Comprehensive Analysis of Management Accounting Reports and Systems

VerifiedAdded on 2023/01/12

|19

|4262

|98

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA) principles and their practical application. It begins by defining MA and its role in providing financial data for internal decision-making, focusing on Grant Thornton and its client, Creams Limited. Task 1 explores various MA systems, including inventory management, cost accounting, price optimization, and job-order costing, highlighting their benefits and applications. It also examines different types of MA reports, such as cost reports, stock reports, and accounts receivable reports, and their correlation with MA systems. Task 2 delves into the preparation of income statements using marginal and absorption costing methods, including their advantages and disadvantages. Task 3 discusses the benefits and drawbacks of planning tools used for budgetary control. Finally, Task 4 emphasizes the importance of MA in solving financial issues, including the role of planning tools and the use of MA to respond to financial problems. The report concludes by summarizing the key findings and insights gained throughout the analysis.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1 MAS and their application..................................................................................................................3

P2 Different ways of MA reports.............................................................................................................5

D1 Correlation between MAS and MA reports.......................................................................................6

TASK 2..........................................................................................................................................................7

P3 Preparation of income statements.......................................................................................................7

M2 Techniques to prepare income statements.......................................................................................11

D2 Interpretation of produced income statement...................................................................................11

TASK 3........................................................................................................................................................11

P4. Benefits and drawbacks of different types of planning tools used for budgetary control.............11

M3 Role of planning tools.....................................................................................................................13

TASK 4........................................................................................................................................................13

P5 Importance of MAS to solve issues..................................................................................................13

M4 MA to respond financial problems..................................................................................................15

D3 Role of planning tools to solve financial issues...............................................................................15

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1 MAS and their application..................................................................................................................3

P2 Different ways of MA reports.............................................................................................................5

D1 Correlation between MAS and MA reports.......................................................................................6

TASK 2..........................................................................................................................................................7

P3 Preparation of income statements.......................................................................................................7

M2 Techniques to prepare income statements.......................................................................................11

D2 Interpretation of produced income statement...................................................................................11

TASK 3........................................................................................................................................................11

P4. Benefits and drawbacks of different types of planning tools used for budgetary control.............11

M3 Role of planning tools.....................................................................................................................13

TASK 4........................................................................................................................................................13

P5 Importance of MAS to solve issues..................................................................................................13

M4 MA to respond financial problems..................................................................................................15

D3 Role of planning tools to solve financial issues...............................................................................15

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION

MA is described as an accounting system that allows a business to operate more effectively.

This can be defined as the implementation of accounting methods to find out need of monetary

data for better management. It concentrates on aspects of accounting (Bromwichand Scapens,

2016). Under this accounting both financial and non financial information is used in order to

produce internal reports that lead to better decisions. The collected information is used by

managers to determine systematically. MA is a system mechanism that offers the details

necessary for various levels of management. The report is based on company that is Grant

Thornton, headquartered in United Kingdom. This company is one of the main accounting firms

which provide its services to its clients. Creams limited are a client company of above

accounting firm. This company sells ice cream, doughnuts. The project report covers detailed

information about various accounting systems and reports as well as different range of planning

tools are also mentioned. The further part of report demonstrates about role of MA in solving

financial issues.

TASK 1

P1 MAS and their application

MA is also considered as managerial accounting and is characterized as a judgment creating

process for providing monetary data to administrators. MA is generally utilized for the

accounting department of the company, since that is mainly the different from financial

accounting concepts (McLaren, Appleyard,and Mitchell, 2016). Through this process financial

information and tax forms are shared through a financial division with the management

personnel of the company. This background knowledge is used to take better as well as for more

accurate decisions, track the organization performance, business trends etc. It includes various

kinds of accounting systems like:

Inventory Management System- The system for stock management is a tool for better

stock regulation through the organization’s supply chain. In Creams limited the whole

distribution cycle from placing orders to suppliers is constrained by this method and it

enables the whole path of in a systematic manner (Aria and Rahadjeng, 2018). Through

using the inventory control method, sales firms, retailers, manufacturers and vendors can

MA is described as an accounting system that allows a business to operate more effectively.

This can be defined as the implementation of accounting methods to find out need of monetary

data for better management. It concentrates on aspects of accounting (Bromwichand Scapens,

2016). Under this accounting both financial and non financial information is used in order to

produce internal reports that lead to better decisions. The collected information is used by

managers to determine systematically. MA is a system mechanism that offers the details

necessary for various levels of management. The report is based on company that is Grant

Thornton, headquartered in United Kingdom. This company is one of the main accounting firms

which provide its services to its clients. Creams limited are a client company of above

accounting firm. This company sells ice cream, doughnuts. The project report covers detailed

information about various accounting systems and reports as well as different range of planning

tools are also mentioned. The further part of report demonstrates about role of MA in solving

financial issues.

