Macroeconomics Assignment: Inflation and Interest Rates

VerifiedAdded on 2022/07/28

|14

|1789

|28

Homework Assignment

AI Summary

This macroeconomics assignment delves into the relationship between inflation and interest rates, exploring how unexpected inflation affects borrowers and lenders. It examines the impact of inflation on fixed-rate mortgages and bank investments, as well as how inflation expectations influence mortgage decisions. The assignment further analyzes the velocity of money, the effects of new financial products on money demand, and the quantity theory of money. It includes a market analysis of loanable funds, illustrating the impact of increased demand on interest rates and savings. The assignment also covers aggregate demand and supply, evaluating the effects of consumer and investor pessimism and suggesting fiscal and monetary policy responses. Finally, it explores international trade, purchasing power parity, and the effects of transaction costs on exchange rates.

Running head: MACROECONOMICS

Macroeconomics

Name of the Student

Name of the University

Course ID

Macroeconomics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MACROECONOMICS

Table of Contents

Question 1........................................................................................................................................2

Question a....................................................................................................................................2

Question b....................................................................................................................................2

Question c....................................................................................................................................3

Question d....................................................................................................................................3

Question e....................................................................................................................................3

Question 2........................................................................................................................................4

Question a....................................................................................................................................4

Question b....................................................................................................................................4

Question c....................................................................................................................................4

Question d....................................................................................................................................5

Question e....................................................................................................................................5

Question 3........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................6

Question c....................................................................................................................................7

Question 4........................................................................................................................................7

Question a....................................................................................................................................7

Question b....................................................................................................................................8

Question c....................................................................................................................................8

Question 5........................................................................................................................................9

Question a....................................................................................................................................9

Question b....................................................................................................................................9

Question c....................................................................................................................................9

Question d....................................................................................................................................9

Question e..................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Question 1........................................................................................................................................2

Question a....................................................................................................................................2

Question b....................................................................................................................................2

Question c....................................................................................................................................3

Question d....................................................................................................................................3

Question e....................................................................................................................................3

Question 2........................................................................................................................................4

Question a....................................................................................................................................4

Question b....................................................................................................................................4

Question c....................................................................................................................................4

Question d....................................................................................................................................5

Question e....................................................................................................................................5

Question 3........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................6

Question c....................................................................................................................................7

Question 4........................................................................................................................................7

Question a....................................................................................................................................7

Question b....................................................................................................................................8

Question c....................................................................................................................................8

Question 5........................................................................................................................................9

Question a....................................................................................................................................9

Question b....................................................................................................................................9

Question c....................................................................................................................................9

Question d....................................................................................................................................9

Question e..................................................................................................................................10

References......................................................................................................................................11

2MACROECONOMICS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MACROECONOMICS

Question 1

Question a

If inflation rate turns out to be lower than expected, then real interest rate increases

(Heijdra 2017).

Question b

Suppose nominal interest rate on the loan is 10% and the expected inflation rate is 4%.

Therefore, the expected real interest rate is

Real interest rate=Nominal interest rate−Expected inflation rate

¿ 10 %−4 %

¿ 6 %

Now if actual interest rate is 2% which is lower than the expected inflation rate, then real interest

rate will be

Real interest rate=Nominal interest rate−Inflation rate

¿ 10 %−2 %

¿ 8 %

This shows, real interest rate increases if actual inflation rate is less than the expected inflation.

Question 1

Question a

If inflation rate turns out to be lower than expected, then real interest rate increases

(Heijdra 2017).

Question b

Suppose nominal interest rate on the loan is 10% and the expected inflation rate is 4%.

Therefore, the expected real interest rate is

Real interest rate=Nominal interest rate−Expected inflation rate

¿ 10 %−4 %

¿ 6 %

Now if actual interest rate is 2% which is lower than the expected inflation rate, then real interest

rate will be

Real interest rate=Nominal interest rate−Inflation rate

¿ 10 %−2 %

¿ 8 %

This shows, real interest rate increases if actual inflation rate is less than the expected inflation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MACROECONOMICS

Question c

The lender gains from this unexpectedly low inflation. This is because lower inflation

increases real value of money and therefore the lender get back a higher real value of money than

expected.

