Macquarie University ECON334: Financial Econometrics Assignment

VerifiedAdded on 2023/06/04

|14

|1955

|219

Homework Assignment

AI Summary

This financial econometrics assignment focuses on time series analysis and forecasting, utilizing the 'SPREAD' dataset from 1957M01 to 2015M03. The assignment involves plotting the data, calculating Autocorrelation (ACF) and Partial Autocorrelation Functions (PACF), and selecting the best ARIMA model based on the Akaike Information Criterion (AIC). The analysis compares static and rolling window forecasting methods, as well as one-step-ahead and dynamic forecasting. The assignment also includes forecast evaluation, and considers the Ljung-Box test for residuals, using the chi-square test to assess autocorrelation. The results from different AR models are presented, along with forecast evaluation statistics such as RMSE, MAE, MAPE, SMAPE, Theil U1, and Theil U2. The concluding remarks discuss the trends and accuracy of the forecasting models applied to the 'SPREAD' data.

Financial Econometrics

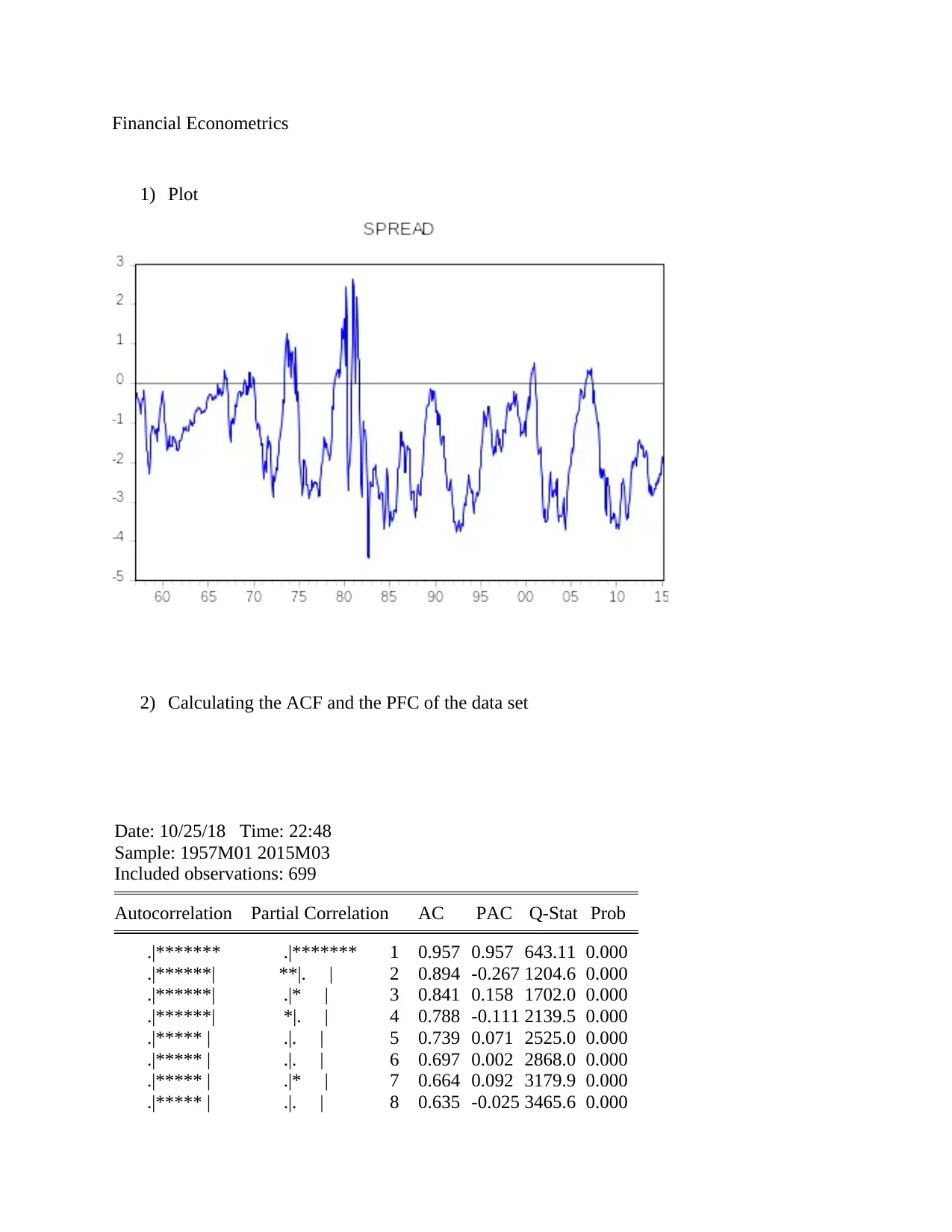

1) Plot

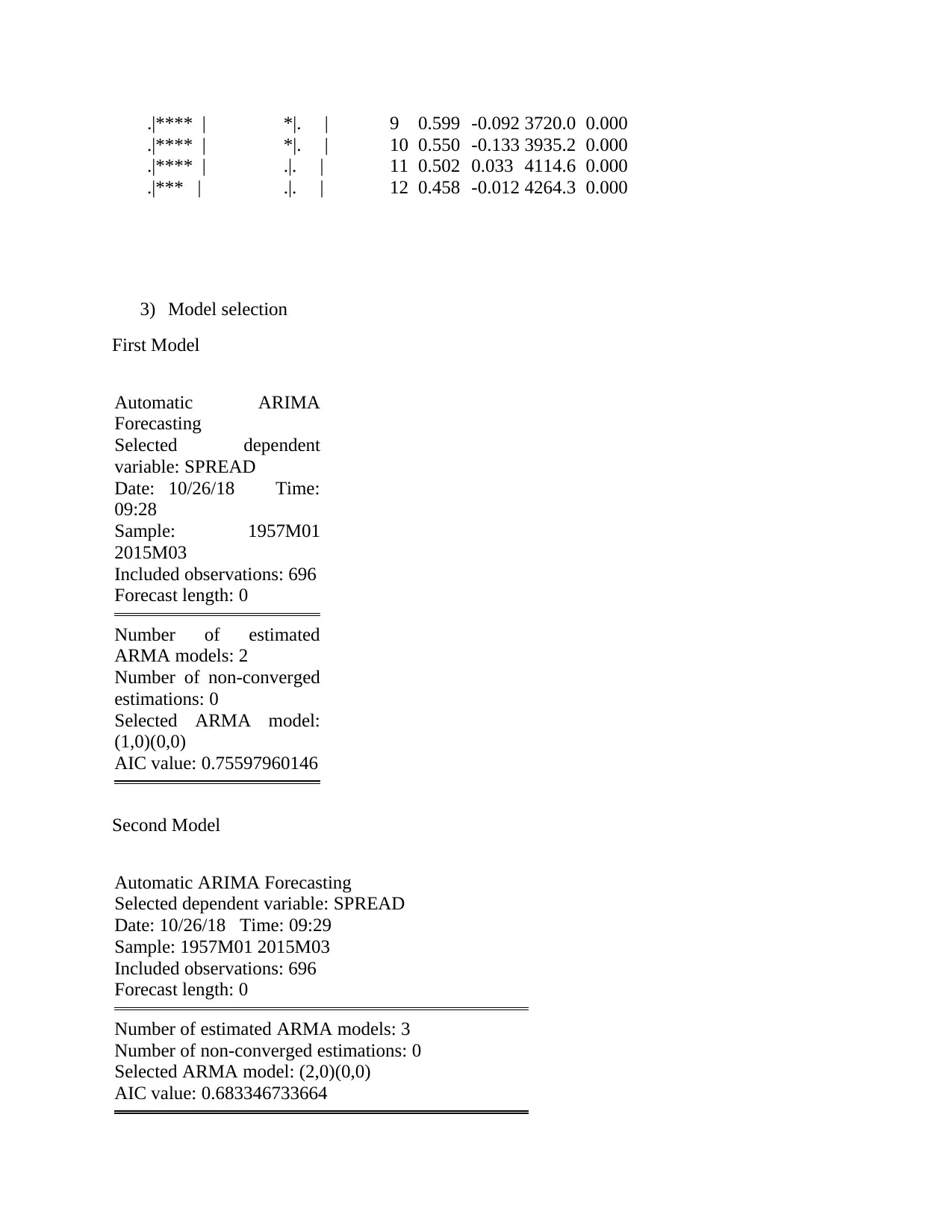

2) Calculating the ACF and the PFC of the data set

Date: 10/25/18 Time: 22:48

Sample: 1957M01 2015M03

Included observations: 699

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|******* .|******* 1 0.957 0.957 643.11 0.000

.|******| **|. | 2 0.894 -0.267 1204.6 0.000

.|******| .|* | 3 0.841 0.158 1702.0 0.000

.|******| *|. | 4 0.788 -0.111 2139.5 0.000

.|***** | .|. | 5 0.739 0.071 2525.0 0.000

.|***** | .|. | 6 0.697 0.002 2868.0 0.000

.|***** | .|* | 7 0.664 0.092 3179.9 0.000

.|***** | .|. | 8 0.635 -0.025 3465.6 0.000

1) Plot

2) Calculating the ACF and the PFC of the data set

Date: 10/25/18 Time: 22:48

Sample: 1957M01 2015M03

Included observations: 699

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|******* .|******* 1 0.957 0.957 643.11 0.000

.|******| **|. | 2 0.894 -0.267 1204.6 0.000

.|******| .|* | 3 0.841 0.158 1702.0 0.000

.|******| *|. | 4 0.788 -0.111 2139.5 0.000

.|***** | .|. | 5 0.739 0.071 2525.0 0.000

.|***** | .|. | 6 0.697 0.002 2868.0 0.000

.|***** | .|* | 7 0.664 0.092 3179.9 0.000

.|***** | .|. | 8 0.635 -0.025 3465.6 0.000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.|**** | *|. | 9 0.599 -0.092 3720.0 0.000

.|**** | *|. | 10 0.550 -0.133 3935.2 0.000

.|**** | .|. | 11 0.502 0.033 4114.6 0.000

.|*** | .|. | 12 0.458 -0.012 4264.3 0.000

3) Model selection

First Model

Automatic ARIMA

Forecasting

Selected dependent

variable: SPREAD

Date: 10/26/18 Time:

09:28

Sample: 1957M01

2015M03

Included observations: 696

Forecast length: 0

Number of estimated

ARMA models: 2

Number of non-converged

estimations: 0

Selected ARMA model:

(1,0)(0,0)

AIC value: 0.75597960146

Second Model

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 09:29

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 3

Number of non-converged estimations: 0

