Deakin Uni MAA262 Management Accounting Assignment Solution 2018

VerifiedAdded on 2023/06/12

|8

|1664

|156

Homework Assignment

AI Summary

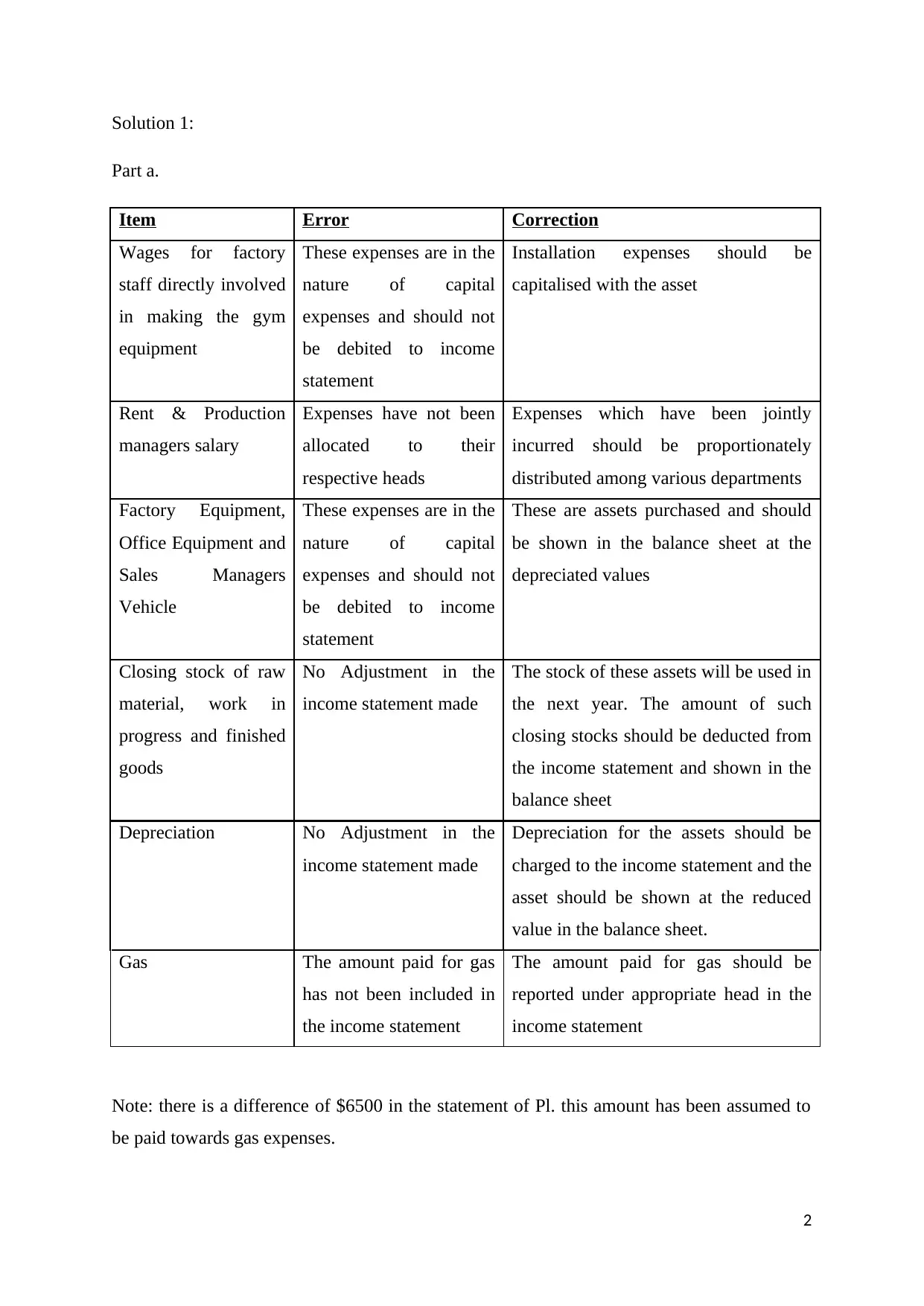

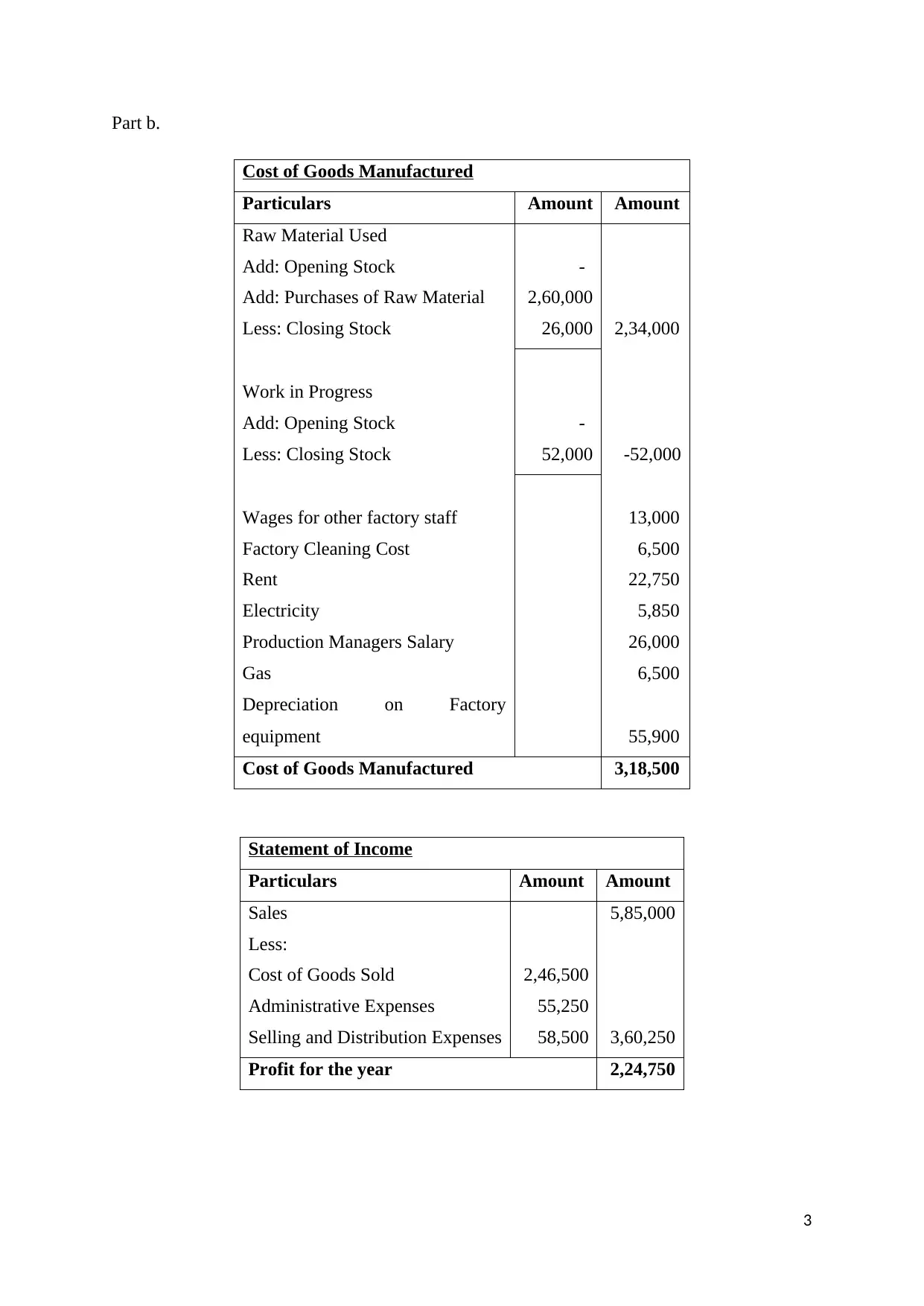

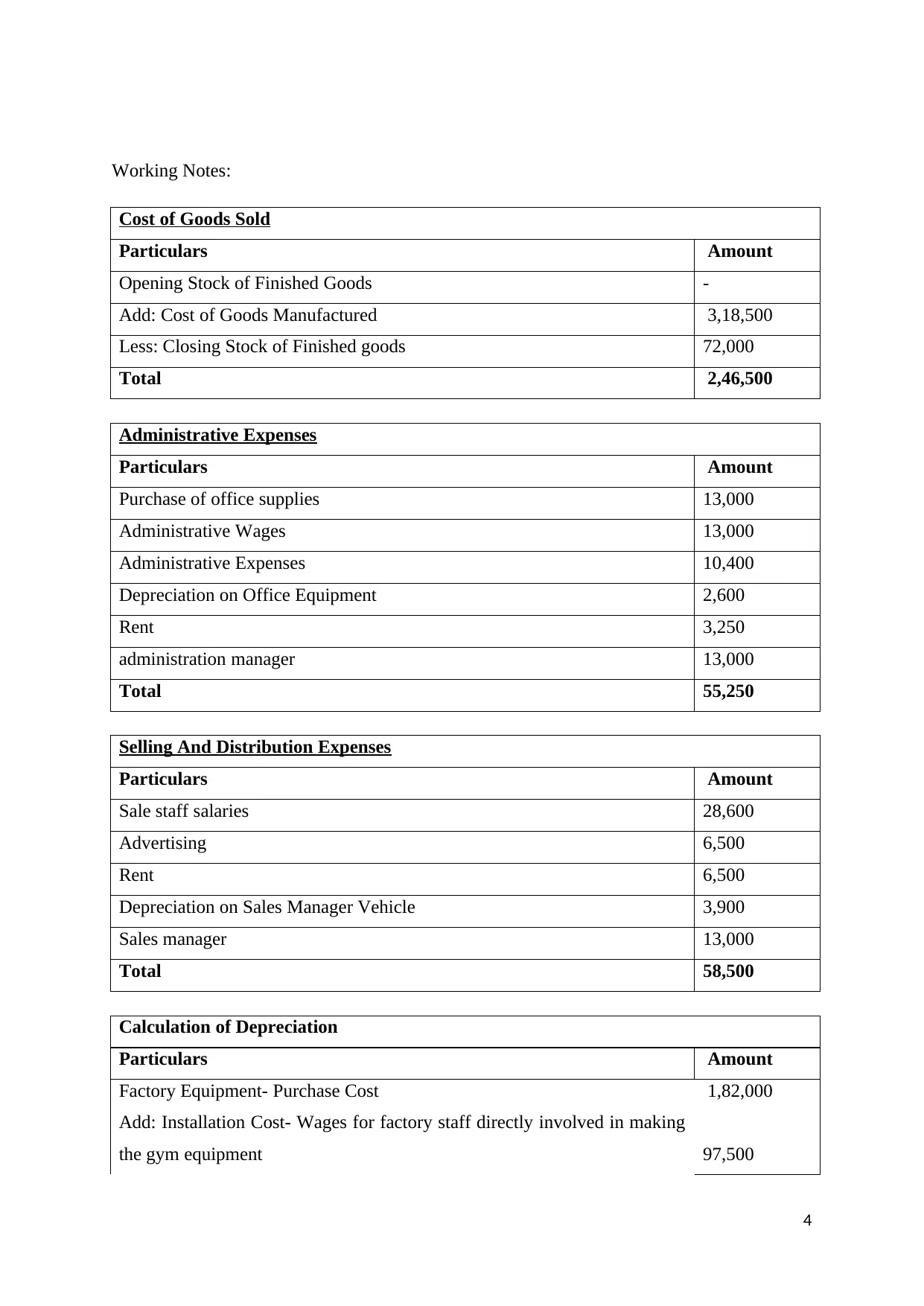