The borrower in contrast loses since he has to return the money that has a higher real

value now compared to the real value of amount originally borrowed (Uribe and Schmitt-Grohe

2017).

Question d

In the case of fixed rate borrowing investors who have generally financed their mortgage

at a fixed rate, have done the same on the verge of scenario that the future interest rate would be

increasing. Now inflation acts as a key component while determining the interest rate and

changes in the inflation rate affect the interest rate (Agenor and Montiel 2015). In the given case

the inflation rate has remained constantly at a lower rate which has affected all those consumers

who have borrowed at a fixed rate and have ended up paying a higher interest rate

Banks have also invested their assets or investment at a given set of expected rate of

return and the expected rate of return has been higher for determine or evaluating the assets, now

this would have lead the banks to reject assets or investment which are comparatively risky and

could have been accepted if the expected return or inflation would have been low at that point of

time

Question e

Question c

The lender gains from this unexpectedly low inflation. This is because lower inflation

increases real value of money and therefore the lender get back a higher real value of money than

expected.

The borrower in contrast loses since he has to return the money that has a higher real

value now compared to the real value of amount originally borrowed (Uribe and Schmitt-Grohe

2017).

Question d

In the case of fixed rate borrowing investors who have generally financed their mortgage

at a fixed rate, have done the same on the verge of scenario that the future interest rate would be

increasing. Now inflation acts as a key component while determining the interest rate and

changes in the inflation rate affect the interest rate (Agenor and Montiel 2015). In the given case

the inflation rate has remained constantly at a lower rate which has affected all those consumers

who have borrowed at a fixed rate and have ended up paying a higher interest rate

Banks have also invested their assets or investment at a given set of expected rate of

return and the expected rate of return has been higher for determine or evaluating the assets, now

this would have lead the banks to reject assets or investment which are comparatively risky and

could have been accepted if the expected return or inflation would have been low at that point of

time

Question e

5MACROECONOMICS

Inflation is a key factor when we determine the level of interest rate. The two key factors

which are well used for the purpose of determining the interest rate is the real interest rate and

inflation now if the factor of inflation is dominating or is set in accordance with a future prospect

of trend that is higher or lower the consumer would be accordingly going for a fixed or floating

rate (Guilmi, Gallegati and Landini 2017). If the borrower believes that the level of inflation will

increase he will be going for a fixed rate and on the other hand if he thinks that the level of

inflation will be decreased, then he will be going for a floating rate of interest rate.

Question 2

Question a

Aggregate nominal spending=Velocity of money × money supply

¿ 7 ×50 million

¿ 350 million

Question b

Velocity of money is inversely proportional to aggregate nominal spending. If residents

of Angria use less money to conduct transactions, then there will be lower aggregate nominal

spending which reduces velocity of money.

Question c

The introduction of new financial product named “bonds” encourages people to invest in

the financial market. As a result, people will be willing to save and invest more rather than

holding money to in hand (Ehnts 2016). As a result, demand for money falls. Since, people now

Inflation is a key factor when we determine the level of interest rate. The two key factors

which are well used for the purpose of determining the interest rate is the real interest rate and

inflation now if the factor of inflation is dominating or is set in accordance with a future prospect

of trend that is higher or lower the consumer would be accordingly going for a fixed or floating

rate (Guilmi, Gallegati and Landini 2017). If the borrower believes that the level of inflation will

increase he will be going for a fixed rate and on the other hand if he thinks that the level of

inflation will be decreased, then he will be going for a floating rate of interest rate.

Question 2

Question a

Aggregate nominal spending=Velocity of money × money supply

¿ 7 ×50 million

¿ 350 million

Question b

Velocity of money is inversely proportional to aggregate nominal spending. If residents

of Angria use less money to conduct transactions, then there will be lower aggregate nominal

spending which reduces velocity of money.

