MAA262 Management Accounting: Purity Ltd Revenue Budget, 2019

VerifiedAdded on 2023/04/19

|13

|2401

|118

Homework Assignment

AI Summary

This assignment solution covers various aspects of management accounting, including the preparation of a revenue budget for Purity Ltd, calculation of minimum production volume, and analysis of beginning inventory. It also addresses cash flow estimation, return on investment (ROI) analysis for different divisions, and the calculation of residual income under varying assumptions. Furthermore, the solution advises on production arrangements to maximize profit, performs direct material and labor variance analysis, and links these variances to assess their overall impact on the company. The analysis incorporates relevant references to support the findings and recommendations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................4

a) Revenues budget for Purity Ltd for the year ending 31 December 2019................................4

b) Minimum number of 1-litre bottles Purity Ltd must produce during 2019.............................4

c) The amount of beginning inventory of 15-litre containers on 1 January 2019.......................4

Question 2........................................................................................................................................5

Calculation of the estimated cash received from debtors in May 2015.......................................5

Question 3........................................................................................................................................5

a) Which Division is more successful on the basis of ROI.........................................................5

b) Calculation of Residual income under each of assumption....................................................6

c) ROI may lead to bad decision and ways to overcome this problem........................................6

Question 4........................................................................................................................................7

Advise the company how to arrange the production of each product to maximize the

company’s profit..........................................................................................................................7

Question 5........................................................................................................................................8

a)Direct materials price and quantity variances...........................................................................8

b) Direct labor rate and efficiency variances...............................................................................9

c) Linked in the variance computed in part (a) and (b).............................................................10

References......................................................................................................................................11

Question 1........................................................................................................................................4

a) Revenues budget for Purity Ltd for the year ending 31 December 2019................................4

b) Minimum number of 1-litre bottles Purity Ltd must produce during 2019.............................4

c) The amount of beginning inventory of 15-litre containers on 1 January 2019.......................4

Question 2........................................................................................................................................5

Calculation of the estimated cash received from debtors in May 2015.......................................5

Question 3........................................................................................................................................5

a) Which Division is more successful on the basis of ROI.........................................................5

b) Calculation of Residual income under each of assumption....................................................6

c) ROI may lead to bad decision and ways to overcome this problem........................................6

Question 4........................................................................................................................................7

Advise the company how to arrange the production of each product to maximize the

company’s profit..........................................................................................................................7

Question 5........................................................................................................................................8

a)Direct materials price and quantity variances...........................................................................8

b) Direct labor rate and efficiency variances...............................................................................9

c) Linked in the variance computed in part (a) and (b).............................................................10

References......................................................................................................................................11

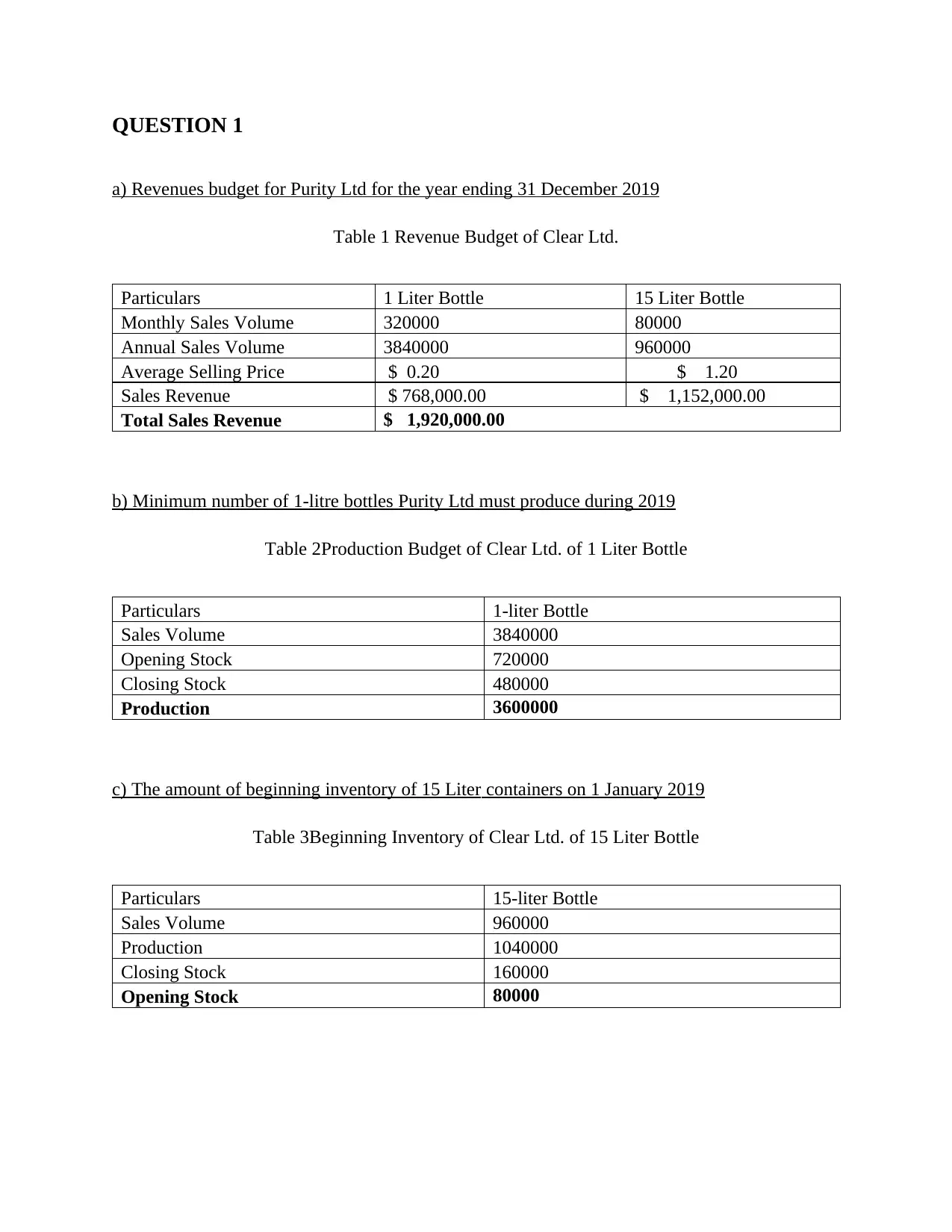

QUESTION 1

a) Revenues budget for Purity Ltd for the year ending 31 December 2019

Table 1 Revenue Budget of Clear Ltd.

