Management Accounting Report: LVS Small Plastic Parts Analysis

VerifiedAdded on 2021/02/21

|14

|2831

|30

Report

AI Summary

This report delves into the realm of management accounting, focusing on its significance in the business world and its practical applications within LVS Small Plastic Parts Ltd. It begins by defining management accounting and its role in aiding crucial business decisions. The report then explores various management accounting systems, including inventory management, cost accounting, price optimization, and job costing systems. Different methodologies like cost accounting reports, performance reports, budget reports, and inventory management reports are discussed. Furthermore, it provides an in-depth analysis of costing techniques, such as marginal costing and absorption costing, to prepare income statements. The report also covers material cost variances and the advantages and disadvantages of different planning tools. Overall, the report emphasizes how management accounting systems respond to financial problems, offering a comprehensive overview of the subject.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

P1. Management accounting systems.....................................................................................3

P2 Different methodologies used in management accounting reporting;...............................5

TASK 2......................................................................................................................................6

P3 Appropriate costing techniques to prepare income statement...........................................6

TASK 3....................................................................................................................................10

P4 Advantage and disadvantage of different types of planning tools..................................10

TASK 4....................................................................................................................................12

P5. Management accounting systems to respond to financial problems:.............................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

P1. Management accounting systems.....................................................................................3

P2 Different methodologies used in management accounting reporting;...............................5

TASK 2......................................................................................................................................6

P3 Appropriate costing techniques to prepare income statement...........................................6

TASK 3....................................................................................................................................10

P4 Advantage and disadvantage of different types of planning tools..................................10

TASK 4....................................................................................................................................12

P5. Management accounting systems to respond to financial problems:.............................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION

In business world the concept of management accounting is defined as the systematic

approach that collect, analyse, report crucial business operations so that essential decision are

made by management in order to grow entire performance and profitability of business

(Abdelmoneim Mohamed and Jones, 2014). To better recognise the importance of

management accounting LVS Small Plastic Parts Ltd is selected which is a client company of

Aon Consulting. Company use to manufacture plastic product that are further used in

producing essential goods.

The reports cover importance of management accounting, different types of report and

system that are helpful in dealing with various financial problems. In this report several

costing techniques are used to calculate net profit for the year. In Addition, advantages and

disadvantages of planning tool and benefits of management accounting in dealing with

various financial problems are defined in detail.

TASK 1

P1. Management accounting systems.

Management accounting systems are the methods used to process, collect, gather,

analyse, report and evaluate meaningful business information in order to make effective

decisions regarding the use of the funds of any organization. Each kind of financial and non-

financial information is presented in a way that help managers to estimate budgets, plans

accordingly with the business objectives, and also permit them to be focused on the analysis

of business activities in order to fulfil those objectives. There are different kinds of effective

management accounting systems that support the decision making process and improve

overall the productivity of company and also provide essential guidelines so that entire

strategy can be helpful to attain the desired objective. Some of these in the context of LVS

Small Plastic Parts Ltd are discussed below:

Inventory management system: One of the most crucial system for manufacture

company as it help to maintain a valid record of inventory company holds during a specific

period. This system aids manager of company to forecast stock, materials tracking, automatic

reordering etc. It is recycled for defining goods accessible through whole supply series along

with business processes events (Bloomfield, 2015). In respective company manager use this

system to keep a valid record of entire inventory available during a period. This helps them to

In business world the concept of management accounting is defined as the systematic

approach that collect, analyse, report crucial business operations so that essential decision are

made by management in order to grow entire performance and profitability of business

(Abdelmoneim Mohamed and Jones, 2014). To better recognise the importance of

management accounting LVS Small Plastic Parts Ltd is selected which is a client company of

Aon Consulting. Company use to manufacture plastic product that are further used in

producing essential goods.

The reports cover importance of management accounting, different types of report and

system that are helpful in dealing with various financial problems. In this report several

costing techniques are used to calculate net profit for the year. In Addition, advantages and

disadvantages of planning tool and benefits of management accounting in dealing with

various financial problems are defined in detail.

TASK 1

P1. Management accounting systems.

Management accounting systems are the methods used to process, collect, gather,

analyse, report and evaluate meaningful business information in order to make effective

decisions regarding the use of the funds of any organization. Each kind of financial and non-

financial information is presented in a way that help managers to estimate budgets, plans

accordingly with the business objectives, and also permit them to be focused on the analysis

of business activities in order to fulfil those objectives. There are different kinds of effective

management accounting systems that support the decision making process and improve

overall the productivity of company and also provide essential guidelines so that entire

strategy can be helpful to attain the desired objective. Some of these in the context of LVS

Small Plastic Parts Ltd are discussed below:

Inventory management system: One of the most crucial system for manufacture

company as it help to maintain a valid record of inventory company holds during a specific

period. This system aids manager of company to forecast stock, materials tracking, automatic

reordering etc. It is recycled for defining goods accessible through whole supply series along

with business processes events (Bloomfield, 2015). In respective company manager use this

system to keep a valid record of entire inventory available during a period. This helps them to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

produce goods accordingly and make order for raw material in case of shortage of good. This

system also benefits them supporting required inventory, real time movement and various

kinds of inventories essential in achievement of customer demands. Furthermore, this system

also assess the management to keep a close control on raw material so that they can be

effectively utilise to increase manufacturing. It also help to record the waste generated while

producing useful product and make startegies to control excess wastage.