Selected ARMA model: (2,0)(0,0)

AIC value: 0.683346733664

.|**** | *|. | 10 0.550 -0.133 3935.2 0.000

.|**** | .|. | 11 0.502 0.033 4114.6 0.000

.|*** | .|. | 12 0.458 -0.012 4264.3 0.000

3) Model selection

First Model

Automatic ARIMA

Forecasting

Selected dependent

variable: SPREAD

Date: 10/26/18 Time:

09:28

Sample: 1957M01

2015M03

Included observations: 696

Forecast length: 0

Number of estimated

ARMA models: 2

Number of non-converged

estimations: 0

Selected ARMA model:

(1,0)(0,0)

AIC value: 0.75597960146

Second Model

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 09:29

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 3

Number of non-converged estimations: 0

Selected ARMA model: (2,0)(0,0)

AIC value: 0.683346733664

Third Model

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 09:30

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 4

Number of non-converged estimations: 0

Selected ARMA model: (3,0)(0,0)

AIC value: 0.660012693068

On the basis of the results from the above table, the AIC is lowest for the third model with three

lags. So the best model is the third model.

Plotting the ACF and PCF for the Preferred Model

Date: 10/26/18 Time: 09:31

Sample: 1957M01 2015M03

Included observations: 696

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|******* .|******* 1 0.957 0.957 640.22 0.000

.|******| **|. | 2 0.894 -0.265 1199.3 0.000

.|******| .|* | 3 0.840 0.155 1694.5 0.000

.|******| *|. | 4 0.788 -0.106 2130.3 0.000

.|***** | .|. | 5 0.739 0.063 2514.1 0.000

.|***** | .|. | 6 0.696 0.005 2855.3 0.000

.|***** | .|* | 7 0.663 0.085 3165.0 0.000

.|***** | .|. | 8 0.633 -0.017 3448.4 0.000

.|**** | *|. | 9 0.597 -0.099 3700.3 0.000

.|**** | *|. | 10 0.549 -0.122 3913.4 0.000

.|**** | .|. | 11 0.501 0.038 4091.7 0.000

.|*** | .|. | 12 0.459 -0.006 4241.5 0.000

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 09:30

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 4

Number of non-converged estimations: 0

Selected ARMA model: (3,0)(0,0)

AIC value: 0.660012693068

On the basis of the results from the above table, the AIC is lowest for the third model with three

lags. So the best model is the third model.

Plotting the ACF and PCF for the Preferred Model

Date: 10/26/18 Time: 09:31

Sample: 1957M01 2015M03

Included observations: 696

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|******* .|******* 1 0.957 0.957 640.22 0.000

.|******| **|. | 2 0.894 -0.265 1199.3 0.000

.|******| .|* | 3 0.840 0.155 1694.5 0.000

.|******| *|. | 4 0.788 -0.106 2130.3 0.000

.|***** | .|. | 5 0.739 0.063 2514.1 0.000

.|***** | .|. | 6 0.696 0.005 2855.3 0.000

.|***** | .|* | 7 0.663 0.085 3165.0 0.000

.|***** | .|. | 8 0.633 -0.017 3448.4 0.000

.|**** | *|. | 9 0.597 -0.099 3700.3 0.000

.|**** | *|. | 10 0.549 -0.122 3913.4 0.000

.|**** | .|. | 11 0.501 0.038 4091.7 0.000

.|*** | .|. | 12 0.459 -0.006 4241.5 0.000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

