Management Accounting Role Evolution: A Critical Literature Review

VerifiedAdded on 2019/09/20

|8

|3043

|312

Essay

AI Summary

This paper critically examines the evolution of management accounting roles, analyzing the shift from traditional functions like cost control and scorekeeping to broader strategic roles in decision-making and planning. The paper is divided into two sections, presenting arguments for and against the changing roles of management accountants, drawing on various scholarly perspectives and literature. It assesses how the adoption of advanced management accounting tools and techniques, such as the balanced scorecard and activity-based costing, has influenced the responsibilities and skills required of management accountants. The analysis explores whether these changes are universally accepted or if traditional techniques remain relevant, considering factors like implementation costs, skill requirements, and the competitive environment. The paper concludes by suggesting that while the role of management accountants has evolved, the extent of this change varies based on the adoption of new tools and techniques within specific organizations.

Abstract

The prime objective of the paper is to explain the traditional management accounting and how it

has evolved. The paper critically evaluated the role of management accountants present in the

firm for examining the change induced by using emerging advanced and sophisticated

management accounting tools and techniques in their roles. The paper assessed the roles which

was perceived traditionally to be as a controller and cost recorded and how their roles have

evolved to broader strategic roles which are important vitally in decision-making and planning.

The paper been separated into two sections where the suggestion from various scholars on the

roles being changed and not changed have been mentioned. The paper can be considered as a

modest study of various literature works for identification of reasons as to why some scholars

have suggested that the role of management accountants have changed and some disagree with

the same. The paper attempts to evaluate critically the various sets of arguments. In order to

assess their roles, the roles, activities and skill requirements of the management accountants have

been studied.

Introduction

The changes being incorporated in the recent years in the role of management accountants have

been argued strongly in the academic literature due to the development of various emerging

advanced and sophisticated management accounting (MA) systems, tools and techniques

(Guilding, Cravens and Tayles 2000; Tsamenyi, Cullen and Gonzalez 2006; Scapens and

Jazayeri2003). The emerging management accounting techniques like the balanced scorecard

(BSC), activity-based costing (ABC), strategic pricing, quality costing, strategic management

accounting (SMA), throughput costing etc. have been investigated and examined by various

researchers and academics (Atkinson, Balakrishnan, Booth, Cote, Groot, Malmi, Roberts, Uliana

and Wu 1997;Emsley 2005). The acceptance of the management accounting tools being

mentioned above and the inherent skills being demanded from the management accountants have

been argues in favor and against the motion (Yazdifar and Tsamenyi 2005; Kennedy and

Sorensen 2006).

The applications of these management accounting tools and techniques have been contributed to

the change in the roles of all the management accountants by becoming a vital member of the

organization participating in the decision-making team and being a strategic planner as compared

to the traditional functions of the cost controllers and the scorekeepers. (Seal, Cullen, Dunlop,

Berry and Ahmed 1999; Burns, Ezzamel and Scrapens 1999). The effectiveness of the

management accountants tools and techniques have been evaluated by various scholars (Haka

and Heitger 2004), and how these tools have been adopted in the firms and organization as

opposed to the counterpart traditional tools (Joshi 2001; Crenhall and Langfield-Smith 1998a).

Further the preferences and attitudes of the managers regarding the realized and perceived

benefited were also derived by various study from using the specific tools (Guilding, Cravens

and Tayles 2000; Adler, Everett and Waldron 2000).

Arguments In Favor of the Changing Role

Earlier it was seen that the management accountants were functioning as support staff for all the

decision makers but with the emergence of various tools and techniques, their roles is seen to

The prime objective of the paper is to explain the traditional management accounting and how it

has evolved. The paper critically evaluated the role of management accountants present in the

firm for examining the change induced by using emerging advanced and sophisticated

management accounting tools and techniques in their roles. The paper assessed the roles which

was perceived traditionally to be as a controller and cost recorded and how their roles have

evolved to broader strategic roles which are important vitally in decision-making and planning.

The paper been separated into two sections where the suggestion from various scholars on the

roles being changed and not changed have been mentioned. The paper can be considered as a

modest study of various literature works for identification of reasons as to why some scholars

have suggested that the role of management accountants have changed and some disagree with

the same. The paper attempts to evaluate critically the various sets of arguments. In order to

assess their roles, the roles, activities and skill requirements of the management accountants have

been studied.

Introduction

The changes being incorporated in the recent years in the role of management accountants have

been argued strongly in the academic literature due to the development of various emerging

advanced and sophisticated management accounting (MA) systems, tools and techniques

(Guilding, Cravens and Tayles 2000; Tsamenyi, Cullen and Gonzalez 2006; Scapens and

Jazayeri2003). The emerging management accounting techniques like the balanced scorecard

(BSC), activity-based costing (ABC), strategic pricing, quality costing, strategic management

accounting (SMA), throughput costing etc. have been investigated and examined by various

researchers and academics (Atkinson, Balakrishnan, Booth, Cote, Groot, Malmi, Roberts, Uliana

and Wu 1997;Emsley 2005). The acceptance of the management accounting tools being

mentioned above and the inherent skills being demanded from the management accountants have

been argues in favor and against the motion (Yazdifar and Tsamenyi 2005; Kennedy and

Sorensen 2006).

The applications of these management accounting tools and techniques have been contributed to

the change in the roles of all the management accountants by becoming a vital member of the

organization participating in the decision-making team and being a strategic planner as compared

to the traditional functions of the cost controllers and the scorekeepers. (Seal, Cullen, Dunlop,

Berry and Ahmed 1999; Burns, Ezzamel and Scrapens 1999). The effectiveness of the

management accountants tools and techniques have been evaluated by various scholars (Haka

and Heitger 2004), and how these tools have been adopted in the firms and organization as

opposed to the counterpart traditional tools (Joshi 2001; Crenhall and Langfield-Smith 1998a).