Question c

The introduction of new financial product named “bonds” encourages people to invest in

the financial market. As a result, people will be willing to save and invest more rather than

holding money to in hand (Ehnts 2016). As a result, demand for money falls. Since, people now

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MACROECONOMICS

have less money to hold they spend less resulting in a decrease in number of transaction. As

transaction decreases, there is a decrease in velocity of money.

have less money to hold they spend less resulting in a decrease in number of transaction. As

transaction decreases, there is a decrease in velocity of money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MACROECONOMICS

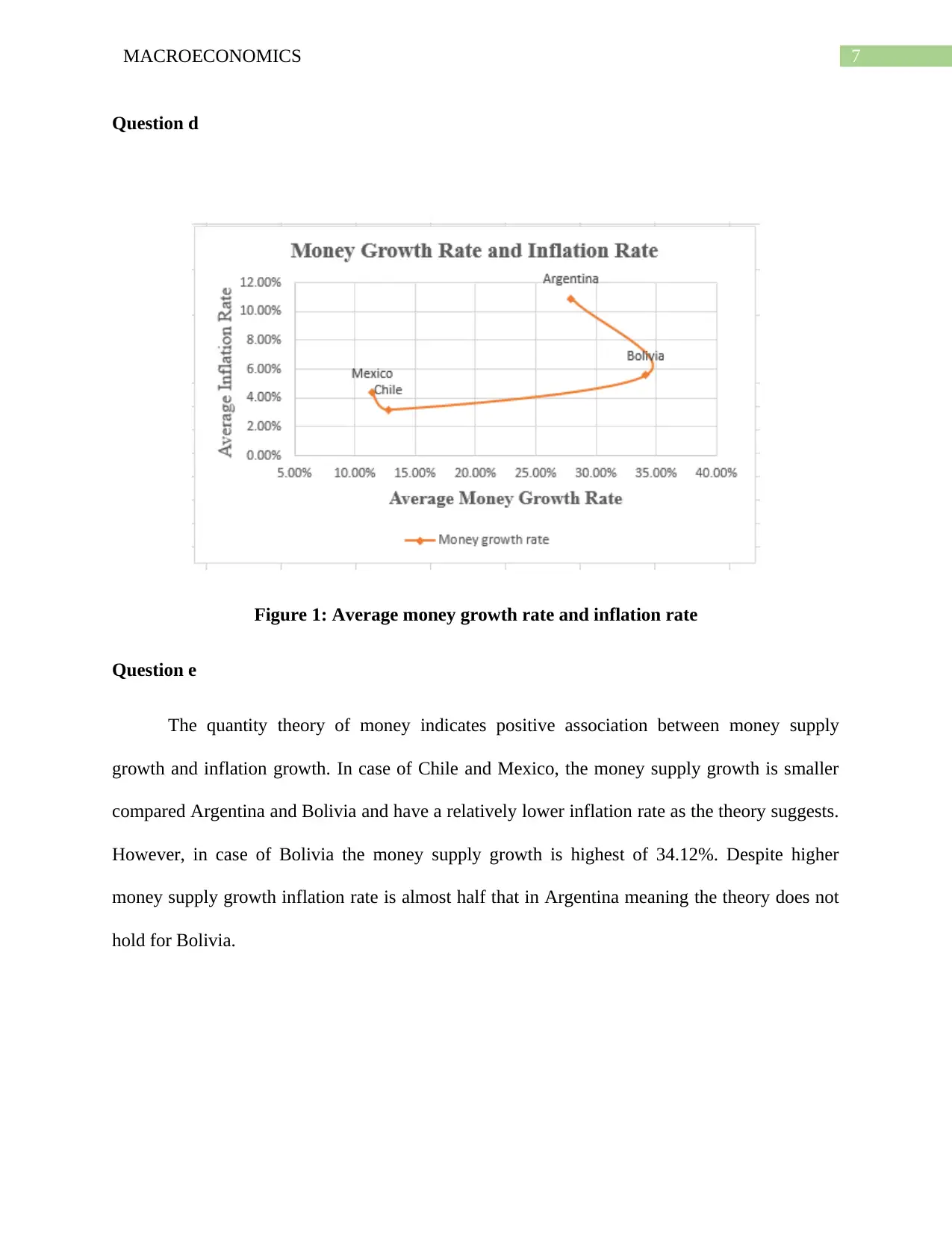

Question d

Figure 1: Average money growth rate and inflation rate

Question e

The quantity theory of money indicates positive association between money supply

growth and inflation growth. In case of Chile and Mexico, the money supply growth is smaller