Particulars 1 Liter Bottle 15 Liter Bottle

Monthly Sales Volume 320000 80000

Annual Sales Volume 3840000 960000

Average Selling Price $ 0.20 $ 1.20

Sales Revenue $ 768,000.00 $ 1,152,000.00

Total Sales Revenue $ 1,920,000.00

b) Minimum number of 1-litre bottles Purity Ltd must produce during 2019

Table 2Production Budget of Clear Ltd. of 1 Liter Bottle

Particulars 1-liter Bottle

Sales Volume 3840000

Opening Stock 720000

Closing Stock 480000

Production 3600000

c) The amount of beginning inventory of 15 Liter containers on 1 January 2019

Table 3Beginning Inventory of Clear Ltd. of 15 Liter Bottle

Particulars 15-liter Bottle

Sales Volume 960000

Production 1040000

Closing Stock 160000

Opening Stock 80000

a) Revenues budget for Purity Ltd for the year ending 31 December 2019

Table 1 Revenue Budget of Clear Ltd.

Particulars 1 Liter Bottle 15 Liter Bottle

Monthly Sales Volume 320000 80000

Annual Sales Volume 3840000 960000

Average Selling Price $ 0.20 $ 1.20

Sales Revenue $ 768,000.00 $ 1,152,000.00

Total Sales Revenue $ 1,920,000.00

b) Minimum number of 1-litre bottles Purity Ltd must produce during 2019

Table 2Production Budget of Clear Ltd. of 1 Liter Bottle

Particulars 1-liter Bottle

Sales Volume 3840000

Opening Stock 720000

Closing Stock 480000

Production 3600000

c) The amount of beginning inventory of 15 Liter containers on 1 January 2019

Table 3Beginning Inventory of Clear Ltd. of 15 Liter Bottle

Particulars 15-liter Bottle

Sales Volume 960000

Production 1040000

Closing Stock 160000

Opening Stock 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

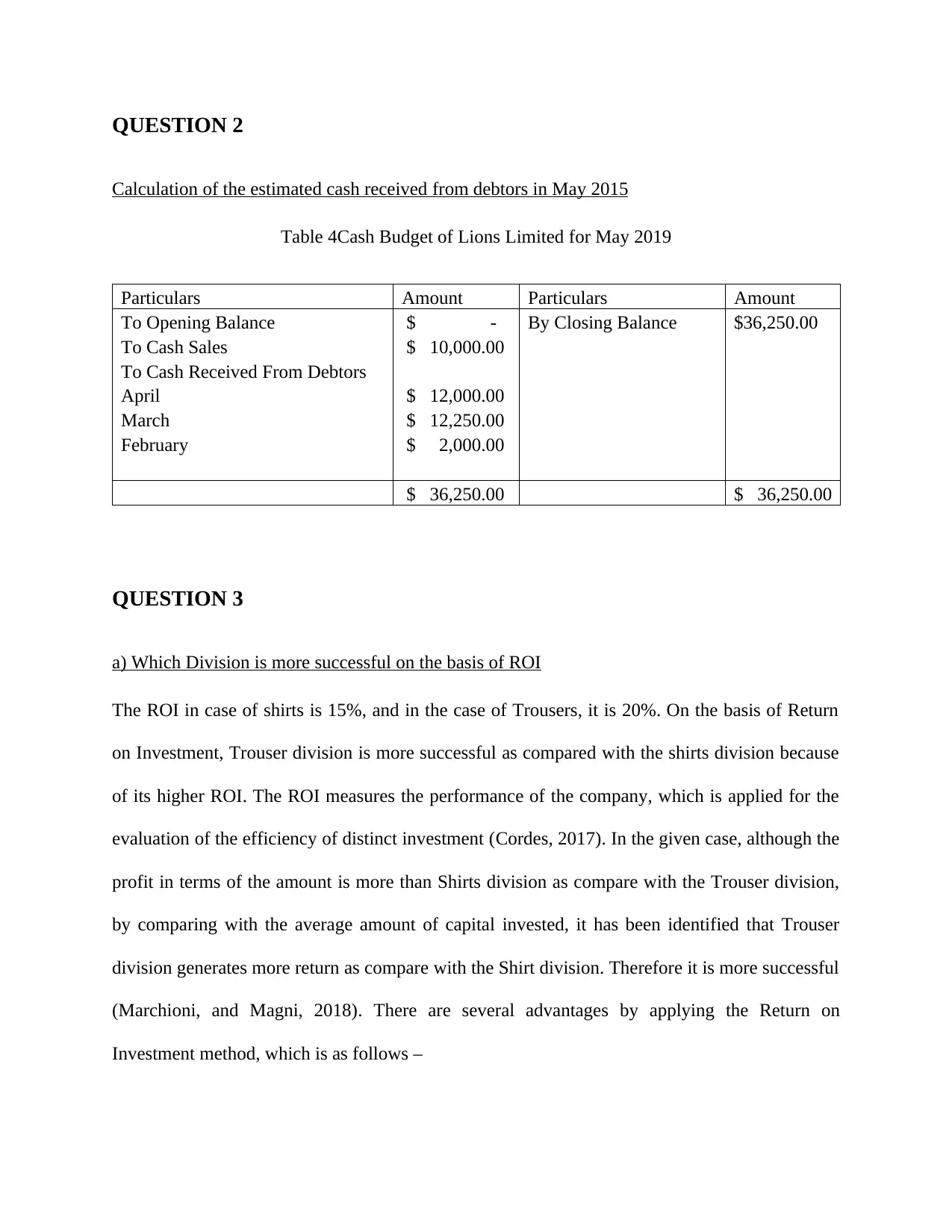

QUESTION 2

Calculation of the estimated cash received from debtors in May 2015

Table 4Cash Budget of Lions Limited for May 2019

Particulars Amount Particulars Amount

To Opening Balance $ - By Closing Balance $36,250.00

To Cash Sales $ 10,000.00

To Cash Received From Debtors

April $ 12,000.00

March $ 12,250.00

February $ 2,000.00

$ 36,250.00 $ 36,250.00

QUESTION 3

a) Which Division is more successful on the basis of ROI

The ROI in case of shirts is 15%, and in the case of Trousers, it is 20%. On the basis of Return

on Investment, Trouser division is more successful as compared with the shirts division because

of its higher ROI. The ROI measures the performance of the company, which is applied for the

evaluation of the efficiency of distinct investment (Cordes, 2017). In the given case, although the

profit in terms of the amount is more than Shirts division as compare with the Trouser division,

by comparing with the average amount of capital invested, it has been identified that Trouser

division generates more return as compare with the Shirt division. Therefore it is more successful

(Marchioni, and Magni, 2018). There are several advantages by applying the Return on