Further the preferences and attitudes of the managers regarding the realized and perceived

benefited were also derived by various study from using the specific tools (Guilding, Cravens

and Tayles 2000; Adler, Everett and Waldron 2000).

Arguments In Favor of the Changing Role

Earlier it was seen that the management accountants were functioning as support staff for all the

decision makers but with the emergence of various tools and techniques, their roles is seen to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have evolved from serving as internal customers directly to the strategic planner and business

partners. Now that the management accountants are equal member of the decision making

system, they have the authority and responsibility for telling the operating executives and the

various types of information which they may or may not consider relevant to the business

decisions and they also have the authority to improve the quality of decisions, if they desire to do

so (Zimmerman 2009: 13).

The researchers like Emsley 2005 and Abernethy and Brownell 1999 suggest that due to inherent

relationship of Mas with diverse array of disciplines of management, it might be suggested that

the use of tools and techniques can help in expanding the tasks of management accountants from

bean counting, score keeping, cost controlling to a wider strategic and multi-disciplinary roles.

For example, the BSC or Balance Scorecard is not merely a performance measurement

framework in the organization but is used as a comprehensive strategic planning system,

sustaining the ability for transforming and improvement, enabling all the Mas in recognizing the

image of organization in customers’ eye and for focusing on the critical business processes.

(Kaplan and Norton 1992; Silk 1998).

This indirectly suggests the fact that the management accountants spend more time in

classifying, identifying activities and analyzing the costs. Further they have to allot these costs to

procurement, designing, distribution and marketing of products and services (Cardinaels et al.

2004). Therefore the accountants have to assess the system of products, marketing,

manufacturing and other work processes of the various departments (Cadez and Guilding 2008).

Additionally, it has been investigated by various manufacturing firms that a varying combination

of various tools and techniques of Mas are used for greater strategic focus (Crenhall and

Langfield-Smith 1998a).

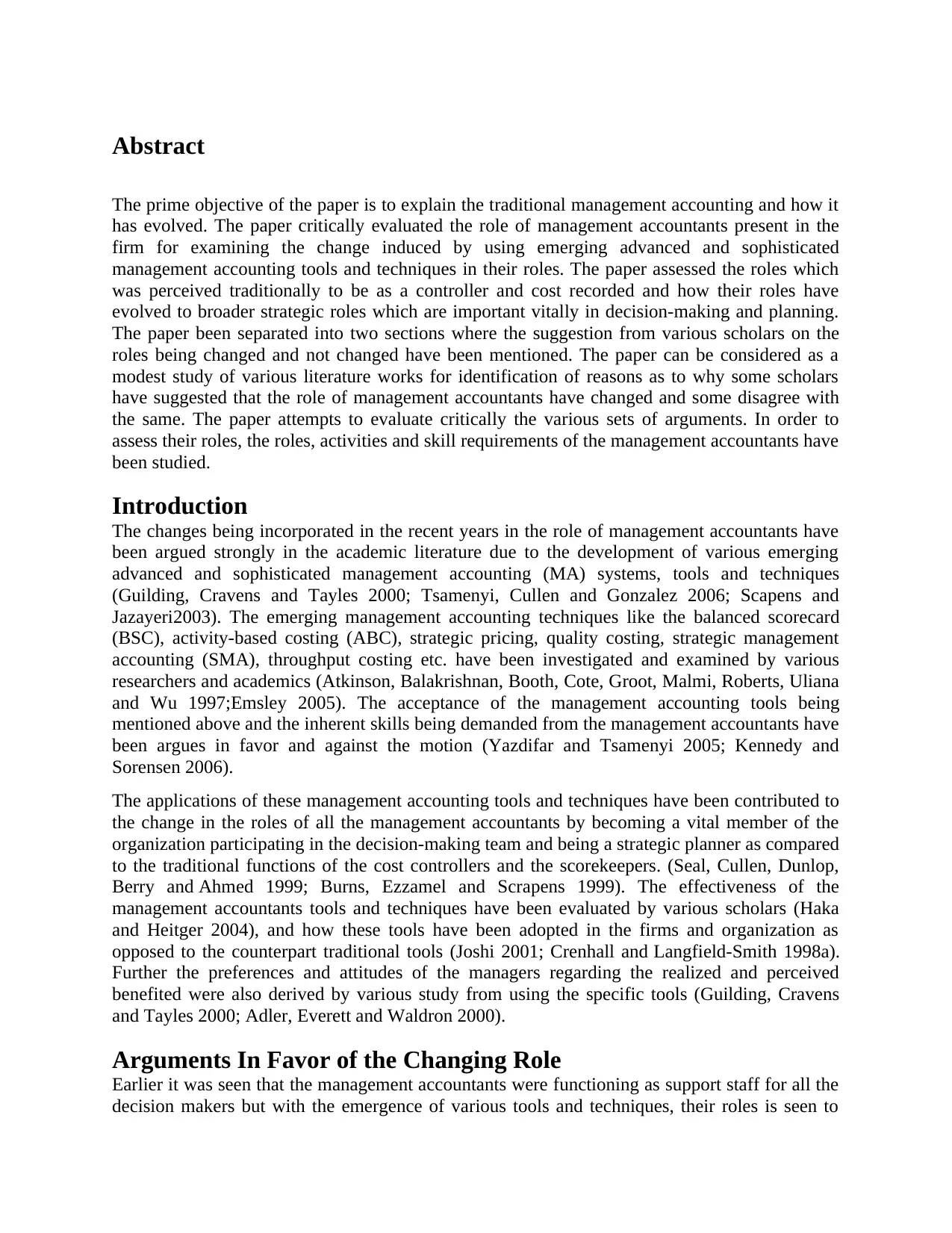

Granlund and Lukka (1998), and Malmi (1999), investigated the transition phase in the practices

of MAs Finland and studied the transformation in their roles and responsibilities from being the

cost controllers to one of the most vital part of the managerial decision-making. The table

provided below compares the usage rate traditional as well as advanced MA techniques.

