MA619 Accounting Research: Evaluating Bank Performance Using RPD

VerifiedAdded on 2023/06/11

|38

|7359

|143

Report

AI Summary

This accounting research report investigates the competitive performance and financial positions of four major Australian banks: ANZ, Westpac, Macquarie, and Suncorp. It employs Relative Profit Difference (RPD) analysis to assess the competitive strengths within the Australian banking sector. The report examines key performance indicators derived from the banks' financial statements over several years, focusing on metrics like gross revenue from interests, net interest revenue, earnings from continuous operations before tax, and net income. The analysis aims to determine the relationship between changes in financial performance and the competitive dynamics of the industry. The research methodology involves a detailed evaluation of the banks' accounting and financial reporting practices to understand the impact of competition on their performance.

Running head: ACCOUNTING RESEARCH

Accounting Research

Name of the Student:

Name of the University:

Authors Note:

Accounting Research

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING RESEARCH

Contents

Abstract:...........................................................................................................................................2

Introduction:....................................................................................................................................3

Literature review:.............................................................................................................................4

Relative Profit Difference (RPD):...................................................................................................4

Research question:...........................................................................................................................5

Methodology to be used:.................................................................................................................5

Data analysis:...................................................................................................................................5

Findings of empirical investigation:..............................................................................................28

Conclusion:....................................................................................................................................32

References:....................................................................................................................................33

Appendix:......................................................................................................................................34

ACCOUNTING RESEARCH

Contents

Abstract:...........................................................................................................................................2

Introduction:....................................................................................................................................3

Literature review:.............................................................................................................................4

Relative Profit Difference (RPD):...................................................................................................4

Research question:...........................................................................................................................5

Methodology to be used:.................................................................................................................5

Data analysis:...................................................................................................................................5

Findings of empirical investigation:..............................................................................................28

Conclusion:....................................................................................................................................32

References:....................................................................................................................................33

Appendix:......................................................................................................................................34

2

ACCOUNTING RESEARCH

Abstract:

Banks are the foundations of any Economy. The progress and development of a country’s

Economy is very much dependent on the efficiency of its banking system. Banking system of a

country provides the financial resources to each and every sector of an economy to ensure

efficient operations of these sectors. In Australia, the banks and Banking services are governed

by the provisions of Banking Act, 1959 and Reserve Act, 1959. In addition Australian Securities

and Investments Commission Act, 2001, Australian Prudential Regulation authority Act, 1998

and Anti-Money Laundering and Counter-Terrorism Financing Act 2006 also regulates different

functions of banking system. The purpose of the discussion here is to conduct a detailed

investigation on the competitive performance and position of four well know banks in the

country. The document shall be helpful in providing important information about the financial

performance and position of Australia and New Zealand Banking Group Limited, Westpac

Banking Group, Macquarie Banking Group and Suncorp Banking Group. Conducting Relative

Profit Difference research on the four banks mentioned above to measure the competitive

strengths in banking and financial industry in Australia is explained with significant amount of

emphasis on financial performance of these four banks over the years. The data analysis shall be

conducted by taking into consideration the financial information of these banks provided in the

financial reports. The research shall specifically focus on certain key performance yardsticks and

how these have changed over the last few years to come to a particular assertion about the

findings from the research.

ACCOUNTING RESEARCH

Abstract:

Banks are the foundations of any Economy. The progress and development of a country’s

Economy is very much dependent on the efficiency of its banking system. Banking system of a

country provides the financial resources to each and every sector of an economy to ensure

efficient operations of these sectors. In Australia, the banks and Banking services are governed

by the provisions of Banking Act, 1959 and Reserve Act, 1959. In addition Australian Securities

and Investments Commission Act, 2001, Australian Prudential Regulation authority Act, 1998

and Anti-Money Laundering and Counter-Terrorism Financing Act 2006 also regulates different

functions of banking system. The purpose of the discussion here is to conduct a detailed

investigation on the competitive performance and position of four well know banks in the

country. The document shall be helpful in providing important information about the financial

performance and position of Australia and New Zealand Banking Group Limited, Westpac

Banking Group, Macquarie Banking Group and Suncorp Banking Group. Conducting Relative

Profit Difference research on the four banks mentioned above to measure the competitive

strengths in banking and financial industry in Australia is explained with significant amount of

emphasis on financial performance of these four banks over the years. The data analysis shall be

conducted by taking into consideration the financial information of these banks provided in the

financial reports. The research shall specifically focus on certain key performance yardsticks and

how these have changed over the last few years to come to a particular assertion about the

findings from the research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING RESEARCH

Introduction:

The Australia and New Zealand Banking Group Limited, here in after to be referred to as

ANZ, is one of the largest banks in Australia. In fact currently it is ranked third after the

Commonwealth and Westpac Banking Corporation in term of market capitalization. It largely

operates in Australia and New Zealand. Westpac Banking Corporation (Westpac) is the second

largest bank in Australia in terms of market capitalization behind Commonwealth Bank of

Australia. Headquarter of Westpac is in Sydney, New South Wales (NSW). Suncorp Group is a

Brisbane based organization that provides services in finance, banking and insurance related

matters. Macquarie is finance and baking organization listed in Australia with operations and

services spreading in different parts of the world. In order to measure the competitive strength in

an industry, different and alternative methods have been suggested. In fact still number of

theories are being developed and empirical work is been conducted to introduce new and

improved methods to measure relative strengths in different industries.

Relative Profit Difference (RPD) analysis is one such method that is used to measure the

competitive strengths in different industry. A detailed analysis of RPD and empirical

investigation on the competition between four above mentioned banks shall be conducted with

the objective of measuring competitive strengths in these banks. Boone (2008) introduced the

approach to the world where the relative profit difference can be used to measure competitive

strengths in an industry. According to Boone (2008) the efficiency of an organization will

determine the profitability of such organization. Even under extreme competitive scenario

business organization will be able to manage its profitability level by improving its efficiency.