Investment method, which is as follows –

Calculation of the estimated cash received from debtors in May 2015

Table 4Cash Budget of Lions Limited for May 2019

Particulars Amount Particulars Amount

To Opening Balance $ - By Closing Balance $36,250.00

To Cash Sales $ 10,000.00

To Cash Received From Debtors

April $ 12,000.00

March $ 12,250.00

February $ 2,000.00

$ 36,250.00 $ 36,250.00

QUESTION 3

a) Which Division is more successful on the basis of ROI

The ROI in case of shirts is 15%, and in the case of Trousers, it is 20%. On the basis of Return

on Investment, Trouser division is more successful as compared with the shirts division because

of its higher ROI. The ROI measures the performance of the company, which is applied for the

evaluation of the efficiency of distinct investment (Cordes, 2017). In the given case, although the

profit in terms of the amount is more than Shirts division as compare with the Trouser division,

by comparing with the average amount of capital invested, it has been identified that Trouser

division generates more return as compare with the Shirt division. Therefore it is more successful

(Marchioni, and Magni, 2018). There are several advantages by applying the Return on

Investment method, which is as follows –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

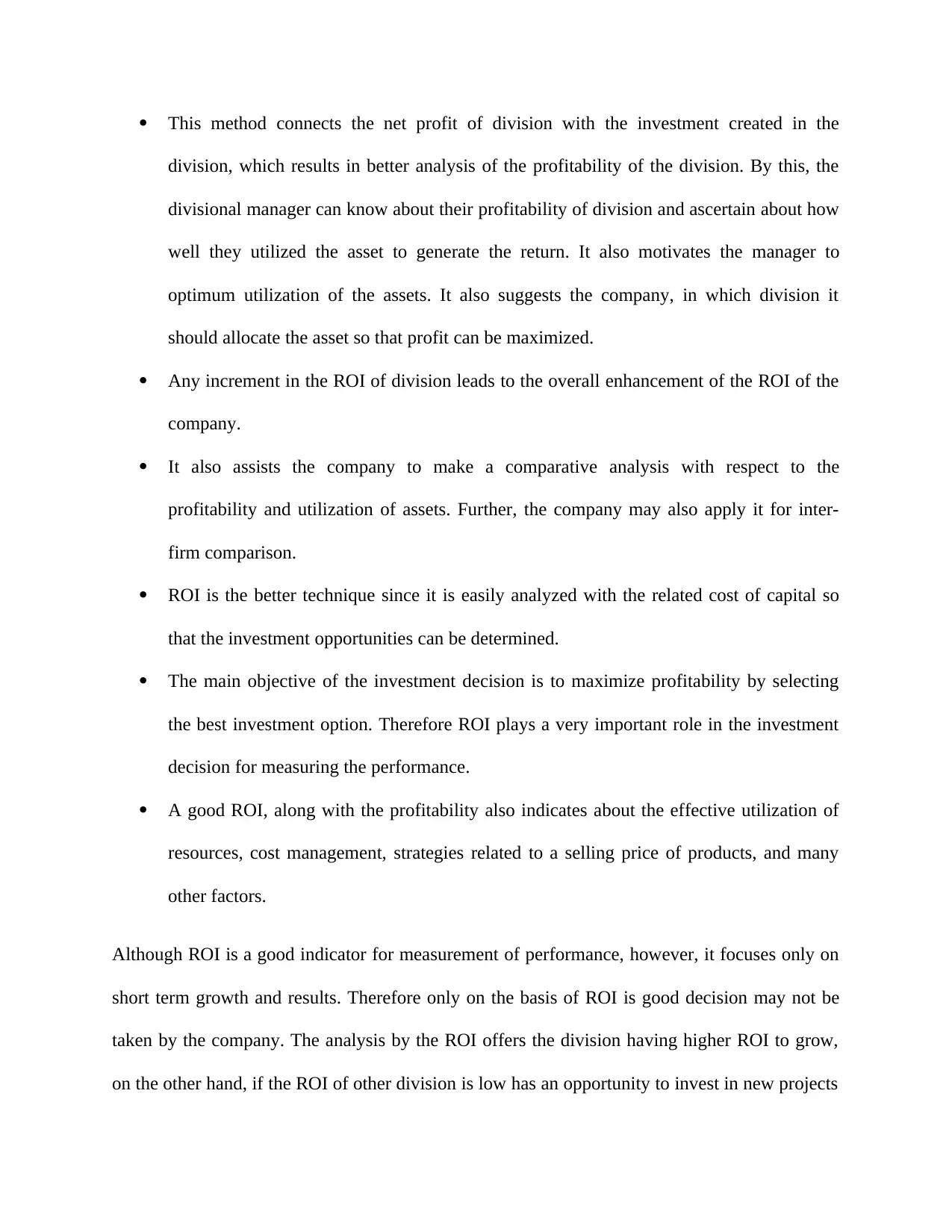

This method connects the net profit of division with the investment created in the

division, which results in better analysis of the profitability of the division. By this, the

divisional manager can know about their profitability of division and ascertain about how

well they utilized the asset to generate the return. It also motivates the manager to

optimum utilization of the assets. It also suggests the company, in which division it

should allocate the asset so that profit can be maximized.

Any increment in the ROI of division leads to the overall enhancement of the ROI of the

company.

It also assists the company to make a comparative analysis with respect to the

profitability and utilization of assets. Further, the company may also apply it for inter-

firm comparison.

ROI is the better technique since it is easily analyzed with the related cost of capital so

that the investment opportunities can be determined.

The main objective of the investment decision is to maximize profitability by selecting

the best investment option. Therefore ROI plays a very important role in the investment

decision for measuring the performance.

A good ROI, along with the profitability also indicates about the effective utilization of

resources, cost management, strategies related to a selling price of products, and many

other factors.

Although ROI is a good indicator for measurement of performance, however, it focuses only on

short term growth and results. Therefore only on the basis of ROI is good decision may not be

taken by the company. The analysis by the ROI offers the division having higher ROI to grow,

on the other hand, if the ROI of other division is low has an opportunity to invest in new projects

division, which results in better analysis of the profitability of the division. By this, the

divisional manager can know about their profitability of division and ascertain about how

well they utilized the asset to generate the return. It also motivates the manager to

optimum utilization of the assets. It also suggests the company, in which division it

should allocate the asset so that profit can be maximized.

Any increment in the ROI of division leads to the overall enhancement of the ROI of the

company.

It also assists the company to make a comparative analysis with respect to the

profitability and utilization of assets. Further, the company may also apply it for inter-

firm comparison.

ROI is the better technique since it is easily analyzed with the related cost of capital so

that the investment opportunities can be determined.