partners. Now that the management accountants are equal member of the decision making

system, they have the authority and responsibility for telling the operating executives and the

various types of information which they may or may not consider relevant to the business

decisions and they also have the authority to improve the quality of decisions, if they desire to do

so (Zimmerman 2009: 13).

The researchers like Emsley 2005 and Abernethy and Brownell 1999 suggest that due to inherent

relationship of Mas with diverse array of disciplines of management, it might be suggested that

the use of tools and techniques can help in expanding the tasks of management accountants from

bean counting, score keeping, cost controlling to a wider strategic and multi-disciplinary roles.

For example, the BSC or Balance Scorecard is not merely a performance measurement

framework in the organization but is used as a comprehensive strategic planning system,

sustaining the ability for transforming and improvement, enabling all the Mas in recognizing the

image of organization in customers’ eye and for focusing on the critical business processes.

(Kaplan and Norton 1992; Silk 1998).

This indirectly suggests the fact that the management accountants spend more time in

classifying, identifying activities and analyzing the costs. Further they have to allot these costs to

procurement, designing, distribution and marketing of products and services (Cardinaels et al.

2004). Therefore the accountants have to assess the system of products, marketing,

manufacturing and other work processes of the various departments (Cadez and Guilding 2008).

Additionally, it has been investigated by various manufacturing firms that a varying combination

of various tools and techniques of Mas are used for greater strategic focus (Crenhall and

Langfield-Smith 1998a).

Granlund and Lukka (1998), and Malmi (1999), investigated the transition phase in the practices

of MAs Finland and studied the transformation in their roles and responsibilities from being the

cost controllers to one of the most vital part of the managerial decision-making. The table

provided below compares the usage rate traditional as well as advanced MA techniques.

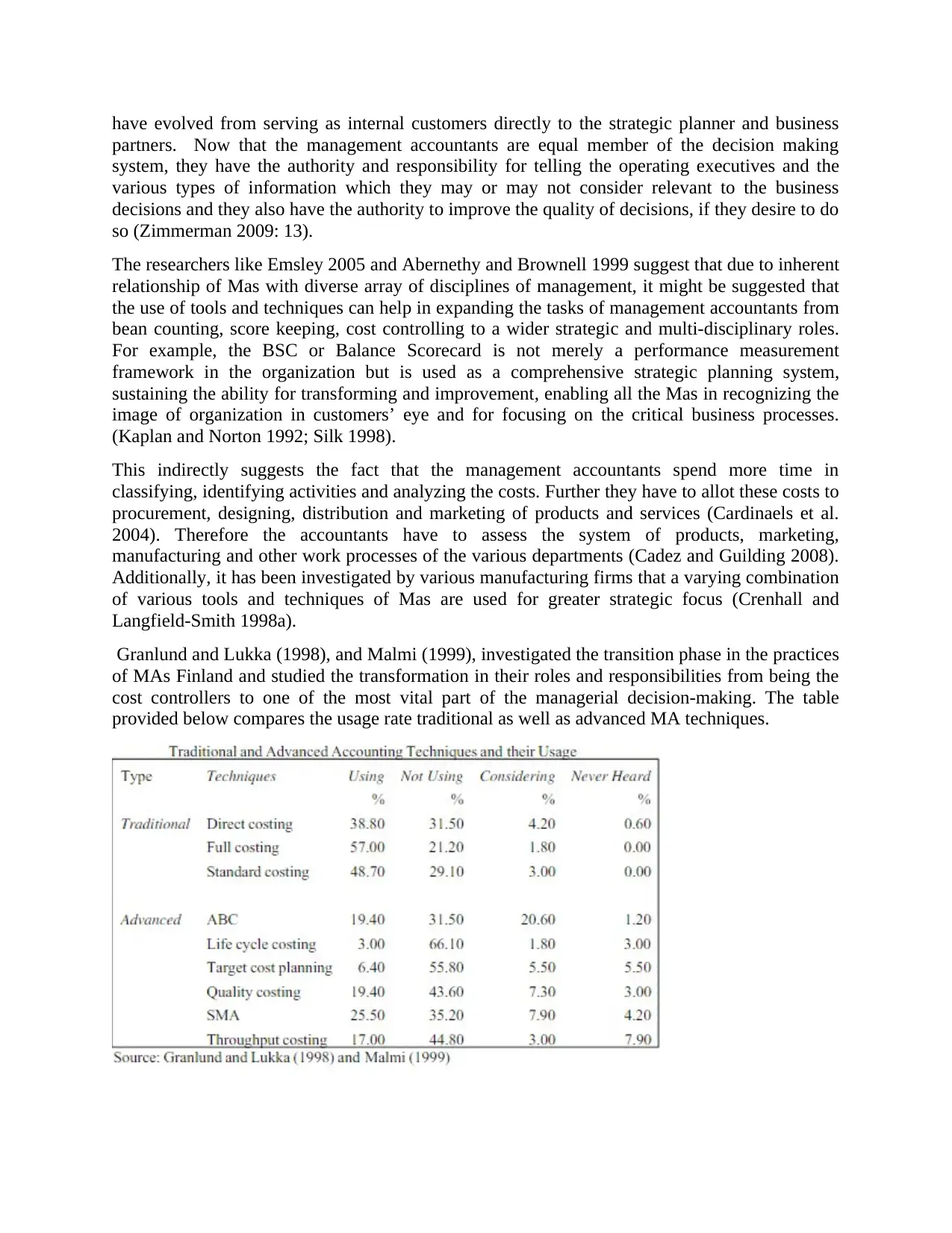

Similarly, a study by Yazdifar and Tsamenyi’s (2005) estimated that one of the most important