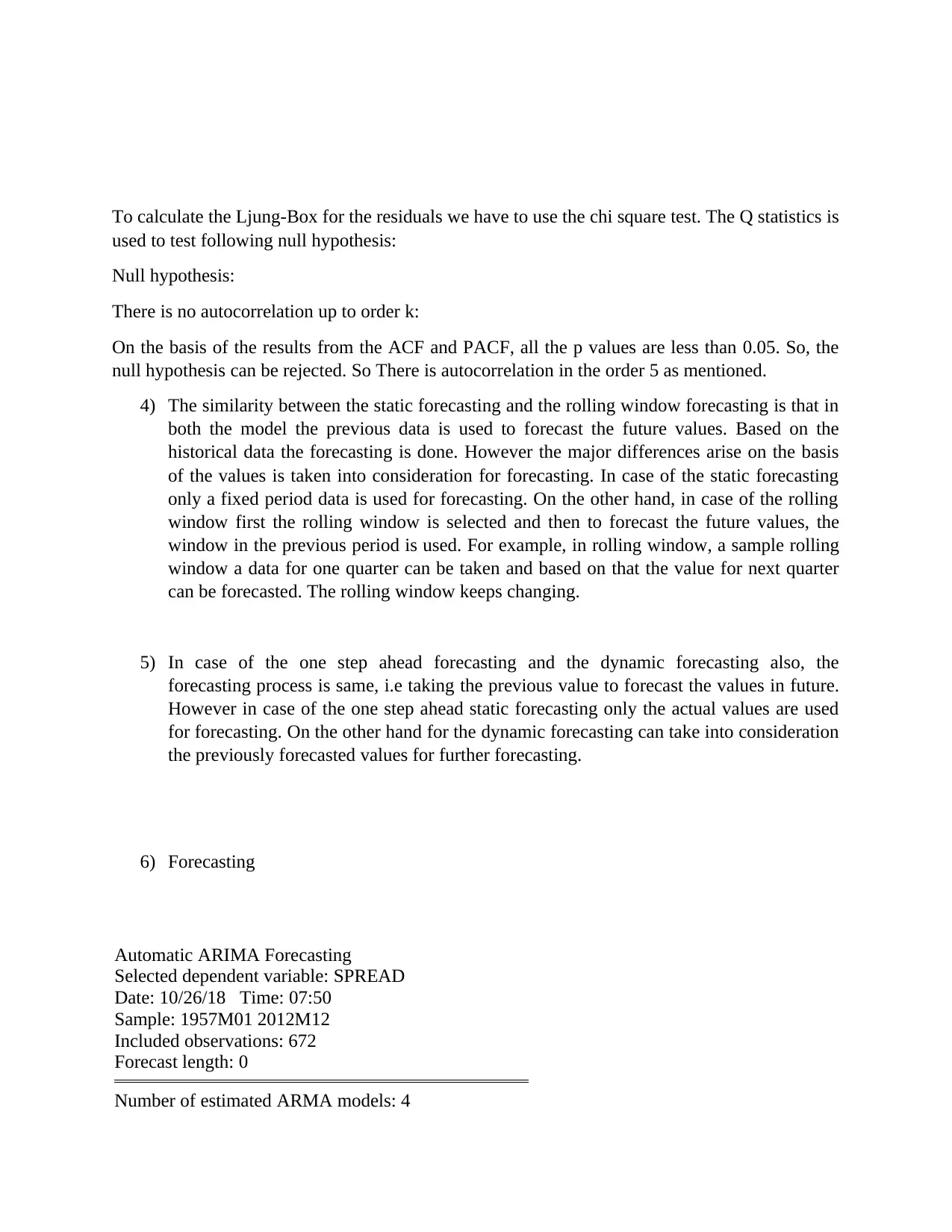

To calculate the Ljung-Box for the residuals we have to use the chi square test. The Q statistics is

used to test following null hypothesis:

Null hypothesis:

There is no autocorrelation up to order k:

On the basis of the results from the ACF and PACF, all the p values are less than 0.05. So, the

null hypothesis can be rejected. So There is autocorrelation in the order 5 as mentioned.

4) The similarity between the static forecasting and the rolling window forecasting is that in

both the model the previous data is used to forecast the future values. Based on the

historical data the forecasting is done. However the major differences arise on the basis

of the values is taken into consideration for forecasting. In case of the static forecasting

only a fixed period data is used for forecasting. On the other hand, in case of the rolling

window first the rolling window is selected and then to forecast the future values, the

window in the previous period is used. For example, in rolling window, a sample rolling

window a data for one quarter can be taken and based on that the value for next quarter

can be forecasted. The rolling window keeps changing.

5) In case of the one step ahead forecasting and the dynamic forecasting also, the

forecasting process is same, i.e taking the previous value to forecast the values in future.

However in case of the one step ahead static forecasting only the actual values are used

for forecasting. On the other hand for the dynamic forecasting can take into consideration

the previously forecasted values for further forecasting.

6) Forecasting

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 07:50

Sample: 1957M01 2012M12

Included observations: 672

Forecast length: 0

Number of estimated ARMA models: 4

used to test following null hypothesis:

Null hypothesis:

There is no autocorrelation up to order k:

On the basis of the results from the ACF and PACF, all the p values are less than 0.05. So, the

null hypothesis can be rejected. So There is autocorrelation in the order 5 as mentioned.

4) The similarity between the static forecasting and the rolling window forecasting is that in

both the model the previous data is used to forecast the future values. Based on the

historical data the forecasting is done. However the major differences arise on the basis

of the values is taken into consideration for forecasting. In case of the static forecasting

only a fixed period data is used for forecasting. On the other hand, in case of the rolling

window first the rolling window is selected and then to forecast the future values, the

window in the previous period is used. For example, in rolling window, a sample rolling

window a data for one quarter can be taken and based on that the value for next quarter

can be forecasted. The rolling window keeps changing.

5) In case of the one step ahead forecasting and the dynamic forecasting also, the

forecasting process is same, i.e taking the previous value to forecast the values in future.

However in case of the one step ahead static forecasting only the actual values are used

for forecasting. On the other hand for the dynamic forecasting can take into consideration

the previously forecasted values for further forecasting.

6) Forecasting

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 07:50

Sample: 1957M01 2012M12

Included observations: 672

Forecast length: 0

Number of estimated ARMA models: 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Number of non-converged estimations: 0

Selected ARMA model: (1,1)(0,0)