The main objective of the investment decision is to maximize profitability by selecting

the best investment option. Therefore ROI plays a very important role in the investment

decision for measuring the performance.

A good ROI, along with the profitability also indicates about the effective utilization of

resources, cost management, strategies related to a selling price of products, and many

other factors.

Although ROI is a good indicator for measurement of performance, however, it focuses only on

short term growth and results. Therefore only on the basis of ROI is good decision may not be

taken by the company. The analysis by the ROI offers the division having higher ROI to grow,

on the other hand, if the ROI of other division is low has an opportunity to invest in new projects

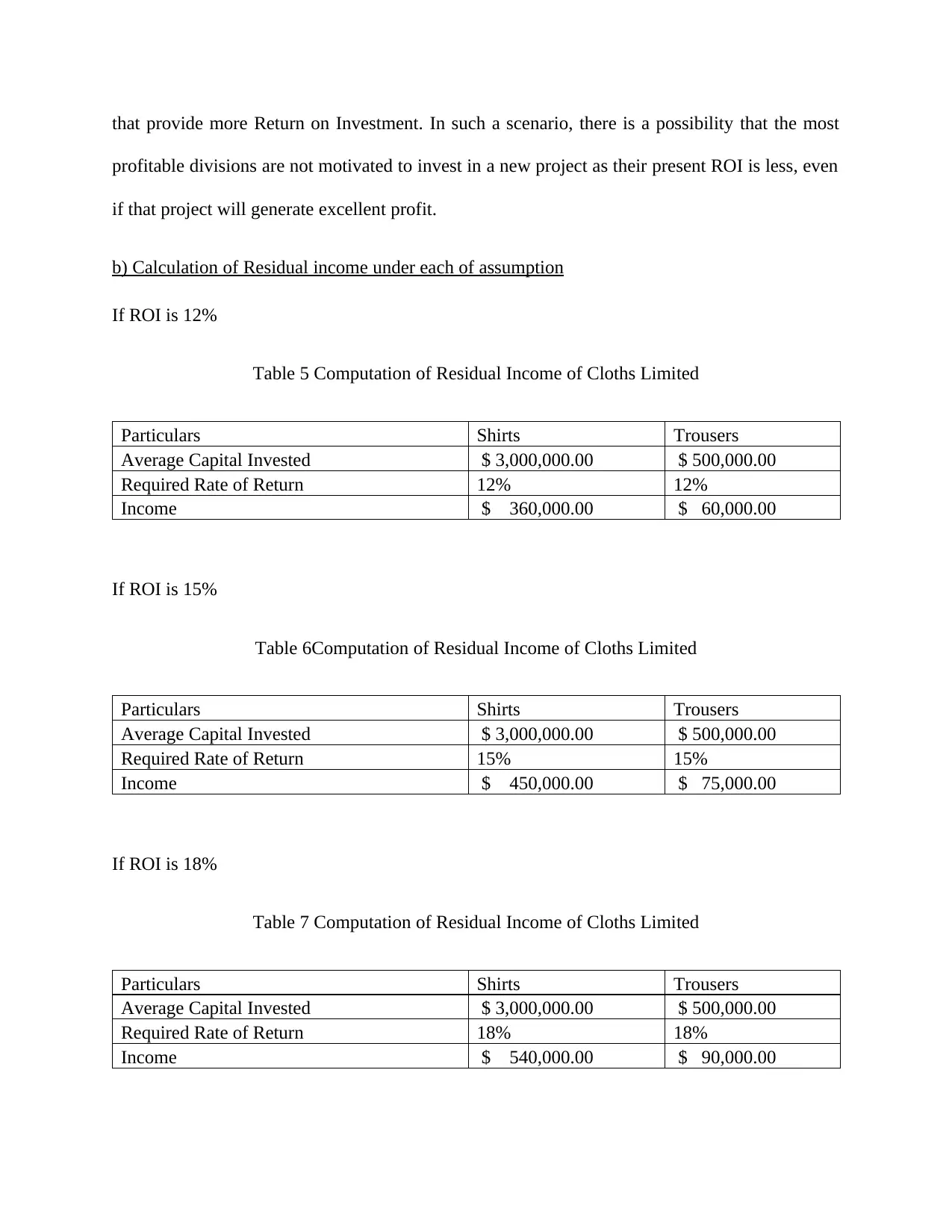

that provide more Return on Investment. In such a scenario, there is a possibility that the most

profitable divisions are not motivated to invest in a new project as their present ROI is less, even

if that project will generate excellent profit.

b) Calculation of Residual income under each of assumption

If ROI is 12%

Table 5 Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 12% 12%

Income $ 360,000.00 $ 60,000.00

If ROI is 15%

Table 6Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 15% 15%

Income $ 450,000.00 $ 75,000.00

If ROI is 18%

Table 7 Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 18% 18%

Income $ 540,000.00 $ 90,000.00

profitable divisions are not motivated to invest in a new project as their present ROI is less, even

if that project will generate excellent profit.

b) Calculation of Residual income under each of assumption

If ROI is 12%

Table 5 Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 12% 12%

Income $ 360,000.00 $ 60,000.00

If ROI is 15%

Table 6Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 15% 15%

Income $ 450,000.00 $ 75,000.00

If ROI is 18%

Table 7 Computation of Residual Income of Cloths Limited

Particulars Shirts Trousers

Average Capital Invested $ 3,000,000.00 $ 500,000.00

Required Rate of Return 18% 18%

Income $ 540,000.00 $ 90,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) ROI may lead to bad decision and ways to overcome this problem

The ROI is the management technique, which is implemented by several companies for their

departments (Tadeu, & et al. 2016). This technique motivates the divisional manager to

implement the action which may be contrary to the overall company. Further, it may also

influence the divisional manager to invest in only those projects, by which they can achieve the

higher ROI, even if by the investment in another project the value of the firm enhanced. It only

focuses on short term results and profitability. Moreover, it is also essential that companies must

use the same accounting policy and method with respect to the allocation of fixed asset,

valuation of inventory and fixed asset and other. The better technique as compared with the ROI

technique is Net Present Value. This method considers the inflows as well as outflows of project.

Further, it also considers the concept of the time value of money, by which the expected.

Therefore, the company should apply the Net Present Value method.

