Management Accounting Methods and Income Statement Analysis

VerifiedAdded on 2020/07/22

|19

|5363

|70

Report

AI Summary

This report focuses on management accounting practices within R.L. Maynard Limited, a small construction business. The assignment begins by defining management accounting and exploring its various systems, including cost accounting, inventory management, price optimization, and job costing. It then delves into different reporting methods used by the firm, such as job cost reports, operating budget reports, accounts receivables aging, departmental reports, and inventory management reports. The core of the report involves the preparation of income statements using both marginal and absorption costing methods to analyze the firm's financial performance. The analysis includes the presentation of income statements, providing insights into the company's profitability and cost structure under each costing method. The assignment highlights the importance of these accounting tools in decision-making and financial planning within the construction industry.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

A method through which effective financial plans or schedules are prepared at the

workplace for taking fruitful decisions of business is known as management accounting (MA). It

consists of wide range of methods, techniques and tools which are supportive for each entity. For

the present study, R.L. Maynard Limited firm is taken as base which is a small business

enterprise and operating in construction industry of UK. The reason for selecting this firm is that,

it has less than 50 employees and generates annual turnover less than £500,000 (R.L. MAYNARD

LIMITED, 2016). The present assignment shows various systems along with methods that are

considered for reporting by chosen firm. Further, requirements and needs of such systems and

techniques are also explained in the project. Apart from this, income statements are formulated

with the help of two methods i.e. marginal as well as absorption costing. Besides this, planning

tools which are taken into account for controlling budgetary procedure are described with merits

and limitations. At the end, some systems which are used by R.L. Maynard Ltd for responding

financial obstacles are explained.

TASK 1

P1 Explaining MA and its systems with reference to R.L. Maynard Limited

Business Report

From: Management Accounting Officer

To: General manager

R.L. Maynard Limited

Subject: Different management accounting systems

Introduction

At the internal environment of any business various decisions are required to take in proper and

fruitful direction. So that, it will be able to fulfil its desired objectives related to any branch of

the enterprise. In the present study financial aspect or area isused where several decisions are

needed to make like cost, margin, expenses etc. Moreover, the report describes about some

methods and their key requirements with context to R.L. Maynard Limited. Those systems

which are undertaken by the small enterprise are like cost accounting, job costing, stock

1

A method through which effective financial plans or schedules are prepared at the

workplace for taking fruitful decisions of business is known as management accounting (MA). It

consists of wide range of methods, techniques and tools which are supportive for each entity. For

the present study, R.L. Maynard Limited firm is taken as base which is a small business

enterprise and operating in construction industry of UK. The reason for selecting this firm is that,

it has less than 50 employees and generates annual turnover less than £500,000 (R.L. MAYNARD

LIMITED, 2016). The present assignment shows various systems along with methods that are

considered for reporting by chosen firm. Further, requirements and needs of such systems and

techniques are also explained in the project. Apart from this, income statements are formulated

with the help of two methods i.e. marginal as well as absorption costing. Besides this, planning

tools which are taken into account for controlling budgetary procedure are described with merits

and limitations. At the end, some systems which are used by R.L. Maynard Ltd for responding

financial obstacles are explained.

TASK 1

P1 Explaining MA and its systems with reference to R.L. Maynard Limited

Business Report

From: Management Accounting Officer

To: General manager

R.L. Maynard Limited

Subject: Different management accounting systems

Introduction

At the internal environment of any business various decisions are required to take in proper and

fruitful direction. So that, it will be able to fulfil its desired objectives related to any branch of

the enterprise. In the present study financial aspect or area isused where several decisions are

needed to make like cost, margin, expenses etc. Moreover, the report describes about some

methods and their key requirements with context to R.L. Maynard Limited. Those systems

which are undertaken by the small enterprise are like cost accounting, job costing, stock

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management and price optimisation.

Various systems of MA

Cost accounting system: It is framework where cost of the products are analysed which incurred

to manufacture goods are services is referred as cost accounting. It is one of the highly used

way because it gives details about the expenses after segregating in structured manner. R.L.

Maynard uses this aspect for assess amount which spent to build specific building or house or

any other. Basic need due to which it is undertaken is for analysing position of the profitability,

valuing level of stock etc (Ismail and King, 2014). Further, on the basis of total costs the

management easily able to take pricing decisions which is one of attractive point of customers

towards the enterprise. It covers basically three kinds of the expenses which are like actual,

normal as well as standard.

Inventory management system: An approach where stock levels are tracked using specific

software in the firm and analyse orders, sales as well as deliveries is known as inventory

management. In short, when stock is needed to manage in business of R.L. Maynard with

proper way then this system is considered. It is necessary to reduce this aspect because it leads

to affect efficiency or entity in negative direction. Therefore, stock turnover ratio also decreased

which is sign of declining the business performance in construction industry. Further, to know

value of stock in terms of amount and units then R.L. Maynard incorporates basic three ways

which involve LIFO, FIFO and weighted average.

