MIS775 - Portfolio Optimization using LP, ILP & NLP Decision Models

VerifiedAdded on 2023/06/13

|22

|1262

|286

Project

AI Summary

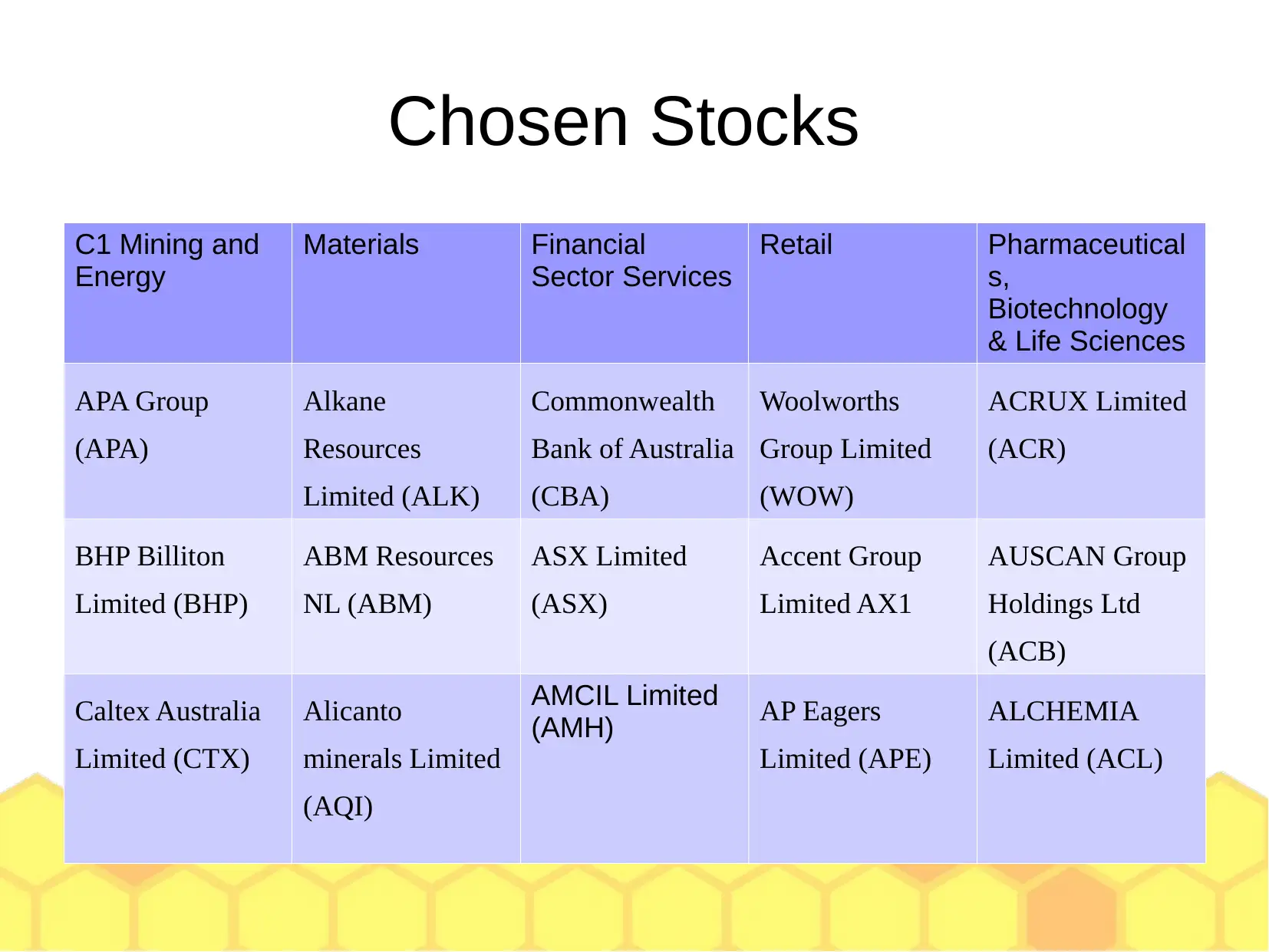

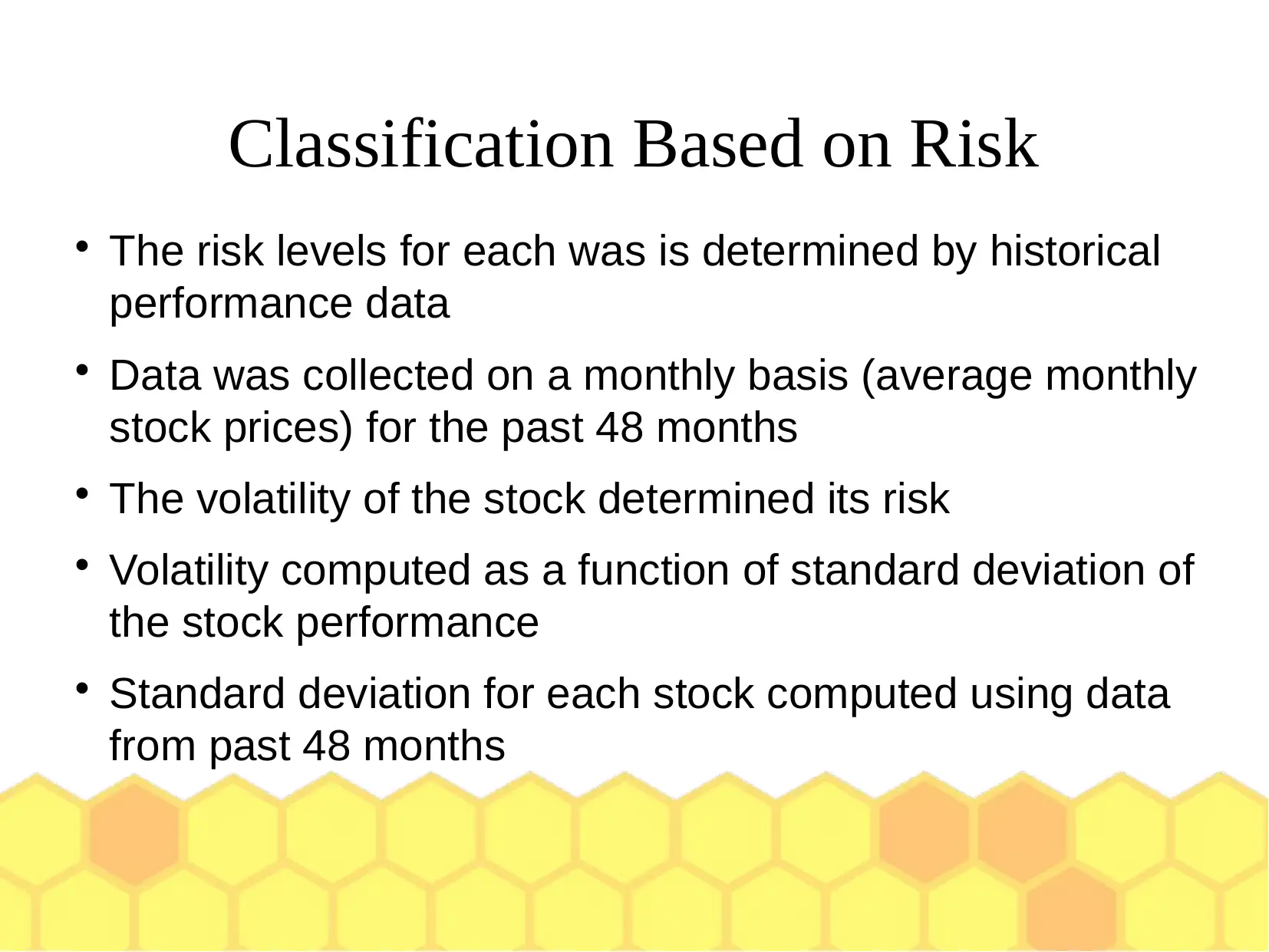

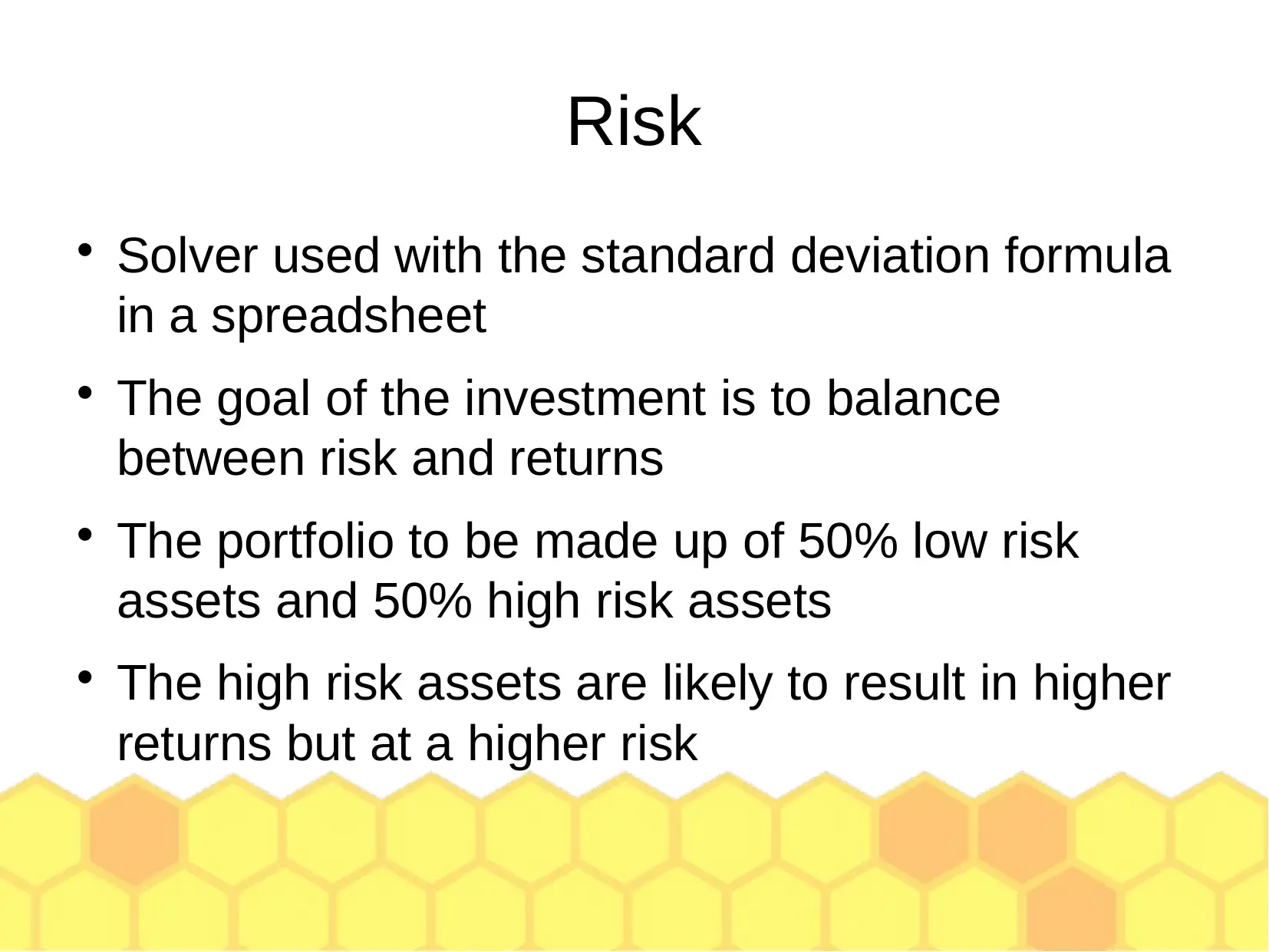

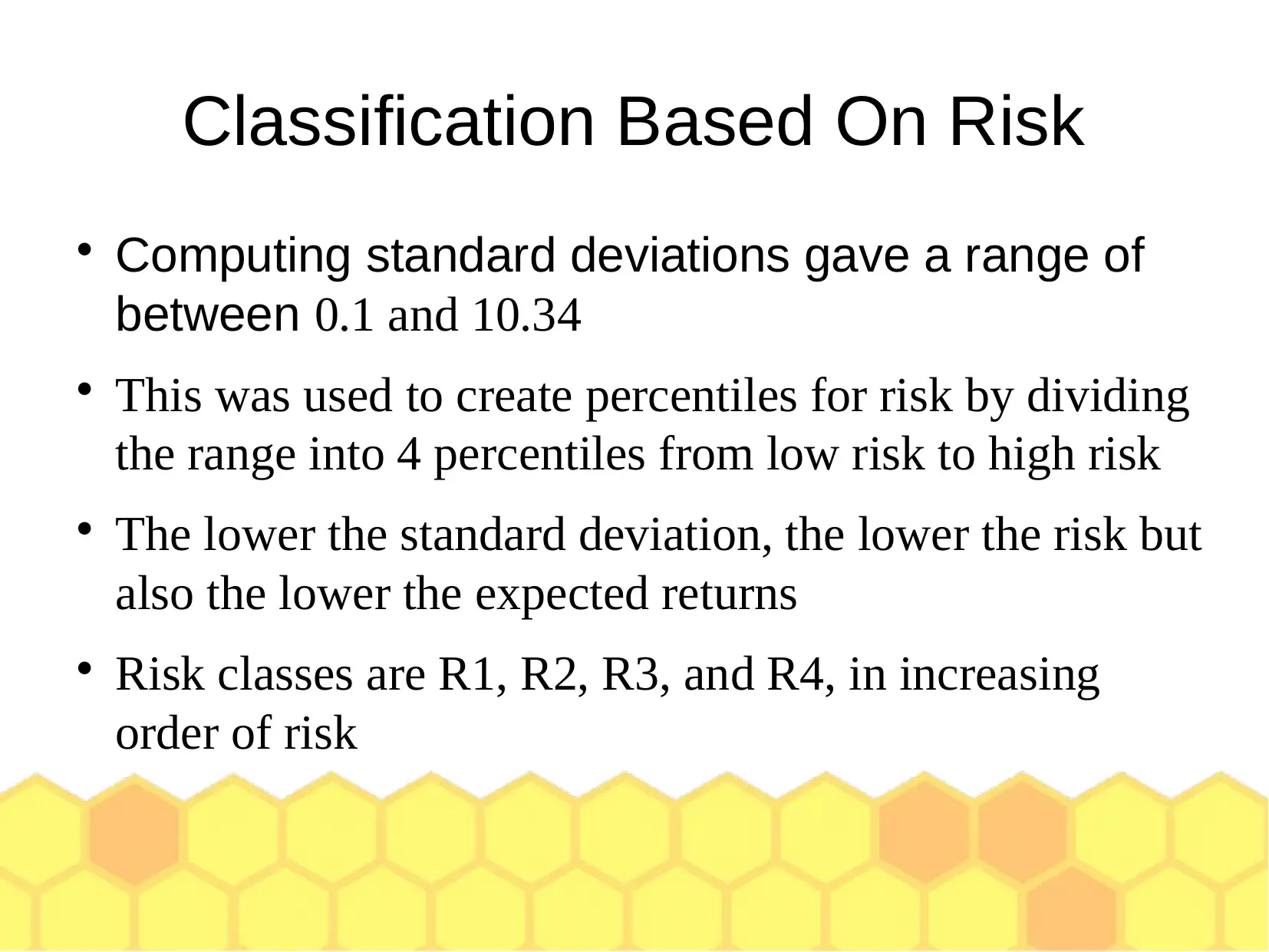