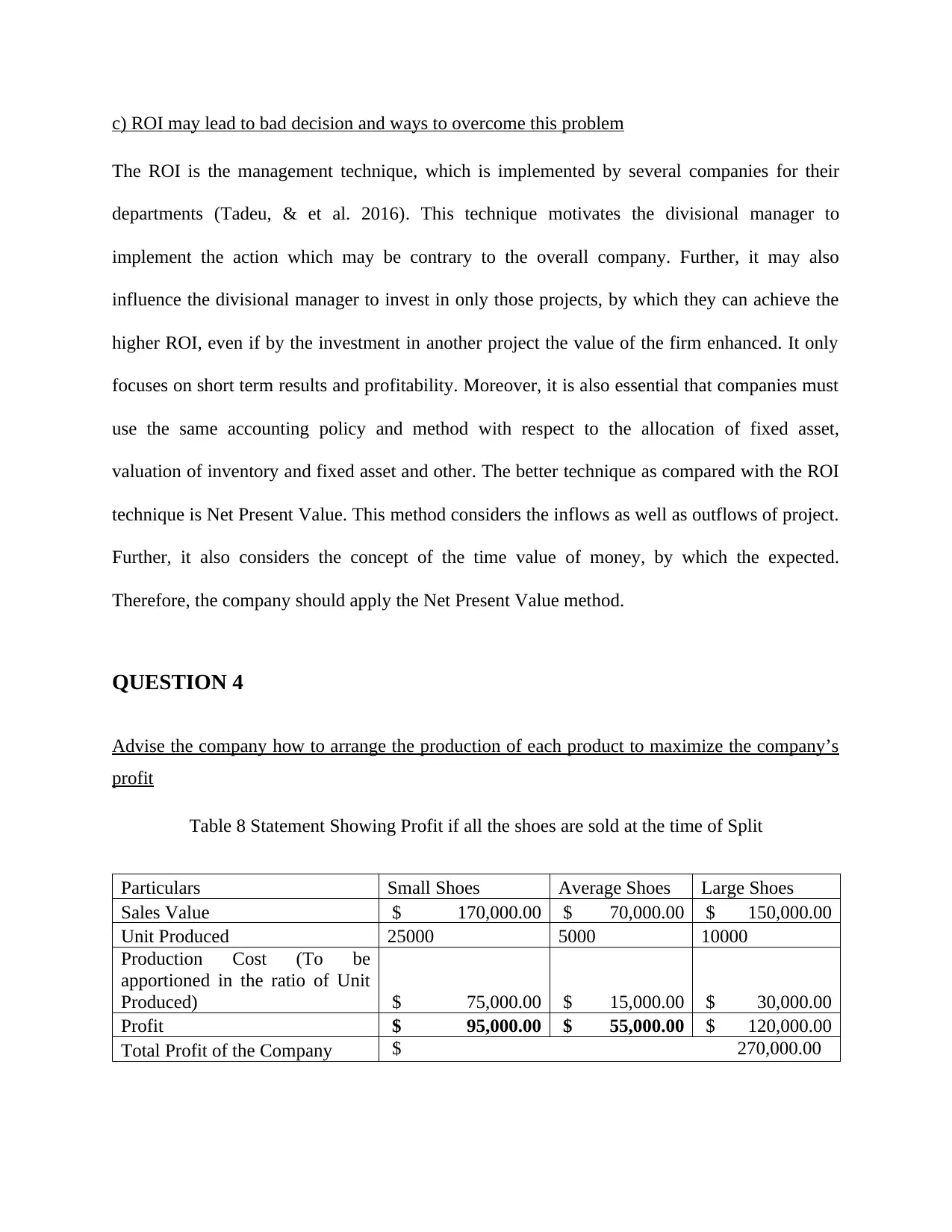

QUESTION 4

Advise the company how to arrange the production of each product to maximize the company’s

profit

Table 8 Statement Showing Profit if all the shoes are sold at the time of Split

Particulars Small Shoes Average Shoes Large Shoes

Sales Value $ 170,000.00 $ 70,000.00 $ 150,000.00

Unit Produced 25000 5000 10000

Production Cost (To be

apportioned in the ratio of Unit

Produced) $ 75,000.00 $ 15,000.00 $ 30,000.00

Profit $ 95,000.00 $ 55,000.00 $ 120,000.00

Total Profit of the Company $ 270,000.00

The ROI is the management technique, which is implemented by several companies for their

departments (Tadeu, & et al. 2016). This technique motivates the divisional manager to

implement the action which may be contrary to the overall company. Further, it may also

influence the divisional manager to invest in only those projects, by which they can achieve the

higher ROI, even if by the investment in another project the value of the firm enhanced. It only

focuses on short term results and profitability. Moreover, it is also essential that companies must

use the same accounting policy and method with respect to the allocation of fixed asset,

valuation of inventory and fixed asset and other. The better technique as compared with the ROI

technique is Net Present Value. This method considers the inflows as well as outflows of project.

Further, it also considers the concept of the time value of money, by which the expected.

Therefore, the company should apply the Net Present Value method.

QUESTION 4

Advise the company how to arrange the production of each product to maximize the company’s

profit

Table 8 Statement Showing Profit if all the shoes are sold at the time of Split

Particulars Small Shoes Average Shoes Large Shoes

Sales Value $ 170,000.00 $ 70,000.00 $ 150,000.00

Unit Produced 25000 5000 10000

Production Cost (To be

apportioned in the ratio of Unit

Produced) $ 75,000.00 $ 15,000.00 $ 30,000.00

Profit $ 95,000.00 $ 55,000.00 $ 120,000.00

Total Profit of the Company $ 270,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