skill required in the Mas was the business performance evaluation. This factor continues to

remain the most important task for MAs in future. The other strategic tasks and requirements

were estimated to be planning and managing operations of the budget, cost and financial control

and profit improvement.

skill required in the Mas was the business performance evaluation. This factor continues to

remain the most important task for MAs in future. The other strategic tasks and requirements

were estimated to be planning and managing operations of the budget, cost and financial control

and profit improvement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

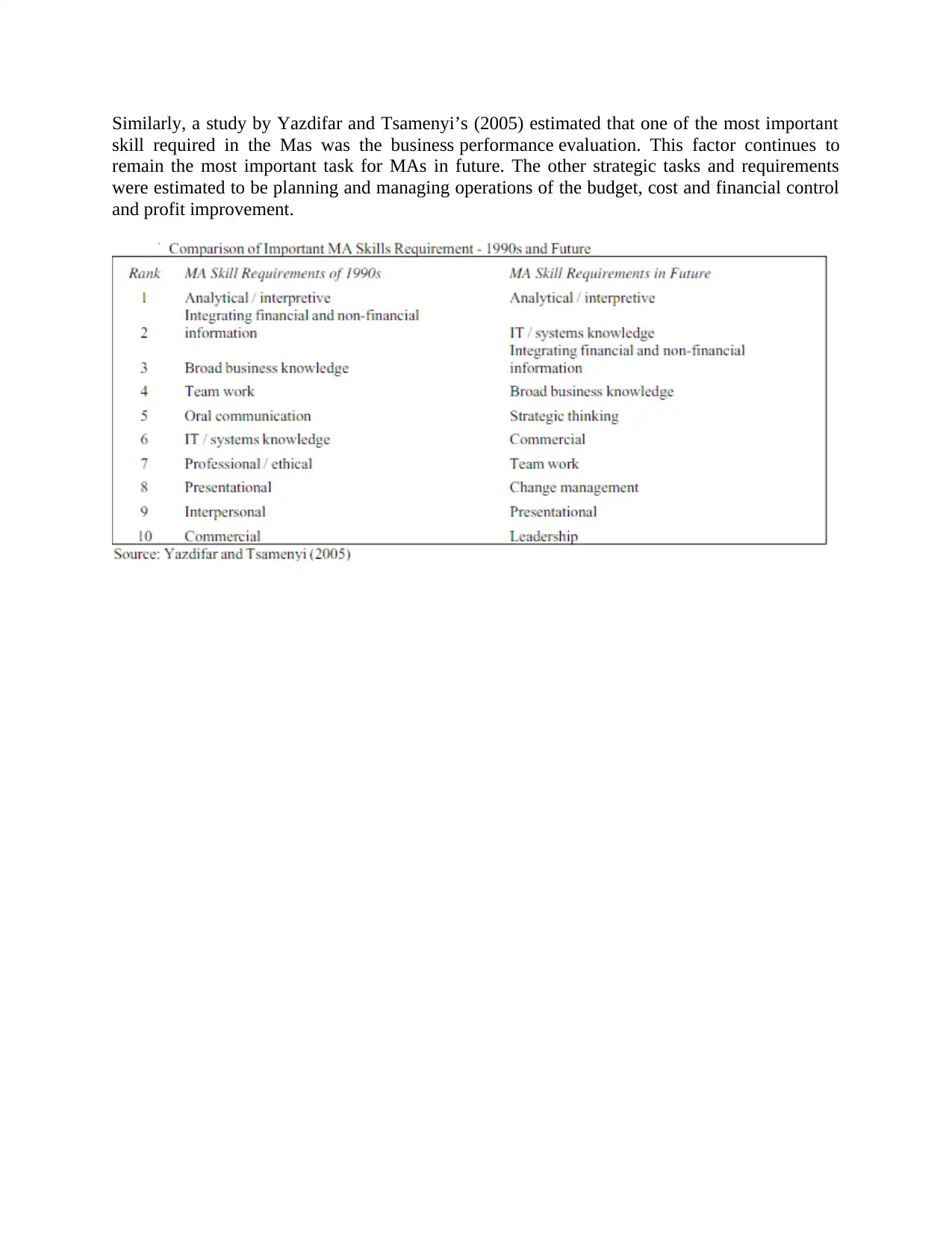

Therefore it can be estimated that the Management accountants are positioned in their respective

teams for solving intricate issues and problems and for improving esiting processes. They are

also called for organizational skills and analyzing the quantitative and oral information especially

in the cross-functional team meetings (Kennedy and Sorensen 2006, Nilsson and Rapp 1999).

The same was reported by findings of Crenhall and Langfield-Smith (1998b) who reported that

the management accountants present in the firms have adopted the team based structure which is

imperative for adapting to the authority and skills as compared to the formal hierarchies so as to

be highly effective in the team settings.