TASK 1

P1 MAS and their application

MA is also considered as managerial accounting and is characterized as a judgment creating

process for providing monetary data to administrators. MA is generally utilized for the

accounting department of the company, since that is mainly the different from financial

accounting concepts (McLaren, Appleyard,and Mitchell, 2016). Through this process financial

information and tax forms are shared through a financial division with the management

personnel of the company. This background knowledge is used to take better as well as for more

accurate decisions, track the organization performance, business trends etc. It includes various

kinds of accounting systems like:

Inventory Management System- The system for stock management is a tool for better

stock regulation through the organization’s supply chain. In Creams limited the whole

distribution cycle from placing orders to suppliers is constrained by this method and it

enables the whole path of in a systematic manner (Aria and Rahadjeng, 2018). Through

using the inventory control method, sales firms, retailers, manufacturers and vendors can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

make their stores effective by taking correct decisions for stock purchasing. The system

involves vital range of methods such as LIFO, FIFO and Average Costs. It is essential for

companies to take corrective actions for management of stored inventories. Below

description of these methods is done:

LIFO (Last in first out) - It is a type of method in which stock that comes last is used

first for production.

FIFO (First in first out) - This method is different from previous method, as under it

stock that comes first in store is used for production.

Cost accounting system- It is a form of management accounting method that

encompasses a large wide range of operations as well as financial factors. In order to

hold cost under estimate, it is important for companies (Fleischman and Parker, 2017).

This accounting is used, as in the aspect of the above company, to maintain production

expenses below the expected cost. The main objective of this is to focus on keeping cost

of various operations lower as much as possible. Without it, this can possible to keep

their cost lower from estimated value of cost. It is not associated to specific company as

it can be applied in any business whether it is financial and non financial.

Price optimization system- It is a method which includes a particular way of setting

pricing and service requirements for the customer. This accounting method helps

businesses to gain useful market patterns and data on consumer requests. Basically, this

collected information is used by businesses to take suitable actions for setting of prices

of their products. In the sense of the abovementioned chosen company their selling

department changes price strategies in accordance with consumer needs and they do so

by help of this accounting system.

Job-order Costing- The job ordering system monitors the expense of each work inside

the organization. The management can closely track each task's costs and determine if

the actual costs generated is relatively close and expected costs is higher. Substantial

shortfalls in costs will force management to analyze and implement corrective steps to

address the cost increase cause. This approach collects and accumulates costs for

specific workers, work orders or assignments. The cost of each task is calculated

appropriately and each work described separately. Under above business they implement

it in order to manage cost of each job in an effective manner.

involves vital range of methods such as LIFO, FIFO and Average Costs. It is essential for

companies to take corrective actions for management of stored inventories. Below

description of these methods is done:

LIFO (Last in first out) - It is a type of method in which stock that comes last is used

first for production.

FIFO (First in first out) - This method is different from previous method, as under it

stock that comes first in store is used for production.

Cost accounting system- It is a form of management accounting method that

encompasses a large wide range of operations as well as financial factors. In order to

hold cost under estimate, it is important for companies (Fleischman and Parker, 2017).

This accounting is used, as in the aspect of the above company, to maintain production

expenses below the expected cost. The main objective of this is to focus on keeping cost

of various operations lower as much as possible. Without it, this can possible to keep

their cost lower from estimated value of cost. It is not associated to specific company as

it can be applied in any business whether it is financial and non financial.

Price optimization system- It is a method which includes a particular way of setting

pricing and service requirements for the customer. This accounting method helps

businesses to gain useful market patterns and data on consumer requests. Basically, this

collected information is used by businesses to take suitable actions for setting of prices

of their products. In the sense of the abovementioned chosen company their selling

department changes price strategies in accordance with consumer needs and they do so

by help of this accounting system.

Job-order Costing- The job ordering system monitors the expense of each work inside

the organization. The management can closely track each task's costs and determine if

the actual costs generated is relatively close and expected costs is higher. Substantial

shortfalls in costs will force management to analyze and implement corrective steps to

address the cost increase cause. This approach collects and accumulates costs for

specific workers, work orders or assignments. The cost of each task is calculated

appropriately and each work described separately. Under above business they implement

it in order to manage cost of each job in an effective manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Different ways of MA reports.

These are defined as documented reports consisting of detailed information about the

monetary and anti-monetary components (Maas, Schaltegger and Crutzen, 2016). Such reported

details are frequently used by organizational departments to take effective measures at the right

time. The accountant of Cream limited generates the below reports which are as follows:

Cost report- This includes details on expenditures for the execution of a variety of

business and operations (Yin and Tian, 2017). Along with under this report, the activities

are classified by their expense level. The aim of the report is to concentrate on certain

elements and factors that are more expensive (Machado, 2016). In relation to the above

company, their finance team uses this report in order to manage overall number of

expenses below standard cost. Under this report, different types of costs are classified as

per its nature like direct cost, indirect cost and many more. Due to which it becomes

easier for managers to take appropriate actions.

