MA514 Business Finance: Melbourne Housing Market Analysis Report

VerifiedAdded on 2023/06/11

|13

|2263

|495

Report

AI Summary

This report provides a detailed analysis of the Melbourne housing market, focusing on historical price trends, income data, and affordability. It includes calculations and assumptions related to future housing prices and income growth, utilizing data from the ABS and ATO tax calculator. The report examines a client's potential borrowing amount, stamp duty, and financial plans with varying upfront payments (20% and 5%). It also assesses the impact of interest rate increments on a lender's capability and outlines potential risks associated with the financial plan. The analysis aims to determine the feasibility of achieving the 'Australian dream' of homeownership, considering factors like income, expenses, and mortgage payments. Desklib offers a range of resources including past papers and solved assignments for students.

Running head: BUSINESS FINANCE

Business finance

Name of the student

Name of the University

Author Note

Business finance

Name of the student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

1. Detection and justification of the historical prices of houses of Melbourne that indicate

assumptions taken regarding future prices:................................................................................2

2. Evaluation of the historical data of Melbourne to justify the assumptions for the income

data:............................................................................................................................................4

3. Detection of the net income through using ATO calculator to detect the home loan rate and

maximum borrowing amount that a client could receive:..........................................................6

4. Calculation of stamp duty related with property purchase at the time of detecting the

affordability of house prices.......................................................................................................8

5. Calculation and presentation of a financial plan with 20% upfront payment and 5% upfront

payment for the loan:.................................................................................................................9

6. Calculation regarding increment of interest rate payment that can destroy lender’s

capability regarding interest rate payment:..............................................................................10

7. Providing the relevant plan along with detailed risk that the assumption regarding financial

plan has entailed.......................................................................................................................11

References:...............................................................................................................................12

Table of Contents

1. Detection and justification of the historical prices of houses of Melbourne that indicate

assumptions taken regarding future prices:................................................................................2

2. Evaluation of the historical data of Melbourne to justify the assumptions for the income

data:............................................................................................................................................4

3. Detection of the net income through using ATO calculator to detect the home loan rate and

maximum borrowing amount that a client could receive:..........................................................6

4. Calculation of stamp duty related with property purchase at the time of detecting the

affordability of house prices.......................................................................................................8

5. Calculation and presentation of a financial plan with 20% upfront payment and 5% upfront

payment for the loan:.................................................................................................................9

6. Calculation regarding increment of interest rate payment that can destroy lender’s

capability regarding interest rate payment:..............................................................................10

7. Providing the relevant plan along with detailed risk that the assumption regarding financial

plan has entailed.......................................................................................................................11

References:...............................................................................................................................12

2BUSINESS FINANCE

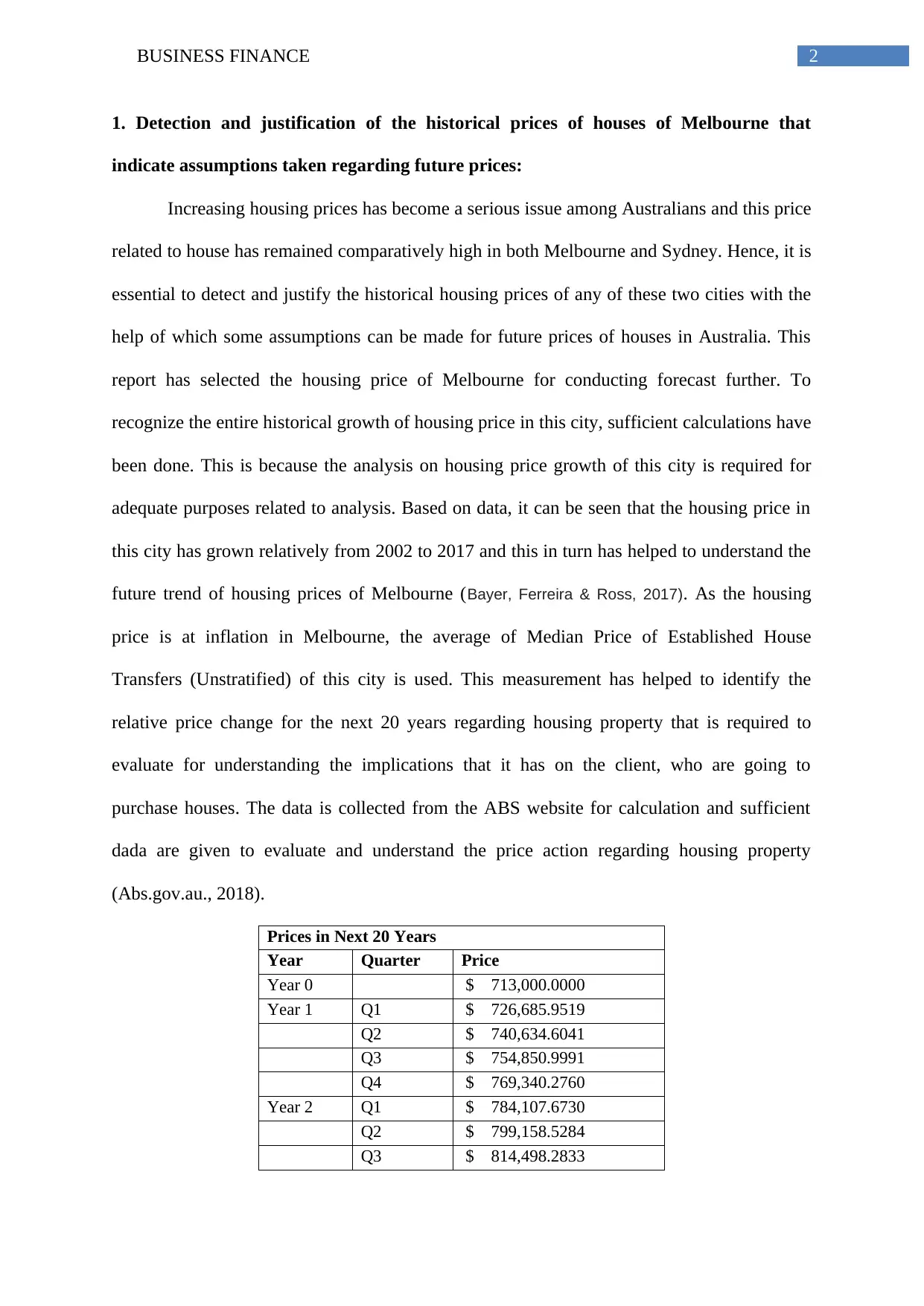

1. Detection and justification of the historical prices of houses of Melbourne that

indicate assumptions taken regarding future prices:

Increasing housing prices has become a serious issue among Australians and this price

related to house has remained comparatively high in both Melbourne and Sydney. Hence, it is

essential to detect and justify the historical housing prices of any of these two cities with the

help of which some assumptions can be made for future prices of houses in Australia. This

report has selected the housing price of Melbourne for conducting forecast further. To

recognize the entire historical growth of housing price in this city, sufficient calculations have

been done. This is because the analysis on housing price growth of this city is required for

adequate purposes related to analysis. Based on data, it can be seen that the housing price in

this city has grown relatively from 2002 to 2017 and this in turn has helped to understand the

future trend of housing prices of Melbourne (Bayer, Ferreira & Ross, 2017). As the housing

price is at inflation in Melbourne, the average of Median Price of Established House

Transfers (Unstratified) of this city is used. This measurement has helped to identify the

relative price change for the next 20 years regarding housing property that is required to

evaluate for understanding the implications that it has on the client, who are going to

purchase houses. The data is collected from the ABS website for calculation and sufficient

dada are given to evaluate and understand the price action regarding housing property

(Abs.gov.au., 2018).

Prices in Next 20 Years

Year Quarter Price

Year 0 $ 713,000.0000

Year 1 Q1 $ 726,685.9519

Q2 $ 740,634.6041

Q3 $ 754,850.9991

Q4 $ 769,340.2760

Year 2 Q1 $ 784,107.6730

Q2 $ 799,158.5284

Q3 $ 814,498.2833

1. Detection and justification of the historical prices of houses of Melbourne that

indicate assumptions taken regarding future prices:

Increasing housing prices has become a serious issue among Australians and this price

related to house has remained comparatively high in both Melbourne and Sydney. Hence, it is

essential to detect and justify the historical housing prices of any of these two cities with the

help of which some assumptions can be made for future prices of houses in Australia. This

report has selected the housing price of Melbourne for conducting forecast further. To

recognize the entire historical growth of housing price in this city, sufficient calculations have

been done. This is because the analysis on housing price growth of this city is required for

adequate purposes related to analysis. Based on data, it can be seen that the housing price in

this city has grown relatively from 2002 to 2017 and this in turn has helped to understand the

future trend of housing prices of Melbourne (Bayer, Ferreira & Ross, 2017). As the housing

price is at inflation in Melbourne, the average of Median Price of Established House

Transfers (Unstratified) of this city is used. This measurement has helped to identify the

relative price change for the next 20 years regarding housing property that is required to

evaluate for understanding the implications that it has on the client, who are going to

purchase houses. The data is collected from the ABS website for calculation and sufficient

dada are given to evaluate and understand the price action regarding housing property

(Abs.gov.au., 2018).