Arguments against the Changing Role

With the organization being highly centered on the MA tools and techniques, their benefits are

usually seen to be over emphasized. According to Yazdifar and Tsamenyi (2005) the benefits of

implementation of such tools have not always outweighed the cost of implementation. In

developing countries, the adoption rate for new MA tools is seen to be quite low (Scapens 2000,

Yazdifar and Tsamenyi 2005) suggesting that there is no drive to widen the roles of management

accountants. There are various factors that are responsible for lower probability of adoption of

the new techniques like the requirement of extensive data extraction from various divisions,

teams for solving intricate issues and problems and for improving esiting processes. They are

also called for organizational skills and analyzing the quantitative and oral information especially

in the cross-functional team meetings (Kennedy and Sorensen 2006, Nilsson and Rapp 1999).

The same was reported by findings of Crenhall and Langfield-Smith (1998b) who reported that

the management accountants present in the firms have adopted the team based structure which is

imperative for adapting to the authority and skills as compared to the formal hierarchies so as to

be highly effective in the team settings.

Arguments against the Changing Role

With the organization being highly centered on the MA tools and techniques, their benefits are

usually seen to be over emphasized. According to Yazdifar and Tsamenyi (2005) the benefits of

implementation of such tools have not always outweighed the cost of implementation. In

developing countries, the adoption rate for new MA tools is seen to be quite low (Scapens 2000,

Yazdifar and Tsamenyi 2005) suggesting that there is no drive to widen the roles of management

accountants. There are various factors that are responsible for lower probability of adoption of

the new techniques like the requirement of extensive data extraction from various divisions,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

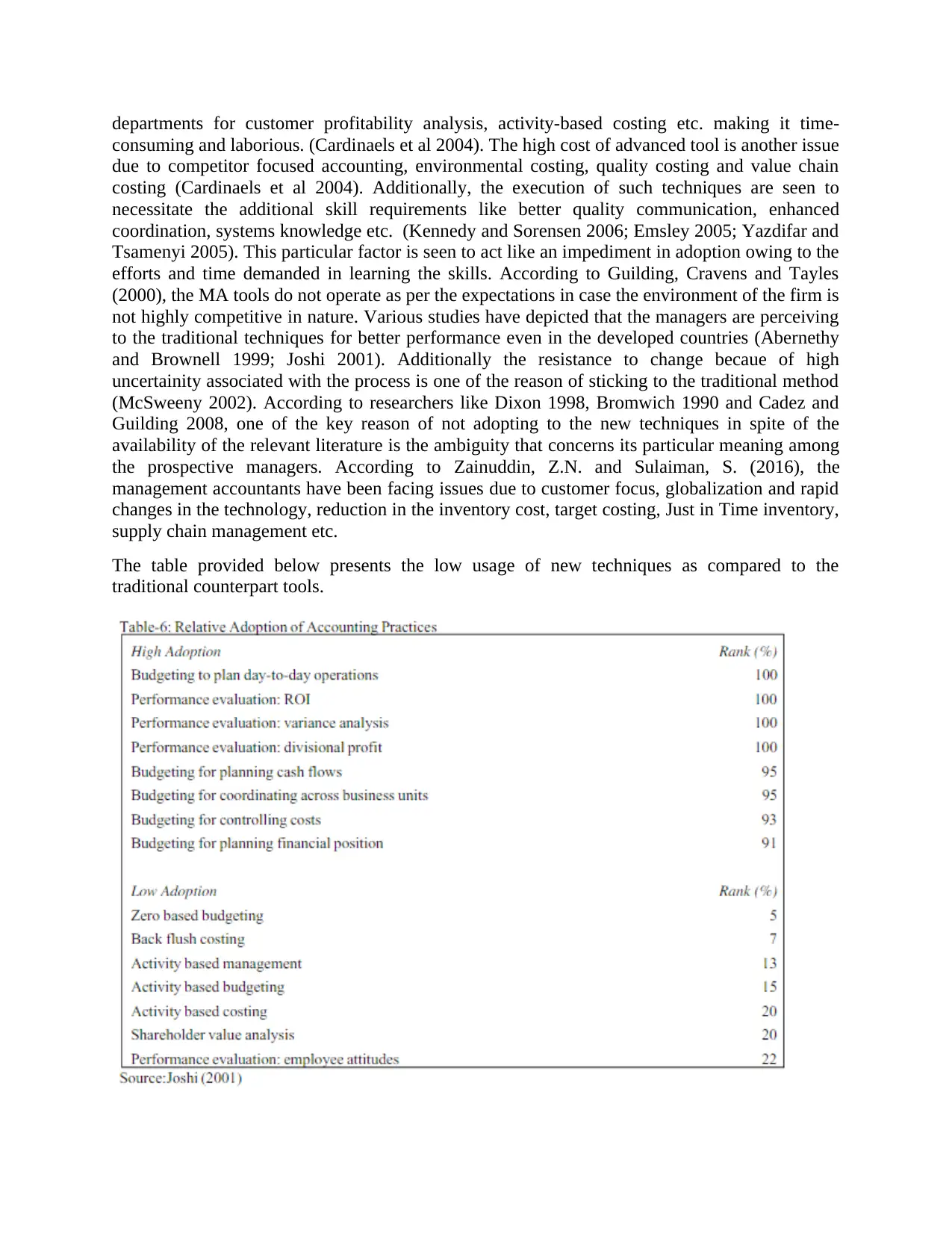

departments for customer profitability analysis, activity-based costing etc. making it time-

consuming and laborious. (Cardinaels et al 2004). The high cost of advanced tool is another issue

due to competitor focused accounting, environmental costing, quality costing and value chain

costing (Cardinaels et al 2004). Additionally, the execution of such techniques are seen to

necessitate the additional skill requirements like better quality communication, enhanced

coordination, systems knowledge etc. (Kennedy and Sorensen 2006; Emsley 2005; Yazdifar and