Cost accounting system: In large or small companies it is essential to maintain an

authentic record of overall cost included in maintaining inventory, cost utilised in production

process etc. thus cost accounting system is very much essential. Approximation of definite

cost is very essential for any industry as it support to calculate overall profitability of

business. It includes events founded on accepting, recording, examining, grouping and

summarizing costs related with valuable goods and services. In LVS Small plastic Part Ltd

cost accounting system is useful to calculate the total; cost included in running different

production operation, cost incurred of workforce and other miscellaneous cost. This further

useful to calculate and measure the entire profitability of business and in case of any miss-

happening improvement are made to attain desired results.

Price Optimisation system: It is also consider an important system, used by

companies that help to analyse the perception of customer in respect to price of different

goods offered by company. With the support of price optimisation system manager are bale

to calculate the best possible price of their goods that will attract large number of customer

and support them, top maintain desired profit. In LVS Small plastic Part Ltd to increase the

sales figure manager first use this system to analyse the entire cost utilised on producing a

specific product so that they are able to fix the best price of product. Suitable price help

company to attract more number of customer which directly increase the profit of company

and make enough funds to reach the desired target (Bagautdinova, Kundakchyan and

Malakhov, 2013).

Job costing system: This system is used for accumulation of information related to

cost associated with particular job or service. In LVS Small Plastic Part Ltd this system is

beneficial to determine the expenses related with particular job involved in production

process and other department. Job costing system is set of resources used to measure, control,

and make decisions about the specific investment or amount of funds needed to accomplish a

specific activity which can be very more or less complex.

system also benefits them supporting required inventory, real time movement and various

kinds of inventories essential in achievement of customer demands. Furthermore, this system

also assess the management to keep a close control on raw material so that they can be

effectively utilise to increase manufacturing. It also help to record the waste generated while

producing useful product and make startegies to control excess wastage.

Cost accounting system: In large or small companies it is essential to maintain an

authentic record of overall cost included in maintaining inventory, cost utilised in production

process etc. thus cost accounting system is very much essential. Approximation of definite

cost is very essential for any industry as it support to calculate overall profitability of

business. It includes events founded on accepting, recording, examining, grouping and

summarizing costs related with valuable goods and services. In LVS Small plastic Part Ltd

cost accounting system is useful to calculate the total; cost included in running different

production operation, cost incurred of workforce and other miscellaneous cost. This further

useful to calculate and measure the entire profitability of business and in case of any miss-

happening improvement are made to attain desired results.

Price Optimisation system: It is also consider an important system, used by

companies that help to analyse the perception of customer in respect to price of different

goods offered by company. With the support of price optimisation system manager are bale

to calculate the best possible price of their goods that will attract large number of customer

and support them, top maintain desired profit. In LVS Small plastic Part Ltd to increase the

sales figure manager first use this system to analyse the entire cost utilised on producing a

specific product so that they are able to fix the best price of product. Suitable price help

company to attract more number of customer which directly increase the profit of company

and make enough funds to reach the desired target (Bagautdinova, Kundakchyan and

Malakhov, 2013).

Job costing system: This system is used for accumulation of information related to

cost associated with particular job or service. In LVS Small Plastic Part Ltd this system is

beneficial to determine the expenses related with particular job involved in production

process and other department. Job costing system is set of resources used to measure, control,

and make decisions about the specific investment or amount of funds needed to accomplish a

specific activity which can be very more or less complex.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Different methodologies used in management accounting reporting;

Cost accounting report: Companies are not able to maintain desired profit unless

and until they have an accurate record of total cost involved in entire financial and non-

financial operation. Cost accounting system is a method this related with gathering,

examining, grouping and posting important cost related traction into accounts so that compete

cost can be calculated. In LVS Small Plastic Part Ltd this report maintain a detail record of

total cost company use on producing plastic goods, cost related with depreciation, rent, wages

etc. so that actual earning can be calculated and future cost reduction decision are made.

Performance Report: It is very crucial to analyse and evaluate the performance of

different operation, business dealing and worker as it support to make possible changes in

order to increase entire performance of company in upcoming year. Performance report are

mainly maintained by every kind of organisation in order to fix few measurements which

further support to accomplish objectives and compare the victory of consequences in relation

to the capacities (Bargate, 2012). In respective firm this report is used to evaluate and

measure the total performance of every project and performance of employee. This supports

them to increase the efficiency and capability of company by making suitable changes for

better results. This technique helps in supervisory the price and handling the staff.

Budget Report: Budget are effective techniques that help companies to execute the

business operation in desired manner so that budgeted target are meet and profit margin are

attained. Manager use this report to make proper estimate of total expenses that are related

with different operations and total income that can be generated so that profitability can be

maintained. Basically manager of LVS Small Plastic Parts Ltd this report use to include every

variances and reasons of variances among budgeted outcomes and authentic results related

with different operation company during a year. This process benefits the association in

figuring out the mistakes in budget, balances in budget and adjusts the cost and adverse

alterations. It also supports the manager to make sure that each resource are utilise in definite

manner that gives favourable results.

