M92 Insurance Business and Finance Coursework Assignment Solution

VerifiedAdded on 2023/01/13

|20

|3840

|23

Homework Assignment

AI Summary

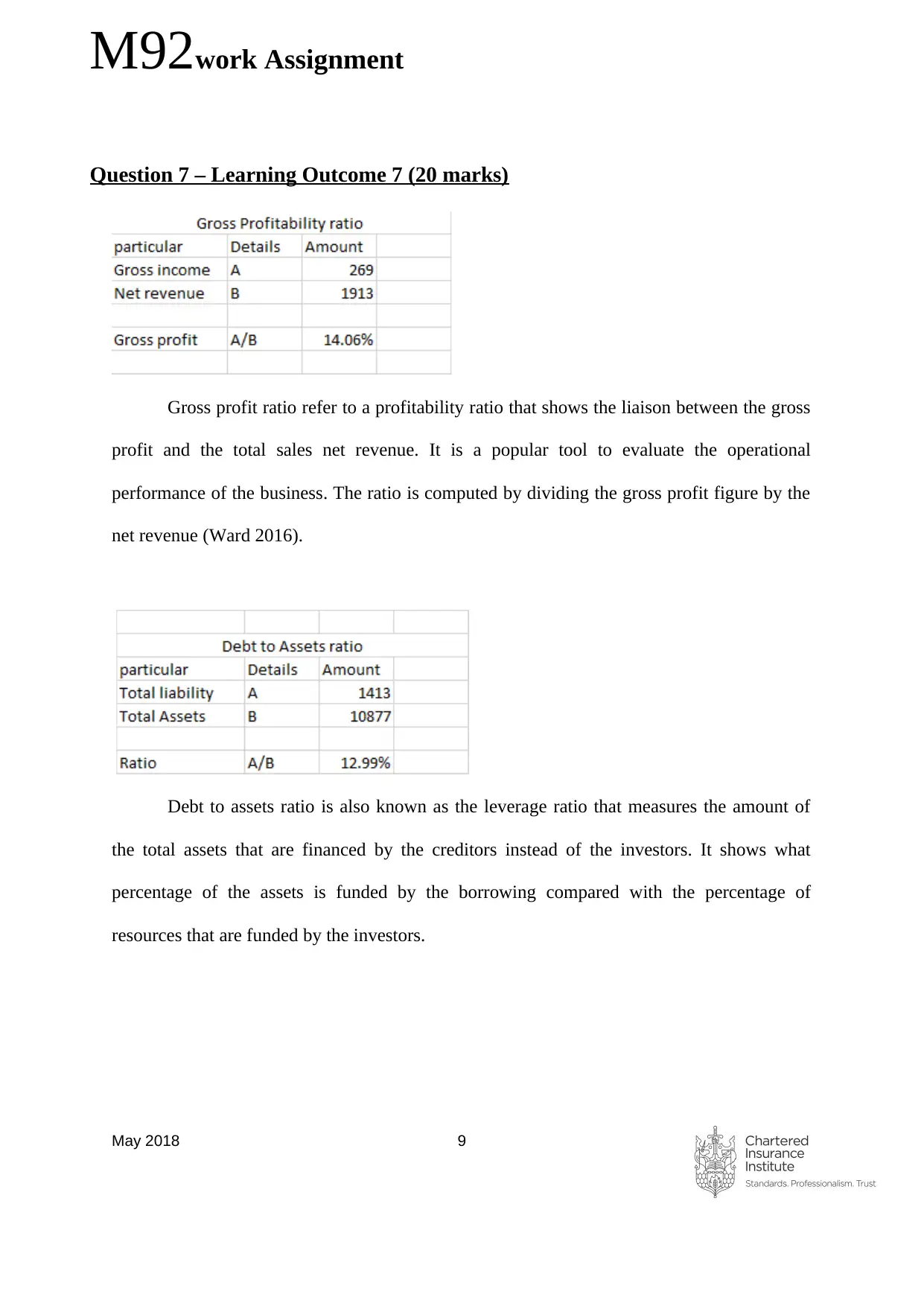

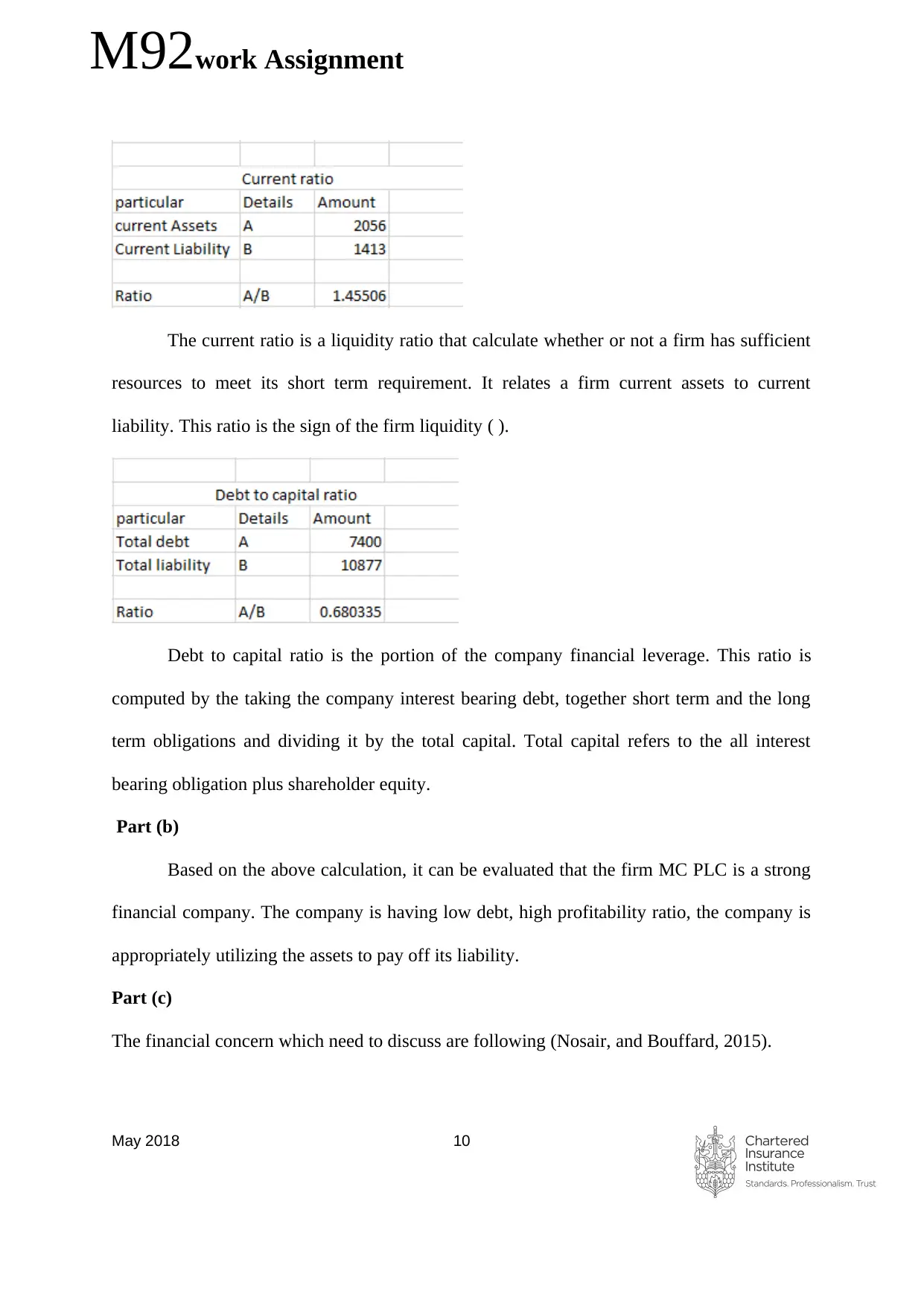

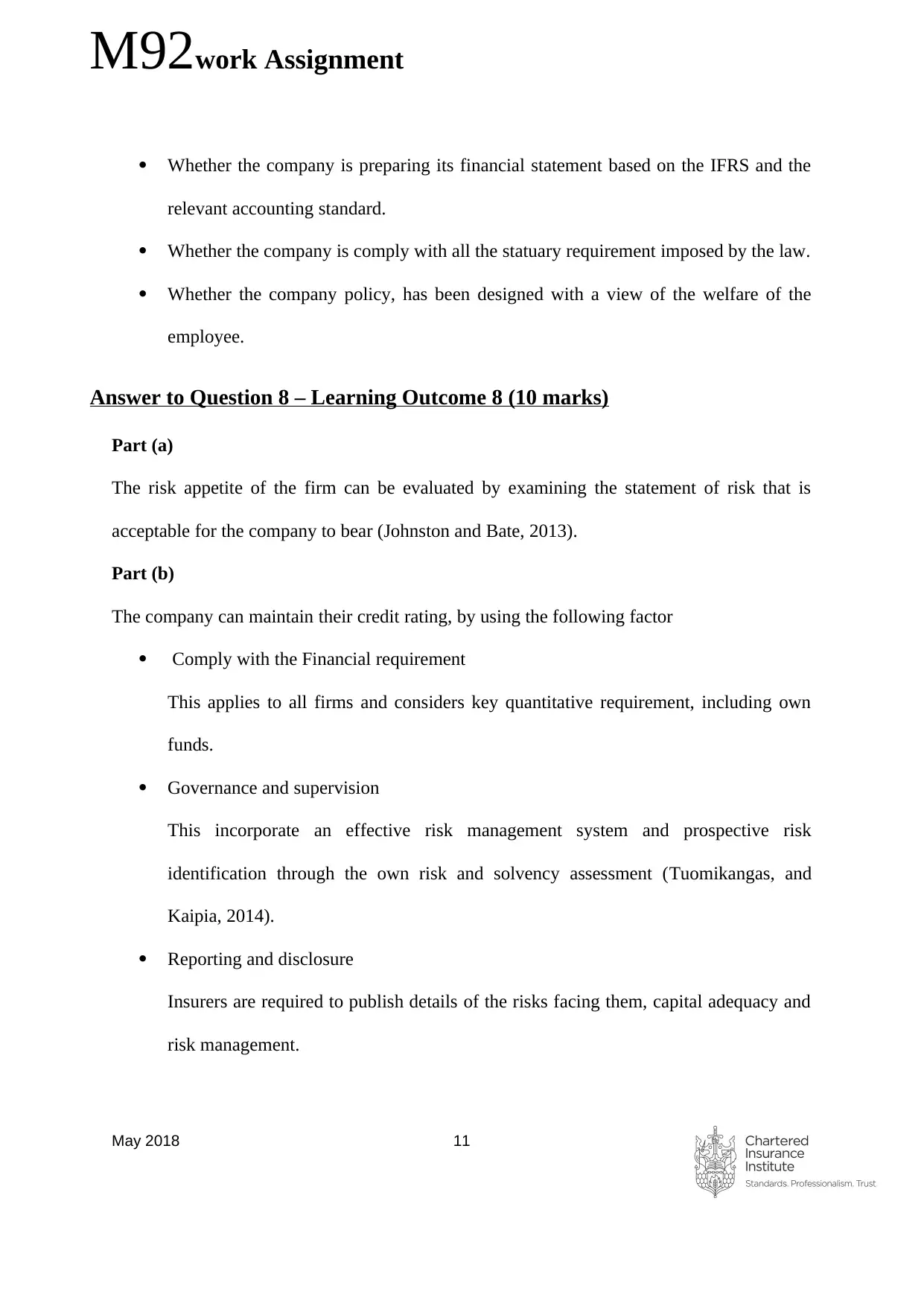

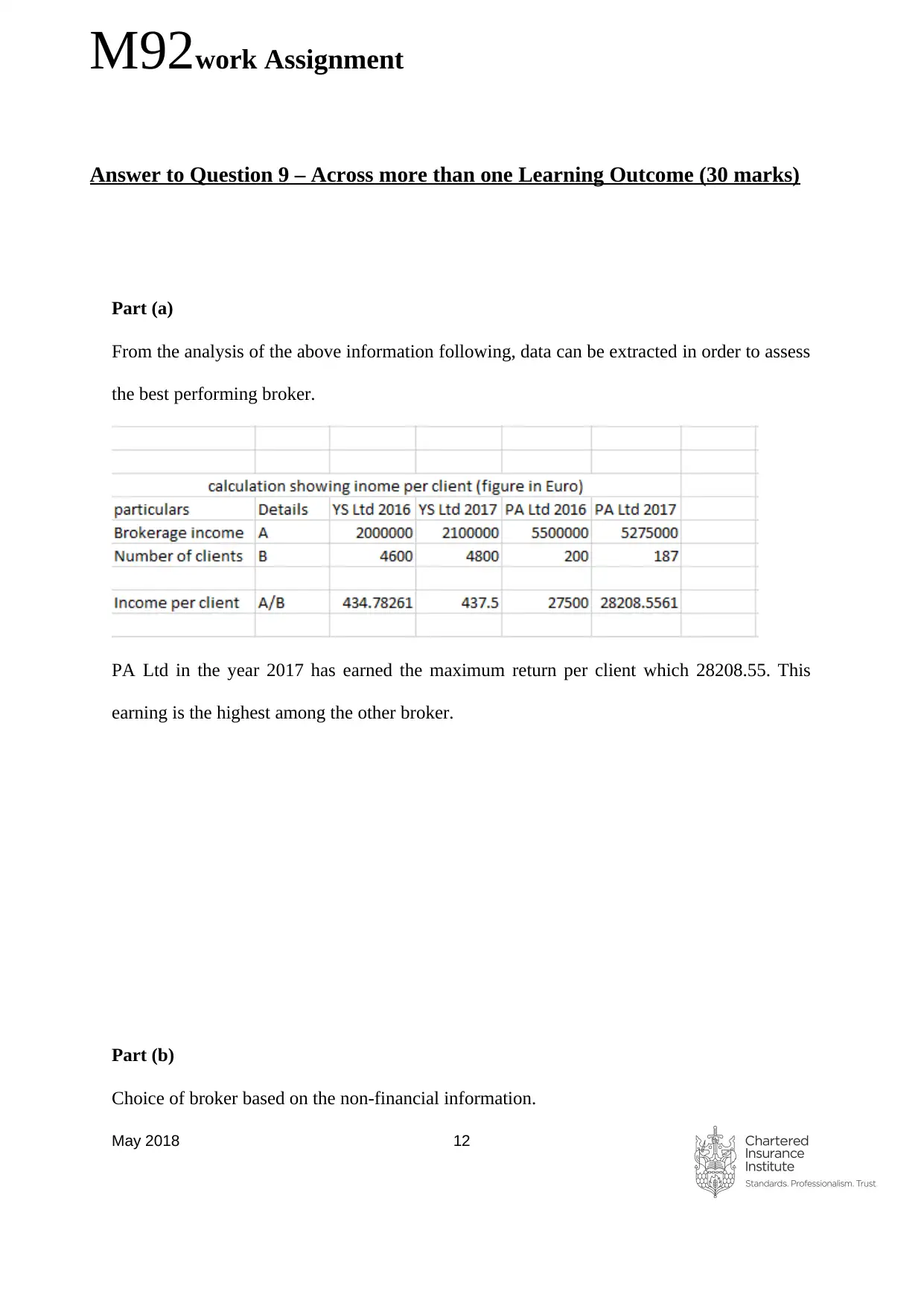

This document presents a comprehensive solution to a coursework assignment for the M92 Insurance Business and Finance module. It addresses various aspects of insurance and finance, starting with outsourcing challenges faced by WSP PLC, including data confidentiality and service improvement strategies. The assignment then delves into corporate governance issues at ORI PLC, exploring challenges in management style and the implementation of organizational changes. It further examines corporate governance requirements for RKU Ltd. before listing on the LSE, and the actions needed to meet these requirements. The solution also analyzes the impact of issues in MGA on PFO PLC, focusing on affected functions and delegated responsibility terms. It includes an evaluation of existing and prospective classes of business, identifying profitability risks and discussing the risks of comparing business classes. Furthermore, the assignment addresses accounting requirements, including true and fair view, and the resolution of potential conflicts for insurers. Finally, it covers financial analysis using ratios like gross profit ratio and debt-to-assets ratio for MC PLC, offering a comprehensive understanding of insurance business and finance principles.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.