Tsamenyi 2005). This particular factor is seen to act like an impediment in adoption owing to the

efforts and time demanded in learning the skills. According to Guilding, Cravens and Tayles

(2000), the MA tools do not operate as per the expectations in case the environment of the firm is

not highly competitive in nature. Various studies have depicted that the managers are perceiving

to the traditional techniques for better performance even in the developed countries (Abernethy

and Brownell 1999; Joshi 2001). Additionally the resistance to change becaue of high

uncertainity associated with the process is one of the reason of sticking to the traditional method

(McSweeny 2002). According to researchers like Dixon 1998, Bromwich 1990 and Cadez and

Guilding 2008, one of the key reason of not adopting to the new techniques in spite of the

availability of the relevant literature is the ambiguity that concerns its particular meaning among

the prospective managers. According to Zainuddin, Z.N. and Sulaiman, S. (2016), the

management accountants have been facing issues due to customer focus, globalization and rapid

changes in the technology, reduction in the inventory cost, target costing, Just in Time inventory,

supply chain management etc.

The table provided below presents the low usage of new techniques as compared to the

traditional counterpart tools.

consuming and laborious. (Cardinaels et al 2004). The high cost of advanced tool is another issue

due to competitor focused accounting, environmental costing, quality costing and value chain

costing (Cardinaels et al 2004). Additionally, the execution of such techniques are seen to

necessitate the additional skill requirements like better quality communication, enhanced

coordination, systems knowledge etc. (Kennedy and Sorensen 2006; Emsley 2005; Yazdifar and

Tsamenyi 2005). This particular factor is seen to act like an impediment in adoption owing to the

efforts and time demanded in learning the skills. According to Guilding, Cravens and Tayles

(2000), the MA tools do not operate as per the expectations in case the environment of the firm is

not highly competitive in nature. Various studies have depicted that the managers are perceiving

to the traditional techniques for better performance even in the developed countries (Abernethy

and Brownell 1999; Joshi 2001). Additionally the resistance to change becaue of high

uncertainity associated with the process is one of the reason of sticking to the traditional method

(McSweeny 2002). According to researchers like Dixon 1998, Bromwich 1990 and Cadez and

Guilding 2008, one of the key reason of not adopting to the new techniques in spite of the

availability of the relevant literature is the ambiguity that concerns its particular meaning among

the prospective managers. According to Zainuddin, Z.N. and Sulaiman, S. (2016), the

management accountants have been facing issues due to customer focus, globalization and rapid

changes in the technology, reduction in the inventory cost, target costing, Just in Time inventory,

supply chain management etc.

The table provided below presents the low usage of new techniques as compared to the

traditional counterpart tools.

Lord (1996) and Dixon (1998) have stated that the perceived benefits of the Management

Accountant can easily be achieved even in the absence of any MA tool or process therefore the

overall importance of the emerging MA framework can easily be diluted. Similarly, studies have

reported that various MA tools are under-utilized owing to extensive information demands and

lower benefits of these techniques as compared to the traditional techniques (Crenhall and

Langfield-Smith 1998a, b; Joshi 2001). Therefore, the management accountants should go

beyond their own traditional responsibilities and roles and play as a strategists on their own in

spite on deeding on the sophisticated MA tools.

The Verdict

It is difficult to attain an absolute reconciliation among the two arguments presented in the study.

The modest reconciliation that can be drawn from the study is that the role of management

accountants have gradually changed in the recent years with their immense importance released

in the industry (Kennedy and Sorensen 2006). If the transition is not as steep as from the cost

controller to the full-fledged strategic planner, then at least to a critical role player who is

responsible for analyzing, planning, classifying as well as controlling the cost (Zimmerman

2009).

According to Emsley 2005, their roles have changed from coordinating the outcome towards

assisting in the formulation of critical strategy. It has also been recognized that the acceptance of

the emerging and sophisticated MA tools is quite low (Joshi2001; Yazdifar and Tsamenyi 2005)

and majority of the organization still prefer the traditional techniques to be highly beneficial as

compared to these tools. Although there emergence has ensured that the role of current

management accountants is not going to be the same again (Malmi 1999). However, ti has to be

considered that the smaller firms are avoiding the implementation of such tools and one can

aruge that the role of management accountants have changed proportionally to the degree of

using the tools and their adoption in the specific organizations only. The same cannot be

generalized for all the management accountants (Shank 1989).

Conclusion

One must acknowledge the fact that the business is a dynamic discipline where everything is

bound to change (McSweeny 2009). The role of management accountants has been severely

affected by the emergence and development of several advanced MA techniques. One must

recognize that their benefits are usually over-emphasized and they have a plethora drawbacks

(Lord 1996), and the organizations have been using these tools immensely (Cadez and Guilding

2008). The greater amount of use of such tools is bound to enhance the importance of the

management accountants and their role in the firms in the near future. However, with the

emergence of such techniques, the management accountants are also facing various challenges.

The issues of intense competition and globalization will shift the focus of managements from

core activities and needs of the customers (Zainuddin, Z.N. and Sulaiman, S., 2016).

Accountant can easily be achieved even in the absence of any MA tool or process therefore the

overall importance of the emerging MA framework can easily be diluted. Similarly, studies have

reported that various MA tools are under-utilized owing to extensive information demands and

lower benefits of these techniques as compared to the traditional techniques (Crenhall and

Langfield-Smith 1998a, b; Joshi 2001). Therefore, the management accountants should go

beyond their own traditional responsibilities and roles and play as a strategists on their own in

spite on deeding on the sophisticated MA tools.