Inventory Management Report: This report is very much crucial for company as it

aid to maintain the total inventory hold during a year. Inventory management report covers

essential detail of total raw material available in warehouses, goods in transit and finished

products ready for sales. Therefore, managers are required to maintain an authentic record of

goods as they are the main source of income for company. In this context of client company

Cost accounting report: Companies are not able to maintain desired profit unless

and until they have an accurate record of total cost involved in entire financial and non-

financial operation. Cost accounting system is a method this related with gathering,

examining, grouping and posting important cost related traction into accounts so that compete

cost can be calculated. In LVS Small Plastic Part Ltd this report maintain a detail record of

total cost company use on producing plastic goods, cost related with depreciation, rent, wages

etc. so that actual earning can be calculated and future cost reduction decision are made.

Performance Report: It is very crucial to analyse and evaluate the performance of

different operation, business dealing and worker as it support to make possible changes in

order to increase entire performance of company in upcoming year. Performance report are

mainly maintained by every kind of organisation in order to fix few measurements which

further support to accomplish objectives and compare the victory of consequences in relation

to the capacities (Bargate, 2012). In respective firm this report is used to evaluate and

measure the total performance of every project and performance of employee. This supports

them to increase the efficiency and capability of company by making suitable changes for

better results. This technique helps in supervisory the price and handling the staff.

Budget Report: Budget are effective techniques that help companies to execute the

business operation in desired manner so that budgeted target are meet and profit margin are

attained. Manager use this report to make proper estimate of total expenses that are related

with different operations and total income that can be generated so that profitability can be

maintained. Basically manager of LVS Small Plastic Parts Ltd this report use to include every

variances and reasons of variances among budgeted outcomes and authentic results related

with different operation company during a year. This process benefits the association in

figuring out the mistakes in budget, balances in budget and adjusts the cost and adverse

alterations. It also supports the manager to make sure that each resource are utilise in definite

manner that gives favourable results.

Inventory Management Report: This report is very much crucial for company as it

aid to maintain the total inventory hold during a year. Inventory management report covers

essential detail of total raw material available in warehouses, goods in transit and finished

products ready for sales. Therefore, managers are required to maintain an authentic record of

goods as they are the main source of income for company. In this context of client company

manager are required to maintain a valid record of total raw material present in storehouse

that is ready to be use in producing valuable product, total goods that are already in transit

and actual manufacture goods which are ready for sales that use to generate income and

increase profit margin. Thus the actual greatest way to keep the stock aid to path the

accessibility of the goods, reduce the cost of storing goods and take advantage of the

profitability, mechanize the addition between the various departments and attain a high

cheerful customer base.