Price optimisation system: MA includes pricing decisions also which is used to charge amount

of one product from the consumers with higher ratio. As per this system, profitable decision of

pricing of each building or house is taken in beneficial direction (Bruynseels and Cardinaels,

2013). The construction firm i.e. R.L. Maynard changes its prices on specific time where

response of customers also fluctuate up to the greater level. A particular amount at which when

more purchasers of the house are attracted then that will be used as price on permanent basis.

Hence, key requirement of price optimisation system in R.L. Maynard enterprise is to opt a

pricing level in the business to make it profitable. Apart from this, some strategies are also for

making decisions regarding to the pricing which are market penetration, cost, competitor and

market based, cost plus, skimming etc.

2

Various systems of MA

Cost accounting system: It is framework where cost of the products are analysed which incurred

to manufacture goods are services is referred as cost accounting. It is one of the highly used

way because it gives details about the expenses after segregating in structured manner. R.L.

Maynard uses this aspect for assess amount which spent to build specific building or house or

any other. Basic need due to which it is undertaken is for analysing position of the profitability,

valuing level of stock etc (Ismail and King, 2014). Further, on the basis of total costs the

management easily able to take pricing decisions which is one of attractive point of customers

towards the enterprise. It covers basically three kinds of the expenses which are like actual,

normal as well as standard.

Inventory management system: An approach where stock levels are tracked using specific

software in the firm and analyse orders, sales as well as deliveries is known as inventory

management. In short, when stock is needed to manage in business of R.L. Maynard with

proper way then this system is considered. It is necessary to reduce this aspect because it leads

to affect efficiency or entity in negative direction. Therefore, stock turnover ratio also decreased

which is sign of declining the business performance in construction industry. Further, to know

value of stock in terms of amount and units then R.L. Maynard incorporates basic three ways

which involve LIFO, FIFO and weighted average.

Price optimisation system: MA includes pricing decisions also which is used to charge amount

of one product from the consumers with higher ratio. As per this system, profitable decision of

pricing of each building or house is taken in beneficial direction (Bruynseels and Cardinaels,

2013). The construction firm i.e. R.L. Maynard changes its prices on specific time where

response of customers also fluctuate up to the greater level. A particular amount at which when

more purchasers of the house are attracted then that will be used as price on permanent basis.

Hence, key requirement of price optimisation system in R.L. Maynard enterprise is to opt a

pricing level in the business to make it profitable. Apart from this, some strategies are also for

making decisions regarding to the pricing which are market penetration, cost, competitor and

market based, cost plus, skimming etc.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: When an enterprise produces different range of the products and services

and it wants to know cost associated with each batch then job costing is applied. The R.L.

Maynard constructs buildings, houses, offices etc. where it has to determine that each kind of

product takes how much amount of cost. For this, it has to segregate all the expenses associated

with this separately and then can know about expenditures of each item (Tools and techniques

of Management Accounting, 2017). The job costing is a system through which management of

R.L. Maynard can analyse cost of every product which constructed in different batches.

Therefore, it can make effective decisions for charging amount in terms of price of each unit

properly.

Conclusion

It can be summarised that, cost accounting is used for tracking record of costs and analyses total

expenses incurred by the firm. When decisions related to pricing and stock is required to be

taken by R.L. Maynard then price optimisation and inventory management systems are used

respectively. Hence, the systems of MA are highly incorporated by cited firm to make various

judgements.

P2 Several methods of reporting in MA using example of R.L. Maynard Ltd.

Business Report

From: Management Accounting Officer

To: General manager

R.L. Maynard Limited

Subject: Different management accounting reports

Introduction

Reporting is a system in which small reports related to financial transactions are prepared and

then used for formulating financial statements of the firm at the end of an accounting period.

The current report presented to general manager where various methods of management

accounting reporting are discussed. The company R.L. Maynard Limited uses some ways which

3

and it wants to know cost associated with each batch then job costing is applied. The R.L.

Maynard constructs buildings, houses, offices etc. where it has to determine that each kind of

product takes how much amount of cost. For this, it has to segregate all the expenses associated

with this separately and then can know about expenditures of each item (Tools and techniques

of Management Accounting, 2017). The job costing is a system through which management of

R.L. Maynard can analyse cost of every product which constructed in different batches.

Therefore, it can make effective decisions for charging amount in terms of price of each unit

properly.

Conclusion

It can be summarised that, cost accounting is used for tracking record of costs and analyses total

expenses incurred by the firm. When decisions related to pricing and stock is required to be

taken by R.L. Maynard then price optimisation and inventory management systems are used

respectively. Hence, the systems of MA are highly incorporated by cited firm to make various

judgements.

P2 Several methods of reporting in MA using example of R.L. Maynard Ltd.

Business Report

From: Management Accounting Officer

To: General manager

R.L. Maynard Limited

Subject: Different management accounting reports

Introduction

Reporting is a system in which small reports related to financial transactions are prepared and

then used for formulating financial statements of the firm at the end of an accounting period.