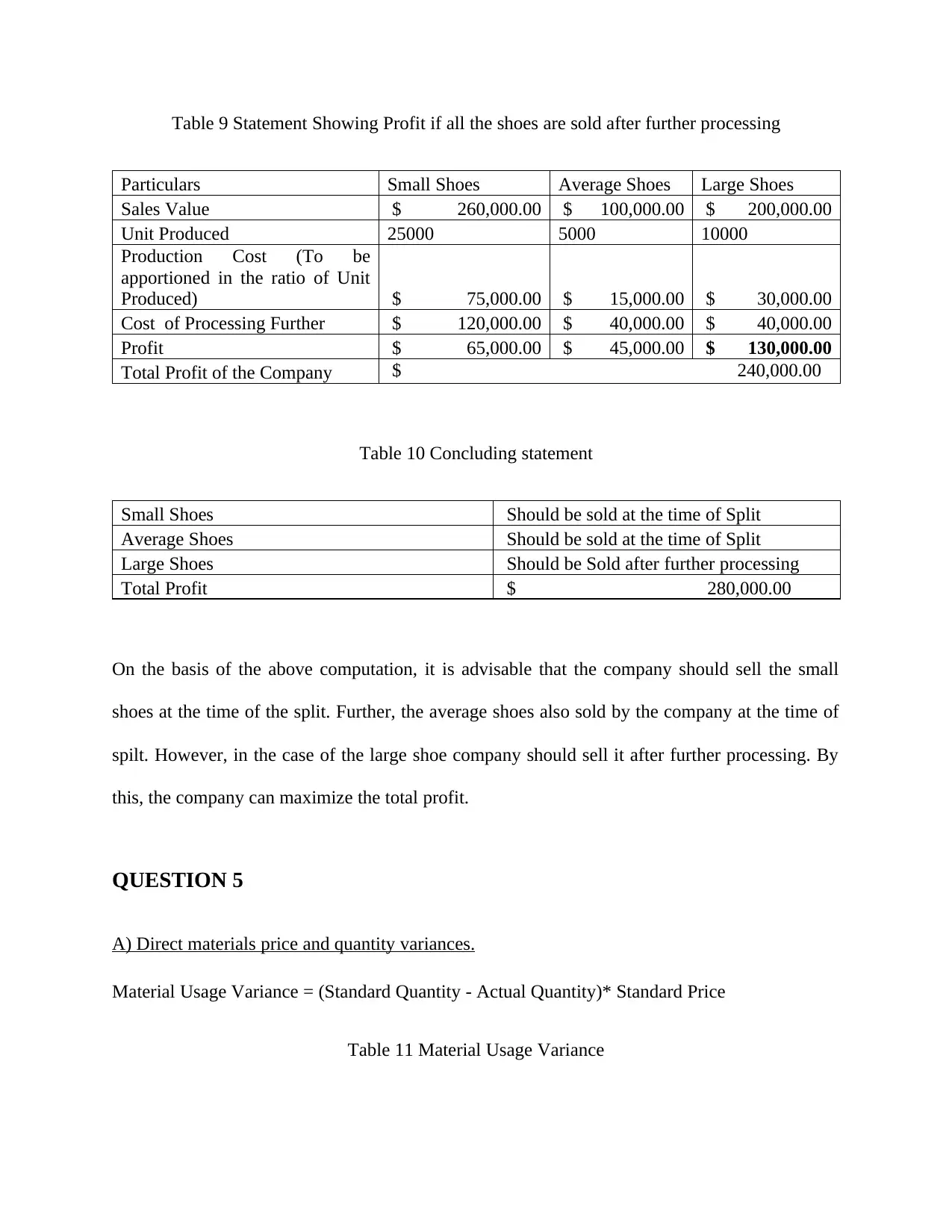

Table 9 Statement Showing Profit if all the shoes are sold after further processing

Particulars Small Shoes Average Shoes Large Shoes

Sales Value $ 260,000.00 $ 100,000.00 $ 200,000.00

Unit Produced 25000 5000 10000

Production Cost (To be

apportioned in the ratio of Unit

Produced) $ 75,000.00 $ 15,000.00 $ 30,000.00

Cost of Processing Further $ 120,000.00 $ 40,000.00 $ 40,000.00

Profit $ 65,000.00 $ 45,000.00 $ 130,000.00

Total Profit of the Company $ 240,000.00

Table 10 Concluding statement

Small Shoes Should be sold at the time of Split

Average Shoes Should be sold at the time of Split

Large Shoes Should be Sold after further processing

Total Profit $ 280,000.00

On the basis of the above computation, it is advisable that the company should sell the small

shoes at the time of the split. Further, the average shoes also sold by the company at the time of

spilt. However, in the case of the large shoe company should sell it after further processing. By

this, the company can maximize the total profit.

QUESTION 5

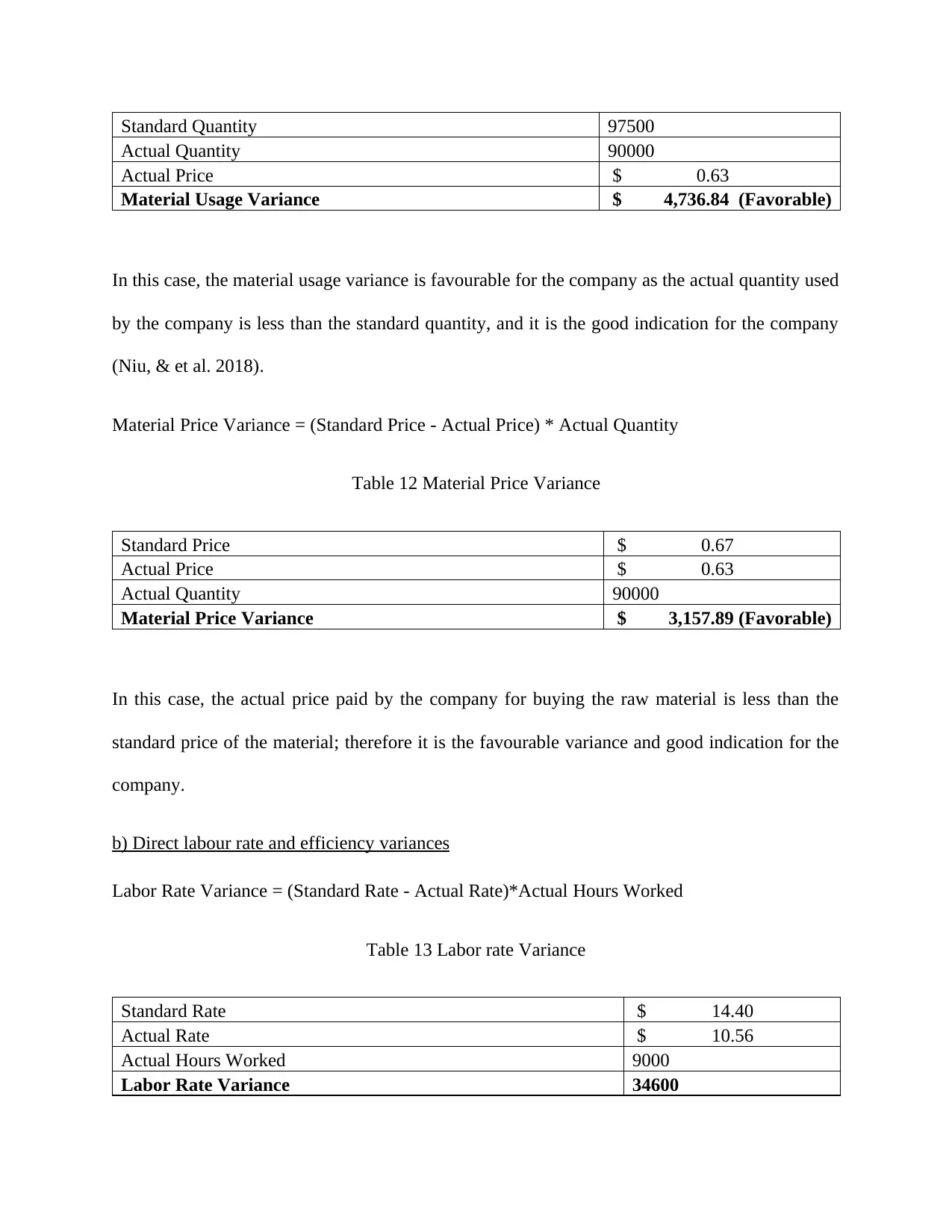

A) Direct materials price and quantity variances.

