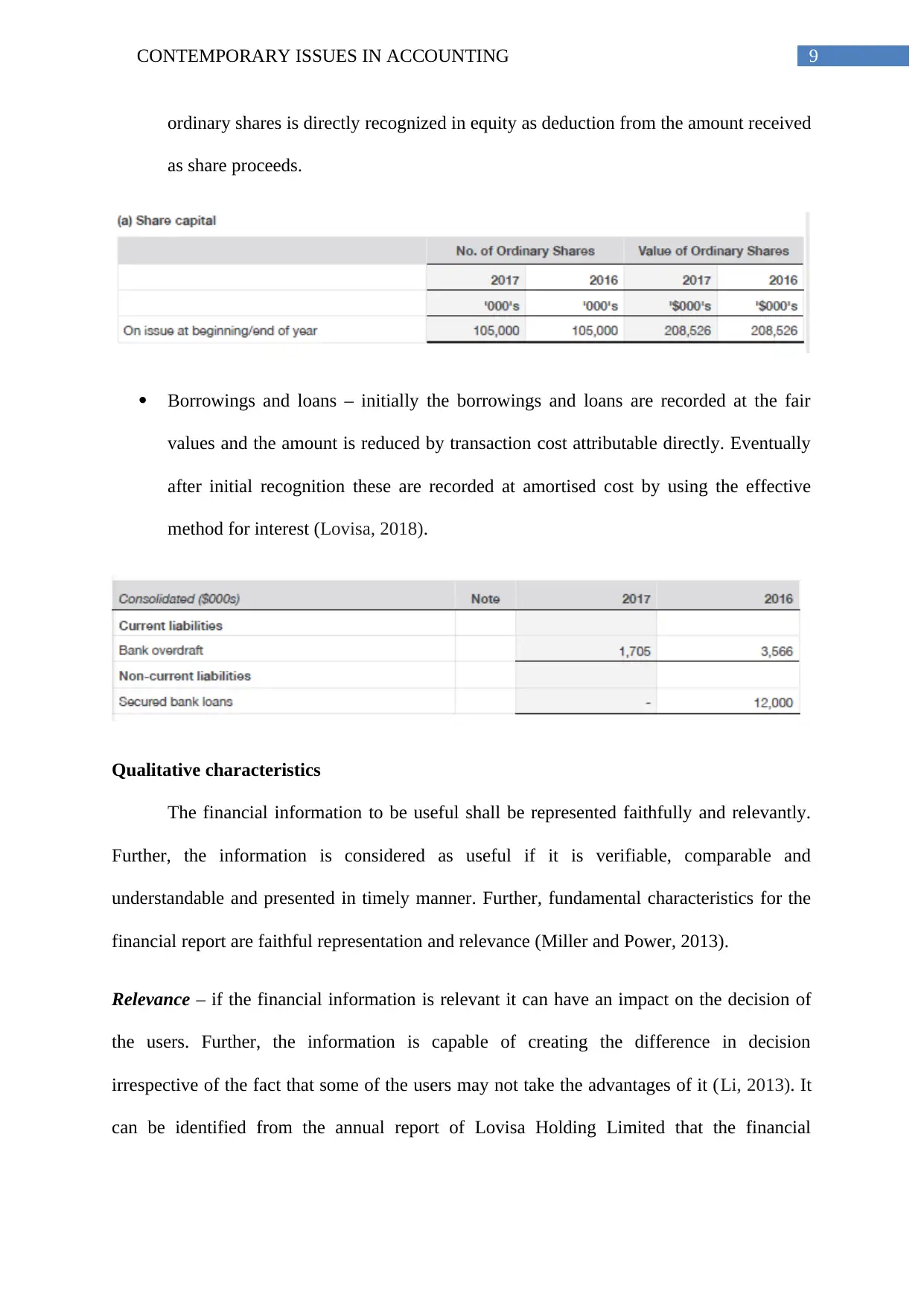

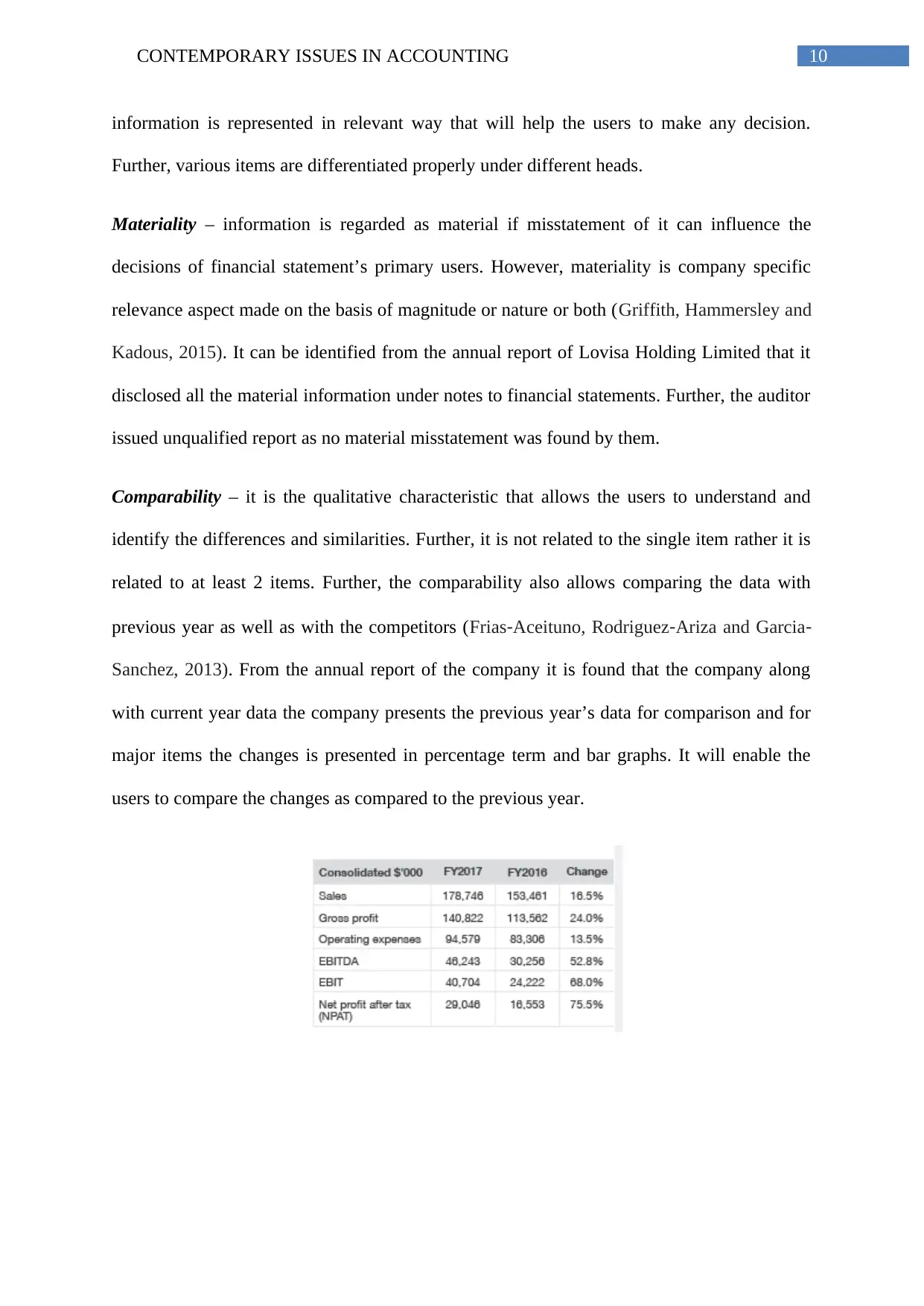

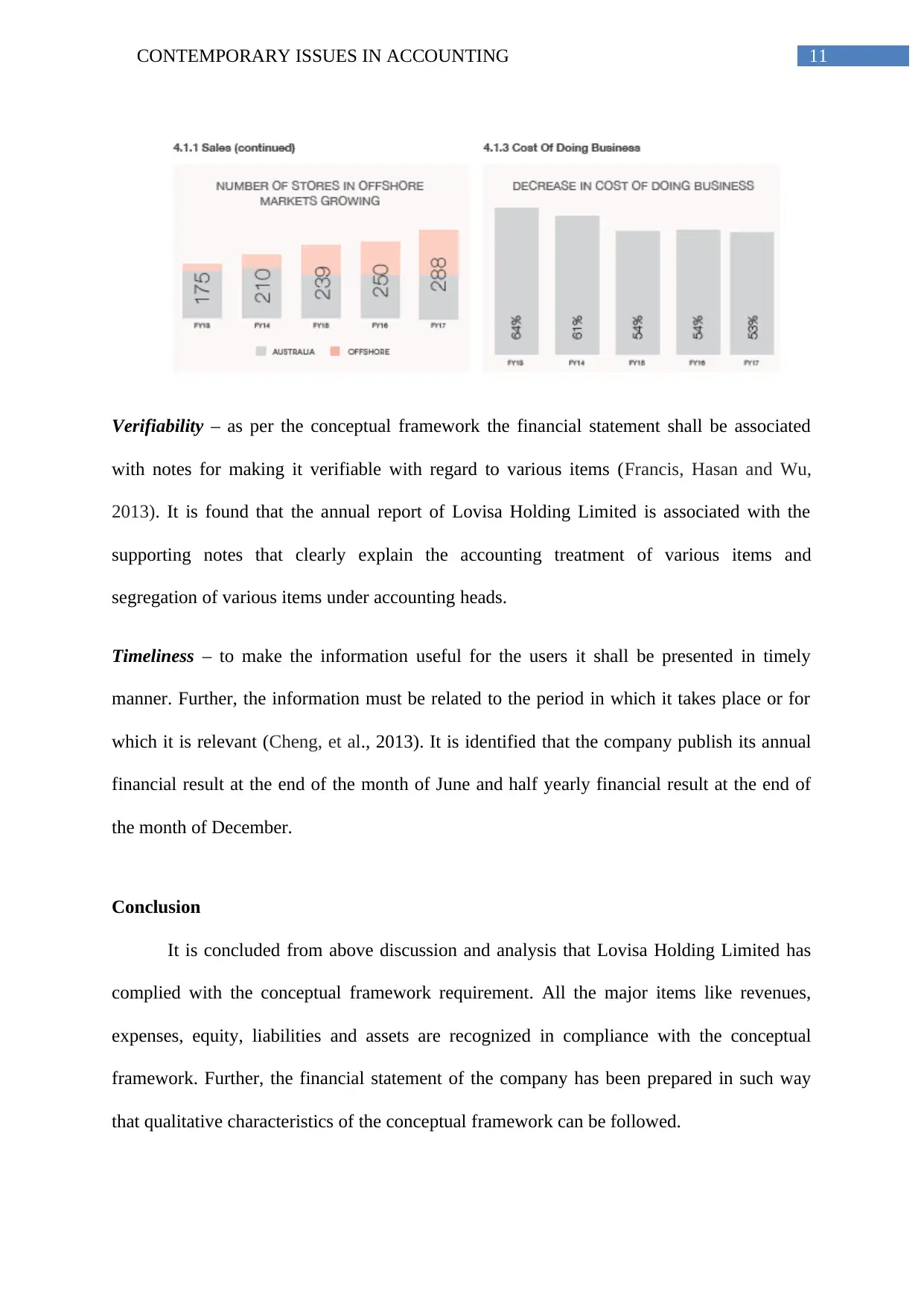

This report examines Lovisa Holdings Limited's compliance with the conceptual framework for financial reporting, focusing on its adherence to International Financial Reporting Standards (IFRS) and Australian Accounting Standards Board (AASB) guidelines. It analyzes the company's recognition criteria for assets, liabilities, incomes, expenses, and equity, evaluating whether Lovisa Holdings follows the qualitative characteristics of the conceptual framework in preparing its financial statements. The report finds that Lovisa Holdings generally complies with the conceptual framework, but recommends the inclusion of five years of financial data in table format to enhance comparability and analysis for users and potential investors. The analysis covers revenue recognition, expense recording, asset valuation, liability management, and equity measurement, ensuring a comprehensive understanding of Lovisa Holdings' financial reporting practices.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.