The current report presented to general manager where various methods of management

accounting reporting are discussed. The company R.L. Maynard Limited uses some ways which

3

are like job cost, operating budget, departmental, stock management as well as account

receivables, which are explained at here.

Explanation

Job cost report: A method in which data related to cost aspect recorded of each batch or job at

the workplace is considered as job cost report. It helps to know those types of expenses which

are associated to construct building, office, house or any other kind of product. It is one of the

highly used method because of providing clear information about the every cost for each job.

Total amount of this particular is treated in the books of profit as well as loss and deducted from

the revenue generated (Johnson, 2013). If this cost is higher, then affect to the profitability of

R.L. Maynard in adverse direction. However, if job cost is low then able to charge lower pricing

of the houses and buildings. Therefore, sales and profits will give positive response in the

financial statements.

Operating budget report: According to this, incomes as well as outflows are forecasted for the

next fiscal year in the present times. Further, it keeps record of only operation department

where expenses and incomes related to operation are analysed. Amount which is incurred to

construct building only like materials, labour, purchase of instruments etc. in R.L. Maynard is

recorded under this for upcoming period. Once this report is completed or prepared then treated

in P&L account as operating expenses. Therefore, operating profit at the end of year is analysed

by the cited firm of construction sector.

Accounts receivables ageing: A firm when selling products and services in the market then

usually go through two types which are like cash as well as credit. The method of reporting in

which sales of the R.L. Maynard recorded which are done on credit is known as accounts

receivables ageing. As name it can be clearly identified that amount which will be received by

cited firm in the future is recorded in this (Burns, 2014). In short, credit sales and revenue are

transacted in this mentioned report and shows the amount will be generated in upcoming period.

When this report is completed at the year ending then total amount treated in the statement of

financial position. In the B/S it is recorded as debtors who purchased buildings from R.L.

Maynard on credit.

Departmental report: In the business of every firm, various departments work there for

4

receivables, which are explained at here.

Explanation

Job cost report: A method in which data related to cost aspect recorded of each batch or job at

the workplace is considered as job cost report. It helps to know those types of expenses which

are associated to construct building, office, house or any other kind of product. It is one of the

highly used method because of providing clear information about the every cost for each job.

Total amount of this particular is treated in the books of profit as well as loss and deducted from

the revenue generated (Johnson, 2013). If this cost is higher, then affect to the profitability of

R.L. Maynard in adverse direction. However, if job cost is low then able to charge lower pricing

of the houses and buildings. Therefore, sales and profits will give positive response in the

financial statements.

Operating budget report: According to this, incomes as well as outflows are forecasted for the

next fiscal year in the present times. Further, it keeps record of only operation department

where expenses and incomes related to operation are analysed. Amount which is incurred to

construct building only like materials, labour, purchase of instruments etc. in R.L. Maynard is

recorded under this for upcoming period. Once this report is completed or prepared then treated

in P&L account as operating expenses. Therefore, operating profit at the end of year is analysed

by the cited firm of construction sector.

Accounts receivables ageing: A firm when selling products and services in the market then

usually go through two types which are like cash as well as credit. The method of reporting in

which sales of the R.L. Maynard recorded which are done on credit is known as accounts

receivables ageing. As name it can be clearly identified that amount which will be received by

cited firm in the future is recorded in this (Burns, 2014). In short, credit sales and revenue are

transacted in this mentioned report and shows the amount will be generated in upcoming period.

When this report is completed at the year ending then total amount treated in the statement of

financial position. In the B/S it is recorded as debtors who purchased buildings from R.L.

Maynard on credit.

Departmental report: In the business of every firm, various departments work there for

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achieving objectives and gaols of it. Various segments are like human resource, production,

finance and accounts, operation, marketing, research and development, selling and distribution

etc. The method in which expenses, costs and other financial information recorded after

segregating department wise is known as departmental report. A reason due to which this

technique used by R.L. Maynard is to determine financial performance of each and every

organisational function. During this, if management finds that specific department incurs more

expenses and less return, then corrective actions and strategies are applied on that.

Inventory management report: Lastly, a method in which data as well as information related to

stock recorded and analysed is considered as inventory management report. In the firm when

level of stock is high and create adverse influence on the revenue and profit (Fullerton,

Kennedy and Widener, 2014). Along with this, turnover ratio of this also give negative response

to R.L. Maynard. Therefore, management of this aspect is necessary in highly efficient

direction. The chosen enterprise of construction segment uses this particular reports which

reflects stock available at the beginning of year and inventory remained at the end of accounting

period. To manage this some techniques are used which are like re-order point, EOQ, LIFO,

FIFO, just-in-time etc.

Conclusion

By considering the above analysis it can be said that reporting system is essential part for each

enterprise because it helps to track the financial performance of it. Apart from this, it helps to

prepare final accounts like trial balance, income statement, changes in equity and gains, balance

sheet etc. Methods of reporting used by R.L. Maynard Limited are like job cost, stock

management, departmental, operating budget and accounts receivables ageing. Further, when

cited firm is going to manage and reduce stock then some methods used.