Prices in Next 20 Years

Year Quarter Price

Year 0 $ 713,000.0000

Year 1 Q1 $ 726,685.9519

Q2 $ 740,634.6041

Q3 $ 754,850.9991

Q4 $ 769,340.2760

Year 2 Q1 $ 784,107.6730

Q2 $ 799,158.5284

Q3 $ 814,498.2833

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

Q4 $ 830,132.4829

Year 3 Q1 $ 846,066.7792

Q2 $ 862,306.9325

Q3 $ 878,858.8136

Q4 $ 895,728.4061

Year 4 Q1 $ 912,921.8085

Q2 $ 930,445.2363

Q3 $ 948,305.0242

Q4 $ 966,507.6286

Year 5 Q1 $ 985,059.6300

Q2 $ 1,003,967.7348

Q3 $ 1,023,238.7785

Q4 $ 1,042,879.7276

Year 6 Q1 $ 1,062,897.6825

Q2 $ 1,083,299.8797

Q3 $ 1,104,093.6947

Q4 $ 1,125,286.6445

Year 7 Q1 $ 1,146,886.3905

Q2 $ 1,168,900.7412

Q3 $ 1,191,337.6547

Q4 $ 1,214,205.2422

Year 8 Q1 $ 1,237,511.7704

Q2 $ 1,261,265.6646

Q3 $ 1,285,475.5121

Q4 $ 1,310,150.0648

Year 9 Q1 $ 1,335,298.2427

Q2 $ 1,360,929.1369

Q3 $ 1,387,052.0131

Q4 $ 1,413,676.3149

Year 10 Q1 $ 1,440,811.6670

Q2 $ 1,468,467.8791

Q3 $ 1,496,654.9490

Q4 $ 1,525,383.0663

Year 11 Q1 $ 1,554,662.6166

Q2 $ 1,584,504.1844

Q3 $ 1,614,918.5576

Q4 $ 1,645,916.7312

Year 12 Q1 $ 1,677,509.9111

Q2 $ 1,709,709.5184

Q3 $ 1,742,527.1934

Q4 $ 1,775,974.7998

Year 13 Q1 $ 1,810,064.4292

Q2 $ 1,844,808.4050

Q3 $ 1,880,219.2874

Q4 $ 830,132.4829

Year 3 Q1 $ 846,066.7792

Q2 $ 862,306.9325

Q3 $ 878,858.8136

Q4 $ 895,728.4061

Year 4 Q1 $ 912,921.8085

Q2 $ 930,445.2363

Q3 $ 948,305.0242

Q4 $ 966,507.6286

Year 5 Q1 $ 985,059.6300

Q2 $ 1,003,967.7348

Q3 $ 1,023,238.7785

Q4 $ 1,042,879.7276

Year 6 Q1 $ 1,062,897.6825

Q2 $ 1,083,299.8797

Q3 $ 1,104,093.6947

Q4 $ 1,125,286.6445

Year 7 Q1 $ 1,146,886.3905

Q2 $ 1,168,900.7412

Q3 $ 1,191,337.6547

Q4 $ 1,214,205.2422

Year 8 Q1 $ 1,237,511.7704

Q2 $ 1,261,265.6646

Q3 $ 1,285,475.5121

Q4 $ 1,310,150.0648

Year 9 Q1 $ 1,335,298.2427

Q2 $ 1,360,929.1369

Q3 $ 1,387,052.0131

Q4 $ 1,413,676.3149

Year 10 Q1 $ 1,440,811.6670

Q2 $ 1,468,467.8791

Q3 $ 1,496,654.9490

Q4 $ 1,525,383.0663

Year 11 Q1 $ 1,554,662.6166

Q2 $ 1,584,504.1844

Q3 $ 1,614,918.5576

Q4 $ 1,645,916.7312

Year 12 Q1 $ 1,677,509.9111

Q2 $ 1,709,709.5184

Q3 $ 1,742,527.1934

Q4 $ 1,775,974.7998

Year 13 Q1 $ 1,810,064.4292

Q2 $ 1,844,808.4050

Q3 $ 1,880,219.2874