Material Usage Variance = (Standard Quantity - Actual Quantity)* Standard Price

Table 11 Material Usage Variance

Particulars Small Shoes Average Shoes Large Shoes

Sales Value $ 260,000.00 $ 100,000.00 $ 200,000.00

Unit Produced 25000 5000 10000

Production Cost (To be

apportioned in the ratio of Unit

Produced) $ 75,000.00 $ 15,000.00 $ 30,000.00

Cost of Processing Further $ 120,000.00 $ 40,000.00 $ 40,000.00

Profit $ 65,000.00 $ 45,000.00 $ 130,000.00

Total Profit of the Company $ 240,000.00

Table 10 Concluding statement

Small Shoes Should be sold at the time of Split

Average Shoes Should be sold at the time of Split

Large Shoes Should be Sold after further processing

Total Profit $ 280,000.00

On the basis of the above computation, it is advisable that the company should sell the small

shoes at the time of the split. Further, the average shoes also sold by the company at the time of

spilt. However, in the case of the large shoe company should sell it after further processing. By

this, the company can maximize the total profit.

QUESTION 5

A) Direct materials price and quantity variances.

Material Usage Variance = (Standard Quantity - Actual Quantity)* Standard Price

Table 11 Material Usage Variance

Standard Quantity 97500

Actual Quantity 90000

Actual Price $ 0.63

Material Usage Variance $ 4,736.84 (Favorable)

In this case, the material usage variance is favourable for the company as the actual quantity used

by the company is less than the standard quantity, and it is the good indication for the company

(Niu, & et al. 2018).

Material Price Variance = (Standard Price - Actual Price) * Actual Quantity

Table 12 Material Price Variance

Standard Price $ 0.67

Actual Price $ 0.63

Actual Quantity 90000

Material Price Variance $ 3,157.89 (Favorable)

In this case, the actual price paid by the company for buying the raw material is less than the

standard price of the material; therefore it is the favourable variance and good indication for the

company.

b) Direct labour rate and efficiency variances

Labor Rate Variance = (Standard Rate - Actual Rate)*Actual Hours Worked

Table 13 Labor rate Variance

Standard Rate $ 14.40

Actual Rate $ 10.56

Actual Hours Worked 9000

Labor Rate Variance 34600

Actual Quantity 90000

Actual Price $ 0.63

Material Usage Variance $ 4,736.84 (Favorable)

In this case, the material usage variance is favourable for the company as the actual quantity used

by the company is less than the standard quantity, and it is the good indication for the company

(Niu, & et al. 2018).

Material Price Variance = (Standard Price - Actual Price) * Actual Quantity

Table 12 Material Price Variance

Standard Price $ 0.67

Actual Price $ 0.63

Actual Quantity 90000

Material Price Variance $ 3,157.89 (Favorable)

In this case, the actual price paid by the company for buying the raw material is less than the

standard price of the material; therefore it is the favourable variance and good indication for the

company.

b) Direct labour rate and efficiency variances

Labor Rate Variance = (Standard Rate - Actual Rate)*Actual Hours Worked

Table 13 Labor rate Variance

Standard Rate $ 14.40

Actual Rate $ 10.56

Actual Hours Worked 9000

Labor Rate Variance 34600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

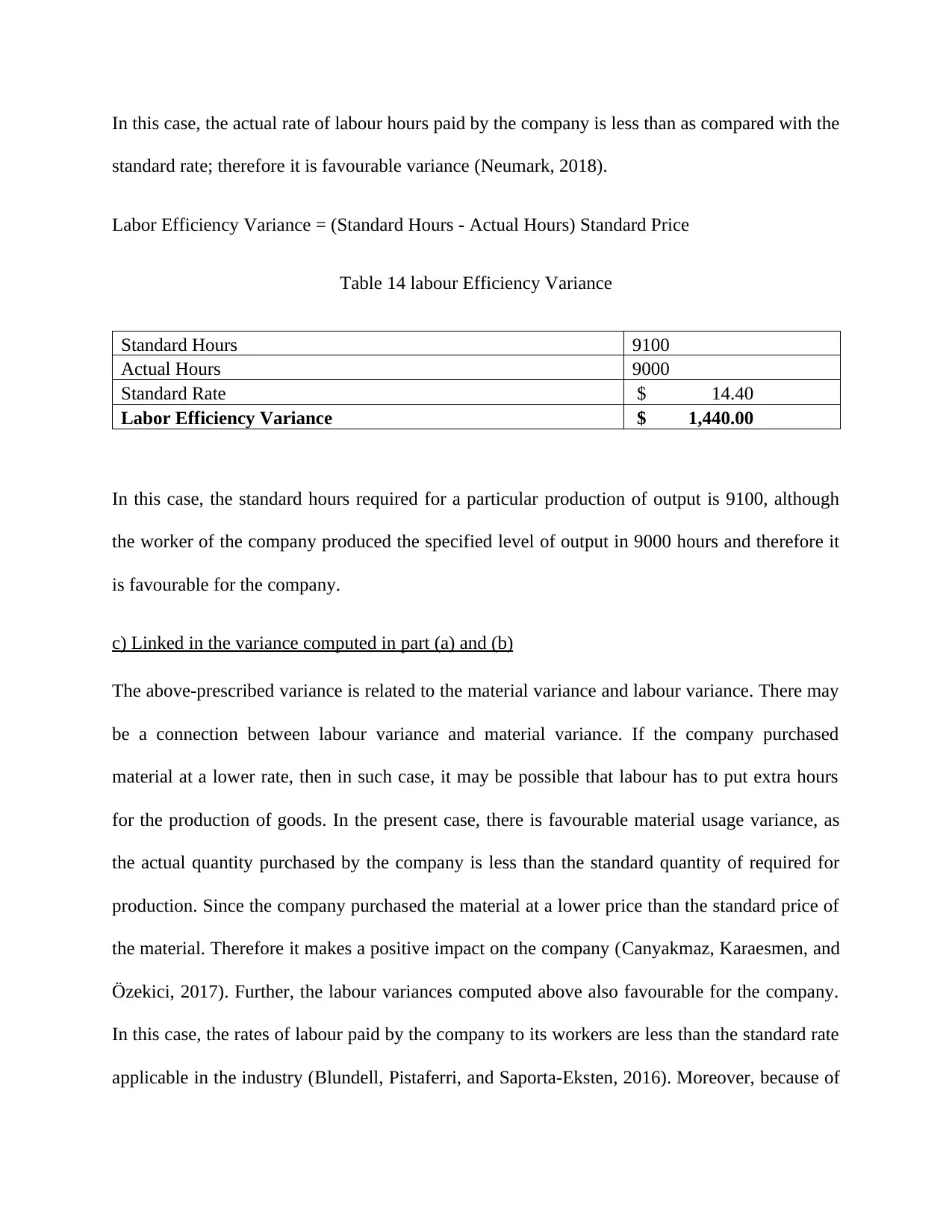

In this case, the actual rate of labour hours paid by the company is less than as compared with the

standard rate; therefore it is favourable variance (Neumark, 2018).