TASK 2

P3 Computing costs and formulate income statement by incorporating marginal and absorption

costing

For preparing the financial statements, there are some methods included in the area of

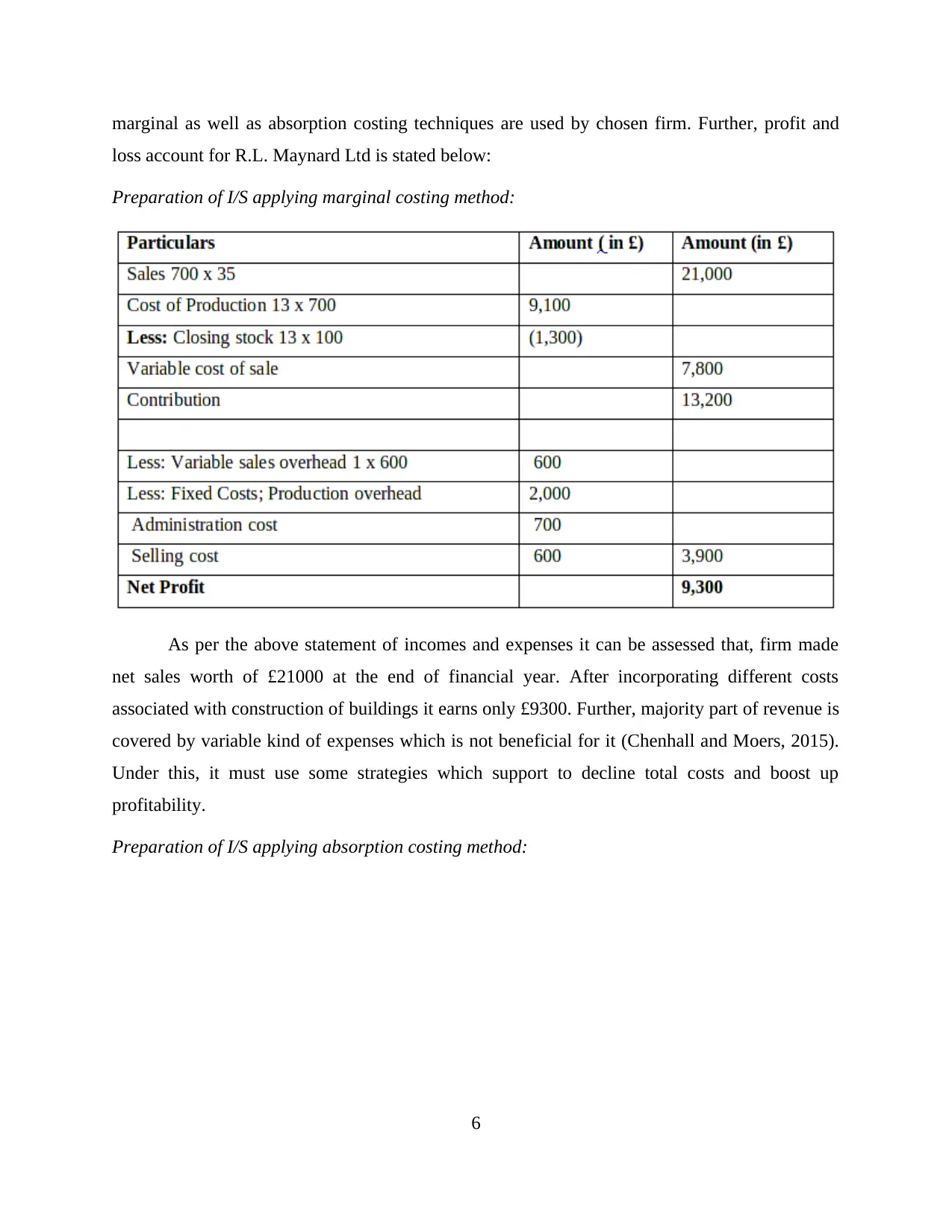

accounting study. The present task reflects about the income statement and to prepare this

5

finance and accounts, operation, marketing, research and development, selling and distribution

etc. The method in which expenses, costs and other financial information recorded after

segregating department wise is known as departmental report. A reason due to which this

technique used by R.L. Maynard is to determine financial performance of each and every

organisational function. During this, if management finds that specific department incurs more

expenses and less return, then corrective actions and strategies are applied on that.

Inventory management report: Lastly, a method in which data as well as information related to

stock recorded and analysed is considered as inventory management report. In the firm when

level of stock is high and create adverse influence on the revenue and profit (Fullerton,

Kennedy and Widener, 2014). Along with this, turnover ratio of this also give negative response

to R.L. Maynard. Therefore, management of this aspect is necessary in highly efficient

direction. The chosen enterprise of construction segment uses this particular reports which

reflects stock available at the beginning of year and inventory remained at the end of accounting

period. To manage this some techniques are used which are like re-order point, EOQ, LIFO,

FIFO, just-in-time etc.