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

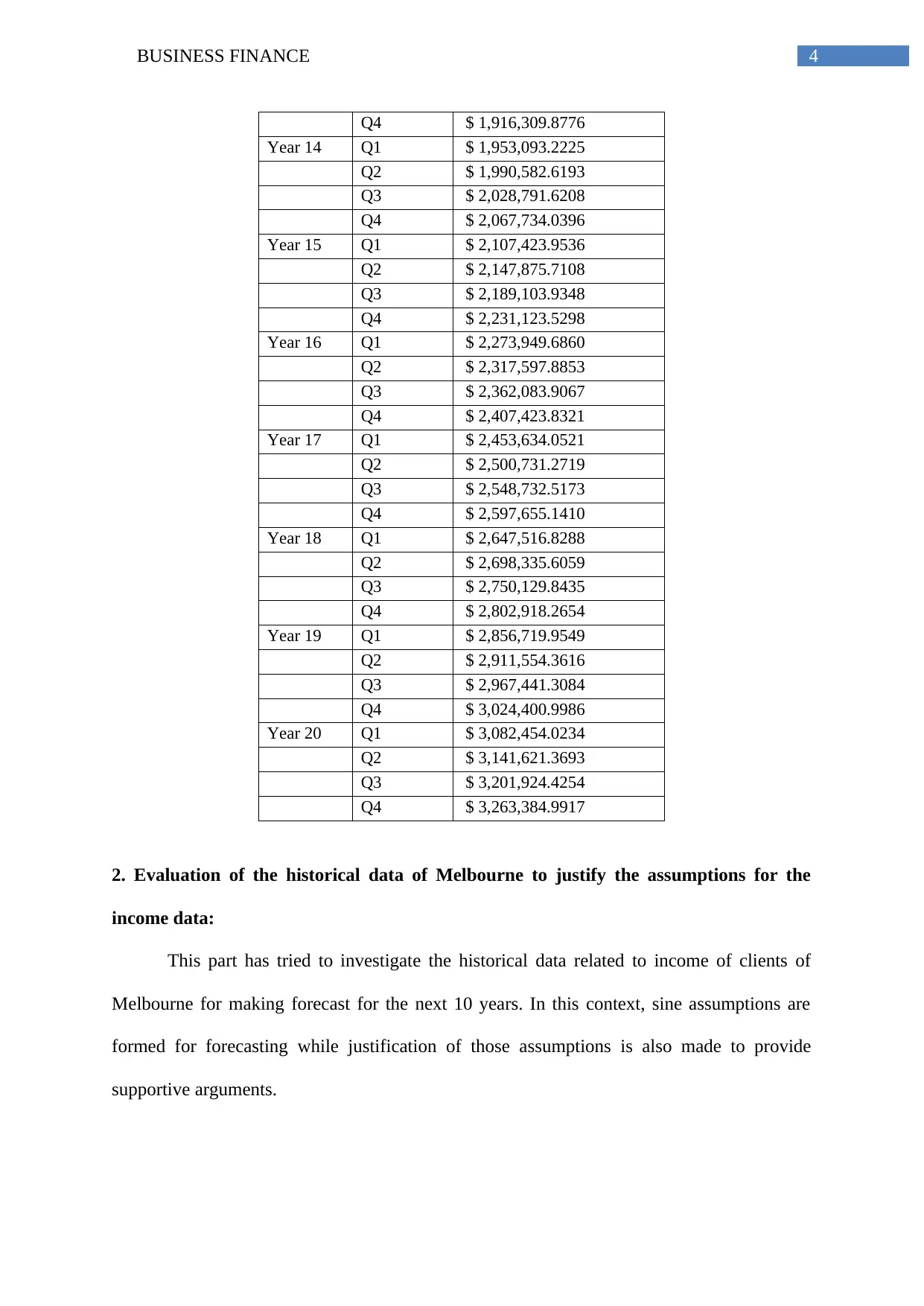

Q4 $ 1,916,309.8776

Year 14 Q1 $ 1,953,093.2225

Q2 $ 1,990,582.6193

Q3 $ 2,028,791.6208

Q4 $ 2,067,734.0396

Year 15 Q1 $ 2,107,423.9536

Q2 $ 2,147,875.7108

Q3 $ 2,189,103.9348

Q4 $ 2,231,123.5298

Year 16 Q1 $ 2,273,949.6860

Q2 $ 2,317,597.8853

Q3 $ 2,362,083.9067

Q4 $ 2,407,423.8321

Year 17 Q1 $ 2,453,634.0521

Q2 $ 2,500,731.2719

Q3 $ 2,548,732.5173

Q4 $ 2,597,655.1410

Year 18 Q1 $ 2,647,516.8288

Q2 $ 2,698,335.6059

Q3 $ 2,750,129.8435

Q4 $ 2,802,918.2654

Year 19 Q1 $ 2,856,719.9549

Q2 $ 2,911,554.3616

Q3 $ 2,967,441.3084

Q4 $ 3,024,400.9986

Year 20 Q1 $ 3,082,454.0234

Q2 $ 3,141,621.3693

Q3 $ 3,201,924.4254

Q4 $ 3,263,384.9917

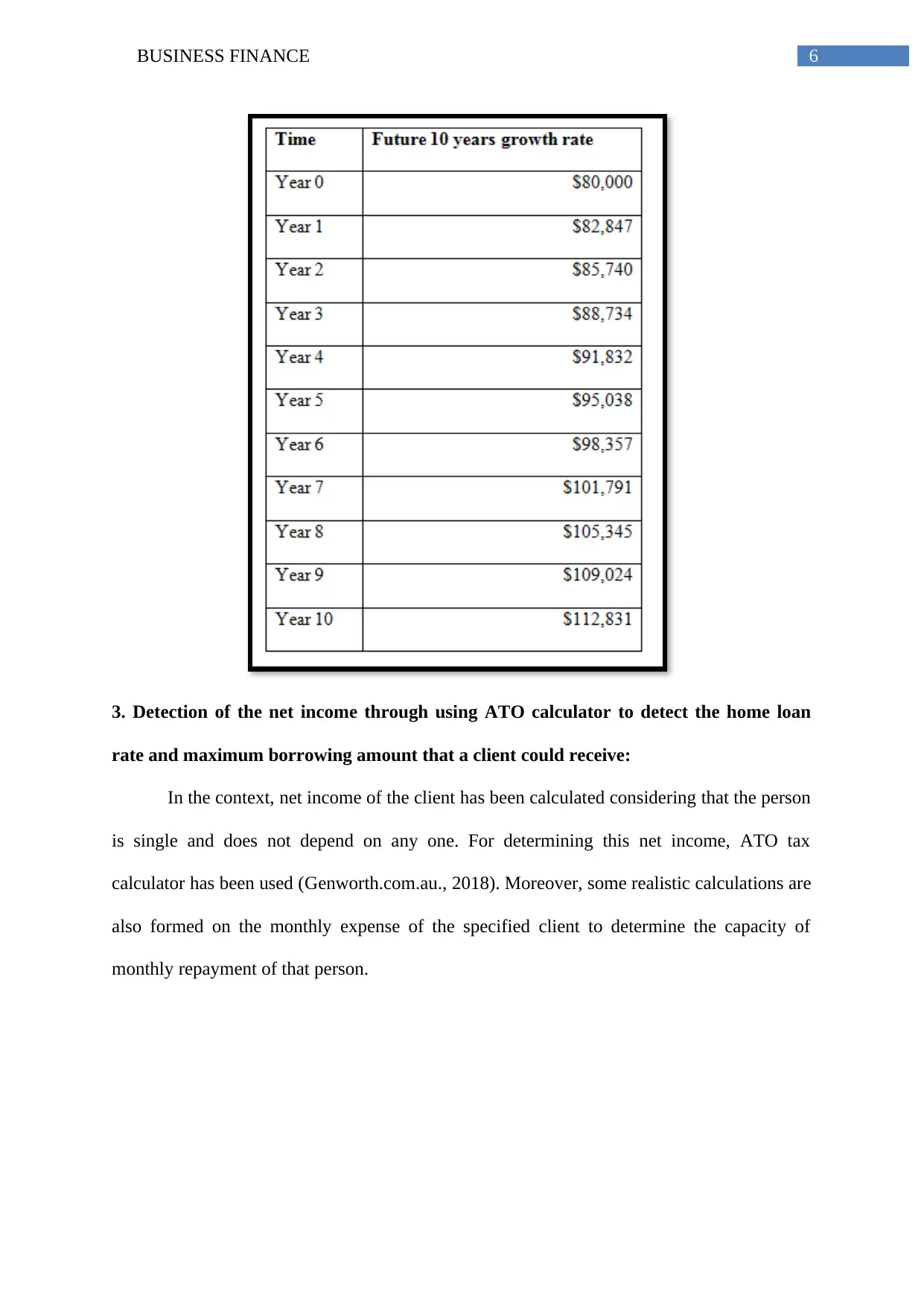

2. Evaluation of the historical data of Melbourne to justify the assumptions for the

income data:

This part has tried to investigate the historical data related to income of clients of

Melbourne for making forecast for the next 10 years. In this context, sine assumptions are

formed for forecasting while justification of those assumptions is also made to provide

supportive arguments.

Q4 $ 1,916,309.8776

Year 14 Q1 $ 1,953,093.2225

Q2 $ 1,990,582.6193

Q3 $ 2,028,791.6208

Q4 $ 2,067,734.0396

Year 15 Q1 $ 2,107,423.9536

Q2 $ 2,147,875.7108

Q3 $ 2,189,103.9348

Q4 $ 2,231,123.5298

Year 16 Q1 $ 2,273,949.6860

Q2 $ 2,317,597.8853

Q3 $ 2,362,083.9067

Q4 $ 2,407,423.8321

Year 17 Q1 $ 2,453,634.0521

Q2 $ 2,500,731.2719

Q3 $ 2,548,732.5173

Q4 $ 2,597,655.1410

Year 18 Q1 $ 2,647,516.8288

Q2 $ 2,698,335.6059

Q3 $ 2,750,129.8435

Q4 $ 2,802,918.2654

Year 19 Q1 $ 2,856,719.9549

Q2 $ 2,911,554.3616

Q3 $ 2,967,441.3084

Q4 $ 3,024,400.9986

Year 20 Q1 $ 3,082,454.0234

Q2 $ 3,141,621.3693

Q3 $ 3,201,924.4254

Q4 $ 3,263,384.9917

2. Evaluation of the historical data of Melbourne to justify the assumptions for the

income data:

This part has tried to investigate the historical data related to income of clients of

Melbourne for making forecast for the next 10 years. In this context, sine assumptions are

formed for forecasting while justification of those assumptions is also made to provide

supportive arguments.