Stock report- This can be known as a report that includes information about stored

volume of products of stores. This report is prepared with the assistance of the stock

management system. The main aim of this report is to assist the production department in

taking the appropriate measures about how many units are needed. The above-mentioned

organization produces different types of food products in accordance of this report’s

information. In this report information about all types of goods is included such as raw

material, WIP and prepared products. Such information helps to managers to take right

action.

Accounts receivable report- It includes information about the amount of debtors liable for

companies with the actual date of sale. The importance of it is to assist finance

department to devise specific policies and strategies (Darko, Adarkwah, Donkor and

Kyei, 2016). Basically, this report is mainly used in that organization in which credit

transactions are done on higher basis. By help of it managers can determine efficiency of

their debtors. Their financial team in the above organization utilizes crucial details by

help of this report in order to collect debts on time from debtors.

M1 Importance of MAS.

System Name Benefits

These are defined as documented reports consisting of detailed information about the

monetary and anti-monetary components (Maas, Schaltegger and Crutzen, 2016). Such reported

details are frequently used by organizational departments to take effective measures at the right

time. The accountant of Cream limited generates the below reports which are as follows:

Cost report- This includes details on expenditures for the execution of a variety of

business and operations (Yin and Tian, 2017). Along with under this report, the activities

are classified by their expense level. The aim of the report is to concentrate on certain

elements and factors that are more expensive (Machado, 2016). In relation to the above

company, their finance team uses this report in order to manage overall number of

expenses below standard cost. Under this report, different types of costs are classified as

per its nature like direct cost, indirect cost and many more. Due to which it becomes

easier for managers to take appropriate actions.

Stock report- This can be known as a report that includes information about stored

volume of products of stores. This report is prepared with the assistance of the stock

management system. The main aim of this report is to assist the production department in

taking the appropriate measures about how many units are needed. The above-mentioned

organization produces different types of food products in accordance of this report’s

information. In this report information about all types of goods is included such as raw

material, WIP and prepared products. Such information helps to managers to take right

action.

Accounts receivable report- It includes information about the amount of debtors liable for

companies with the actual date of sale. The importance of it is to assist finance

department to devise specific policies and strategies (Darko, Adarkwah, Donkor and

Kyei, 2016). Basically, this report is mainly used in that organization in which credit

transactions are done on higher basis. By help of it managers can determine efficiency of

their debtors. Their financial team in the above organization utilizes crucial details by

help of this report in order to collect debts on time from debtors.

M1 Importance of MAS.

