Project Report: Management Accounting Analysis for BBQ and Balloons

VerifiedAdded on 2022/11/14

|11

|1998

|497

Project

AI Summary

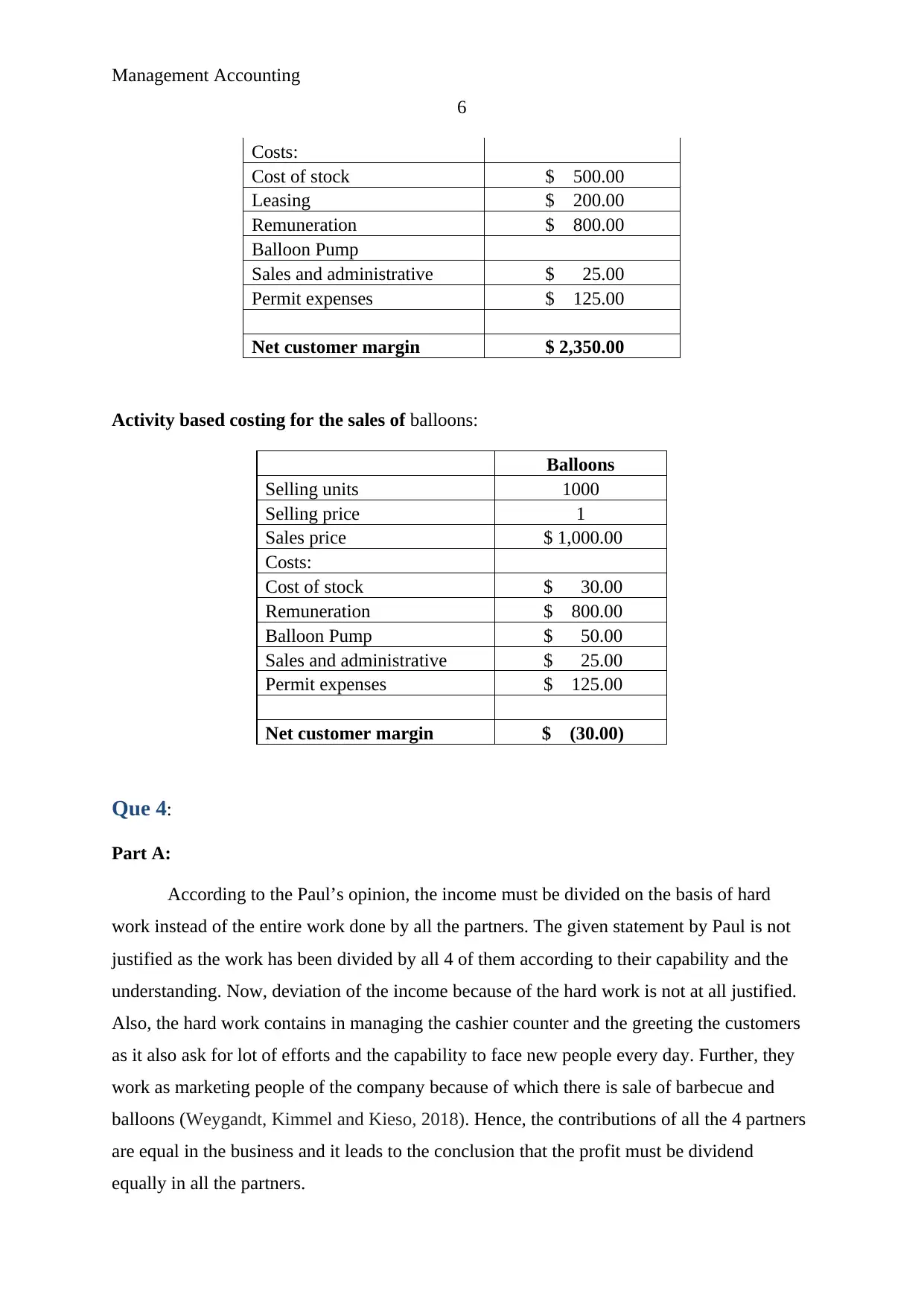

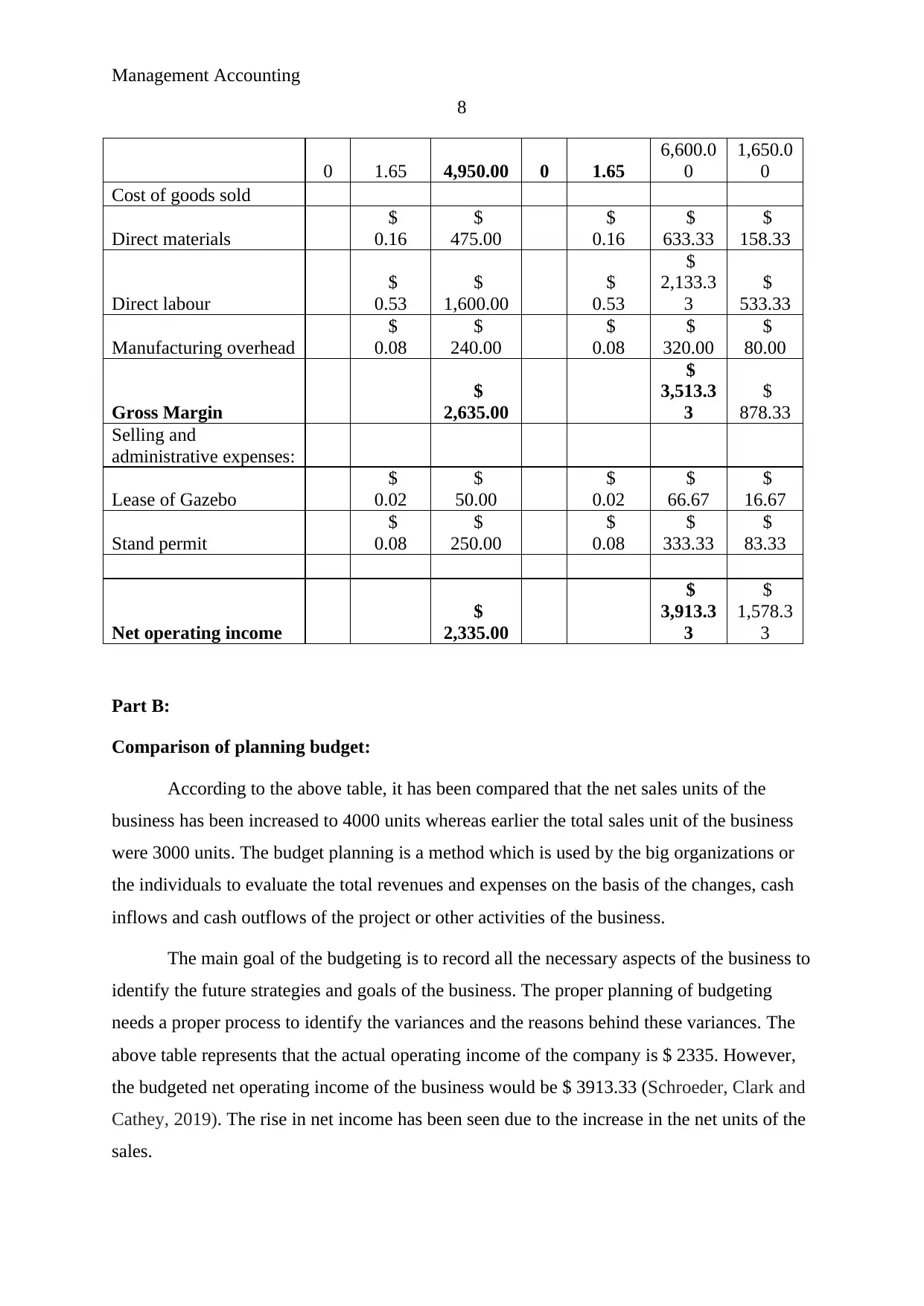

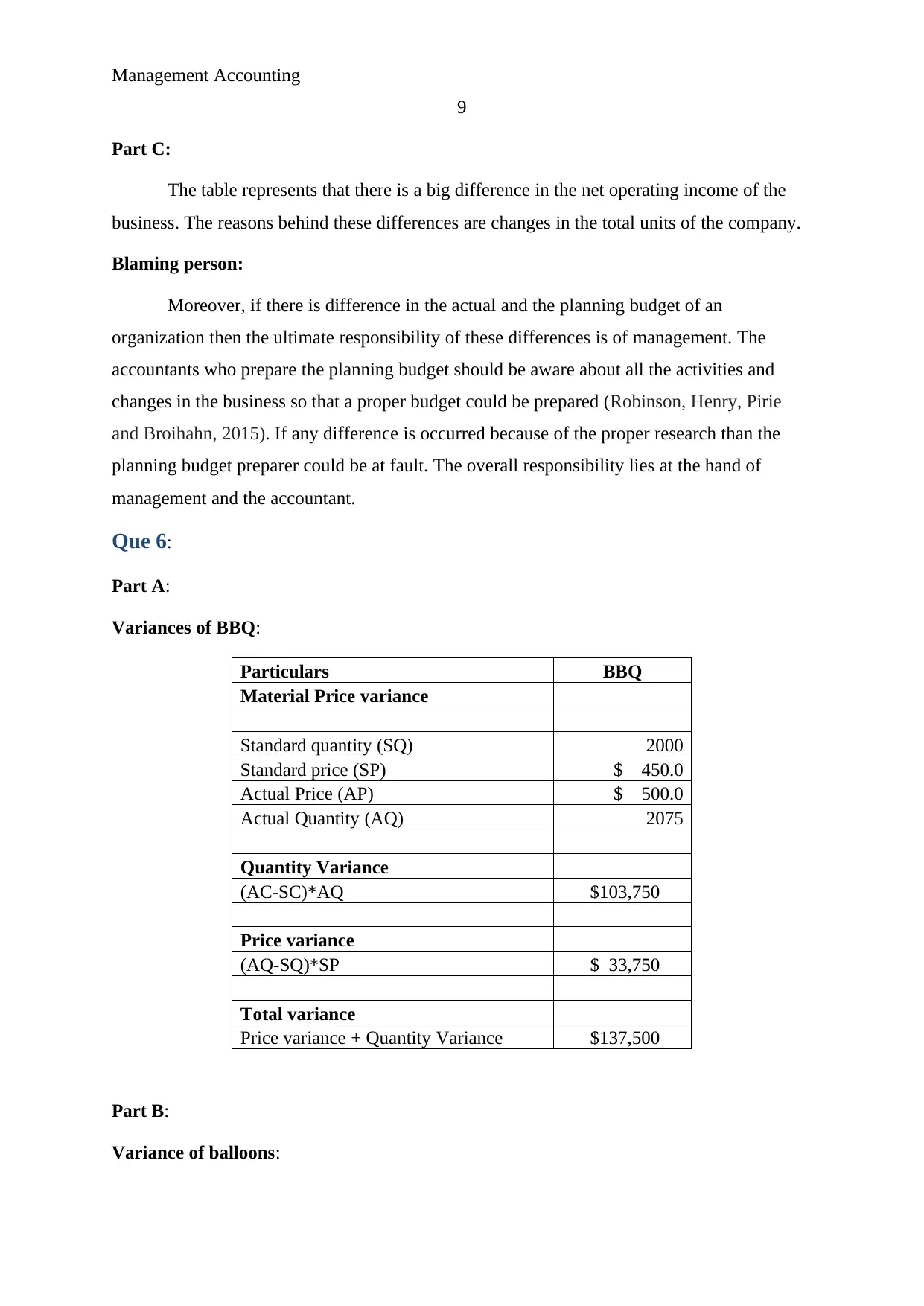

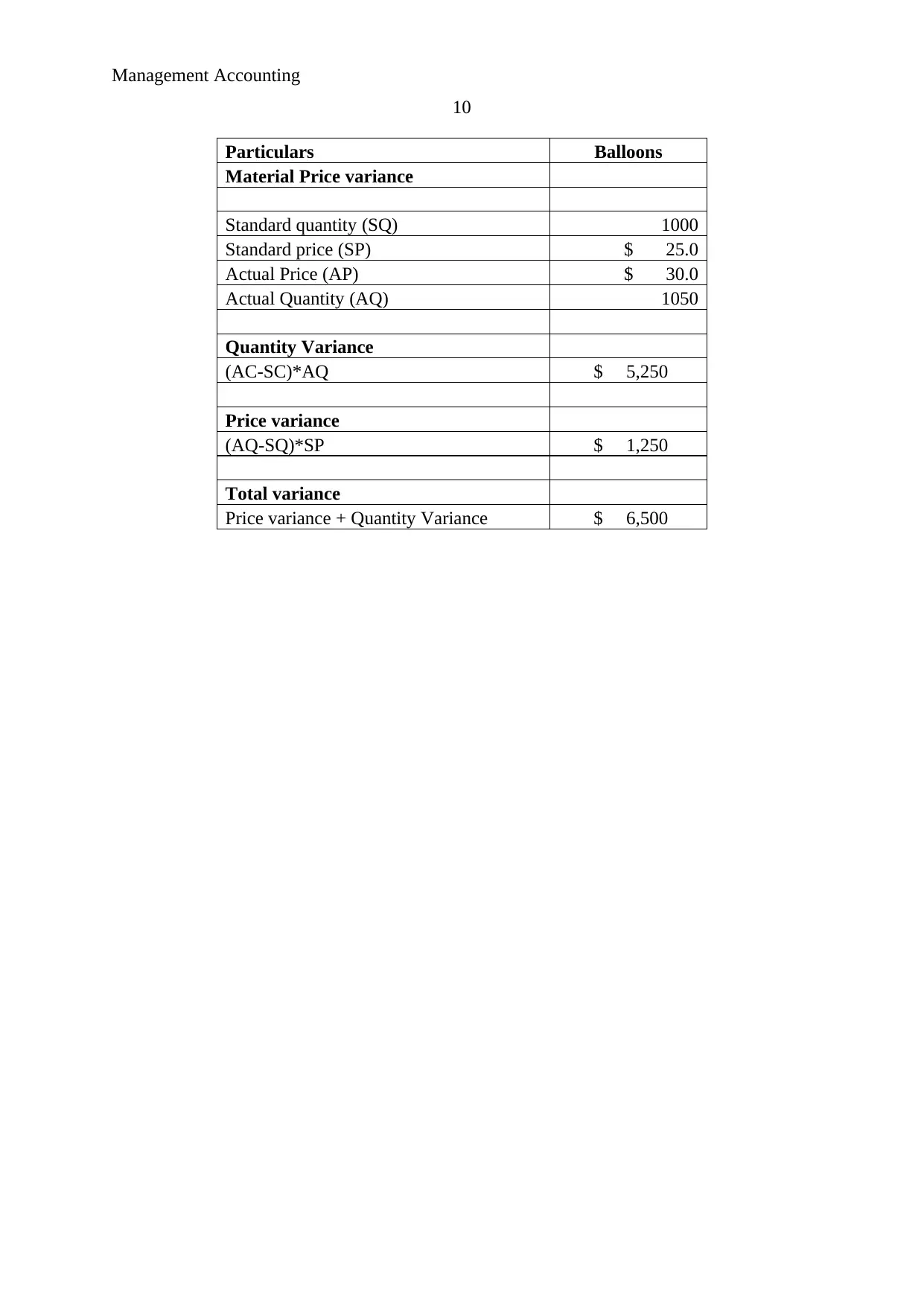

This project report analyzes the financial performance of a BBQ and Balloons business through the lens of management accounting principles. The report begins with an introduction to management accounting and its role in organizational decision-making, followed by an income statement analysis of the business. The report then delves into labor cost calculations, activity-based costing, and variance analysis to assess the profitability and efficiency of the business. The analysis includes calculations of labor costs per unit, activity rates, and net customer margins for both barbecues and balloons. The report also addresses qualitative aspects, such as the division of income among partners and the strategic implications of selling balloons. Furthermore, it covers planning budgets and variance analysis for material costs. The report concludes with references to relevant academic sources, providing a comprehensive overview of management accounting concepts applied to a real-world business scenario.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.