5BUSINESS FINANCE

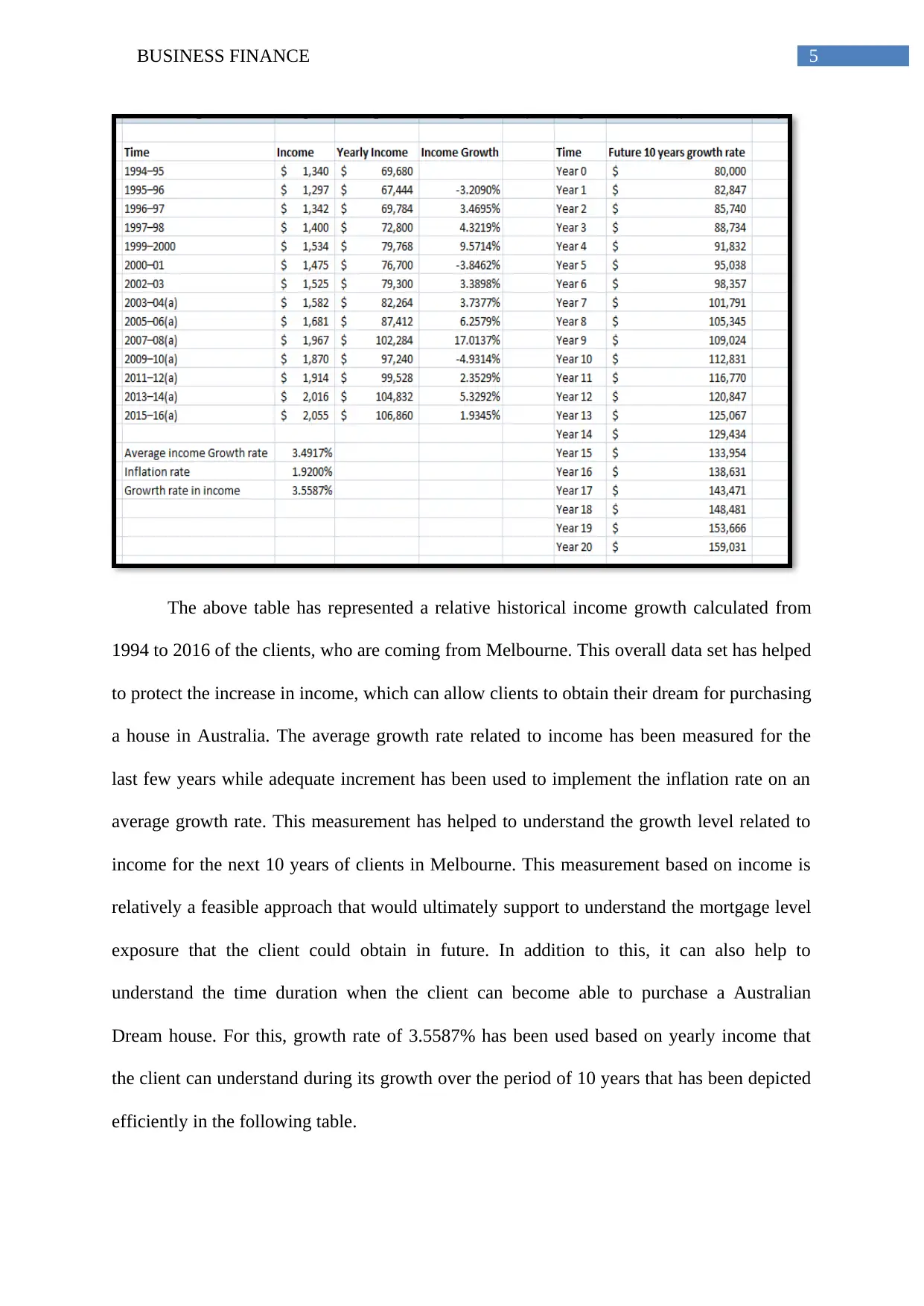

The above table has represented a relative historical income growth calculated from

1994 to 2016 of the clients, who are coming from Melbourne. This overall data set has helped

to protect the increase in income, which can allow clients to obtain their dream for purchasing

a house in Australia. The average growth rate related to income has been measured for the

last few years while adequate increment has been used to implement the inflation rate on an

average growth rate. This measurement has helped to understand the growth level related to

income for the next 10 years of clients in Melbourne. This measurement based on income is

relatively a feasible approach that would ultimately support to understand the mortgage level

exposure that the client could obtain in future. In addition to this, it can also help to

understand the time duration when the client can become able to purchase a Australian

Dream house. For this, growth rate of 3.5587% has been used based on yearly income that

the client can understand during its growth over the period of 10 years that has been depicted

efficiently in the following table.

The above table has represented a relative historical income growth calculated from

1994 to 2016 of the clients, who are coming from Melbourne. This overall data set has helped

to protect the increase in income, which can allow clients to obtain their dream for purchasing

a house in Australia. The average growth rate related to income has been measured for the

last few years while adequate increment has been used to implement the inflation rate on an

average growth rate. This measurement has helped to understand the growth level related to

income for the next 10 years of clients in Melbourne. This measurement based on income is

relatively a feasible approach that would ultimately support to understand the mortgage level

exposure that the client could obtain in future. In addition to this, it can also help to

understand the time duration when the client can become able to purchase a Australian

Dream house. For this, growth rate of 3.5587% has been used based on yearly income that

the client can understand during its growth over the period of 10 years that has been depicted

efficiently in the following table.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