compared Argentina and Bolivia and have a relatively lower inflation rate as the theory suggests.

However, in case of Bolivia the money supply growth is highest of 34.12%. Despite higher

money supply growth inflation rate is almost half that in Argentina meaning the theory does not

hold for Bolivia.

Question d

Figure 1: Average money growth rate and inflation rate

Question e

The quantity theory of money indicates positive association between money supply

growth and inflation growth. In case of Chile and Mexico, the money supply growth is smaller

compared Argentina and Bolivia and have a relatively lower inflation rate as the theory suggests.

However, in case of Bolivia the money supply growth is highest of 34.12%. Despite higher

money supply growth inflation rate is almost half that in Argentina meaning the theory does not

hold for Bolivia.

8MACROECONOMICS

Question 3

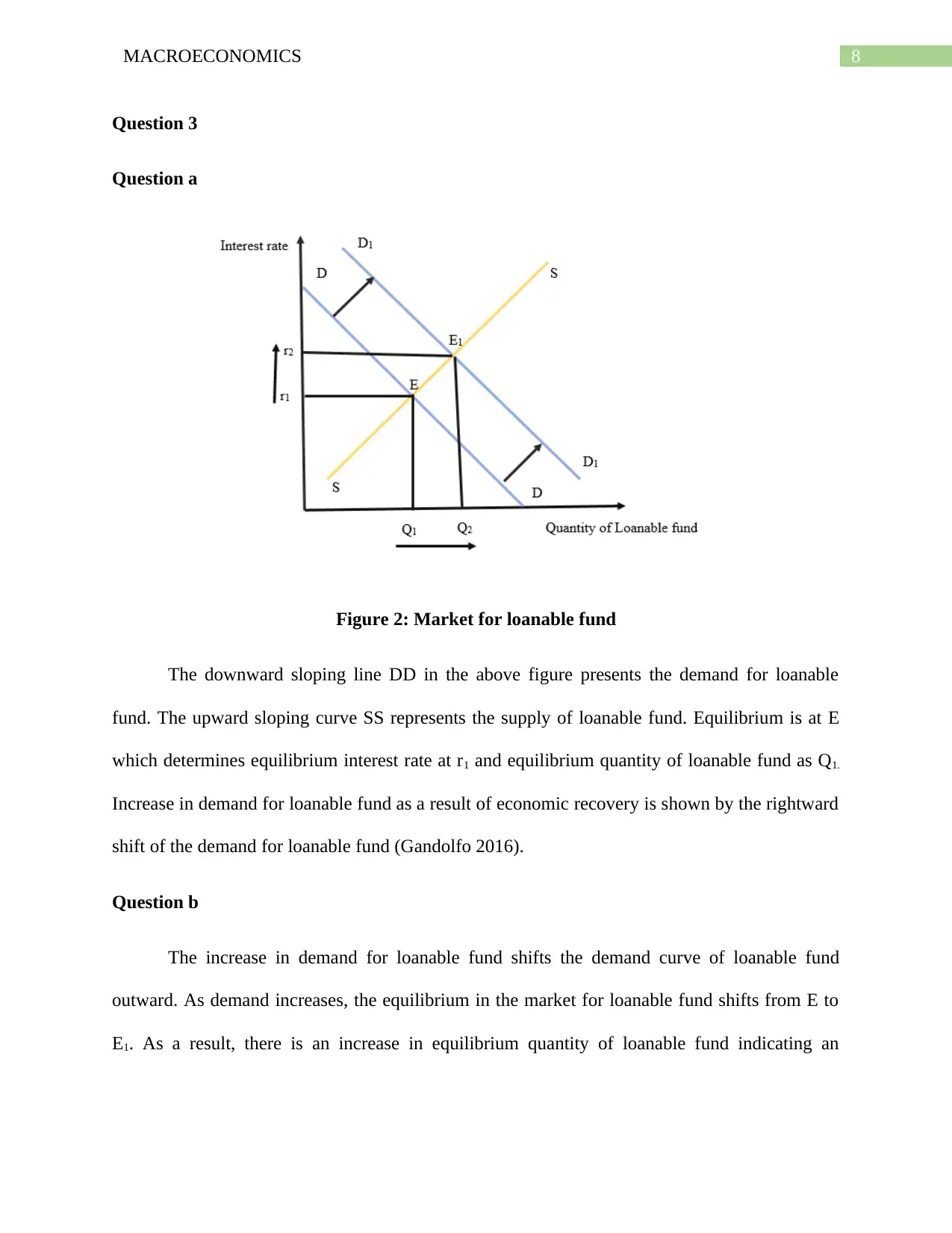

Question a

Figure 2: Market for loanable fund

The downward sloping line DD in the above figure presents the demand for loanable

fund. The upward sloping curve SS represents the supply of loanable fund. Equilibrium is at E

which determines equilibrium interest rate at r1 and equilibrium quantity of loanable fund as Q1.

Increase in demand for loanable fund as a result of economic recovery is shown by the rightward

shift of the demand for loanable fund (Gandolfo 2016).

Question b

The increase in demand for loanable fund shifts the demand curve of loanable fund

outward. As demand increases, the equilibrium in the market for loanable fund shifts from E to

E1. As a result, there is an increase in equilibrium quantity of loanable fund indicating an

Question 3

Question a

Figure 2: Market for loanable fund

The downward sloping line DD in the above figure presents the demand for loanable

fund. The upward sloping curve SS represents the supply of loanable fund. Equilibrium is at E

which determines equilibrium interest rate at r1 and equilibrium quantity of loanable fund as Q1.

Increase in demand for loanable fund as a result of economic recovery is shown by the rightward

shift of the demand for loanable fund (Gandolfo 2016).

Question b

The increase in demand for loanable fund shifts the demand curve of loanable fund

outward. As demand increases, the equilibrium in the market for loanable fund shifts from E to

E1. As a result, there is an increase in equilibrium quantity of loanable fund indicating an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MACROECONOMICS

increase in saving and investment of for the economy of Islandia. As demand for loanable fund

increases, the interest rate increases from r1 to r2.

Question c

The equilibrium quantity of saving and investment will increase less than the amount of

initial change in the demand. The increased demand for loanable firm increases interest rate

which increase borrowing cost of investors discouraging private investment (Dullien et al. 2017).

Since higher interest rate crowds out private investment causing saving and investment to

increase at a lower proportion than increase in demand for loanable demand.