ACCOUNTING RESEARCH

Introduction:

The Australia and New Zealand Banking Group Limited, here in after to be referred to as

ANZ, is one of the largest banks in Australia. In fact currently it is ranked third after the

Commonwealth and Westpac Banking Corporation in term of market capitalization. It largely

operates in Australia and New Zealand. Westpac Banking Corporation (Westpac) is the second

largest bank in Australia in terms of market capitalization behind Commonwealth Bank of

Australia. Headquarter of Westpac is in Sydney, New South Wales (NSW). Suncorp Group is a

Brisbane based organization that provides services in finance, banking and insurance related

matters. Macquarie is finance and baking organization listed in Australia with operations and

services spreading in different parts of the world. In order to measure the competitive strength in

an industry, different and alternative methods have been suggested. In fact still number of

theories are being developed and empirical work is been conducted to introduce new and

improved methods to measure relative strengths in different industries.

Relative Profit Difference (RPD) analysis is one such method that is used to measure the

competitive strengths in different industry. A detailed analysis of RPD and empirical

investigation on the competition between four above mentioned banks shall be conducted with

the objective of measuring competitive strengths in these banks. Boone (2008) introduced the

approach to the world where the relative profit difference can be used to measure competitive

strengths in an industry. According to Boone (2008) the efficiency of an organization will

determine the profitability of such organization. Even under extreme competitive scenario

business organization will be able to manage its profitability level by improving its efficiency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING RESEARCH

Kar, A.K. (2016) has defined that the RPD analysis is effective in the context of

Equilibrium market condition where fair number of firs operating under perfect oligopoly

market. Thus, the RPD analysis will not be effective in any other market situation and will not

provide the actual strengths of competition in a market.

Literature review:

Relative Profit Difference (RPD):

RPD approach was developed and suggested by Boone (2008) to measure competition in

an industry. The approach was suggested in the context of an industry where firms can enter and

compete despite differences in efficiency. The RPD approach assumes that initially firms are

unsure about the decision of whether to enter the market or not. However, once the firms decide

to enter the market, they look to maximize their profits. According to the theory an equilibrium

profit is established where the profit of the firms in the industry is directly related to the

efficiency of the firm. Thus, the RPD approach establishes that a firm in an industry where free

competition exists the firm’s profitability will be equal to its efficiency (Abel, Khobai & Le

Roux, 2017).

Relative Profit Difference approach is a technique developed by Boone (2008) for

measurement of competitive strengths of an industry. The approach is definitely effective but

only in equilibrium condition under multi-firm oligopoly market as explained by Kar, K.A.

(2016). In this case the industry is banking and financial sector in Australia. The shortcoming of

the RPD approach in this specific industry is that the banking and financial sector in Australia

can hardly be defined as multi-firm oligopoly market. Neither there is equilibrium condition in

the market place.

ACCOUNTING RESEARCH

Kar, A.K. (2016) has defined that the RPD analysis is effective in the context of

Equilibrium market condition where fair number of firs operating under perfect oligopoly

market. Thus, the RPD analysis will not be effective in any other market situation and will not

provide the actual strengths of competition in a market.

Literature review:

Relative Profit Difference (RPD):

RPD approach was developed and suggested by Boone (2008) to measure competition in

an industry. The approach was suggested in the context of an industry where firms can enter and

compete despite differences in efficiency. The RPD approach assumes that initially firms are

unsure about the decision of whether to enter the market or not. However, once the firms decide

to enter the market, they look to maximize their profits. According to the theory an equilibrium

profit is established where the profit of the firms in the industry is directly related to the

efficiency of the firm. Thus, the RPD approach establishes that a firm in an industry where free

competition exists the firm’s profitability will be equal to its efficiency (Abel, Khobai & Le

Roux, 2017).

Relative Profit Difference approach is a technique developed by Boone (2008) for

measurement of competitive strengths of an industry. The approach is definitely effective but

only in equilibrium condition under multi-firm oligopoly market as explained by Kar, K.A.

(2016). In this case the industry is banking and financial sector in Australia. The shortcoming of

the RPD approach in this specific industry is that the banking and financial sector in Australia

can hardly be defined as multi-firm oligopoly market. Neither there is equilibrium condition in

the market place.

5

ACCOUNTING RESEARCH

Since time in memorial scholars are looking to develop better methods to measure the strengths

of competition in an industry with significant results to show their efforts. RPD approach of

Boone (2008) is one of such approach that provide a different scope and measurement technique

to measure the competitive strengths in an industry. This approach definitely helps in assessing

the relative strengths of firms in an industry. However, to measure the competitive strengths of

an entire industry with relative profit difference approach is definitely a challenging task and

requires impeccable methodology to collect data on the basis of which analysis shall be

conducted to form a particular conclusion. Apart from that all underlying variables must be

present and assumption must be correct in order to measure the competitive strengths of an

industry effectively.

