Strategic Management Accounting MAC007: Wattle Jet Case Stakeholders

VerifiedAdded on 2023/06/10

|4

|971

|88

Case Study

AI Summary

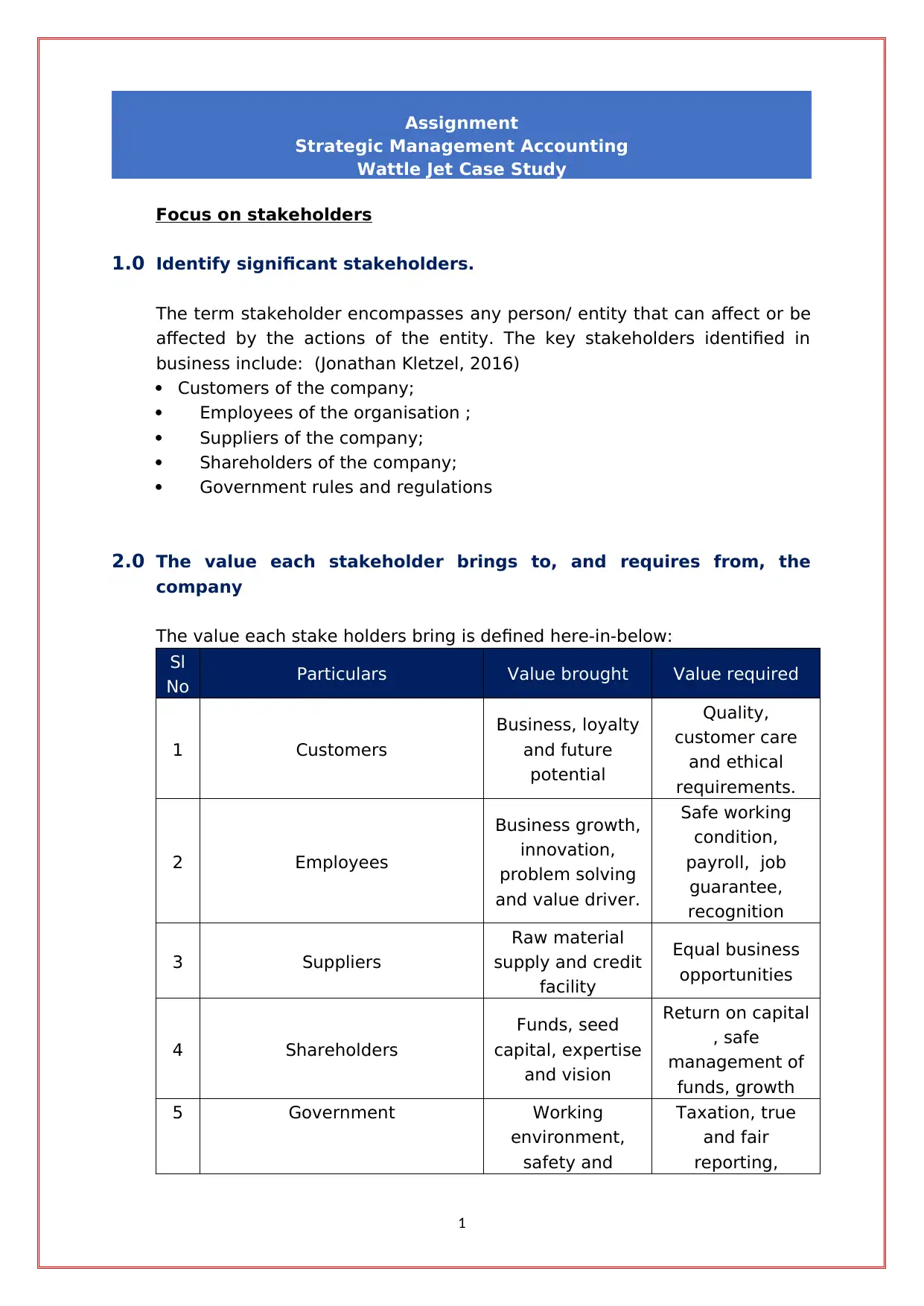

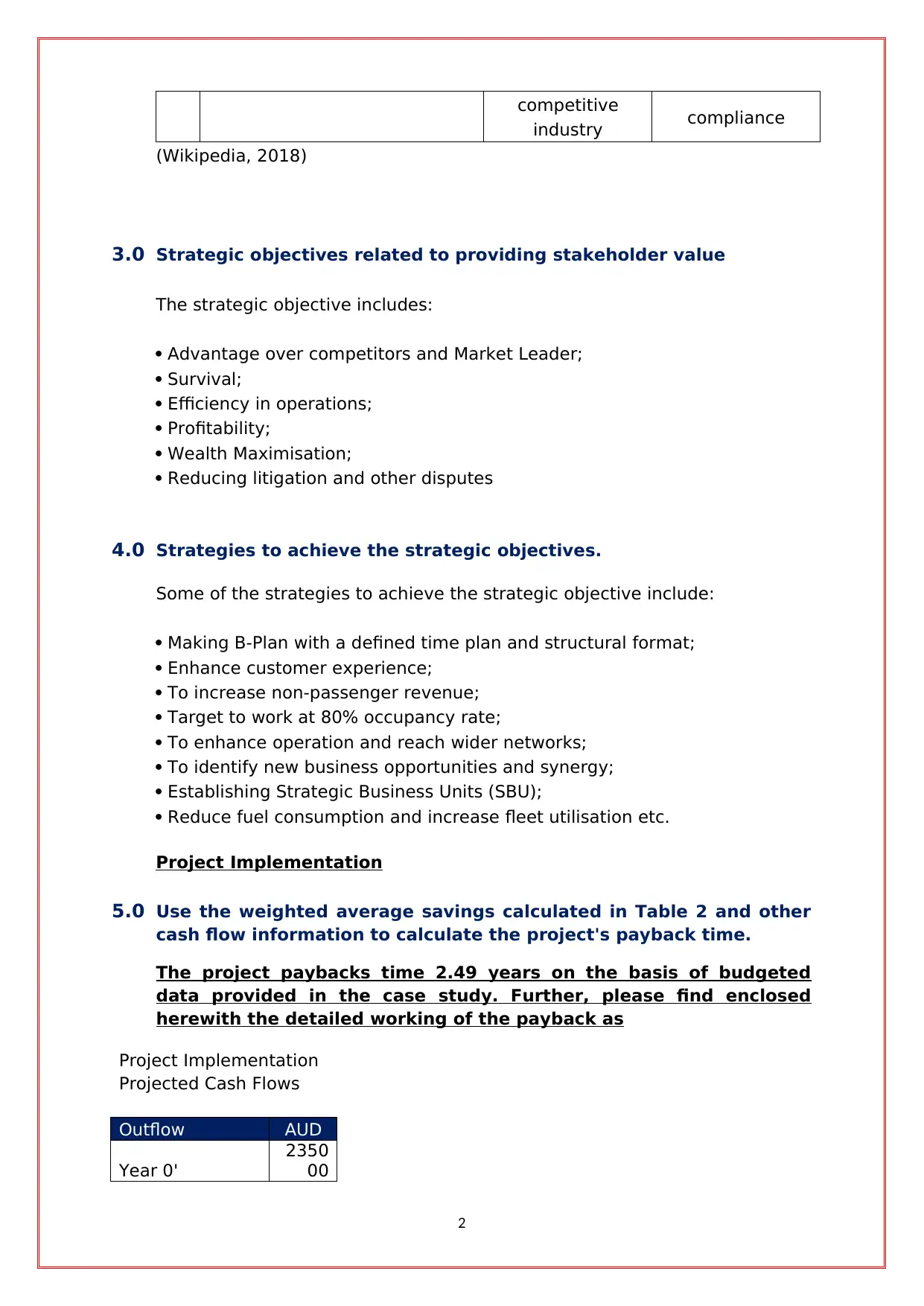

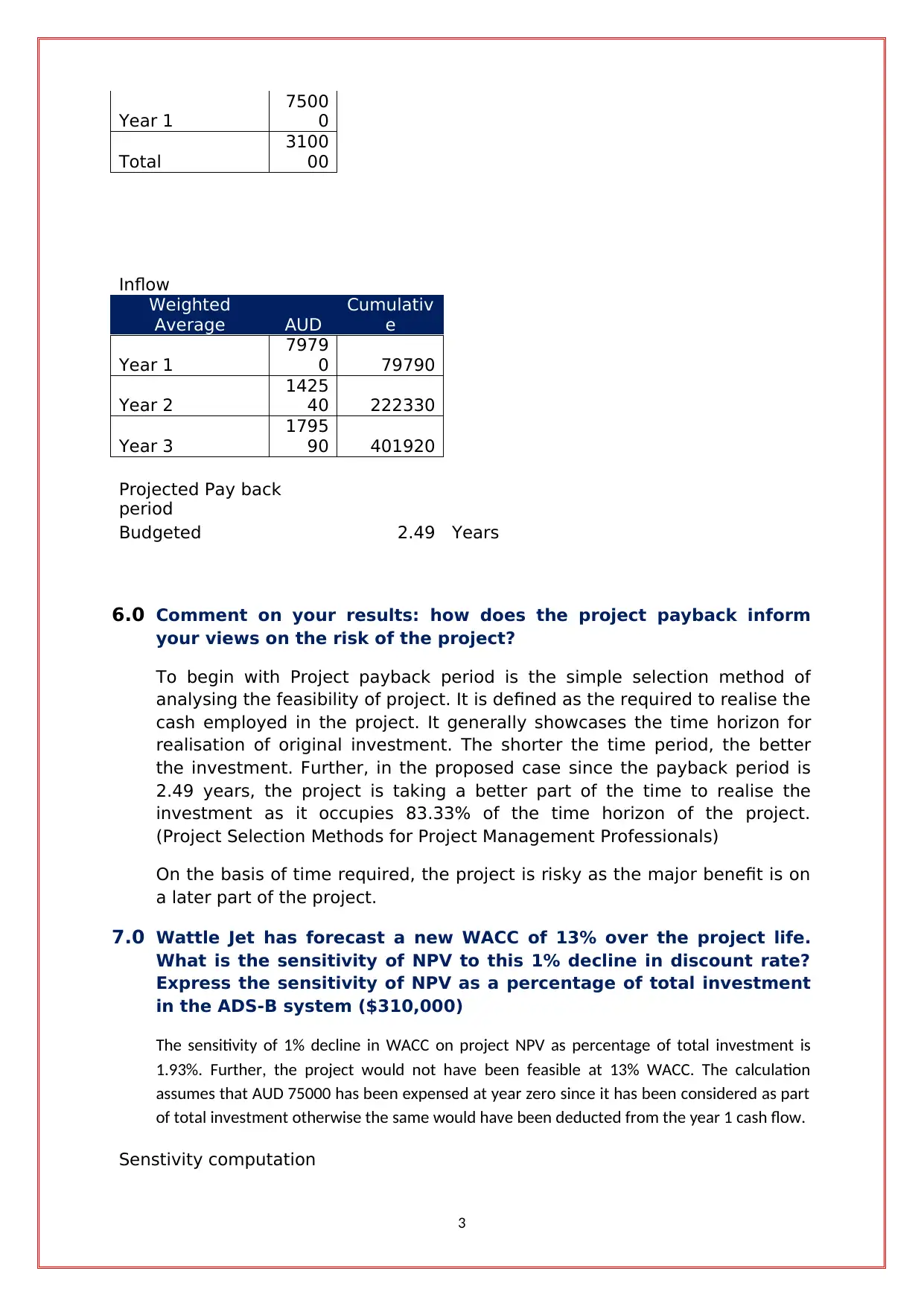

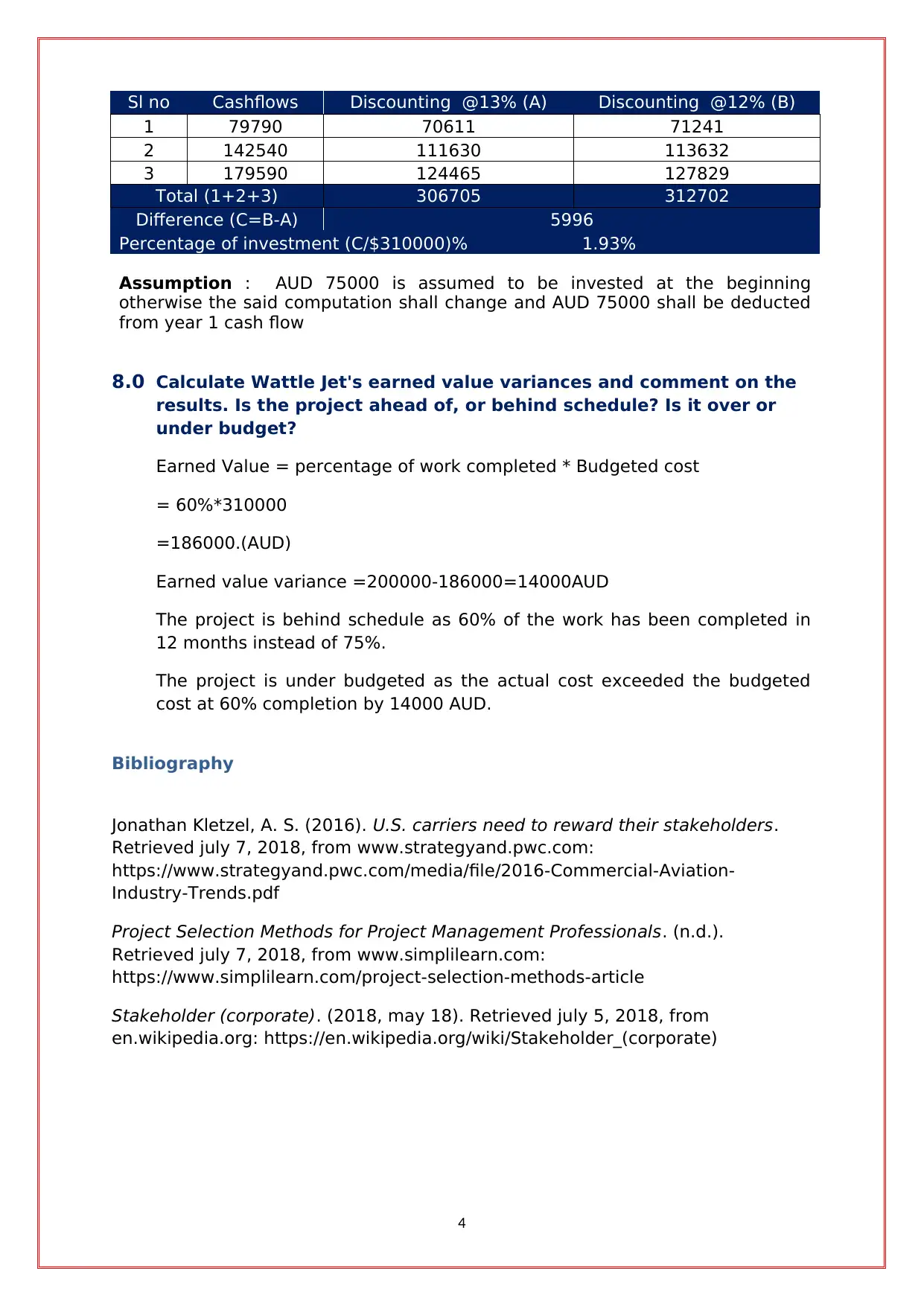

This case study solution focuses on Wattle Jet, analyzing its stakeholders, their value to the company, and related strategic objectives. It identifies key stakeholders such as customers, employees, suppliers, shareholders, and the government, detailing the value each brings and requires. The solution outlines strategic objectives like competitive advantage, survival, and profitability, and proposes strategies to achieve them, including B-plan development, customer experience enhancement, and operational efficiency. The project's payback time is calculated as 2.49 years, informing the project's risk assessment. Furthermore, it assesses the sensitivity of NPV to changes in the discount rate and evaluates earned value variances, determining the project's schedule and budget status. The analysis concludes with a bibliography referencing relevant sources, offering a comprehensive understanding of Wattle Jet's strategic management accounting challenges and potential solutions. Desklib offers more solved assignments and resources for students.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.