Conclusion

By considering the above analysis it can be said that reporting system is essential part for each

enterprise because it helps to track the financial performance of it. Apart from this, it helps to

prepare final accounts like trial balance, income statement, changes in equity and gains, balance

sheet etc. Methods of reporting used by R.L. Maynard Limited are like job cost, stock

management, departmental, operating budget and accounts receivables ageing. Further, when

cited firm is going to manage and reduce stock then some methods used.

TASK 2

P3 Computing costs and formulate income statement by incorporating marginal and absorption

costing

For preparing the financial statements, there are some methods included in the area of

accounting study. The present task reflects about the income statement and to prepare this

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

marginal as well as absorption costing techniques are used by chosen firm. Further, profit and

loss account for R.L. Maynard Ltd is stated below:

Preparation of I/S applying marginal costing method:

As per the above statement of incomes and expenses it can be assessed that, firm made

net sales worth of £21000 at the end of financial year. After incorporating different costs

associated with construction of buildings it earns only £9300. Further, majority part of revenue is

covered by variable kind of expenses which is not beneficial for it (Chenhall and Moers, 2015).

Under this, it must use some strategies which support to decline total costs and boost up

profitability.

Preparation of I/S applying absorption costing method:

6

loss account for R.L. Maynard Ltd is stated below:

Preparation of I/S applying marginal costing method:

As per the above statement of incomes and expenses it can be assessed that, firm made

net sales worth of £21000 at the end of financial year. After incorporating different costs

associated with construction of buildings it earns only £9300. Further, majority part of revenue is

covered by variable kind of expenses which is not beneficial for it (Chenhall and Moers, 2015).

Under this, it must use some strategies which support to decline total costs and boost up

profitability.

Preparation of I/S applying absorption costing method:

6

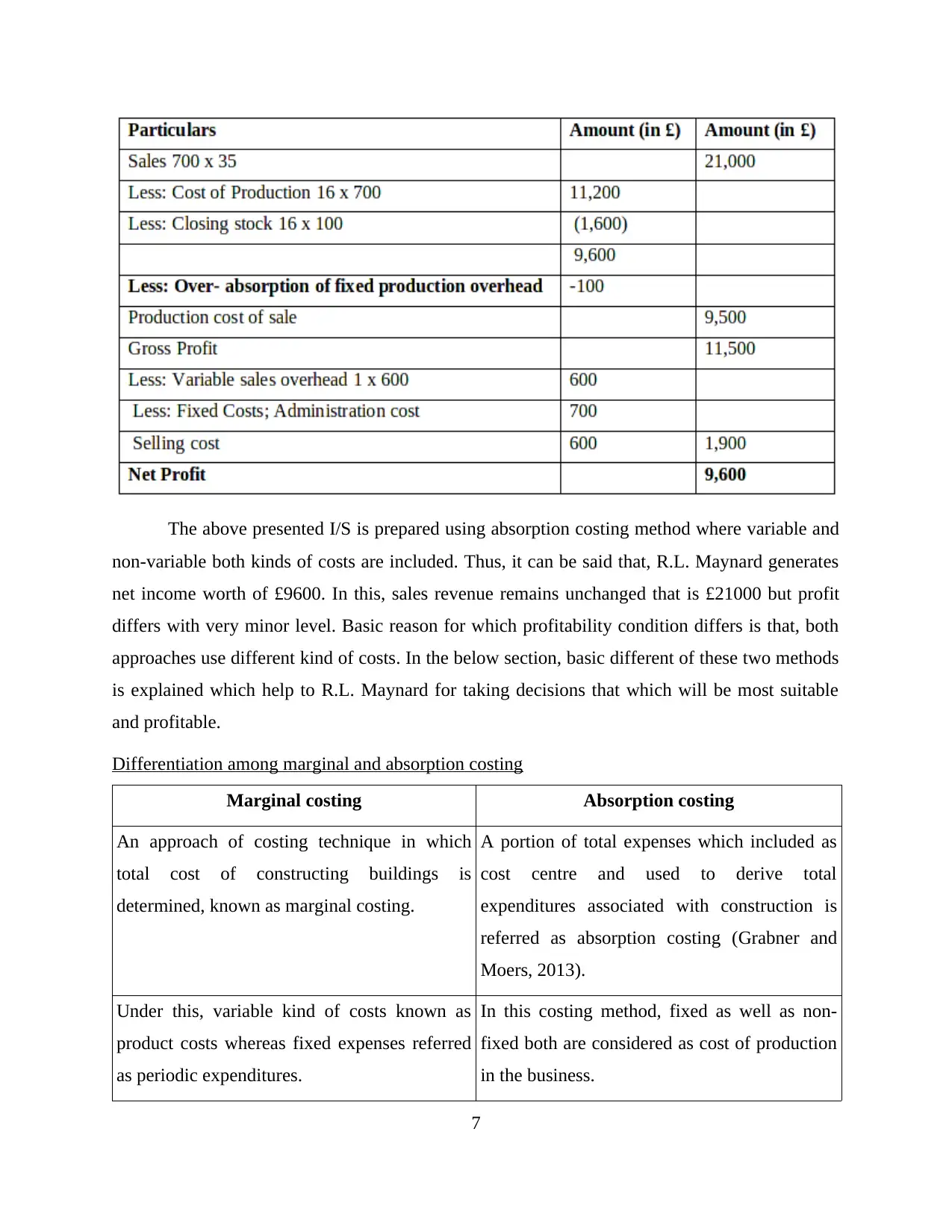

The above presented I/S is prepared using absorption costing method where variable and