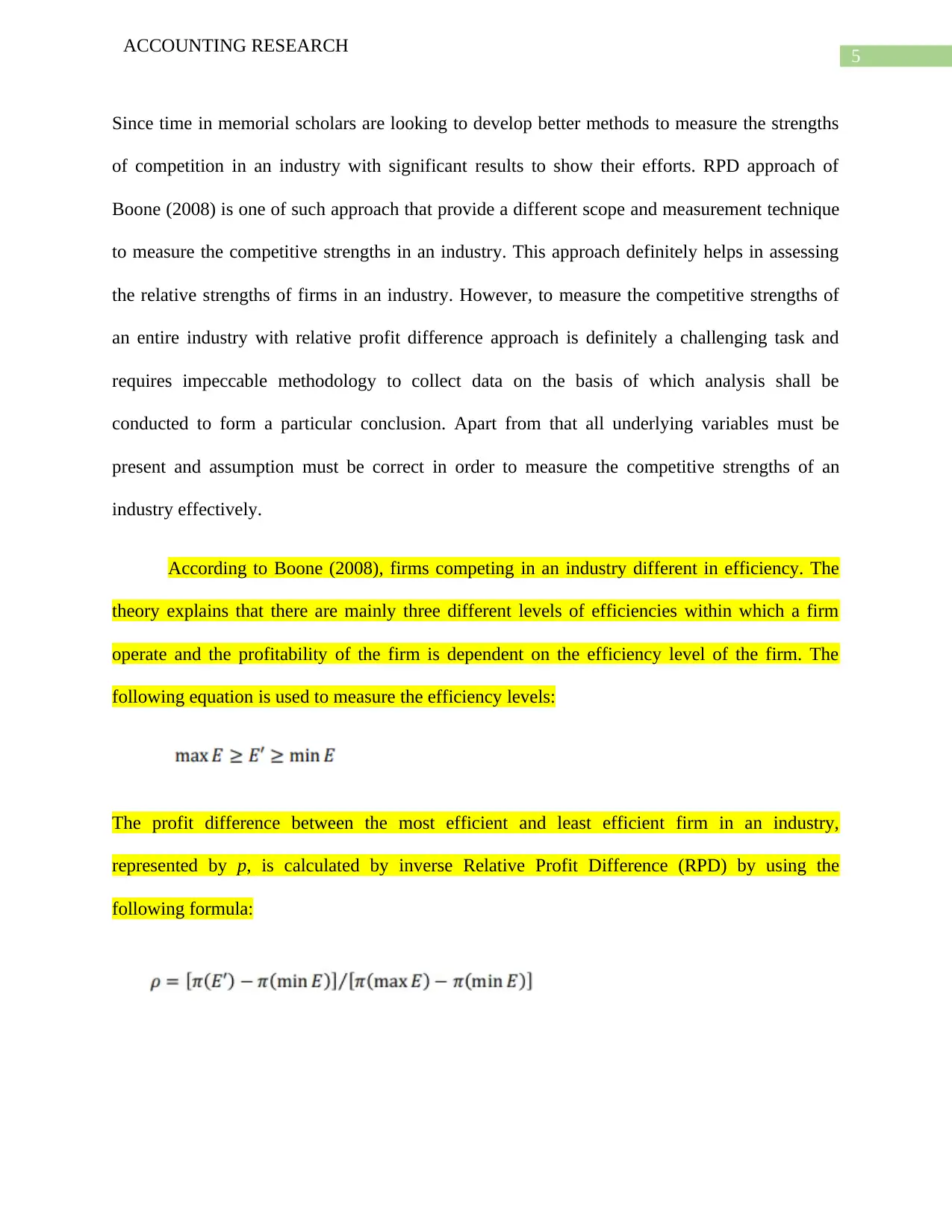

According to Boone (2008), firms competing in an industry different in efficiency. The

theory explains that there are mainly three different levels of efficiencies within which a firm

operate and the profitability of the firm is dependent on the efficiency level of the firm. The

following equation is used to measure the efficiency levels:

The profit difference between the most efficient and least efficient firm in an industry,

represented by p, is calculated by inverse Relative Profit Difference (RPD) by using the

following formula:

ACCOUNTING RESEARCH

Since time in memorial scholars are looking to develop better methods to measure the strengths

of competition in an industry with significant results to show their efforts. RPD approach of

Boone (2008) is one of such approach that provide a different scope and measurement technique

to measure the competitive strengths in an industry. This approach definitely helps in assessing

the relative strengths of firms in an industry. However, to measure the competitive strengths of

an entire industry with relative profit difference approach is definitely a challenging task and

requires impeccable methodology to collect data on the basis of which analysis shall be

conducted to form a particular conclusion. Apart from that all underlying variables must be

present and assumption must be correct in order to measure the competitive strengths of an

industry effectively.

According to Boone (2008), firms competing in an industry different in efficiency. The

theory explains that there are mainly three different levels of efficiencies within which a firm

operate and the profitability of the firm is dependent on the efficiency level of the firm. The

following equation is used to measure the efficiency levels:

The profit difference between the most efficient and least efficient firm in an industry,

represented by p, is calculated by inverse Relative Profit Difference (RPD) by using the

following formula:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING RESEARCH