TASK 2

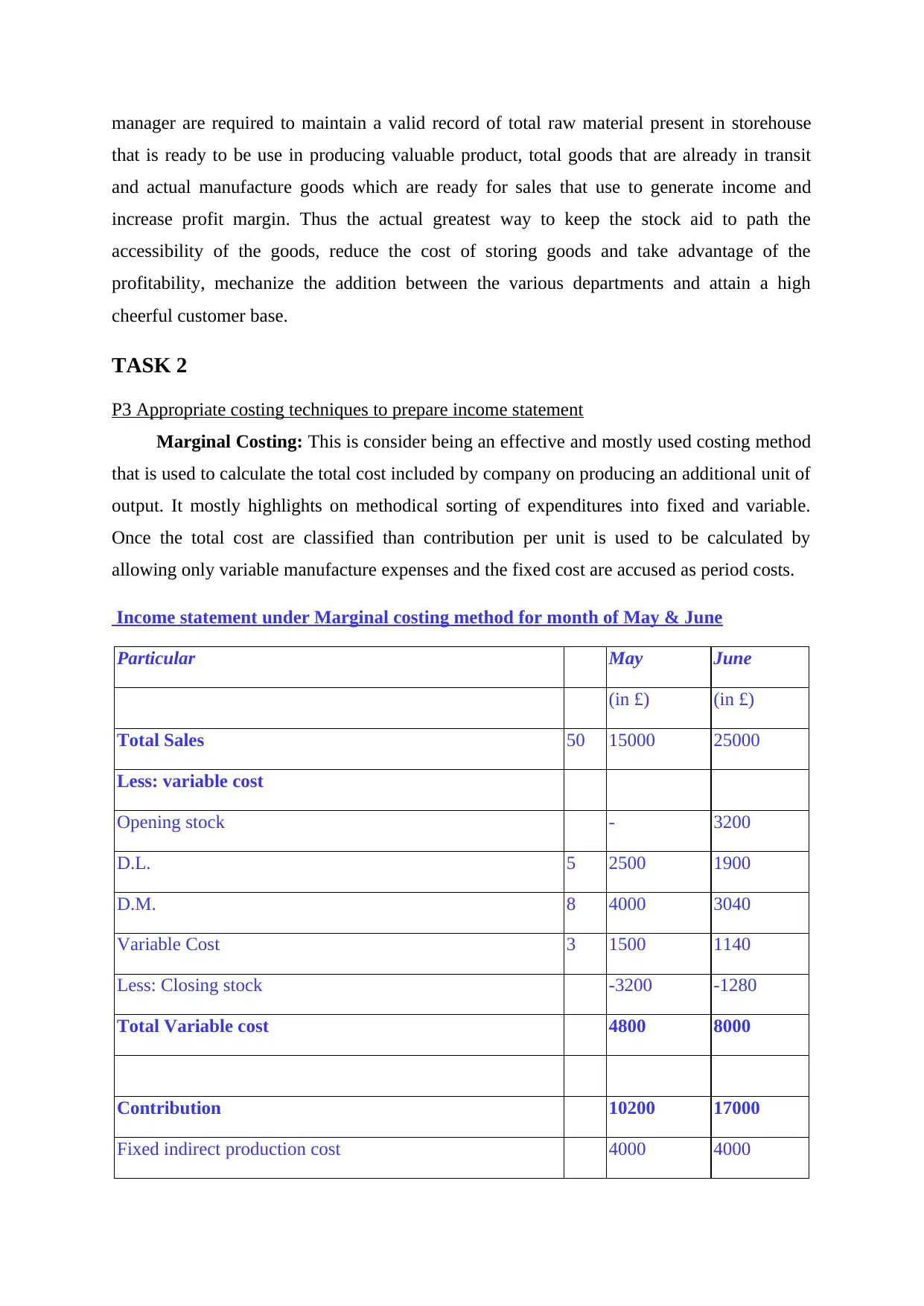

P3 Appropriate costing techniques to prepare income statement

Marginal Costing: This is consider being an effective and mostly used costing method

that is used to calculate the total cost included by company on producing an additional unit of

output. It mostly highlights on methodical sorting of expenditures into fixed and variable.

Once the total cost are classified than contribution per unit is used to be calculated by

allowing only variable manufacture expenses and the fixed cost are accused as period costs.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

that is ready to be use in producing valuable product, total goods that are already in transit

and actual manufacture goods which are ready for sales that use to generate income and

increase profit margin. Thus the actual greatest way to keep the stock aid to path the

accessibility of the goods, reduce the cost of storing goods and take advantage of the

profitability, mechanize the addition between the various departments and attain a high

cheerful customer base.

TASK 2

P3 Appropriate costing techniques to prepare income statement

Marginal Costing: This is consider being an effective and mostly used costing method

that is used to calculate the total cost included by company on producing an additional unit of

output. It mostly highlights on methodical sorting of expenditures into fixed and variable.

Once the total cost are classified than contribution per unit is used to be calculated by

allowing only variable manufacture expenses and the fixed cost are accused as period costs.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

