MAA716 Assignment 1 - Accounting for Income Tax, T2 2017, Mamamia LTD

VerifiedAdded on 2020/03/04

|8

|902

|83

Homework Assignment

AI Summary

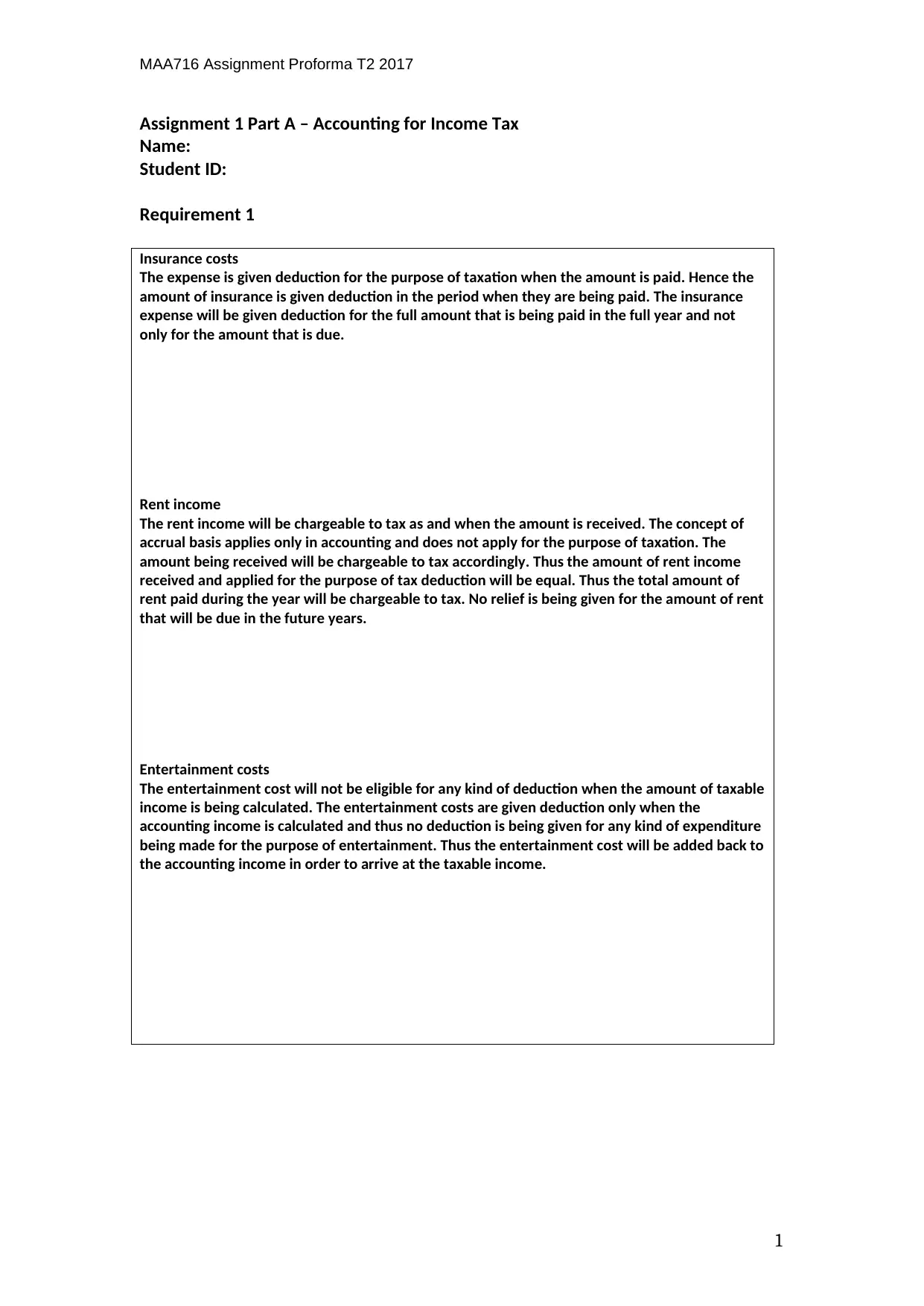

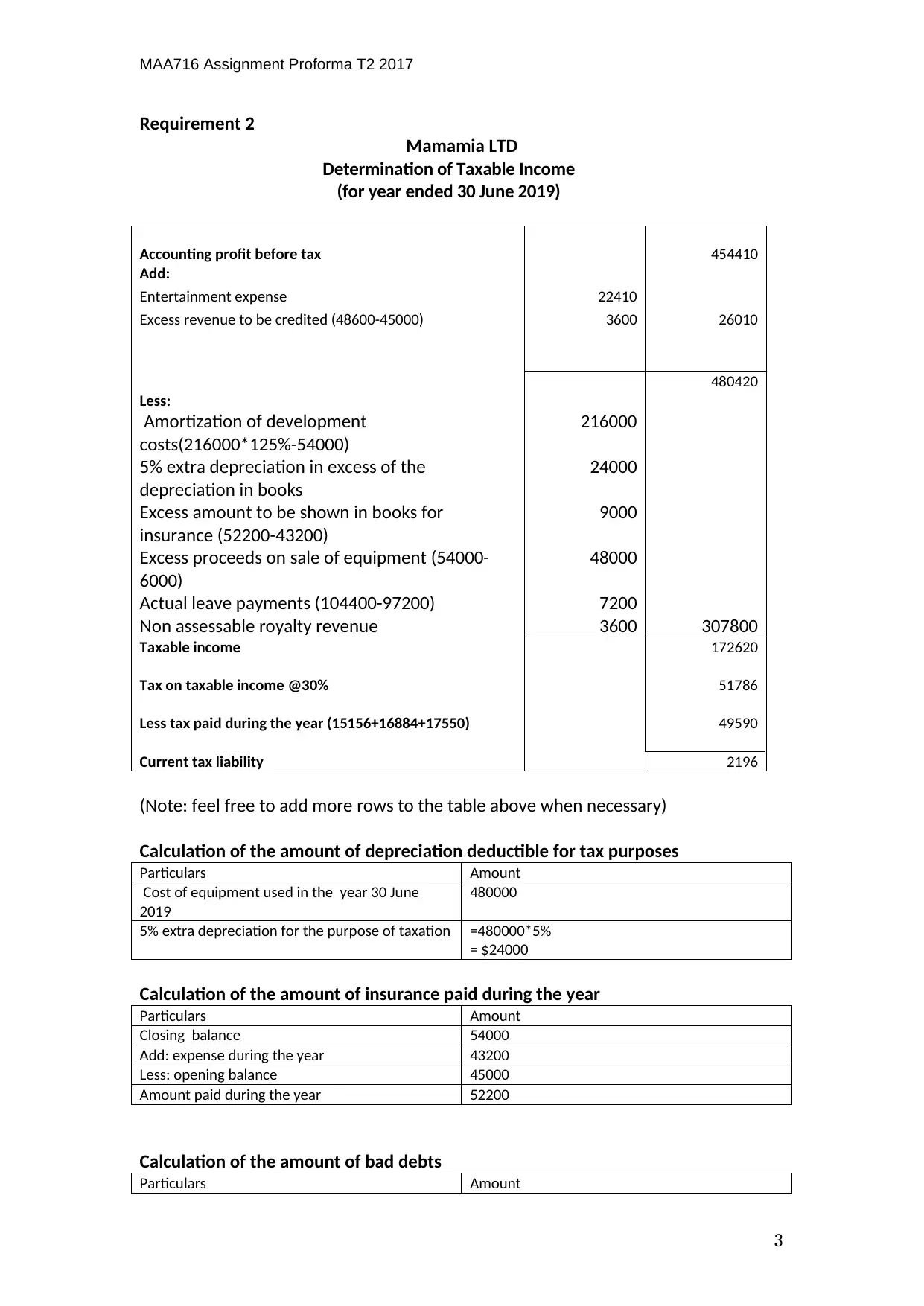