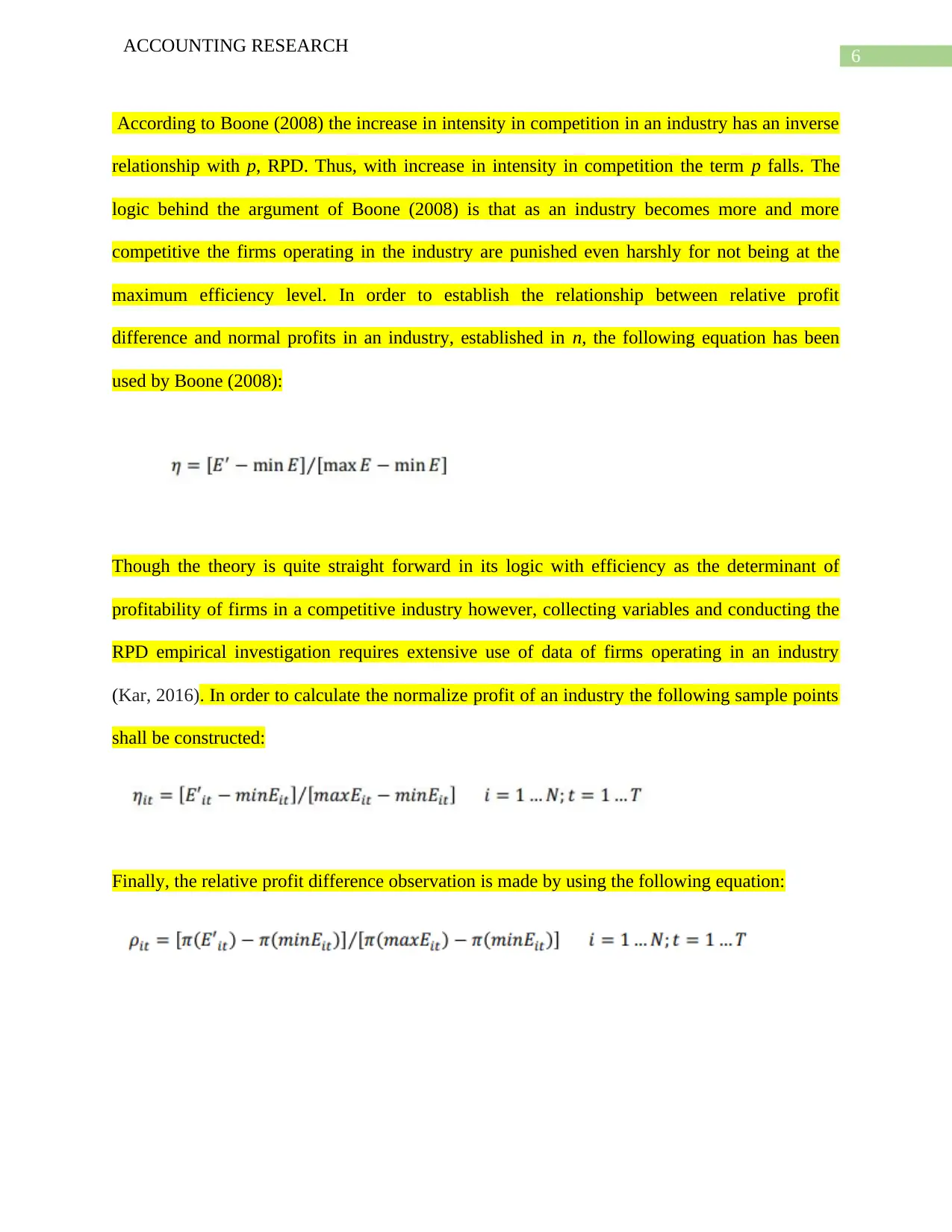

According to Boone (2008) the increase in intensity in competition in an industry has an inverse

relationship with p, RPD. Thus, with increase in intensity in competition the term p falls. The

logic behind the argument of Boone (2008) is that as an industry becomes more and more

competitive the firms operating in the industry are punished even harshly for not being at the

maximum efficiency level. In order to establish the relationship between relative profit

difference and normal profits in an industry, established in n, the following equation has been

used by Boone (2008):

Though the theory is quite straight forward in its logic with efficiency as the determinant of

profitability of firms in a competitive industry however, collecting variables and conducting the

RPD empirical investigation requires extensive use of data of firms operating in an industry

(Kar, 2016). In order to calculate the normalize profit of an industry the following sample points

shall be constructed:

Finally, the relative profit difference observation is made by using the following equation:

ACCOUNTING RESEARCH

According to Boone (2008) the increase in intensity in competition in an industry has an inverse

relationship with p, RPD. Thus, with increase in intensity in competition the term p falls. The

logic behind the argument of Boone (2008) is that as an industry becomes more and more

competitive the firms operating in the industry are punished even harshly for not being at the

maximum efficiency level. In order to establish the relationship between relative profit

difference and normal profits in an industry, established in n, the following equation has been

used by Boone (2008):

Though the theory is quite straight forward in its logic with efficiency as the determinant of

profitability of firms in a competitive industry however, collecting variables and conducting the

RPD empirical investigation requires extensive use of data of firms operating in an industry

(Kar, 2016). In order to calculate the normalize profit of an industry the following sample points

shall be constructed:

Finally, the relative profit difference observation is made by using the following equation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING RESEARCH

Research question:

How the financial performance of 4 banks have affected over the years and is there a direct

connection between the changes in financial performance of these banks and the

competitive strengths of the industry?

The data shall be collected from the financial statements of these banks to evaluate the changes

in the key performance yardsticks of these banks such as revenue, profit and others to explain the

impact of competition in the market. The RPD analysis shall be conducted to calculate the

relative difference in profits of these entities over the years and how the competition in the

industry has influenced the performances of these banks.

Methodology to be used:

Taking into consideration the approach that RPD methodology used to measure the competition

in an industry a detailed investigation of the financial performance of the four banks, i.e. ANZ,

Macquarie, Westpac and Suncorp, shall be conducted with specific focus on accounting and

financial reporting aspects of these banks.

Data analysis:

ANZ:

In order to investigate the financial performance of ANZ over the last few years the income

statements of the company for last few years shall be evaluated. A simple evaluation of the

income statements of the company over the years shall be helpful in assessing how the bank has

performed over the years. However, in order to analyse the competitive performance of the bank

a comparative analysis of the bank’s performance shall be conducted with the performance of

other three banks.

ACCOUNTING RESEARCH

Research question:

How the financial performance of 4 banks have affected over the years and is there a direct

connection between the changes in financial performance of these banks and the

competitive strengths of the industry?