The Verdict

It is difficult to attain an absolute reconciliation among the two arguments presented in the study.

The modest reconciliation that can be drawn from the study is that the role of management

accountants have gradually changed in the recent years with their immense importance released

in the industry (Kennedy and Sorensen 2006). If the transition is not as steep as from the cost

controller to the full-fledged strategic planner, then at least to a critical role player who is

responsible for analyzing, planning, classifying as well as controlling the cost (Zimmerman

2009).

According to Emsley 2005, their roles have changed from coordinating the outcome towards

assisting in the formulation of critical strategy. It has also been recognized that the acceptance of

the emerging and sophisticated MA tools is quite low (Joshi2001; Yazdifar and Tsamenyi 2005)

and majority of the organization still prefer the traditional techniques to be highly beneficial as

compared to these tools. Although there emergence has ensured that the role of current

management accountants is not going to be the same again (Malmi 1999). However, ti has to be

considered that the smaller firms are avoiding the implementation of such tools and one can

aruge that the role of management accountants have changed proportionally to the degree of

using the tools and their adoption in the specific organizations only. The same cannot be

generalized for all the management accountants (Shank 1989).

Conclusion

One must acknowledge the fact that the business is a dynamic discipline where everything is

bound to change (McSweeny 2009). The role of management accountants has been severely

affected by the emergence and development of several advanced MA techniques. One must

recognize that their benefits are usually over-emphasized and they have a plethora drawbacks

(Lord 1996), and the organizations have been using these tools immensely (Cadez and Guilding

2008). The greater amount of use of such tools is bound to enhance the importance of the

management accountants and their role in the firms in the near future. However, with the

emergence of such techniques, the management accountants are also facing various challenges.

The issues of intense competition and globalization will shift the focus of managements from

core activities and needs of the customers (Zainuddin, Z.N. and Sulaiman, S., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abernethy, M.A. and P. Brownell. 1999. The Role of Budgets in Organizations Facing Strategic

Change: An Exploratory Study. Accounting, Organizations and Society, 24(3): 189-204.

Adler, R., A. M. Everett and M. Waldron. 2000. Advanced Management Accounting Techniques

in Manufacturing: Utilization, Benefits, and Barriers to Implementation. Accounting Forum,

24(2):131-149

Burns, J., Ezzamel, M. and Scapens, R., 1999. Management accounting change in the

UK. MANAGEMENT ACCOUNTING-LONDON-, 77, pp.28-32.

Cadez, S. and Guilding, C., 2008. An exploratory investigation of an integrated contingency

model of strategic management accounting. Accounting, organizations and society, 33(7),

pp.836-863.

Cardinaels, E., 2008. The interplay between cost accounting knowledge and presentation formats

in cost-based decision-making. Accounting, Organizations and Society, 33(6), pp.582-602.

Crenhall, R.H. and K. Langfield-Smith. 1998b. Factors Influencing The Role of Management

Accounting inThe Development of Performance Measures Within Organizational Change

Programs. Management Accounting Research, 9: 361-386

Crenhall, R.H. and K. Langfield-Smith. 1998a. Adoption and Benefits of Management

Accounting Practices:An Australian Study. Management Accounting Research, 9: 1-19.

Dixon, R., 1998. Accounting for strategic management: a practical application. Long Range

Planning, 31(2), pp.272-279.

Emsley, D., 2005. Restructuring the management accounting function: A note on the effect of

role involvement on innovativeness. Management Accounting Research, 16(2), pp.157-177.

Granlund, M. and Lukka, K., 1998. It's a small world of management accounting

practices. Journal of management accounting research, 10, p.153.

Guilding, C., 1999. Competitor-focused accounting: an exploratory note. Accounting,

Organizations and Society, 24(7), pp.583-595.

Haka, S.F. and D.L. Heitger. 2004. International Managerial Accounting Research: A

ContractingFramework and Opportunities. The International Journal of Accounting, 39(1): 21-69

Joshi, P.L., 2001. The international diffusion of new management accounting practices: the case

of India. Journal of International Accounting, Auditing and Taxation, 10(1), pp.85-109.

Kaplan, R.S. and Norton, D.P., 2001. Transforming the balanced scorecard from performance

measurement to strategic management: Part II. Accounting Horizons, 15(2), pp.147-160.

Kennedy, F.A. and Sorensen, J.E., 2006. Enabling the management accountant to become a

business partner: Organizational and verbal analysis toolkit. Journal of accounting

education, 24(2), pp.149-171.

Abernethy, M.A. and P. Brownell. 1999. The Role of Budgets in Organizations Facing Strategic

Change: An Exploratory Study. Accounting, Organizations and Society, 24(3): 189-204.

Adler, R., A. M. Everett and M. Waldron. 2000. Advanced Management Accounting Techniques

in Manufacturing: Utilization, Benefits, and Barriers to Implementation. Accounting Forum,

24(2):131-149

Burns, J., Ezzamel, M. and Scapens, R., 1999. Management accounting change in the

UK. MANAGEMENT ACCOUNTING-LONDON-, 77, pp.28-32.

Cadez, S. and Guilding, C., 2008. An exploratory investigation of an integrated contingency

model of strategic management accounting. Accounting, organizations and society, 33(7),

pp.836-863.

Cardinaels, E., 2008. The interplay between cost accounting knowledge and presentation formats

in cost-based decision-making. Accounting, Organizations and Society, 33(6), pp.582-602.