Labor Efficiency Variance = (Standard Hours - Actual Hours) Standard Price

Table 14 labour Efficiency Variance

Standard Hours 9100

Actual Hours 9000

Standard Rate $ 14.40

Labor Efficiency Variance $ 1,440.00

In this case, the standard hours required for a particular production of output is 9100, although

the worker of the company produced the specified level of output in 9000 hours and therefore it

is favourable for the company.

c) Linked in the variance computed in part (a) and (b)

The above-prescribed variance is related to the material variance and labour variance. There may

be a connection between labour variance and material variance. If the company purchased

material at a lower rate, then in such case, it may be possible that labour has to put extra hours

for the production of goods. In the present case, there is favourable material usage variance, as

the actual quantity purchased by the company is less than the standard quantity of required for

production. Since the company purchased the material at a lower price than the standard price of

the material. Therefore it makes a positive impact on the company (Canyakmaz, Karaesmen, and

Özekici, 2017). Further, the labour variances computed above also favourable for the company.

In this case, the rates of labour paid by the company to its workers are less than the standard rate

applicable in the industry (Blundell, Pistaferri, and Saporta-Eksten, 2016). Moreover, because of

standard rate; therefore it is favourable variance (Neumark, 2018).

Labor Efficiency Variance = (Standard Hours - Actual Hours) Standard Price

Table 14 labour Efficiency Variance

Standard Hours 9100

Actual Hours 9000

Standard Rate $ 14.40

Labor Efficiency Variance $ 1,440.00

In this case, the standard hours required for a particular production of output is 9100, although

the worker of the company produced the specified level of output in 9000 hours and therefore it

is favourable for the company.

c) Linked in the variance computed in part (a) and (b)

The above-prescribed variance is related to the material variance and labour variance. There may

be a connection between labour variance and material variance. If the company purchased

material at a lower rate, then in such case, it may be possible that labour has to put extra hours

for the production of goods. In the present case, there is favourable material usage variance, as

the actual quantity purchased by the company is less than the standard quantity of required for

production. Since the company purchased the material at a lower price than the standard price of

the material. Therefore it makes a positive impact on the company (Canyakmaz, Karaesmen, and

Özekici, 2017). Further, the labour variances computed above also favourable for the company.

In this case, the rates of labour paid by the company to its workers are less than the standard rate

applicable in the industry (Blundell, Pistaferri, and Saporta-Eksten, 2016). Moreover, because of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the good efficiency and effectiveness of worker, the actual hours applied for the production is

less than the standard hours; therefore the efficiency variance is favourable for the company

(Chang, Hong, and Karabarbounis, 2018). Overall, the material variance and labour variance

both are favourable for the company.

less than the standard hours; therefore the efficiency variance is favourable for the company

(Chang, Hong, and Karabarbounis, 2018). Overall, the material variance and labour variance

both are favourable for the company.

REFERENCES

Blundell, R., Pistaferri, L. and Saporta-Eksten, I., 2016. Consumption inequality and family

labor supply. American Economic Review, 106(2), pp.387-435.

Canyakmaz, C., Karaesmen, F. and Özekici, S., 2017. Minimum-Variance Hedging for

Managing Risks in Inventory Models with Price Fluctuations. Foundations and Trends® in

Technology, Information and Operations Management, 11(1-2), pp.107-123.

Chang, Y., Hong, J.H. and Karabarbounis, M., 2018. Labor market uncertainty and portfolio

choice puzzles. American Economic Journal: Macroeconomics, 10(2), pp.222-62.

Cordes, J.J., 2017. Using cost-benefit analysis and social return on investment to evaluate the

impact of social enterprise: Promises, implementation, and limitations. Evaluation and program

planning, 64(1), pp.98-104.

Marchioni, A. and Magni, C.A., 2018. Investment decisions and sensitivity analysis: NPV-

consistency of rates of return. European Journal of Operational Research, 268(1), pp.361-372.

Neumark, D., 2018. Experimental research on labour market discrimination. Journal of

Economic Literature, 56(3), pp.799-866.

Niu, B., Chu, L.K., Ni, J. and Wang, J., 2018. Buy now and price later: Supply contracts with

time-consistent mean-variance financial hedgingAuthor-Name: Li, Qiang. European Journal of

Operational Research, 268(2), pp.582-595.

Blundell, R., Pistaferri, L. and Saporta-Eksten, I., 2016. Consumption inequality and family

labor supply. American Economic Review, 106(2), pp.387-435.

Canyakmaz, C., Karaesmen, F. and Özekici, S., 2017. Minimum-Variance Hedging for

Managing Risks in Inventory Models with Price Fluctuations. Foundations and Trends® in

Technology, Information and Operations Management, 11(1-2), pp.107-123.

Chang, Y., Hong, J.H. and Karabarbounis, M., 2018. Labor market uncertainty and portfolio

choice puzzles. American Economic Journal: Macroeconomics, 10(2), pp.222-62.

Cordes, J.J., 2017. Using cost-benefit analysis and social return on investment to evaluate the

impact of social enterprise: Promises, implementation, and limitations. Evaluation and program

planning, 64(1), pp.98-104.

Marchioni, A. and Magni, C.A., 2018. Investment decisions and sensitivity analysis: NPV-

consistency of rates of return. European Journal of Operational Research, 268(1), pp.361-372.

Neumark, D., 2018. Experimental research on labour market discrimination. Journal of

Economic Literature, 56(3), pp.799-866.

Niu, B., Chu, L.K., Ni, J. and Wang, J., 2018. Buy now and price later: Supply contracts with

time-consistent mean-variance financial hedgingAuthor-Name: Li, Qiang. European Journal of

Operational Research, 268(2), pp.582-595.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.