The data shall be collected from the financial statements of these banks to evaluate the changes

in the key performance yardsticks of these banks such as revenue, profit and others to explain the

impact of competition in the market. The RPD analysis shall be conducted to calculate the

relative difference in profits of these entities over the years and how the competition in the

industry has influenced the performances of these banks.

Methodology to be used:

Taking into consideration the approach that RPD methodology used to measure the competition

in an industry a detailed investigation of the financial performance of the four banks, i.e. ANZ,

Macquarie, Westpac and Suncorp, shall be conducted with specific focus on accounting and

financial reporting aspects of these banks.

Data analysis:

ANZ:

In order to investigate the financial performance of ANZ over the last few years the income

statements of the company for last few years shall be evaluated. A simple evaluation of the

income statements of the company over the years shall be helpful in assessing how the bank has

performed over the years. However, in order to analyse the competitive performance of the bank

a comparative analysis of the bank’s performance shall be conducted with the performance of

other three banks.

8

ACCOUNTING RESEARCH

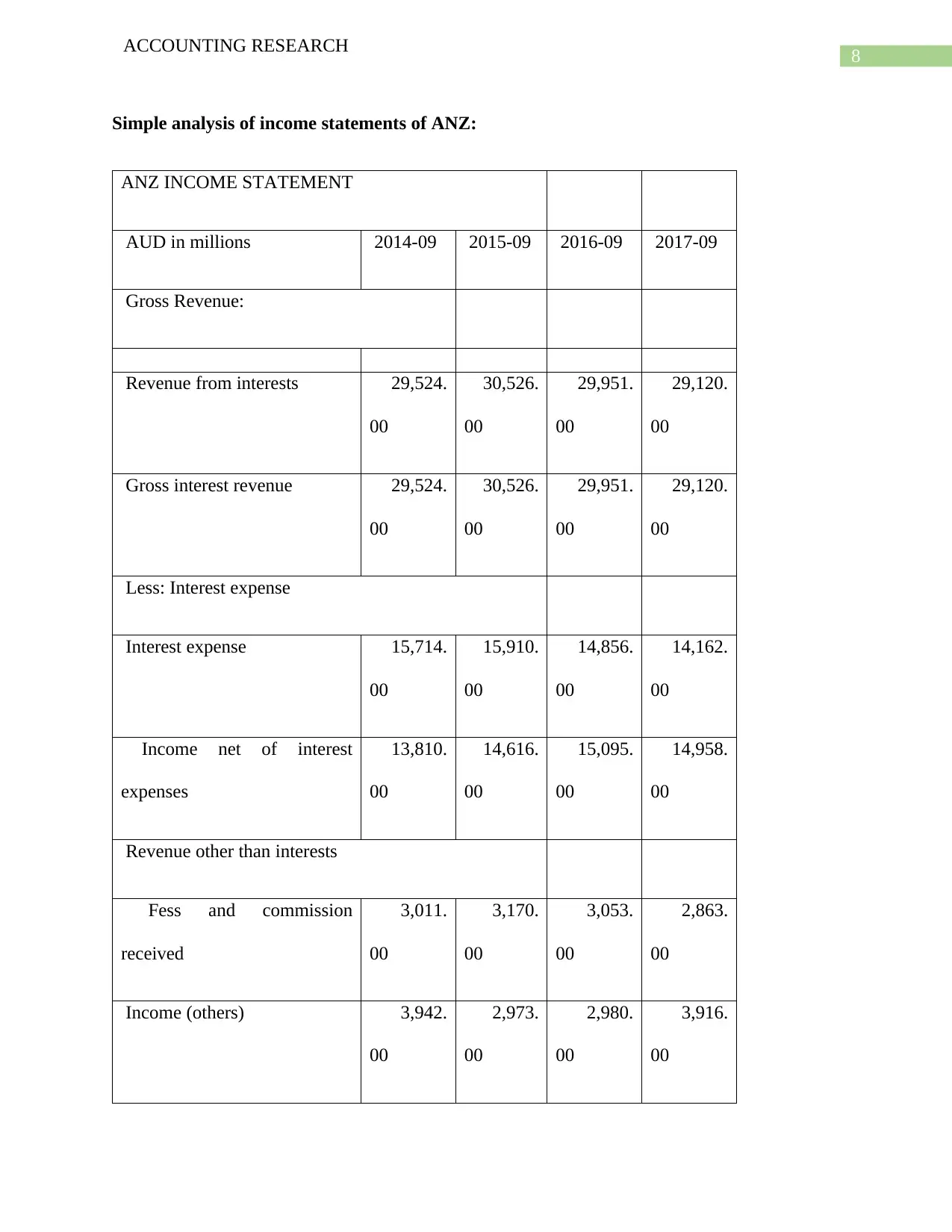

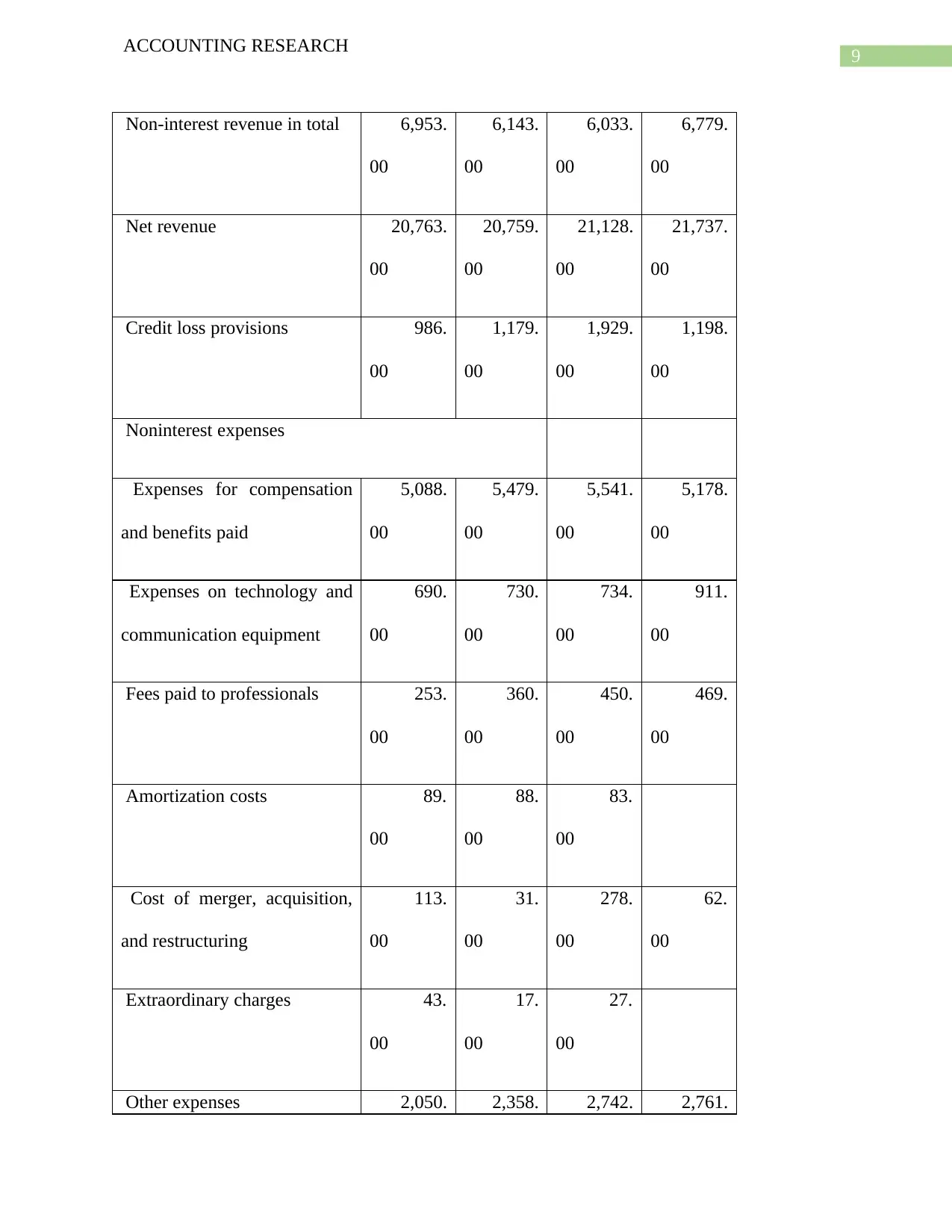

Simple analysis of income statements of ANZ:

ANZ INCOME STATEMENT

AUD in millions 2014-09 2015-09 2016-09 2017-09

Gross Revenue:

Revenue from interests 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Gross interest revenue 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Less: Interest expense

Interest expense 15,714.

00

15,910.

00

14,856.

00

14,162.

00

Income net of interest

expenses

13,810.

00

14,616.

00

15,095.

00

14,958.

00

Revenue other than interests

Fess and commission

received

3,011.

00

3,170.

00

3,053.

00

2,863.

00

Income (others) 3,942.

00

2,973.

00

2,980.

00

3,916.

00