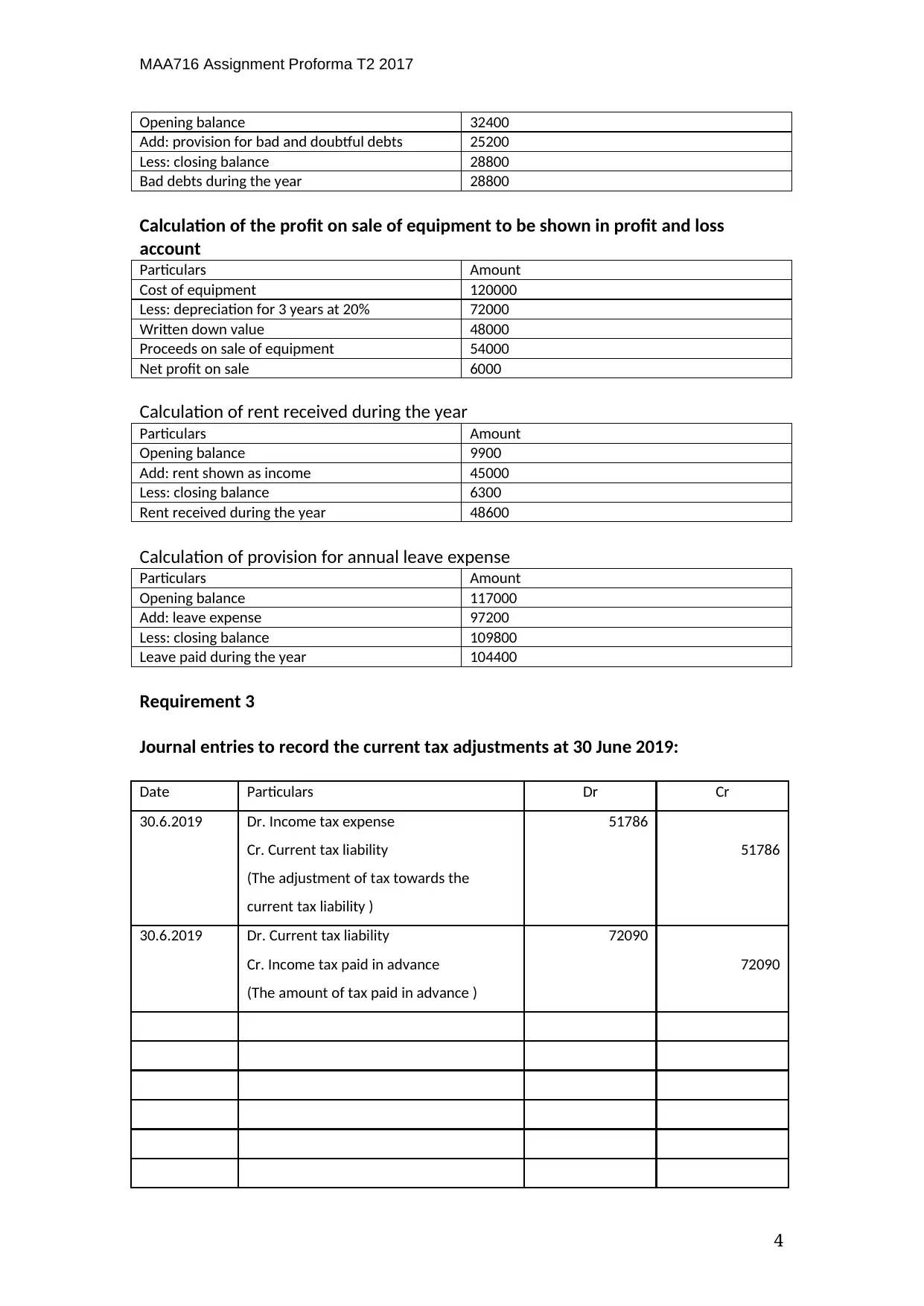

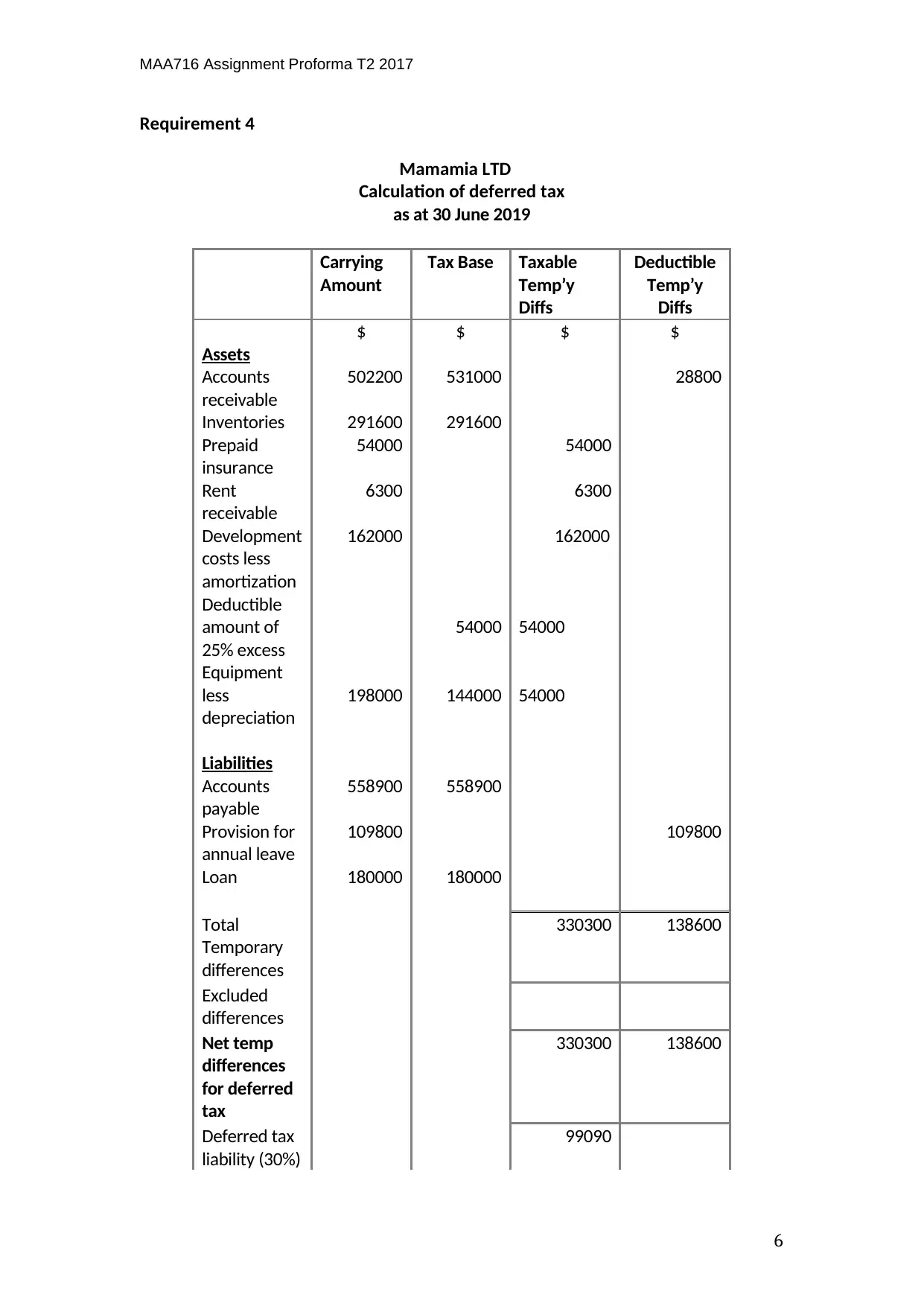

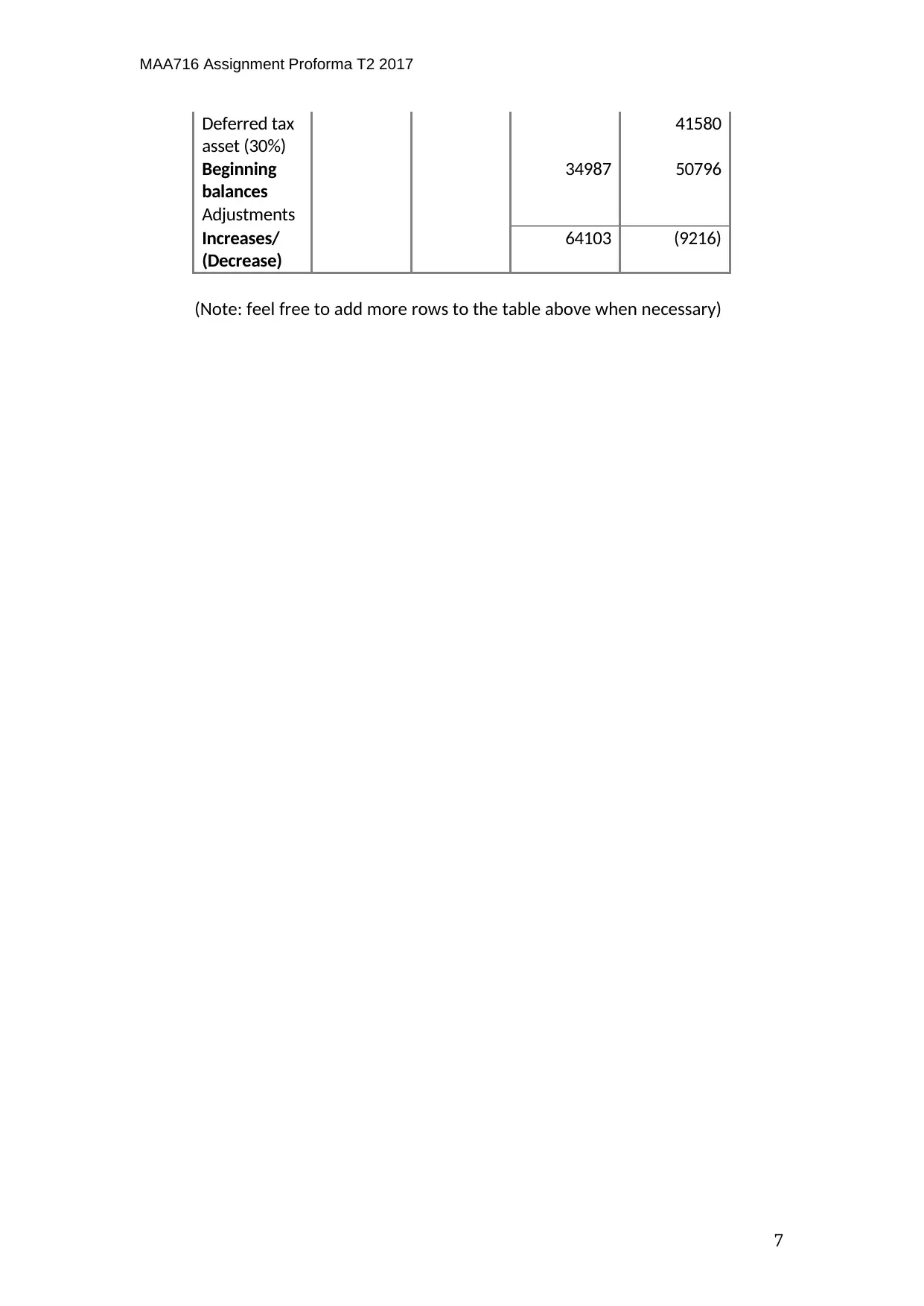

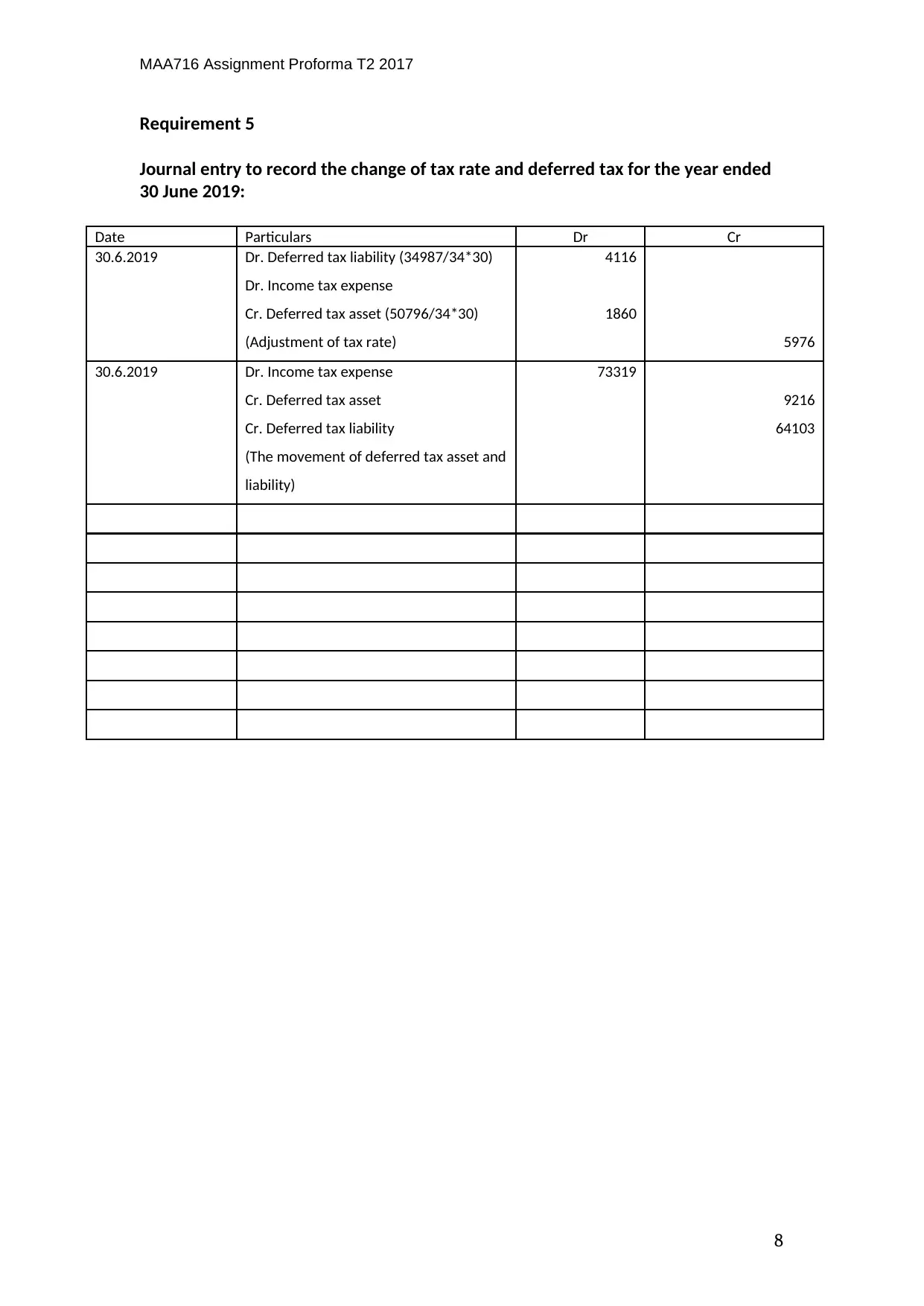

This assignment solution addresses the accounting for income tax, specifically focusing on the case of Mamamia LTD. It begins by outlining the tax treatment of various expenses and income items such as insurance costs, rent income, and entertainment costs. The solution then calculates Mamamia LTD's taxable income for the year ended 30 June 2019, including adjustments for entertainment expenses, amortization, depreciation, and other items. Furthermore, it calculates the depreciation, insurance, bad debts, profit on sale of equipment, rent received and leave expense. The solution also presents the journal entries required to record current tax adjustments and calculates deferred tax assets and liabilities, including the impact of a tax rate change. Finally, the solution provides detailed calculations and journal entries for deferred tax adjustments, offering a complete analysis of the company's tax position.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.