System Name Benefits

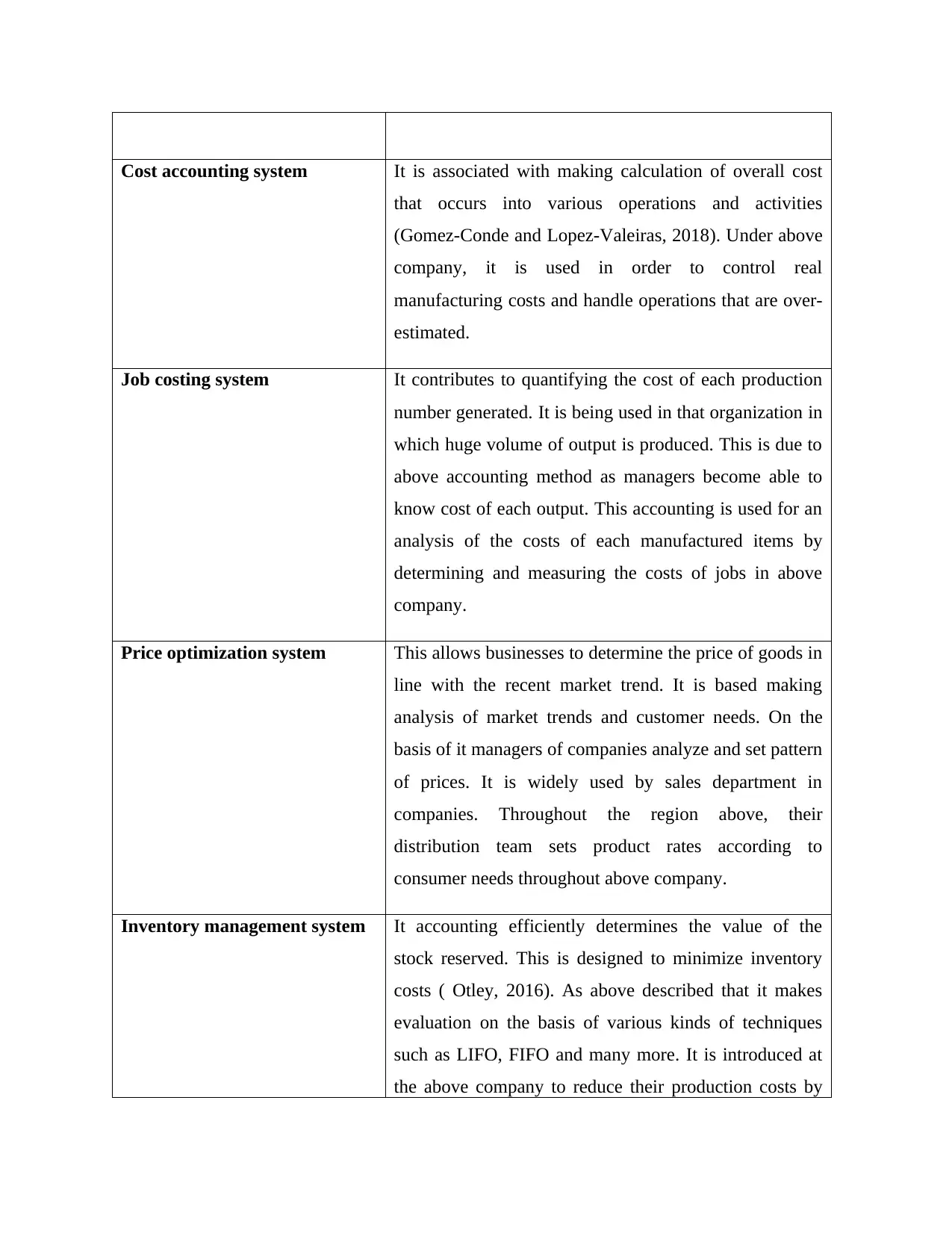

Cost accounting system It is associated with making calculation of overall cost

that occurs into various operations and activities

(Gomez-Conde and Lopez-Valeiras, 2018). Under above

company, it is used in order to control real

manufacturing costs and handle operations that are over-

estimated.

Job costing system It contributes to quantifying the cost of each production

number generated. It is being used in that organization in

which huge volume of output is produced. This is due to

above accounting method as managers become able to

know cost of each output. This accounting is used for an

analysis of the costs of each manufactured items by

determining and measuring the costs of jobs in above

company.

Price optimization system This allows businesses to determine the price of goods in

line with the recent market trend. It is based making

analysis of market trends and customer needs. On the

basis of it managers of companies analyze and set pattern

of prices. It is widely used by sales department in

companies. Throughout the region above, their

distribution team sets product rates according to

consumer needs throughout above company.

Inventory management system It accounting efficiently determines the value of the

stock reserved. This is designed to minimize inventory

costs ( Otley, 2016). As above described that it makes

evaluation on the basis of various kinds of techniques

such as LIFO, FIFO and many more. It is introduced at

the above company to reduce their production costs by

that occurs into various operations and activities

(Gomez-Conde and Lopez-Valeiras, 2018). Under above

company, it is used in order to control real

manufacturing costs and handle operations that are over-

estimated.

Job costing system It contributes to quantifying the cost of each production

number generated. It is being used in that organization in

which huge volume of output is produced. This is due to

above accounting method as managers become able to

know cost of each output. This accounting is used for an

analysis of the costs of each manufactured items by

determining and measuring the costs of jobs in above

company.

Price optimization system This allows businesses to determine the price of goods in

line with the recent market trend. It is based making

analysis of market trends and customer needs. On the

basis of it managers of companies analyze and set pattern

of prices. It is widely used by sales department in

companies. Throughout the region above, their

distribution team sets product rates according to

consumer needs throughout above company.

Inventory management system It accounting efficiently determines the value of the

stock reserved. This is designed to minimize inventory

costs ( Otley, 2016). As above described that it makes

evaluation on the basis of various kinds of techniques

such as LIFO, FIFO and many more. It is introduced at

the above company to reduce their production costs by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

making evaluation of stored quantity of stock.

D1 Correlation between MAS and MA reports.

The MA includes a variety of accounting systems and records which comply with

company procedure and enterprises (Rebelo, Santos and Silva, 2016). With regard to the above

business, their separate departments are linked to the accounting system. For example in the

Creams limited in order to of raise profits, the price optimization system is aligned in sales team.

The stock report is related to the production department. For instance in the above mentioned

company, their managers use different reports for corrective measures in the retail field. Apart

from it, rest of reports are also linked to companies departments such as finance department of

above company take decisions regards to credit facility to customers in accordance of accounts

receivable report. This link between process of company and accounting systems leads to higher

success of business entities.