AIC value: 0.677963363957

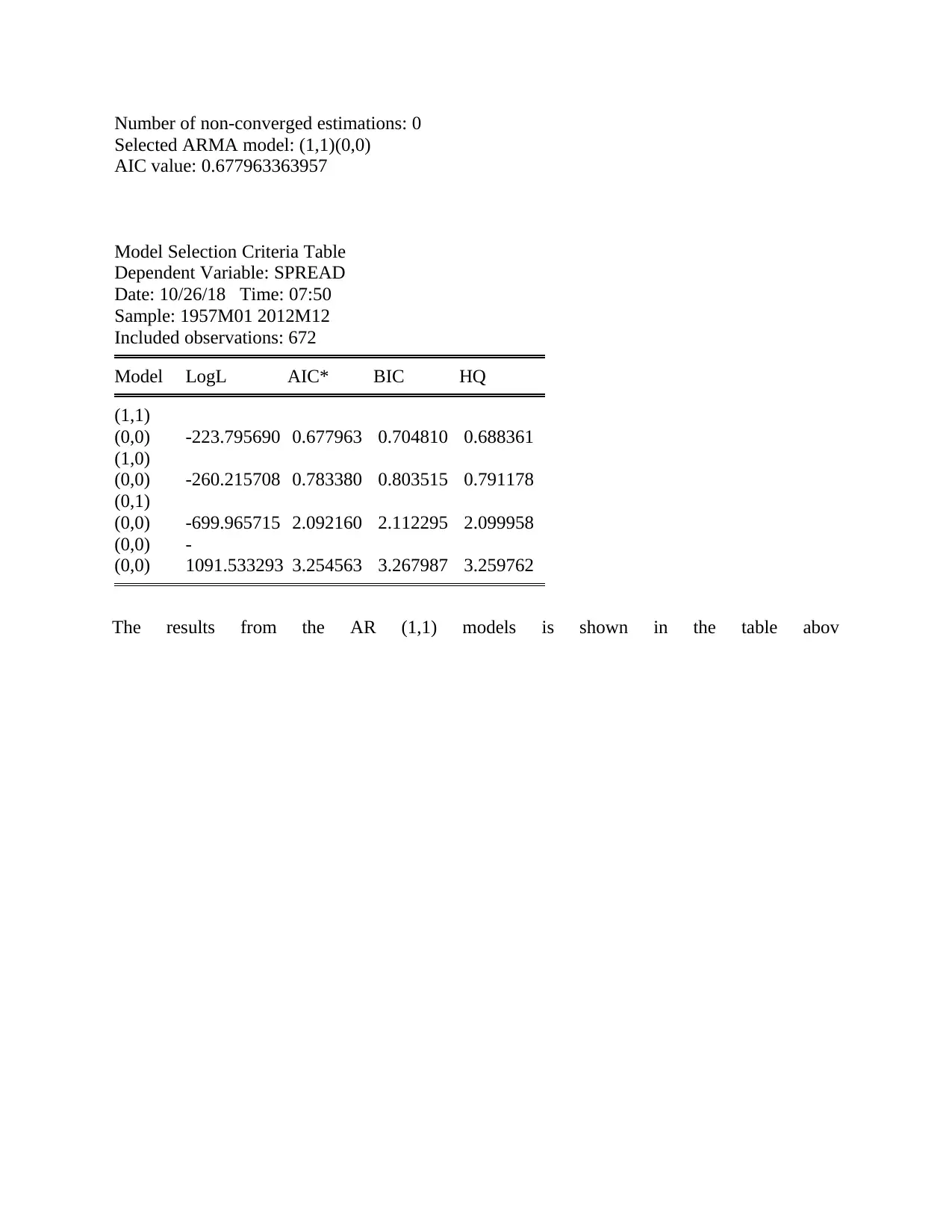

Model Selection Criteria Table

Dependent Variable: SPREAD

Date: 10/26/18 Time: 07:50

Sample: 1957M01 2012M12

Included observations: 672

Model LogL AIC* BIC HQ

(1,1)

(0,0) -223.795690 0.677963 0.704810 0.688361

(1,0)

(0,0) -260.215708 0.783380 0.803515 0.791178

(0,1)

(0,0) -699.965715 2.092160 2.112295 2.099958

(0,0)

(0,0)

-

1091.533293 3.254563 3.267987 3.259762

The results from the AR (1,1) models is shown in the table abov

Selected ARMA model: (1,1)(0,0)

AIC value: 0.677963363957

Model Selection Criteria Table

Dependent Variable: SPREAD

Date: 10/26/18 Time: 07:50

Sample: 1957M01 2012M12

Included observations: 672

Model LogL AIC* BIC HQ

(1,1)

(0,0) -223.795690 0.677963 0.704810 0.688361

(1,0)

(0,0) -260.215708 0.783380 0.803515 0.791178

(0,1)

(0,0) -699.965715 2.092160 2.112295 2.099958

(0,0)

(0,0)

-

1091.533293 3.254563 3.267987 3.259762

The results from the AR (1,1) models is shown in the table abov

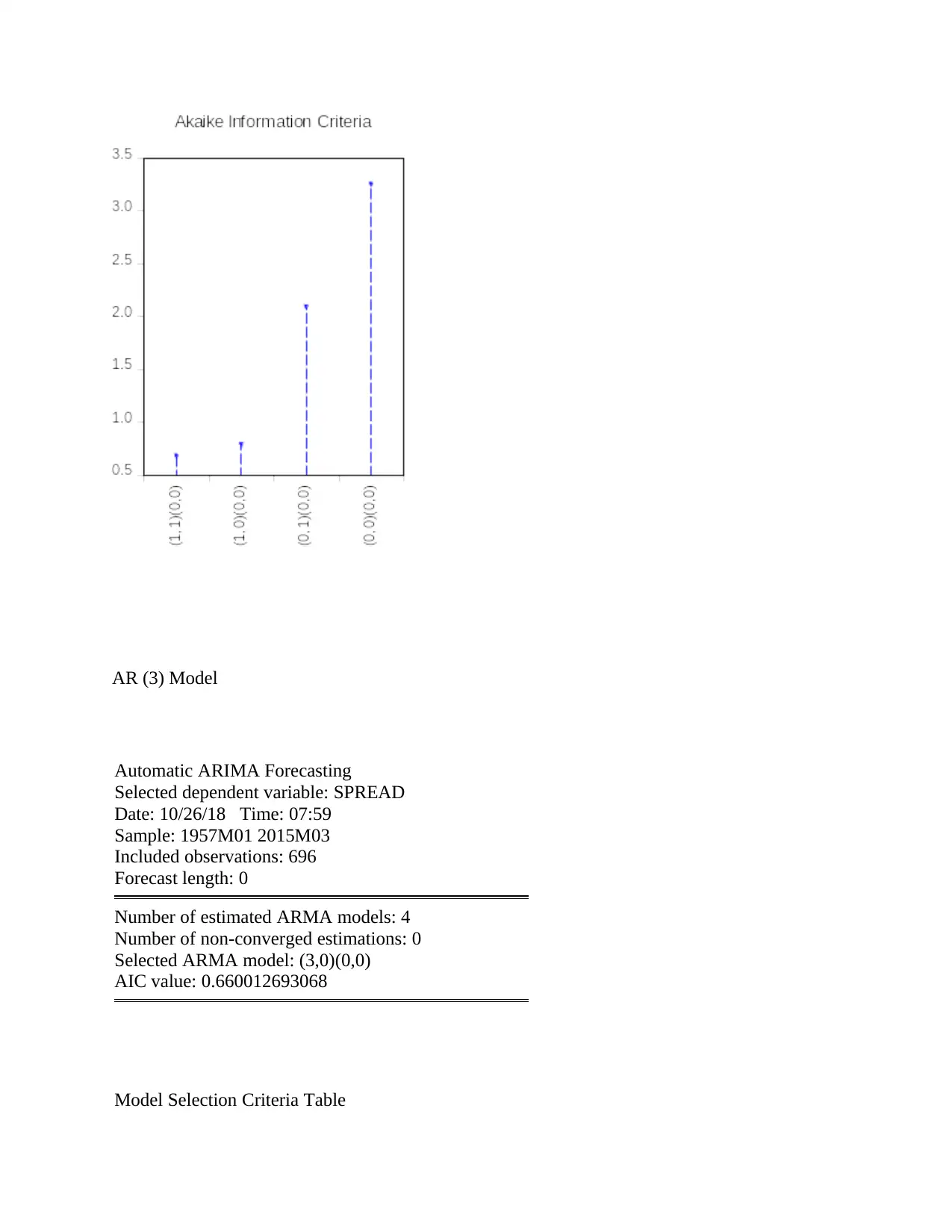

AR (3) Model

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 07:59

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 4

Number of non-converged estimations: 0

Selected ARMA model: (3,0)(0,0)