Question 4

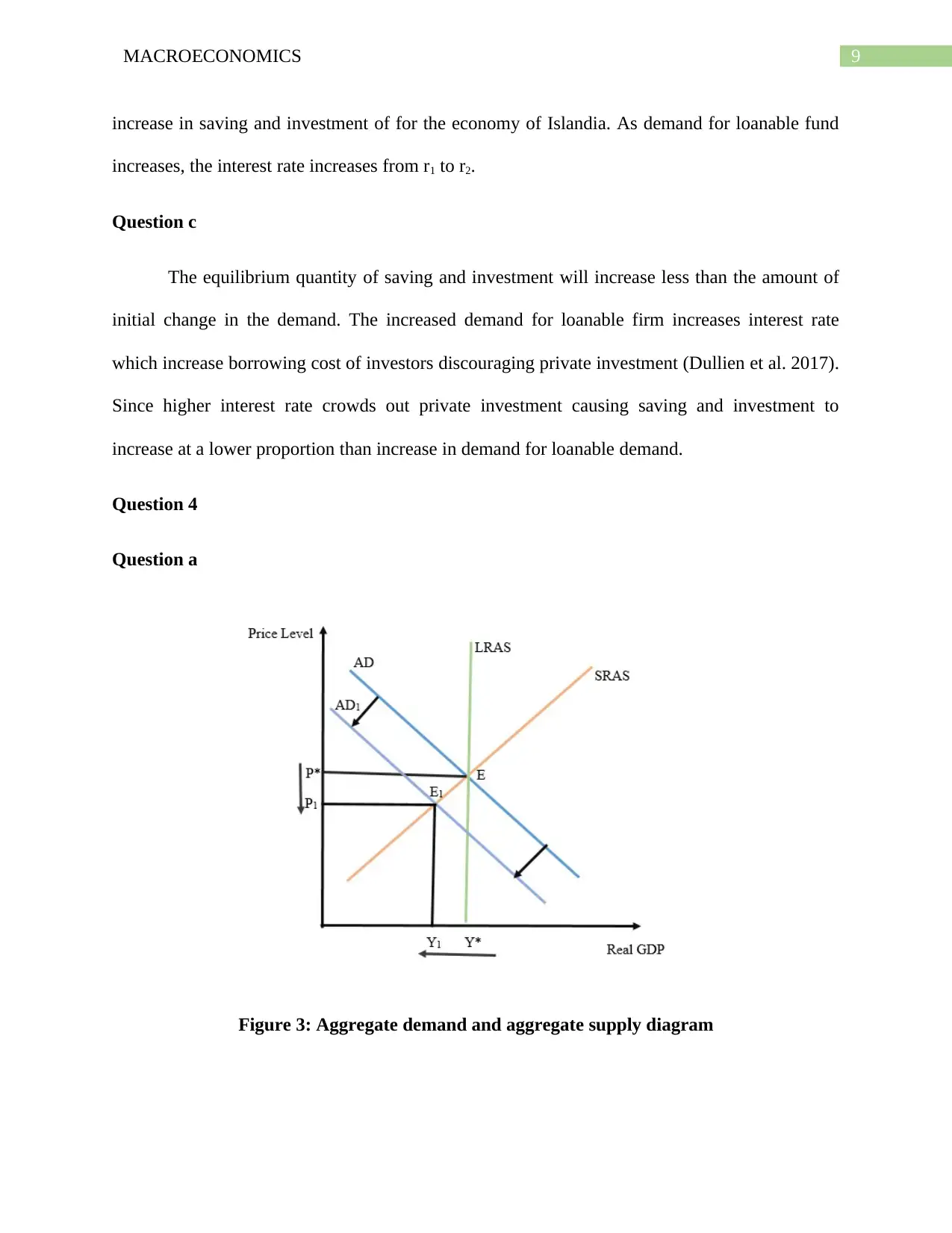

Question a

Figure 3: Aggregate demand and aggregate supply diagram

increase in saving and investment of for the economy of Islandia. As demand for loanable fund

increases, the interest rate increases from r1 to r2.

Question c

The equilibrium quantity of saving and investment will increase less than the amount of

initial change in the demand. The increased demand for loanable firm increases interest rate

which increase borrowing cost of investors discouraging private investment (Dullien et al. 2017).

Since higher interest rate crowds out private investment causing saving and investment to

increase at a lower proportion than increase in demand for loanable demand.

Question 4

Question a

Figure 3: Aggregate demand and aggregate supply diagram

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MACROECONOMICS

The long run equilibrium of the economy corresponds to point E where aggregate

demand (AD), short run aggregate supply (SRAS) and long run aggregate supply (LRAS)

intersect. Long run output is at Y* and that of long run price level is at P*. Now because of the

pessimism among consumers and investors because on expected recession consumption and

investment spending will fall which will shift the aggregate demand curve to the left to AD1. The

new equilibrium is at E1 where real GDP falls to Y1 and price level falls to P1.