non-variable both kinds of costs are included. Thus, it can be said that, R.L. Maynard generates

net income worth of £9600. In this, sales revenue remains unchanged that is £21000 but profit

differs with very minor level. Basic reason for which profitability condition differs is that, both

approaches use different kind of costs. In the below section, basic different of these two methods

is explained which help to R.L. Maynard for taking decisions that which will be most suitable

and profitable.

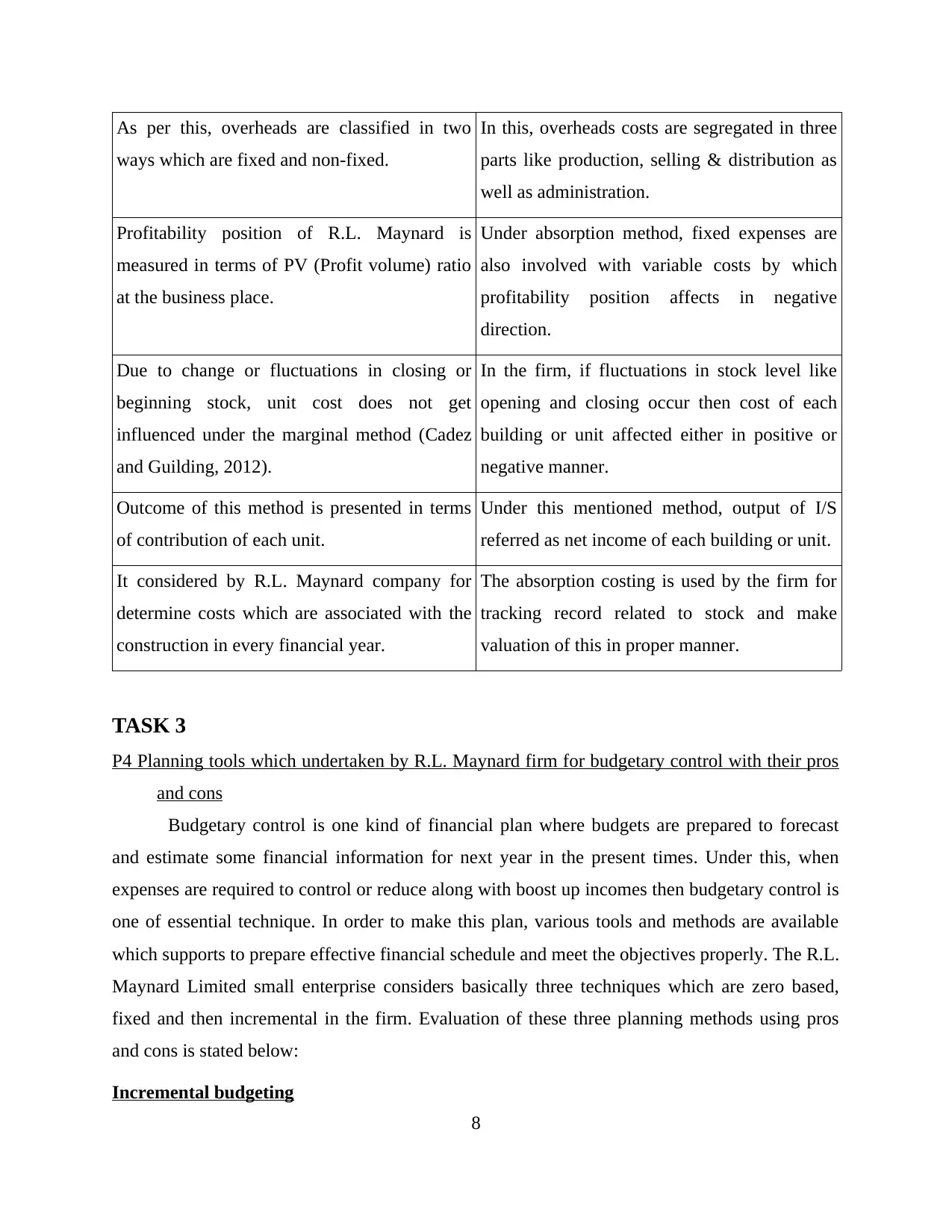

Differentiation among marginal and absorption costing

Marginal costing Absorption costing

An approach of costing technique in which

total cost of constructing buildings is

determined, known as marginal costing.