AIC value: 0.660012693068

Model Selection Criteria Table

Automatic ARIMA Forecasting

Selected dependent variable: SPREAD

Date: 10/26/18 Time: 07:59

Sample: 1957M01 2015M03

Included observations: 696

Forecast length: 0

Number of estimated ARMA models: 4

Number of non-converged estimations: 0

Selected ARMA model: (3,0)(0,0)

AIC value: 0.660012693068

Model Selection Criteria Table

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

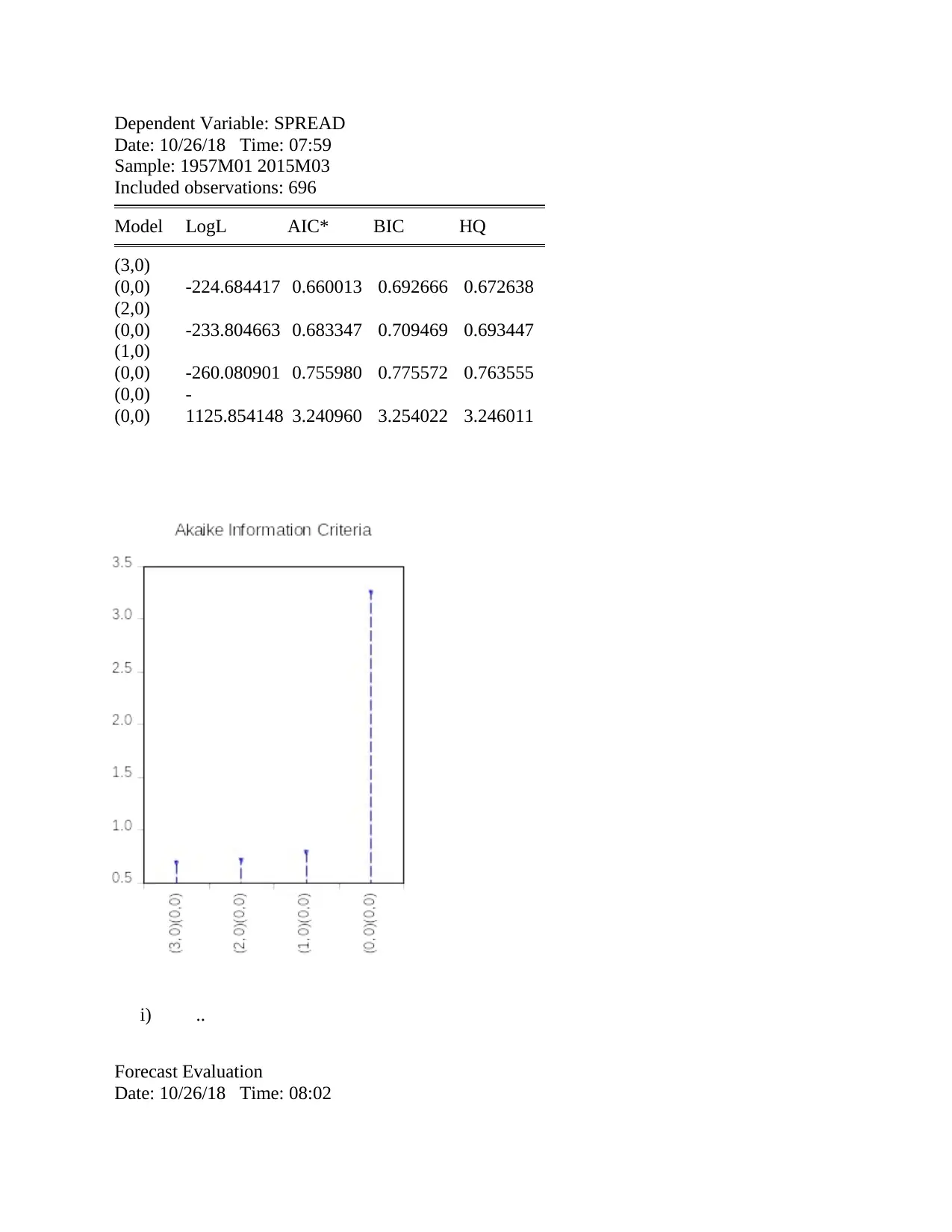

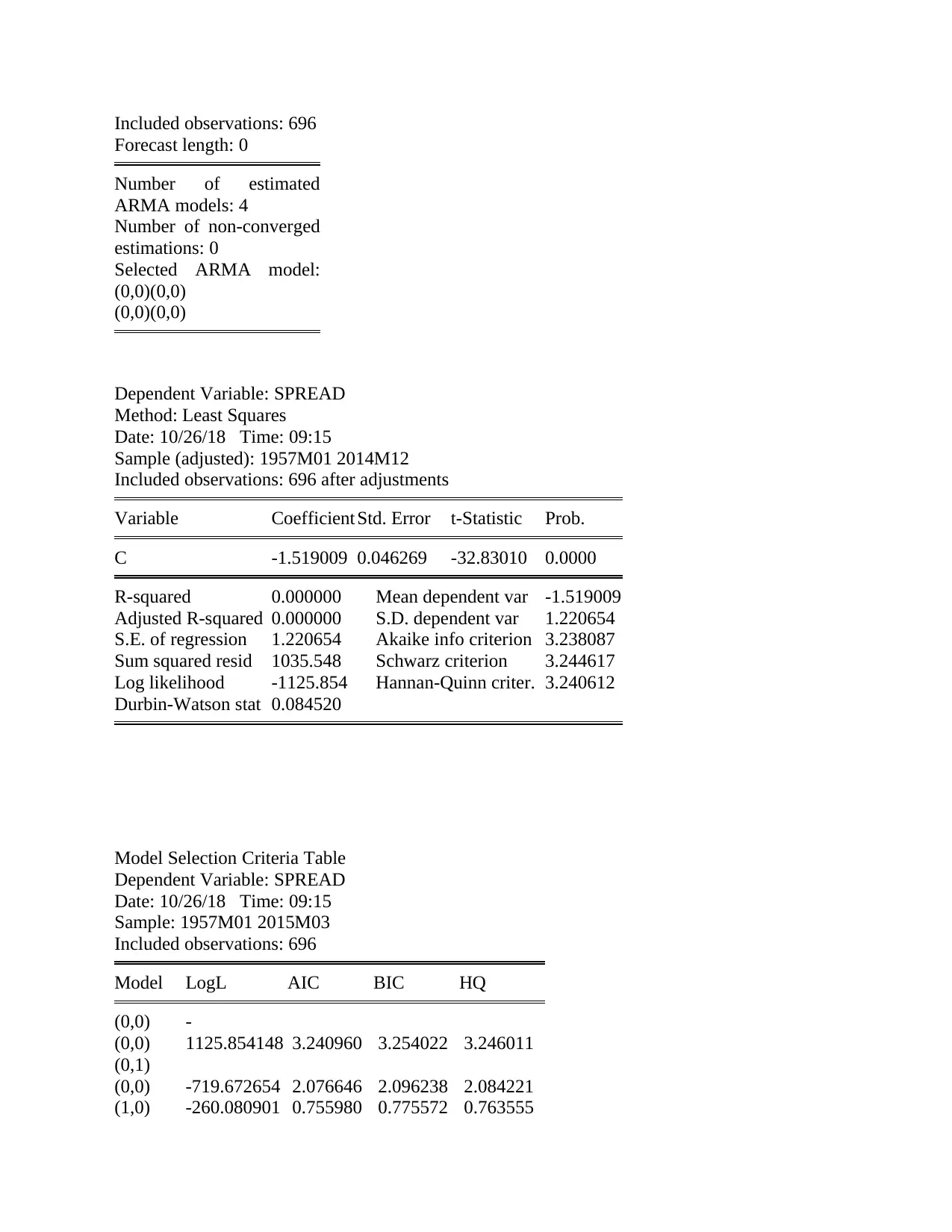

Dependent Variable: SPREAD

Date: 10/26/18 Time: 07:59

Sample: 1957M01 2015M03

Included observations: 696

Model LogL AIC* BIC HQ

(3,0)

(0,0) -224.684417 0.660013 0.692666 0.672638

(2,0)

(0,0) -233.804663 0.683347 0.709469 0.693447

(1,0)

(0,0) -260.080901 0.755980 0.775572 0.763555

(0,0)

(0,0)

-

1125.854148 3.240960 3.254022 3.246011

i) ..

Forecast Evaluation

Date: 10/26/18 Time: 08:02

Date: 10/26/18 Time: 07:59

Sample: 1957M01 2015M03

Included observations: 696

Model LogL AIC* BIC HQ

(3,0)

(0,0) -224.684417 0.660013 0.692666 0.672638

(2,0)

(0,0) -233.804663 0.683347 0.709469 0.693447

(1,0)

(0,0) -260.080901 0.755980 0.775572 0.763555

(0,0)

(0,0)

-