Question b

In order to correct the impact of the fall in spending government should take

expansionary policy measures that is expansionary fiscal policy or expansionary monetary

policy. In order to take expansionary fiscal policy government should increase government

spending or lower the tax rate which contributes to a higher aggregate spending (Minford and

Peel 2019). For expansionary monetary policy government should lower the interest rate which

by increasing investing spending increases aggregate spending.

Question c

As a result of these policies there will be an increase in aggregate demand in the long. As

aggregate demand increases, the aggregate demand curve shifts right to move back to its original

position. Macroeconomic equilibrium shifts toward attaining the long run equilibrium with GDP

moves towards potential GDP and price level backs to the long run level.

The long run equilibrium of the economy corresponds to point E where aggregate

demand (AD), short run aggregate supply (SRAS) and long run aggregate supply (LRAS)

intersect. Long run output is at Y* and that of long run price level is at P*. Now because of the

pessimism among consumers and investors because on expected recession consumption and

investment spending will fall which will shift the aggregate demand curve to the left to AD1. The

new equilibrium is at E1 where real GDP falls to Y1 and price level falls to P1.

Question b

In order to correct the impact of the fall in spending government should take

expansionary policy measures that is expansionary fiscal policy or expansionary monetary

policy. In order to take expansionary fiscal policy government should increase government

spending or lower the tax rate which contributes to a higher aggregate spending (Minford and

Peel 2019). For expansionary monetary policy government should lower the interest rate which

by increasing investing spending increases aggregate spending.

Question c

As a result of these policies there will be an increase in aggregate demand in the long. As

aggregate demand increases, the aggregate demand curve shifts right to move back to its original

position. Macroeconomic equilibrium shifts toward attaining the long run equilibrium with GDP

moves towards potential GDP and price level backs to the long run level.

11MACROECONOMICS

Question 5

Question a

Given the price of wheat per tonne in Ambrosian and Bolumbian wheat and the nominal

exchange rate between BMD and AMD, it is profitable to buy wheat from Ambrosia and sells

wheat to Bolumbia (Audretsch and Lehmann 2016).

Question b

Exchange rate between BMD and AMD is 5 BMD = 1 BMD

Price of Ambrosian wheat is $100 per tonne. Cost of Ambrosian wheat in BMD is ($100*5) =

$500 BMD

Price of Bolumbian wheat is $550 per tonne.

Therefore,

Profit= ( $ 550−$ 500 ) per tonne

¿ $ 50 per tonne

Question c

If other people exploit the same opportunity, supply of wheat in Bolumbia increases. This

will lead to an increase in price of wheat in Bolumbia. In Ambrosia in contrast, there will be

shortage of wheat. The shortage of wheat will lead to an increase price of wheat in Ambrosia.

Question d

The law of one price requires price of the identical commodity to be same in across the

globe. Now if wheat is the only commodity traded and the law of one price and Purchasing

Question 5

Question a

Given the price of wheat per tonne in Ambrosian and Bolumbian wheat and the nominal

exchange rate between BMD and AMD, it is profitable to buy wheat from Ambrosia and sells

wheat to Bolumbia (Audretsch and Lehmann 2016).

Question b

Exchange rate between BMD and AMD is 5 BMD = 1 BMD

Price of Ambrosian wheat is $100 per tonne. Cost of Ambrosian wheat in BMD is ($100*5) =

$500 BMD

Price of Bolumbian wheat is $550 per tonne.

Therefore,

Profit= ( $ 550−$ 500 ) per tonne

¿ $ 50 per tonne

Question c

If other people exploit the same opportunity, supply of wheat in Bolumbia increases. This

will lead to an increase in price of wheat in Bolumbia. In Ambrosia in contrast, there will be

shortage of wheat. The shortage of wheat will lead to an increase price of wheat in Ambrosia.

Question d

The law of one price requires price of the identical commodity to be same in across the

globe. Now if wheat is the only commodity traded and the law of one price and Purchasing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.