ACCOUNTING RESEARCH

Simple analysis of income statements of ANZ:

ANZ INCOME STATEMENT

AUD in millions 2014-09 2015-09 2016-09 2017-09

Gross Revenue:

Revenue from interests 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Gross interest revenue 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Less: Interest expense

Interest expense 15,714.

00

15,910.

00

14,856.

00

14,162.

00

Income net of interest

expenses

13,810.

00

14,616.

00

15,095.

00

14,958.

00

Revenue other than interests

Fess and commission

received

3,011.

00

3,170.

00

3,053.

00

2,863.

00

Income (others) 3,942.

00

2,973.

00

2,980.

00

3,916.

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING RESEARCH

Non-interest revenue in total 6,953.

00

6,143.

00

6,033.

00

6,779.

00

Net revenue 20,763.

00

20,759.

00

21,128.

00

21,737.

00

Credit loss provisions 986.

00

1,179.

00

1,929.

00

1,198.

00

Noninterest expenses

Expenses for compensation

and benefits paid

5,088.

00

5,479.

00

5,541.

00

5,178.

00

Expenses on technology and

communication equipment

690.

00

730.

00

734.

00

911.

00

Fees paid to professionals 253.

00

360.

00

450.

00

469.

00

Amortization costs 89.

00

88.

00

83.

00

Cost of merger, acquisition,

and restructuring

113.

00

31.

00

278.

00

62.

00

Extraordinary charges 43.

00

17.

00

27.

00

Other expenses 2,050. 2,358. 2,742. 2,761.

ACCOUNTING RESEARCH

Non-interest revenue in total 6,953.

00

6,143.

00

6,033.

00

6,779.

00

Net revenue 20,763.

00

20,759.

00

21,128.

00

21,737.

00

Credit loss provisions 986.

00

1,179.

00

1,929.

00

1,198.

00

Noninterest expenses

Expenses for compensation

and benefits paid

5,088.

00

5,479.

00

5,541.

00

5,178.

00

Expenses on technology and

communication equipment

690.

00

730.

00

734.

00

911.

00

Fees paid to professionals 253.

00

360.

00

450.

00

469.

00

Amortization costs 89.

00

88.

00

83.

00

Cost of merger, acquisition,

and restructuring

113.

00

31.

00

278.

00

62.