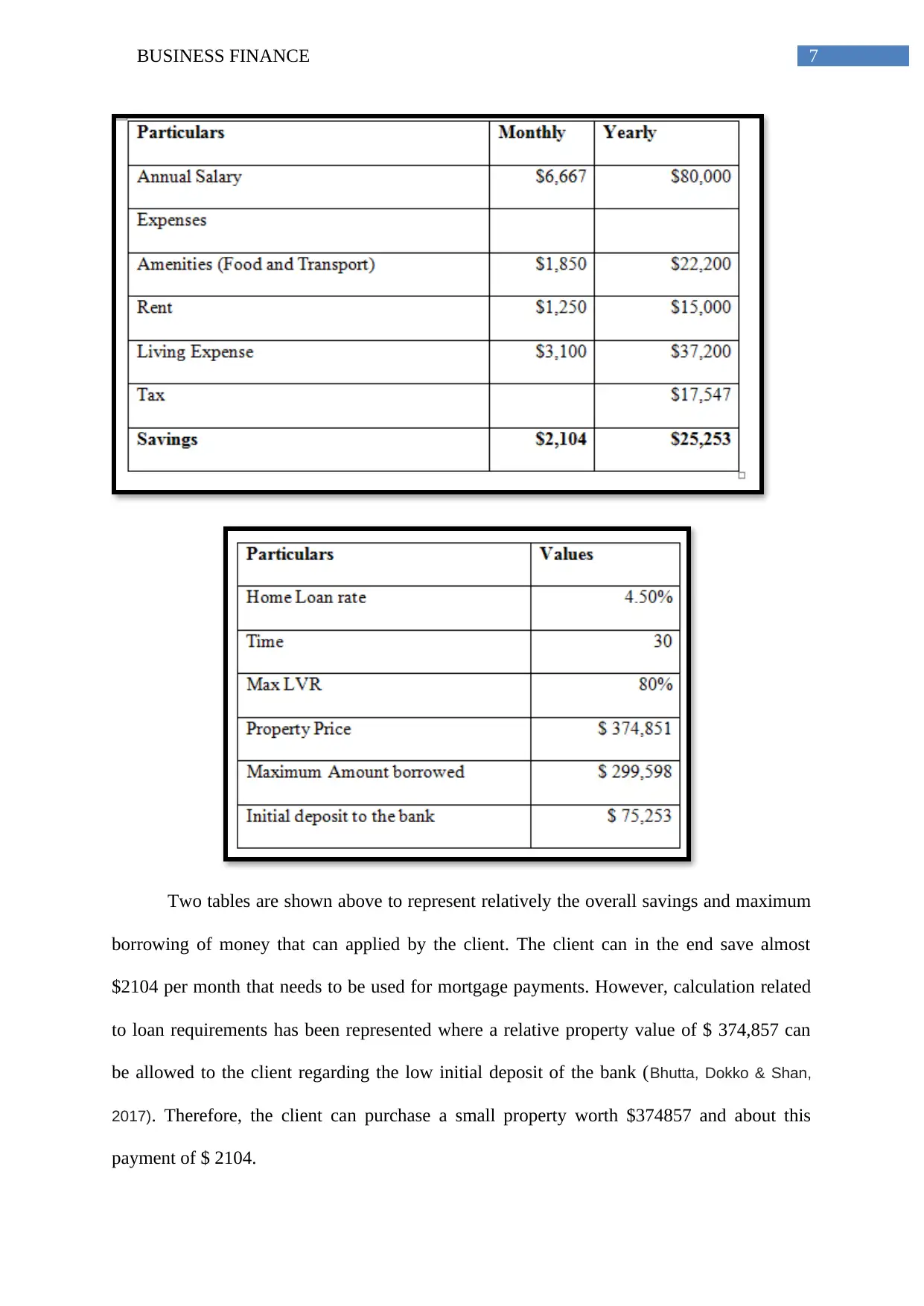

3. Detection of the net income through using ATO calculator to detect the home loan

rate and maximum borrowing amount that a client could receive:

In the context, net income of the client has been calculated considering that the person

is single and does not depend on any one. For determining this net income, ATO tax

calculator has been used (Genworth.com.au., 2018). Moreover, some realistic calculations are

also formed on the monthly expense of the specified client to determine the capacity of

monthly repayment of that person.

3. Detection of the net income through using ATO calculator to detect the home loan

rate and maximum borrowing amount that a client could receive:

In the context, net income of the client has been calculated considering that the person

is single and does not depend on any one. For determining this net income, ATO tax

calculator has been used (Genworth.com.au., 2018). Moreover, some realistic calculations are

also formed on the monthly expense of the specified client to determine the capacity of

monthly repayment of that person.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

Two tables are shown above to represent relatively the overall savings and maximum

borrowing of money that can applied by the client. The client can in the end save almost

$2104 per month that needs to be used for mortgage payments. However, calculation related

to loan requirements has been represented where a relative property value of $ 374,857 can

be allowed to the client regarding the low initial deposit of the bank (Bhutta, Dokko & Shan,

2017). Therefore, the client can purchase a small property worth $374857 and about this

payment of $ 2104.

Two tables are shown above to represent relatively the overall savings and maximum

borrowing of money that can applied by the client. The client can in the end save almost

$2104 per month that needs to be used for mortgage payments. However, calculation related

to loan requirements has been represented where a relative property value of $ 374,857 can

be allowed to the client regarding the low initial deposit of the bank (Bhutta, Dokko & Shan,

2017). Therefore, the client can purchase a small property worth $374857 and about this

payment of $ 2104.