1125.854148 3.240960 3.254022 3.246011

i) ..

Forecast Evaluation

Date: 10/26/18 Time: 08:02

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

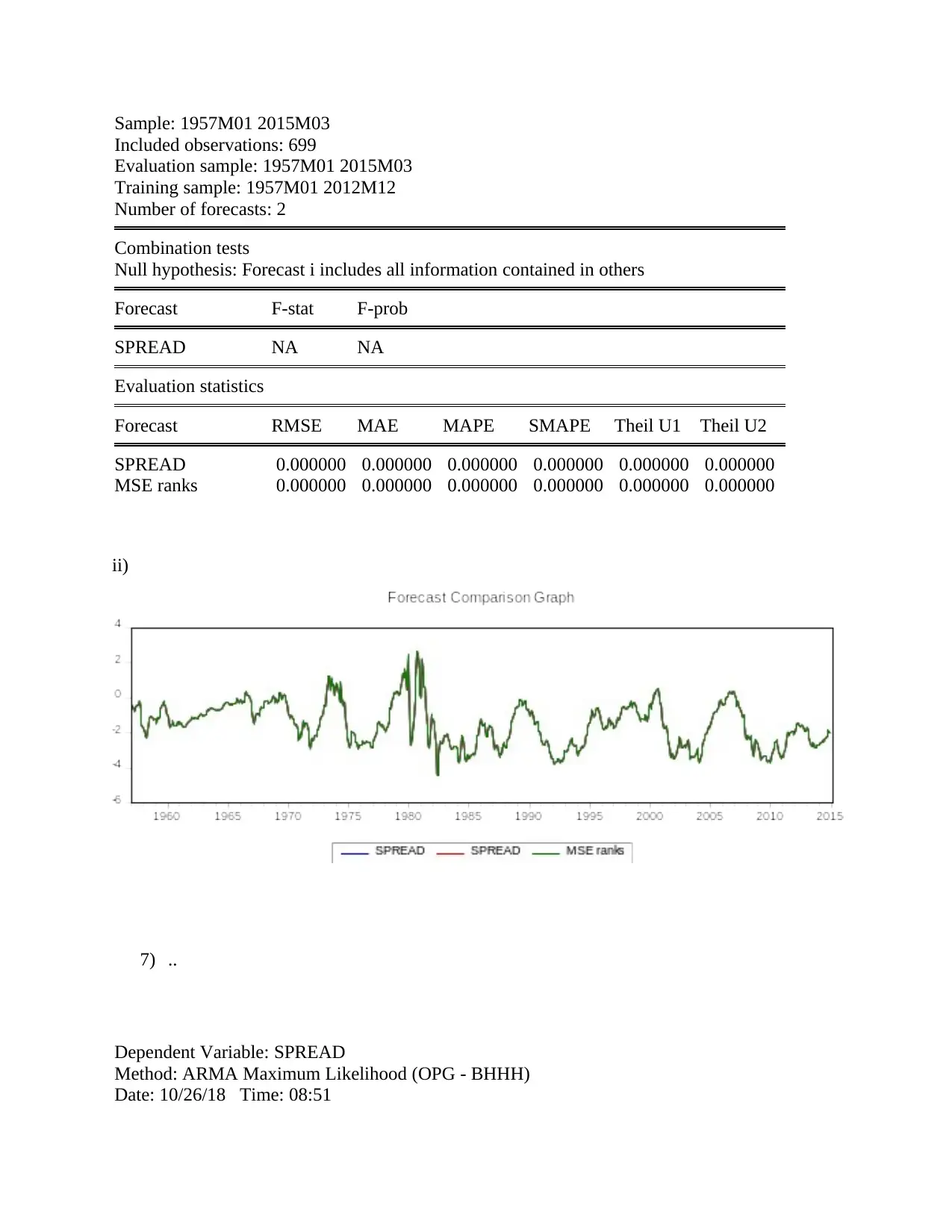

Sample: 1957M01 2015M03

Included observations: 699

Evaluation sample: 1957M01 2015M03

Training sample: 1957M01 2012M12

Number of forecasts: 2

Combination tests

Null hypothesis: Forecast i includes all information contained in others

Forecast F-stat F-prob

SPREAD NA NA

Evaluation statistics

Forecast RMSE MAE MAPE SMAPE Theil U1 Theil U2

SPREAD 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

MSE ranks 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

ii)

7) ..

Dependent Variable: SPREAD

Method: ARMA Maximum Likelihood (OPG - BHHH)

Date: 10/26/18 Time: 08:51

Included observations: 699

Evaluation sample: 1957M01 2015M03

Training sample: 1957M01 2012M12

Number of forecasts: 2

Combination tests

Null hypothesis: Forecast i includes all information contained in others

Forecast F-stat F-prob

SPREAD NA NA

Evaluation statistics

Forecast RMSE MAE MAPE SMAPE Theil U1 Theil U2

SPREAD 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

MSE ranks 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

ii)

7) ..