TASK 2

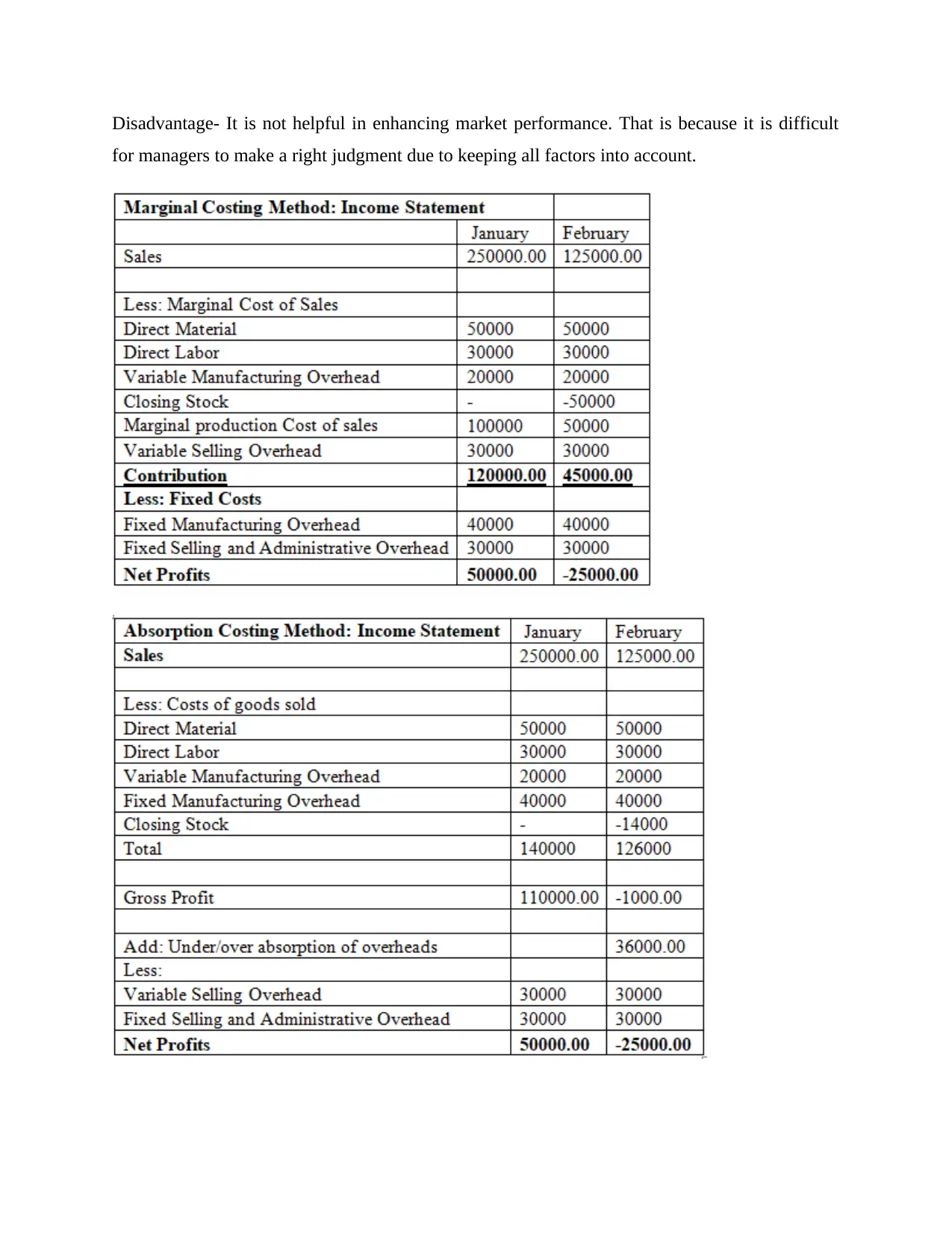

P3 Preparation of income statements.

Marginal costing method: This can be interpreted as a costing method by which the effects

of different activities occur in various ways (Nathwani, 2020). The fix expenses are considered

as time cost while non fix costs are viewed as unit costs.

Advantages- It is of essence continuous. That is because variable expenses differ periodically

but the total cost will not shift over a long period of time.

Disadvantage- One of the key problems of this technique is that the time dimension is not taken

into account.

Absorption costing- This is a system of costing that defines and allocates in common the costs

paid for various tasks and operations (Gersil and Kayal, 2016). The cost of the product is

considered under fixed and non-fixed costs. There are also other limitations and benefits such as:

Advantages- The biggest benefit of this system is that it can efficiently track revenue.

D1 Correlation between MAS and MA reports.

The MA includes a variety of accounting systems and records which comply with

company procedure and enterprises (Rebelo, Santos and Silva, 2016). With regard to the above

business, their separate departments are linked to the accounting system. For example in the

Creams limited in order to of raise profits, the price optimization system is aligned in sales team.

The stock report is related to the production department. For instance in the above mentioned

company, their managers use different reports for corrective measures in the retail field. Apart

from it, rest of reports are also linked to companies departments such as finance department of

above company take decisions regards to credit facility to customers in accordance of accounts

receivable report. This link between process of company and accounting systems leads to higher

success of business entities.

TASK 2

P3 Preparation of income statements.

Marginal costing method: This can be interpreted as a costing method by which the effects

of different activities occur in various ways (Nathwani, 2020). The fix expenses are considered

as time cost while non fix costs are viewed as unit costs.

Advantages- It is of essence continuous. That is because variable expenses differ periodically

but the total cost will not shift over a long period of time.

Disadvantage- One of the key problems of this technique is that the time dimension is not taken

into account.