8BUSINESS FINANCE

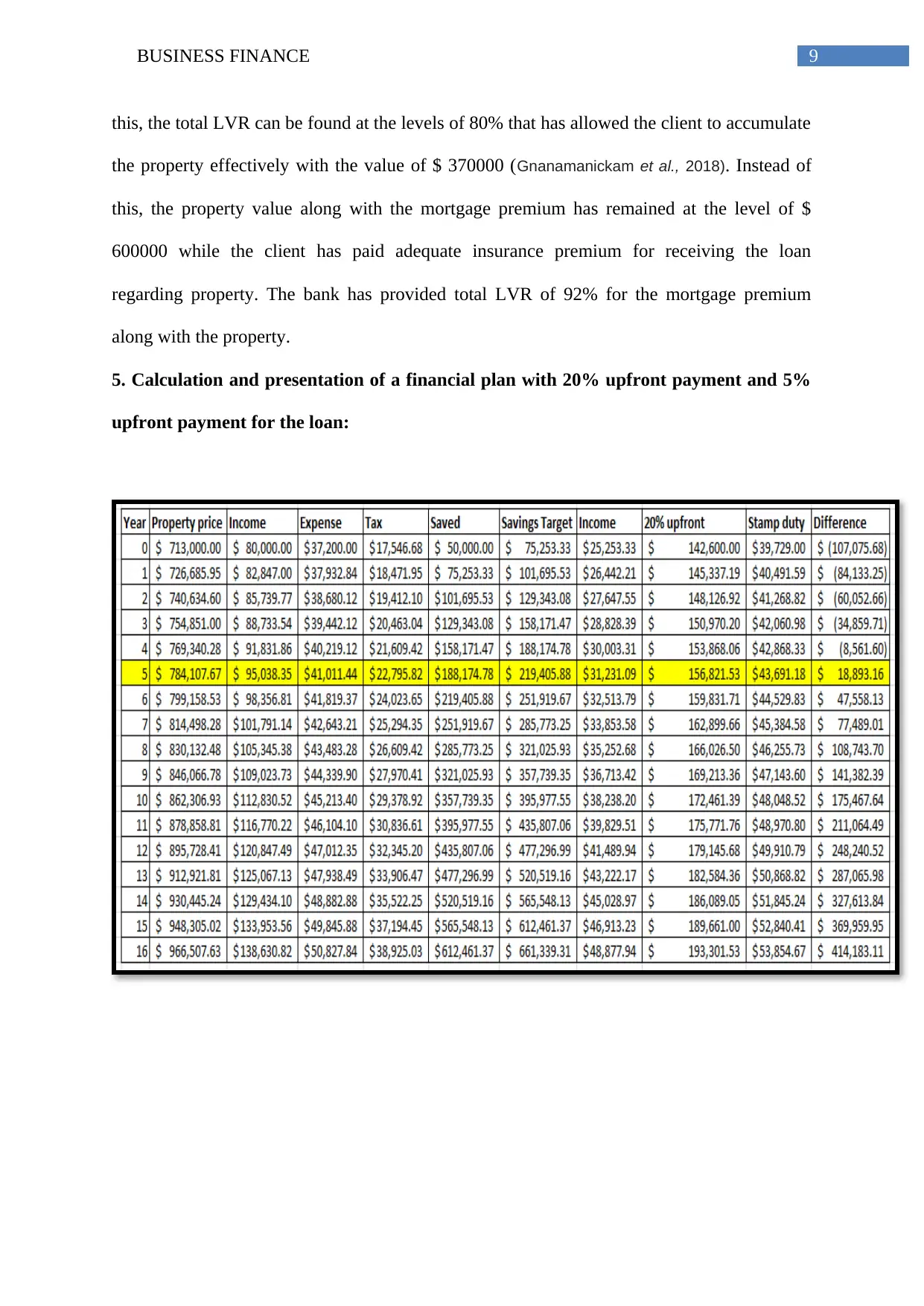

4. Calculation of stamp duty related with property purchase at the time of detecting the

affordability of house prices

The two tables represented above have showed overall property value in a relative sense and

client can provide this value when mortgage premium is used and also when mortgage

premium is not used. Based on valuation, the property value can be obtained worth $370000

by the client while the overall savings has remained at the level of $ 75253. In addition to

4. Calculation of stamp duty related with property purchase at the time of detecting the

affordability of house prices

The two tables represented above have showed overall property value in a relative sense and

client can provide this value when mortgage premium is used and also when mortgage

premium is not used. Based on valuation, the property value can be obtained worth $370000

by the client while the overall savings has remained at the level of $ 75253. In addition to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

this, the total LVR can be found at the levels of 80% that has allowed the client to accumulate

the property effectively with the value of $ 370000 (Gnanamanickam et al., 2018). Instead of

this, the property value along with the mortgage premium has remained at the level of $

600000 while the client has paid adequate insurance premium for receiving the loan

regarding property. The bank has provided total LVR of 92% for the mortgage premium

along with the property.