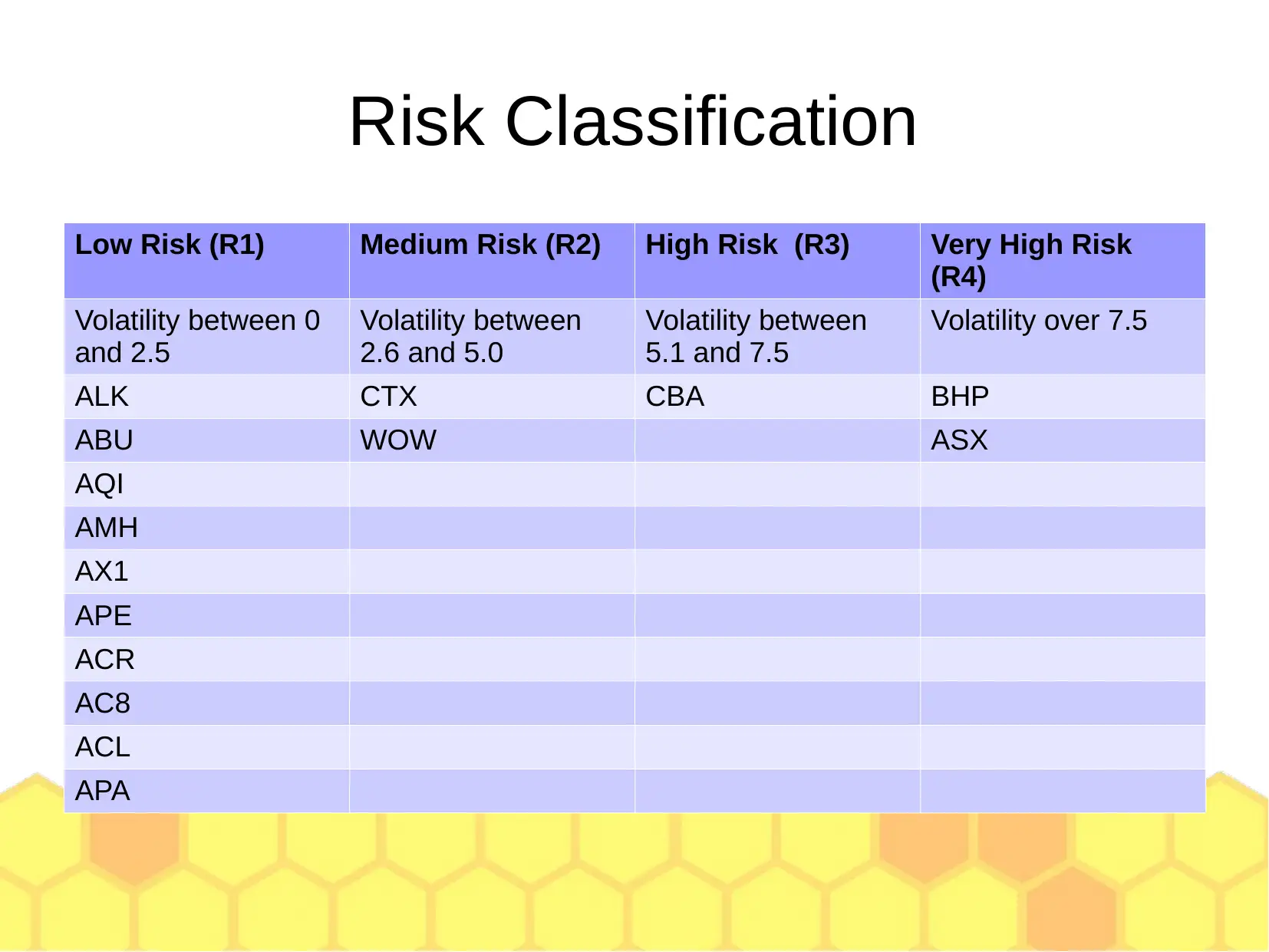

This project evaluates 15 stocks from the ASX (Australian Stock Exchange) using Linear Programming (LP), Integer Linear Programming (ILP), and Non-Linear Programming (NLP) models to optimize an investment portfolio. The securities are chosen based on asset class restrictions, individual risk appetites, portfolio size constraints, and required returns. Stocks are classified into industries like Mining and Energy, Materials, Financial Sector, Retail, and Pharmaceuticals, Biotechnology, and Life Sciences, and further categorized by risk levels determined by historical performance data and volatility. The investment goal is to balance risk and returns, with a portfolio comprising 50% low-risk and 50% high-risk assets. The LP model maximizes returns subject to constraints on investment amounts in each risk class, while the ILP model requires a minimum number of stocks from the least and most risky categories. The NLP model uses a variance/covariance matrix to optimize the portfolio. The project concludes with a discussion on the advantages and challenges of each method, favoring the linear model for its ease of use in obtaining the optimum solution.

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.