A portion of total expenses which included as

cost centre and used to derive total

expenditures associated with construction is

referred as absorption costing (Grabner and

Moers, 2013).

Under this, variable kind of costs known as

product costs whereas fixed expenses referred

as periodic expenditures.

In this costing method, fixed as well as non-

fixed both are considered as cost of production

in the business.

7

non-variable both kinds of costs are included. Thus, it can be said that, R.L. Maynard generates

net income worth of £9600. In this, sales revenue remains unchanged that is £21000 but profit

differs with very minor level. Basic reason for which profitability condition differs is that, both

approaches use different kind of costs. In the below section, basic different of these two methods

is explained which help to R.L. Maynard for taking decisions that which will be most suitable

and profitable.

Differentiation among marginal and absorption costing

Marginal costing Absorption costing

An approach of costing technique in which

total cost of constructing buildings is

determined, known as marginal costing.

A portion of total expenses which included as

cost centre and used to derive total

expenditures associated with construction is

referred as absorption costing (Grabner and

Moers, 2013).

Under this, variable kind of costs known as

product costs whereas fixed expenses referred

as periodic expenditures.

In this costing method, fixed as well as non-

fixed both are considered as cost of production

in the business.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per this, overheads are classified in two

ways which are fixed and non-fixed.

In this, overheads costs are segregated in three

parts like production, selling & distribution as

well as administration.

Profitability position of R.L. Maynard is

measured in terms of PV (Profit volume) ratio

at the business place.

Under absorption method, fixed expenses are

also involved with variable costs by which

profitability position affects in negative

direction.

Due to change or fluctuations in closing or

beginning stock, unit cost does not get

influenced under the marginal method (Cadez

and Guilding, 2012).

In the firm, if fluctuations in stock level like

opening and closing occur then cost of each

building or unit affected either in positive or

negative manner.

Outcome of this method is presented in terms

of contribution of each unit.

Under this mentioned method, output of I/S

referred as net income of each building or unit.

It considered by R.L. Maynard company for

determine costs which are associated with the

construction in every financial year.

The absorption costing is used by the firm for

tracking record related to stock and make

valuation of this in proper manner.

TASK 3

P4 Planning tools which undertaken by R.L. Maynard firm for budgetary control with their pros

and cons

Budgetary control is one kind of financial plan where budgets are prepared to forecast

and estimate some financial information for next year in the present times. Under this, when

expenses are required to control or reduce along with boost up incomes then budgetary control is

one of essential technique. In order to make this plan, various tools and methods are available

which supports to prepare effective financial schedule and meet the objectives properly. The R.L.

Maynard Limited small enterprise considers basically three techniques which are zero based,

fixed and then incremental in the firm. Evaluation of these three planning methods using pros

and cons is stated below:

Incremental budgeting

8

ways which are fixed and non-fixed.

In this, overheads costs are segregated in three

parts like production, selling & distribution as

well as administration.

Profitability position of R.L. Maynard is

measured in terms of PV (Profit volume) ratio

at the business place.

Under absorption method, fixed expenses are

also involved with variable costs by which

profitability position affects in negative

direction.

Due to change or fluctuations in closing or

beginning stock, unit cost does not get

influenced under the marginal method (Cadez

and Guilding, 2012).

In the firm, if fluctuations in stock level like

opening and closing occur then cost of each

building or unit affected either in positive or

negative manner.

Outcome of this method is presented in terms

of contribution of each unit.

Under this mentioned method, output of I/S

referred as net income of each building or unit.

It considered by R.L. Maynard company for

determine costs which are associated with the

construction in every financial year.

The absorption costing is used by the firm for

tracking record related to stock and make

valuation of this in proper manner.

TASK 3

P4 Planning tools which undertaken by R.L. Maynard firm for budgetary control with their pros

and cons

Budgetary control is one kind of financial plan where budgets are prepared to forecast

and estimate some financial information for next year in the present times. Under this, when

expenses are required to control or reduce along with boost up incomes then budgetary control is

one of essential technique. In order to make this plan, various tools and methods are available

which supports to prepare effective financial schedule and meet the objectives properly. The R.L.

Maynard Limited small enterprise considers basically three techniques which are zero based,

fixed and then incremental in the firm. Evaluation of these three planning methods using pros

and cons is stated below:

Incremental budgeting

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A method in which base of the past financial statements is taken and values increases

with specific percentage each period for preparing budgets is known as incremental budgeting.

Under this, incomes are increased with high rate whereas change in expenses mentioned with

low rate comparatively (Davies and Crawford, 2011). It is used by R.L. Maynard on major and

wide basis due to supportive for enhancing business performance continuously. Further, its

benefits and drawbacks are stated below:

Benefits:

Budget statement prepared under incremental method is in the nature of stable

improvement where change occurs gradually.

Managers of R.L. Maynard easily able to operate this in all the departments on

continuous basis.