Absorption costing- This is a system of costing that defines and allocates in common the costs

paid for various tasks and operations (Gersil and Kayal, 2016). The cost of the product is

considered under fixed and non-fixed costs. There are also other limitations and benefits such as:

Advantages- The biggest benefit of this system is that it can efficiently track revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantage- It is not helpful in enhancing market performance. That is because it is difficult

for managers to make a right judgment due to keeping all factors into account.

for managers to make a right judgment due to keeping all factors into account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

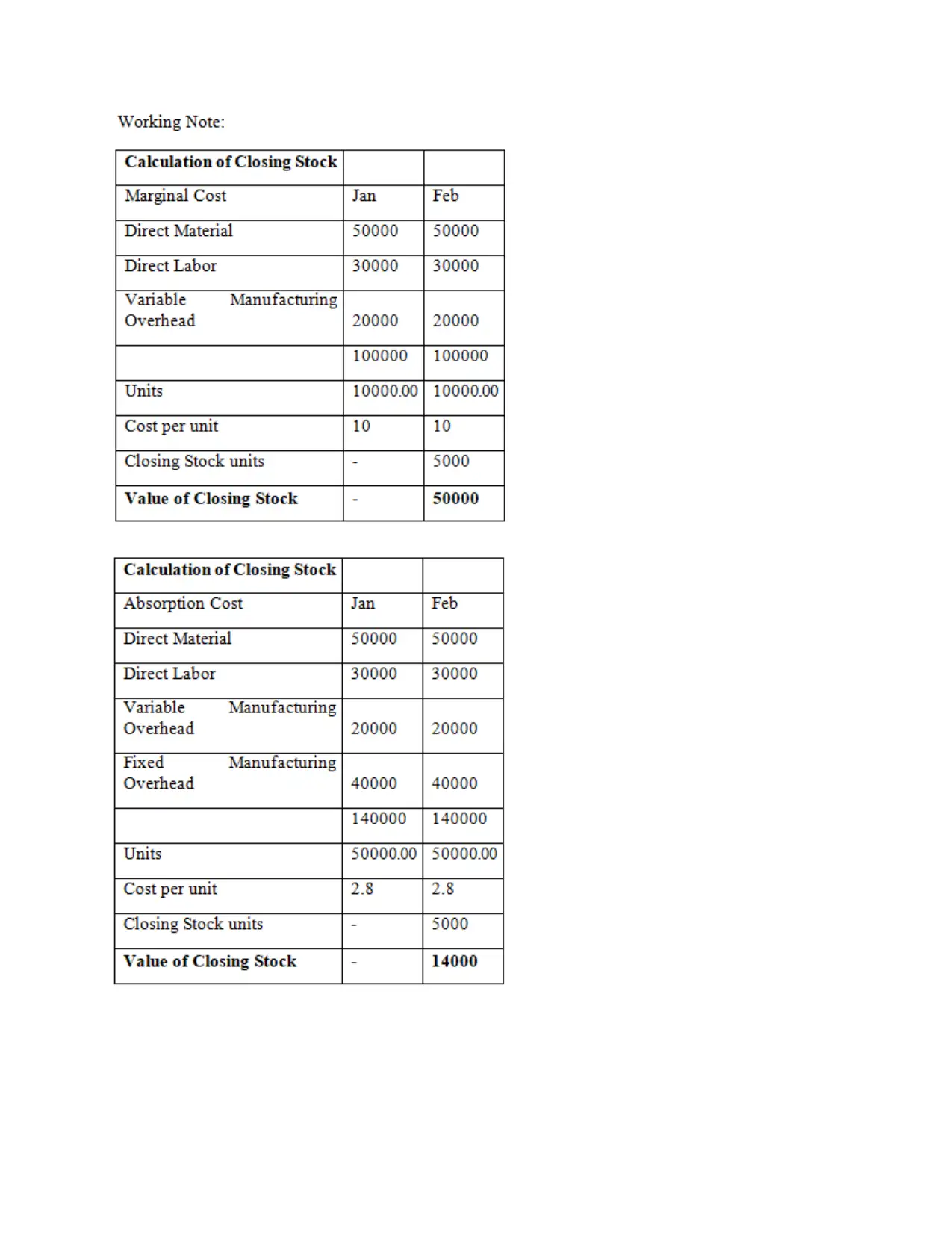

M2 Techniques to prepare income statements.

There are different types of techniques in order to produce financial statements. It

depends on companies that which method they implement for financial reports (Armitage, Webb

and Glynn, 2016). In the above report, profit and loss accounts are produced on the behalf of two

methods which are marginal and absorption costing. Under both of these techniques value of net