Dependent Variable: SPREAD

Method: ARMA Maximum Likelihood (OPG - BHHH)

Date: 10/26/18 Time: 08:51

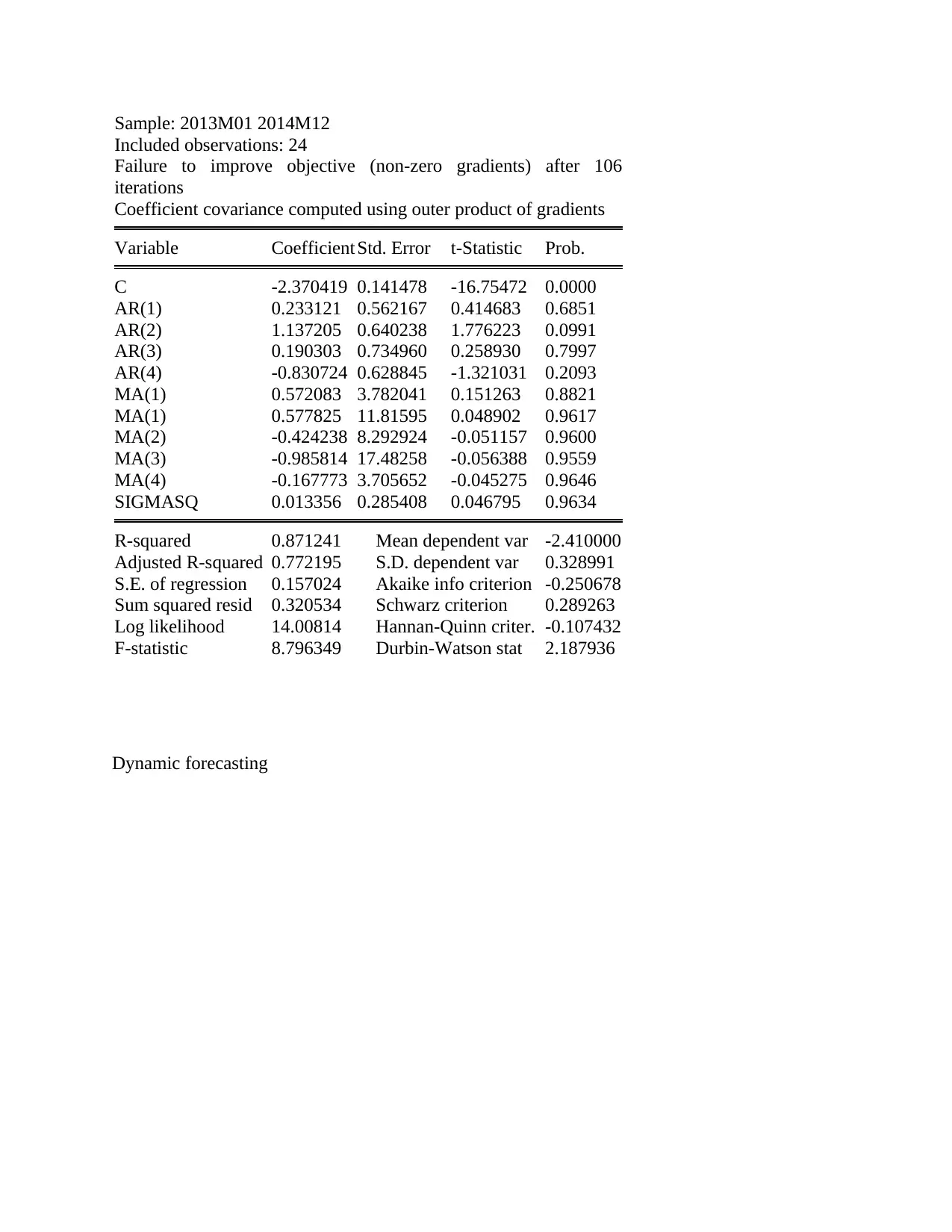

Sample: 2013M01 2014M12

Included observations: 24

Failure to improve objective (non-zero gradients) after 106

iterations

Coefficient covariance computed using outer product of gradients

Variable Coefficient Std. Error t-Statistic Prob.

C -2.370419 0.141478 -16.75472 0.0000

AR(1) 0.233121 0.562167 0.414683 0.6851

AR(2) 1.137205 0.640238 1.776223 0.0991

AR(3) 0.190303 0.734960 0.258930 0.7997

AR(4) -0.830724 0.628845 -1.321031 0.2093

MA(1) 0.572083 3.782041 0.151263 0.8821

MA(1) 0.577825 11.81595 0.048902 0.9617

MA(2) -0.424238 8.292924 -0.051157 0.9600

MA(3) -0.985814 17.48258 -0.056388 0.9559

MA(4) -0.167773 3.705652 -0.045275 0.9646

SIGMASQ 0.013356 0.285408 0.046795 0.9634

R-squared 0.871241 Mean dependent var -2.410000

Adjusted R-squared 0.772195 S.D. dependent var 0.328991

S.E. of regression 0.157024 Akaike info criterion -0.250678

Sum squared resid 0.320534 Schwarz criterion 0.289263

Log likelihood 14.00814 Hannan-Quinn criter. -0.107432

F-statistic 8.796349 Durbin-Watson stat 2.187936

Dynamic forecasting

Included observations: 24

Failure to improve objective (non-zero gradients) after 106

iterations

Coefficient covariance computed using outer product of gradients

Variable Coefficient Std. Error t-Statistic Prob.

C -2.370419 0.141478 -16.75472 0.0000

AR(1) 0.233121 0.562167 0.414683 0.6851

AR(2) 1.137205 0.640238 1.776223 0.0991

AR(3) 0.190303 0.734960 0.258930 0.7997

AR(4) -0.830724 0.628845 -1.321031 0.2093

MA(1) 0.572083 3.782041 0.151263 0.8821

MA(1) 0.577825 11.81595 0.048902 0.9617

MA(2) -0.424238 8.292924 -0.051157 0.9600

MA(3) -0.985814 17.48258 -0.056388 0.9559

MA(4) -0.167773 3.705652 -0.045275 0.9646

SIGMASQ 0.013356 0.285408 0.046795 0.9634

R-squared 0.871241 Mean dependent var -2.410000

Adjusted R-squared 0.772195 S.D. dependent var 0.328991

S.E. of regression 0.157024 Akaike info criterion -0.250678

Sum squared resid 0.320534 Schwarz criterion 0.289263

Log likelihood 14.00814 Hannan-Quinn criter. -0.107432

F-statistic 8.796349 Durbin-Watson stat 2.187936

Dynamic forecasting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8) ..