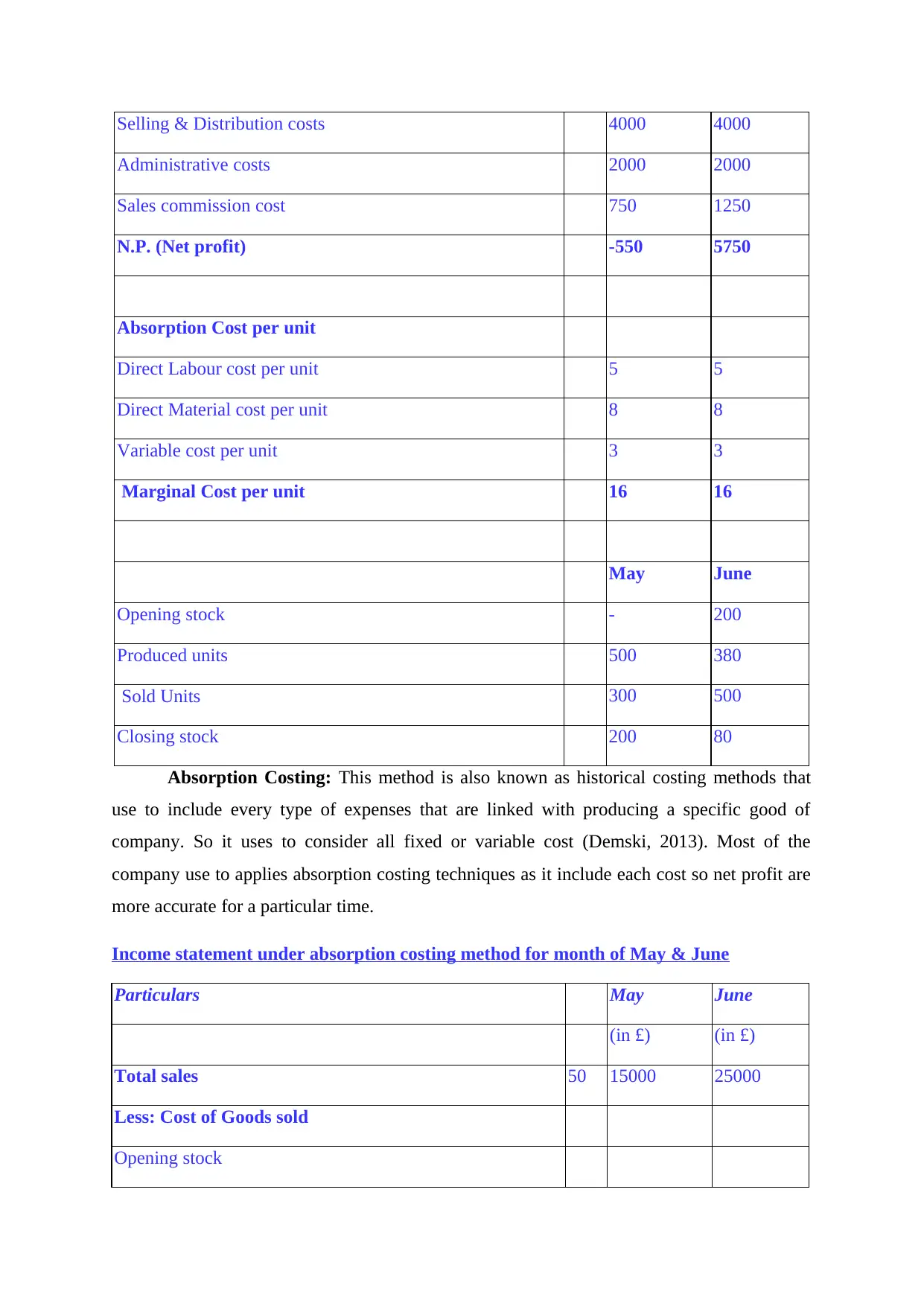

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Absorption Costing: This method is also known as historical costing methods that

use to include every type of expenses that are linked with producing a specific good of

company. So it uses to consider all fixed or variable cost (Demski, 2013). Most of the

company use to applies absorption costing techniques as it include each cost so net profit are

more accurate for a particular time.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Absorption Costing: This method is also known as historical costing methods that

use to include every type of expenses that are linked with producing a specific good of

company. So it uses to consider all fixed or variable cost (Demski, 2013). Most of the

company use to applies absorption costing techniques as it include each cost so net profit are

more accurate for a particular time.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