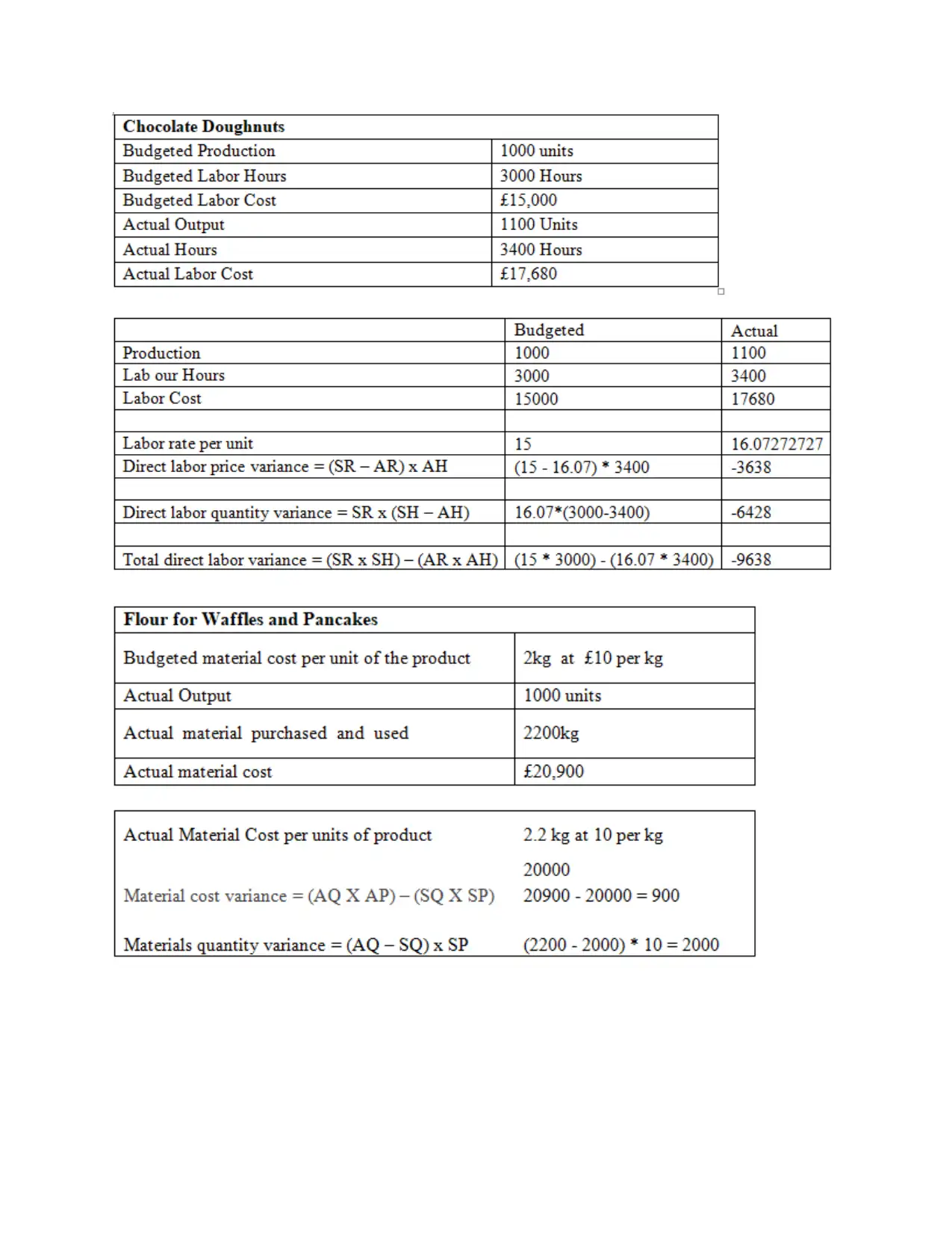

profit is different due to way of taking expenses. Apart from it, various kinds of labor and

material variances are calculated in accordance of particular formula. For instance under labor

variance four types of variances are calculated such as labor price, quantity etc. same as under

material variance too, different types of variances are computed as per given scenario.

D2 Interpretation of produced income statement.

In accordance of produced financial system under different methods this can be find out

that net profit is 50000 and -25000 under marginal costing. As well as under absorption costing

profit is also similar that is of 50000 and -25000 for similar time period. In addition, variances

are also computed including labor and material variances.

TASK 3

P4. Benefits and drawbacks of different types of planning tools used for budgetary control.

Budgetary control- It can be described as a way to manage financial and anti-financial

performance across a number of budgets (Mohamed, Kerosi and Tirimba, 2016). In this

dimension of the budgetary function, the managers of businesses undertake corrective measures

to produce more results by means of such financial plans. In other words, this can be defined as

process of making budgets on the basis of gathered past years’ financial information. Under it, a

vital range of budgets are included which leads to effective decision making. There are a number

of budgets, several of which are:

Operational budget- It is a form of budget that is related to do the forecast over a certain

amount of time of revenue and expenditures. With the aid of this budget, administrators

can predict the volume of material required to execute different activities more

effectively. Objective of this to manage operations and activities of a company in an

effective manner. It becomes possible by correct prediction of further income and

expenses of a particular time period. In the context of above Creams limited, their

There are different types of techniques in order to produce financial statements. It

depends on companies that which method they implement for financial reports (Armitage, Webb

and Glynn, 2016). In the above report, profit and loss accounts are produced on the behalf of two

methods which are marginal and absorption costing. Under both of these techniques value of net

profit is different due to way of taking expenses. Apart from it, various kinds of labor and

material variances are calculated in accordance of particular formula. For instance under labor

variance four types of variances are calculated such as labor price, quantity etc. same as under

material variance too, different types of variances are computed as per given scenario.