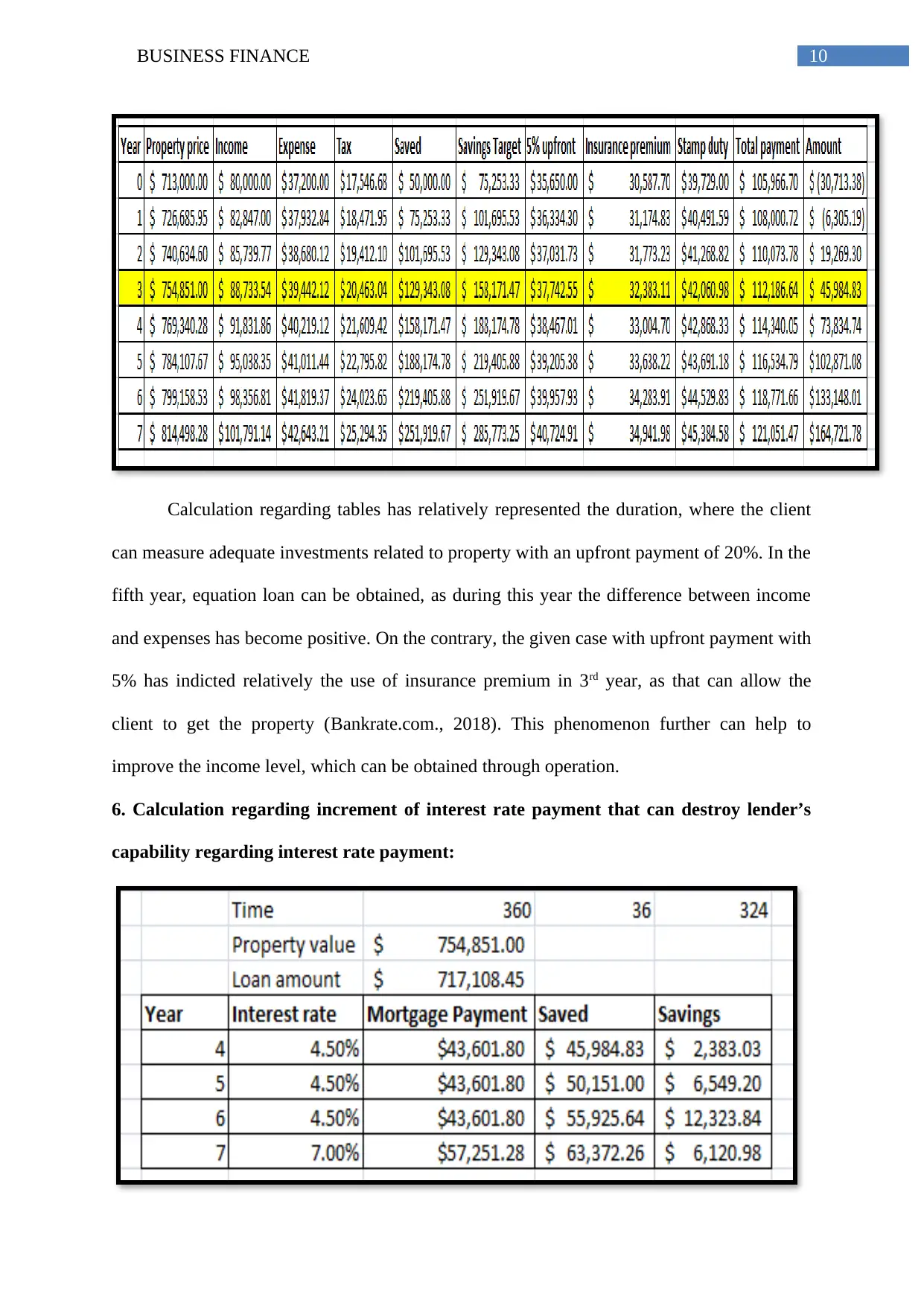

5. Calculation and presentation of a financial plan with 20% upfront payment and 5%

upfront payment for the loan:

this, the total LVR can be found at the levels of 80% that has allowed the client to accumulate

the property effectively with the value of $ 370000 (Gnanamanickam et al., 2018). Instead of

this, the property value along with the mortgage premium has remained at the level of $

600000 while the client has paid adequate insurance premium for receiving the loan

regarding property. The bank has provided total LVR of 92% for the mortgage premium

along with the property.

5. Calculation and presentation of a financial plan with 20% upfront payment and 5%

upfront payment for the loan:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

Calculation regarding tables has relatively represented the duration, where the client

can measure adequate investments related to property with an upfront payment of 20%. In the

fifth year, equation loan can be obtained, as during this year the difference between income

and expenses has become positive. On the contrary, the given case with upfront payment with

5% has indicted relatively the use of insurance premium in 3rd year, as that can allow the

client to get the property (Bankrate.com., 2018). This phenomenon further can help to

improve the income level, which can be obtained through operation.

6. Calculation regarding increment of interest rate payment that can destroy lender’s

capability regarding interest rate payment:

Calculation regarding tables has relatively represented the duration, where the client

can measure adequate investments related to property with an upfront payment of 20%. In the

fifth year, equation loan can be obtained, as during this year the difference between income

and expenses has become positive. On the contrary, the given case with upfront payment with

5% has indicted relatively the use of insurance premium in 3rd year, as that can allow the

client to get the property (Bankrate.com., 2018). This phenomenon further can help to

improve the income level, which can be obtained through operation.

6. Calculation regarding increment of interest rate payment that can destroy lender’s

capability regarding interest rate payment:

11BUSINESS FINANCE

From the above table has been represented the entire mortgage payments that the

client is going to conduct after purchasing of the property. However, the interest rate has

changed from 4.50% to 7% during four years and this in turn has slightly influenced the

overall mortgage payments of the concerned client (Kareem, 2017). Hence, during the initial

investment period, the above-mentioned table has represented the overall income and savings

of the client’s mortgage payments. This initial investment related to property can be

conducted over 3 years where interest rate increment can be obtained from year 7

(Stampduty.calculatorsaustralia.com.au., 2014). On the other side, changing mortgage

payments from $ 43601.80 to $ 57251.28 has remained unable to influence the overall

income of the client negatively regarding its continuous savings and increasing income

during the year.

7. Providing the relevant plan along with detailed risk that the assumption regarding

financial plan has entailed

Based on the above analysis, a report has been written with financial plan of the client

for detaining about the assumptions underlying in the financial plan when the “Australian

dream” can be true. Moreover, this section is going to discuss about the potential risks, which

are entailed by the assumptions and the way it is managed in the financial plan.

To achieve the Australian dream, assumptions are made for client, as the person’s

entire income is sufficient for supporting a mortgage regarding the new home. Hence, the

changing income of the client during the period has been represented with the calculations of

the financial planner (Clark, Lusardi & Mitchell, 2017). This calculation may support a new

mortgage. However, it can be seen from the evaluation that clients may lose their jobs and

consequently the entire aim for achieving the Australian dream may remain unfeasible.

Hence, the chief focus on the financial plan has remained only on the income that the client

can generate over the period. This financial plan can support the mortgage plan.

From the above table has been represented the entire mortgage payments that the

client is going to conduct after purchasing of the property. However, the interest rate has

changed from 4.50% to 7% during four years and this in turn has slightly influenced the

overall mortgage payments of the concerned client (Kareem, 2017). Hence, during the initial

investment period, the above-mentioned table has represented the overall income and savings

of the client’s mortgage payments. This initial investment related to property can be

conducted over 3 years where interest rate increment can be obtained from year 7

(Stampduty.calculatorsaustralia.com.au., 2014). On the other side, changing mortgage

payments from $ 43601.80 to $ 57251.28 has remained unable to influence the overall

income of the client negatively regarding its continuous savings and increasing income

during the year.

7. Providing the relevant plan along with detailed risk that the assumption regarding

financial plan has entailed

Based on the above analysis, a report has been written with financial plan of the client

for detaining about the assumptions underlying in the financial plan when the “Australian

dream” can be true. Moreover, this section is going to discuss about the potential risks, which

are entailed by the assumptions and the way it is managed in the financial plan.

To achieve the Australian dream, assumptions are made for client, as the person’s

entire income is sufficient for supporting a mortgage regarding the new home. Hence, the

changing income of the client during the period has been represented with the calculations of

the financial planner (Clark, Lusardi & Mitchell, 2017). This calculation may support a new

mortgage. However, it can be seen from the evaluation that clients may lose their jobs and

consequently the entire aim for achieving the Australian dream may remain unfeasible.

Hence, the chief focus on the financial plan has remained only on the income that the client

can generate over the period. This financial plan can support the mortgage plan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.