00

Extraordinary charges 43.

00

17.

00

27.

00

Other expenses 2,050. 2,358. 2,742. 2,761.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING RESEARCH

00 00 00 00

Total expenses (Non-interest) 8,326.

00

9,063.

00

9,855.

00

9,381.

00

Earnings from continuous

operations before tax

11,451.

00

10,517.

00

9,344.

00

11,158.

00

Provision (benefit) for taxes 3,025.

00

3,026.

00

2,458.

00

3,206.

00

Other income (expense) (1,155.0

0)

2.

00

(1,177.0

0)

(1,546.0

0)

Net income after tax 7,271.

00

7,493.

00

5,709.

00

6,406.

00

Preferred dividend 6.

00

1.

00

earnings available to common

shareholders

7,265.

00

7,492.

00

5,709.

00

6,406.

00

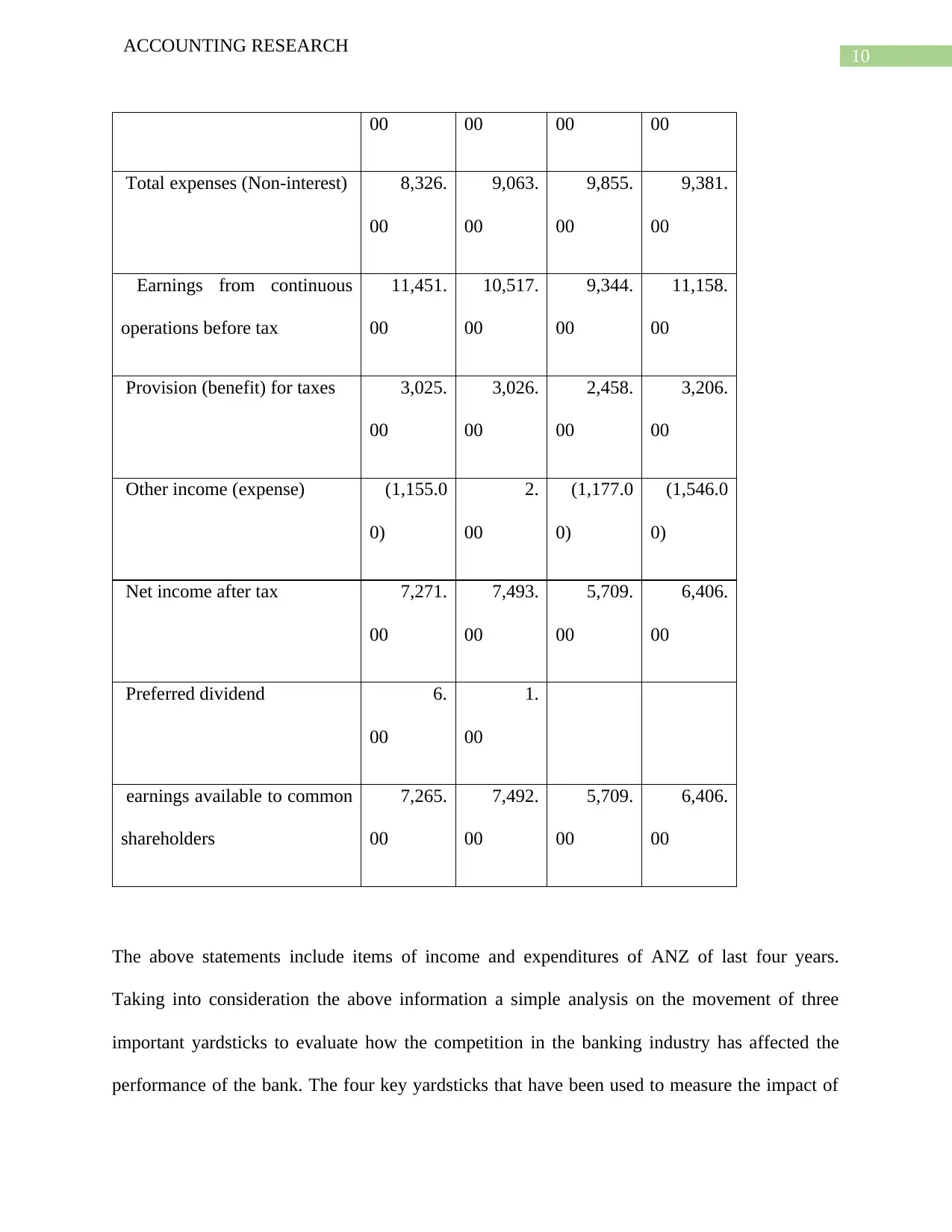

The above statements include items of income and expenditures of ANZ of last four years.

Taking into consideration the above information a simple analysis on the movement of three

important yardsticks to evaluate how the competition in the banking industry has affected the

performance of the bank. The four key yardsticks that have been used to measure the impact of

ACCOUNTING RESEARCH

00 00 00 00

Total expenses (Non-interest) 8,326.

00

9,063.

00

9,855.

00

9,381.

00

Earnings from continuous

operations before tax

11,451.

00

10,517.

00

9,344.

00

11,158.

00

Provision (benefit) for taxes 3,025.

00

3,026.

00

2,458.

00

3,206.

00

Other income (expense) (1,155.0

0)

2.

00

(1,177.0

0)

(1,546.0

0)

Net income after tax 7,271.

00

7,493.

00

5,709.

00

6,406.

00

Preferred dividend 6.

00

1.

00

earnings available to common

shareholders

7,265.

00

7,492.

00

5,709.

00

6,406.

00

The above statements include items of income and expenditures of ANZ of last four years.