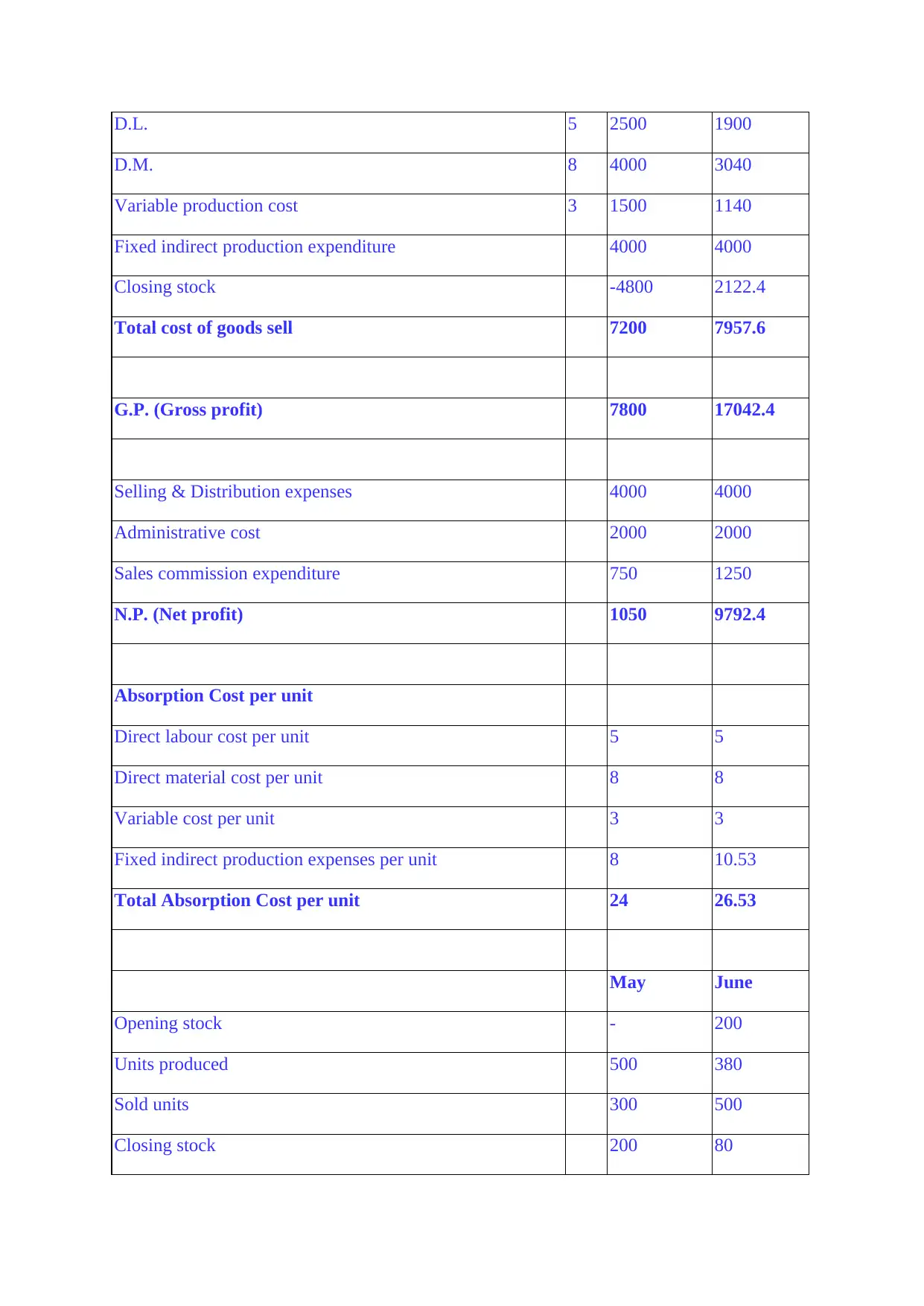

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

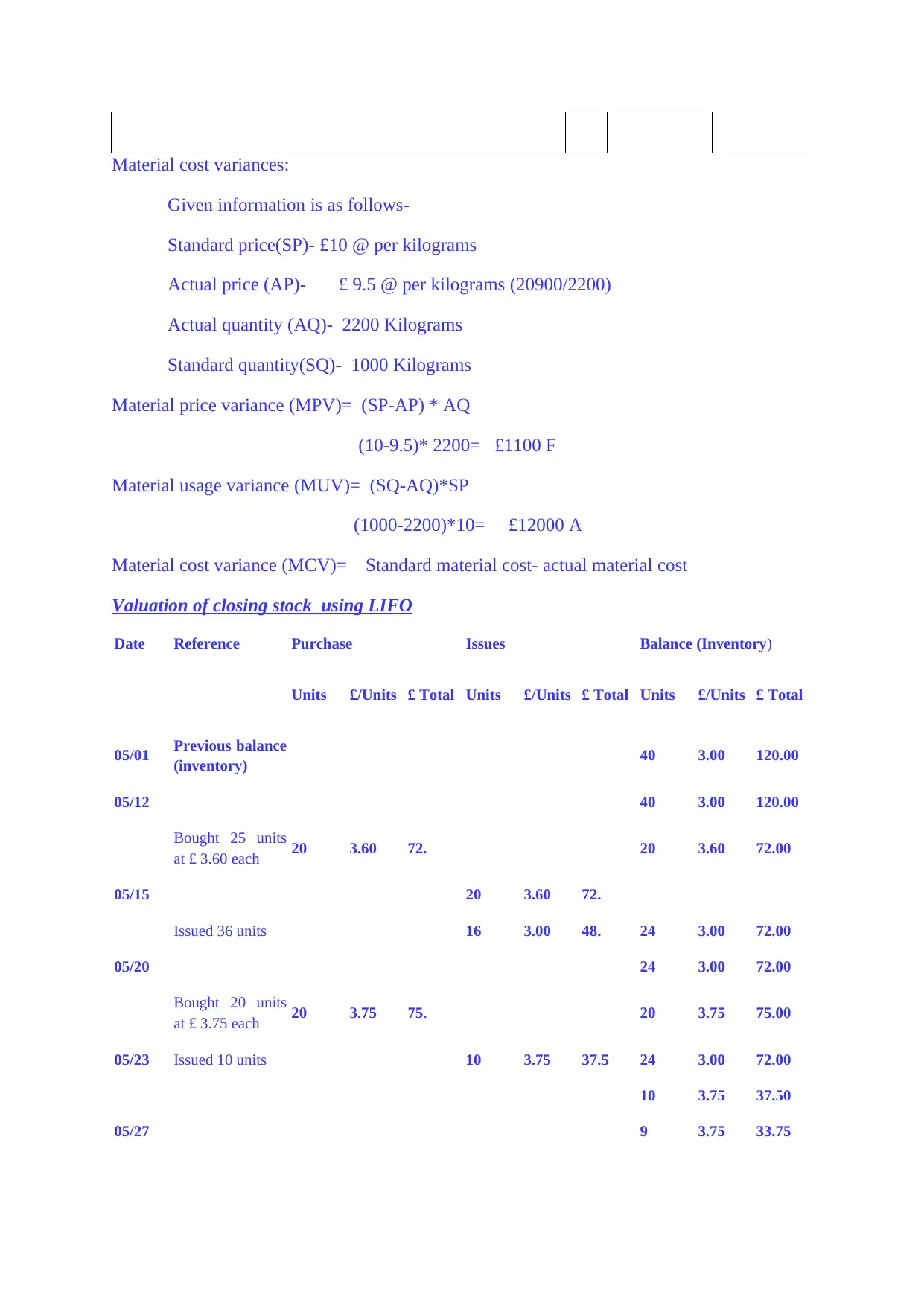

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

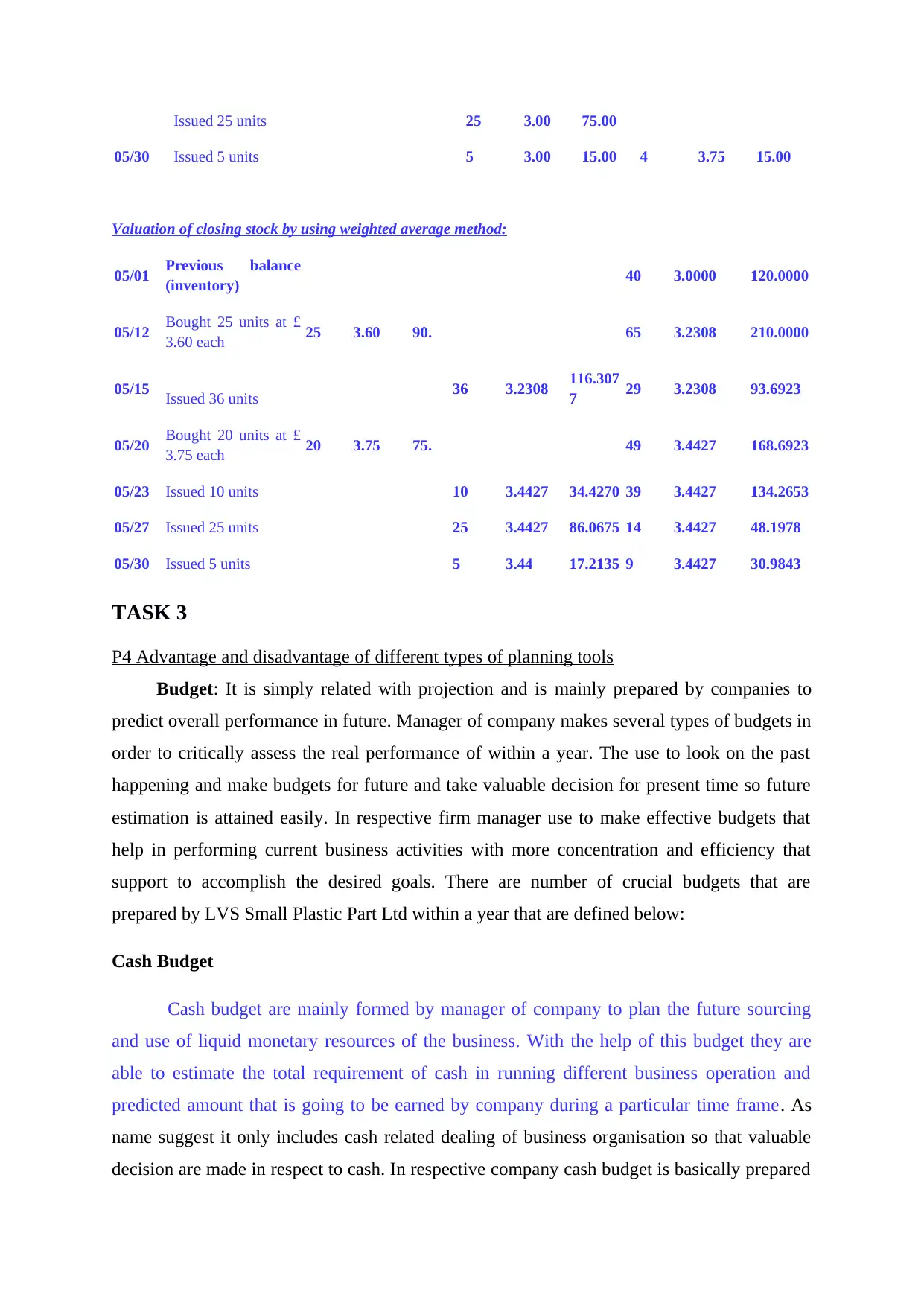

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

TASK 3

P4 Advantage and disadvantage of different types of planning tools

Budget: It is simply related with projection and is mainly prepared by companies to

predict overall performance in future. Manager of company makes several types of budgets in

order to critically assess the real performance of within a year. The use to look on the past

happening and make budgets for future and take valuable decision for present time so future

estimation is attained easily. In respective firm manager use to make effective budgets that

help in performing current business activities with more concentration and efficiency that

support to accomplish the desired goals. There are number of crucial budgets that are

prepared by LVS Small Plastic Part Ltd within a year that are defined below:

Cash Budget

Cash budget are mainly formed by manager of company to plan the future sourcing

and use of liquid monetary resources of the business. With the help of this budget they are

able to estimate the total requirement of cash in running different business operation and

predicted amount that is going to be earned by company during a particular time frame. As

name suggest it only includes cash related dealing of business organisation so that valuable

decision are made in respect to cash. In respective company cash budget is basically prepared

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

TASK 3

P4 Advantage and disadvantage of different types of planning tools

Budget: It is simply related with projection and is mainly prepared by companies to

predict overall performance in future. Manager of company makes several types of budgets in

order to critically assess the real performance of within a year. The use to look on the past

happening and make budgets for future and take valuable decision for present time so future

estimation is attained easily. In respective firm manager use to make effective budgets that

help in performing current business activities with more concentration and efficiency that

support to accomplish the desired goals. There are number of crucial budgets that are

prepared by LVS Small Plastic Part Ltd within a year that are defined below:

Cash Budget

Cash budget are mainly formed by manager of company to plan the future sourcing

and use of liquid monetary resources of the business. With the help of this budget they are

able to estimate the total requirement of cash in running different business operation and

predicted amount that is going to be earned by company during a particular time frame. As

name suggest it only includes cash related dealing of business organisation so that valuable

decision are made in respect to cash. In respective company cash budget is basically prepared

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to classify and recover the weak areas of business due to which there is huge and negative

cash flow. In company cash budget is set department-wise and there are various advantages

and disadvantages that are defined below:

Advantage:

It benefits company to track the movement of overall cash arrivals and discharges that

maintain effective cash management.