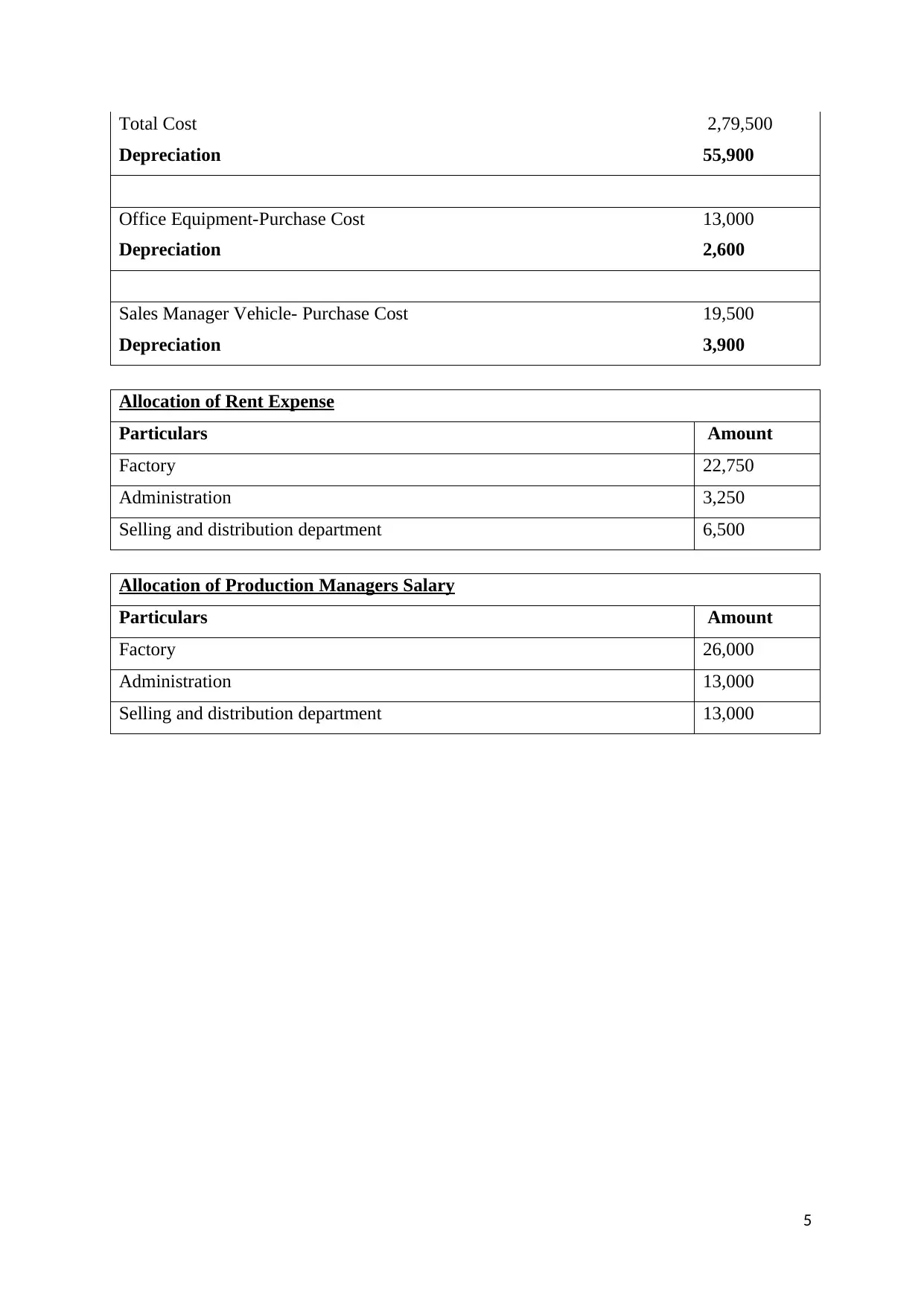

This assignment solution addresses key aspects of management accounting, including error correction in financial statements, cost of goods manufactured, and income statement preparation for Twister Pty Ltd. It covers the allocation of various expenses, depreciation calculations, and provides a profitability analysis. The solution also discusses the financial viability of the company, focusing on securing an overdraft facility and ethical considerations related to raw material sourcing. The document includes detailed workings for cost of goods sold, administrative expenses, and selling & distribution expenses. It emphasizes the importance of maintaining quality and ethical standards in business operations. Desklib offers a range of similar solved assignments and past papers to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.