Automatic ARIMA

Forecasting

Selected dependent

variable: SPREAD

Date: 10/26/18 Time:

09:15

Sample: 1957M01

2015M03

Automatic ARIMA

Forecasting

Selected dependent

variable: SPREAD

Date: 10/26/18 Time:

09:15

Sample: 1957M01

2015M03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Included observations: 696

Forecast length: 0

Number of estimated

ARMA models: 4

Number of non-converged

estimations: 0

Selected ARMA model:

(0,0)(0,0)

(0,0)(0,0)

Dependent Variable: SPREAD

Method: Least Squares

Date: 10/26/18 Time: 09:15

Sample (adjusted): 1957M01 2014M12

Included observations: 696 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C -1.519009 0.046269 -32.83010 0.0000

R-squared 0.000000 Mean dependent var -1.519009

Adjusted R-squared 0.000000 S.D. dependent var 1.220654

S.E. of regression 1.220654 Akaike info criterion 3.238087

Sum squared resid 1035.548 Schwarz criterion 3.244617

Log likelihood -1125.854 Hannan-Quinn criter. 3.240612

Durbin-Watson stat 0.084520

Model Selection Criteria Table

Dependent Variable: SPREAD

Date: 10/26/18 Time: 09:15

Sample: 1957M01 2015M03

Included observations: 696

Model LogL AIC BIC HQ

(0,0)

(0,0)

-

1125.854148 3.240960 3.254022 3.246011

(0,1)

(0,0) -719.672654 2.076646 2.096238 2.084221

(1,0) -260.080901 0.755980 0.775572 0.763555

Forecast length: 0

Number of estimated

ARMA models: 4

Number of non-converged

estimations: 0

Selected ARMA model:

(0,0)(0,0)

(0,0)(0,0)

Dependent Variable: SPREAD

Method: Least Squares

Date: 10/26/18 Time: 09:15

Sample (adjusted): 1957M01 2014M12

Included observations: 696 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C -1.519009 0.046269 -32.83010 0.0000

R-squared 0.000000 Mean dependent var -1.519009

Adjusted R-squared 0.000000 S.D. dependent var 1.220654

S.E. of regression 1.220654 Akaike info criterion 3.238087

Sum squared resid 1035.548 Schwarz criterion 3.244617

Log likelihood -1125.854 Hannan-Quinn criter. 3.240612

Durbin-Watson stat 0.084520

Model Selection Criteria Table

Dependent Variable: SPREAD

Date: 10/26/18 Time: 09:15

Sample: 1957M01 2015M03

Included observations: 696

Model LogL AIC BIC HQ

(0,0)

(0,0)

-

1125.854148 3.240960 3.254022 3.246011

(0,1)

(0,0) -719.672654 2.076646 2.096238 2.084221

(1,0) -260.080901 0.755980 0.775572 0.763555

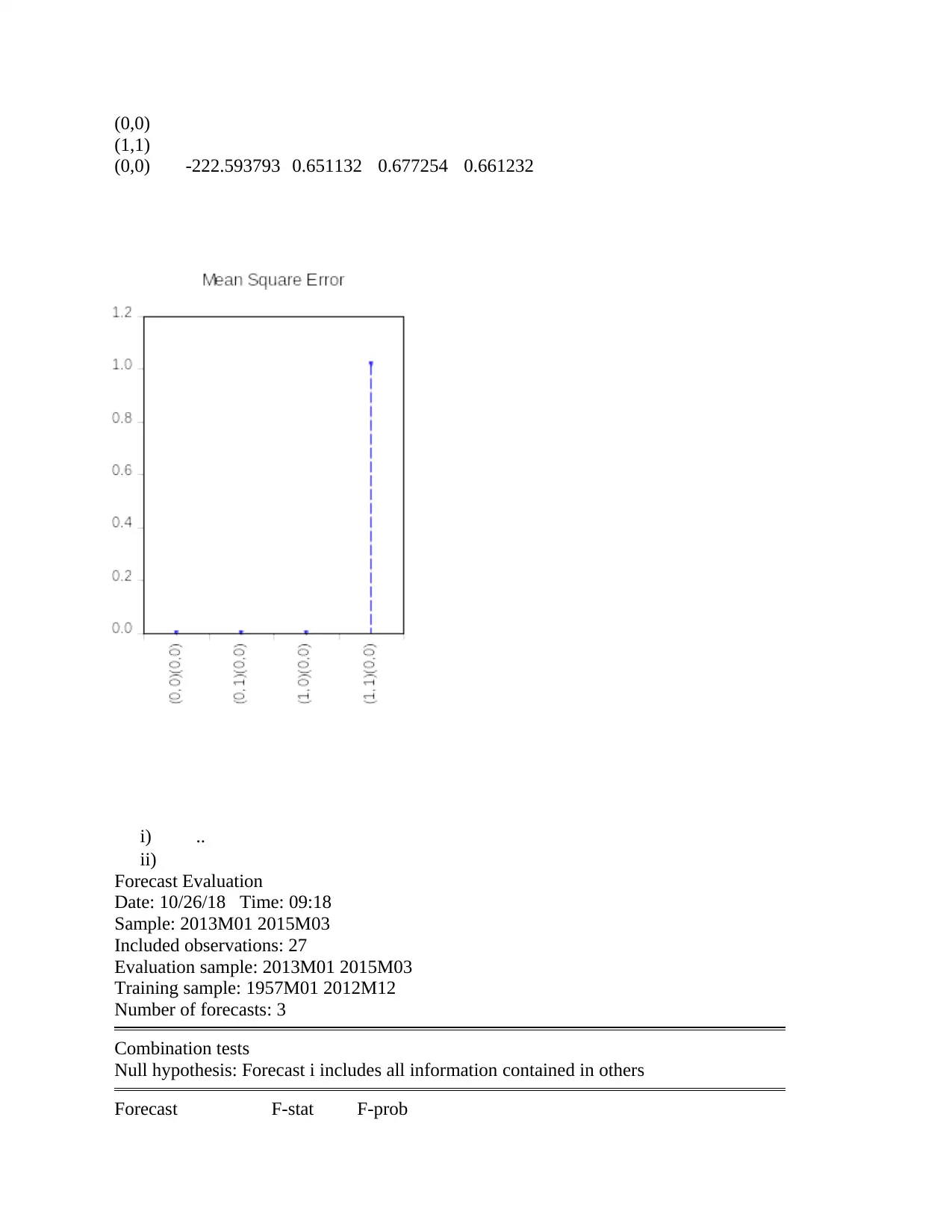

(0,0)

(1,1)

(0,0) -222.593793 0.651132 0.677254 0.661232

i) ..

ii)

Forecast Evaluation

Date: 10/26/18 Time: 09:18

Sample: 2013M01 2015M03

Included observations: 27

Evaluation sample: 2013M01 2015M03

Training sample: 1957M01 2012M12

Number of forecasts: 3

Combination tests

Null hypothesis: Forecast i includes all information contained in others

Forecast F-stat F-prob

(1,1)

(0,0) -222.593793 0.651132 0.677254 0.661232

i) ..

ii)

Forecast Evaluation

Date: 10/26/18 Time: 09:18

Sample: 2013M01 2015M03

Included observations: 27

Evaluation sample: 2013M01 2015M03

Training sample: 1957M01 2012M12

Number of forecasts: 3

Combination tests

Null hypothesis: Forecast i includes all information contained in others

Forecast F-stat F-prob

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.