Crenhall, R.H. and K. Langfield-Smith. 1998b. Factors Influencing The Role of Management

Accounting inThe Development of Performance Measures Within Organizational Change

Programs. Management Accounting Research, 9: 361-386

Crenhall, R.H. and K. Langfield-Smith. 1998a. Adoption and Benefits of Management

Accounting Practices:An Australian Study. Management Accounting Research, 9: 1-19.

Dixon, R., 1998. Accounting for strategic management: a practical application. Long Range

Planning, 31(2), pp.272-279.

Emsley, D., 2005. Restructuring the management accounting function: A note on the effect of

role involvement on innovativeness. Management Accounting Research, 16(2), pp.157-177.

Granlund, M. and Lukka, K., 1998. It's a small world of management accounting

practices. Journal of management accounting research, 10, p.153.

Guilding, C., 1999. Competitor-focused accounting: an exploratory note. Accounting,

Organizations and Society, 24(7), pp.583-595.

Haka, S.F. and D.L. Heitger. 2004. International Managerial Accounting Research: A

ContractingFramework and Opportunities. The International Journal of Accounting, 39(1): 21-69

Joshi, P.L., 2001. The international diffusion of new management accounting practices: the case

of India. Journal of International Accounting, Auditing and Taxation, 10(1), pp.85-109.

Kaplan, R.S. and Norton, D.P., 2001. Transforming the balanced scorecard from performance

measurement to strategic management: Part II. Accounting Horizons, 15(2), pp.147-160.

Kennedy, F.A. and Sorensen, J.E., 2006. Enabling the management accountant to become a

business partner: Organizational and verbal analysis toolkit. Journal of accounting

education, 24(2), pp.149-171.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3,

pp.135-154.

Malmi, T., 1999. Activity-based costing diffusion across organizations: an exploratory empirical

analysis of Finnish firms. Accounting, organizations and society, 24(8), pp.649-672.

McSweeney, B., 2009. The roles of financial asset market failure denial and the economic crisis:

Reflections on accounting and financial theories and practices. Accounting, Organizations and

Society, 34(6), pp.835-848.

Nilsson, F. and Rapp, B., 1999. Implementing business unit strategies: the role of management

control systems. Scandinavian Journal of Management, 15(1), pp.65-88.

Scapens, R.W. and Jazayeri, M., 2003. ERP systems and management accounting change:

opportunities or impacts? A research note. European accounting review, 12(1), pp.201-233.

Seal, W., Cullen, J., Dunlop, A., Berry, T. and Ahmed, M., 1999. Enacting a European supply

chain: a case study on the role of management accounting. Management Accounting

Research, 10(3), pp.303-322.

Shank, J.K., 1989. Strategic cost management: new wine, or just new bottles. Journal of

Management Accounting Research, 1(1), pp.47-65.

Silk, S., 1998. Automating the balanced scorecard. Strategic Finance, 79(11), p.38.

Tsamenyi, M., Cullen, J. and González, J.M.G., 2006. Changes in accounting and financial

information system in a Spanish electricity company: A new institutional theory

analysis. Management Accounting Research, 17(4), pp.409-432.

West, C. and Zimmerman, D.H., 2009. Accounting for doing gender. Gender and society, 23(1),

pp.112-122.

Yazdifar*, H. and Tsamenyi, M., 2005. Management accounting change and the changing roles

of management accountants: a comparative analysis between dependent and independent

organizations. Journal of Accounting & Organizational Change, 1(2), pp.180-198.

Zainuddin, Z.N. and Sulaiman, S., 2016. Challenges Faced by Management Accountants in the

21st Century. Procedia Economics and Finance, 37, pp.466-470.

pp.135-154.

Malmi, T., 1999. Activity-based costing diffusion across organizations: an exploratory empirical

analysis of Finnish firms. Accounting, organizations and society, 24(8), pp.649-672.

McSweeney, B., 2009. The roles of financial asset market failure denial and the economic crisis:

Reflections on accounting and financial theories and practices. Accounting, Organizations and

Society, 34(6), pp.835-848.

Nilsson, F. and Rapp, B., 1999. Implementing business unit strategies: the role of management

control systems. Scandinavian Journal of Management, 15(1), pp.65-88.

Scapens, R.W. and Jazayeri, M., 2003. ERP systems and management accounting change:

opportunities or impacts? A research note. European accounting review, 12(1), pp.201-233.

Seal, W., Cullen, J., Dunlop, A., Berry, T. and Ahmed, M., 1999. Enacting a European supply

chain: a case study on the role of management accounting. Management Accounting

Research, 10(3), pp.303-322.

Shank, J.K., 1989. Strategic cost management: new wine, or just new bottles. Journal of

Management Accounting Research, 1(1), pp.47-65.

Silk, S., 1998. Automating the balanced scorecard. Strategic Finance, 79(11), p.38.

Tsamenyi, M., Cullen, J. and González, J.M.G., 2006. Changes in accounting and financial

information system in a Spanish electricity company: A new institutional theory

analysis. Management Accounting Research, 17(4), pp.409-432.

West, C. and Zimmerman, D.H., 2009. Accounting for doing gender. Gender and society, 23(1),

pp.112-122.

Yazdifar*, H. and Tsamenyi, M., 2005. Management accounting change and the changing roles

of management accountants: a comparative analysis between dependent and independent

organizations. Journal of Accounting & Organizational Change, 1(2), pp.180-198.

Zainuddin, Z.N. and Sulaiman, S., 2016. Challenges Faced by Management Accountants in the

21st Century. Procedia Economics and Finance, 37, pp.466-470.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.