D2 Interpretation of produced income statement.

In accordance of produced financial system under different methods this can be find out

that net profit is 50000 and -25000 under marginal costing. As well as under absorption costing

profit is also similar that is of 50000 and -25000 for similar time period. In addition, variances

are also computed including labor and material variances.

TASK 3

P4. Benefits and drawbacks of different types of planning tools used for budgetary control.

Budgetary control- It can be described as a way to manage financial and anti-financial

performance across a number of budgets (Mohamed, Kerosi and Tirimba, 2016). In this

dimension of the budgetary function, the managers of businesses undertake corrective measures

to produce more results by means of such financial plans. In other words, this can be defined as

process of making budgets on the basis of gathered past years’ financial information. Under it, a

vital range of budgets are included which leads to effective decision making. There are a number

of budgets, several of which are:

Operational budget- It is a form of budget that is related to do the forecast over a certain

amount of time of revenue and expenditures. With the aid of this budget, administrators

can predict the volume of material required to execute different activities more

effectively. Objective of this to manage operations and activities of a company in an

effective manner. It becomes possible by correct prediction of further income and

expenses of a particular time period. In the context of above Creams limited, their

administrators take corrective steps to handle multiple organizational forms. Specific

strategies are used in this budget, for example:

Variance analysis- It is related to differentiating between actual results and estimates.

Standard costing- This is a form of method that is linked to the calculation of incremental

costs and used as a comparison measure.

Benefits- This budget is valuable for businesses to monitor their actual regular spending.

As well as it is useful for companies to ensure proper utilization of resources and capital

into various operations.

Drawbacks- This budget has constraints as well as the benefit. For example, this budget

takes so much time and money which is impossible to achieve for small companies.

Flexible budget- This is a financial plan that fluctuates in terms of output and quantity

shift (Boyabatlı, Leng and Toktay, 2016). This budget is widely used in those companies

in which activities are expected to change in future. One of the key features of this budget

is that it is user friendly. This is so because it can be updated whenever company needs.

Like the above-mentioned firm, this budget is designed for potential fluctuating

operations by accountants.

Advantages- It is so simple to use, because companies can track their everyday expenses

and revenue. As well as this budget can be applied in any kinds of business. There are no

any specifications to apply this budget, even small companies can also adopt this budget.

Disadvantage- This adds to data theft, because users can conceal real data by modifying it

every day. Along with this budget needs to be updated on daily or monthly basis that

leads to complexity.

Capital budget- This can be described as a kind of budget that is linked to the output

assessment of lengthy-term investments such as machinery, plants and many more (Dong

and Smith, 2017). The Finance Department takes important long-term investment choices

on the basis of this budget. Basically, this budget is used in those companies which make

large financial investments into various projects. This is so because it guides to finance

managers to take corrective actions before making a higher capital investment.

Throughout the above-mentioned Creams limited, their finance team has used this budget

for disciplinary steps in order to control financial capital properly. As well as they allow

strategies are used in this budget, for example:

Variance analysis- It is related to differentiating between actual results and estimates.

Standard costing- This is a form of method that is linked to the calculation of incremental

costs and used as a comparison measure.

Benefits- This budget is valuable for businesses to monitor their actual regular spending.

As well as it is useful for companies to ensure proper utilization of resources and capital

into various operations.

Drawbacks- This budget has constraints as well as the benefit. For example, this budget

takes so much time and money which is impossible to achieve for small companies.

Flexible budget- This is a financial plan that fluctuates in terms of output and quantity

shift (Boyabatlı, Leng and Toktay, 2016). This budget is widely used in those companies

in which activities are expected to change in future. One of the key features of this budget

is that it is user friendly. This is so because it can be updated whenever company needs.

Like the above-mentioned firm, this budget is designed for potential fluctuating

operations by accountants.

Advantages- It is so simple to use, because companies can track their everyday expenses

and revenue. As well as this budget can be applied in any kinds of business. There are no

any specifications to apply this budget, even small companies can also adopt this budget.

Disadvantage- This adds to data theft, because users can conceal real data by modifying it

every day. Along with this budget needs to be updated on daily or monthly basis that

leads to complexity.

Capital budget- This can be described as a kind of budget that is linked to the output

assessment of lengthy-term investments such as machinery, plants and many more (Dong

and Smith, 2017). The Finance Department takes important long-term investment choices

on the basis of this budget. Basically, this budget is used in those companies which make

large financial investments into various projects. This is so because it guides to finance

managers to take corrective actions before making a higher capital investment.

Throughout the above-mentioned Creams limited, their finance team has used this budget

for disciplinary steps in order to control financial capital properly. As well as they allow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.