Taking into consideration the above information a simple analysis on the movement of three

important yardsticks to evaluate how the competition in the banking industry has affected the

performance of the bank. The four key yardsticks that have been used to measure the impact of

11

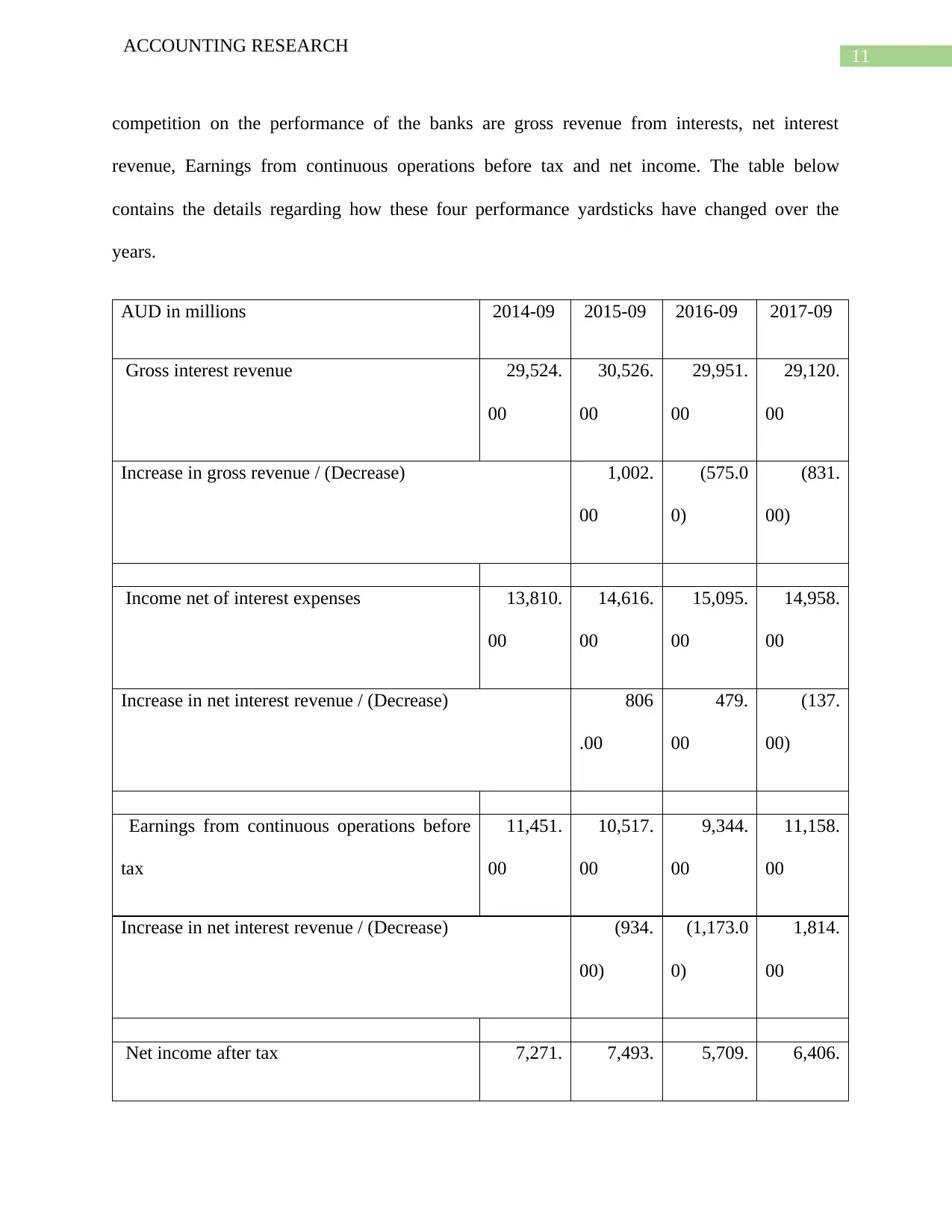

ACCOUNTING RESEARCH

competition on the performance of the banks are gross revenue from interests, net interest

revenue, Earnings from continuous operations before tax and net income. The table below

contains the details regarding how these four performance yardsticks have changed over the

years.

AUD in millions 2014-09 2015-09 2016-09 2017-09

Gross interest revenue 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Increase in gross revenue / (Decrease) 1,002.

00

(575.0

0)

(831.

00)

Income net of interest expenses 13,810.

00

14,616.

00

15,095.

00

14,958.

00

Increase in net interest revenue / (Decrease) 806

.00

479.

00

(137.

00)

Earnings from continuous operations before

tax

11,451.

00

10,517.

00

9,344.

00

11,158.

00

Increase in net interest revenue / (Decrease) (934.

00)

(1,173.0

0)

1,814.

00

Net income after tax 7,271. 7,493. 5,709. 6,406.

ACCOUNTING RESEARCH

competition on the performance of the banks are gross revenue from interests, net interest

revenue, Earnings from continuous operations before tax and net income. The table below

contains the details regarding how these four performance yardsticks have changed over the

years.

AUD in millions 2014-09 2015-09 2016-09 2017-09

Gross interest revenue 29,524.

00

30,526.

00

29,951.

00

29,120.

00

Increase in gross revenue / (Decrease) 1,002.

00

(575.0

0)

(831.

00)

Income net of interest expenses 13,810.

00

14,616.

00

15,095.

00

14,958.

00

Increase in net interest revenue / (Decrease) 806

.00

479.

00

(137.

00)

Earnings from continuous operations before

tax

11,451.

00

10,517.

00

9,344.

00

11,158.

00

Increase in net interest revenue / (Decrease) (934.

00)

(1,173.0

0)

1,814.

00

Net income after tax 7,271. 7,493. 5,709. 6,406.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.