It is very simple to prepare in the business along with easily understandable for every

employee who works in the enterprise.

Influence of change or increment can be visualised quickly as per this stated planning

tool.

Issues of the conflicts in the firm are to be avoided when all the departments treated in

same or similar direction.

It helps to establish an effective kind of coordination among the budgets and managers of

various functions properly (Budgeting Methods - Incremental Budgeting, 2015). Apart from this, for achieving financial objectives on consistent basis and boost up

growth rate also incremental tool is beneficial for R.L. Maynard small business.

Drawbacks:

Major problem associated with incremental budgeting is that, it makes assumptions that

all the working activities will continue with same manner as responded in the past

financial years.

Opportunities or chances to earn incentives amount behind developing new opinions and

ideas are lost by R.L. Maynard when it implements this planning tool of budgetary

control.

9

with specific percentage each period for preparing budgets is known as incremental budgeting.

Under this, incomes are increased with high rate whereas change in expenses mentioned with

low rate comparatively (Davies and Crawford, 2011). It is used by R.L. Maynard on major and

wide basis due to supportive for enhancing business performance continuously. Further, its

benefits and drawbacks are stated below:

Benefits:

Budget statement prepared under incremental method is in the nature of stable

improvement where change occurs gradually.

Managers of R.L. Maynard easily able to operate this in all the departments on

continuous basis.

It is very simple to prepare in the business along with easily understandable for every

employee who works in the enterprise.

Influence of change or increment can be visualised quickly as per this stated planning

tool.

Issues of the conflicts in the firm are to be avoided when all the departments treated in

same or similar direction.

It helps to establish an effective kind of coordination among the budgets and managers of

various functions properly (Budgeting Methods - Incremental Budgeting, 2015). Apart from this, for achieving financial objectives on consistent basis and boost up

growth rate also incremental tool is beneficial for R.L. Maynard small business.

Drawbacks:

Major problem associated with incremental budgeting is that, it makes assumptions that

all the working activities will continue with same manner as responded in the past

financial years.

Opportunities or chances to earn incentives amount behind developing new opinions and

ideas are lost by R.L. Maynard when it implements this planning tool of budgetary

control.

9

There are no incentives occurred to decline costs and expenditures.

Priority in order to utilise the resources can be fluctuated or changed until and unless the

budgets are not set originally.

Fixed budgeting

This budget does not fluctuate when there is increase or decrease in sales observed by the

organisation and it is also called as s static budget. It does not change as the volume changes.

This does not flex whenever sales increases or vice -versa (Kotas, 2014). Eg: commission on

sales is 10%, then whether firm is earning or not it will pay the said commission only.

Advantages:

The first advantage of fixed budgeting is that it helps R.L. Maynard Ltd to prioritize. It

helps us to put an eye so that our expenses does not exceed out of our planned budget.

Next advantage relating to cited company is that its construction company and in that

context it will be helpful in clearing debt due to past financial choices, company has

made.

The R.L. Maynard finds it easy to implement it and then follow accordingly because it

need not to be updated continuously throughout the accounting period of that year.

As it is construction company, it offers great insight into company's costs and profits. The company can put an eye about under estimating and over estimating and shift the

over estimations to under estimations.

Limitations:

Firm cannot constantly update it which makes it more degradable because company is

dynamic in nature and what has planned needs to altered or changed accordingly as may

be the case be (Zimmerman and Yahya-Zadeh, 2011).

No flexibility is observed as it cannot be changed through the accounting period to which

it is applicable.

R.L. Maynard Limited company which allows increasing its sales volume, it cannot add

additional resources as resources are tied up in this budget.

10

Priority in order to utilise the resources can be fluctuated or changed until and unless the

budgets are not set originally.

Fixed budgeting

This budget does not fluctuate when there is increase or decrease in sales observed by the

organisation and it is also called as s static budget. It does not change as the volume changes.

This does not flex whenever sales increases or vice -versa (Kotas, 2014). Eg: commission on

sales is 10%, then whether firm is earning or not it will pay the said commission only.

Advantages:

The first advantage of fixed budgeting is that it helps R.L. Maynard Ltd to prioritize. It

helps us to put an eye so that our expenses does not exceed out of our planned budget.

Next advantage relating to cited company is that its construction company and in that

context it will be helpful in clearing debt due to past financial choices, company has

made.

The R.L. Maynard finds it easy to implement it and then follow accordingly because it

need not to be updated continuously throughout the accounting period of that year.

As it is construction company, it offers great insight into company's costs and profits. The company can put an eye about under estimating and over estimating and shift the

over estimations to under estimations.

Limitations:

Firm cannot constantly update it which makes it more degradable because company is

dynamic in nature and what has planned needs to altered or changed accordingly as may

be the case be (Zimmerman and Yahya-Zadeh, 2011).

No flexibility is observed as it cannot be changed through the accounting period to which

it is applicable.

R.L. Maynard Limited company which allows increasing its sales volume, it cannot add

additional resources as resources are tied up in this budget.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.