It supports company as cash budget accumulates funds for upcoming possibility so

that operation can be managed and controlled well and it also helps to prevent any

lack of liquidity.

Disadvantage:

This budget uses approaches that are many time manipulative and do not relates with

the cash transaction of company.

Operating Budget

These type of budgets are set by companies that are related with total income and

expenses related with operation during a specific year and if company are able to maintain

profitability then they may continue using this budget. Operation budgets covers

approximation of revenue and expenditures apprehensive with operating functions of with

company (Malinić and Todorović, 2012). This budgets are most useful for manufacture

company has the manager use this budget to calculate the total expenses incurred on

production activities and actual income received by company through these operation. Some

advantages and disadvantages are discussed below:

Advantage

Managers in LVS Small Plastic Part Ltd use this budget to organise and control day to

day operations and measure total income.

It also assists company in improving and weak area of operation so that it provides a

foundation for overcoming from such weakness.

Disadvantage

This budget is set usually on everyday basis so it require specific team to look which

increase liability of company (McLaren, Appleyard and Mitchell, 2016).

cash flow. In company cash budget is set department-wise and there are various advantages

and disadvantages that are defined below:

Advantage:

It benefits company to track the movement of overall cash arrivals and discharges that

maintain effective cash management.

It supports company as cash budget accumulates funds for upcoming possibility so

that operation can be managed and controlled well and it also helps to prevent any

lack of liquidity.

Disadvantage:

This budget uses approaches that are many time manipulative and do not relates with

the cash transaction of company.

Operating Budget

These type of budgets are set by companies that are related with total income and

expenses related with operation during a specific year and if company are able to maintain

profitability then they may continue using this budget. Operation budgets covers

approximation of revenue and expenditures apprehensive with operating functions of with

company (Malinić and Todorović, 2012). This budgets are most useful for manufacture

company has the manager use this budget to calculate the total expenses incurred on

production activities and actual income received by company through these operation. Some

advantages and disadvantages are discussed below:

Advantage

Managers in LVS Small Plastic Part Ltd use this budget to organise and control day to

day operations and measure total income.

It also assists company in improving and weak area of operation so that it provides a

foundation for overcoming from such weakness.

Disadvantage

This budget is set usually on everyday basis so it require specific team to look which

increase liability of company (McLaren, Appleyard and Mitchell, 2016).

Master Budget

It is most applicable and widely used budget by companies as it includes all other

budgets. A master budget is mainly used by respective firm for assessment of mutual and

entire performance by seeing all financial and accounting aspects of business. This budget is

use to take crucial decision related with manufacturing and other activities. Some advantages

and disadvantages are discussed below:

Advantage

It is used to classify any possible monetary occasion that may make danger for

company in upcoming time.

Master budget also aid respective company to make effective co-ordination among

various product sections so important decision are made.

Disadvantage

Master budgets are depended on specific assumption that might not be accurate in

different situation of business.

TASK 4

P5. Management accounting systems to respond to financial problems:

Financial problems are faced by companies at different phases of entire business

activities so they are required to make proper planning in order to recuse the impact of these

problems. There are various financial problem that are faced by LVS Small Plastic Part Ltd

are related with Lack of liquid funds and special order. Thus it reduces the overall

performance and profitability of company.

In order to determine and overcome these problem different management accounting

tool are used by company that are discussed below:

Benchmarking: In respective company this tool is used to measure and compare the

performance with other companies dealing within same industry or companies that are

operating in different operations. With the help of this tool manager are able to determine the

problem of Special order.

Key financial indicators: This is related with positive measures that assist firm to

assign financial areas and resolve financial problems. It is related with analyse and evaluating

It is most applicable and widely used budget by companies as it includes all other

budgets. A master budget is mainly used by respective firm for assessment of mutual and

entire performance by seeing all financial and accounting aspects of business. This budget is

use to take crucial decision related with manufacturing and other activities. Some advantages

and disadvantages are discussed below:

Advantage

It is used to classify any possible monetary occasion that may make danger for

company in upcoming time.

Master budget also aid respective company to make effective co-ordination among

various product sections so important decision are made.

Disadvantage

Master budgets are depended on specific assumption that might not be accurate in

different situation of business.

TASK 4

P5. Management accounting systems to respond to financial problems:

Financial problems are faced by companies at different phases of entire business

activities so they are required to make proper planning in order to recuse the impact of these

problems. There are various financial problem that are faced by LVS Small Plastic Part Ltd

are related with Lack of liquid funds and special order. Thus it reduces the overall

performance and profitability of company.

In order to determine and overcome these problem different management accounting

tool are used by company that are discussed below:

Benchmarking: In respective company this tool is used to measure and compare the

performance with other companies dealing within same industry or companies that are

operating in different operations. With the help of this tool manager are able to determine the

problem of Special order.

Key financial indicators: This is related with positive measures that assist firm to

assign financial areas and resolve financial problems. It is related with analyse and evaluating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.